TSM $4.7M Put Protection - Institutions Hedging Before Q4 Earnings Call

January 12, 2026 | Unusual Activity Detected

The Quick Take

Someone just spent $4.7 MILLION on TSM puts this morning at 10:46:53, buying 5,000 contracts of the $320 strike puts expiring February 13th. With TSM's Q4 2025 earnings call just 3 days away on January 15th, this looks like classic institutional hedging on a stock that's rallied +60% over the past year. The Z-score of 100.09 makes this an extremely unusual trade - smart money is buying insurance before the biggest catalyst of the quarter.

Company Overview

Taiwan Semiconductor Manufacturing Company (TSM) is the world's largest dedicated chip foundry, commanding mid-60s market share globally:

- Market Cap: $1.68 Trillion (one of the most valuable companies on Earth)

- Industry: Semiconductor Manufacturing

- Current Price: $332.03

- Primary Business: Contract manufacturing of semiconductors for Apple, Nvidia, AMD, and other tech giants - produces 90%+ of the world's most advanced chips

The Option Flow Breakdown

The Tape (January 12, 2026 @ 10:46:53):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:46:53 | TSM | ASK | BUY | PUT $320 | 2026-02-13 | $4,700,000 | $320 | 5,000 | 155 | 5,000 | $332.03 | $9.40 |

Additional Trade Details:

- Order Type: Buy-to-Open (BTO)

- OI Signal: HIGH_ACTIVITY (Vol/OI Ratio: 32.26)

- Z-Score: 100.09 (EXTREMELY_UNUSUAL)

- Strategy: Long Put

What This Actually Means

This is a defensive hedge ahead of a major earnings event. Here's the breakdown:

- Premium paid: $4.7M ($9.40 per contract x 5,000 contracts)

- Protection strike: $320 provides 3.6% downside cushion below current price

- Strategic timing: 3 days before Q4 2025 earnings call (January 15, 2026)

- Size matters: 5,000 contracts represents 500,000 shares worth approximately $166M in notional exposure

- Z-Score of 100.09: This is an extremely unusual trade - roughly 100x the normal activity level

What's really happening here: This trader likely holds a substantial long position in TSM and is protecting gains ahead of the earnings announcement. The February 13th expiration gives them coverage through earnings and the subsequent price action. With TSM up 60%+ over the past year and trading near 52-week highs, this is classic institutional risk management - not a bearish bet.

Unusual Score: EXTREMELY UNUSUAL (100x average activity) - This type of protective positioning happens maybe a few times per quarter around major events.

