⚡ TLN Massive $16.5M Options Roll - Nuclear Power Giant Shifts Bullish Stance! 🔋

📅 December 12, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

A sophisticated trader just executed a $16.5 MILLION options roll on Talen Energy this morning at 10:00:48! They closed out 4,000 contracts of March 2026 $420 calls (selling $9M worth) while simultaneously buying 3,540 contracts of January 2026 $380 calls for $7.5M. With TLN trading at $364.32 and riding the explosive AI data center power demand wave, this represents a strategic repositioning - bringing the strike closer to at-the-money and pulling in the timeline. Translation: Smart money is locking in gains from the $420 calls while doubling down on near-term upside with better-positioned strikes!

📊 Company Overview

Talen Energy (TLN) is an independent power producer and energy infrastructure powerhouse positioned at the intersection of nuclear energy and AI data center demand:

- Market Cap: $16.85 Billion (mid-cap power producer)

- Industry: Electric Services - Independent Power Generation

- Total Capacity: 10.7 GW across United States (43% carbon-free nuclear from Susquehanna plant)

- Primary Business: Wholesale electricity generation through PJM (Mid-Atlantic) and WECC (Montana) markets, with strategic focus on nuclear power for data center partnerships

- Key Asset: 2.2 GW Susquehanna nuclear facility - the crown jewel powering Amazon's AI ambitions

What makes TLN unique: Talen owns one of the largest nuclear power facilities in the U.S. and has secured an $18 billion, 20-year power purchase agreement with Amazon to supply 1,920 MW of carbon-free nuclear power through 2042 for AI data centers. This positions TLN as a premier play on the AI infrastructure buildout requiring massive, reliable, zero-emission baseload power.

💰 The Option Flow Breakdown

The Tape (December 12, 2025 @ 10:00:48):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Z-Score |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:00:48 | TLN | ASK | SELL | CALL $420 | 2026-03-20 | $9M | $420 | 4,000 | 470 | 4,000 | $364.32 | $22.50 | 6.81 |

| 10:00:48 | TLN | ASK | BUY | CALL $380 | 2026-01-16 | $7.5M | $380 | 3,500 | 3,600 | 3,540 | $364.32 | $21.05 | 10.31 |

🤓 What This Actually Means

This is a sophisticated "roll down and in" adjustment on a massive position! Here's what went down:

- 💰 Net cost: Essentially neutral - Collected $9M from closing March $420 calls, immediately redeployed $7.5M into January $380 calls (net credit of ~$1.5M)

- 🎯 Strike adjustment: Rolled DOWN from $420 (15.3% above current price) to $380 (4.3% above) - much better positioned to profit

- ⏰ Timeline shift: Pulled expiration IN from March 20 (98 days) to January 16 (35 days) - betting on near-term catalyst

- 📊 Size matters: This represents ~$1.4 billion in notional exposure (3,540 contracts × 100 shares × $380 strike)

- 🔥 Extreme unusual activity: Z-scores of 6.81 and 10.31 mean BOTH sides are wildly unusual (happens only a few times per year)

What's really happening here: This trader likely bought the $420 March calls months ago when TLN was trading much lower (probably in the $200-250 range). With the stock now at $364 and those calls worth $22.50, they're sitting on MASSIVE gains. Rather than take profits and walk away, they're repositioning for the next leg higher - rolling to a strike that's closer to at-the-money ($380 vs $420) which gives much better delta exposure and profit potential.

The timing is CRITICAL: They rolled into January 16 expiration which captures:

- Q4 2025 completion of $3.5 billion gas plant acquisitions (expected this month!)

- Full-year 2024 earnings report (late February 2026)

- Continued execution on Amazon partnership ramp

- Year-end portfolio positioning into 2026

What this tells us: This trader is so confident in near-term upside (next 35 days) that they're willing to give up the extra 63 days of time value in the March calls to get better strike positioning in January. They're essentially saying: "TLN is going significantly higher SOON - I want maximum bang for my buck over the next month, not spread over 3 months."

Unusual Score Analysis:

- March $420 calls (close): Z-score 6.81 = EXTREMELY UNUSUAL (7x standard deviations above average)

- January $380 calls (buy): Z-score 10.31 = OFF THE CHARTS (10x standard deviations!)

- Combined significance: This is institutional-sized repositioning - likely a hedge fund or proprietary trading desk managing $100M+ portfolio

The fact they're buying January calls at $380 (only 4.3% above current price) instead of continuing to hold the already-profitable $420 calls tells us they expect a MOVE in the next 35 days. At-the-money calls have much higher delta (~0.55-0.65) vs out-of-the-money $420 calls (~0.30-0.40), meaning they'll capture more of every dollar TLN moves higher.

