💊 TEVA Pharmaceutical $6.5M Call Bet on Turnaround Story! 🚀

📅 December 12, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just placed a $6.5 MILLION bullish bet on TEVA this morning at 10:03:14! This institutional player bought 6,800 contracts of September 2026 $22 calls - betting on continued upside for the Israeli generic drug giant that's already surging +141% year-to-date. With TEVA at $29.81 and riding an epic turnaround wave (11 consecutive quarters of growth), smart money is positioning for the stock to hold above $22 through next September. Translation: Big money believes this pharmaceutical comeback story has legs to run another 9 months!

📊 Company Overview

Teva Pharmaceutical Industries (TEVA) is the world's leading generic drug manufacturer based in Israel, with an expanding innovative medicines portfolio:

- Market Cap: $34.62 Billion

- Industry: Pharmaceutical Preparations

- Current Price: $29.81

- Primary Business: Generic drugs (world's largest producer), innovative CNS/respiratory/oncology medicines, pharmaceutical ingredients, U.S. distribution (Anda)

- Key Products: Austedo (Huntington's/tardive dyskinesia), generic Saxenda (first GLP-1 weight loss), biosimilars portfolio

- Turnaround Status: 11th consecutive quarter of growth, debt/EBITDA below 3x for first time since 2016

💰 The Option Flow Breakdown

The Tape (December 12, 2025 @ 10:03:14):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:03:14 | TEVA | ASK | BUY | CALL $22 | 2026-09-18 | $6.5M | $22 | 6,800 | 15,000 | 6,800 | $29.81 | $9.50 |

🤓 What This Actually Means

This is a long-dated bullish positioning trade on TEVA's turnaround thesis! Here's what went down:

- 💸 Massive premium deployed: $6.5M ($9.50 per contract × 6,800 contracts × 100 shares)

- 🎯 Deep in-the-money: $22 strike is $7.81 below current price (26.2% cushion already!)

- ⏰ Long duration: 280 days to expiration captures 2 earnings reports, olanzapine LAI FDA review, multiple biosimilar launches

- 📊 Substantial position: 6,800 contracts represents 680,000 shares worth ~$20.3M at current price

- 🏦 High conviction trade: Paying $9.50 for DITM calls with $7.81 intrinsic value means $1.69 time premium for 9 months

What's really happening here:

This trader is making a LONG-TERM bet on TEVA's pharmaceutical turnaround continuing through September 2026. By buying deep in-the-money $22 calls, they get stock-like exposure (high delta ~0.85) with defined risk and leverage. The $22 strike sits just above major gamma support at $22, showing they expect TEVA to consolidate gains or move higher - NOT fall back to pre-turnaround levels around $15-18.

Think of it like this: instead of buying 680,000 shares at $29.81 ($20.3M outlay), they're controlling the same exposure for $6.5M with 280 days to expiration. If TEVA continues rallying to $35-40 as analysts project, these calls print HUGE profits. If TEVA drops below $22, max loss is capped at $6.5M versus potentially larger losses on stock.

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-score: 3.61) - This trade is 3.61 standard deviations above normal TEVA activity, happening only a few times per year. The volume (6,800) represents 45.3% of existing open interest (15,000), signaling fresh institutional positioning rather than existing position adjustment.