Technical Setup / Chart Check-Up

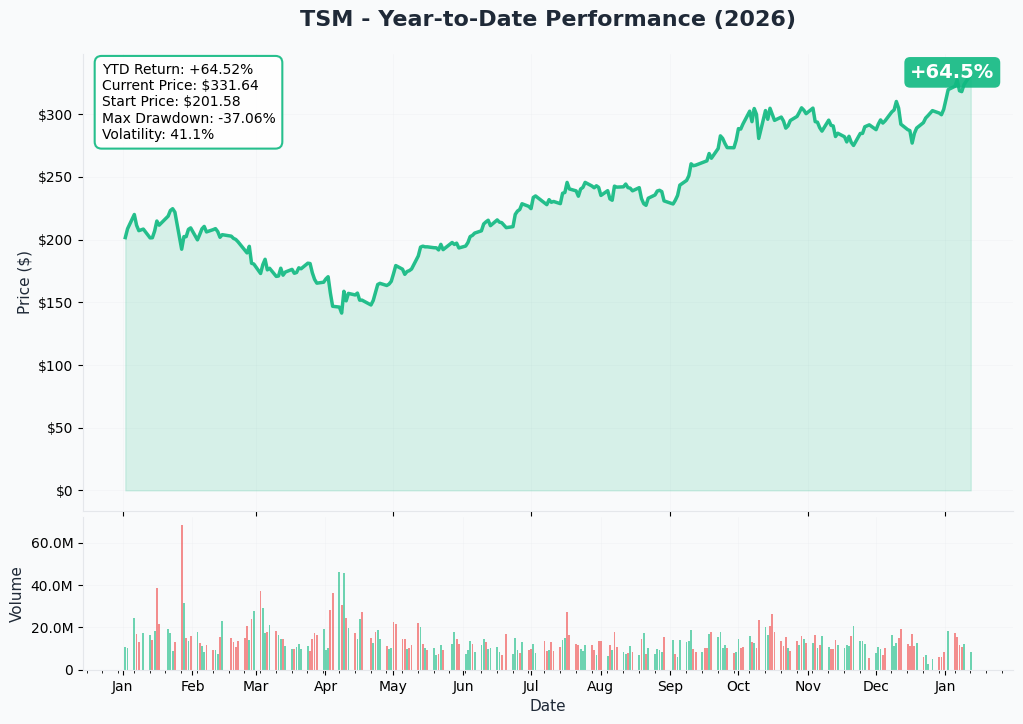

YTD Performance Chart

TSM has been on a strong run, trading near its 52-week high of $333.08 reached on January 6, 2026. The stock touched this level following Goldman Sachs' 35% price target increase, with shares jumping as much as 6.9% in a single session (Bloomberg).

Key observations:

- 52-Week High: $333.08 (January 6, 2026) - current price just below this level (Stock Analysis)

- 52-Week Low: $134.25 - stock has more than doubled from the lows (Stock Analysis)

- 1-Year Return: +60.72% from $201.36 on January 13, 2025 (Fintel)

- 2025 Full-Year Return: +50%+ (Motley Fool)

