💊 TEVA $1M Covered Call - Pharma Turnaround Play Hits Resistance! 🛡️

📅 January 5, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just sold 4,800 covered calls on TEVA for $1 MILLION this morning at 09:36:26! This massive position sold June 18th $34 strike calls against existing stock holdings - a strategic move to generate income while capping upside at 10% above current prices. With TEVA trading at $30.81 after a monster 40% rally over the past year, smart money is taking chips off the table while maintaining core exposure to the pharma turnaround story. Translation: Institutional investors are locking in gains after the big run, expecting sideways consolidation into mid-2026.

📊 Company Overview

Teva Pharmaceutical Industries (TEVA) is the world's largest generic drug manufacturer fighting to complete a multi-year turnaround:

- Market Cap: $35.5 Billion

- Industry: Pharmaceutical Preparations

- Current Price: $30.81 (near 52-week high of $31.99)

- Primary Business: Global leader in generic drugs with 3,500+ products in 60+ countries, plus innovative medicines portfolio including blockbuster Austedo (tardive dyskinesia/Huntington's disease treatment), biosimilar launches (Selarsdi, Simlandi), and CNS/respiratory therapies

- Employees: 35,686 worldwide

- Headquarters: Tel Aviv, Israel (NYSE-listed ADRs)

💰 The Option Flow Breakdown

The Tape (January 5, 2026 @ 09:36:26):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order Type | Strategy | Confidence | Z-Score | Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-05 | 09:36:26 | TEVA | SELL | CALL $34 | 2026-06-18 | $34 | 4,800 | $1.00M | STO | Short Call (Covered Call) | MEDIUM | 43.72 | EXTREMELY UNUSUAL |

🤓 What This Actually Means

This is a strategic covered call position on a massive long stock holding! Here's what went down:

- 💸 Income generation: $1M premium collected ($2.08 per share × 4,800 contracts)

- 📦 Underlying exposure: Represents 480,000 shares worth ~$14.8M at current prices

- 🎯 Cap on upside: Willing to sell stock at $34 (10.3% above current $30.81)

- ⏰ Strategic timing: 164 days to expiration captures Q4 2025 earnings (Feb 11), olanzapine LAI FDA review, MI325X launch updates, and early biosimilar performance data

- 🛡️ Downside protection: Collects $2.08/share premium providing 6.8% cushion on existing position

- 🏦 Sophisticated strategy: This trader accumulated TEVA during the rally from $22 to $31, now monetizing volatility while staying invested

What's really happening here: This institutional player likely owns a MASSIVE TEVA position accumulated throughout the turnaround story - maybe from $20-25 levels over the past year. After TEVA's 11 consecutive quarters of growth and successful debt reduction (net debt/EBITDA below 3x for first time since 2016), they're now selling $34 calls expiring June 18th to collect $1M in premium. They're saying: "I'm happy to sell my shares at $34 (35% gain from my $25 cost basis), but if the stock stays below $34, I'll keep my shares AND pocket the $1M." Classic income play when you think momentum is slowing.

Unusual Score: 🔥 EXTREME (43.72x average size) - This happens a few times per year for TEVA. The Z-score of 43.72 means this is massively larger than typical TEVA option activity. No similar trades in the past 30 days - this is a one-off strategic position, not part of ongoing strategy.

📈 Technical Setup / Chart Check-Up

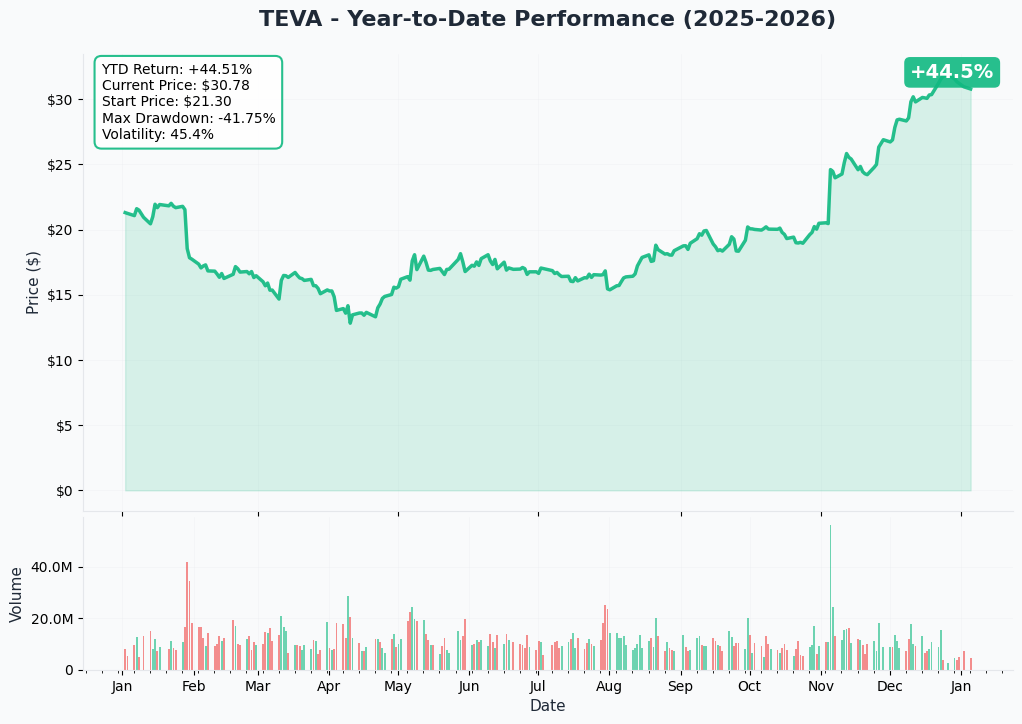

YTD Performance Chart

TEVA has been on fire - up +40.3% over the past year from $22.62 on December 26, 2024 to current price of $30.95 (as of January 2, 2026). The chart tells a compelling turnaround story - after bouncing off $12.47 lows in mid-2025, TEVA exploded to 52-week highs of $31.99.