📈 Technical Setup / Chart Check-Up

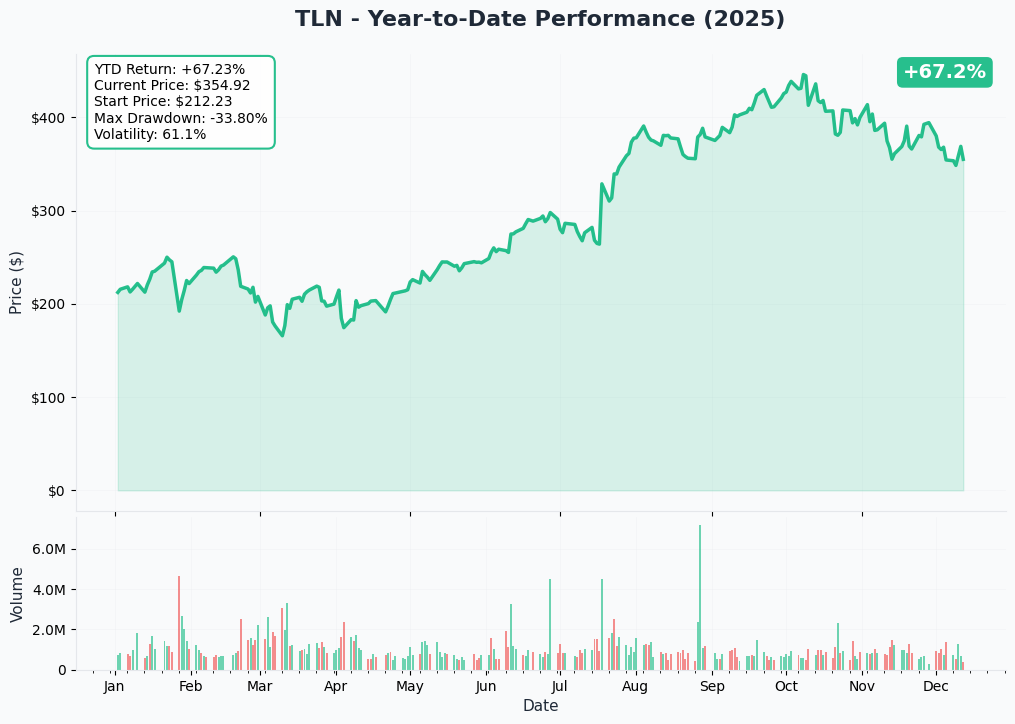

YTD Performance Chart

TLN has been absolutely ON FIRE this year - currently trading at $359.15 after an explosive +100% YTD performance that made it one of the best-performing large-cap energy stocks in 2025. The chart tells an incredible AI power demand story:

Key observations:

- 🚀 Parabolic rally: Vertical move from $213 in December 2024 to all-time highs near $390 in November on Amazon partnership expansion

- 📈 Multiple breakouts: Cleared major resistance at $250, $300, $350 - each level became support

- 📊 Volume explosion: Massive institutional accumulation throughout 2025 as AI data center catalysts materialized

- ⚠️ Recent consolidation: After hitting $390, pulled back 9.85% to mid-$350s - healthy digestion before next leg

- 🎯 Support holding: YTD gains remain intact, trading well above 50-day and 200-day moving averages

The recent pullback from $390 to $354 (9.85% in early December) actually represents a BUYING OPPORTUNITY rather than a breakdown. The stock consolidated gains, shook out weak hands, and is now setting up for another run. The options activity today suggests smart money sees the consolidation as complete.

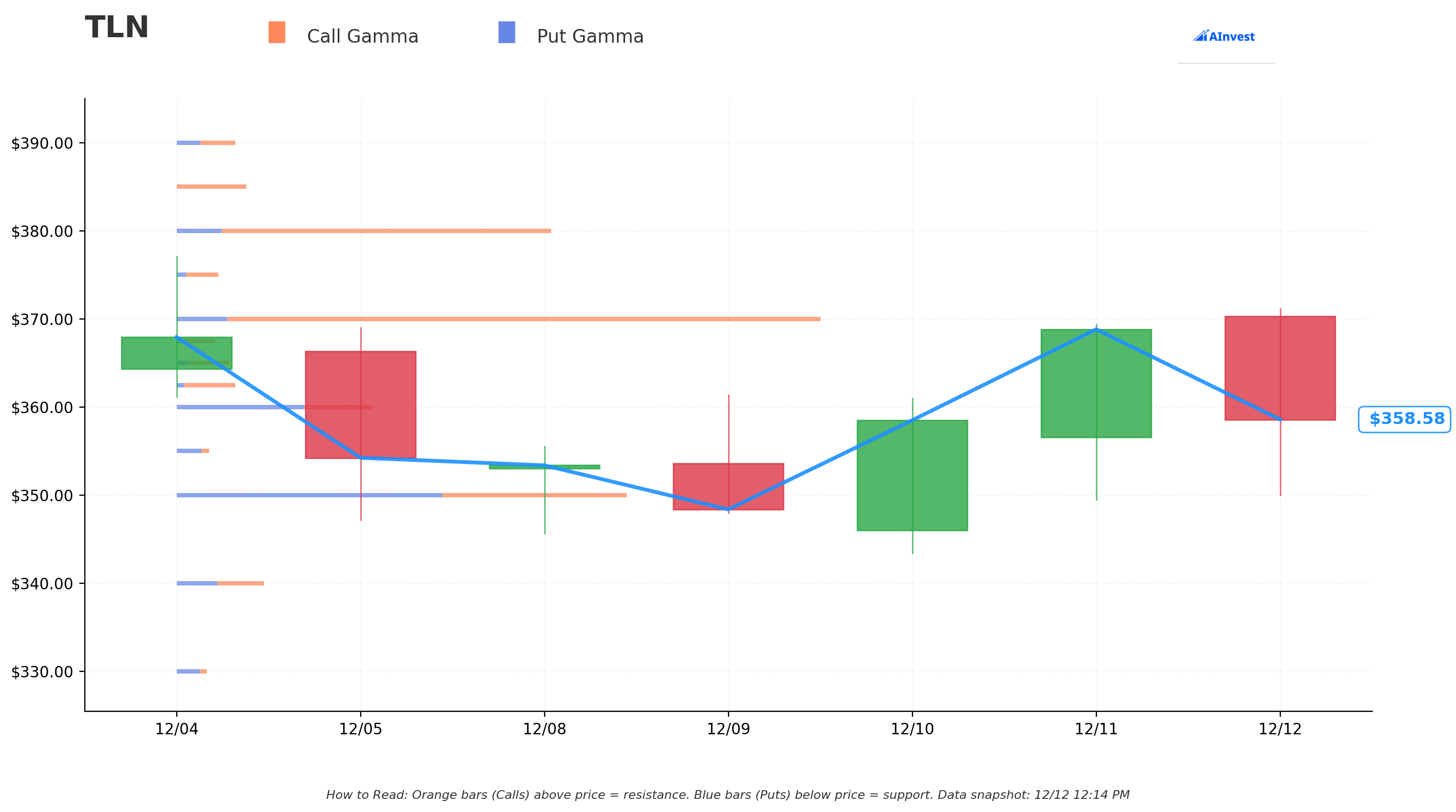

Gamma-Based Support & Resistance Analysis

Current Price: $359.15

The gamma exposure map reveals critical price magnets and walls that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $350 - STRONGEST IMMEDIATE SUPPORT with 1.66B total gamma exposure (0.98B put gamma) - only 2.5% below current price

- $340 - Secondary support at 0.32B gamma (5.3% below current)

- $320 - Extended support zone with 0.25B gamma (10.9% below)

- $300 - Major psychological floor with 0.33B gamma (16.5% below)

🟠 Resistance Levels (Call Gamma Above Price):

- $360 - Immediate ceiling with 0.72B gamma (0.47B put gamma creates complexity) - virtually at current price!

