🚀 TSLA: MASSIVE $51.7M Call Roll - Whales Double Down with 73-Day Extension!

📅 January 6, 2026 | 🔥 Extreme Unusual Activity Detected

🎯 The Quick Take

Holy smokes! Someone just executed a $51.7 MILLION options roll on TSLA - closing their January 16 $450 calls (about to expire worthless) and rolling the entire position into March 20 $440 calls. This isn't taking profits - this is doubling down with a fresh $36.3M net bet that TSLA will rally before Q1 delivery numbers drop. With the stock at $435, someone just bought themselves 73 more days and lowered their strike to a more realistic target. This is one of the largest single-day TSLA option trades we've tracked!

💰 The Option Flow Breakdown

📊 What Just Happened

Here's the exact tape from this morning's session:

| Time | Symbol | Side | Strike | Exp | Type | Size | Premium | Option Price | Spot | Vol | OI | Strategy | Z-Score |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:54:19 | TSLA | ASK | $440 | 2026-03-20 | CALL | 12,011 | $44.0M | $36.55 | $435.19 | 13K | 3K | BUY TO OPEN | 62.1 |

| 10:54:19 | TSLA | BID | $450 | 2026-01-16 | CALL | 12,011 | $7.7M | $6.40 | $435.19 | 18K | 26K | SELL TO CLOSE | 4.21 |

🐋 Combined Premium: $51.7M | Net Cost to Roll: ~$36.3M

🤓 What This Actually Means

Let me break this down in plain English:

The Old Position (Being Closed):

- 12,011 contracts of Jan 16 $450 calls

- With TSLA at $435, these are $15 out of the money

- Only 10 days until expiration = basically dead money

- Collected $7.7M by closing this position

The New Position (Being Opened):

- 12,011 contracts of March 20 $440 calls

- Strike is only $5 above current price (more achievable target)

- 73 days until expiration (vs. 10 days before)

- Cost $44M to open = Net spend of $36.3M to roll

💡 Translation for us regular folks:

This trader isn't giving up - they're reloading! Instead of letting their January calls expire worthless in 10 days, they're paying $36.3M MORE to:

- ✅ Lower their strike from $450 to $440 (10% drop in breakeven)

- ✅ Buy 63 extra days of time value

- ✅ Capture Q1 delivery numbers (late January)

- ✅ Stay positioned for potential Robotaxi/FSD news

- ✅ Hold through Q4 earnings on January 28

The Z-Score of 62.1 on the new position? That's 555x the average trade size - this is institutional money making a massive bet, not retail fomo. This trader believes something big is coming in the next 2-3 months!