📈 Technical Setup / Chart Check-Up

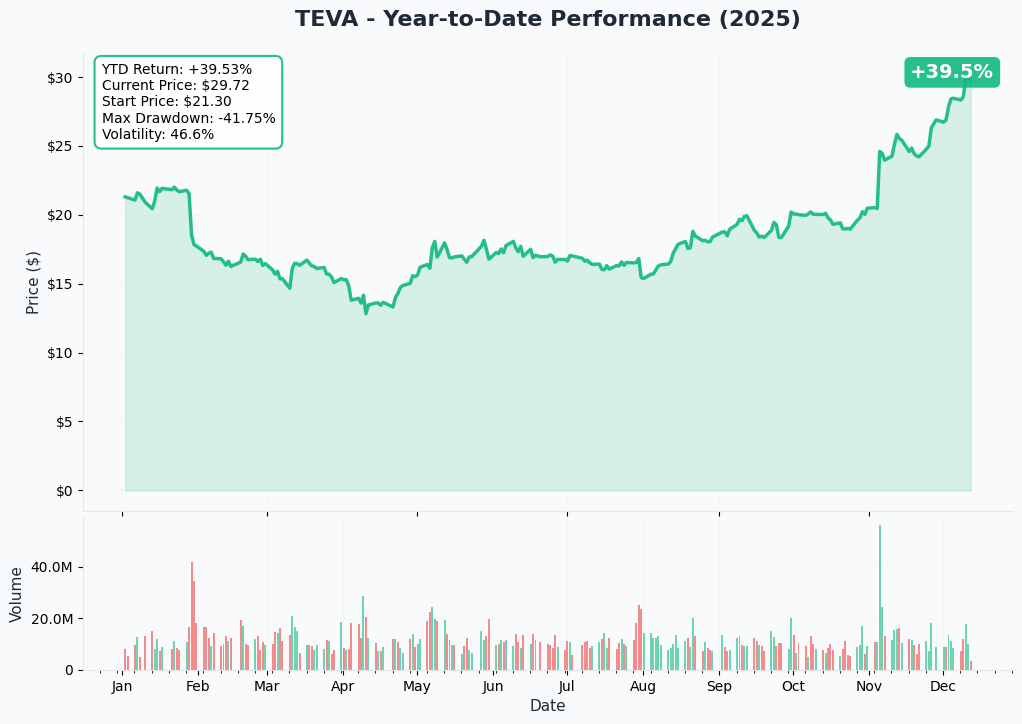

YTD Performance Chart

TEVA is having an EXPLOSIVE year - up +141% YTD with current price at $29.81. The stock started 2025 at its 52-week low of $12.47 and rocketed to a 52-week high of $30.39 this week. This isn't just a technical rally - it's a complete fundamental transformation backed by 11 consecutive quarters of growth, massive debt reduction, and a robust pipeline.

Key observations:

- 🚀 V-shaped recovery: Brutal multi-year decline from $60+ (2015-2017 peak) bottomed at $12.47 in early 2025, reversed violently

- 📈 Sustained momentum: Up 17.22% over past 2 weeks alone, rising 8 out of last 10 trading days

- 💪 Q3 earnings catalyst: Stock jumped 12% on November 5th after beating estimates by 14.71%

- 📊 Analyst validation: December 2025 upgrades from Barclays (Overweight, $35 target), Goldman Sachs (Buy, $31), Scotiabank ($35)

- ⚠️ Elevated valuation: Forward P/E at 10.79x is reasonable, but trailing P/E of 48.67x shows market pricing in aggressive growth

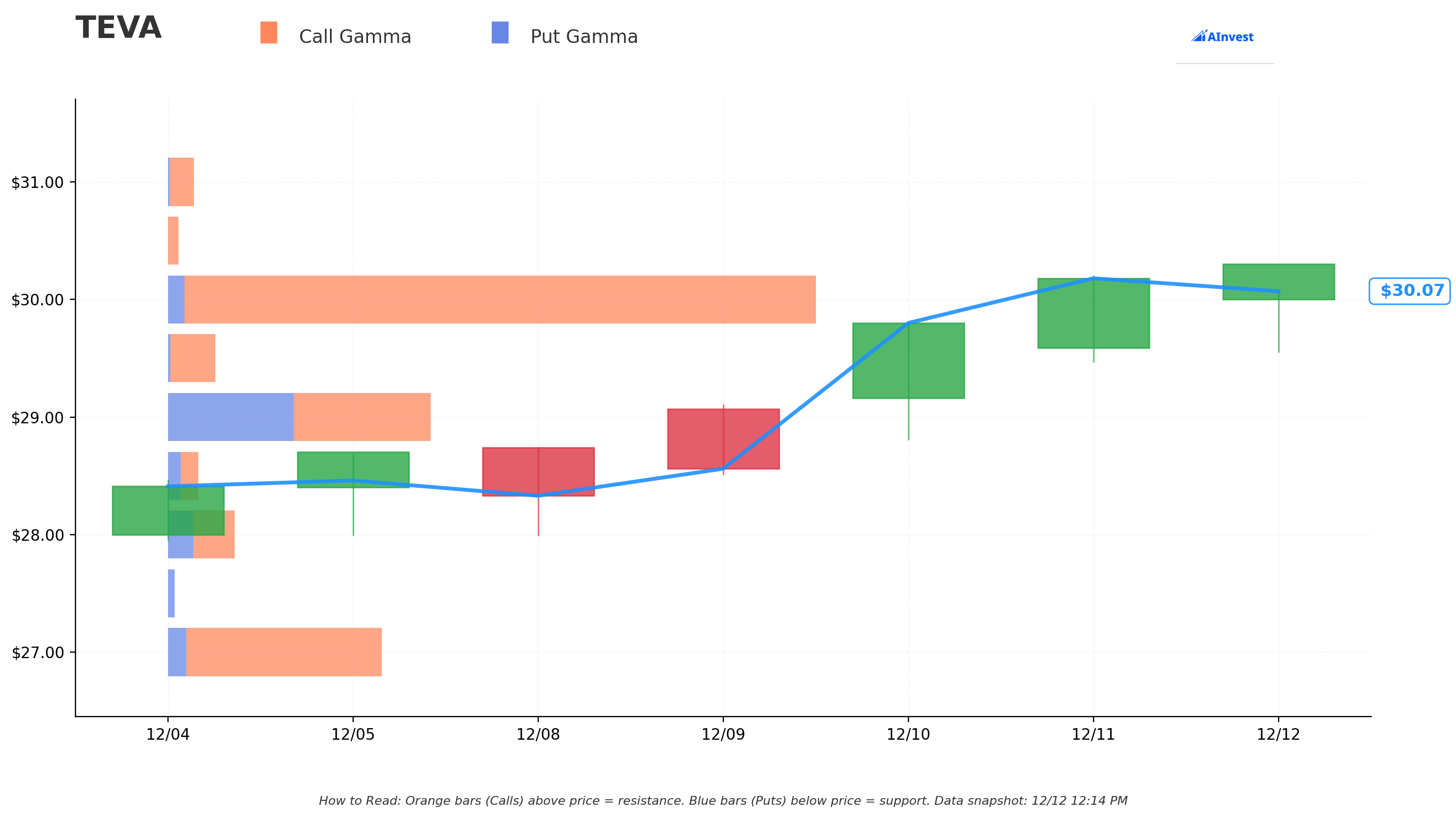

Gamma-Based Support & Resistance Analysis

Current Price: $30.08

The gamma exposure map reveals critical price magnets that will govern near-term trading:

🔵 Support Levels (Put Gamma Below Price):

- $30.00 - STRONGEST immediate support with 20.2M total gamma (19.7M call + 0.5M put) - THIS IS THE LINE IN THE SAND!

