TSLA $198M Put Sale - Institutional Conviction on Long-Term Autonomous Future

January 12, 2026 | Unusual Activity Detected

The Quick Take

Someone just collected $198 MILLION in premium by selling long-dated puts on TSLA at two strike levels - $520 (Dec 2028) and $450 (Jan 2028). This is a massively bullish LEAPS positioning where a sophisticated trader is betting Tesla stays above these strikes over the next 2-3 years. The $520 strike trades 15% above current price ($450.77), while $450 sits right at current levels - both representing institutional confidence in Tesla's autonomous driving transformation. With multiple trades classified as EXTREMELY_UNUSUAL (Z-score up to 8.61) and Q4 earnings on January 28, 2026, this whale is collecting substantial premium while expressing long-term conviction in Cybercab, robotaxi expansion, and FSD commercialization.

Company Overview

Tesla, Inc. (TSLA) is the world's leading electric vehicle manufacturer transforming into an AI and robotics company:

- Market Cap: $1.51 Trillion (as of January 12, 2026)1

- Industry: Electric Vehicles / Autonomous Technology

- Sector: Consumer Discretionary / Technology

- Current Price: $450.77

- P/E Ratio: ~314x forward earnings1

- Primary Business: Tesla designs, manufactures, and sells electric vehicles (Model S/3/X/Y, Cybertruck), energy storage systems (Megapack, Powerwall), and is developing autonomous driving technology (FSD) and humanoid robots (Optimus). The company operates four Gigafactories globally and is expanding into robotaxi services with the upcoming Cybercab.

The Option Flow Breakdown

The Tape (January 12, 2026 @ 11:45:15):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Strategy |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:45:15 | TSLA | MID | SELL | PUT $520 | 2028-12-15 | $75M | $520 | 8,200 | - | 820K | $450.77 | $91.46 | Short Put |

| 11:45:15 | TSLA | MID | SELL | PUT $450 | 2028-01-21 | $48M | $450 | 8,200 | 10K | 820K | $450.77 | $58.54 | Short Put |

| 11:45:15 | TSLA | MID | SELL | PUT $520 | 2028-12-15 | $15M | $520 | 1,600 | - | 160K | $450.77 | $93.75 | Short Put |

| 11:45:15 | TSLA | MID | SELL | PUT $520 | 2028-12-15 | $15M | $520 | 3,300 | - | 330K | $450.77 | $45.45 | Short Put |

| 11:45:15 | TSLA | MID | SELL | PUT $520 | 2028-12-15 | $15M | $520 | 815 | - | 81.5K | $450.77 | $184.05 | Short Put |

| 11:45:15 | TSLA | MID | SELL | PUT $520 | 2028-12-15 | $15M | $520 | 2,400 | - | 240K | $450.77 | $62.50 | Short Put |

| 11:45:15 | TSLA | MID | SELL | PUT $520 | 2028-12-15 | $15M | $520 | 4,100 | - | 410K | $450.77 | $36.59 | Short Put |

| 11:45:15 | TSLA | MID | SELL | PUT $450 | 2028-01-21 | $9.7M | $450 | 1,600 | 10K | 160K | $450.77 | $60.63 | Short Put |

| 11:45:15 | TSLA | MID | SELL | PUT $450 | 2028-01-21 | $9.7M | $450 | 3,300 | 10K | 330K | $450.77 | $29.39 | Short Put |

| 11:45:15 | TSLA | MID | SELL | PUT $450 | 2028-01-21 | $9.7M | $450 | 2,500 | 10K | 250K | $450.77 | $38.80 | Short Put |

| 11:45:15 | TSLA | MID | SELL | PUT $450 | 2028-01-21 | $9.7M | $450 | 4,100 | 10K | 410K | $450.77 | $23.66 | Short Put |

What This Actually Means

This is a two-tier bullish short put campaign - someone is SELLING puts at two strike levels for substantial premium. Here's the breakdown:

$520 Strike Puts (Dec 2028 Expiration):

- Premium collected: ~$135M across multiple tranches

- Strike positioned: 15% ABOVE current price of $450.77 - aggressive bullishness

- Time horizon: ~1,069 days until December 2028 expiration - ultra long-term strategic bet

- Contract volume: 20,415 contracts total represents ~2.04M shares worth ~$920M at current prices

$450 Strike Puts (Jan 2028 Expiration):

- Premium collected: ~$77M across multiple tranches (excluding 820 contract closing trade)

- Strike positioned: Right at current price - at-the-money positioning

- Time horizon: ~740 days until January 2028 expiration

- Contract volume: 19,700+ contracts represents ~1.97M shares worth ~$888M at current prices

- Z-Score: Up to 8.61 (EXTREMELY_UNUSUAL) - this activity is statistically rare

What's really happening here:

This trader is running the "sell puts, keep premium" strategy at institutional scale across two expiration dates. By selling $520 strike puts expiring December 2028 and $450 strike puts expiring January 2028, they collect $198M TODAY. As long as TSLA stays above these strikes at expiration, they keep the entire premium with zero obligation. Think of it like being an insurance company - they're selling "crash protection" to nervous traders, confident the crash won't materialize over 2-3 years.