📈 Chart Check-Up

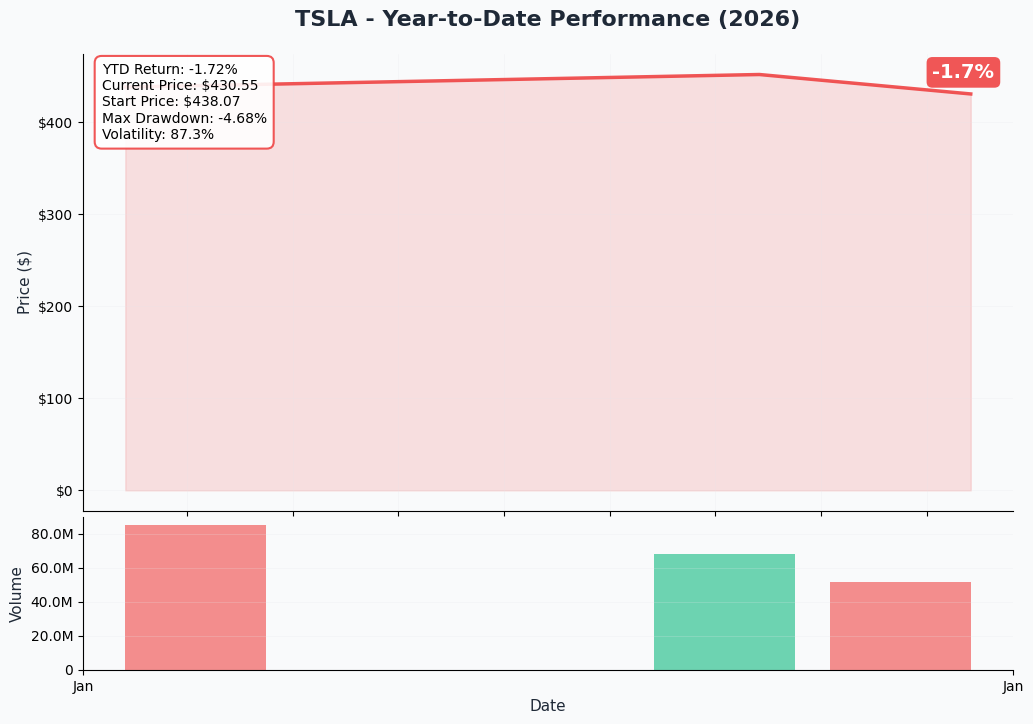

📊 YTD Performance Context

TSLA is trading at $435.19, sitting in a critical zone after pulling back from its recent high near $500. The stock is up roughly 6.57% year-over-year but has faced significant headwinds in 2025 including:

- Lost global EV crown to BYD (deliveries down 9%)

- Brand damage from Musk's DOGE involvement

- Margin compression from 28% (2022) to ~15.4% (2025)

But here's the thing - the options market is pricing in a major move ahead. That's why this whale is rolling forward rather than walking away!

