:warning: TSLA Massive $8.2M Put Hedge - Smart Money Bracing for Volatility!

February 5, 2026 | Unusual Activity Detected

The Quick Take

Someone just dropped $8.2 MILLION on TSLA puts this morning! This monster trade bought 3,291 contracts of $400 strike puts expiring March 6th - a serious downside bet on a stock trading at $391.29 with Tesla navigating its most transformative period yet. With a Z-Score of 40.13 (EXTREMELY UNUSUAL), this is the kind of institutional positioning that happens only a few times a year. Translation: Big money is buying insurance ahead of major catalysts including Cybercab production launch in April and continued Robotaxi expansion!

Company Overview

Tesla, Inc. (TSLA) is the world's leading electric vehicle manufacturer and AI technology company, now pivoting aggressively into robotics and autonomous driving:

- Market Cap: $1.52 Trillion (8th-9th largest globally)

- Industry: Motor Vehicles and Passenger Car Bodies

- Current Price: $391.29 (near session lows)

- YTD Performance: -0.17% (essentially flat)

- Primary Business: Electric vehicles, autonomous driving software (FSD), energy storage (Megapack), humanoid robots (Optimus), and upcoming Robotaxi/Cybercab services

- Employees: 134,785 globally

- Headquarters: Austin, Texas

Tesla has lost its position as the world's largest EV maker to BYD after delivering 1.63 million vehicles in 2025 (down 8.6% YoY), but the company is doubling down on what CEO Elon Musk calls "Physical AI" - autonomous vehicles and humanoid robots.

The Option Flow Breakdown

The Tape (February 5, 2026 @ 10:18:46):

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:18:46 | TSLA | BUY | PUT | 2026-03-06 | $8.2M | $400 | 7,100 | 1,300 | 3,291 | $391.29 | $25.00 |

What This Actually Means

This is a directional bearish bet OR protective hedge on a substantial Tesla position! Here's the breakdown:

- Massive premium paid: $8.2M ($25.00 per contract x 3,291 contracts executed, 7,100 total volume)

- Slightly in-the-money: $400 strike is 2.2% ABOVE current price of $391.29 - puts already have intrinsic value

- Strategic timing: 29 days to expiration captures key period before Cybercab production launch in April

- Size matters: 7,100 contracts represents 710,000 shares worth ~$278M notional exposure

- Volume/OI ratio: 5.46x (HIGH_ACTIVITY signal) - significant new positioning vs existing open interest

What's really happening here: This trader is either: (A) Making a directional bearish bet that Tesla drops below $375 by March 6th, OR (B) Hedging a massive long stock/call position ahead of the Cybercab production announcement in April and other major catalysts. Given the premium paid and the timing (after Q4 earnings already released January 28th), this looks like sophisticated risk management ahead of execution risk on Tesla's AI/robotics pivot.

Strategy Detection: Long Put - This trade was classified as a standalone directional put purchase, not part of a spread or complex structure.

Unusual Score: EXTREMELY_UNUSUAL (Z-Score: 40.13) - This type of concentrated put buying happens only a handful of times per year. The trade is 40 standard deviations above average activity levels for this strike/expiration combination.

