🎯 TSM Options Flow: $14M CALL Buy Signals Big Money Positioning!

📅 December 31, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just bought $14 MILLION worth of TSM call options with a February 2026 expiration at the $250 strike! This massive institutional bet on Taiwan Semiconductor suggests big money is positioning for continued upside ahead of Q4 2025 earnings (January 15, 2026) and the company's 2nm chip production ramp. With TSM currently trading at $304.56, this deep in-the-money call purchase shows serious conviction in the AI chip leader.

🏢 Company Overview

Taiwan Semiconductor Manufacturing Company (TSM) is the world's largest dedicated chip foundry, commanding mid-60s market share in the global semiconductor manufacturing industry. The company serves tech giants like Apple, AMD, and NVIDIA, producing the most advanced chips that power AI, smartphones, and high-performance computing.

Key Stats:

- 💰 Market Cap: $1.55 trillion

- 🏭 Industry: Semiconductor Manufacturing / Foundry Services

- 🌍 Position: Dominant player with 67.6% foundry market share

- 🔬 Technology: Leading-edge 2nm production now live (started Q4 2025)

💰 The Option Flow Breakdown

📊 What Just Happened

Here's the complete trade that caught our attention:

| Time | Symbol | Buy/Sell | C/P | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:55:05 | TSM | BUY | CALL | 2026-02-20 | $14,000,000 | $250 | 2,700 | 25,000 | 2,500 | $305.41 | $57.75 | TSM20260220C250 |

🤓 What This Actually Means

This isn't your average retail trade - here's the breakdown:

- 🐋 Monster Position: $14M premium shows institutional-level capital at work

- 📈 Deep ITM Strategy: $250 strike vs. $305 spot = $55.41 intrinsic value per contract

- 📅 51 Days to Expiration: Feb 20, 2026 gives flexibility through Q4 earnings and beyond

- 🎯 Classification: This is classified as a "Close Short CALL" position (BTC - Buy to Close)

Real Talk: When we see a "Close Short CALL" order, it means someone who sold these calls earlier is now buying them back. This could indicate:

- The seller wants to close out a covered call position

- They're unwinding a short call hedge because they now want more upside exposure

- It's part of a larger options roll strategy

The confidence level is MEDIUM with a z-score of 0.58 (classified as TYPICAL activity). The volume-to-OI ratio of 0.108 suggests LOW_ACTIVITY overall, but the dollar amount is what matters here.