- $370 - KEY RESISTANCE with 2.38B gamma exposure (STRONGEST LEVEL - 2.19B call gamma!) - 3.0% above current

- $380 - Secondary ceiling at 1.38B gamma (EXACTLY where the new calls are struck!) - 5.8% above current

- $385 - Minor resistance at 0.26B gamma (7.2% above)

- $390 - Extended resistance at 0.22B gamma (8.6% above)

- $400 - Major psychological ceiling at 0.95B gamma (11.4% above)

What this means for traders: TLN is trading in a critical zone - just cleared $360 resistance and heading toward the massive $370 wall (2.38B gamma - THE SINGLE LARGEST LEVEL). Notice anything? The call buyer struck at $380 which has 1.38B gamma and sits just above the major $370 resistance. This isn't random - they're positioning for a breakout THROUGH $370 that targets $380-390.

The gamma structure is OVERWHELMINGLY BULLISH:

- Total call gamma: 7.52B

- Total put gamma: 3.31B

- Net GEX bias: Bullish (2.3:1 call-to-put ratio)

This setup creates a "gamma squeeze" scenario: If TLN breaks above $370, market makers will need to buy stock to hedge their short call exposure, accelerating the move toward $380-390. Conversely, $350 support should be rock-solid given the large put gamma concentration there.

Critical observation: The stock is sitting at $359 (just below $360) with the next major resistance at $370 only 3% away. Once TLN clears $370, there's relatively light resistance until $380 (the new call strike) and $400. This creates an asymmetric setup - risk 2.5% to $350 support, reward 6-11% to $380-400 resistance.

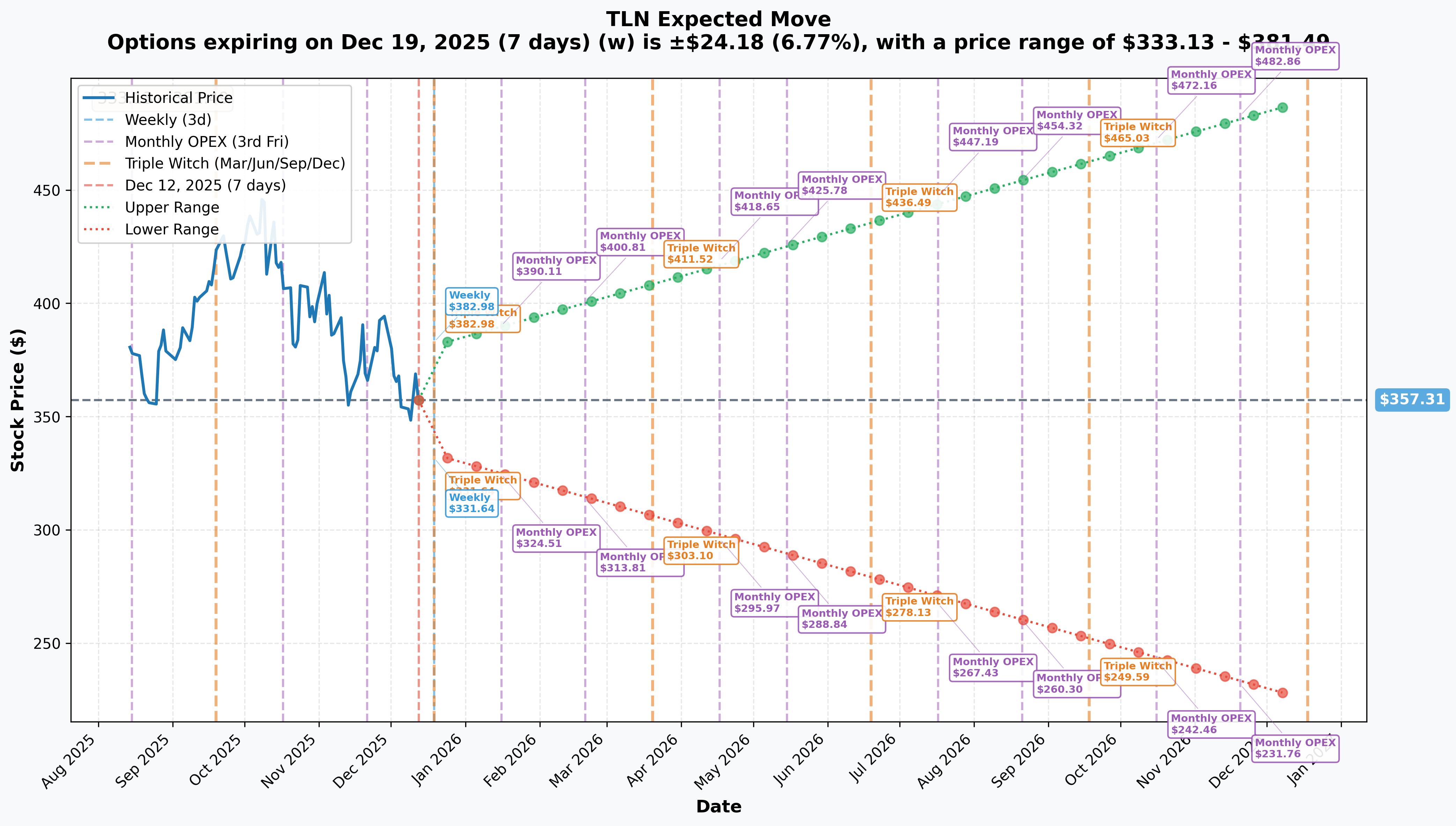

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 7 days): ±$24.18 (±6.77%) → Range: $333.13 - $381.49

- 📅 Monthly OPEX (Dec 19 - same as weekly): Same implied move (coincides with Triple Witch)

- 📅 Quarterly Triple Witch (Dec 19 - 7 days): Same ±$24.18 / ±6.77% → THIS IS THE NEAR-TERM CATALYST!