Key observations:

- 🚀 Sustained rally: Steady climb from $22 range in late 2024 to $31+ levels

- 📈 Breakout confirmed: Smashed through $28-29 resistance in December, testing multi-year highs

- 📊 Recent pullback: Stock fell 2.95% week-over-week as of January 2nd - some profit-taking after the run

- ⚠️ Near resistance: At $30.81, stock is within 3% of all-time high $31.99 - consolidation likely

- 💪 Strong fundamentals backing rally: 11 consecutive quarters of growth, Austedo revenue up 38% YoY to $618M in Q3, debt reduction ahead of schedule

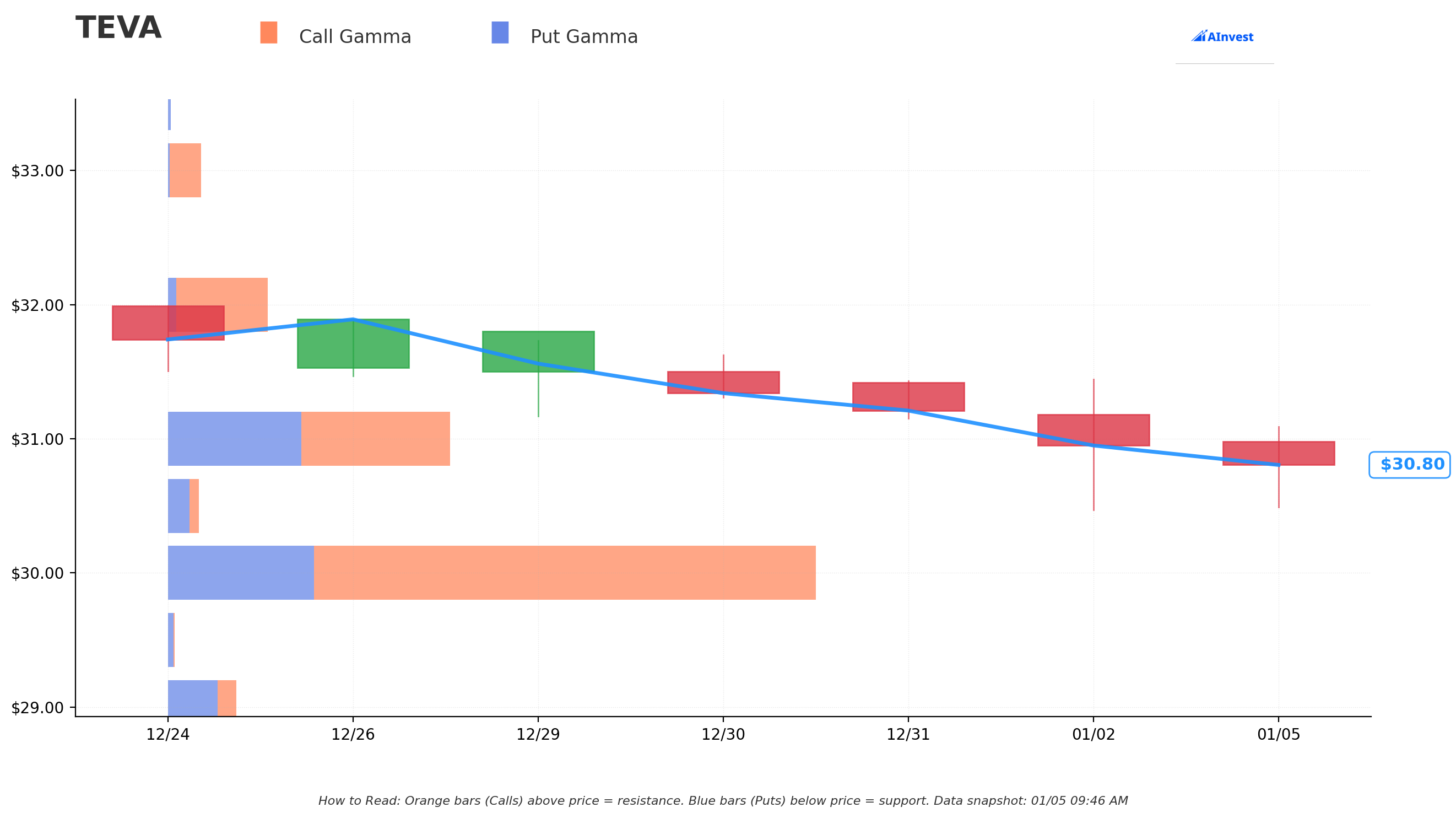

Gamma-Based Support & Resistance Analysis

Current Price: $30.81

The gamma exposure map reveals critical price magnets and barriers for TEVA over the next several months:

🔵 Support Levels (Put Gamma Below Price):

- $30.00 - STRONGEST NEARBY SUPPORT with 27.67B total gamma exposure (15.16B net call gamma - dealers will aggressively defend this level)

- $29.00 - Secondary support at 2.91B total gamma (slight net negative at -1.35B due to put positioning)

- $28.00 - Tertiary support at 1.77B gamma (nearly neutral with 0.002B net)

- $27.00 - Deeper floor with 5.60B gamma (strong 4.86B net call gamma)

- $26.00 - Extended support zone at 1.56B gamma

- $25.00 - Major structural floor with 3.58B gamma

🟠 Resistance Levels (Call Gamma Above Price):

- $31.00 - Immediate ceiling with 12.06B total gamma (only 0.64B net - could break through easily!)