📈 Chart Check-Up

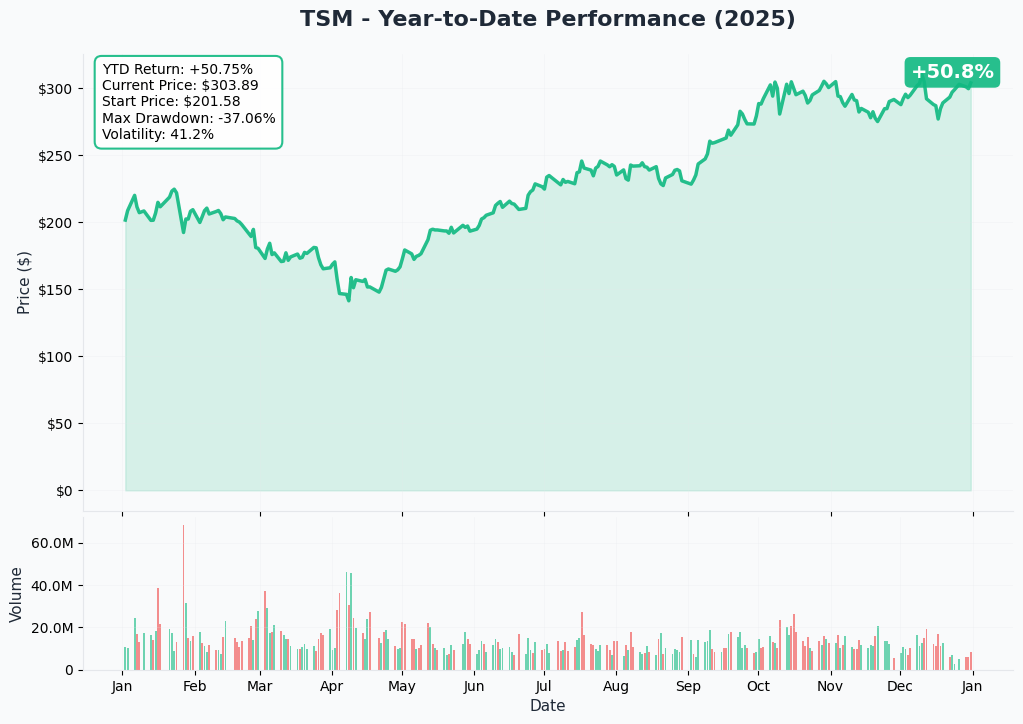

YTD Performance Analysis

TSM has had an impressive 2025, with the stock climbing from around $134 in April to a peak of $314 in December. Currently trading at $304.56, the stock is up +43% YTD according to recent reports.

Key Observations:

- Strong uptrend established throughout 2025

- Brief consolidation in summer months

- Explosive move higher in Q4 2025 on AI chip demand

- Currently near all-time highs with strong support established

The chart shows TSM has built a solid foundation of support in the $290-$300 range, with multiple successful tests holding. The recent pullback from $314 looks more like healthy profit-taking than a trend reversal.