- 📅 January OPEX (Jan 16 - 35 days - THIS TRADE!): ±$32.81 (±9.18%) → Range: $324.51 - $390.11

Translation for regular folks: Options traders are pricing in a 6.77% move ($24) by next week's Triple Witch expiration on December 19th. The market expects meaningful volatility heading into year-end, likely driven by Q4 acquisition closure news and year-end positioning. The upper range of $381.49 for the weekly move gets TLN very close to the $380 strike where the new calls are positioned!

More importantly, the January 16th expiration (when this $7.5M trade expires) has an upper range of $390.11 - meaning the market sees legitimate probability of TLN trading as high as $390 over the next 35 days. The $380 calls would be worth $10+ in that scenario, delivering 50%+ return from the $21.05 entry price.

Key insight: The expansion in implied volatility from 6.77% (weekly) to 9.18% (monthly) reflects anticipation of multiple catalysts converging in December-January timeframe. The call buyer is betting TLN breaks out above $380 (currently 5.8% away) and potentially runs to $390-400 by January expiration.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Freedom & Guernsey Gas Plant Acquisitions Close - Q4 2025 (IMMINENT!) 🏭

Talen's massive $3.5 billion acquisition of two combined-cycle gas plants is expected to close THIS MONTH (Q4 2025):

- 🏭 Moxie Freedom Energy Center: 1,045 MW in Pennsylvania

- 🏭 Guernsey Power Station: 1,836 MW in Ohio

- 💰 Total cost: $3.8 billion gross ($3.5B net after tax benefits)

- 📈 FCF Impact: Expected to increase free cash flow per share by >40% in 2026 and >50% in following two years

- 🎯 Strategic value: Adds 2,881 MW of flexible gas capacity to complement nuclear baseload, enhancing data center offering portfolio

Why this matters NOW: The acquisition closing represents an IMMEDIATE re-rating catalyst. Once the deal closes, TLN instantly becomes a 13.6 GW power producer (up from 10.7 GW) with significantly more geographic and fuel diversity. The 40%+ FCF per share accretion in 2026 will force analysts to raise earnings estimates and price targets. This is the type of transformative acquisition that drives 10-20% stock moves when it officially closes.

December 19 Triple Witch Expiration (7 DAYS AWAY!) 📊

Quarterly options expiration on December 19th creates technical pressure with massive open interest rolling:

- 🎯 Options market pricing ±6.77% move ($24) through Dec 19

- 📊 Implied range: $333-$381 (upper bound very close to $380 call strike)

- ⚡ Triple witch expirations historically volatile for heavily-optioned stocks

- 🔄 Dealer hedging flows can amplify moves in either direction

Year-End Portfolio Positioning (Next 2 Weeks) 💼

Late December traditionally sees:

- 📈 Tax-loss harvesting complete, buying resumes

- 🎯 Window dressing by institutional investors

- 💰 Year-end bonuses deployed into January

- 📊 Light volume creates potential for outsized moves

- 🚀 "Santa Claus rally" seasonality favors risk assets

🚀 Near-Term Catalysts (Q1 2026 - Within January Expiration)

Full-Year 2024 Earnings Report - Late February 2026 📈

Talen expected to report FY 2024 and Q4 2024 results in late February (based on historical pattern of February 27 timing):

- 💰 Key metrics: Full-year Adjusted EBITDA vs. $395-595M FCF guidance (narrowed in Q3 2025)

- 🏭 Acquisition update: First full quarter of Freedom/Guernsey operations post-close

- 📊 Amazon PPA progress: Updates on transmission reconfiguration timeline (Spring 2026 target)

- ⚡ Nuclear PTC monetization: Expected to announce sale of 2025 production tax credits (~$191M like 2024)

- 🎯 2026 guidance: Critical for validating 40%+ FCF growth thesis from acquisitions

Historical performance: Talen crushed Q3 2024 expectations, delivering $230M Adjusted EBITDA and $97M FCF while raising full-year guidance. Q3 2024 earnings showed $1.64 EPS vs. $1.15 consensus (+42.6% surprise). Continued execution would validate the bullish thesis.

Share Repurchase Program Execution (Through 2028) 💵

Talen's $2 billion buyback authorization through December 2028 creates ongoing support:

- 💰 Size: $2B represents ~12% of current $16.85B market cap

- 📊 Recent activity: Repurchased over 20% of shares in past year, ~75% of market cap since 2023 bankruptcy emergence

- 🎯 Shares outstanding: Reduced to 45.96M shares post-repurchase

- ⚡ EPS accretion: Every dollar of buyback boosts per-share metrics, especially as FCF expands 40%+ in 2026

Buyback programs provide natural bid support during pullbacks and amplify earnings growth through share count reduction. With TLN generating strong cash flow from record PJM capacity pricing ($670M annually), expect aggressive buying on any weakness.

Transmission Reconfiguration for Amazon - Spring 2026 (WITHIN VIEW) ⚡

The transmission work to shift Amazon's arrangement from co-located to front-of-meter scheduled for Spring 2026:

- ⏰ Timing: Spring 2026 during Susquehanna nuclear refueling outage

- 🎯 Impact: Enables transition from 300 MW co-located to pathway for full 1,920 MW delivery by 2032

- 💡 Structure: Avoids FERC co-location approval issues by using transmission grid

- 📈 Revenue visibility: De-risks the $18 billion Amazon revenue stream through proven infrastructure path

Any positive updates on reconfiguration progress (permits approved, timeline acceleration, additional capacity potential) would be major catalysts within the January expiration window.

📊 Medium-Term Catalysts (2026 and Beyond)

Amazon Nuclear Power Partnership: The $18 Billion Tailwind 🤝

Talen's expanded PPA with Amazon announced June 11, 2025 represents a generational growth driver:

- 💰 Contract value: $18 billion in total revenue through 2042 (20-year term)

- ⚡ Power delivery: 1,920 MW of carbon-free nuclear power at full ramp (no later than 2032)

- 🏭 Current status: Existing 300 MW co-location being reconfigured to front-of-meter (Spring 2026)

- 🚀 Growth potential: Joint exploration of Small Modular Reactors (SMRs) and Susquehanna uprates to expand capacity

- 🌍 Market validation: Proves nuclear is THE solution for AI data center power demands (24/7 baseload, zero emissions)

Why this matters: Amazon (AWS) chose Talen's Susquehanna nuclear facility over all other U.S. power options for their AI infrastructure buildout. This validates nuclear as the ONLY technology that can deliver the combination of:

- 24/7 reliability (AI can't tolerate interruptions)

- Massive scale (1.9 GW = enough for ~1.5 million homes)

- Zero carbon emissions (corporate sustainability mandates)

- Price certainty (20-year fixed contract vs. volatile gas/coal)

As other hyperscalers (Google, Microsoft, Meta) race to secure similar nuclear power deals, Talen has first-mover advantage and proven ability to deliver at scale.