- $32.00 - Secondary resistance at 4.27B gamma (3.54B net call gamma - moderate obstacle)

- $33.00 - Lighter resistance at 1.41B gamma (1.26B net call gamma)

- $35.00 - Extended upside target at 3.49B gamma (3.47B net - potential magnet if breakout occurs)

What this means for traders: TEVA is trading in an interesting technical zone. The massive $30 support (27.67B gamma - BY FAR the strongest level) provides a solid floor just 2.6% below current price. The immediate $31 resistance is relatively weak (only 12.06B gamma, mostly balanced), suggesting the stock could easily pop to $32-33 on positive catalysts. However, the covered call seller struck at $34 - just above the $33 resistance level - because they expect the rally to stall out in that zone over the next 5 months.

Notice anything? The call seller is positioned PERFECTLY. They're collecting premium with strikes at $34, which is above the $33 resistance level (1.41B gamma) but below the $35 level (3.49B gamma). If TEVA breaks out to $35, they're happy to sell at $34 for a nice profit. If it stays range-bound at $30-32, they keep the stock AND the $1M premium. Smart positioning.

Net GEX Bias: Bullish (53.01B call gamma vs 23.70B put gamma) - Overall market positioning remains bullish with 2.2:1 call to put ratio, but the covered call seller thinks upside is limited in the near term.

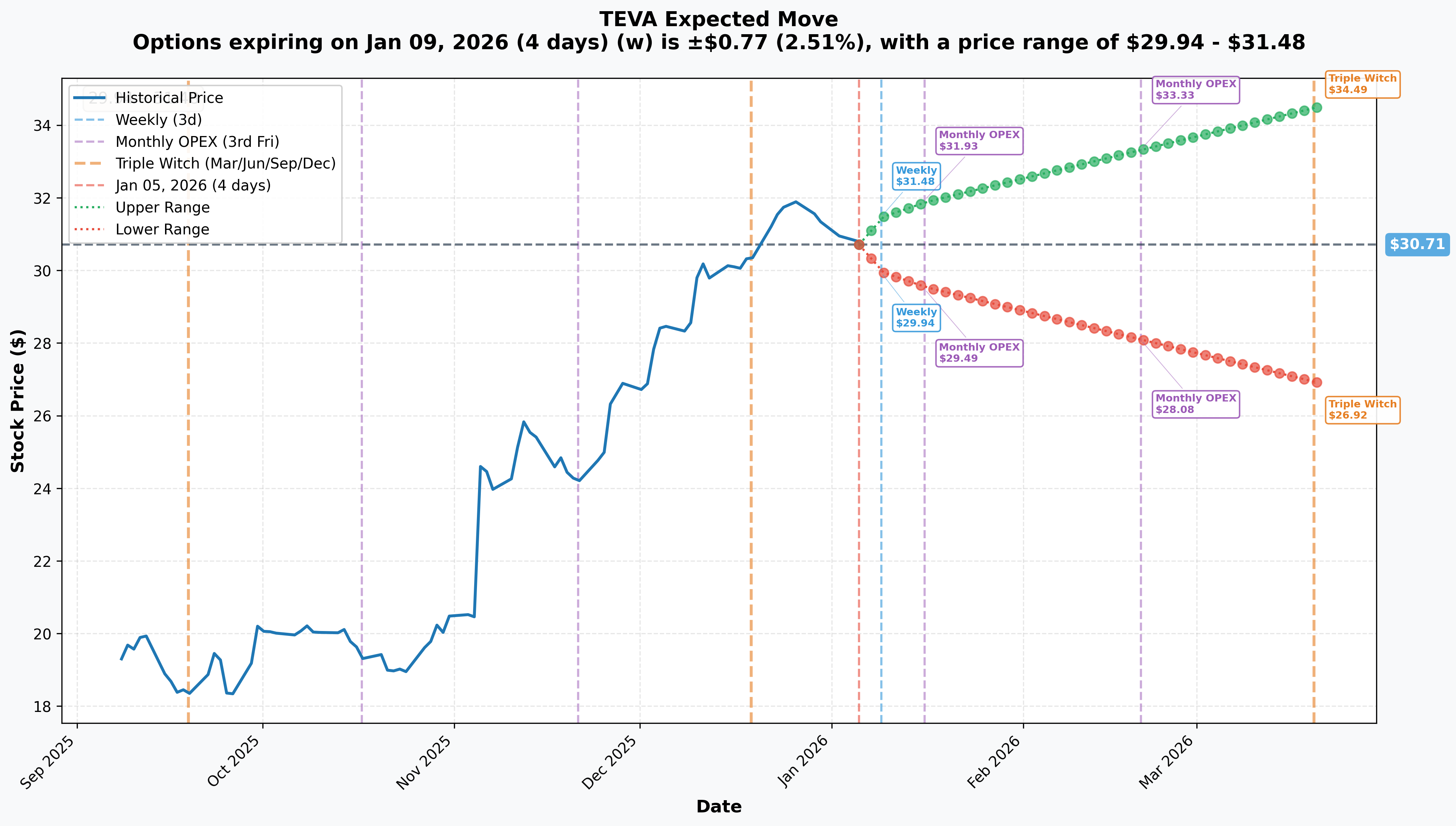

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 9 - 4 days): ±$0.77 (±2.51%) → Range: $29.94 - $31.48