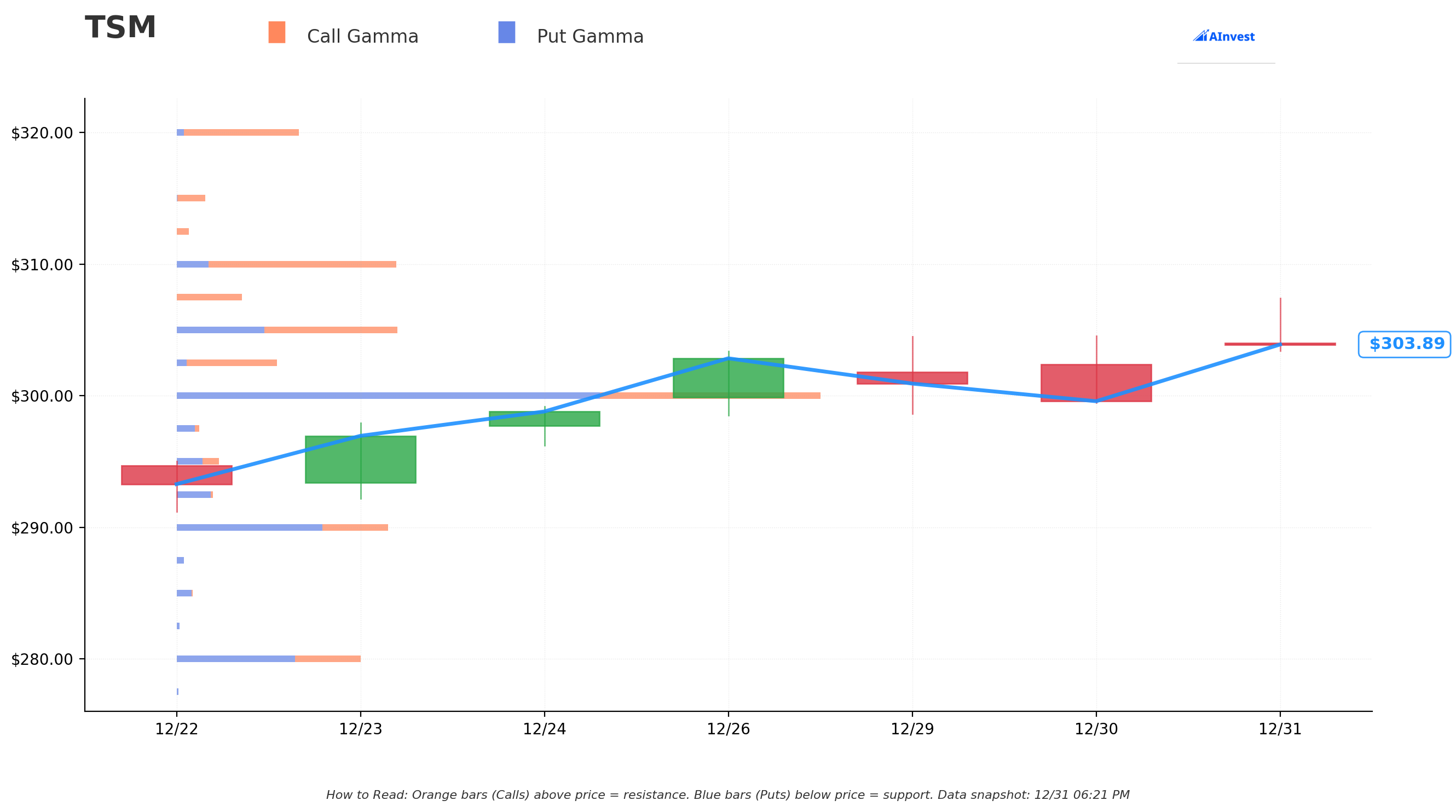

🎯 Gamma-Based Support & Resistance Analysis

What The Gamma Levels Tell Us:

The gamma exposure (GEX) data reveals some critical price levels where options activity is creating natural support and resistance zones. Let me break this down in plain English:

Key Support Levels (Blue Bars - Put Gamma):

- 🔵 $302.50 - Strongest nearby support with 6.36M net call gamma (0.68% below current price)

- 🔵 $300.00 - Major support zone with 50.76M total GEX, heavily skewed to puts (-15.98M net put gamma)

- 🔵 $290.00 - Secondary support at 4.78% below current price

- 🔵 $280.00 - Strong floor if we see a deeper pullback (8.06% below)

Key Resistance Levels (Orange Bars - Call Gamma):

- 🟠 $305.00 - Immediate resistance just 0.14% away with 3.58M net call gamma

- 🟠 $310.00 - Major resistance with 12.28M net call gamma (1.79% above)

- 🟠 $320.00 - Next big target with 8.53M net call gamma (5.07% upside)

- 🟠 $330.00 - Longer-term resistance at 8.35% above current price

Translation for regular folks: The $300 level is absolutely loaded with put protection (33.37M put GEX vs only 17.39M call GEX), making it a natural floor. Meanwhile, there's a cluster of call gamma at $305-$310 that could act as a magnet for price action.

Net GEX Bias: BULLISH with total call GEX of 106.77M vs put GEX of 99.55M. This suggests dealers are positioned for upside movement.