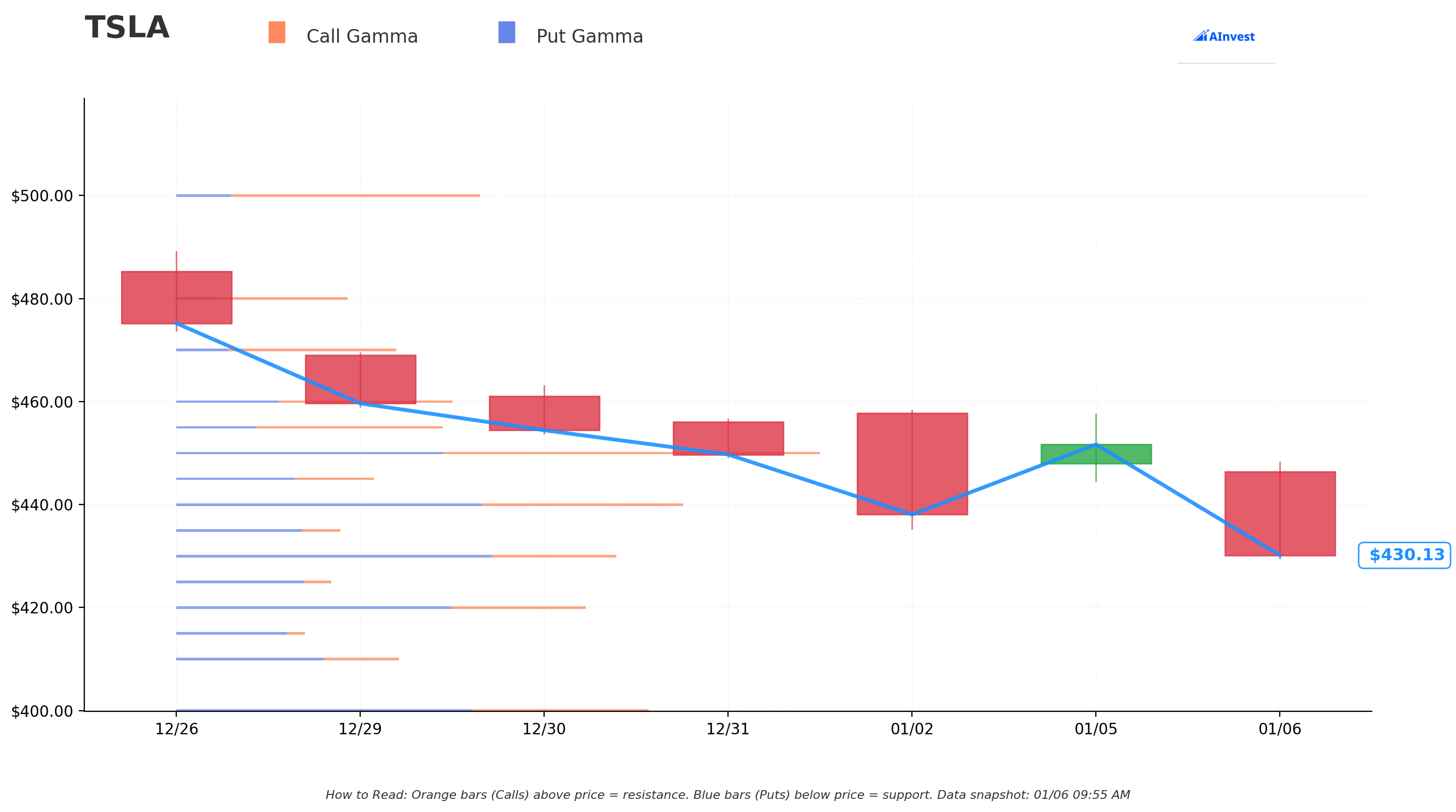

🛡️ Gamma-Based Support & Resistance Analysis

Here's what the gamma levels are screaming at us:

🔵 Support Levels (Put Gamma Below):

- $420.00 - 28.7B total gamma (first major floor)

- $410.00 - 15.7B total gamma (secondary support)

- $400.00 - 33.3B total gamma (MASSIVE psychological and gamma floor)

Current Price: $429.98 - Right between support and resistance!

🟠 Resistance Levels (Call Gamma Above):

- $430.00 - 31.1B total gamma (immediate ceiling)

- $440.00 - 35.7B total gamma (THE NEW STRIKE - this is the target!)

- $450.00 - 45.3B total gamma (old strike, MAJOR resistance)

- $500.00 - 21.4B total gamma (breakout level)

💡 What this means for traders:

The gamma profile shows net bullish bias with heavy call activity stacked above current price. The fact that our whale rolled from $450 to $440 is SMART - there's a massive gamma wall at $450 that would be tough to breach. But $440? That's achievable with one good catalyst. Notice how $400-$420 creates a "put wall" underneath, giving this trade a nice safety cushion.