If TSLA drops below the strikes at expiration: They'd be obligated to buy shares at the strike price. For the $520 puts, the premium collected provides significant downside cushion. For the $450 puts, the premium creates an effective cost basis well below $400 per share.

The bullish thesis: This position only makes sense if they believe Tesla will trade significantly higher than $520 over the next 3 years, driven by Cybercab production starting April 2026, robotaxi expansion to multiple cities, FSD reaching unsupervised capability, and continued energy storage growth (+84% YoY)2.

Unusual Score: EXTREMELY UNUSUAL (8.61x Z-score on lead $450 trade) - This is massive institutional positioning that happens rarely. The multiple tranches executed simultaneously suggest a coordinated institutional allocation, potentially from a fund accumulating exposure or a sophisticated premium-selling strategy.

Technical Setup / Chart Check-Up

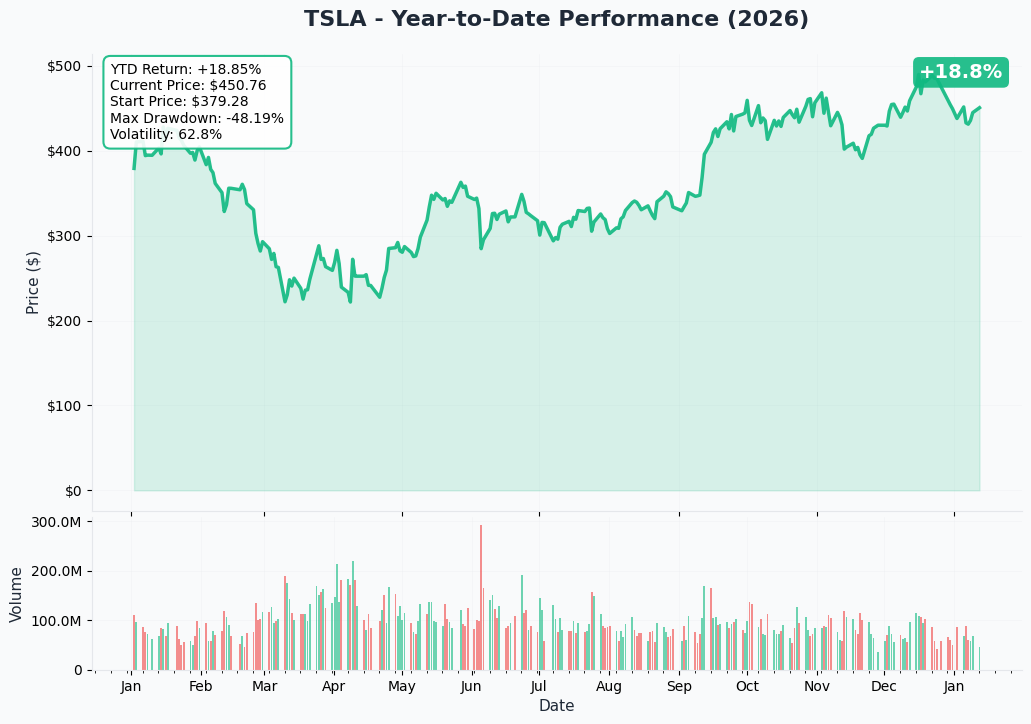

YTD Performance Chart

TSLA has been volatile - after hitting a 52-week high of $498.83 on December 16, 2025, the stock has pulled back ~10% to current levels around $450. The stock gained substantially from its 52-week low of $214.25, more than doubling as investors priced in the robotaxi opportunity and autonomous driving potential despite two consecutive years of delivery declines.

Key observations:

- 52-Week Range: $214.25 - $498.83 (currently trading mid-range)

- Recent pullback: Down ~10% from December 2025 highs, creating consolidation pattern

- Strong 2025 recovery: Stock recovered from mid-year 45% plunge to finish near highs3

- Support holding: Currently consolidating above $445-450 gamma support zone

- Earnings catalyst: Q4 2025 results on January 28, 2026 will set direction for next quarter

