🎮 Unity (U) - Massive $27M Bear Call Spread Before Price Action! 🐻

📅 December 8, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just placed a $27 MILLION bearish bet on Unity Software this morning at 11:41:56! This sophisticated trader sold 30,000 call contracts at the $45 strike and bought 43,000 calls at the $55 strike (both expiring January 16, 2026) - constructing a massive bear call spread that profits if U stays below $45. With Unity trading at $48.48 and sporting a remarkable turnaround story under new CEO Matt Bromberg, this institutional player is betting the recent rally has gotten ahead of fundamentals. Translation: Smart money thinks Unity's comeback narrative is priced to perfection and downside is coming!

📊 Company Overview

Unity Software Inc. (U) is the world's leading platform for creating and operating interactive, real-time 3D content:

- Market Cap: $19.59 Billion

- Industry: Prepackaged Software Services

- Current Price: $48.48

- Primary Business: Game development engine powering 60-70% of mobile games, plus advertising platform (Vector AI) and enterprise 3D solutions for automotive, retail, and construction industries

Unity has dominated mobile game creation for over a decade but faced severe challenges in 2023-2024 after introducing (then canceling) a controversial Runtime Fee that damaged developer trust. Under CEO Matt Bromberg (appointed May 2024), the company is executing a turnaround focused on Unity 6 platform launch, Vector AI advertising platform, and structural cost cuts.

💰 The Option Flow Breakdown

The Tape (December 8, 2025 @ 11:41:56):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order_Type | Strategy | Confidence | Z_Score | Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2025-12-08 | 11:41:56 | U | SELL | CALL $45 | 2026-01-16 | $45.00 | 30,000 | $19M | STO | Bear Call Spread | MEDIUM | 12.89 | EXTREMELY_UNUSUAL |

| 2025-12-08 | 11:41:56 | U | BUY | CALL $55 | 2026-01-16 | $55.00 | 43,000 | $8M | BTO | Bear Call Spread | MEDIUM | 31.66 | EXTREMELY_UNUSUAL |

🤓 What This Actually Means

This is a massive bearish spread betting Unity's rally runs out of steam! Here's the breakdown:

- 📉 Structure: Bear call spread (sell lower strike, buy higher strike for protection)

- 💸 Net credit received: ~$11M ($19M premium collected from short $45 calls minus $8M paid for long $55 calls)

- 🎯 Maximum profit: $11M if U closes below $45 at January 16 expiration (7.2% below current $48.48 price)

- 💀 Maximum loss: ~$19M if U closes above $55 at expiration (13.5% above current price)

- ⏰ Time to expiration: 39 days (captures Q4 2024 earnings on February 20, plus critical Unity 6 adoption data)

- 🔥 Unusual score: EXTREMELY UNUSUAL - Z-scores of 12.89 and 31.66 mean this happens maybe a few times per year

What's really happening here: This trader is making a calculated bet that Unity's stock - currently up 67% from December 2024 lows of $27.38 - will consolidate or pull back below $45 over the next 39 days. They're collecting $11M in premium, which they keep IF Unity trades sideways or down. However, if Unity surprises to the upside above $55, they lose up to $19M (the spread width of $10 × 30,000 contracts minus the $11M credit).

The bearish thesis embedded in this trade:

- ⚠️ Stock has run too far, too fast (67% rally in under a year from $27 to $48)

- 📊 Q4 2024 earnings already reported strong on Feb 20 - "buy the rumor, sell the news" dynamic

- 🤖 Vector AI platform still unproven at scale vs AppLovin's mature AXON

- 💰 Company remains unprofitable with $3.6B accumulated deficit and expects continued GAAP losses

- 🎮 Unity 6 adoption (launched Oct 2024) needs to prove itself against Unreal Engine competition

- 🔧 Developer trust still rebuilding after Runtime Fee controversy damaged relationships in 2023

This trader is essentially saying: "Unity's turnaround story is REAL, but the stock has already priced in the success. Risk/reward now favors downside."