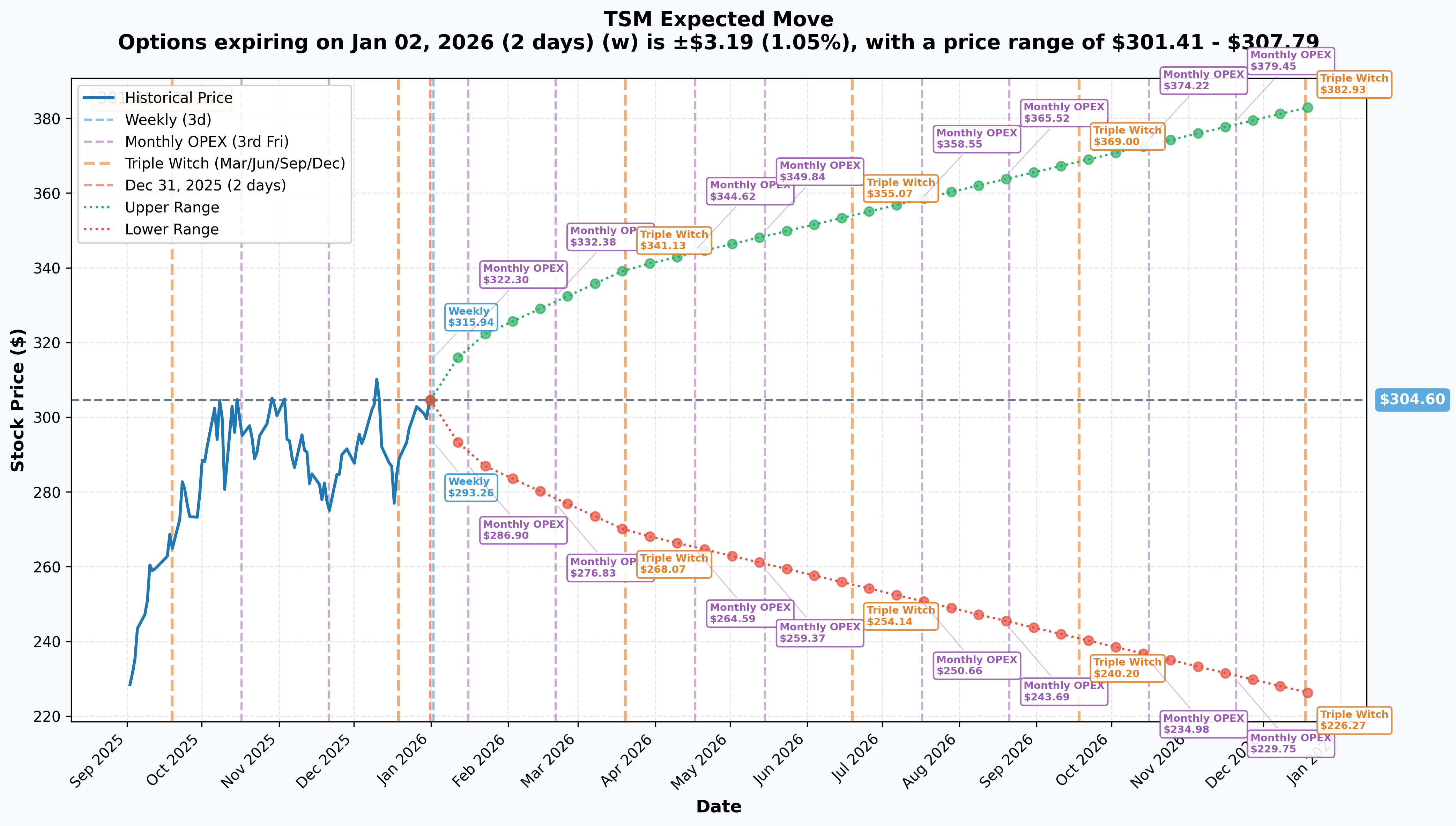

📊 Implied Move Analysis

What Options Are Pricing In:

Based on current options pricing, here's what the market expects for TSM price movement across different timeframes:

Weekly (Jan 2, 2026 - 2 days out):

- 📍 Implied Move: ±1.05% (±$3.19)

- 📊 Range: $301.41 - $307.79

- ✅ Reliability: High (very short-term, high confidence)

Monthly OPEX (Jan 16, 2026 - 16 days out):

- 📍 Implied Move: ±5.21% (±$15.87)

- 📊 Range: $288.73 - $320.47

- ✅ Reliability: High

- 🎯 Why It Matters: This covers Q4 earnings on January 15!

Quarterly Triple Witch (March 20, 2026 - 79 days out):

- 📍 Implied Move: ±11.52% (±$35.10)

- 📊 Range: $269.50 - $339.71

- ✅ Reliability: High

- 🎯 Key Events: Full 2nm production ramp visibility

Yearly LEAPS (Dec 18, 2026 - 352 days out):

- 📍 Implied Move: ±25.71% (±$78.33)

- 📊 Range: $226.27 - $382.93

- ✅ Reliability: High

- 🎯 Big Picture: Market pricing in significant volatility over full year

What This Means: Options are pricing in a $288-$320 range through the critical January earnings event. That $14M call buyer at the $250 strike has a massive cushion - the stock would need to drop nearly -18% just to hit that strike!