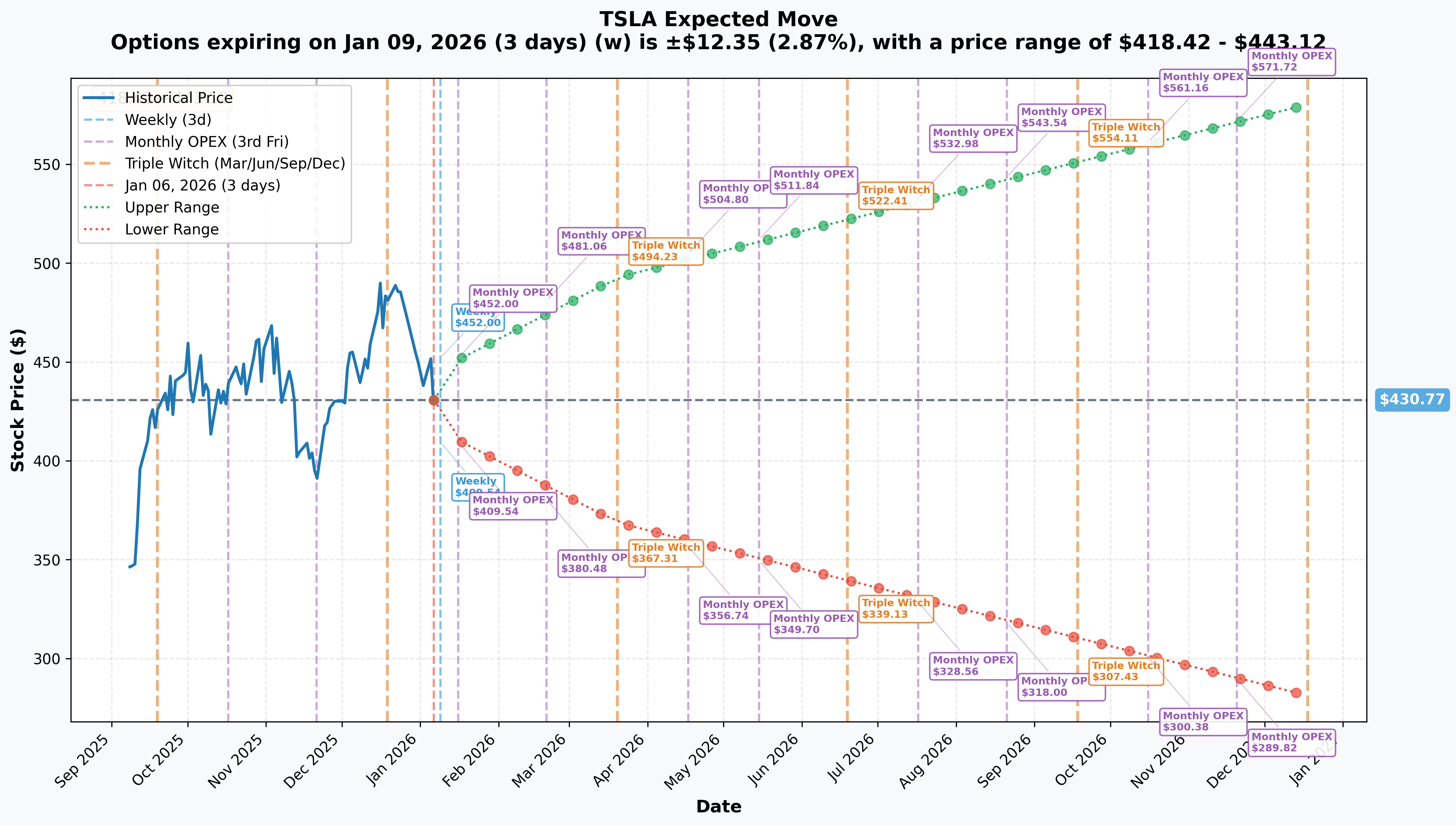

🎯 Implied Move Analysis

What the options market is pricing in:

Current Price: $430.77

-

Weekly (Jan 9): ±2.87% → Range: $418.42 - $443.12

- This suggests a quiet week ahead, staying inside the gamma bands

-

Monthly OPEX (Jan 16 - old expiration): ±4.78% → Range: $410.20 - $451.34

- The old position would need TSLA at $456.40 to breakeven ($450 strike + $6.40 paid)

- Market was only pricing 1% chance of that happening

-

Quarterly Triple Witch (Mar 20 - new expiration): ±14.43% → Range: $368.59 - $492.95

- The $440 strike sits comfortably in the middle of the expected range

- Breakeven is $476.55 ($440 + $36.55 paid)

- This gives TSLA room to run to $493 - plenty of runway!

🤔 Key Insight:

By rolling to March, this trader went from having a <1% probability of profit to having a much more realistic shot. The quarterly implied move suggests the market expects massive volatility into Q1 - and this whale is betting on the upside of that volatility!

🏢 Company Overview: What Does Tesla Do?

Tesla, Inc. (TSLA) | Market Cap: $1.44 Trillion

Sector: Motor Vehicles & Passenger Car Bodies

What They Do: Tesla is a vertically integrated electric vehicle manufacturer and real-world AI software developer. Beyond cars (luxury sedans, SUVs, light trucks, semi trucks), they operate a growing energy business (stationary batteries, solar panels, Supercharger network) and are expanding into robotaxis, humanoid robots (Optimus), and autonomous driving software (FSD).

The Numbers:

- 125,665 employees worldwide

- 1.64 million vehicles delivered in 2025 (down 9% YoY)

- Lost global EV crown to BYD for first time

- Energy storage business: 30%+ gross margins, 50%+ YoY growth

- Headquarters: Austin, Texas

🎪 Catalysts: What's Driving This Trade?

🔮 Upcoming Events (Why The Roll Makes Sense)

📊 Q4 2025 Earnings - January 28, 2026

- Just 22 days away - MAJOR catalyst!