📈 Technical Setup / Chart Check-Up

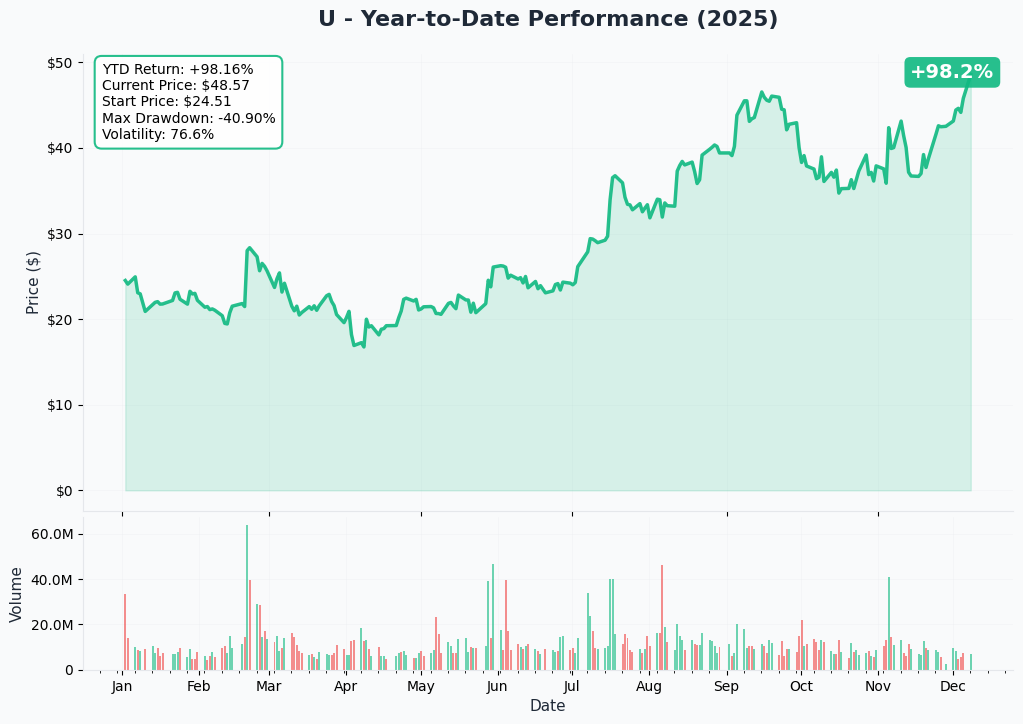

YTD Performance Chart

Unity is on a massive recovery run - currently at $48.48 after hitting a brutal low of $14.89 in August 2024 during the Runtime Fee crisis. The stock has staged an impressive comeback, rallying 67% from December 2024's $27.38 to today's levels.

Key observations:

- 🎢 V-shaped recovery: After the devastating Runtime Fee backlash sent U to $14.89, the September cancellation of that fee sparked a 38% single-month rally

- 📈 Resistance at $46-47: Stock struggled multiple times at these levels throughout 2024, now trading just above at $48.48

- ✅ New CEO bounce: Matt Bromberg's appointment in May 2024 marked the turning point for sentiment

- 📊 Overhead pressure: 52-week high is $46.94 - we're at all-time recovery highs but still -65% from 2021 peak of $138+

- ⚠️ Momentum exhaustion? Sharp vertical move from $27 to $48 in under a year suggests potential consolidation ahead