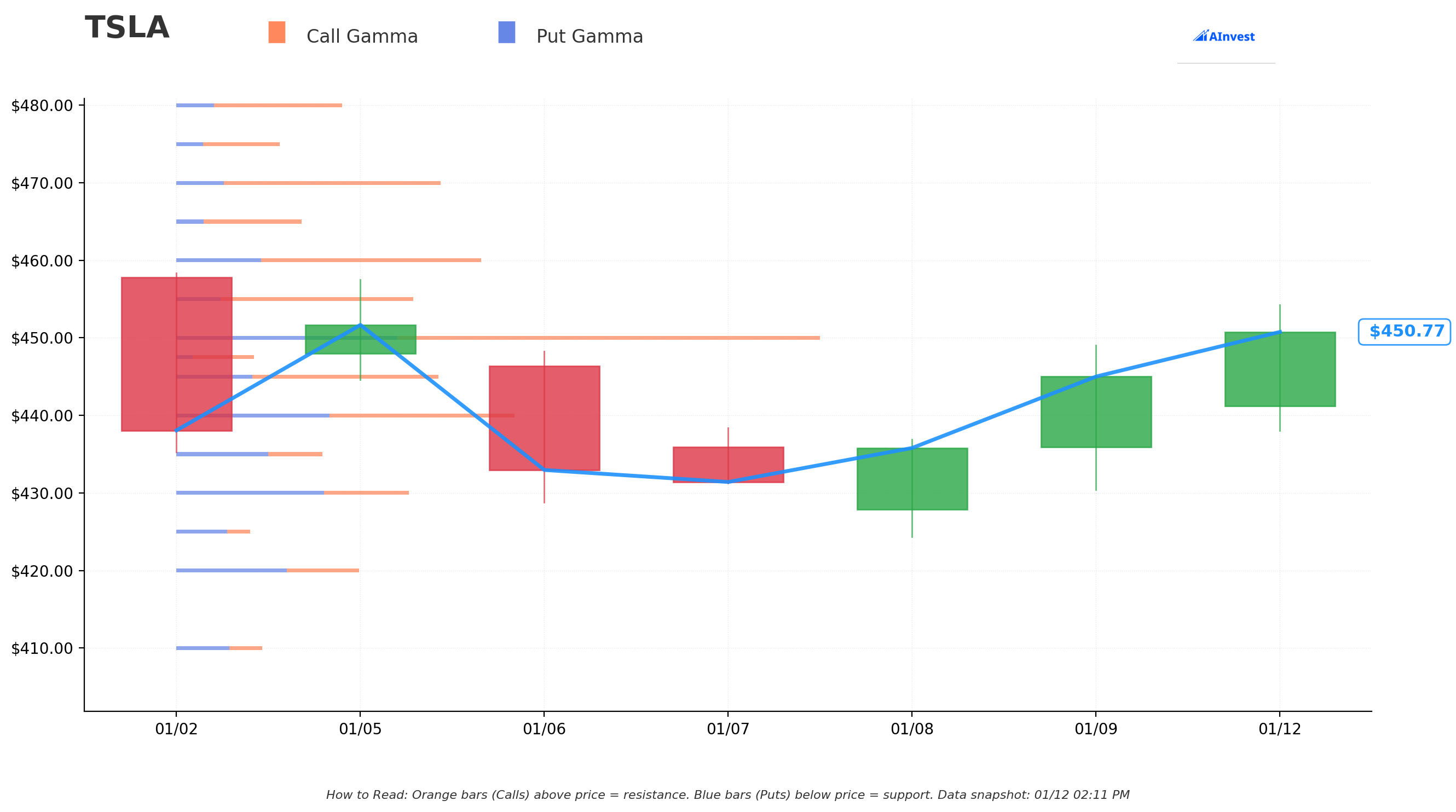

Gamma-Based Support & Resistance Analysis

Current Price: $450.77

The gamma exposure map reveals critical price magnets where options market activity creates natural support and resistance:

Support Levels (Put Gamma Below Price):

- $450 - Immediate support right at current price (strongest gamma concentration with 67.3 total GEX)

- $445 - Secondary support with solid put gamma wall (1.3% downside cushion)

- $440 - Tertiary support level (2.4% below current)

- $430 - Extended support if $440 breaks (4.6% downside)

- $420 - Major support floor (6.8% below current)

Resistance Levels (Call Gamma Above Price):

- $455 - Immediate resistance overhead (0.9% above current)

- $460 - Secondary resistance zone (2.0% above current price)

- $470 - Major resistance barrier (4.3% rally required to reach)

- $480 - Extended upside target (6.5% above current)

- $500 - Psychological resistance with significant call gamma (10.9% rally needed)

What this means for traders:

TSLA is consolidating right at $450, the strongest gamma support level. The options market is creating a tight "price prison" between $445-455 where dealers' hedging activity will dampen moves in either direction short-term. The Net GEX bias is Bullish (Total Call GEX: 400.4, Total Put GEX: 209.0), suggesting upside potential if a catalyst breaks the stock out of this range.