- 📅 Monthly OPEX (Jan 16 - 11 days): ±$1.18 (±3.85%) → Range: $29.53 - $31.89

- 📅 February OPEX (Feb 20 - 46 days): ±$2.62 (±8.53%) → Range: $28.08 - $33.33

- 📅 Quarterly Triple Witch (Mar 20 - 74 days): ±$3.79 (±12.33%) → Range: $26.92 - $34.49

Translation for regular folks: Options traders are pricing in a relatively CALM next few weeks for TEVA - only 2.5% move ($0.77) by this Friday, and 3.9% move through monthly OPEX on January 16th. The quarterly triple witch expiration (March 20th) shows an upper range of $34.49 - almost exactly where the covered call seller struck their $34 calls!

Key insight: The market expects TEVA to trade in a $29-32 range over the next month, with potential to reach $33-34 by March. The covered call seller's $34 strike on June expiration aligns perfectly with this - they're giving the stock 5+ months to potentially hit $34, but betting it won't get there before earnings catalysts (Q4 results Feb 11, FDA decisions later in year).

Low implied volatility (2.5-3.9% for near-term expirations) confirms this is NOT a momentum name right now - it's a value turnaround story trading in a range.

🎪 Catalysts

🔥 Upcoming Catalysts (Next 6 Months)

Q4 2025 Earnings - February 11, 2026 (37 DAYS AWAY!) 📊

TEVA reports fiscal Q4 2025 results on Tuesday, February 11, 2026 before market open. This is THE catalyst that could validate or challenge the turnaround thesis:

- 📊 Consensus EPS: $0.66 (range: $0.58 - $0.78)

- 💰 2026 Full-Year EPS: $2.61 (range: $2.56 - $2.64) - critical guidance update expected

- 🎯 Key metrics to watch:

- Full-year 2025 Austedo revenue vs guidance ($2.05-$2.15B target)

- Net debt/EBITDA trajectory toward 2.8x year-end target

- 2026 guidance addressing the Revlimid revenue cliff (generic competition intensifies January 31st)

- Biosimilar revenue ramp (Selarsdi, Simlandi performance)

- MI325X launch timing and early feedback

- Gross margin expansion progress

Upside surprise potential: If TEVA beats consensus AND provides strong 2026 guidance that offsets Revlimid headwinds, stock could rally to $33-35 range. Austedo revenue tracking toward $2.5B by 2027 and successful biosimilar launches could drive multiple expansion.

Downside risk factors: The 2026 Revlimid revenue cliff is a KNOWN headwind - generic lenalidomide competition intensifies starting January 31, 2026, potentially eliminating $1B+ in high-margin revenue. Any conservative 2026 guidance acknowledging this could pressure shares back toward $28-29 support.

Olanzapine LAI (TEV-749) FDA Review - Potential Approval Late 2026 💊

TEVA's NDA submission on December 9, 2025 for olanzapine extended-release injectable (once-monthly treatment for schizophrenia) represents a major pipeline catalyst:

- 🎯 Peak sales potential: $1.5-2.0 billion combined with UZEDY for schizophrenia franchise

- ⏰ Standard FDA review timeline suggests decision late 2026 (10-12 months from submission)

- 💪 If approved, could launch H1 2027 and contribute meaningfully to $5B innovative medicines target by 2030

- 📊 Updates on FDA review process likely during Q4 earnings call or Q1 2026 earnings

Eylea Biosimilar (AVT06) Launch - Q4 2026 or Earlier 👁️

Settlement with Regeneron enables Eylea biosimilar launch in Q4 2026 or potentially earlier:

- 💰 Eylea is a $5B+ annual revenue product - even modest market share could add hundreds of millions to TEVA

- 🏥 First major ophthalmology biosimilar launch in U.S. - huge market opportunity

- 📈 Part of strategy to launch 5 new biosimilars by 2027

- ⏰ Launch timing falls AFTER June covered call expiration - could be catalyst for second half 2026

Duvakitug Phase 3 Trials - H1 2026 Expected Initiation 🔬

Duvakitug (anti-TL1A antibody) showed best-in-class potential in Phase 2b results for inflammatory bowel disease (IBD):

- 🎯 47.8% clinical remission in ulcerative colitis vs 20.45% placebo

- 🤝 Partnership with Sanofi to lead Phase 3 development

- 💊 IBD market growing rapidly - potential multi-billion dollar opportunity if approved

- 📅 Phase 3 initiation expected H1 2026 - positive update could boost confidence in pipeline depth

📊 Recently Completed Catalysts (Past 3 Months)

Q3 2025 Earnings Beat - November 5, 2025 ✅

TEVA crushed Q3 expectations, delivering the 11th consecutive quarter of growth:

- 💰 Revenue: $4.48B vs $4.36B consensus (up 3% YoY)

- 📈 Non-GAAP EPS: $0.78 vs $0.69 consensus (14.71% earnings surprise!)