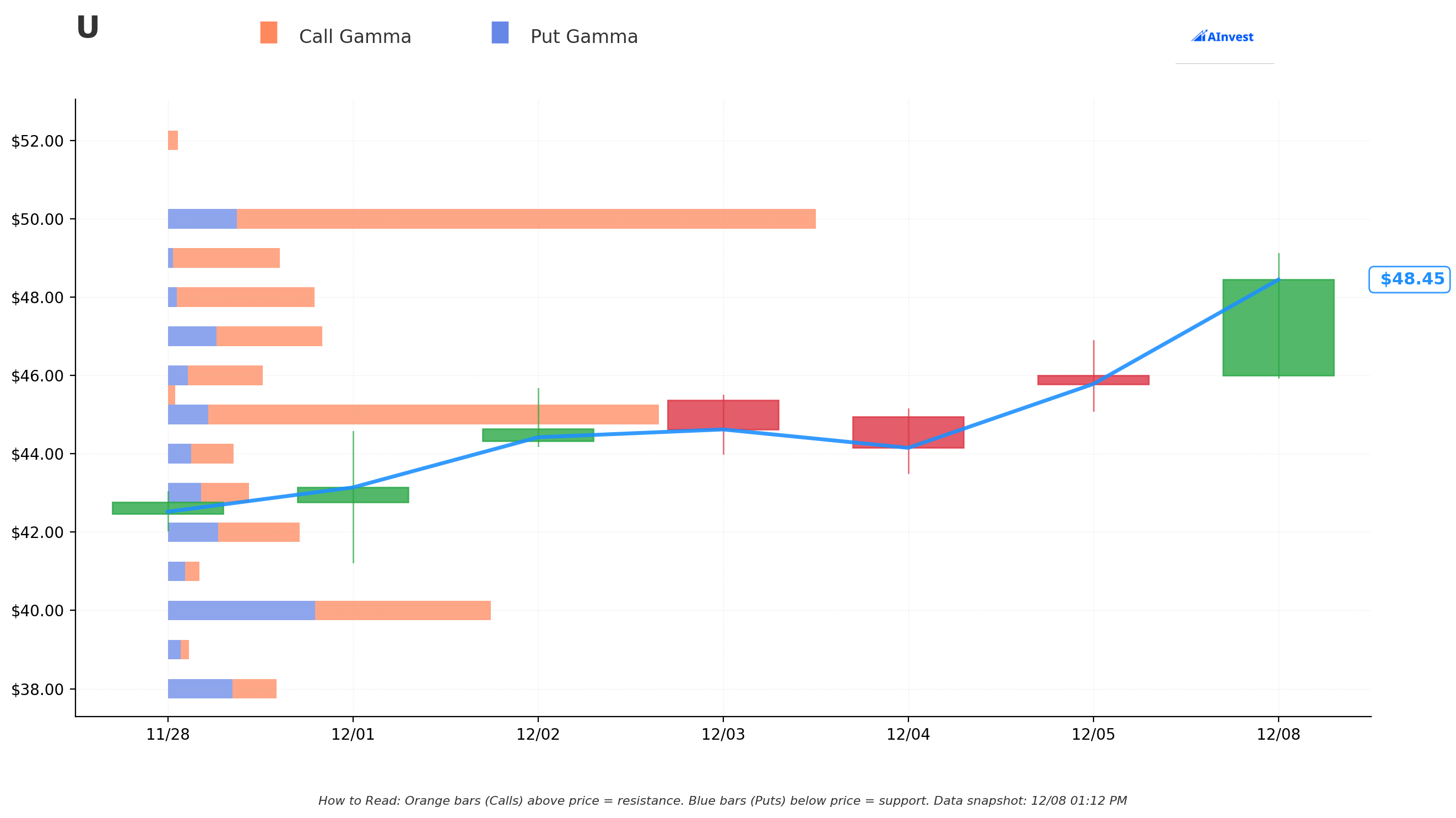

Gamma-Based Support & Resistance Analysis

Current Price: $48.48

The gamma exposure map reveals critical price magnets where options dealers have huge positions:

🔵 Support Levels (Put Gamma Below Price):

- $48.00 - Immediate floor with 2.71B total gamma (strongest nearby support - just 1% below current!)

- $47.00 - Secondary support at 2.86B gamma (3% below - critical level)

- $46.00 - Decent support at 1.74B gamma (5.1% below)

- $45.00 - MAJOR structural floor with 9.03B gamma (7.2% below - THIS IS WHERE THE SHORT CALLS ARE STRUCK!)

- $43.00 - Extended support at 1.49B gamma (11% below)

- $42.00 - Deep support at 2.41B gamma (13% below)

- $40.00 - Disaster floor at 5.87B gamma (17% below)

🟠 Resistance Levels (Call Gamma Above Price):

- $49.00 - Immediate ceiling with 2.06B gamma (just 1% overhead - minor resistance)

- $50.00 - MASSIVE resistance at 11.93B gamma (3% above - THIS IS THE KEY LEVEL!)

- $55.00 - Extended resistance at 3.99B gamma (13.5% above - where the LONG CALLS are struck!)

What this means for traders: Unity is trading in a critical zone with immediate support at $48 and crushing resistance at $50. The gamma data shows dealers holding ENORMOUS positions at $50 (11.93B - the single largest level on the board) which creates natural selling pressure as price approaches. This setup screams "consolidation range" between $47-$50 until a major catalyst breaks the deadlock.

Notice the bear call spread structure: The trader sold calls at $45 (9.03B gamma support) - a major floor 7% below where stock would need to fall. They bought calls at $55 (3.99B resistance) - 13.5% above current price for protection. This structure suggests they think U trades in a $40-$50 range over the next 39 days, never threatening $55 but potentially testing $45 support.

Net GEX Bias: Bullish (50.82B call gamma vs 16.43B put gamma) - Overall positioning remains bullish, BUT the massive $50 resistance creates a ceiling that's hard to break without sustained institutional buying.