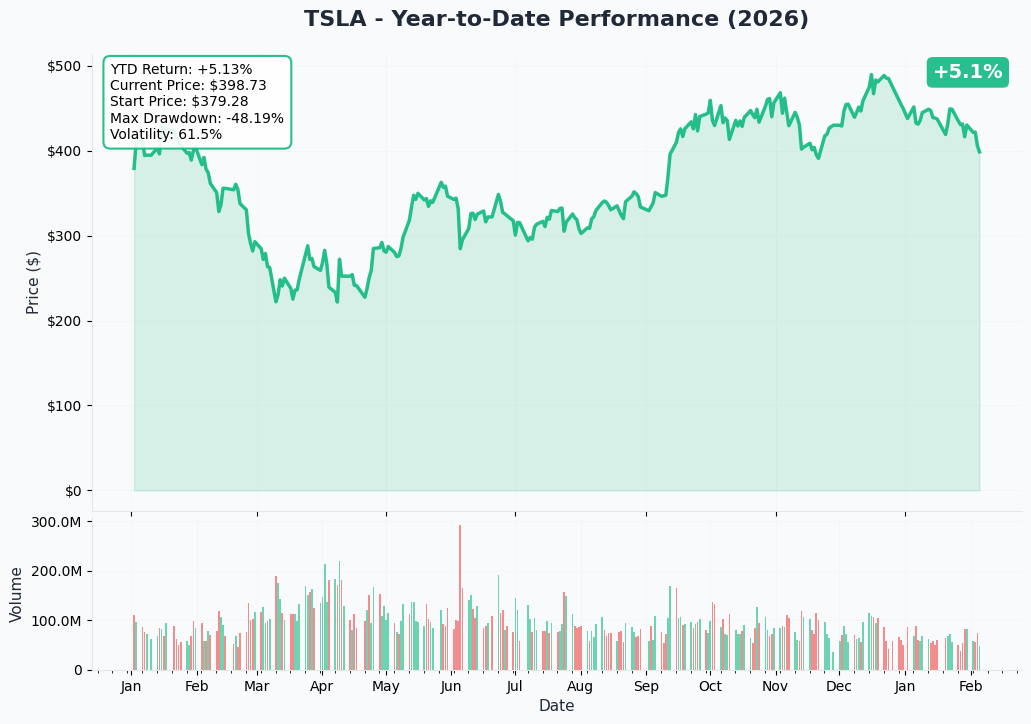

Technical Setup / Chart Check-Up

YTD Performance Chart

TSLA is essentially flat YTD at -0.17% with current price around $398-401. The chart tells a story of consolidation after the explosive 2024 rally:

Key observations:

- Range-bound trading: Stock oscillating between $350-475 over the past year

- Q4 earnings reaction: Mixed results on January 28th with revenue miss but EPS beat kept stock supported

- Volatility compression: Recent price action shows tightening range, setting up for next major move

- 52-week range: Approximately $250-$475, currently trading mid-range

- Critical inflection point: Stock needs to break above $420 resistance or below $380 support for directional clarity