- Consensus: $27-29B revenue, $0.46 EPS

- Key focus: Energy storage revenue (hit record 14.2 GWh in Q4), FSD progress, Cybercab timeline, 2026 delivery guidance

- Q4 deliveries disappointed (418,227 vs. 422,850+ expected), but energy segment crushing it

- Source: Tesla Investor Relations

🤖 Cybercab Production Start - April 2026

- Robotaxi production beginning at Giga Texas

- Seven Cybercab prototypes already testing in Austin

- Morgan Stanley expects ~1,000 vehicles in robotaxi fleet by end of 2026

- This could be a GAME-CHANGER if execution delivers

- Source: Eletric Vehicles - Cybercab Production Timeline

🇪🇺 FSD European Approval - Expected February 2026

- Tesla conducting demonstrations to Dutch regulators (RDW)

- Once Netherlands approves, other EU states can recognize immediately

- Would unlock massive new revenue stream

- Over 1 million kilometers of testing across 17 EU countries

- Source: Electrek - FSD Europe Timeline

🦾 Optimus V3 Production Prototype - February/March 2026

- Pilot production underway at Fremont Factory

- Target price: ~$20,000 per unit

- Targeting 50,000-100,000 units by year-end 2026

- Source: Tesla North - Optimus Ramp

⚡ Energy Storage Expansion

- Houston Megafactory: 50 GWh capacity coming online 2026

- Total capacity reaching ~133 GWh by 2026

- CFO expects at least 50% YoY growth continuing into 2026

- Already 13% of revenue but 23% of total profit (31.4% margins!)

- Source: AInvest - Energy Storage Growth

📉 Recent Events (Already Happened)

🏁 Q4 Deliveries Miss - January 2, 2026

- Delivered 418,227 vehicles vs. 422,850-434,487 consensus

- Full year 2025: 1.64M vehicles (-9% YoY)

- BYD overtakes Tesla as #1 global EV seller (2.26M units)

- Energy storage hit record 14.2 GWh (growth engine!)

- Source: CNBC - Q4 Delivery Report

💔 Brand Damage from Musk's DOGE Role

- Yale study: Musk's politics cost Tesla 1-1.26 million U.S. sales

- Tesla now least trusted EV brand in America (-13 net perception score)

- Musk stepped back from DOGE in April 2025 after acknowledging stock impact

- Source: Yale Insights - Political Impact

📉 Morgan Stanley Downgrade - December 2025

- Downgraded from Overweight to Equal Weight

- Price target: $425 (Bull: $860, Bear: $145)

- Added $60/share robotics value but cut auto volume expectations 10.5% for 2026

- Source: Yahoo Finance - Morgan Stanley Downgrade

✅ Q3 2025 Beat - October 22, 2025

- Revenue: $28.1B (+12% YoY) vs. $26.37B consensus

- Record FCF: $3.99B

- Energy segment: $3.42B revenue (+44% YoY), $1.1B gross profit

- Vehicle deliveries: 497,099 (record quarter, +7% YoY)

- Source: CNBC - Q3 Earnings

🎲 Price Targets & Probabilities

Let's use the gamma levels, implied moves, and catalyst calendar to map out realistic scenarios:

🚀 Bull Case - Target: $475-$500 (March 20 expiration) Probability: 30-35%

What needs to happen:

- ✅ Q4 earnings beat on January 28 with strong energy segment performance

- ✅ FSD gets European approval in February (major revenue unlock)

- ✅ Cybercab production starts on time in April with positive reception

- ✅ 2026 delivery guidance surprises to upside

- ✅ Market rotation back into growth/tech continues

Path to profit: Breakeven is $476.55 ($440 strike + $36.55 paid). A move to $485-$500 would deliver 2-3x returns on the calls. The quarterly implied move range extends to $492.95, so this isn't crazy. The $450 gamma wall would need to break, but with strong catalysts, that's doable.