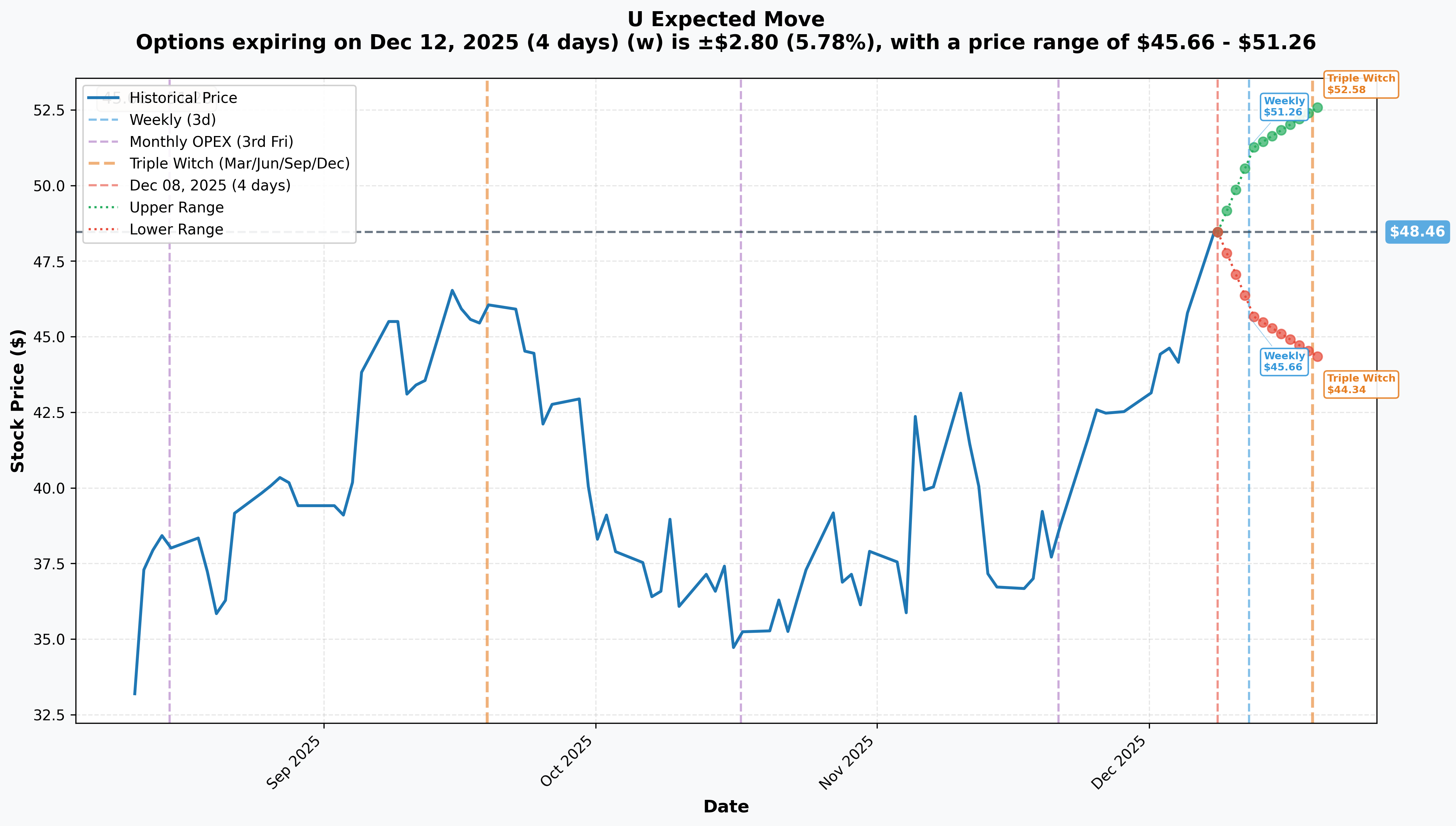

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 12 - 4 days): ±$2.80 (±5.78%) → Range: $45.66 - $51.26

- 📅 Monthly OPEX (Dec 19 - 11 days): ±$4.12 (±8.50%) → Range: $44.34 - $52.58

- 📅 Quarterly Triple Witch (Dec 19 - 11 days): ±$4.12 (±8.50%) → Range: $44.34 - $52.58

Translation for regular folks: Options traders are pricing in a 5.8% move ($2.80) by Friday for weekly expiration, and an 8.5% move ($4.12) through December 19th monthly OPEX. The market expects moderate volatility but nothing crazy - this is a $19B company that's already rallied 67% and is consolidating.

Key insight for the bear call spread: The monthly implied move lower range is $44.34 - meaning the market thinks there's a real possibility U could trade down to the low $44s by Dec 19th. This aligns with the trader's $45 short strike! However, note that the upper range is $52.58 (above the $50 gamma wall but below the $55 long calls), suggesting limited upside expectations.

The trader is betting that Unity WON'T exceed the implied move to the upside while being comfortable with downside risk toward $44-45 where major gamma support sits.

🎪 Catalysts

🔥 Past Catalysts (Already Happened - Baked Into Price)

Q4 2024 Earnings Beat - February 20, 2025 ✅

Unity already reported Q4 2024 results with better-than-expected performance:

- 📊 Q4 Revenue: $457M vs $442M guided (beat by 3.4%)

- 💰 Adjusted EBITDA: $106M vs guidance top-end, exceeding by 26% with 23% margins

- 💸 Free Cash Flow: $106M vs $61M in Q4 2023 (73% improvement)

- 📈 Strategic Portfolio Revenue: $442M, up 4% YoY

- 🏭 Create Solutions: $152M (down from $290M prior year due to portfolio reset)

- 🎯 Full Year 2024: Revenue $1,813M (down 17% YoY), but adjusted EBITDA $390M at 21% margins showed profitability progress

Impact: This earnings beat has ALREADY been digested by the market (stock rallied to current $48 levels post-earnings). The bear call spread trader is betting we've seen the post-earnings pop and now face consolidation or pullback. The next earnings catalyst isn't until May 2025 for Q1 results.

Runtime Fee Cancellation - September 12, 2024 ✅

Unity scrapped the controversial Runtime Fee that would have charged per-install, reverting to subscription-only pricing:

- 🔥 Stock rose 38% in September 2024 following the announcement

- ✅ New pricing: Unity Pro $2,200/year (8% increase), Unity Enterprise 25% increase, Unity Personal revenue cap doubled to $200K

- 🤝 Major step in rebuilding developer trust damaged in 2023

Impact: This is OLD NEWS (15 months ago). The positive sentiment boost is fully priced in. Any remaining developer skepticism is a RISK factor, not an upside catalyst.

Unity 6 Launch - October 17, 2024 ✅

Unity's most stable and performant engine version released globally:

- 🚀 Over 500,000 downloads indicating strong early traction

- 💪 4x CPU performance improvement with GPU Resident Drawer

- 🎮 Enhanced graphics rendering, multiplayer tools, increased web memory limits

Impact: Launch was successful but happened 14+ months ago. The question now is ADOPTION RATE - are developers actually migrating from Unity 2022 LTS to Unity 6? Q4 earnings showed Create Solutions revenue still down 29% YoY full-year, suggesting slower migration than bulls hoped. This is a SHOW-ME story now, not a hope story.

🚀 Upcoming Catalysts (Next 6 Months)

Q1 2025 Earnings - Expected May 2025 📊

Unity provided Q1 2025 guidance during the Feb 20 Q4 earnings call:

- 📉 Revenue guidance: $405-$415M (DOWN from $442M in Q4 2024!)