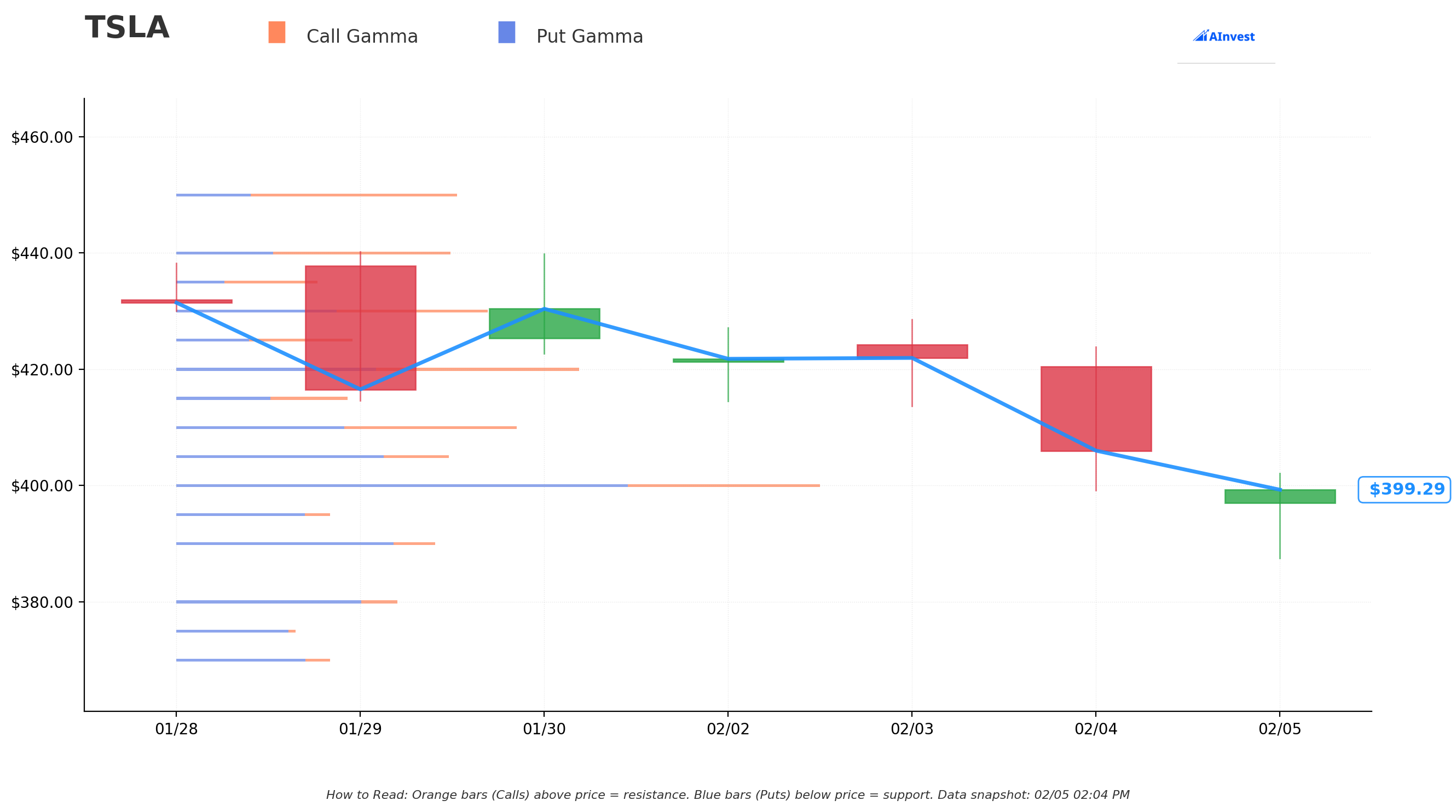

Gamma-Based Support & Resistance Analysis

Current Price: $398.84

The gamma exposure map reveals critical price levels that will govern near-term price action:

Support Levels (Put Gamma Below Price):

- $390 - Immediate support with -12.6B net gamma (strongest nearby floor!)

- $380 - Secondary support at -10.7B net gamma (dealers will buy dips aggressively here)

- $350 - Deep structural floor with -6.8B net gamma (major support zone if sell-off accelerates)

Resistance Levels (Call Gamma Above Price):

- $400 - MASSIVE resistance with 45.6B total gamma (STRONGEST LEVEL - dealers will sell into rallies)

- $405 - Secondary resistance at 19.0B total gamma

- $410 - Key ceiling with +0.27B net gamma (turning point from bearish to bullish gamma)

- $420 - Strong resistance at 27.9B total gamma

- $440 - Extended upside with +5.8B positive net gamma

- $450 - Major upside target at +9.2B positive net gamma

What this means for traders: TSLA is pinned just below the MASSIVE $400 gamma wall (45.6B total exposure - by far the largest level). This creates natural ceiling pressure as market makers hedge their positions. The Net GEX Bias is BEARISH (291B put gamma vs 251B call gamma), suggesting dealers are positioned for downside moves.

Notice the trade structure: The put buyer struck EXACTLY at $400 where there's maximum gamma resistance. They're betting that if TSLA can't break through $400, it will retreat to $390 or lower. Smart positioning right at the gamma wall.