Notice the put seller's strategy? They struck at $520 for the longest-dated position - 15% above current price and well above all resistance levels shown on the gamma chart. They're betting TSLA breaks out of this consolidation range over the next 3 years and establishes a new trading range in the $500-600+ zone as autonomous driving revenue materializes.

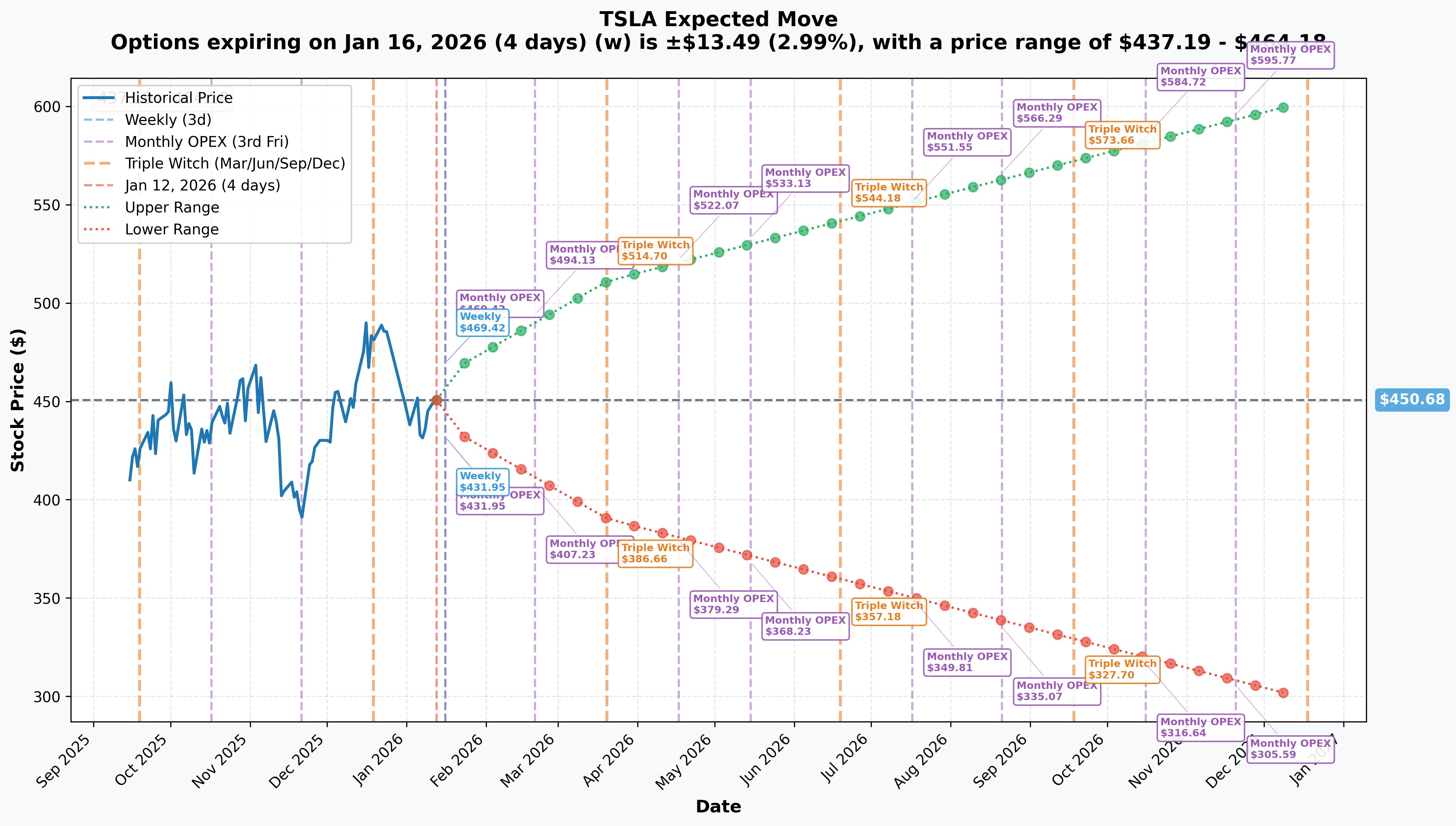

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 16 - 4 days): +/-$13.49 (+/-2.99%) -> Range: $437 - $464

- Monthly OPEX (Jan 16 - 4 days): +/-$13.49 (+/-2.99%) -> Range: $437 - $464

- Quarterly Triple Witch (Mar 20 - 67 days): +/-$60.67 (+/-13.46%) -> Range: $390 - $511

- Yearly LEAPS (Dec 18 - 340 days): +/-$152.13 (+/-33.76%) -> Range: $299 - $603

Translation for regular folks:

Options traders are pricing in a quiet 3% move ($13.49) through weekly OPEX, but the real uncertainty shows up in longer timeframes. The quarterly expiration shows a substantial 13.5% implied move, reflecting uncertainty around Q4 earnings (January 28), Cybercab production timeline, and robotaxi expansion updates.