- $29.50 - Secondary support at 1.5M gamma

- $29.00 - Solid floor at 8.1M gamma (4.2M call + 3.9M put)

- $28.50 - Support zone at 0.9M gamma

- $28.00 - Structural support at 2.1M gamma

- $27.00 - Deep support at 6.6M gamma

- $26.00 - Extended floor at 2.1M gamma

- $25.00 - Disaster scenario at 3.4M gamma

🟠 Resistance Levels (Call Gamma Above Price):

- $32.00 - Immediate ceiling with 2.0M call gamma (just 6.4% overhead)

- $35.00 - Major resistance at 2.5M call gamma (analyst price target cluster!)

What this means for traders:

TEVA is sitting RIGHT on top of its strongest gamma support level at $30 with 20.2M total gamma. This creates a powerful magnetic effect - dealers need to buy aggressively if price dips below $30 to hedge their short gamma exposure. The next resistance isn't until $32, creating a clear path for upside continuation if momentum holds.

Notice the setup? The call buyer struck at $22 - well below ALL gamma support levels. They're betting TEVA consolidates between $25-35 over the next 9 months, never threatening the $22 level. This is "sleep well at night" positioning for someone bullish on the turnaround but wanting downside protection below major support.

Net GEX Bias: BULLISH (44.3M call gamma vs 16.0M put gamma = 2.76:1 ratio) - Overwhelmingly bullish positioning with call gamma dominating. This creates upside momentum potential as dealers buy stock into rallies to hedge.

Implied Move Analysis

Options market pricing for December 19th Triple Witch (7 days out):

- 📅 Weekly/Monthly/Quarterly (Dec 19 - 7 days): ±$0.80 (±2.69%) → Range: $29.03 - $30.63

Translation for regular folks:

Options traders are pricing in a relatively CALM week ahead with only a 2.7% expected move ($0.80) through next Friday's December 19th triple witch expiration. This tight implied move (±$0.80) suggests the market expects TEVA to consolidate recent gains in the $29-31 range rather than making explosive moves either direction.

Key insight: The low implied volatility tells us there are NO major binary catalysts (earnings, FDA decisions) expected in the next 7 days. The next big event is Q4 2025 earnings on February 11, 2026 - which falls well within this call trade's September 2026 expiration window.

🎪 Catalysts

🔥 Already Happened (Past 3 Months) - Foundation for This Trade

Q3 2025 Earnings Beat - November 5, 2025:

- 💰 Revenue: $4.48B vs $4.36B consensus (+3% YoY growth)

- 📈 EPS: $0.78 vs $0.68 consensus (14.71% beat!)

- 🚀 Stock jumped 12% post-earnings

- 📊 Raised full-year guidance: EPS to $2.55-$2.65, Austedo sales to $2.05-$2.15B

- 💪 11th consecutive quarter of growth - turnaround validated

Olanzapine LAI NDA Submission - December 9, 2025 (3 DAYS AGO!): TEVA submitted New Drug Application to FDA for olanzapine extended-release injectable suspension (TEV-'749) for once-monthly treatment of schizophrenia. Based on Phase 3 SOLARIS trial (675 patients, Week 56 data) showing NO post-injection delirium/sedation syndrome (PDSS) events. Patient satisfaction: 92% of patients, 87% of nurses, 73% of physicians reported high satisfaction. Analysts project peak sales potential exceeding $2 billion - potential blockbuster!

Analyst Upgrades - December 2025:

- 🔥 Barclays: Initiated "Overweight," $35 target (December 8) → upgraded to "Strong Buy" December 11

- 📈 Goldman Sachs: Maintained "Buy," raised target $28 → $31 (December 8)

- 💎 Scotiabank: Initiated "Sector Outperform," $35 target (December 5)

- Consensus: 87.5% Strong Buy ratings (7 of 8 analysts), average target $29.78-$31.13

European Biosimilar Approvals - November 25, 2025: European Commission granted marketing authorizations for PONLIMSI (denosumab biosimilar to Prolia) and DEGEVMA (denosumab biosimilar to Xgeva). Launches planned in key European markets in coming months.

Debt Reduction Progress - Q3 2025:

- 💪 Total debt decreased to $16.8B (down ~$1B since year-end 2024)

- 🎯 Net debt/EBITDA fell below 3x for first time since Q3 2016 - major deleveraging milestone!