PJM Capacity Market: Record Pricing Windfall ⚡

The 2025/2026 PJM capacity auction results delivered an extraordinary windfall:

- 💰 Capacity cleared: 6,820 MW across MAAC, PPL, and PSEG zones

- 📈 Clearing price: $269.92 per MW-day (9x increase from prior year's $28.92/MW-day!)

- 💵 Revenue impact: ~$670 million in capacity revenues for 2025/2026 planning year (June 2025 - May 2026)

- 🎯 Future auctions: Next auction results will determine 2026/2027 revenues - current pricing provides strong baseline

Context: PJM capacity prices exploded due to tight supply/demand fundamentals (coal retirements, data center load growth, extreme weather reliability needs). While unlikely to sustain 9x levels indefinitely, even modest pullback to $150-200/MW-day would still represent 5-7x historical averages and massive profit tailwind for Talen.

Nuclear Production Tax Credit Monetization 💵

Annual monetization of nuclear PTCs provides predictable cash flow:

- 💰 2024 precedent: Sold 2024 credits for $191.2 million cash in September 2025

- 📅 2025 credits: Expected to sell late 2025/early 2026 for similar magnitude (~$190-200M)

- ⏰ Duration: PTC available through 2032

- 🎯 Use of proceeds: Debt reduction, acquisition funding, share buybacks

This represents ~$1.4 billion in cumulative cash flow through 2032 from tax credit monetization alone - pure incremental value not dependent on power prices or capacity market outcomes.

Small Modular Reactor (SMR) Development 🔬

Joint SMR development with Amazon within Pennsylvania footprint:

- 🏗️ Technology: Next-generation modular reactors with faster build times than traditional reactors

- 📅 Timeline: Multi-year exploratory phase (no SMRs currently operational in U.S.)

- 💡 Potential: Could double nuclear capacity beyond current 2.2 GW Susquehanna plant

- 🇺🇸 Policy support: $1B DOE supercomputer contracts validate federal backing for nuclear expansion

While speculative and long-dated, SMR success would transform Talen into the dominant nuclear power provider for AI data centers with decades of growth visibility.

⚠️ Risk Catalysts (Headwinds to Monitor)

FERC Regulatory Overhang 🚨

FERC's November 2024 rejection of amended interconnection agreement remains a significant overhang:

- ⚖️ Issue: FERC rejected increasing Susquehanna co-located load from 300 MW to 480 MW

- 🎯 Concerns: Cost-shifting to ratepayers ($140M annually per opponents), grid reliability, transparency

- 📅 Legal challenge: Talen filed lawsuit January 28, 2025 in Fifth Circuit Court of Appeals

- ⏰ Timeline: Multi-year uncertainty as court proceedings unfold

- 💡 Workaround: The front-of-meter transmission reconfiguration (Spring 2026) sidesteps FERC co-location issues

Good news: The revised Amazon deal structure (front-of-meter vs co-located) appears to resolve FERC's objections, but any new regulatory challenges could delay ramp timeline or reduce economics.

Acquisition Integration Execution Risk 🏭

Integrating $3.5 billion of new assets while managing existing operations carries risk:

- ⏰ Timeline pressure: Q4 2025 close requires rapid integration for 2026 targets

- 🏭 Operational complexity: Combined-cycle gas plants in new Ohio market different from existing PJM footprint

- 💰 Debt load: $1.2 billion Term Loan B plus notes increases leverage

- 📊 Synergies: 40%+ FCF accretion assumes successful integration and synergy capture

Any operational hiccups, unexpected capex requirements, or delays in achieving projected synergies could disappoint investors and pressure the stock.

Power Price and Capacity Market Volatility ⚡

Energy markets remain inherently volatile:

- 📊 PJM capacity swings: 9x price increase (2024: $28.92 to 2025: $269.92/MW-day) demonstrates extreme volatility

- 💨 Natural gas prices: Volatility impacts margins despite hedging programs

- 🌤️ Weather dependency: Extreme weather drives both upside (peak pricing) and downside (forced outages)

- 🔄 Regulatory changes: PJM market rule changes can impact economics

While current capacity pricing is extraordinarily favorable, reversion to lower levels would pressure earnings (though still likely above historical averages given structural tightness).

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through January 16th expiration:

📈 Bull Case (55% probability - BASE CASE)

Target: $380-$400

How we get there:

- ✅ Freedom & Guernsey acquisition closes in December as planned with positive market reception

- 💰 Year-end tax-loss harvesting complete, buying resumes into January

- 📈 Analyst upgrades following acquisition close and FCF accretion visibility

- 🏭 Positive updates on Spring 2026 transmission reconfiguration progress

- ⚡ Any incremental Amazon partnership news (additional capacity, timeline acceleration)

- 💵 Continued aggressive share buyback execution supports valuation

- 📊 Breakout above $370 gamma resistance triggers technical rally to $380-390

Path: $359 → $370 (breakthrough) → $380 (call strike) → $390-400 (implied move upper range)

Key metrics needed:

- Acquisition close announcement (transformative catalyst)

- Maintenance of $350 support floor during any pullbacks

- Volume confirmation on break above $370 resistance

- Analyst price target raises following acquisition (currently $415 average)

Probability assessment: 55% because this is the PATH OF LEAST RESISTANCE. TLN already consolidated from $390 to $354 (pullback complete), sits just below $370 resistance, has immediate positive catalyst (acquisition close) within days/weeks, and benefits from favorable seasonality (year-end rally). The gamma structure (7.52B call vs 3.31B put) supports upside. Most importantly, the unusual options activity today (rolling into near-term $380 calls) signals smart money positioning for this exact scenario.