- 🚀 Austedo revenue: $618M, up 38% YoY

- 💪 Adjusted EBITDA: Up 6% YoY

- 💵 Free cash flow: >$500M in Q3

- 📊 2025 guidance raised: Austedo to $2.05-2.15B, non-GAAP EPS to $2.55-2.65

Biosimilar Approvals & Launches 💉

Successfully launched multiple biosimilars expanding revenue diversity:

- ✅ Selarsdi (ustekinumab-aekn) launched February 2025, biosimilar to Stelara

- ✅ Selarsdi received FDA approval as fully interchangeable May 5, 2025

- ✅ Selarsdi IV formulation approved for Crohn's disease and ulcerative colitis

- ✅ Simlandi (adalimumab-ryvk) interchangeable Humira biosimilar continuing rollout

Debt Reduction Milestone 🏦

Critical deleveraging progress achieved:

- 📉 Net debt to EBITDA fell below 3.0x for first time since 2016

- 💰 Net debt reduced to approximately $15.0B (from $16.7B in March 2025)

- 🎯 On track to end 2025 with net debt/EBITDA ~2.8x

- 💪 Removes existential balance sheet concerns that plagued stock 2016-2023

Strong Analyst Support - December 2025 📈

Multiple analyst upgrades/reiterations:

- ✅ Bank of America: Maintained Buy, raised PT to $32 from $29 (10.5x 2026 EBITDA)

- ✅ Piper Sandler: Raised PT to $40 from $30

- ✅ JP Morgan: Maintained Overweight

- ✅ Goldman Sachs: Maintained Buy

- 📊 Consensus: 9 analysts with Strong Buy, average PT $29.78-$31.13

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timeline, here are the scenarios through June 18th covered call expiration:

📈 Bull Case (20% probability)

Target: $34-37 (CALLS GET ASSIGNED!)

How we get there:

- 💪 Q4 earnings CRUSH expectations with Austedo exceeding $2.15B full-year target, strong gross margin expansion

- 🎯 2026 guidance surprises positively - successfully navigating Revlimid cliff with biosimilar revenue offsetting losses

- 💊 Olanzapine LAI FDA review progresses smoothly with positive agency feedback signaling approval track

- 🚀 Biosimilar revenue ramp accelerates - Selarsdi/Simlandi capturing meaningful Stelara/Humira share

- 📊 Duvakitug Phase 3 initiation announced with strong partnership support from Sanofi

- 🏦 Net debt/EBITDA hits 2.7x or below, potential credit rating upgrade

- 💰 Management announces $700M cost savings program ahead of schedule

- 📈 Breakout above $32 gamma resistance triggers momentum buying to $35+ (implied move upper range)

Key metrics needed:

- Austedo revenue growth maintaining 30%+ trajectory

- 2026 revenue guidance >$16B (offsetting Revlimid headwinds)

- Gross margins expanding to 54-55% range

- Positive pipeline updates (olanzapine LAI, duvakitug, DARI)

What happens to the covered call: Stock rallies to $34-37, calls get assigned, seller delivers shares at $34. They're HAPPY - collected $2.08/share premium PLUS realized $34 sale price on stock they likely bought at $20-25. Total return: ~50-60% from original cost basis. This is the seller's "best case scenario" - maximize profit by selling at $34 cap.

Probability assessment: Only 20% because it requires MULTIPLE positive catalysts aligning perfectly. The 2026 Revlimid cliff is a known headwind, and IRA pricing will reduce Austedo from $6,623 to $4,093/month effective 2027. Stock already up 40% YTD - limited multiple expansion available.

🎯 Base Case (60% probability)

Target: $29-33 range (CHOPPY CONSOLIDATION - SELLER KEEPS STOCK)

Most likely scenario:

- ✅ Solid Q4 earnings meeting consensus ($0.65-0.70 EPS range)

- 📱 2026 guidance conservative but reasonable - acknowledging Revlimid headwinds offset by biosimilar/Austedo growth

- ⚖️ Austedo growth continues but moderates to 20-25% YoY (still strong, not spectacular)

- 🇮🇱 Biosimilar launches progressing steadily - Selarsdi/Simlandi capturing 5-8% market share

- 📊 Debt reduction continues - net debt/EBITDA toward 2.6-2.7x by mid-2026

- 🔄 Stock trades in gamma support ($30) and resistance ($32-33) bands for months

- 💤 Market digests massive YTD gains, waits for olanzapine LAI approval and 2027 revenue visibility

- ⏰ No major negative surprises, but no blockbuster positive catalysts either

What happens to the covered call: Stock stays in $29-33 range through June 18th expiration. $34 calls expire worthless, seller keeps all $1M premium AND continues to own the 480,000 shares. This is actually the seller's IDEAL outcome - collect income without surrendering equity upside beyond June. They can sell another round of calls for Q4 2026 and repeat the strategy.

Why 60% probability: TEVA is in "prove it" mode. Fundamentals improving but execution risk remains high. Revlimid headwind is real. Market likely to be patient, waiting for concrete evidence of sustainable growth beyond Austedo. Trading range most probable outcome.