- 📈 Average debt maturity extended to 5.85 years from 5.5 years

- 🌟 Fitch upgraded TEVA to 'BB+' with stable outlook (May 20, 2025)

Generic Saxenda Launch - August 28, 2025: TEVA announced FDA approval and U.S. launch of generic Saxenda (liraglutide injection) - first-ever generic GLP-1 indicated for weight loss! This was TEVA's fifth first-to-market generic entry in 2025, capturing significant share in the exploding obesity drug market.

🚀 Upcoming Catalysts (Next 9 Months - Within Call Expiration Window!)

Q4 2025 Earnings - February 11, 2026 (60 days out):

TEVA reports Q4 results before market open on Wednesday, February 11, 2026. This is THE near-term catalyst that could validate or challenge the bullish thesis.

Key Metrics to Watch:

- 📊 Consensus EPS: $0.65

- 💰 Full-year 2025 guidance: $16.8-17.0B revenue, $2.55-2.65 EPS (already raised Q3)

- 🤖 Austedo franchise momentum (Q3 run rate: $2.4B+ annually with 38% YoY growth)

- 💊 Generic Saxenda uptake and GLP-1 market share capture

- 🌍 Biosimilar launch timelines (7 U.S. launches planned through 2027)

- 📈 2026 guidance and outlook for "Pivot to Growth" acceleration phase

- 💪 Debt reduction progress toward 2027 target (2x net debt/EBITDA)

Upside surprise potential: If TEVA delivers on raised guidance and provides bullish 2026 outlook, could trigger breakout toward $32-35 analyst targets.

Downside risk: Any disappointment in Austedo growth, generic pricing pressure, or conservative 2026 guidance could test $28-29 support levels.

Olanzapine LAI FDA Review - Expected Decision by October 2026:

With NDA submitted December 9, 2025, standard FDA review timeline is 10 months, pointing to October 2026 decision. This falls AFTER the September 18, 2026 call expiration, but any early FDA feedback or Priority Review designation could come within the window.

Market Opportunity:

- 🎯 First-to-market long-acting olanzapine treatment option for schizophrenia

- 💰 Peak sales potential exceeding $2 billion

- 🏆 No PDSS safety concerns (major competitive advantage)

- 📊 92% patient satisfaction in Phase 3 trials

7 Biosimilar Launches - 2025-2027 (Multiple Within Window):

TEVA plans 7 biosimilar launches in U.S. between 2025 and 2027, with several expected before September 2026:

Already Launched (2025):

- Simlandi, Selarsdi, Epysqli

Under U.S. Review (Expected 2026):

- Biosimilar to Eylea (Regeneron) - ophthalmology

- Biosimilar to Simponi (J&J) - rheumatology

- Biosimilar to Prolia/Xgeva (Amgen denosumab) - oncology/osteoporosis

Strategic Impact:

- 📈 Target to double global biosimilar sales by 2027

- 💰 Currently delivering $3B+ in annual global savings

- 🌍 4 additional biosimilar launches planned in EU

Each launch represents incremental revenue and validates TEVA's complex biologics capabilities.

Austedo XR Market Expansion - Ongoing Through 2026:

TEVA's flagship growth driver Austedo continues aggressive expansion:

- 💪 Q3 U.S. revenue: $601M (+38% YoY)

- 📈 Current run rate: $2.4B+ annually (annualizing Q3 × 4)

- 🎯 Full-year 2025 guidance raised to $2.05-2.15B

- 💊 Four new tablet strengths approved (30, 36, 42, 48 mg) - most once-daily options of any VMAT2 inhibitor

- 💰 ~90% of insured patients pay $10 or less with financial assistance

Risk factor: Medicare price negotiation includes Austedo in second round - mandated price reductions could impact 2026+ revenue, though exact pricing won't be known until mid-2026.

Emrusolmin Phase 2 Trial Results - Expected 2026:

Emrusolmin (TEV-56286) received FDA Fast Track designation (September 9, 2025) for treatment of Multiple System Atrophy (MSA), a rare neurodegenerative disease with no approved treatments. Currently in Phase 2 trial with 200 patients over 56 weeks.

Market Opportunity:

- 🎯 MSA affects 15,000-50,000 Americans with NO disease-modifying treatments

- 💰 Peak sales potential exceeding $2 billion

- 🚀 Fast Track enables expedited FDA review upon trial completion

- 📊 Results expected 2026, supporting $5B innovative medicines revenue target by 2030

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timeline, here are scenarios through September 18, 2026 expiration:

📈 Bull Case (35% probability)

Target: $35-$40

How we get there:

- 💪 Q4 earnings CRUSH with full-year revenue at high-end ($17.0B), EPS beating raised guidance ($2.65+)

- 🚀 Austedo revenue trajectory accelerates toward $2.5B+ for 2025, 2026 guidance $3B+

- 💊 Generic Saxenda captures 20%+ share of GLP-1 weight loss market (Novo losing exclusivity)

- 🌍 Multiple biosimilar approvals (Eylea, Simponi, denosumab) hit U.S. market H1 2026

- 📈 Olanzapine LAI receives Priority Review or early positive FDA feedback

- 💰 2026 guidance blows past expectations: $18-19B revenue, $3.00+ EPS

- 📊 Debt reduction continues: net debt/EBITDA toward 2.5x, credit upgrade to investment grade