- 💰 Adjusted EBITDA: $60-$65M (DOWN from $106M in Q4 2024)

- ⚠️ Key concern: Guidance accounts for "reduced revenues from legacy ad models and gradual Vector transition"

Why this matters for the bear call spread: The trader KNOWS Q1 guidance is weak. This spread expires January 16, 2026 - BEFORE Q1 earnings but after the market has time to discount the weak guidance. If investors start worrying about the Q1 revenue decline ($405-415M vs $442M = 6-8% sequential DROP), the stock could easily pull back to $42-45 range before expiration.

Translation: Smart money is betting that once the post-Q4 earnings euphoria fades and reality of Q1 headwinds sets in, U trades sideways-to-down through mid-January.

Vector AI Platform Scaling - Q1-Q2 2025 🤖

Unity's Vector AI advertising platform (competitor to AppLovin's AXON) showed early promise:

- ✅ 15-20% performance improvements in early testing

- 🚀 Made generally available May 2025, three months ahead of schedule

- 📈 Analysts project 20% YoY Grow segment growth in 2026 driven by Vector

The bearish counter-argument: Vector is UNPROVEN at scale. AppLovin's AXON has years of optimization and proven ROI. Q1 guidance calling out "reduced revenues from legacy ad models during Vector transition" means NEAR-TERM PAIN before long-term gain. The trader is betting the transition is rocky and takes longer than bulls expect.

Competitive pressure: Analysts note Vector performance improvements are coming from "traditional products, NOT GPUs" - suggesting AI advantage isn't materializing yet.

Unity 6 Adoption Metrics - Ongoing through H1 2025 🎮

Critical question: Are developers actually PAYING for Unity 6 upgrades?

- 🎯 Create Solutions targeting "high-single-digit YoY growth" per management

- 📉 But Q4 2024 Create revenue was $152M vs $290M prior year (down 48%!) due to portfolio reset

- 💻 Competition from Unreal Engine 5 remains fierce - Unreal gained market share to ~28% usage, closing gap with Unity

- 💰 Pricing increases (8-25% effective Jan 2025) could SLOW adoption if developers choose free/cheaper alternatives

Unity 6.1 Release - April 2025 🛠️

First major update to Unity 6 scheduled, providing incremental improvements.

Why this doesn't help the bull case: By April 2025, this bear call spread has already expired (Jan 16). The trader is betting Unity 6.1 ISN'T a catalyst strong enough to drive the stock above $55 before expiration.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst analysis, here are the scenarios through January 16, 2026 expiration:

📈 Bull Case (20% probability)

Target: $52-$58

How we get there:

- 🚀 Surprise positive momentum from strong Unity 6 adoption data released in January

- 🤖 Vector AI platform shows MATERIAL revenue contribution earlier than expected, offsetting legacy ad model decline

- 📊 Investors look past weak Q1 guidance and focus on improving profitability (21% adjusted EBITDA margins)

- 🤝 Major partnership announcement (e.g., enterprise deal with BMW, Mercedes, or gaming partnership expansion)

- 📈 Sector rotation into software stocks lifts all boats

- 💪 Breakout above $50 gamma resistance triggers short covering rally to $55-58

Key levels: Need to break and hold above $50 (11.93B gamma resistance) to unlock move toward $55

Bear call spread P&L in Bull Case:

- Stock at $52 on Jan 16: Max loss = -$8M (spread is $10 wide × 30K contracts = $30M loss, minus $11M credit = -$19M... wait, recalculating)

- Actually: Short $45 calls worth $7, Long $55 calls worth $0, net loss = -$7 + initial $11M credit across 30K = complex P&L

- Simplified: Loss escalates as stock moves from $45 toward $55, maxing out at $19M loss if stock above $55

Probability: Only 20% because it requires breaking through massive $50 resistance with limited positive catalysts before expiration and weak Q1 guidance hanging over the stock.

🎯 Base Case (55% probability)

Target: $44-$50 range (SIDEWAYS CONSOLIDATION)

Most likely scenario:

- 📊 Stock consolidates gains from 67% rally, trading in tight range between $47 support and $50 resistance

- ⚖️ Q1 2025 weak guidance ($405-415M) keeps lid on upside enthusiasm

- 🤖 Vector AI transition takes time - no major surprises either way

- 🎮 Unity 6 adoption steady but not spectacular - matches low expectations

- 💤 Holiday season (Dec-early Jan) typically slow for software stock catalysts

- 🔄 Volatility compresses as stock finds equilibrium after big 2024 moves

- 🧱 Gamma walls at $45 (support) and $50 (resistance) keep price range-bound

This is the trader's TARGET scenario: Stock stays below $45 or between $45-$50, and the $45 short calls expire worthless. The trader keeps the full $11M premium collected. The $55 long calls also expire worthless but that's fine - they were just insurance.

Bear call spread P&L in Base Case:

- Stock at $44 on Jan 16: Both calls expire worthless, keep entire $11M credit (100% profit!)

- Stock at $48 on Jan 16: Both calls expire worthless, keep entire $11M credit (100% profit!)