Call option P&L at $380: Worth $0 (at-the-money), breakeven from $21.05 entry (0% return but protected from loss) Call option P&L at $390: Worth $10.00, profit = -$11.05 loss per share (still underwater but reduced) Call option P&L at $400: Worth $20.00, profit = -$1.05 loss per share (near breakeven)

Note: These assume intrinsic value only at expiration. Earlier moves would show greater profit due to remaining time value.

🎯 Moderate Upside (30% probability)

Target: $390-$420 (SUBSTANTIAL BREAKOUT)

What needs to happen:

- 🚀 Acquisition close PLUS unexpected positive surprise (additional capacity, better terms, faster integration)

- 💰 Nuclear PTC monetization announced early (2025 credits) with proceeds allocated to accelerated buyback

- 🎯 PJM announces next capacity auction results showing sustained high pricing ($200+ MW-day)

- 📈 Broader utility/power sector rally lifts all boats (clean energy policy support, data center buildout acceleration)

- ⚡ Amazon partnership expansion beyond 1,920 MW discussed or hinted at

- 📊 Multiple analyst upgrades with price targets raised to $450-500 range

Path: $359 → $380 (quick) → $400 (momentum) → $420 (breakout to new highs)

Why only 30%: Requires MULTIPLE positive catalysts to align within just 35 days. While each individually is plausible, getting several simultaneously in compressed timeframe is lower probability. Would need perfect execution plus favorable macro conditions.

Call option P&L at $420: Worth $40.00, profit = $18.95/share × 3,540 contracts = $6.7M gain (90% return) - This is the old $420 March call strike that was rolled! If stock reaches $420 by January, the trader will have missed that exact strike but the $380 calls would still deliver massive returns with intrinsic value of $40.

📉 Bear Case (15% probability)

Target: $320-$350 (TEST SUPPORT)

What could go wrong:

- 🚨 Acquisition close delayed beyond Q4 2025 (regulatory issues, financing complications)

- ⚖️ New FERC regulatory challenge emerges on front-of-meter Amazon arrangement

- 💸 Broader market correction drags utilities lower (recession fears, interest rate spike)

- 🏭 Unexpected operational issue at Susquehanna nuclear plant (forced outage, maintenance)

- 📉 PJM capacity price outlook weakens (new supply coming online faster than expected)

- ⚡ Transmission reconfiguration timeline pushed from Spring 2026 to later in year

- 🔨 Break below $350 support triggers technical selling cascade

Critical support levels:

- 🛡️ $350: MUST HOLD (1.66B gamma, strongest nearby support) - only 2.5% below current

- 🛡️ $340: Secondary floor (0.32B gamma) - 5.3% below current

- 🛡️ $320: Extended support (0.25B gamma) - 10.9% below current

Probability assessment: Only 15% because it requires significant negative catalyst or broader market selloff to override strong fundamental backdrop. Talen's Amazon partnership, record capacity pricing, pending acquisition, and buyback program create multiple support factors. The $350 gamma support is substantial (1.66B total gamma). Additionally, the unusual call buying today argues against smart money expecting downside.

Call option P&L in Bear Case: Options expire worthless or near-worthless. Loss = -$21.05/share × 3,540 contracts = -$7.45M loss (100% loss of premium) - This is the risk the trader accepted by rolling into near-term calls.

💡 Trading Ideas

🛡️ Conservative: Follow the Leader with Stock + Protective Put

Play: Buy TLN stock at current levels ($359), add protective put for downside insurance

Structure:

- 📈 Buy 100 shares TLN stock at $359 = $35,900 cost

- 🛡️ Buy 1x January $350 put at ~$8-10 = $800-1,000 protection cost

- 💰 Total investment: ~$36,700-36,900

Why this works:

- 🎯 Get stock exposure to capture upside toward $380-400 bull case

- 🛡️ Put protection limits maximum loss to ~$18-20 per share (5-6% max downside)

- ⏰ Captures all catalysts within January expiration (acquisition close, earnings preview, positioning)

- 💡 No leverage risk - you own the stock, put is just insurance

- 📊 If stock rallies to $380-390, put expires worthless ($800 cost) but stock gains $21-31 per share

- 🎯 Breakeven: $367-369 (need 2-3% gain to cover put premium)

Position sizing: Use 20-30% of equity allocation for individual position (diversification)

Risk level: Low-Moderate (defined downside, unlimited upside) | Skill level: Beginner-friendly

Expected outcome: Participate in bull case rally to $380+ while sleeping well knowing downside is limited to $350 support. The $350 put strike sits exactly at the major gamma support level (1.66B), making it high-probability that stock holds above this level.

⚖️ Balanced: Bull Call Spread (Copy the Pro Trade)

Play: Replicate the institutional positioning with bull call spread

Structure: Buy January $370 calls, Sell January $390 calls (1:1 ratio)

Why this works:

- 💰 Defined risk spread ($20 wide = $2,000 max risk per spread)

- 🎯 Targets breakout through $370 gamma resistance toward $380-390

- 📉 Limited capital at risk vs. buying stock outright

- ⏰ 35-day expiration captures imminent acquisition catalyst plus year-end momentum

- 💵 Better risk/reward than naked calls - capping upside at $390 to reduce cost

- 🤝 Positioned similarly to the institutional trader (bullish $370-390 range) but with defined risk

Estimated P&L (adjust based on current market prices):

- 💰 Net debit: ~$8-10 per spread ($800-1,000 per spread)

- 📈 Max profit: $10-12 if TLN above $390 at expiration = $1,000-1,200 gain (100-150% return)

- 📉 Max loss: $8-10 if TLN below $370 at expiration = -$800-1,000 loss (100% of premium)

- 🎯 Breakeven: ~$378-380

Entry timing:

- ✅ Can enter immediately given proximity to $370 resistance and imminent catalysts

- ⏰ Consider scaling in - half position now, half on any dip toward $355

Position sizing: Risk 5-10% of options allocation per spread (this is directional speculation)

Risk level: Moderate (defined risk, directional bullish) | Skill level: Intermediate

Profit zones:

- TLN at $380 at expiration: Spread worth $10, profit ~$1-2/share

- TLN at $390+ at expiration: Spread worth $20 (max value), profit ~$10-12/share (100-150% ROI)