- 🎯 Analysts raise targets to $40+ on multiple blockbuster drugs derisking

- 📈 Breakout above $32 gamma resistance triggers technical rally to $35-40

Key metrics needed:

- Innovative medicines (Austedo, UZEDY, AJOVY) growing 30%+ YoY

- Biosimilar launches delivering $500M+ incremental revenue 2026

- Olanzapine approval probability >70% based on FDA interactions

- Generic business stabilizing (flat to low single-digit growth vs declining)

Call P&L in Bull Case:

- Stock at $35: Calls worth $13.00, profit = $3.50/share × 6,800 × 100 = $2.38M gain (37% ROI)

- Stock at $40: Calls worth $18.00, profit = $8.50/share × 6,800 × 100 = $5.78M gain (89% ROI)

Probability assessment: 35% because TEVA has demonstrated 11 consecutive quarters of execution, multiple near-term catalysts with high probability of success, and strong analyst support. However, requires sustained momentum across multiple fronts with generics headwinds partially offset.

🎯 Base Case (45% probability)

Target: $28-$34 range (MODEST GAINS)

Most likely scenario:

- ✅ Solid Q4 earnings meeting raised guidance (~$17.0B revenue, $2.60-2.65 EPS)

- 📱 Austedo growth continues but moderates to 25-30% YoY (still strong, less parabolic)

- ⚖️ Biosimilar launches proceed on schedule but uptake gradual (not explosive)

- 💊 Generic Saxenda performs in-line, capturing 10-15% GLP-1market share

- 🤖 Olanzapine LAI review proceeding normally, no major positive/negative surprises

- 📊 2026 guidance conservative but solid: $17.5-18.0B revenue, $2.70-2.85 EPS

- 🇨🇳 Generic business faces continued pricing pressure but stable volumes

- 🔄 Trading between $28 support and $32 resistance for months, consolidating YTD gains

- 💤 Market waits for FDA approval catalysts (olanzapine, biosimilars) before re-rating higher

This is the call buyer's target scenario: Stock consolidates gains in $28-32 range, calls maintain intrinsic value between $6-10, modest profit taken at expiration. The deep ITM structure ($22 strike vs $29.81 spot) provides downside cushion - even if stock drifts to $28, calls still worth $6.00 ($4.1M value vs $6.5M cost = -37% vs -100% for ATM calls).

Call P&L in Base Case:

- Stock at $28: Calls worth $6.00, loss = -$3.50/share × 6,800 × 100 = -$2.38M loss (-37%)

- Stock at $32: Calls worth $10.00, profit = $0.50/share × 6,800 × 100 = $340K gain (5%)

Why 45% probability: Most likely path given solid fundamentals, manageable risks, and historical pattern of pharma turnarounds consolidating before next leg. Valuation at 10.79x forward P/E is reasonable but not cheap - limits explosive upside without incremental catalysts.

📉 Bear Case (20% probability)

Target: $22-$26 (TEST THE STRIKE!)

What could go wrong:

- 😰 Q4 earnings disappoint or guidance conservative - even small miss could trigger -10-15% selloff given YTD gains

- 🚨 Austedo growth stalls due to Medicare price negotiation impact or competition

- ⏰ Biosimilar approvals delayed or launches underwhelm on uptake

- 💊 Generic Saxenda pricing collapses faster than expected (typical generic dynamic)

- 🇨🇳 Generic business deteriorates faster than expected - pricing and volume both declining

- 📊 Olanzapine LAI hits FDA roadblock (Complete Response Letter) or delayed approval

- 💸 Debt reduction pace slows - operating cash flow challenges resurface

- 🔨 Broader pharma selloff on healthcare policy uncertainty (drug pricing legislation)

- ⚖️ EU antitrust fine €462.6M upheld on appeal - additional penalties possible

- 🛡️ Break below $28 gamma support triggers cascade to $26, then toward $22 strike

Critical support levels:

- 🛡️ $30: Current strongest gamma support (20.2M) - MUST HOLD near-term

- 🛡️ $28-29: Secondary support cluster (8.1M + 1.5M gamma)

- 🛡️ $27: Deep support at 6.6M gamma

- 🛡️ $25: Extended floor at 3.4M gamma

- 🛡️ $22: This call strike - buyer's "worst case" support level

Call P&L in Bear Case:

- Stock at $26: Calls worth $4.00, loss = -$5.50/share × 6,800 × 100 = -$3.74M loss (-58%)

- Stock at $22: Calls worth $0.00, loss = -$9.50/share × 6,800 × 100 = -$6.50M loss (-100%)

- Stock at $20: Calls worthless, max loss = -$6.50M (-100%)

Probability assessment: Only 20% because TEVA's fundamental turnaround is REAL (11 consecutive quarters of growth, debt reduction, pipeline execution). Would require multiple negative catalysts aligning simultaneously. The call buyer clearly thinks probability is <20% or they wouldn't risk $6.5M. Deep ITM structure provides significant downside buffer vs ATM or OTM calls.