The LEAPS expiration shows a massive 33.8% implied range ($299 - $603), meaning the market sees significant two-way risk over the next year. However, notice that both the put seller's strikes ($520 and $450) sit within this range. For the $520 strike, they're betting on the upper half of the distribution. For the $450 strike, they're betting the lower bound ($299) is unlikely - their premium provides substantial cushion above that level.

Key insight: The widening implied moves from 3% (weekly) to 34% (yearly) reflect massive uncertainty about autonomous driving commercialization, Cybercab production execution, and competitive dynamics with BYD and Chinese rivals. The put sellers are essentially betting they can predict the longer-term trend (up or stable) better than the market can price near-term volatility.

Catalysts

Immediate Catalysts (Next 30 Days)

Q4 2025 Earnings Report - January 28, 2026

TSLA reports fiscal Q4 2025 results on Wednesday, January 28, 2026 after market close. This is the critical catalyst that will either validate or challenge Tesla's valuation. Wall Street consensus and key expectations:

- Revenue: $23.33B consensus

- EPS: $0.44 consensus

- Energy Segment: Expect strong results after record 14.2 GWh Q4 deployments

- 2026 Delivery Guidance: Critical for sentiment given two consecutive years of declines

- Cybercab Production Update: Timeline confirmation for April 2026 start

Key metrics to watch:

- Gross margin trajectory (below 18% could concern investors)4

- FSD software revenue growth and deferred revenue recognition

- Energy segment profitability continuation (31.4% gross margins in Q3)5

- Robotaxi expansion timeline updates for Miami, Dallas, Phoenix, Las Vegas

- Model Y Juniper contribution to deliveries

Upside surprise potential: If Tesla reports strong FSD revenue recognition, confirms April Cybercab production on track, and provides confident 2026 delivery guidance above 1.8M vehicles, stock could gap back toward $480-500 resistance levels.

Downside risk factors: Any delays in Cybercab timeline, weak automotive margins, or conservative 2026 guidance citing competitive pressure from BYD6 could trigger another leg down toward $420-430 support.

Near-Term Catalysts (Q1-Q2 2026)

Cybercab Production Launch (April 2026)

Tesla's most anticipated catalyst for 2026:

- Location: Gigafactory Texas with new "Unboxed" manufacturing process

- Design: No steering wheel, no pedals - purpose-built robotaxi

- Manufacturing target: <10-second cycle time (revolutionary efficiency)

- Deployment: Will replace Model Y in Austin/Bay Area robotaxi fleet initially

- Significance: Validates Tesla's transition from EV manufacturer to autonomous transportation company

Why this matters: Cybercab production starting on schedule in April 2026 would de-risk the autonomous driving thesis significantly. The put sellers' 2028 expiration dates give them ample time to see multiple quarters of Cybercab production ramp and robotaxi revenue before their positions mature.

Robotaxi Geographic Expansion (Q1-Q2 2026)

Tesla's robotaxi service expansion roadmap:

- Current status: ~135 vehicles operating in Austin as of December 2025

- U.S. expansion: Miami, Dallas, Phoenix, Las Vegas announced

- Europe launch: May 2026 planned

- Vehicle transition: Cybercab to replace Model Y in fleet once production ramps

- Revenue model: Per-mile pricing competing with Uber/Lyft

Critical timing: Successful expansion to multiple U.S. cities in H1 2026 would validate Tesla's autonomous driving capability at scale and support premium valuations embedded in current stock price.

Tesla Semi Volume Production (Q1 2026)

Volume production launch details:

- Location: Giga Nevada (adjacent facility)

- Capacity target: 50,000 trucks annually once ramped

- Initial orders: ~100 trucks still owed to PepsiCo from 2017 order

- Significance: Opens commercial truck market opportunity

Medium-Term Catalysts (H2 2026 - 2027)

Progress toward fully autonomous operation:

- Current milestone: 7 billion cumulative miles driven, including 2.5 billion autonomous city miles

- Target: Musk stated 10 billion miles needed for safe unsupervised FSD

- Latest version: FSD v14.2.2.2 released December 28, 2025

- FSD v14.3: Described as "last big piece" of autonomy puzzle, expected Q1 2026

- International: South Korea launch achieved 1 million km in first month

Why the put sellers care: FSD achieving unsupervised capability within the 2026-2028 timeframe would fundamentally transform Tesla's valuation - robotaxi revenue could dwarf current automotive margins, justifying stock prices well above $520.