🚀 Aggressive: Replicate the Institutional Trade (ADVANCED)

Play: Buy January $380 calls - EXACT same structure as the $7.5M institutional trade

Structure: Buy TLN January 16, 2026 $380 calls at current market price (~$21-22)

Why this could work:

- 🐋 You're literally copying a $7.5 MILLION institutional trade - someone with serious conviction and information edge

- 🎯 Strike at $380 (5.8% above current) perfectly positioned above $370 resistance

- ⚡ Captures all near-term catalysts: acquisition close, year-end momentum, early 2026 earnings setup

- 💪 High leverage: Each $1 move in TLN above $380 = $1 in option value (delta ~0.55-0.60)

- 🚀 If bull case plays out ($390-400 by Jan 16), calls worth $10-20 = 50-100% gain from $21 entry

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: $2,100-2,200 per contract, need meaningful capital

- ⏰ TIME DECAY: Theta burns -$50-80/day as expiration approaches

- 📉 Binary catalyst risk: If acquisition delayed or negative news hits, could lose 50-100% of premium quickly

- 🎢 Need execution: Stock must move from $359 to $380+ (6% move) just to reach breakeven at expiration

- ⚠️ Institutional trader has much longer time horizon, may be hedging complex portfolio - don't assume you have same risk tolerance

- 💀 Zero value risk: Below $380 at expiration = total loss of $2,100+ per contract

Estimated P&L:

- 💰 Cost: ~$21-22 per contract ($2,100-2,200 per contract)

- 📈 Profit scenario: TLN at $390 = calls worth $10 = -$11-12 loss per share (ouch - still underwater!)

- 📈 Better scenario: TLN at $400 = calls worth $20 = -$1-2 loss per share (near breakeven)

- 🚀 Home run: TLN at $420 = calls worth $40 = +$18-19 gain per share (85-90% return!)

- 📉 Loss scenario: TLN at $370 = calls worth ~$2-3 = -$18-19 loss (85-90% loss)

- 💀 Total loss: TLN below $380 = lose $21-22 per contract (100% loss)

Breakeven: ~$401-402 at expiration (need 12% rally from current $359!)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded options through binary catalysts before and understand time decay

- ✅ Can afford to lose ENTIRE premium (real possibility if acquisition delays or market sells off)

- ✅ Understand the institutional trader may have information/hedges you don't have

- ✅ Accept that you need TLN to rally 12%+ to breakeven (not just make the $380 strike)

- ⏰ Plan to actively manage position - take profits on rallies to $380-390, cut losses if breaks $350 support

- 📊 Have stop-loss discipline: Consider selling if TLN drops below $350 support to preserve remaining value

Alternative aggressive approach: Instead of buying naked calls, consider a smaller bull call spread ($370/$390 or $375/$395) which reduces cost and defines max loss while still providing good leverage to the bull case.

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~45% (need sustained rally above $380 by January, facing time decay and need for catalyst execution)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🏭 Acquisition closing risk (IMMINENT BINARY EVENT): The $3.5 billion Freedom & Guernsey deal expected to close in Q4 2025 (THIS MONTH!) represents a near-term binary catalyst. Any delay due to regulatory issues, financing complications, or unexpected conditions would be major disappointment. Integration of 2,881 MW of new gas capacity while managing existing 10.7 GW fleet carries execution risk. The 40%+ FCF per share accretion assumes successful integration and synergy capture. Market has likely priced in successful close - delay would trigger selloff.

-

⚖️ FERC regulatory overhang remains unresolved: While the front-of-meter transmission reconfiguration sidesteps prior FERC concerns about co-location, regulatory uncertainty persists. FERC's November 2024 rejection and ongoing legal challenge in Fifth Circuit create multi-year uncertainty. Any new regulatory challenges on the Spring 2026 transmission work could delay Amazon ramp or reduce economics. Opponents (AEP, Exelon, Vistra, PPL) remain hostile to Talen's data center strategy.

-

⚡ PJM capacity market extreme volatility: While current capacity pricing of $269.92/MW-day delivers ~$670M annually, this represents a 9x increase from prior year ($28.92/MW-day). Such extreme swings demonstrate the inherent volatility of capacity markets. Future auctions could see meaningful pullbacks if new supply comes online faster than expected or demand growth disappoints. Even modest reversion to $150-200/MW-day (still strong historically) would significantly impact earnings. PJM market rule changes by FERC or PJM could also alter economics unpredictably.

-

💰 Valuation stretched after 100%+ YTD rally: TLN is up over 100% year-to-date from $180 area to current $359 - extraordinary outperformance. Current $16.85B market cap assumes flawless execution on multiple fronts: Amazon partnership ramp, acquisition integration, sustained capacity pricing, buyback execution. Limited margin for error at current valuation. Any disappointment on these fronts could trigger 15-25% correction back to $270-300 range. Recent 9.85% pullback from $390 high shows stock can move quickly in either direction.

-

🏭 Nuclear operational risk concentration: Talen's entire thesis depends on Susquehanna nuclear facility (2.2 GW, 43% of generation). Any unexpected operational issues - forced outages, maintenance delays, safety incidents, license renewal challenges - would be catastrophic. Nuclear plants operate on strict NRC oversight with zero tolerance for problems. The Spring 2026 transmission reconfiguration must occur during refueling outage - any complications that extend the outage would delay Amazon ramp. Talen has excellent operational track record (3.1% EFOF) but single-asset concentration creates tail risk.

-

📉 Broader utility sector weakness: Despite Talen's unique nuclear/data center positioning, it trades with utility sector correlation. If broader utilities sell off due to rising interest rates (refinancing risk on debt), recession fears (reduced demand), or regulatory headwinds, TLN would likely be dragged lower. The $1.2B Term Loan B and notes offerings increase leverage and interest rate sensitivity.

-

🕰️ Amazon partnership timeline risk (2032 full ramp distant): While the $18 billion Amazon contract through 2042 is transformative, full 1,920 MW delivery isn't expected until 2032 - seven years away! Spring 2026 transmission reconfiguration enables the pathway but actual ramp occurs gradually over many years. Any delays in achieving interim milestones (600 MW by 2028, 1,200 MW by 2030, etc.) would push revenue realization further out. Long time horizon creates numerous execution risk points.