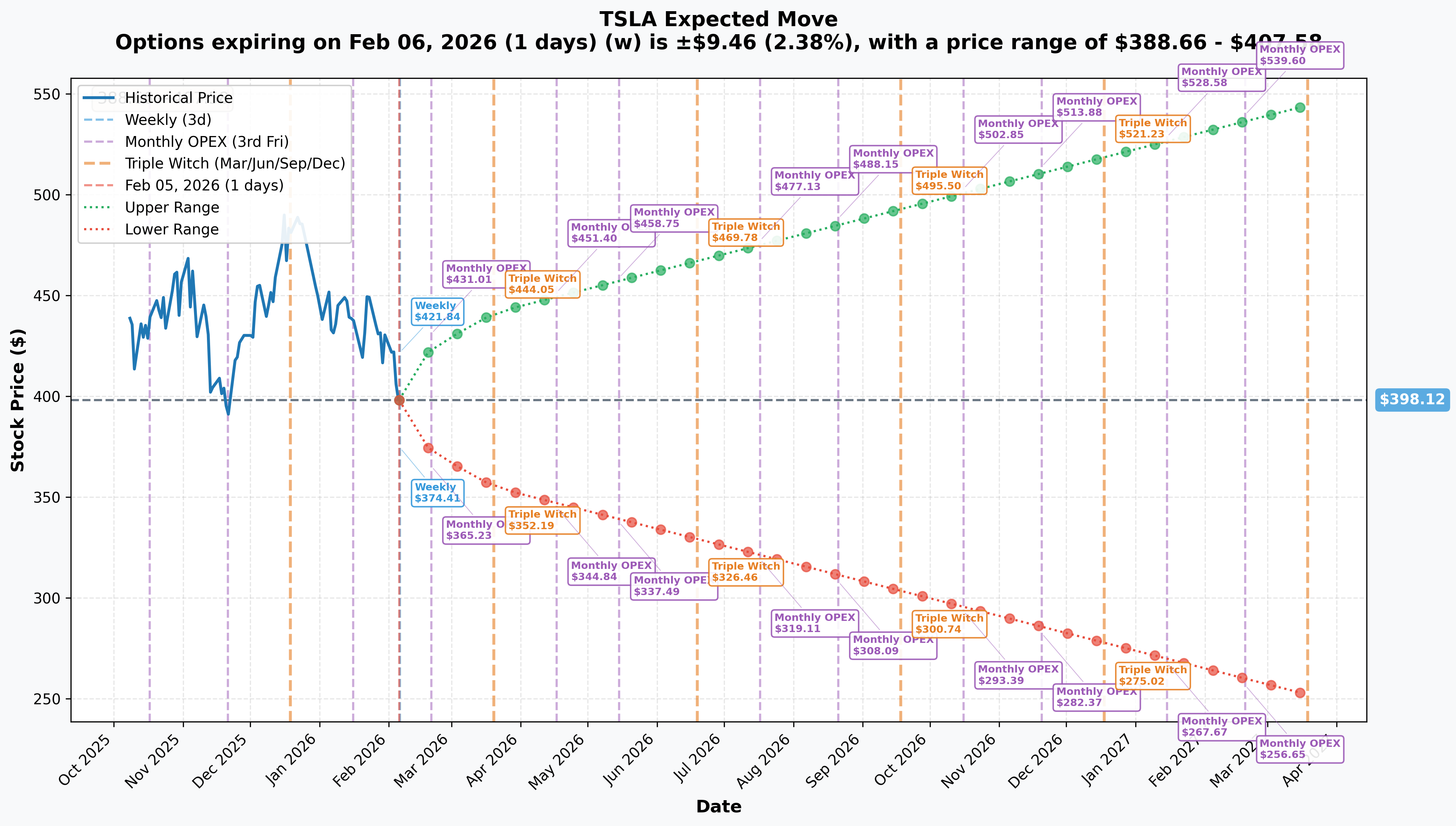

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Feb 6 - 1 day): +/-2.38% (+/-$9.46) | Range: $388.66 - $407.58