Optimus Robot Commercialization

Tesla's humanoid robot timeline:

- Optimus V3 prototype: Targeted for Q1 2026 unveiling

- Factory construction: Giga Texas building 10 million annual capacity by 2027

- Internal use: ~5,000 Optimus robots targeted for Tesla factories in 2025

- Price target: $20,000-$30,000 per unit at scale

- Skeptic view: Experts call project "fantasy thinking" - high execution risk

Energy Storage Business Growth

Tesla's most profitable segment continues to outperform:

- Q3 2025: $3.41B revenue with 31.4% gross margin

- Trailing 12 months: 43.5 GWh deployed (+84% YoY)

- Profit contribution: 23% of total profit despite only 12% of revenue

- Q4 2025: Record 14.2 GWh deployments

- Growth trajectory: Some analysts project energy could eclipse automotive profit by 2029

Risk Catalysts (Negative)

BYD Competitive Pressure Intensifies

BYD has overtaken Tesla as global EV leader:

- 2025 EV Sales: BYD 2.26M vs Tesla 1.64M

- Pricing advantage: BYD EVs priced $5,000-$20,000 below comparable Tesla models in Europe

- Growth trajectory: BYD exports up 150% while Tesla exports declining

- Chinese market: Tesla's first sales decline in China since 2020 (-5% YoY)

Why this matters: If Tesla continues losing market share to BYD and Chinese rivals, the autonomous driving thesis becomes the only support for current valuations. The put sellers are implicitly betting that robotaxi revenue will compensate for potential automotive share losses.

Brand Damage from CEO Political Activities

Quantified impact on Tesla demand:

- Yale study: Musk's politics cost Tesla 1-1.26 million U.S. sales

- SEC filing: Tesla acknowledged "political sentiment" may hurt company

- Q1 2025: Automotive revenue down 20% YoY during peak DOGE controversy

- Europe: Sales down 28% YTD through November 2025, lost market leadership

- Recovery uncertain: Musk stepped back from DOGE in May 2025, but brand damage persists

Valuation Stretched at 314x P/E

At current prices, Tesla trades at extreme multiples:

- P/E ratio: ~314x forward earnings

- Price to Sales: ~10x

- Market cap: 11x larger than Ford + General Motors combined

- Embedded expectations: Requires massive autonomous revenue to justify

- Analyst consensus: Average target $405.94 (current $450 implies 10% downside to consensus)

Put seller perspective: The elevated valuation is actually beneficial for this trade - high IV means they collected substantial premium. If valuation normalizes but fundamentals remain solid, stock could trade $350-450 range and puts still expire worthless or with minimal loss.

Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst analysis, here are the scenarios through the put expiration dates:

Bull Case (30% probability)

Target: $550-$700+ by 2028

How we get there:

- Cybercab production launches on schedule April 2026 and ramps smoothly

- Robotaxi expands to 10+ U.S. cities by end of 2026, 20+ by 2027

- FSD achieves unsupervised certification in key states/countries

- Robotaxi revenue reaches $5-10B annually by 2028

- Energy storage business grows to $25B+ revenue with 30%+ margins

- Optimus robot enters commercial production for external sales

- Tesla maintains EV share despite BYD competition through brand/technology

Put seller outcome: Massive win - collects full $198M premium, both put positions expire worthless, generates 40-50%+ annualized return on capital committed.

Base Case (45% probability)

Target: $400-$520 range (VOLATILE BUT SUPPORTED)

Most likely scenario:

- Cybercab production starts but ramps slower than expected

- Robotaxi expands to 3-5 cities, demonstrating capability but not scale

- FSD improves but unsupervised approval delayed to 2027-2028

- Automotive deliveries stabilize at 1.7-1.9M annually

- Energy storage continues strong growth, providing earnings support

- Valuation compresses from 314x toward 150-200x on 2027 estimates

- Stock trades $400-520 range with quarterly volatility around 15-20%

What happens to stock price: After Q4 earnings (Jan 28), stock moves 5-10% based on Cybercab timeline confirmation. Throughout 2026, trades $420-500 range with volatility around product launches and delivery reports. By late 2026/early 2027, establishes "fair value" range $450-520 as robotaxi revenue trajectory becomes visible but not transformational yet.