🎪 Catalysts

🔥 Upcoming Catalysts (Could Move The Stock)

Q4 2025 Earnings - January 15, 2026 📊

- Earnings Call: 14:00-15:30 Taipei time

- Consensus Revenue: $32.2-33.4 billion

- Expected Gross Margin: 59-61%

- Expected Operating Margin: 49-51%

- Full Year 2025 Growth: Mid-30% YoY in USD terms

- Why It Matters: This will give us first official update on 2nm production ramp and CoWoS capacity expansion progress

2nm Production Ramp (H1 2026) 🔬

- Volume production started Q4 2025 at Fab 22

- Initial customers: Apple, AMD, Intel ramping now

- Second wave: NVIDIA, Qualcomm, MediaTek following close

- Target: 50,000 wafers/month by end 2025, expanding to 120,000-130,000 wpm by end 2026

- Status: 2nm capacity already fully sold out for 2026

- Performance Gains: 10-15% faster OR 25-30% more power efficient vs 3nm

CoWoS Advanced Packaging Expansion 📦

- 2025 capacity: ~75,000-90,000 wafers/month (nearly doubling 2024)

- 2026 target: 120,000-130,000 wafers/month (+33% YoY)

- NVIDIA Alert: Has booked >50% of 2026 CoWoS capacity (800,000+ wafers)

- Why It Matters: CoWoS packaging is the bottleneck for AI accelerators - more capacity = more revenue

Pricing Increases (2026) 💰

- TSMC planning 3-10% price increases for advanced chips starting 2026

- AI demand significantly outpacing supply

- Pricing power demonstrates TSMC's monopoly position

Arizona Fab Acceleration 🇺🇸

- Fab 21 Phase 2 (3nm): Equipment installation accelerated to Q3 2026

- Production targeted for 2027 (several quarters ahead of original 2028 schedule)

- Total U.S. investment expanded from $65B to $165B

- Yield rates reportedly exceed Taiwan facilities by ~4 percentage points

📅 Recent Catalysts (Already Happened)

Q3 2025 Earnings - October 16, 2025 📈

- Revenue: NT$989.92B ($33.10B USD), up 40.8% YoY

- Net Income: NT$452.30B ($14.77B USD), up 39.1% YoY

- EPS: NT$17.44, beating consensus by 11.2%

- Gross Margin: 59.5%, up from 57.8% YoY

- Tech Mix: 74% from advanced nodes (3nm/5nm/7nm), with HPC at 57% of revenue

- Result: Crushed it! Stock rallied to new highs post-earnings

2nm Volume Production Launch - Q4 2025 🚀

- TSMC commenced volume production of N2 (2nm) chips at Fab 22 in Q4 2025

- First adoption of gate-all-around (GAA) nanosheet transistors

- Major technological milestone ahead of Samsung and Intel

Analyst Upgrades - November/December 2025 📊

- Susquehanna raised price target to $400 from $300

- Bernstein raised to $330 from $290

- Huatai maintained Buy with $320 target

- Consensus average: $344-$361 (13-18% upside from current levels)

🎲 Price Targets & Probabilities

Bull Case Target: $320-$330 (5-8% upside)

Path to Get There:

- ✅ Q4 earnings beat expectations (high probability given Q3 momentum)

- ✅ 2nm ramp on track with 50,000+ wafers/month by end of Q1 2026

- ✅ CoWoS capacity expansion updates show no delays

- ✅ Pricing power confirmed for 2026

Supporting Evidence:

- Gamma resistance at $320 shows major call gamma concentration (8.53M net)

- Implied move for March OPEX includes $339.71 upper range

- Analyst consensus of $344-$361 suggests professional expectations align

- Historical pattern: TSM tends to rally 3-5% post-earnings on beats

Probability: 60% - This is the base case if earnings are in-line to slightly better

Base Case Target: $300-$310 (0-2% range)