📉 Bear Case (20% probability)

Target: $24-28 (PULLBACK TO SUPPORT)

What could go wrong:

- 😰 Q4 earnings disappoint or 2026 guidance worse than expected - Revlimid cliff bigger than anticipated

- 🚨 Austedo IRA pricing impact worse than modeled - 38% price reduction from $6,623 to $4,093/month pressures 2027 forecasts

- ⏰ Olanzapine LAI FDA review encounters issues - Complete Response Letter (CRL) or approval delay

- 💸 Biosimilar launches underwhelm - Selarsdi/Simlandi fail to gain meaningful share vs competitors

- 🇨🇳 Generic competition intensifies faster than expected - pricing pressure in core generic portfolio

- 📊 Debt reduction stalls - free cash flow pressured by opioid settlement payments

- 🌍 Israel geopolitical risks escalate - operational disruptions or investor concern

- 🔨 Break below $30 gamma support triggers cascade to $27-28 range

Critical support levels:

- 🛡️ $30.00: Major gamma floor (27.67B) - MUST HOLD or sentiment shifts negative

- 🛡️ $27.00: Deep support (5.60B gamma) - likely buying interest here

- 🛡️ $25.00: Extended floor (3.58B gamma) - represents ~$5 pullback from current levels

What happens to the covered call: Stock pulls back to $26-28 range. Calls expire worthless (good for seller!), but their underlying stock position is down $3-5/share from entry. However, the $2.08/share premium collected cushions the blow - net loss only $1-3/share vs $3-5 without the hedge. Seller still owns shares and can wait for recovery.

Probability assessment: 20% because TEVA's fundamentals remain solid (11 consecutive growth quarters, successful deleveraging, diversifying revenue). The turnaround is real. But execution risks (Revlimid cliff, IRA pricing, pipeline delays) could derail momentum temporarily. The covered call structure shows seller is protecting against this scenario while staying invested long-term.

💡 Trading Ideas

🛡️ Conservative: Share Purchase with Covered Calls (Copy The Strategy!)

Play: Buy TEVA stock at current levels, sell March/April $32-33 calls for income

Why this works:

- 📊 TEVA trading near $30.81 with strong $30 gamma support (27.67B) just 2.6% below

- 💰 Proven turnaround story: 11 consecutive growth quarters, debt reduction ahead of schedule

- 🎯 Valuation reasonable: Trading at discount to historical levels despite improved fundamentals

- 💸 Generate 4-6% income selling calls while waiting for next leg up

- 🛡️ Downside protected by improving balance sheet, diversifying revenue, strong management execution

- ⏰ Q4 earnings February 11th provides near-term catalyst

Position structure:

- 📈 Buy 100-500 shares TEVA at $30-31 (preferably on any dip toward $30 support)

- 📞 Sell 1 call per 100 shares: March 20th $32 calls or April 17th $33 calls

- 💵 Collect $1.50-2.00/share premium (estimate based on current IV)

- 🎯 Willing to sell shares at $32-33 (6-10% profit) if assigned, or keep stock + premium if expires worthless

Example trade (500 shares):

- Buy 500 TEVA @ $30.50 = $15,250 cost

- Sell 5 March $32 calls @ $1.80 = collect $900 premium (5.9% income over 2.5 months)

- Scenario 1: TEVA above $32 at March expiration → shares called away at $32, total profit = $750 (shares) + $900 (premium) = $1,650 (10.8% return in 2.5 months)

- Scenario 2: TEVA below $32 at March expiration → keep shares, keep $900 premium, sell April calls for another round

Risk level: Low-Moderate (own stock, capped upside) | Skill level: Intermediate

Expected outcome: Generate steady income while participating in turnaround thesis. If wrong and stock drops, premium provides cushion. If right and stock rallies, lock in 10-12% gains and repeat strategy.

⚖️ Balanced: Bull Put Spread (Cash-Secured Put Alternative)

Play: Sell put spread targeting $30 gamma support after Q4 earnings

Structure: Sell $30 puts, Buy $28 puts (March 20th expiration - post-earnings)

Why this works:

- 📊 Targets massive $30 gamma support (27.67B total gamma - THE strongest level)

- 💪 Defined risk spread ($2 wide = $200 max risk per spread)

- ✅ Collect premium while expressing bullish thesis on turnaround

- 🎯 Post-earnings timing allows volatility to settle before entry

- 🛡️ Even if TEVA pulls back to $28-29, breakeven is below $30 support

Wait for post-earnings entry (after Feb 11th):

- ⏰ Implied volatility will drop after earnings - makes premium collection more efficient

- 📉 Any earnings-driven dip provides better entry point for put spread

- ✅ Only enter if stock is $30.50+ (gives cushion to work)

Estimated P&L (adjust after Feb 11 earnings):

- 💰 Collect ~$0.60-0.80 net credit per spread post-earnings

- 📈 Max profit: $60-80 if TEVA above $30 at March expiration (keep entire credit)

- 📉 Max loss: $120-140 if TEVA below $28 (spread width minus credit)

- 🎯 Breakeven: ~$29.20-29.40

- 📊 Risk/Reward: ~2:1 risk to reward (acceptable for high-probability trade)

Position sizing: Sell 3-8 spreads depending on portfolio size (risk $600-1,600 max)

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

🚀 Aggressive: Long Call Spread into Earnings (BINARY EVENT PLAY!)

Play: Buy call spread betting on Q4 earnings beat and positive 2026 guidance

Structure: Buy $31 calls, Sell $34 calls (March 20th expiration - same strike as the covered call seller!)