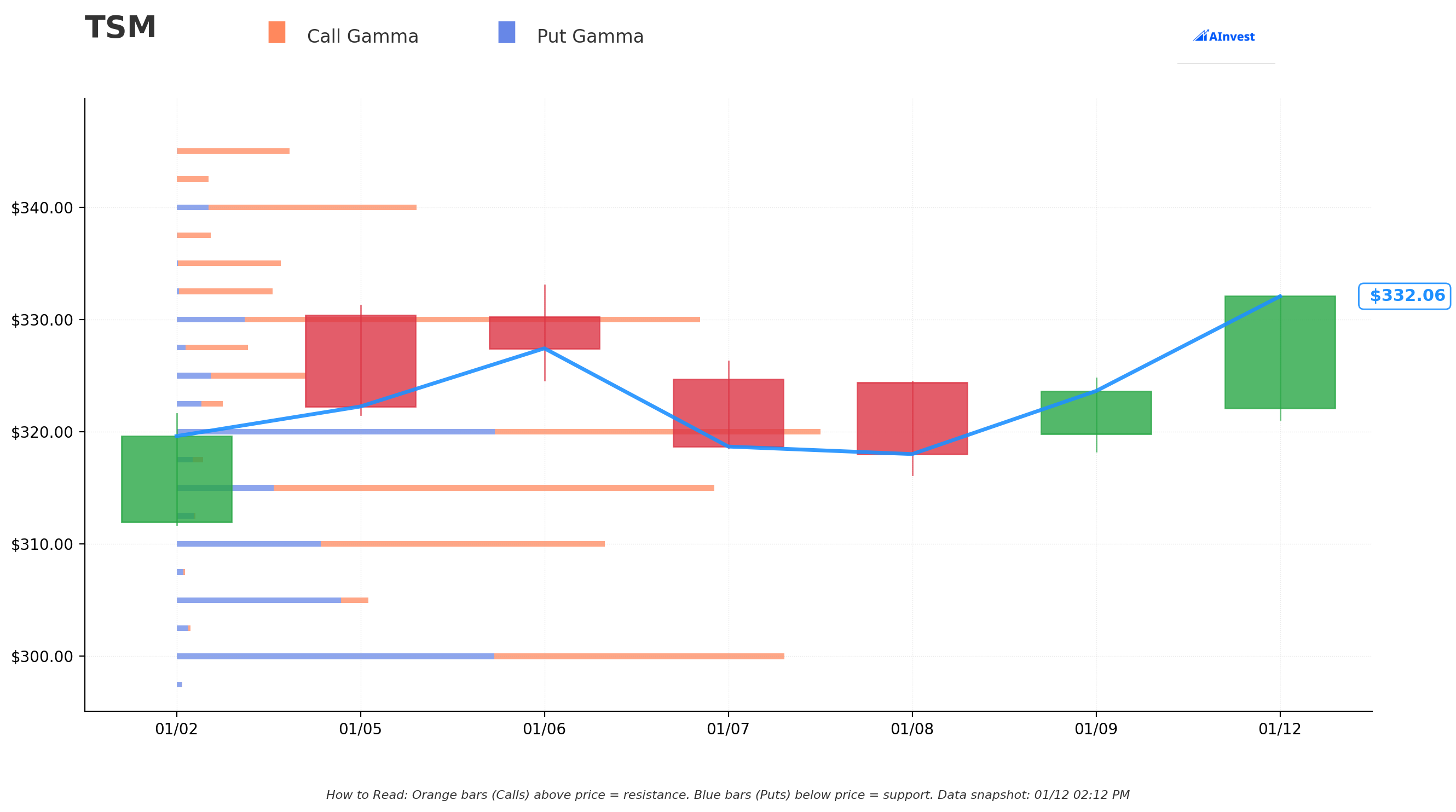

Gamma-Based Support & Resistance Analysis

Current Price: $332.03

The gamma exposure map reveals key price levels where options market makers will need to hedge:

Support Levels (Put Gamma Below Price):

- $330 - Strongest immediate support with 13.7B total gamma (0.6% below current price)

- $320 - Major support at 17.1B gamma (3.6% below) - THIS IS THE PUT STRIKE

- $315 - Secondary support at 14.2B gamma (5.1% below)

- $310 - Deep support at 11.5B gamma (6.6% below)

- $300 - Extended floor at 16.8B gamma (9.6% below)

Resistance Levels (Call Gamma Above Price):

- $340 - Strongest resistance with 6.3B gamma (2.4% above current)

- $350 - Extended resistance at 6.3B gamma (5.4% above)

What this means for traders: TSM is trading just above $330 gamma support with immediate resistance at $340. The put buyer struck exactly at $320, which represents the second-strongest gamma level below current price - a logical choice for protection if the stock breaks down. The bullish Net GEX bias (102B call gamma vs 58B put gamma) suggests overall positioning remains constructive, but earnings can override technicals.