💡 Trading Ideas

🛡️ Conservative: Wait for Q4 Earnings Clarity

Play: Stay on sidelines until February 11, 2026 earnings validate turnaround sustainability

Why this works:

- ⏰ Q4 earnings in 60 days provides critical update on Austedo momentum, biosimilar progress, 2026 outlook

- 💸 Stock already up 141% YTD at $29.81 - significant gains already captured, limited near-term catalysts before earnings

- 📊 Forward P/E of 10.79x is fair valuation IF growth continues, but expensive if momentum stalls

- 🎯 Better entry likely post-earnings after any volatility settles (either dip to buy or breakout to chase)

- 📉 No major binary catalysts for 60 days (olanzapine decision not until Oct 2026) - low urgency

- 🤔 Implied move only ±2.69% for next week suggests market expects consolidation, not fireworks

Action plan:

- 👀 Monitor December-January price action: consolidation $28-32 = healthy, breakdown below $28 = concerning

- 🎯 Watch for pullback to $27-28 gamma support for stock entry with 10% margin of safety vs current price

- ✅ Need to see Q4 Austedo revenue >$650M (continuing 30%+ growth), generic Saxenda uptake commentary

- 📊 Look for 2026 guidance: revenue $17.5-18.5B, EPS $2.75-3.00 to confirm "Pivot to Growth" on track

- ⏰ Revisit post-earnings with clearer picture of biosimilar launch timing and olanzapine FDA feedback

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -15-20% drawdown if turnaround story cracks. Get better entry on any pullback. Maintain flexibility for clearer risk/reward post-earnings.

⚖️ Balanced: Sell Cash-Secured Puts at Major Support

Play: Sell puts at $27-$28 strikes, getting paid to potentially own TEVA at 10-15% discount

Structure: Sell $28 puts (January 16, 2026 expiration - 35 days out)

Why this works:

- 💰 Collect premium ($1.00-1.50 per contract) for agreeing to buy TEVA at $28 (6% below current price)

- 🎯 $28 strike sits on major gamma support level (2.1M gamma) - likely buying zone if tested

- 📊 Effectively lowers your entry to $26.50-27.00 after premium collected

- ⏰ 35 days gives time for any post-earnings volatility to play out (earnings Feb 11)

- 🛡️ If assigned, you own TEVA at attractive valuation (8.5x forward P/E at $28) with 2.98% dividend yield

- 🚀 If stock stays above $28, keep entire premium (10-15% annualized return on capital at risk)

Estimated P&L (confirm current option prices):

- 💰 Collect ~$1.25 premium per put sold

- 📈 Max profit: $125 per contract if TEVA stays above $28 (keep entire premium)

- 📉 Breakeven: $26.75 (strike $28 - premium $1.25)

- ⚠️ Assignment risk: Required to buy 100 shares at $28 ($2,800 per contract) if below strike at expiration

- 🎯 Effective entry: $26.75 = 10% discount to current price with support levels underneath

Position sizing:

- Only sell puts on shares you're WILLING to own at $28

- Ensure sufficient cash in account ($2,800 per put contract)

- Start small: 1-2 contracts for beginners, scale up if comfortable

Risk management:

- 🚨 If TEVA breaks below $27 support, consider buying back puts at loss (30-40% of premium)

- ⏰ Roll puts to February expiration if approaching Jan expiry with stock near $28

- ❌ Don't sell puts below $27 - too close to 2025 starting level around $25

Risk level: Moderate (obligation to buy stock, but at discount) | Skill level: Intermediate

🚀 Aggressive: Bull Call Spread Targeting Analyst Upside (LEVERAGED!)

Play: Bull call spread targeting $32-35 analyst price targets

Structure: Buy $30 calls / Sell $35 calls (March 20, 2026 expiration - 98 days out, post-earnings)

Why this could work:

- 🎯 Targets analyst price target cluster at $31-35 (Goldman $31, Barclays $35, Scotiabank $35)

- 💥 Captures Q4 earnings upside (Feb 11) and gives time for initial biosimilar launch updates

- 📊 Defined risk spread ($5 wide = $500 max risk per spread)

- 🚀 If TEVA breaks through $32 gamma resistance on earnings beat, quick move to $35 likely

- ⚡ Limited capital outlay (~$2.00-2.50 net debit) vs buying stock at $29.81

- 📈 Maximum 2:1 risk/reward if stock reaches $35

Why this could blow up (SERIOUS RISKS):

- 💸 REQUIRES breakout: Need TEVA to rally 7-17% from current levels to profit

- ⏰ Time decay: Theta erodes value daily, especially last 30 days

- 😱 Earnings risk: If Q4 disappoints, stock could drop to $26-28, lose 60-80% of spread value

- 📊 Capped upside: Even if TEVA goes to $40-45, max profit is only $5 per spread

- 🎢 Need sustained momentum - can't just touch $35 briefly, needs to CLOSE above at expiration

- ⚠️ Generic pricing pressure or Austedo slowdown would kill thesis quickly

Estimated P&L (adjust for current option prices):

- 💰 Cost: ~$2.00-2.50 net debit per spread

- 📈 Max profit: $2.50-3.00 if TEVA above $35 at March expiration (100-120% ROI)

- 📉 Max loss: $2.00-2.50 if TEVA below $30 (100% loss)

- 🎯 Breakeven: ~$32.00-32.50

Entry timing:

- ⏰ Enter AFTER any near-term pullback to $29-29.50 (improves risk/reward)

- ❌ Don't chase if stock already above $31 (risk/reward deteriorates)

- ✅ Ideal entry: Stock consolidating $29-30 range with bullish catalyst approaching

Position sizing: Risk only 3-5% of portfolio (this is pure speculation on upside breakout)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can afford to lose ENTIRE premium (real possibility!)