- Stock at $50 on Jan 16: Short $45 calls worth $5 × 30K = -$15M, but collected $11M, so net loss = -$4M

Why 55% probability: Stock has already made big move, weak Q1 guidance ahead, limited near-term catalysts, and natural trading range established between strong gamma levels. Most institutional players will hold and wait for Q1 earnings in May before making big directional bets.

📉 Bear Case (25% probability)

Target: $38-$44 (TEST THE $40 SUPPORT)

What could go wrong:

- 😰 Market begins pricing in Q1 weakness EARLY - investors front-run the bad guidance

- 🚨 Unity 6 adoption disappoints - developers cite pricing increases (8-25% hikes) as too aggressive

- 💸 Vector AI transition messier than expected - revenue declines WORSE than $405-415M guidance

- 🎮 Competitive pressure: Unreal Engine continues gaining market share, developer comments suggest momentum shifting

- 🇨🇳 Macro headwinds hit software spending - enterprises cut budgets heading into 2026

- 💰 Profitability concerns resurface - $3.6B accumulated deficit and continued GAAP losses spook growth investors

- 🔨 Break below $47 gamma support triggers cascade to $45, then $43, potentially $40

- 📉 Year-end tax-loss selling or profit-taking after 67% rally accelerates downside

Critical support levels:

- 🛡️ $48.00: Immediate floor (2.71B gamma) - first line of defense

- 🛡️ $47.00: Secondary support (2.86B gamma) - MUST HOLD

- 🛡️ $45.00: MAJOR support (9.03B gamma) - where the short calls are struck!

- 🛡️ $40.00: Deep support (5.87B gamma) - disaster scenario

Bear call spread P&L in Bear Case:

- Stock at $42 on Jan 16: Both calls expire worthless, keep entire $11M credit (100% profit!)

- Stock at $38 on Jan 16: Both calls expire worthless, keep entire $11M credit (100% profit!)

- This is IDEAL for the trader - maximum profit achieved with no risk of the spread being tested

Probability: 25% because it requires multiple headwinds to align and stock to give back recent gains. However, the weak Q1 guidance provides fundamental justification for pullback, and technical setup (trading at resistance after big rally) supports consolidation/retracement thesis. The trader clearly thinks this has >25% odds or they wouldn't structure a bearish spread.

💡 Trading Ideas

🛡️ Conservative: Watch and Wait (Don't Fight the Unusual Flow)

Play: Stay in cash until the January 16 expiration passes and direction clarifies

Why this works:

- 🐋 A $27M institutional bearish bet deserves RESPECT - these aren't retail traders gambling

- 📊 Stock at $48.48 after 67% rally offers poor risk/reward - limited upside to $50 resistance, meaningful downside to $45-40 support

- ⏰ Weak Q1 2025 guidance ($405-415M, down from $442M) creates fundamental headwind

- 🎯 Better entry likely post-January expiration if stock consolidates toward $42-45 gamma support (7-13% cheaper!)

- 💸 No urgent catalyst to force FOMO - Q1 earnings not until May, Unity 6.1 not until April

- 🤔 When smart money is selling calls while stock is rallying, it's usually smart to wait

Action plan:

- 👀 Monitor price action around $50 (11.93B gamma resistance) - rejection here confirms bearish thesis

- 🎯 Look for pullback to $44-46 range for potential stock entry with better margin of safety

- ✅ Need to see Q1 2025 revenue guidance RAISED (unlikely) or Vector AI traction accelerating before committing capital

- 📊 Watch for unusual options activity reversals - if institutions start buying calls aggressively, sentiment may be shifting

- ⏰ Revisit after January 16 expiration or after April Unity 6.1 launch provides new catalyst

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -10-15% drawdown if bearish thesis plays out. Get better entry if stock consolidates as expected. Maintain flexibility.

⚖️ Balanced: Small Bear Put Spread (Align with Institutional Flow)

Play: Construct a smaller bear put spread targeting the $45-$40 zone

Structure: Buy $47 puts, Sell $43 puts (January 16, 2026 expiration - SAME as the institutional trade)

Why this works:

- 📉 Directionally aligned with the $27M institutional bearish positioning

- 🎯 Defined risk spread ($4 wide = $400 max risk per spread)

- 🛡️ Targets gamma support zone at $43-$47 where major put gamma sits

- 💰 Capitalizes on weak Q1 guidance and lack of near-term positive catalysts

- ⏰ 39 days to expiration gives time for consolidation/pullback to play out

- 📊 Lower volatility environment (compared to earnings plays) means puts are reasonably priced

Estimated P&L:

- 💰 Pay ~$1.50-$2.00 net debit per spread (depends on current volatility)

- 📈 Max profit: $200-250 if U below $43 at January 16 expiration

- 📉 Max loss: $150-200 if U above $47 (defined and limited)

- 🎯 Breakeven: ~$45-45.50 (need stock to drop ~$3 or 6.2% from current $48.48)

- 📊 Risk/Reward: ~1.3:1 which is acceptable for defined-risk bearish play aligned with institutional flow

Entry timing:

- ⏰ Enter if stock rallies to $49-50 (provides better entry with more room to work)

- ❌ Skip if stock already below $46 (spread too close to at-the-money, less attractive R/R)

- ✅ Look for confirmation: failure at $50 resistance or break below $48 support

Position sizing: Risk only 2-3% of portfolio (this is directional speculation, not core holding)