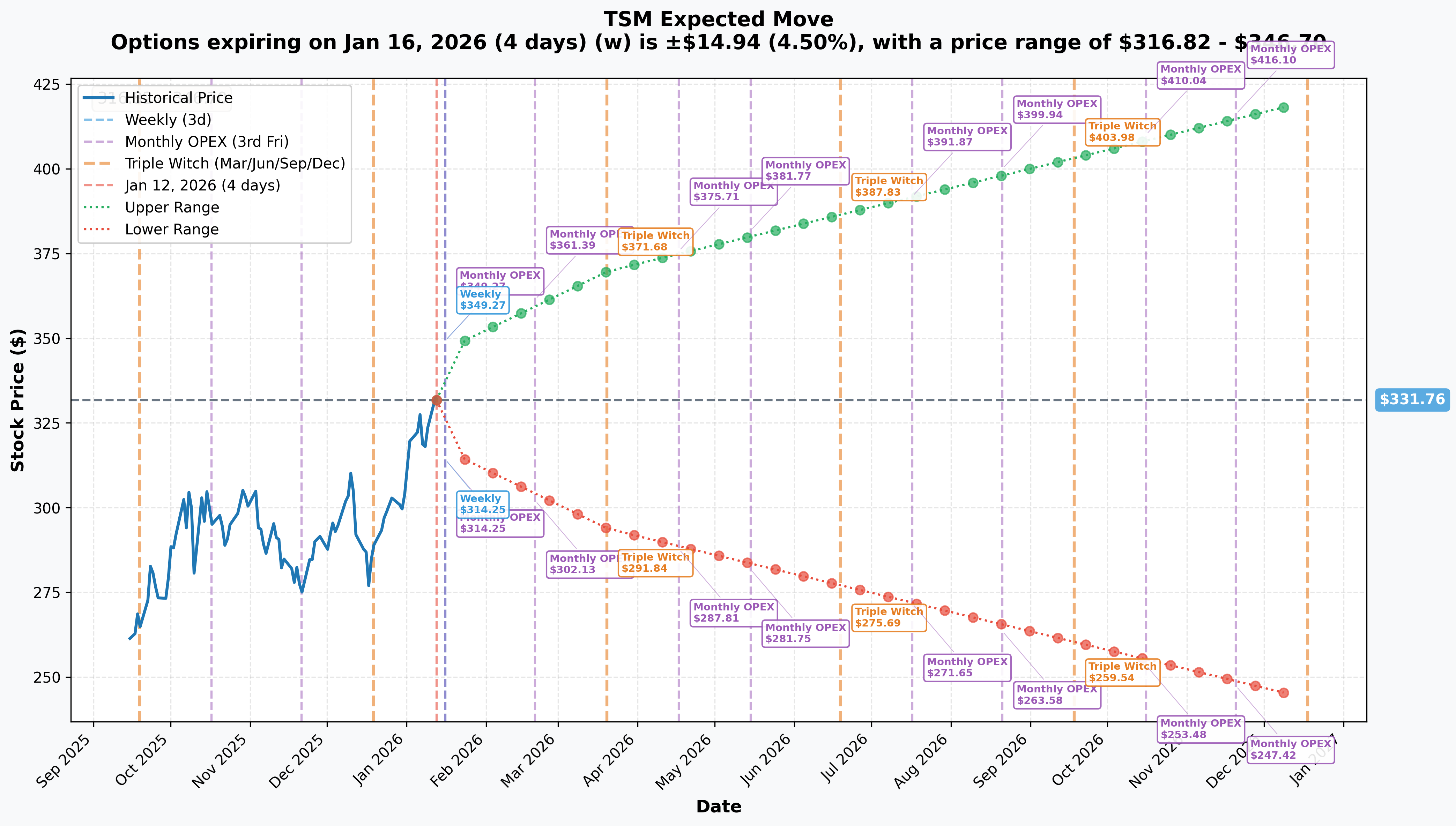

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 16 - 4 days): +/-4.5% ($14.94) -> Range: $316.82 - $346.70

- Monthly OPEX (Jan 16 - 4 days): +/-4.5% ($14.94) -> Range: $314.25 - $349.27

- February OPEX (Feb 20): Range: $302.13 - $361.39

- Quarterly Triple Witch (Mar 20 - 67 days): +/-11.48% ($38.08) -> Range: $293.68 - $369.84

- LEAPS (Dec 18): +/-26.58% ($88.19) -> Range: $243.57 - $419.95

Translation for regular folks: Options traders are pricing in a 4.5% move ($15) by January 16th around the earnings event. The $320 put strike sits right at the lower end of this implied range, suggesting the put buyer is protecting against a worst-case scenario where TSM drops to or below the expected range floor.

Catalysts

Immediate Catalysts (Next 7 Days)

Q4 2025 Earnings Conference Call - January 15, 2026 (3 DAYS AWAY!)

This is THE catalyst driving the put protection. According to TSMC's Financial Calendar:

- Date/Time: January 15, 2026, 14:00 Taiwan time / 1:00 AM ET (TSMC Investor Relations)

- Quiet Period: January 5-14, 2026 (we're in it now) (TSMC Investor Relations)

- Q4 Revenue (Already Reported): NT$1,046.08 billion ($33.05B), up 20.45% YoY, beat consensus (Reuters via Investing.com)

- Full-Year 2025 Revenue: NT$3,809.1 billion (record), up 31.6% YoY (TipRanks)

Key Items to Watch on Earnings Call:

- 2026 full-year revenue growth guidance (Street expects 20-25%, some analysts expect 30%)

- 2026 CapEx budget (expected $48-50B, up from $40-42B in 2025)

- N2/A16 ramp timeline updates

- CoWoS capacity expansion timeline

- Arizona fab production schedule

Recent Catalysts (Already Happened)

2nm (N2) Mass Production Begins (Q4 2025)

- TSMC began volume production of 2nm-class chips in Q4 2025 (Tom's Hardware)

- First GAA (Gate-All-Around) transistor for TSMC, claims up to 15% improvement at ISO power (TechSpot)