- ✅ Understand spread mechanics and won't panic on temporary price swings

- ✅ Accept that even correct directional call can lose money if timing wrong

- ⏰ Plan to close spread 1-2 weeks before expiration if profitable (don't hold to expiry for max gain)

- 📊 Have stop-loss discipline: close at -50% loss if stock breaks below $28

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

Probability of profit: ~35% (matches bull case probability - need sustained rally to $32+)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q4 Earnings February 11, 2026 (60 days): Results will be CRITICAL for validating turnaround sustainability after 11 consecutive quarters of growth. Market expects Austedo revenue >$650M (continuing 30%+ growth trajectory), generic Saxenda early traction update, biosimilar launch timing, and 2026 guidance $17.5-18.5B revenue. Any disappointment could trigger -10-15% gap down given 141% YTD gain with limited valuation cushion. Stock priced for PERFECT execution.

-

💸 Medicare Drug Price Negotiation Impact: AUSTEDO/AUSTEDO XR included in second round of Medicare negotiation, with court rejecting TEVA's legal challenge on November 24, 2025. Mandated price reductions could hit 2026-2027 revenue significantly. Current Austedo run rate ($2.4B annually) at RISK if Medicare cuts 30-40% off pricing. This is TEVA's #1 growth driver - any slowdown would be catastrophic for stock.

-

⚖️ Regulatory and Legal Overhang: Multiple ongoing issues create uncertainty: 1) EU antitrust fine €462.6M for patent abuse (TEVA appealing), 2) FTC patent challenge forcing removal of 200+ Orange Book listings (reputational damage), 3) Ongoing opioid settlement payments ($3B cash through 2036 + $1.2B Narcan supply). These drain cash flow and create headline risk.

-

🚨 Olanzapine LAI Approval Uncertainty: NDA submitted December 9, 2025 with expected October 2026 decision. FDA could issue Complete Response Letter (rejection) citing manufacturing, safety, or efficacy concerns. Competitive landscape may evolve during 10-month review - other companies could file competing long-acting formulations. Peak sales estimates of $2B+ not guaranteed - requires market adoption post-approval.

-

💊 Generic Drug Pricing Pressure Intensifying: Generic business expected flat to low single-digit growth in 2025 due to competitive pressure, tough comparables, and market softness. Structural headwinds from India-based low-cost competitors (Sun, Aurobindo, Cipla) and biosimilar competition for branded products. Generic Saxenda pricing could collapse 70-80% within 12-18 months (typical generic dynamic) as additional competitors enter. TEVA's core business faces margin compression.

-

🌍 Biosimilar Launch Execution Risk: 7 U.S. launches planned through 2027 is AGGRESSIVE timeline requiring flawless execution. Delayed FDA approvals (Eylea, Simponi, denosumab biosimilars under review) or slow market uptake could derail 2027 revenue targets. Biosimilars face formulary access challenges, prescriber skepticism, and branded manufacturer defensive tactics. Need to prove biosimilar portfolio can offset generic erosion.

-

💰 Debt Burden Still Significant: Despite progress to $16.8B total debt, TEVA still highly leveraged. Operating cash flow declined 47% in recent periods, jeopardizing debt reduction velocity toward 2027 target of 2x net debt/EBITDA. Failed TAPI sale delays crucial divestment for complexity reduction and cash generation. Rising interest rates increase refinancing costs. Credit rating still below investment grade (BB+).

-

📊 Valuation Stretched After 141% Rally: Forward P/E of 10.79x seems reasonable but trailing P/E of 48.67x shows market is paying for FUTURE growth, not current earnings. Stock at $29.81 (near 52-week high $30.39) after massive run leaves zero margin of safety. Requires 40% of revenue from innovative medicines by 2027 to justify valuation. Any execution stumble could trigger 25-30% correction back to $22-24 levels (this call strike!).

-

🎯 Emrusolmin Phase 2 Trial Uncertainty: Phase 2 study for Multiple System Atrophy ongoing with 200 patients over 56 weeks. Efficacy/safety data not yet proven - could fail to show statistical significance. Rare disease commercial execution challenging (small patient population, limited reimbursement). Fast Track designation doesn't guarantee approval. $2B+ peak sales projection speculative at this stage.

-

🐋 Institutional Money Taking Chips Off Table: Recent insider selling (EVP sold 30K shares Nov 14, Director sold 50K shares Nov 26) signals executives monetizing YTD gains. While not necessarily bearish, shows even insiders de-risking after massive run. 72% institutional ownership means smart money could rotate out quickly if turnaround thesis cracks.

-

🇨🇳 Opioid Settlement Cash Drain: $3B cash payments over 13 years (through 2036) + $1.2B Narcan supply commitment represents ongoing cash outflow impacting capital allocation flexibility. Reduces financial flexibility for M&A, buybacks, or accelerated debt reduction. Next milestone: Baltimore settlement $45M due by July 1, 2025 (already paid $35M).