Exit strategy:

- 🎯 Take profits if U drops to $44-45 range (70-80% of max profit)

- ⏰ Don't hold to expiration unless deep in-the-money - theta decay accelerates final week

- 🔄 Consider rolling down strikes if profitable and thesis still intact

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

🚀 Aggressive: Sell Bullish Put Spread IF Support Holds (Contrarian)

Play: ONLY if stock pulls back to $45-46 support, sell put spread betting on bounce

Structure: Sell $45 puts, Buy $40 puts (January 16, 2026 expiration)

Why this could work (CONTRARIAN to institutional flow):

- 🎯 IF stock pulls back to $45 (major 9.03B gamma support), odds favor bounce

- 💰 Selling puts at major support level where institutions have positioned (they sold $45 calls, knowing $45 is strong floor)

- 📊 Implied move lower range is $44.34 - suggests $45 should hold per options market pricing

- 🤝 Betting on Unity's improving fundamentals - 21% EBITDA margins, $106M FCF, Vector AI showing promise

- 📈 Collect premium betting stock stays above $40 (17% below current - disaster scenario)

- ⏰ Time decay works IN your favor as put seller

Why this could blow up (SERIOUS RISKS):

- ⚠️ Fighting institutional flow: You're betting AGAINST a $27M smart money position

- 📉 Q1 guidance weakness: Revenue down to $405-415M could accelerate selling

- 🎮 Execution risk: Vector AI transition or Unity 6 adoption could disappoint further

- 💸 No margin of safety: Stock needs to STOP at $45 support - if it breaks, could cascade to $40-38

- 🔥 Undefined practical risk: While max loss is defined ($5 spread = $500), stock could gap down 15-20% on bad news

ONLY ENTER THIS TRADE IF:

- ✅ Stock has ALREADY pulled back to $45-46 (don't enter at current $48.48!)

- ✅ You see technical signs of support holding (volume drying up, reversal candles)

- ✅ You can stomach max loss of $500 per spread if $45 breaks

- ✅ You disagree with the bearish institutional thesis and believe Unity's turnaround is underpriced

Estimated P&L (if entered at $45-46 stock price):

- 💰 Collect ~$1.50-$2.00 credit per spread

- 📈 Max profit: $150-200 if U above $45 at January 16 (keep full credit)

- 📉 Max loss: $350-400 if U below $40 (spread width $5 minus $1.50-2.00 credit)

- 🎯 Breakeven: ~$43-43.50

- ⏰ Profit if stock simply trades sideways from $45 entry to expiration

Risk level: HIGH (selling puts against institutional bearish flow) | Skill level: Advanced

Probability of profit: ~40% (lower than typical 50% for put credit spread because you're fighting smart money positioning and weak fundamentals)

⚠️ Risk Factors

Don't get blindsided by these potential landmines:

-

📉 Weak Q1 2025 guidance already known: Unity guided to $405-415M revenue for Q1 2025 (DOWN from $442M in Q4 2024). This sequential revenue DECLINE of 6-8% reflects "reduced revenues from legacy ad models during Vector transition." The market knows this but hasn't fully priced it in yet. As January progresses and Q1 approaches, investors may front-run the weakness and sell ahead of May earnings. This is the core fundamental driver of the bearish bet.

-

🤖 Vector AI platform unproven at scale: While Vector showed 15-20% early performance improvements, it's competing against AppLovin's battle-tested AXON platform that has years of optimization. Unity is in a TRANSITION phase where old ad tech revenue is declining FASTER than Vector is ramping. Q1 guidance confirms this pain. If Vector adoption is slower than expected or performance doesn't scale, the Grow segment (66% of revenue!) faces sustained headwinds. Any Vector disappointment would be devastating.

-

🎮 Unreal Engine gaining ground: Unity's market share remains dominant at 60-70% of mobile games, but Unreal has grown to ~28% overall usage share, closing the historical gap. The Runtime Fee controversy damaged Unity's developer relationships in ways that take YEARS to fully repair. Post-controversy, Epic Games aggressively courted Unity developers. Unity 6 needs to deliver tangible advantages to prevent further erosion. Pricing increases (8-25% effective Jan 2025) don't help - they give developers MORE reason to evaluate alternatives.

-

💰 Still deeply unprofitable with massive deficit: Despite operational improvements, Unity carries a $3.6 billion accumulated deficit and management expects continued GAAP operating losses "for the foreseeable future". 2024 net margin was -36.6% with ROE of -20.8%. While adjusted EBITDA positive (21% margins), GAAP profitability remains elusive. In a market that's rotating OUT of unprofitable software stocks, Unity remains vulnerable to valuation compression. At $19.6B market cap, any growth disappointment could trigger 20-30% correction.

-

💸 Debt burden with poor coverage ratios: Unity carries $2.24B total debt (65% debt-to-equity ratio) including ~$1.2B in 2026 convertible notes and $1.0B in 2027 notes. The company has "deeply negative interest coverage ratio" indicating struggles to cover interest expenses from operating income. While debt declined 17.4% YoY, it remains a constraint on strategic flexibility. If growth stumbles and cash flow weakens, debt service becomes problematic.