- Monthly OPEX (Feb 20 - 15 days): +/-6.55% (+/-$26.09) | Range: $372.03 - $424.22

- Triple Witch (Mar 20 - 43 days): +/-10.9% (+/-$43.39) | Range: $354.73 - $441.51

- LEAPS (Mar 19, 2027 - 407 days): +/-36.74% (+/-$146.28) | Range: $251.84 - $544.41

Translation for regular folks: Options traders are pricing in a 2.4% move ($9.50) by tomorrow for the weekly expiration, and a SUBSTANTIAL 6.5% move ($26) through February monthly OPEX. The market expects significant volatility over the next month as catalysts unfold.

The March 6th expiration (when this $8.2M trade expires) falls between monthly and quarterly OPEX, with implied move suggesting the lower range could reach $354-372. This aligns with the put buyer's thesis: if TSLA breaks below $390 support, it could quickly test $375-380.

Key insight: The put buyer paid $25 for slightly ITM puts - they need TSLA below $375 at expiration to profit, representing a ~4% decline from current levels. This is an aggressive but achievable target given the gamma structure and near-term catalysts.

Catalysts

Past Catalysts (Already Happened)

Q4 2025 Earnings Results - January 28, 2026

Tesla reported mixed Q4 results that beat on EPS but missed on revenue:

- Q4 Revenue: $24.901B (missed estimates) (source)

- Q4 GAAP EPS: $0.24 / Non-GAAP EPS: $0.50 (beat by 25%) (source)

- Q4 Deliveries: 418,227 vehicles (down 15.6% YoY, missed 440K consensus) (source)

- FY 2025 Total Deliveries: 1.63 million (down 8.6% YoY) (source)

- Energy Storage Record: 14.2 GWh deployed in Q4, 46.7 GWh for full year (source)

- CapEx 2026 Guidance: ~$20B (more than doubling from $8.6B in 2025) (source)

BYD Overtakes Tesla - January 2, 2026

Tesla officially lost its crown as the world's largest EV maker:

- BYD 2025 EV Sales: 2.26 million (+28% YoY)

- Tesla 2025 EV Sales: 1.63 million (-8.6% YoY)

- This marks Tesla's second consecutive year of declining annual deliveries

Robotaxi Austin Launch - January 22, 2026

Tesla launched robotaxi rides in Austin without human safety drivers. Musk announced at Davos that robotaxis will be "widespread" in the US by end of 2026.

SpaceX-xAI Merger - February 2, 2026

SpaceX acquired xAI in $1.25 trillion mega-merger. Notably, Tesla was NOT included in the merger despite having $2B invested in xAI. This creates questions about Musk's focus and resource allocation.

Model S/X Production End Announced - January 28, 2026

Tesla will discontinue Model S and Model X in Q2 2026, converting Fremont factory lines to produce Optimus robots at 1 million units/year capacity.

FSD Subscription-Only Transition - January 14, 2026

Tesla moves FSD to subscription-only model after February 14, 2026. Musk also admitted Tesla needs approximately 10 billion miles of data for "safe unsupervised self-driving" - moving the goalpost once again.

Upcoming Catalysts (Next 6 Months)

| Event | Date | Importance |

|---|---|---|

| FSD Sales End | February 14, 2026 | Medium |

| Cybercab Production Start | April 2026 | HIGH |

| Q1 2026 Earnings | April 28, 2026 | HIGH |

| Model S/X Production End | Q2 2026 | Medium |

| FSD v14 Lite for HW3 | Q2 2026 | Medium |

| Houston Megapack Factory | Late 2026 | Medium |

| Robotaxi "Widespread" US | End of 2026 (Musk claim) | HIGH |

Cybercab Production - April 2026

Cybercab production begins at Gigafactory Texas in April 2026 with target of 2 million units annually at full capacity. This is THE key execution catalyst for the autonomous driving thesis.