Put seller outcomes in Base Case:

- $520 puts (Dec 2028): Likely expire worthless or minimal value - full premium retained

- $450 puts (Jan 2028): At risk if stock trades below $450 at expiration, but premium provides cushion

Bear Case (25% probability)

Target: $280-$380 (PUTS THREATENED)

What could go wrong:

- Cybercab production delayed beyond Q2 2026 due to manufacturing challenges

- FSD regulatory approval blocked or significantly delayed

- Major robotaxi incident creates liability/regulatory concerns

- BYD and Chinese rivals accelerate global market share gains

- Brand damage proves lasting, U.S. market share erodes further

- Automotive margins compress to 10-12% from pricing pressure

- Valuation resets to 50-80x P/E, implying $250-350 price range

- Multiple negative catalysts align over 18-24 months

Put seller outcomes in Bear Case:

- Stock at $400 in Jan 2028: $450 puts worth $50, creates loss vs premium received depending on initial premium

- Stock at $350 in Jan 2028: $450 puts worth $100, significant loss on that position

- Stock at $400 in Dec 2028: $520 puts worth $120, loss depends on premium collected per contract

Why 25% probability: Requires multiple major failures over 2-3 years. Tesla's energy storage business provides earnings floor, robotaxi expansion is progressing (135 vehicles in Austin), and FSD data advantage (7 billion miles) is real. Complete failure of autonomous driving thesis unlikely given current progress, though timing risk remains elevated.

Trading Ideas

Conservative: Wait for Earnings Clarity, Then Reassess

Play: Stay in cash until after January 28 earnings, then evaluate entry points based on Cybercab timeline and 2026 guidance

Why this works:

- Catalyst imminent: Q4 earnings on Jan 28 (16 days away) is a binary event

- IV elevated: Implied volatility reflecting earnings uncertainty - better to wait for clarity

- Consolidation zone: Stock in $445-455 range with no urgency to chase

- Let the whale do the heavy lifting: The $198M put seller has 2-3 year conviction, but you don't need to match their risk horizon

Action plan after Jan 28 earnings:

- If earnings beat + Cybercab on track: Look for pullback to $440-450 support for stock entry

- If earnings in-line: Wait for $420-430 retest to enter

- If earnings disappoint: Let stock find bottom at $380-400 before evaluating

Risk level: Minimal (cash position preserves optionality) | Skill level: Beginner-friendly

Balanced: Mimic the Whale with Smaller Put Sales (After Earnings)

Play: After Jan 28 earnings, sell cash-secured puts at $400 or $420 strikes, collecting premium while expressing bullish bias

Why this works:

- IV crush post-earnings: Volatility will compress, but puts will still pay decent premium for 6-12 month expirations

- Strong gamma support: $450, $440, $430 are major support levels

- Copying institutional logic: Mimicking the whale's strategy at your scale

- Multiple ways to win: Keep premium if stock stays flat/up, or get assigned at attractive basis

Recommended structure (execute AFTER Jan 28 earnings):

- Expiration: June 2026 or September 2026

- Strike selection: $400 puts if conservative (11% below current), $420 if confident (7% below)

- Expected premium: ~$30-50 per contract depending on post-earnings IV

Risk level: Moderate | Skill level: Intermediate

Aggressive: Leveraged Bull Spread Betting on $500+ by End of 2026 (ADVANCED)

Play: Buy call spreads betting TSLA reclaims $500+ by December 2026

Structure: Buy $480 calls, Sell $550 calls, December 2026 expiration

Why this could work:

- Defined risk leverage: Spend $25-35 per spread to control $70 of upside

- Multiple catalysts: Captures earnings, Cybercab launch, robotaxi expansion over 11 months

- Asymmetric payoff: If bull case materializes, spread could return 100-150%

P&L scenarios at December 2026 expiration:

- TSLA at $550+: Spread worth $70, profit ~$35-45 per spread (100-130% ROI)

- TSLA at $500: Spread worth $20, profit ~$0 (breakeven)

- TSLA below $470: Spread worthless, lose entire debit (100% loss)

Risk level: HIGH | Skill level: Advanced only

Risk Factors

Don't get caught by these potential landmines:

-

Q4 earnings binary event (Jan 28): Results could gap stock 10-15% either direction. Gross margin below 18%, weak 2026 guidance, or Cybercab delays would trigger selling. Options pricing ~3% weekly move but actual volatility could exceed this given elevated expectations.

-

Cybercab execution risk: April 2026 production start is unproven timeline. "Unboxed" manufacturing process is untested at scale. Any delays would damage the autonomous driving thesis significantly.

-

FSD regulatory uncertainty: 10 billion miles needed per Musk for safe unsupervised FSD7 - currently at 7 billion. Regulatory approval timeline remains uncertain across jurisdictions. A major accident could set back approvals by years.

-

BYD competitive pressure: Tesla lost global EV crown to BYD in 20256 with 1.64M vs 2.26M deliveries. Chinese competitors iterating faster with aggressive pricing. Europe sales down 28% YTD.

-

Brand/political risk: Yale study found Musk's politics cost Tesla 1-1.26 million U.S. sales8. Tesla acknowledged in SEC filings that "political sentiment" may hurt the company9. Brand damage may prove lasting.

-

Extreme valuation at 314x P/E: Stock prices in near-perfect execution on autonomous driving. Any disappointment triggers multiple compression. Average analyst target of $405.94 implies 10% downside from current $450 levels10.