Why this could work:

- 💥 TEVA has history of beating estimates (14.71% Q3 surprise, consistent guidance raises)

- 🎯 If Q4 earnings beat AND 2026 guidance strong, stock could gap to $33-35 range

- 📈 Call spread caps cost while providing 3:1 or better risk/reward if thesis plays out

- 🚀 Current positioning near $31 is weak resistance - breakout potential on positive news

- 💪 11 consecutive growth quarters builds credibility for continued execution

Why this could blow up (SERIOUS RISKS):

- ⏰ Earnings binary risk: February 11th results could disappoint on Revlimid guidance, Austedo moderation, or margin pressure

- 💸 Limited profit potential: Capped at $34 (same as institutional covered call seller)

- 😱 Total loss possible: If stock stays below $31 through March, spread expires worthless

- 📊 Fighting institutional flow: You're betting UP while $1M covered call seller is capping at $34

- 🎢 Requires 7-10% rally from current levels within 2.5 months

Estimated P&L:

- 💰 Cost: ~$1.00-1.30 per spread (estimate based on 3-wide spread)

- 📈 Max profit: $1.70-2.00 if TEVA above $34 at expiration (130-200% ROI!)

- 🚀 Partial profit: $0.50-1.00 if TEVA rallies to $32-33 range (40-80% ROI)

- 📉 Loss scenario: Lose $0.50-1.00 if TEVA stays below $32

- 💀 Total loss: Stock below $31 = lose entire $1.00-1.30 (100% loss)

Breakeven: ~$32.00-32.30

Entry timing:

- ⏰ Enter 1-2 weeks BEFORE Feb 11th earnings (late January/early February)

- 📊 Only enter if stock holding $30.50+ (below that, wait for recovery)

- ⚠️ Use tight position sizing - this is speculative earnings play

Exit strategy:

- ✅ If earnings beat: Take profits quickly if stock gaps to $33+ (don't get greedy - lock in 100%+ gains)

- ❌ If earnings disappoint: Cut losses immediately if stock gaps down below $30

- 🎯 If earnings neutral: Hold through March if stock holding $31+ support, exit if breaks below

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can afford to lose ENTIRE premium on spread

- ✅ Understand earnings can gap stock 5-10% either direction overnight

- ✅ Accept you're fighting institutional flow (covered call seller disagrees with your thesis)

- ✅ Have traded through earnings events before and can handle volatility

- ⏰ Will actively manage the position post-earnings (not set-and-forget)

Risk level: HIGH (can lose 100% of spread cost) | Skill level: Advanced only

Probability of profit: ~35-40% (need strong earnings beat AND positive guidance to profit)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💊 2026 Revlimid Revenue Cliff (MAJOR HEADWIND!): Generic lenalidomide competition intensifies starting January 31, 2026, when Sun Pharma and Cipla can sell unlimited quantities. This could eliminate over $1 billion in high-margin revenue overnight. TEVA must offset this with biosimilar growth and Austedo expansion or 2026 earnings will disappoint significantly. Q4 earnings guidance will be CRITICAL for understanding management's plan.

-

🏥 IRA Pricing Pressure on Austedo (2027 HEADWIND): Medicare price negotiation reduced Austedo from $6,623 to $4,093/month effective 2027 - a brutal 38% price cut on TEVA's fastest-growing product. While Austedo revenue can still grow via volume, this caps upside significantly. TEVA's legal challenge to IRA was rejected by D.C. Court in November 2025, removing any hope for relief. Market may not be fully pricing this 2027 impact yet.

-

🎯 Pipeline Execution Risk - Olanzapine LAI Critical: The olanzapine LAI NDA submitted December 9, 2025 represents a $1.5-2.0B peak sales opportunity critical to TEVA's $5B innovative medicines target by 2030. Any FDA delays, Complete Response Letter (CRL), or approval rejection would be devastating for long-term thesis. Standard review takes 10-12 months, putting decision in Q4 2026 - plenty of time for issues to emerge.

-

💸 Biosimilar Competition Intensifying: While TEVA launched Selarsdi (Stelara biosimilar) and Simlandi (Humira biosimilar), the market is increasingly crowded with multiple competitors launching similar products. Market share gains may be slower than expected if PBMs negotiate aggressively or favor other manufacturers. Biosimilar pricing pressure could erode margins quickly in race to bottom.

-

🇮🇱 Israel Geopolitical Risk: TEVA is headquartered in Tel Aviv with significant operations in Israel. Escalating Middle East tensions could disrupt operations, impact employee safety, or create investor concern leading to discount valuation vs peers. While hasn't materialized yet, remains tail risk that's difficult to quantify.

-

💰 Debt Burden Still Substantial: Despite progress reducing net debt to ~$15.0B and net debt/EBITDA below 3x, TEVA still carries ~$16.7B total debt. Opioid settlement payments continue to reduce free cash flow flexibility, limiting ability to invest aggressively in R&D or M&A. Rising interest rates could pressure refinancing costs on remaining debt maturities.

-

📊 Generic Drug Pricing Pressure Structural: TEVA's core generic business faces relentless pricing pressure from PBMs and Indian manufacturers (Cipla, Lupin, Sun Pharma) delivering ~11% CAGR vs 3% global market. While U.S. generics sales up 15% in 2024, this is increasingly commoditized business with low barriers to entry. Long-term margin compression likely.