-

💵 Nuclear PTC expiration cliff in 2032: The annual ~$191M in nuclear production tax credit monetization provides meaningful cash flow but expires in 2032. This creates a revenue cliff seven years out that will need to be replaced through other sources (Amazon ramp, acquisitions, power price increases). Market may eventually discount future earnings for this known negative catalyst.

-

🎢 Options positioning highly concentrated at $370-$380: The gamma exposure data shows MASSIVE concentration at $370 resistance (2.38B gamma) and $380 strike (1.38B gamma). This creates potential for violent moves in EITHER direction: breakthrough above $370 could trigger gamma squeeze to $380-390, but failure to break out could result in quick reversal to $350 support. The heavy call positioning also means if TLN disappoints, market makers unhedging short calls amplifies downside.

-

⚠️ Year-end illiquidity creates gap risk: With December 19 Triple Witch (7 days away) and year-end holidays approaching, market liquidity typically thins significantly in final two weeks of December. This creates potential for exaggerated moves on light volume - both upside gaps on positive news and downside gaps on negative headlines. Wide bid-ask spreads during low liquidity can also make option position management difficult.

🎯 The Bottom Line

Real talk: A sophisticated institutional trader just spent $16.5 MILLION repositioning their TLN options from $420 March calls (already profitable) into near-term $380 January calls. This isn't taking money off the table - this is DOUBLING DOWN with better positioning for an imminent move higher.

What this trade tells us:

- 🎯 Smart money expects TLN to move significantly within the next 35 days (January expiration), not 3 months

- 💰 They're willing to sacrifice 63 days of extra time value to get better strike positioning at $380 vs $420

- ⚡ The timing suggests they're positioning for a SPECIFIC catalyst - most likely the $3.5B acquisition closing this month

- 📊 Rolling from $420 to $380 (bringing strike $40 closer) dramatically increases delta/leverage to capture near-term moves

- 🚀 This is a CONVICTION trade - you don't spend $7.5M on 35-day options unless you see something big coming

The setup is compelling:

- ✅ Stock consolidated from $390 to $354 (9.85% pullback) - healthy profit-taking complete

- ✅ Now sitting just below $370 resistance with clear path to $380-390 implied move range

- ✅ Immediate catalyst: $3.5B acquisition closing expected this month (Q4 2025)

- ✅ Gamma structure overwhelmingly bullish (7.52B call vs 3.31B put exposure)

- ✅ Strong support at $350 (1.66B gamma) limits downside risk to 2.5%

- ✅ Multiple positive catalysts converging: acquisition close, year-end positioning, buyback execution, earnings setup

This is a "weight of evidence" bullish setup - but with 35-day options, timing is EVERYTHING.

If you own TLN stock:

- ✅ HOLD with conviction - you're positioned for the bull case ($380-400 by January)

- 📊 Consider selling some covered calls at $390-400 strikes to generate income while maintaining most upside

- 🛡️ Set mental stop at $350 support (major gamma level) to protect if thesis breaks

- ⏰ Key dates to watch: Acquisition closing announcement (likely mid-late December), Dec 19 Triple Witch, Jan 16 expiration

- 🎯 If stock breaks above $370, consider adding to position or letting winners run to $380-390 targets

If you're watching from sidelines:

- 🎯 Best entry: Current levels ($359) offer good risk/reward - only 2.5% to support, 6-11% to targets

- ⏰ Timing matters: Acquisition catalyst expected THIS MONTH - don't wait too long or you'll miss the move

- 🛡️ Risk management: Any close below $350 invalidates the bullish setup - exit quickly if support breaks

- 💡 Position structure: For aggressive traders, consider bull call spreads ($370/$390) to define risk while maintaining leverage

- 📈 Conservative approach: Buy stock + protective $350 put (limit downside, unlimited upside)

If you're bearish:

- ⏰ Wait for clear breakdown below $350 before initiating shorts - fighting this setup is dangerous

- 📊 $350 support is CRITICAL - break below triggers cascade risk to $340, then $320

- ⚠️ Be aware the gamma structure (2.3:1 call/put ratio) works AGAINST short positions if stock rallies

- 🎯 If acquisition closes successfully and stock breaks to new highs above $390, cover immediately

Mark your calendar - Key dates:

- 📅 December 19 (Thursday) - Quarterly Triple Witch expiration (±6.77% implied move window)

- 📅 Mid-Late December - Expected announcement of Freedom & Guernsey acquisition closing (Q4 2025 target)

- 📅 January 16, 2026 (Friday) - Monthly OPEX, expiration of this $7.5M call trade

- 📅 Late February 2026 - Full-year 2024 earnings report (historical timing pattern)

- 📅 Spring 2026 - Transmission reconfiguration during Susquehanna refueling outage

Final verdict: Talen Energy's positioning at the intersection of nuclear power and AI data center demand is truly unique. The $18 billion Amazon partnership, record PJM capacity pricing, $3.5B accretive acquisitions, and $2B buyback program create a powerful multi-year growth story. But the $16.5M options roll today isn't about the multi-year thesis - it's about the NEXT 35 DAYS.

The message is clear: Smart money sees something big coming SOON. The acquisition closing this month could be the catalyst that breaks TLN above $370 resistance and propels it toward $380-400.

The setup is there. The catalysts are imminent. The unusual activity is screaming. Time to pay attention. ⚡

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. The Z-scores (6.81 and 10.31) reflect statistical unusual activity but do not guarantee profitability. The institutional trader may have complex portfolio hedging needs, information advantages, or risk tolerances not applicable to retail traders. Past performance doesn't guarantee future results. Binary catalysts (acquisition closing, regulatory decisions) create significant volatility risk. Always do your own research and consider consulting a licensed financial advisor before trading. Options can expire worthless, resulting in 100% loss of premium.

About Talen Energy: Talen Energy Corporation is an independent power producer and energy infrastructure company operating approximately 10.7 gigawatts of generation capacity across the United States, with a market cap of $16.85 billion in the Electric Services industry. The company generates and distributes electricity through wholesale markets in the PJM and WECC regions, with strategic focus on carbon-free nuclear power for AI data center partnerships.