Robotaxi Expansion Plans

Current operations in Austin (unsupervised). Planned 2026 expansion to Miami, Dallas, Phoenix, Las Vegas. Regulatory approval remains the key bottleneck.

Q1 2026 Earnings - April 28, 2026 (source)

- Consensus Revenue: $23.24B

- Consensus EPS: $0.30

- Key metrics: Delivery numbers, Robotaxi updates, Optimus production ramp, energy deployments

Optimus Robot Mass Production

Tesla commenced Optimus Gen 3 mass production at Fremont with 1 million units/year capacity target. 2027 plans include Gen 4 production at Giga Texas with 4 million units/year capacity.

Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst analysis, here are the scenarios through March 6th expiration:

Bull Case (20% probability)

Target: $420-$450

How we get there:

- Robotaxi expansion announcements to new cities with strong early revenue metrics

- Cybercab production timeline confirmed on-track for April

- FSD v14 receives positive regulatory feedback in international markets

- Energy storage business continues record deployments

- Short squeeze as bearish positioning capitulates

- Breakout above $400 gamma wall triggers mechanical buying to $420-$440

Probability assessment: Only 20% because it requires multiple catalysts to align positively with massive $400 gamma resistance overhead. Stock needs sustained institutional buying to overcome dealer selling pressure.

Base Case (50% probability)

Target: $380-$410 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- Stock oscillates around major gamma levels ($390-$400)

- Robotaxi news flow positive but without dramatic expansion

- Market digests Q4 results and waits for Cybercab production proof

- FSD subscription transition completes without major disruption

- Volatility remains elevated but contained within range

- Put buyer's trade expires near break-even or small loss

This is the put buyer's hedging scenario: They're protecting against downside while maintaining long exposure. If stock stays $385-405, puts expire with modest intrinsic value but serve their purpose as insurance.

Bear Case (30% probability)

Target: $350-$380

What could go wrong:

- Cybercab production delays announced (Musk has history of missed timelines)

- Robotaxi regulatory setbacks (NHTSA investigations, state-level restrictions)

- BYD/Chinese EV competition intensifies, further market share loss

- Musk distraction concerns escalate (SpaceX-xAI merger, DOGE duties)

- Tariff impacts materialize on global supply chain

- Break below $390 gamma support triggers cascade to $380, then $350

- Broader tech selloff drags mega-caps lower

Critical support levels:

- $390: Immediate gamma floor (-12.6B net) - MUST HOLD

- $380: Secondary support (-10.7B net) - key psychological level

- $350: Deep support (-6.8B net) - disaster scenario

Probability assessment: 30% because execution risk on autonomous driving is real given Musk's track record on FSD timelines. The $20B capex increase increases cash burn risk, and political/regulatory headwinds from Musk's DOGE role create uncertainty.

Put P&L Scenarios:

- Stock at $350 on Mar 6: Puts worth $50.00, profit = $25.00/contract x 3,291 = $82.3M gain (1,000%+ ROI!)

- Stock at $375 on Mar 6: Puts worth $25.00, break-even

- Stock at $400 on Mar 6: Puts worth ~$0 (at-the-money), loss = -$25.00/contract = -$8.2M (100% loss)

- Stock at $420 on Mar 6: Puts expire worthless, total loss = -$8.2M

Trading Ideas

Conservative: Wait for Clarity

Play: Stay on sidelines until Cybercab production confirmation in April

Why this works:

- Current price sits right at $400 gamma wall - maximum uncertainty zone

- Multiple execution risks ahead: Cybercab timeline, FSD regulatory, Musk distraction

- Better entry likely at $350-$370 if bear case unfolds, or $420+ on confirmed breakout

- Analyst consensus is "Hold" with wide price target dispersion ($25-$600) - nobody knows

Action plan:

- Watch for Cybercab production updates in March/April

- Look for entry at $350-$370 gamma support if pullback occurs (15-20% margin of safety)

- Alternatively, wait for breakout above $420 resistance with volume confirmation