-

Nvidia autonomous driving competition: Nvidia announced autonomous driving system for personal vehicles at CES 20261 - TSLA dropped 5% on the news. Competition for autonomous software could intensify.

-

Institutional positioning unclear: While this $198M put sale is bullish, we don't have visibility into the seller's full portfolio. They might be hedging a massive long stock position or running complex multi-leg strategies. Don't blindly follow without understanding complete strategy.

The Bottom Line

Real talk: Someone just collected $198 MILLION selling long-dated puts on TSLA, expressing institutional-grade conviction that the stock stays above $450-520 over the next 2-3 years. This is not a short-term trade - this is a multi-year bet on Tesla's transformation from EV manufacturer to autonomous transportation company.

What this trade tells us:

- Long-term bull thesis: Sophisticated player believes Cybercab production, robotaxi expansion, FSD commercialization, and energy storage growth justify $450-520+ valuations through 2028

- Massive premium collection: $198M in immediate cash reflects elevated IV and 2-3 year time premium - they're getting paid handsomely for this conviction

- Tiered positioning: $520 strike (Dec 2028) for aggressive upside bet; $450 strike (Jan 2028) for at-the-money income generation

- Catalyst alignment: Both expirations capture all major catalysts (Q4 earnings Jan 28, Cybercab April 2026, robotaxi expansion 2026-2027, FSD improvements, energy storage growth)

- Willingness to own: If assigned, they're buying TSLA at effective cost basis well below $400 per share after accounting for premium received

This is NOT a "buy everything now" signal - it's a "2-3 year strategic positioning" signal that requires patience and risk management.

The institutional conviction here is notable: $198M in premium collection represents one of the largest single-day put selling campaigns on TSLA. The trader is betting that despite two consecutive years of delivery declines, loss of EV crown to BYD, 314x P/E valuation, and brand headwinds from Musk's political activities, Tesla's autonomous driving and energy storage businesses will support or grow the stock price over the next 2-3 years. They're collecting substantial premium for providing downside protection to nervous investors while expressing long-term confidence in the Cybercab, robotaxi, and FSD thesis.

The key question for you: Can you afford to wait 2-3 years for this thesis to play out? The whale clearly can commit $500M+ in capital (obligation to buy shares if assigned) and weather interim volatility. If you have that patience and risk tolerance, the pullback from $498 to $450 with Q4 earnings and Cybercab production ahead could be interesting. If you need shorter-term results, this trade may not suit your timeline.

Mark your calendar - Key dates:

- January 16, 2026 - Weekly/Monthly OPEX (3% implied move)

- January 28, 2026 - Q4 FY2025 earnings (THE catalyst for Q1 direction)

- March 20, 2026 - Quarterly triple witch (13.5% implied move window)

- April 2026 - Cybercab production launch at Giga Texas

- May 2026 - Europe robotaxi expansion planned

- H1 2026 - Tesla Semi volume production

- Q1 2026 - Optimus V3 prototype reveal

- January 21, 2028 - Expiration of $450 strike puts

- December 15, 2028 - Expiration of $520 strike puts

Final verdict: Tesla's 2-3 year setup is a genuine inflection point - either the Cybercab/robotaxi/FSD thesis materializes and justifies the $1.5T valuation, or the autonomous driving timeline continues to slip and the stock de-rates significantly. The $198M put seller is betting on the former scenario playing out over multiple years.

The energy storage business (+84% YoY, 31.4% margins) provides real earnings support511, robotaxi is operational in Austin with expansion announced12, and FSD has reached 7 billion miles7. These are not vaporware - they're progressing, albeit on uncertain timelines.

BUT - at 314x P/E with delivery declines, BYD competition intensifying, and brand challenges persisting, this is decidedly NOT a "buy blindly and hold" situation. The path to $520+ will include multiple 20-30% drawdowns. Q4 earnings on January 28 will provide the next major directional signal.

Be strategic. Be patient. Let earnings and Cybercab production provide clarity. The autonomous driving revolution will either materialize or it won't - and you'll know a lot more in 6-12 months than you do today.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Selling puts creates obligation to purchase stock at the strike price and requires sufficient capital to cover assignment. The Z-scores (up to 8.61) reflect statistical unusualness relative to recent TSLA activity - it does not imply the trades will be profitable or that you should follow them. Tesla's 314x P/E creates significant downside risk if autonomous driving thesis fails to materialize. Always do your own research and consider consulting a licensed financial advisor before trading. Q4 earnings on January 28 creates binary event risk.

About Tesla, Inc.: Tesla designs, manufactures, and sells electric vehicles, energy storage systems, and develops autonomous driving technology and humanoid robots. With a market cap of $1.51 trillion, Tesla is the world's most valuable automaker despite delivering fewer EVs than BYD in 2025.