What Keeps Us Here:

- Mixed earnings results (revenue beat, margin pressure)

- 2nm ramp progressing but with minor hiccups

- Geopolitical noise from Taiwan-China tensions picks up

- Broader market consolidation after strong 2025

Supporting Evidence:

- Strongest support at $300 with 50.76M total GEX (heavily put-protected)

- Immediate resistance at $305-$310 acts as gravity zone

- January OPEX implied range of $288-$320 centers around current price

- Net bullish GEX bias suggests dealers need to buy if we dip to $300

Probability: 30% - Market seems to want directional move, not consolidation

Bear Case Target: $280-$290 (5-8% downside)

Path to Get There:

- ❌ Q4 earnings disappoint (revenue miss or weak 2026 guidance)

- ❌ 2nm ramp delays or yield issues surface

- ❌ Major geopolitical escalation (China-Taiwan tensions)

- ❌ Broader semiconductor sector weakness on AI spending concerns

Supporting Evidence:

- Support levels at $290 (11.52M total GEX) and $280 (14.52M total GEX)

- March quarterly implied move goes as low as $269.50

- Historical precedent: TSM can drop 5-10% on earnings misses

- VEU status revoked by U.S. creates regulatory uncertainty

Probability: 10% - Low probability given strong fundamentals, but geopolitical risk is real

💡 Trading Ideas

🛡️ Conservative: The "Sleep Well" Covered Call Strategy

Setup:

- Own 100 shares of TSM at current price ($304.56)

- Sell 1 Feb 21, 2026 $315 Call for ~$12.00 credit

- Max Profit: $12.00 premium + $10.44 stock gain = $22.44 per share (7.4% return)

- Downside Protection: $12.00 credit reduces cost basis to $292.56

- Breakeven: $292.56 (3.9% cushion)

Why This Works:

- You collect premium while waiting for upside through earnings

- $315 strike gives room for 3.4% upside before assignment

- Even if called away at $315, you capture solid gains

- The $300 support level provides strong downside protection

Risk Management:

- If TSM rallies above $320, you miss additional upside

- Still profitable, just capped at $315

- Can roll call up/out if stock surges

Ideal For: Investors who own TSM and want income while slightly bullish

⚖️ Balanced: The "Earnings Straddle" for Volatility Play

Setup:

- Buy 1 Jan 16, 2026 $305 Call for ~$14.50

- Buy 1 Jan 16, 2026 $305 Put for ~$15.00

- Total Cost: $29.50 per share ($2,950 total)

- Breakeven Points: $275.50 or $334.50 (±9.7% move needed)

Why This Works:

- January 16 expiration is RIGHT AFTER January 15 earnings

- Implied move of ±5.21% ($288.73-$320.47) is already priced in

- Historical pattern: TSM averages 6-8% post-earnings moves

- You profit if the move exceeds $29.50 in EITHER direction

The Math:

- Need move beyond $275.50 (down 9.5%) OR $334.50 (up 9.8%)

- Q3 earnings: stock moved 8.2% in 3 days post-announcement

- If TSM hits $335, call worth ~$30, put worthless = breakeven

- If TSM hits $340, call worth ~$35, put worthless = $550 profit (18.6% return)

Risk Management:

- Max loss is $2,950 if stock stays near $305

- Time decay accelerates after January 10

- Consider closing one leg if stock moves 4-5% before earnings

Ideal For: Traders expecting a significant post-earnings move who don't want to pick direction

🚀 Aggressive: The "2nm Ramp" Bull Call Spread

Setup:

- Buy 1 March 20, 2026 $310 Call for ~$18.00

- Sell 1 March 20, 2026 $330 Call for ~$8.00

- Net Debit: $10.00 per share ($1,000 total)

- Max Profit: $20.00 per share ($2,000 total) = 100% return

- Max Loss: $10.00 per share ($1,000 total)

- Breakeven: $320.00 (4.9% above current price)

Why This Works:

- March 20 expiration gives time for 2nm ramp updates and earnings catalysts

- Targets the $320-$330 resistance zone identified in gamma analysis

- Implied move for March quarterly OPEX includes $339.71 upper range

- Risk/reward of 2:1 with defined risk

The Thesis:

- Q4 earnings (Jan 15) shows strong 2nm adoption and guidance raise

- By March, TSMC reports 2nm wafer capacity at 60,000+ wpm (ahead of schedule)

- CoWoS expansion updates confirm NVIDIA/AMD demand remains insane

- Stock pushes to $330-$340 range by March OPEX

Profit Scenarios:

- At $320: Spread worth $10, break even

- At $325: Spread worth $15, profit $500 (50% return)

- At $330+: Spread worth $20, profit $1,000 (100% return)

Risk Management:

- Max loss capped at $1,000 even if TSM crashes

- Spread reduces cost vs naked call by $800

- Can close at 50% profit (~$315) to lock gains early

Ideal For: Bullish traders who believe 2nm ramp + earnings will drive TSM to new highs

⚠️ Risk Factors

Geopolitical Wildcard 🌍

Taiwan-China Tensions: The elephant in the room - TSM is headquartered in Taiwan, and Chinese military activity around Taiwan has been increasing (NPR reports on "gray zone" tactics). Any escalation could trigger:

- Sharp selloff regardless of fundamentals (could drop 10-20% on real conflict fears)

- Export controls tightening further (VEU status already revoked as of Dec 31, 2025)

- Supply chain disruption concerns

Mitigation: TSMC is aggressively expanding globally (Arizona, Japan, Germany) to de-risk, but Taiwan still produces 90%+ of advanced chips. This is a tail risk that's hard to quantify but could be devastating.

Execution Risks 🏭

2nm Production Ramp: While TSMC has an excellent track record, ramping a completely new node with GAA technology is complex:

- Yield issues could surface in first 6 months

- Customer delays if chips don't meet specs

- Capacity targets of 120,000 wpm by end 2026 are aggressive

If Things Go Wrong: Stock could give back 5-10% on any 2nm ramp delays, especially if Samsung or Intel gain ground.

CoWoS Capacity Bottleneck: NVIDIA has booked >50% of 2026 CoWoS capacity, but what if:

- Equipment delays push capacity expansion timeline

- Yield issues on advanced packaging

- Customers like NVIDIA experience demand slowdown

Impact: Revenue growth expectations would need to be revised down, pressuring multiples.

Valuation & Competition 📊

Valuation Concerns:

- TSM trades at 30x P/E, which is reasonable vs NVIDIA/AMD but stretched vs historical 20-25x range

- At $305, stock is near all-time highs with $344-$361 analyst targets implying 13-18% upside

- If AI spending slows, multiple could compress to 25x = $250-260 stock price

Competitive Threats:

- Samsung 2nm: Also entering production in 2025, historically struggles with yields but could surprise

- Intel 18A: Claims ~1 year lead in backside power delivery, targeting H2 2025 production

- If either competitor gains significant share, TSMC's pricing power diminishes

Regulatory & Export Controls 🚨

Recent Developments: According to South China Morning Post, TSMC's Validated End User (VEU) status was revoked effective December 31, 2025. This means:

- Shipments of U.S.-origin chipmaking tools to China now require export licenses

- TSMC halted 7nm+ advanced chip shipments to Chinese AI customers

- Nanjing fab contributes <3% of revenue, so financial impact is "minor"

But Watch Out For:

- Retaliation from China (rare earth export controls)

- Further U.S. restrictions if Huawei incident repeats

- Political pressure from Trump administration for 50-50 U.S.-Taiwan chip production split

Macro Headwinds 🌊

Broader Market Risks:

- AI spending skepticism if capex ROI questioned (though no signs yet)

- Global semiconductor demand cyclicality outside AI segment

- Currency fluctuations (NT$ vs USD) impacting reported revenue

- Rising interest rates affecting capital-intensive expansion plans ($40-50B annual CapEx)

🎯 The Bottom Line

Real Talk: This $14M call purchase is interesting, but here's the twist - it's classified as "Buy to Close" a short call position, not a fresh bullish bet. Someone who previously sold these $250 calls is now buying them back. This could mean they want to recapture upside ahead of earnings, or they're repositioning a larger strategy.