- Monitor unusual options activity for institutional positioning shifts

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Balanced: Put Spread Targeting Support

Play: Buy bearish put spread capturing the institutional positioning thesis

Structure: Buy $400 puts, Sell $380 puts (March 6 expiration - SAME as $8.2M trade)

Why this works:

- Defined risk spread ($20 wide = $2,000 max risk per spread)

- Targets gamma support zone at $380-$390 where dealers will defend

- Essentially "copying" the smart money positioning at smaller scale

- March 6 expiration captures Cybercab production risk window

- Bearish gamma bias (-39.7B net) supports directional thesis

Estimated P&L:

- Cost: ~$8-10 net debit per spread

- Max profit: $1,000-1,200 if TSLA below $380 at expiration

- Max loss: $800-1,000 if TSLA above $400

- Breakeven: ~$390-392

- Risk/Reward: ~1:1 to 1.2:1

Position sizing: Risk only 2-5% of portfolio

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

Aggressive: Naked Put Sale (Cash-Secured) - Premium Collection

Play: Sell cash-secured puts at $350 support to collect premium while waiting for entry

Structure: Sell $350 puts (March 6 expiration)

Why this could work:

- Collect premium while waiting for potential pullback entry

- $350 is major gamma support (-6.8B net) - dealers will defend aggressively

- If assigned, buying TSLA at ~$340-345 effective cost (12-15% below current)

- Premium of ~$5-8 provides income while waiting

- Implied move lower range of $354.73 for March 20 suggests $350 support should hold

Why this could blow up (RISKS):

- Cybercab delay announcement could crater stock below $350

- Requires ~$35,000 cash per contract for assignment

- BYD competition or Musk distraction narrative could accelerate selloff

- Black swan event (regulatory, geopolitical) could gap through support

Estimated P&L:

- Premium collected: ~$5-8 per contract ($500-800)

- Max profit: Full premium if TSLA stays above $350

- Breakeven: ~$342-345 (strike minus premium)

- Max loss: Substantial if TSLA collapses (assignment at $350 with unlimited downside)

CRITICAL WARNING - Only attempt if:

- You WANT to own TSLA at $340-345 effective cost

- You have $35,000+ cash per contract for potential assignment

- You're comfortable with unlimited downside risk below strike

- You have experience with options assignment mechanics

Risk level: HIGH (undefined downside risk) | Skill level: Advanced

Risk Factors

Don't get caught by these potential landmines:

-

Execution risk on autonomous driving: Musk has repeatedly missed FSD and robotaxi deadlines and now admits 10 billion miles needed for unsupervised driving. Cybercab production starting April may face delays. Regulatory approval for robotaxi expansion remains uncertain with NHTSA probing Tesla's Autopilot.

-

Competition from BYD and Chinese EV makers: BYD now sells 38% more EVs than Tesla globally. Chinese EVs priced 20,000-40,000 EUR grabbing market share. Tesla's 5-year zero-interest financing in China signals desperation.

-

Musk distraction and DOGE conflicts: Musk leads DOGE while his companies hold ~$15.4B in government contracts. Democratic senators introducing conflict-of-interest legislation. SpaceX-xAI merger adds questions about where Musk's focus lies.

-

Tariff exposure on global supply chain: Tesla CFO flagged company is "very reliant" on global parts with tariffs up to 145% on some Chinese components. Could add 5-10% to vehicle costs.

-

CapEx surge increases cash burn: ~$20B capex in 2026 (more than doubling from $8.6B) creates execution risk if AI/robotics investments don't deliver returns.

-

Valuation stretched for declining core business: At $1.52T market cap, Tesla trades at massive premium despite FY 2025 revenue declining from $97.7B to $94.8B and two consecutive years of falling deliveries. Requires flawless execution on AI pivot to justify valuation.