Support from: Energy business momentum (31.4% margins, 50%+ growth), potential Robotaxi hype (Cybercab production starting April), FSD monetization acceleration

⚖️ Base Case - Target: $440-$460 (choppy range) Probability: 40-45%

What this looks like:

- Mixed Q4 earnings (weak auto, strong energy)

- FSD Europe gets delayed to late Q1

- Cybercab production starts but with limited initial scale

- Stock trades between $440 gamma resistance and $450 ceiling

- No major breakthrough, no major disaster

Path to breakeven: Calls would be worth $0-$20 at expiration depending on where in range. Would likely need to manage position actively, potentially rolling again or taking small loss/small gain.

😰 Bear Case - Target: $380-$410 (test support) Probability: 25-30%

What could go wrong:

- ❌ Q4 earnings disappoint with weak 2026 guidance

- ❌ FSD Europe approval gets rejected or pushed to late 2026

- ❌ Cybercab production delays or regulatory issues

- ❌ Further market share losses to BYD/Chinese competitors

- ❌ Margin compression continues (automotive gross margins fall below 15%)

- ❌ Broader market correction hits high-multiple growth stocks

Path to loss: Calls expire worthless if TSLA trades below $440 at March expiration. The $410-$420 gamma support zone would likely hold absent major negative catalyst. At $400-$410, this would be a total loss scenario for the whale.

Risk factors: BYD now #1 globally, brand trust at all-time low, 206x forward P/E vs. 10.65x industry average, regulatory challenges

💡 Trading Ideas

🛡️ Conservative - "The Energy Storage Believer"

Strategy: Bull put spread (sell $410 put / buy $400 put) expiring March 21 Cost: Collect ~$3.00 credit per spread Max Profit: $300 per spread Max Loss: $700 per spread Breakeven: $407

Why this works: You're betting TSLA stays above $410 (the gamma support floor) through March. Even if the auto business struggles, the energy storage momentum (14.2 GWh deployed in Q4) should keep the stock from collapsing. The $400-$420 zone has massive put gamma support.

Probability of success: ~65-70%

⚖️ Balanced - "The Earnings Straddle"

Strategy: Calendar spread - Buy March 20 $440 call, Sell Jan 30 $440 call (right after earnings) Cost: ~$28 net debit Max Profit: $10-15 if volatility expands post-earnings and stock stays near $440 Max Loss: $28 if stock moves far from $440 by Jan 30

Why this works: You're playing the volatility crush after earnings while maintaining exposure to the March catalysts (FSD Europe, Cybercab). If earnings causes a big move up or down, you take a loss on the short Jan call but keep your March exposure. If stock stays range-bound near $440, you profit from the theta decay differential.

Probability of success: ~50-55%

🚀 Aggressive - "The Whale Follower"

Strategy: Buy March 20 $440 calls (same strike as the whale) Cost: $36.55 per contract ($3,655 per contract) Breakeven: $476.55 Profit Potential: Unlimited above $477; 2x at $513, 3x at $550

Why this works: You're literally following a $44M institutional bet. This trader clearly has conviction about multiple March catalysts aligning. With 73 days of time value, you can sell on any spike toward $460-$480 without holding to expiration.

Risk Management:

- Don't deploy more than 3-5% of your options portfolio

- Set a stop loss at 50% (sell if calls drop to $18)

- Consider taking profits at 50-75% gain rather than swinging for home run

- Watch for roll signals if whale exits early

Probability of success: ~30-35% (but asymmetric upside if it works)

⚠️ Risk Factors

Let's be real - there's a lot that could go wrong here:

🔴 Valuation Risk: 206x forward P/E vs. 10.65x industry average. TSLA trades like a tech stock, not an auto manufacturer. If the AI/robotaxi narrative cracks, the multiple could collapse fast. Source: Artificall - Tesla Valuation Analysis

🔴 Execution Risk: Tesla has a history of missed timelines. Optimus production was supposed to hit 5,000 units by end of 2025 - they made "hundreds." Cybercab production starting April without guaranteed regulatory approval is risky. Source: Mike Kalil - Optimus Delays