-

🎢 Valuation Multiple Constrained by Generic Exposure: Despite turnaround progress, TEVA trades at discount to pure-play pharma peers due to 50%+ revenue from generic drugs. Market unlikely to award premium multiple until innovative medicines reach 40%+ of revenue mix (currently ~20%). This limits upside even if execution perfect.

-

🏛️ Legal/Regulatory Overhang: Historical price-fixing allegations and ongoing opioid litigation create headline risk. While nationwide settlement resolved with all 50 states and >99% of subdivisions, future lawsuits or regulatory actions remain possible.

-

📉 Institutional Seller at $34 Signals Caution: The $1M covered call sale at $34 strike by sophisticated institutional player signals smart money thinks upside is LIMITED over next 5 months. When funds managing hundreds of millions cap their upside at 10% above current levels rather than staying fully long, it's a caution flag about near-term momentum.

🎯 The Bottom Line

Real talk: A sophisticated institutional player just sold $1 MILLION worth of covered calls on TEVA, capping their upside at $34 through June 18th. This isn't bearish on TEVA's turnaround story - it's smart portfolio management by someone who's made EXCELLENT money on the 40% rally from $22 to $31 and wants to lock in income while staying invested.

What this trade tells us:

- 🎯 Sophisticated player expects CONSOLIDATION not continuation - stock range-bound $29-34 over next 5 months

- 💰 They're generating 6.8% income ($2.08/share on $30.81 stock) while waiting for next catalyst

- ⚖️ Willing to sell at $34 (happy to take 10% gains from current levels if it happens)

- 📊 They structured at $34 strike which is just above $33 gamma resistance - expects rally to stall there

- ⏰ June expiration captures Q4 earnings (Feb 11), Revlimid cliff impact (Jan 31+), biosimilar performance data

This is NOT a "sell everything" signal - it's a "take some profits and manage risk" signal while staying long-term bullish.

If you own TEVA:

- ✅ Consider selling March/April $32-33 calls to generate income (copy this strategy at smaller scale)

- 📊 Set MENTAL STOP at $30 (major gamma support 27.67B) to protect against earnings disappointment

- ⏰ You've already won with 40% YTD gains - protecting profits is smart, not weak

- 🎯 If earnings beat AND stock breaks $32, let it run to $34-35 before trimming

- 🛡️ Consider taking 25-40% profits at current levels and re-entering on any pullback to $28-29

If you're watching from sidelines:

- ⏰ February 11th before market open is the moment of truth - wait for Q4 earnings clarity!

- 🎯 Best entry likely post-earnings: $28-30 range on any profit-taking or conservative guidance

- 📈 Looking for confirmation of: Austedo on track to $2.5B by 2027, 2026 revenue guidance successfully navigating Revlimid cliff, biosimilar revenue ramping, olanzapine LAI on track for late 2026 approval

- 🚀 Longer-term (12-18 months), turnaround thesis remains compelling if execution continues - target $5B innovative medicines by 2030

- ⚠️ Current valuation fair but not cheap after 40% rally - need flawless execution to justify $34+

If you're bearish:

- 🎯 Wait for earnings to play out - shorting into turnaround momentum is dangerous

- 📊 First breakdown level at $30 (27.67B gamma support), major breakdown at $27

- ⚠️ Post-earnings put spreads ($32/$30 or $30/$28) offer defined-risk way to play downside if guidance disappoints

- 📉 Watch for break below $30 - that's trigger for cascade to $27-28

- ⏰ Timing matters: Premature bearish bets risk getting run over by earnings beat

Mark your calendar - Key dates:

- 📅 January 31, 2026 - Revlimid generic competition intensifies (Sun Pharma, Cipla unlimited quantities)

- 📅 February 11, 2026 (Tuesday) before market open - Q4 FY2025 earnings report (37 DAYS!)

- 📅 February 12, 2026 - Post-earnings price action and analyst reactions

- 📅 March 20, 2026 - Quarterly triple witch OPEX

- 📅 June 18, 2026 - Expiration of this $1M covered call trade

- 📅 Q4 2026 - Eylea biosimilar potential launch

- 📅 Late 2026 - Olanzapine LAI FDA decision expected (10-12 months from Dec 9 submission)

Final verdict: TEVA's turnaround is REAL - 11 consecutive growth quarters, debt reduction ahead of schedule, Austedo growing 38% YoY, successful biosimilar launches, and credible pipeline (olanzapine LAI $1.5-2.0B peak sales potential). BUT, after a 40% rally with major headwinds looming (2026 Revlimid cliff, 2027 Austedo IRA pricing), the risk/reward at $31 is BALANCED not compelling. The $1M institutional covered call signals: smart money is derisking and generating income while staying invested.

Be patient. Let earnings clear February 11th. If you own it, consider covered calls to generate income. If watching, wait for pullback to $28-30 for better entry. The pharma turnaround will still be here in 2-3 months, and you'll get a better price.

This is a show-me story now. Execution is everything. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 43.72x unusual score reflects this specific trade's size relative to recent TEVA history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Covered call strategies cap upside potential while providing limited downside protection through premium collection. The institutional seller may have complex portfolio needs not applicable to retail traders.

About Teva Pharmaceutical Industries: Teva Pharmaceutical, based in Israel, is the leading generic drug manufacturer in the world with a market cap of $35.5 billion in the Pharmaceutical Preparations industry. The company derives half of its sales from North America and makes up a high-single-digit percentage of total U.S. generic prescriptions, with additional operations in Europe, Japan, Russia, and Israel.