-

$400 gamma ceiling creates resistance: Massive 45.6B gamma at $400 means market makers will systematically sell into rallies. Stock needs sustained institutional buying to break through. Net GEX bias is bearish.

-

$8.2M institutional put signals concern: This EXTREMELY UNUSUAL trade (Z-Score 40.13) signals sophisticated players are positioning for downside. When funds pay $8.2M for protection at $400 strike with stock at $391, they see real risk of decline.

The Bottom Line

Real talk: Someone just spent $8.2 MILLION on TSLA $400 puts with stock trading BELOW the strike price. This is either a highly confident directional bet that Tesla drops to $370-375, or a sophisticated hedge protecting hundreds of millions in long exposure ahead of the Cybercab production launch in April.

What this trade tells us:

- Sophisticated player expects VOLATILITY through March 6th expiration

- They're positioned for a move below $390 support toward $375-380

- The timing (post-Q4 earnings, pre-Cybercab) shows they see execution risk

- They struck EXACTLY at $400 gamma wall - betting resistance holds and reversal follows

- At $25/contract for slightly ITM puts, they need ~7% decline to profit meaningfully

This is a CAUTIONARY signal - smart money is positioned defensively at a key inflection point.

If you own TSLA:

- Consider trimming 20-30% at $395-405 if you haven't already locked in gains

- Set MENTAL STOP at $380 (secondary gamma support) to protect core position

- If stock breaks above $410, resistance shifts to $420 - momentum could accelerate

- Monitor Cybercab production updates in March for fundamental confirmation

If you're watching from sidelines:

- $350-$370 pullback would be EXCELLENT entry (10-15% below current with gamma support)

- Looking for confirmation: Cybercab on-track, Robotaxi expansion news, FSD regulatory progress

- Wait for breakout above $420 OR breakdown below $380 for directional clarity

- Current $390-$400 range is NO MAN'S LAND - maximum uncertainty

If you're bearish:

- Put spreads offer defined-risk way to play downside ($400/$380 structure)

- Watch for break below $390 - that's the trigger for cascade to $380, then $350

- Don't fight massive gamma at $400 with naked shorts - risk/reward poor

- Catalyst window (Cybercab April, Q1 earnings April 28) provides clear timeline

Mark your calendar - Key dates:

- February 14, 2026 - FSD one-time purchase ends, subscription-only begins

- March 6, 2026 - This $8.2M put trade expires

- April 2026 - Cybercab production begins (KEY CATALYST)

- April 28, 2026 - Q1 2026 earnings report

- Q2 2026 - Model S/X production ends, Optimus conversion begins

- End of 2026 - Robotaxi "widespread" in US (Musk's claim)

Final verdict: Tesla's transformation from EV company to AI/robotics powerhouse is genuinely exciting - Robotaxi service, Cybercab production, Optimus robots, and energy storage all represent massive TAM expansion. BUT, execution risk is real given Musk's history of timeline misses, regulatory uncertainty, and distractions from DOGE/SpaceX/xAI. The $8.2M institutional put is a CLEAR signal that sophisticated investors see near-term downside risk.

The Cybercab production launch in April is THE catalyst that will determine whether Tesla's AI pivot is real or another unfulfilled promise. Until then, the risk/reward favors patience.

Trade smart. Manage risk. Let the catalysts play out.

About Tesla, Inc.: Tesla operates as a vertically integrated battery electric vehicle automaker and developer of real world artificial intelligence software, including autonomous driving and humanoid robots. The company manufactures multiple vehicle types spanning luxury sedans, crossover SUVs, light trucks, and semi trucks, with plans for robotaxi services. Beyond vehicles, Tesla produces batteries for stationary energy storage, solar panels and roofs, operates a fast-charging network, and provides auto insurance. Market cap: $1.52 trillion.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-Score of 40.13 reflects this specific trade's unusualness relative to recent TSLA history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Tesla's stock price can move 5-10% on news flow without warning. The put buyer may have complex hedging needs not applicable to retail traders.