🔴 Competitive Pressure: BYD just overtook Tesla globally with 28% YoY growth while TSLA shrunk 9%. Chinese EV makers (Geely, Leapmotor, Xiaomi) are flooding the market with cheaper alternatives. Tesla's automotive gross margins have compressed from 28% (2022) to ~15.4% (2025). Source: CNBC - BYD Overtakes Tesla

🔴 Brand Damage: Yale study found Musk's DOGE involvement cost 1-1.26 million U.S. sales. Tesla is now the least trusted EV brand in America with only 26% positive perception. This is hard to reverse quickly. Source: Yale Insights - Brand Impact

🔴 Regulatory Uncertainty: FSD is still Level 2 ADAS requiring human supervision. European approval is NOT guaranteed - Dutch regulator (RDW) has not committed to February timeline. Cybercab can't operate at scale without unsupervised FSD approval. Source: Teslarati - FSD Europe Uncertainty

🔴 Macro Headwinds: EV tax credit expired September 30, 2025 (pull-forward effect hurt Q4). Trade tensions with 25% tariffs on cars/parts. European markets cut EV subsidies (Germany ended subsidies, sales fell 41%). Source: Electrek - Q4 Delivery Analysis

🔴 Implied Volatility Risk: Options are expensive right now (IV elevated ahead of earnings). If IV crushes post-earnings and stock doesn't move, these calls will bleed theta fast.

🎯 The Bottom Line

Real talk: This is one of the most interesting TSLA trades I've seen in months - not because someone's making a huge bet (institutions do that daily), but because they're doubling down after being wrong.

Here's what this whale is telling us:

They had January $450 calls that were dead (10 days left, $15 OTM). Instead of walking away, they paid $36.3M MORE to roll into March $440 calls. That's not stubbornness - that's conviction.

What they see coming:

- 📊 Q4 earnings on Jan 28 could surprise on energy storage strength

- 🇪🇺 FSD Europe approval in Feb would be a $5-10B revenue unlock

- 🤖 Cybercab production start in April = proof of concept

- 🦾 Optimus V3 reveal in Feb/Mar = AI/robotics narrative boost

- ⚡ Energy storage business hitting inflection point (50%+ growth, 31% margins)

What they're worried about:

- Stock sitting at $435 vs. $440 strike = needs 1.1% move just to be ITM

- Breakeven of $476.55 = needs 9.5% rally

- Q4 delivery miss already known (priced in?)

- BYD competition intensifying

- Brand damage takes time to repair

My take for three types of traders:

If you own TSLA stock: This roll suggests institutional money believes in the March catalysts. Consider holding through earnings on Jan 28. Set stops at $410 (gamma support floor). Upside targets: $460 short-term, $485-500 if catalysts hit.

If you're watching TSLA: Wait for earnings on Jan 28. If they guide strong for 2026 and energy storage momentum continues, that's your entry signal. The $420-430 zone offers good risk/reward with $400 as ultimate support.

If you're bearish: This trade could be institutional capitulation (averaging down a losing bet). The 206x P/E is insane for a company losing market share to BYD. Wait for breakdown below $420, then target $390-400. But respect the $400 gamma floor - that's where put buyers will defend.

Mark your calendars:

- 📅 January 28: Q4 earnings - Make or break moment

- 📅 February: FSD Europe decision - Watch for announcement

- 📅 April: Cybercab production start - Proof of execution

- 📅 March 20: Options expiration - Judgment day for our whale

One final thought: The implied move of ±14.43% by March suggests the market expects FIREWORKS. This whale is betting on the upside of that volatility. The question is - are they smart money following a catalyst roadmap we can't see, or are they catching a falling knife?

At $36.3M to roll this position, they clearly believe the former. 🎯

⚖️ Disclaimer

Options trading involves substantial risk of loss and is not suitable for all investors. The analysis above is for informational and educational purposes only and should not be considered financial advice. Past performance does not guarantee future results. Always conduct your own research and consider consulting with a licensed financial advisor before making investment decisions.

The unusual options activity described represents the actions of individual market participants and may not reflect broader market sentiment or future price movements. Options can expire worthless, resulting in a total loss of premium paid. Trade sizes and strategies mentioned are for illustrative purposes and may not be appropriate for your personal financial situation or risk tolerance.