- 2nm capacity fully booked for all of 2026 (WCCFTech)

Arizona Fab Acceleration (December 2025)

- Second Arizona fab (3nm) equipment installation moved up to Q3 2026 (TrendForce)

- Total U.S. investment: $165 billion project including 5 chipmaking plants (Seeking Alpha)

Analyst Upgrades (January 2026) (Bloomberg)

- Goldman Sachs: NT$2,330 (+35% from NT$1,726)

- JPMorgan: NT$2,100 (+24% from NT$1,700)

- Citi: NT$2,450 (+36% from NT$1,800)

Upcoming Catalysts (H1 2026)

A16 (1.6nm) Mass Production (H2 2026)

- First angstrom-class process node with Super Power Rail (SPR) backside power delivery (TSMC Technology)

- NVIDIA confirmed as first A16 customer (WCCFTech)

Q1 2026 Earnings (April 2026)

- Consensus Revenue: ~$25.5B

- Consensus EPS: ~$2.90-3.00 per ADS

Price Targets & Probabilities

Using gamma levels, implied move data, and earnings catalyst positioning:

Bull Case (30% probability)

Target: $350-$370

How we get there:

- Earnings call provides 2026 revenue growth guidance of 30%+ (Morgan Stanley/JPMorgan bull case)

- CapEx budget signals strong AI demand visibility ($50B+)

- 2nm ramp commentary exceeds expectations

- CoWoS capacity expansion ahead of schedule

- Break above $340 gamma resistance triggers momentum to $350

Key metrics needed:

- 2026 revenue growth guidance above 25%

- Gross margin guidance maintained at 59-61%

- Strong A16/N2P commentary for H2 2026

Base Case (50% probability)

Target: $320-$345 range (CONSOLIDATION)

Most likely scenario:

- Solid earnings call with guidance in-line with Street expectations (20-22% growth)

- Stock consolidates between $330 gamma support and $340 resistance

- Market digests recent analyst upgrades and January rally

- Trading range through February as investors await Q1 results

- Put buyer's $320 protection proves unnecessary but provides peace of mind

This is the put buyer's target scenario: Stock consolidates, puts expire with little value, but the hedge served its purpose through the uncertain earnings period.

Bear Case (20% probability)

Target: $300-$320

What could go wrong:

- Guidance disappoints on revenue growth (sub-20% for 2026)

- Geopolitical concerns escalate around Taiwan

- AI spending commentary suggests potential deceleration

- Arizona fab execution concerns raised

- Break below $330 support triggers cascade toward $320 put strike, then $300

Critical support levels:

- $330: Major gamma floor (13.7B) - MUST HOLD

- $320: Deep support (17.1B gamma) + this put strike

- $300: Extended floor at 16.8B gamma - disaster scenario

Trading Ideas

Conservative: Wait and Watch

Play: Stay on sidelines until after January 15th earnings clarity

Why this works:

- Earnings in 3 days creates binary event risk

- Options expensive pre-earnings (elevated IV)

- Stock at 52-week highs with premium valuation

- Better entry likely post-earnings after IV crush

Action plan:

- Watch earnings call January 15th closely for 2026 guidance

- Look for pullback to $320-330 range post-earnings for stock entry

- Monitor institutional flow for follow-through

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Balanced: Post-Earnings Put Spread

Play: After earnings, sell put spread at gamma support levels

Structure: Buy $320 puts, Sell $310 puts (February 13 expiration - same as the $4.7M trade)

Why this works:

- IV crush after earnings makes put spreads cheaper

- Defined risk spread ($10 wide = $1,000 max risk per spread)

- Targets gamma support zone where institutions are positioned

- Mirrors smart money positioning at better prices post-IV crush

Estimated P&L:

- Pay ~$3-4 net debit per spread post-earnings

- Max profit: $600-700 if TSM below $310 at February expiration

- Max loss: $300-400 if TSM above $320

- Breakeven: ~$316-317

Entry timing: Wait 1-2 days post-earnings for IV collapse

Risk level: Moderate | Skill level: Intermediate

Aggressive: Earnings Straddle

Play: Buy straddle betting on post-earnings volatility exceeding implied move

Structure: Buy $330 calls + Buy $330 puts (January 16 expiration)