🎯 The Bottom Line

Real talk: Someone just committed $6.5 MILLION to a 9-month bullish bet on TEVA's pharmaceutical turnaround - and they did it in a SMART way. By buying deep in-the-money $22 calls instead of stock or ATM options, they get leveraged upside with substantial downside protection. Stock would need to fall 26% (from $29.81 to $22) before these calls lose ALL value.

What this trade tells us:

- 🎯 Sophisticated institutional player expects TEVA to SUSTAIN gains through September 2026 (not just a momentum pop)

- 💰 They're willing to pay $1.69 time premium per share for 280 days of exposure - implies high conviction in continued execution

- ⚖️ The $22 strike placement sits well below all major support levels ($25-30 range), showing they expect consolidation ABOVE $25 minimum

- ⏰ September 2026 expiration captures Q4 2025 earnings (Feb), Q1 2026 earnings (May), biosimilar approvals, and early olanzapine FDA feedback

- 📊 This isn't a "home run" trade structure - it's a capital-efficient way to own TEVA exposure while limiting downside to $6.5M vs $20.3M for stock

This is NOT a "YOLO" - it's sophisticated portfolio construction by someone who believes in the turnaround story but wants protection.

If you own TEVA:

- ✅ HOLD through Q4 earnings (Feb 11) - turnaround story still intact with multiple near-term catalysts

- 📊 Set MENTAL STOP at $27-28 (major gamma support cluster) to protect 141% YTD gains if thesis breaks

- ⏰ Don't get greedy at current levels - consider trimming 20-30% if stock touches $32-33 (take some profits!)

- 🎯 If earnings beat AND stock breaks $32, could re-add trimmed shares on momentum to $35

- 🛡️ Consider selling covered calls at $32-35 strikes to generate income while holding

If you're watching from sidelines:

- ⏰ February 11, 2026 before market open is the moment of truth - DO NOT chase current levels!

- 🎯 Post-earnings pullback to $27-28 would be EXCELLENT entry (10% pullback from highs with support)

- 📈 Looking for confirmation of: Austedo >$650M Q4 revenue, generic Saxenda early traction, 2026 guidance $17.5-18.5B

- 🚀 Longer-term (12-18 months), olanzapine approval October 2026 and biosimilar portfolio doubling by 2027 are legitimate catalysts for $35-40

- ⚠️ Current valuation (10.79x forward P/E) is FAIR but not cheap - requires continued growth to justify

If you're bearish:

- 🎯 Respect the 11 consecutive quarters of growth - this turnaround is REAL, not hype

- 📊 First major support at $30 (20.2M gamma - strongest level), then $28-29 cluster

- ⚠️ Post-earnings put spreads ($30/$27 or $28/$25) offer better risk/reward than fighting momentum now

- 📉 Watch for break below $28 - that's the trigger for cascade to $25-26 range

- ⏰ Don't fight institutional flow - this $6.5M call buy shows smart money is BULLISH, not bearish

Mark your calendar - Key dates:

- 📅 December 19, 2025 - Weekly/Monthly/Quarterly OPEX (±2.69% implied move)

- 📅 February 11, 2026 (before open) - Q4 FY2025 earnings report (CRITICAL CATALYST!)

- 📅 May 2026 - Q1 FY2026 earnings

- 📅 June-August 2026 - Expected biosimilar approval decisions (Eylea, Simponi, denosumab)

- 📅 September 18, 2026 - Expiration of this $6.5M call trade

- 📅 October 2026 - Expected FDA decision on olanzapine LAI (potential $2B+ drug)

Final verdict: TEVA's turnaround story is LEGITIMATE - 11 consecutive quarters of growth, debt reduction to 3x net debt/EBITDA (first time since 2016), Austedo growing 38% YoY, generic Saxenda first-to-market GLP-1, and robust biosimilar pipeline are all REAL catalysts. BUT, after 141% YTD gain at $29.81, the easy money has been made. Current levels require PERFECT execution to justify valuation.

The $6.5M institutional call buy is NOT a signal to FOMO in - it's a signal that smart money believes the $22-30 range is sustainable for the next 9 months, but they're structuring for protection below $22.

Be patient. Let Q4 earnings provide confirmation. Look for any pullbacks to $27-28 for better entry. The pharmaceutical turnaround will still be here in 2-3 months, and you'll sleep better owning TEVA at $28 instead of $30 if the generic pricing headwinds intensify or Medicare cuts Austedo pricing.

This is a quality company executing a solid turnaround - but price matters. Don't overpay. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The extremely unusual score (Z-score 3.61) reflects this trade's size relative to recent TEVA history - it does not imply the trade will be profitable or that you should follow it. Deep ITM call structures are advanced strategies with different risk profiles than stock ownership. Always do your own research and consider consulting a licensed financial advisor before trading. Pharmaceutical companies face regulatory, competitive, and execution risks that can cause significant price volatility.

About Teva Pharmaceutical Industries: Teva Pharmaceutical Industries is the world's leading generic drug manufacturer based in Israel, with an innovative medicines portfolio spanning CNS, respiratory, and oncology, plus pharmaceutical ingredients and U.S. distribution, with a market cap of $34.62 billion in the Pharmaceutical Preparations industry.