What We Know:

- TSM just started 2nm production (volume production live in Q4 2025)

- Q4 earnings on January 15, 2026 will be critical for guidance

- 2nm capacity is fully booked through 2026 at higher prices (+3-10% increases)

- CoWoS advanced packaging remains the AI supply chain bottleneck

- Geopolitical risk is real but being addressed through global expansion

The Setup:

- Stock at $304.56, near all-time highs but with strong support at $300

- Gamma analysis shows $300-$302.50 as key support, $310-$320 as resistance

- Implied move for January OPEX: $288.73-$320.47 (±5.21%)

- Net bullish GEX bias (106.77M call vs 99.55M put)

Three Scenarios - Pick Your Poison:

1. If You Own TSM (or want to): ✅ Hold through earnings with a trailing stop at $290 ✅ Consider selling Feb $315 calls against shares for 7.4% potential return ✅ Add on any dip to $295-300 range where put gamma provides strong support ✅ Mark your calendar for January 15, 2026 earnings - this will set the tone for Q1 2026

2. If You're Watching from the Sidelines: 👀 Wait for post-earnings clarity before entering 👀 Watch for break above $310 with volume as bullish confirmation 👀 Below $295, reassess - that would break multiple support levels 👀 Q1 2026 will give first real data on 2nm production volumes

3. If You're Bearish: 📉 Hard to fight this tape given fundamentals, but geopolitical risk is your edge 📉 Any escalation in Taiwan-China tensions = immediate 10-15% drop opportunity 📉 Watch for 2nm ramp hiccups or CoWoS capacity delays in January earnings call 📉 Below $280, support gets thin until $270 level

Action Plan:

- Now through Jan 15: Position sizing based on risk tolerance; TSM has binary risk around earnings

- Jan 15-16: Watch earnings closely; TSMC typically provides detailed updates on production ramps

- Jan 16-Feb 20: Reassess based on guidance; 2nm progress and CoWoS capacity updates will drive next leg

- March onward: Look for confirmation that 2nm volumes are hitting 60,000+ wafer/month targets

The Lesson: TSM is the singular bottleneck for AI infrastructure. NVIDIA, AMD, Apple - they all need TSMC to deliver. The company has a proven track record of execution and is printing money (59.5% gross margins!). But at 30x P/E near all-time highs, the expectations are sky-high. This isn't a value play - it's a growth story that requires continued flawless execution. The geopolitical risk is the only thing that could derail the fundamentals in the near term.

Bottom Line: Bullish into earnings with well-defined support at $300, but don't ignore the tail risk. The $14M call position closing suggests even professionals are taking some risk off the table ahead of a potentially volatile period.

⚖️ Disclaimer

This analysis is for educational and informational purposes only and should not be considered financial advice. Options trading carries substantial risk and is not suitable for all investors. The risk of loss in trading options can be significant, and you should carefully consider whether options trading is appropriate for your financial situation. Past performance does not guarantee future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.

Specific Risks for TSM:

- Geopolitical risk from Taiwan-China tensions could result in immediate and severe losses

- Semiconductor industry is cyclical and capital-intensive

- Options strategies presented have defined risks but can result in total loss of premium paid

- Volatility around earnings can be extreme; manage position sizing accordingly

Data Sources: Trade data from proprietary options flow analysis. Company information from public filings and financial news sources. Gamma exposure calculated from aggregated options positioning data. Implied moves derived from at-the-money straddle pricing.

Analysis Date: December 31, 2025 TSM Stock Price: $304.56 Market Cap: $1.55 Trillion

Remember: Smart money is positioning, but they also manage risk religiously. Don't bet the farm - size your positions based on your risk tolerance and always have an exit plan. 💪