Why this could work:

- Implied move only 4.5% - TSM has history of larger moves on major guidance events

- 2026 guidance could surprise significantly in either direction

- Only need stock to move >5% to profit

Why this could blow up:

- EXPENSIVE: Straddle costs substantial premium

- IV CRUSH: Even if stock moves 3-4%, IV collapse could result in loss

- Need ~5%+ move to breakeven

Risk level: HIGH | Skill level: Advanced only

Risk Factors

Don't get caught by these potential landmines:

-

Earnings binary event in 3 days: January 15th earnings call creates significant volatility risk. The market is pricing +/-4.5% implied move, but actual moves could be larger depending on 2026 guidance quality and geopolitical commentary.

-

Geopolitical/Taiwan Strait Risk: This is the elephant in the room. A Taiwan chip supply disruption could cost the global economy $2.5 trillion annually (The New Global Order). TSMC produces 90%+ of world's most advanced chips in Taiwan (ScienceDirect).

-

Competition Risk: Intel 18A gaining traction with Microsoft, Amazon (Financial Content); Samsung targeting HPC market with SF2P in 2026 (PatentPC).

-

Arizona Fab Execution: Q3 2025 power outage scrapped thousands of wafers (Seeking Alpha), highlighting operational management gaps vs Taiwan operations.

-

AI Demand Cyclicality: Some concern that AI spending could slow in 2026 (Yahoo Finance). Heavy CapEx commitments (~$50B) could pressure margins if demand disappoints.

-

Valuation at premium levels: Trading at ~24x forward P/E after 60%+ 1-year gain. While reasonable relative to growth, any disappointment could trigger multiple compression.

The Bottom Line

Real talk: Someone just spent $4.7M protecting a substantial TSM position 3 days before the most important earnings call of the quarter. This isn't bearish on TSMC's long-term story - it's prudent risk management by institutions who've made strong returns on the 60%+ rally and don't want to give it back on one bad earnings print.

What this trade tells us:

- Sophisticated player expects volatility through February (not necessarily crash, but protecting against 5-10% downside scenario)

- They're concerned enough about $332->$320 move to pay ~$9.40/share for insurance

- The timing (3 days pre-earnings) shows they see binary risk around 2026 guidance

- $320 strike sits right at major gamma support - expects that IF stock breaks, it goes there quickly

The institutional thesis appears to be: TSMC fundamentals remain excellent - 2nm production underway, CoWoS sold out, 30%+ revenue growth achievable. But with stock at all-time highs and a major guidance event imminent, the risk/reward favors protection over aggressive new positioning.

If you own TSM:

- Consider trimming 15-25% at $330-335 levels to lock in gains

- If holding through earnings, watch $330 gamma support closely

- Protective puts at $320 strike mirror smart money positioning

If you're watching from sidelines:

- January 15th earnings call is the moment of truth - watch for 2026 guidance quality

- Post-earnings pullback to $320-330 would be solid entry for long-term position

- Looking for confirmation of: 25%+ revenue growth guidance, 59%+ gross margin, strong A16/N2P commentary

Key dates:

- January 15, 2026 - Q4 2025 Earnings Call (2026 guidance reveal)

- February 13, 2026 - This put trade expiration

- H2 2026 - A16 mass production begins

- April 2026 (Est.) - Q1 2026 Earnings

Final verdict: TSM's long-term AI chip story remains compelling - 2nm leadership, CoWoS dominance, 64-66% foundry market share. But at all-time highs with earnings in 3 days, the $4.7M put buy signals smart money is playing defense. Consider waiting for post-earnings clarity before adding exposure.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-score of 100.09 reflects this specific trade's size relative to recent TSM history - it does not imply the trade will be profitable. Always do your own research and consider consulting a licensed financial advisor before trading.

About Taiwan Semiconductor Manufacturing Company: TSMC is the world's largest dedicated chip foundry with mid-60s market share, manufacturing semiconductors for Apple, Nvidia, AMD, and other leading technology companies. Market cap of $1.68 trillion in the Semiconductor Manufacturing industry.