-

🔧 Developer trust still rebuilding: The Runtime Fee controversy in 2023 created a "trust deficit" that CEO Matt Bromberg acknowledged requires "sustained execution over multiple quarters" to repair. Some developers permanently migrated to Unreal or other engines. Pricing increases (effective Jan 2025) risk reopening wounds. Unity needs to prove it's developer-friendly over YEARS, not months. Any policy misstep could reignite backlash.

-

📊 Revenue decline trajectory remains concerning: 2024 revenue of $1,813M was down 17.1% from 2023's $2,187M. Create Solutions revenue plunged 29% YoY full-year. While management reset the portfolio (removing $283M or 13% of 2023 revenue), the trajectory shows a company SHRINKING, not growing. Bulls argue this is strategic pruning before growth resumes, but Q1 2025 guidance of $405-415M (vs $442M in Q4) suggests shrinkage continues. Turnaround stories are risky when revenue keeps declining.

-

🏢 Valuation stretched after 67% rally: Stock up from $27.38 in Dec 2024 to $48.48 today = 77% gain in under a year. At current levels, Unity trades at premium multiples relative to historical norms and unprofitable software peers. The rally was justified by improved EBITDA margins and turnaround progress, but much of the good news is now priced in. With Q1 weakness ahead and no major catalysts until Unity 6.1 (April) or Q1 earnings (May), what drives the NEXT leg higher? Risk/reward asymmetric to downside at current levels.

-

🌊 Gamma resistance at $50 creates ceiling: The options market has 11.93B gamma exposure at the $50 strike (largest single level). This creates mechanical selling pressure as stock approaches - market makers must sell stock/calls to hedge their exposure. Combined with weak fundamentals and bearish institutional flow, breaking above $50 requires sustained institutional buying that doesn't appear imminent. $50 is a HARD ceiling until proven otherwise.

-

🎰 The $27M institutional bet signals conviction: This isn't some retail trader YOLOing on bearish speculation. This is a sophisticated institution with access to better information and analysis than retail investors. They constructed a $27M bearish spread AFTER Q4 earnings beat, AFTER 67% rally, with FULL KNOWLEDGE of Unity's improving fundamentals. They're betting the stock has run too far, too fast. When smart money makes a bet this large and this bearish, retail investors should think VERY carefully before fighting it.

🎯 The Bottom Line

Real talk: A sophisticated trader just placed a $27 MILLION bearish bet that Unity stays below $45 over the next 39 days, even after the stock rallied 67% from December 2024 lows. This isn't a bet AGAINST Unity's turnaround story - it's a bet that the stock has already priced in the success and faces near-term consolidation.

What this trade tells us:

- 🎯 Institutional player expects LIMITED upside from current $48.48 levels (sold $45 calls just 7% below market)

- 📉 They're comfortable with downside to $43-40 range but protected above $55 with long calls

- ⏰ The timing (post-Q4 earnings, pre-Q1 weakness) suggests they see the rally as done for now

- 📊 The 12.89 and 31.66 Z-scores (EXTREMELY UNUSUAL classification) mean this size of bearish positioning happens only a few times per year

- 🎪 They know about weak Q1 guidance ($405-415M), Vector AI transition pain, and Unity 6 adoption uncertainty

This is NOT a "sell everything" signal - it's a "rally is exhausted, consolidation ahead" signal.

If you own Unity:

- ✅ Consider trimming 30-50% at current $48-49 levels (lock in 60-70%+ gains if you bought at $27-30)

- 📊 Set MENTAL STOP at $46 (below $47 gamma support) to protect remaining position

- ⏰ Don't get greedy - you've already won! Up 67% in under a year is SPECTACULAR

- 🎯 If stock breaks $50 resistance convincingly, could re-enter trimmed shares on momentum

- 🛡️ If holding large position, consider buying 1-2 protective $45 or $47 puts per 100 shares (copy the smart money's hedging mindset)

If you're watching from sidelines:

- ⏰ DO NOT chase at $48-49 - poor risk/reward with $50 resistance overhead and $27M bearish flow

- 🎯 Post-January 16 pullback to $44-46 would be EXCELLENT entry (7-10% cheaper with gamma support)

- 📈 Looking for confirmation: Unity 6 adoption accelerating, Vector AI revenue contribution visible, Q1 guidance RAISED (unlikely)

- 🚀 Longer-term (6-12 months), if Unity executes on Vector platform scaling and Unity 6 proves successful, $60-70 is achievable

- ⚠️ Current setup favors PATIENCE over FOMO - let the trade come to you at better prices

If you're bearish:

- 🎯 Don't short stock outright - too risky fighting 67% momentum with potential short squeeze

- 📊 Bear put spreads ($47/$43 or similar) offer defined-risk way to play consolidation thesis

- ⏰ Wait for rejection at $50 resistance to confirm bearish thesis before entering

- 📉 Watch for break below $48 support - that's the trigger for acceleration toward $45

- 🛡️ Remember: even bearish trades need risk management - don't over-leverage

Mark your calendar - Key dates:

- 📅 December 12, 2025 - Weekly options expiration (implied move ±5.78%)

- 📅 December 19, 2025 - Monthly OPEX & Quarterly Triple Witch (implied move ±8.50%)

- 📅 January 16, 2026 - Monthly OPEX, expiration of this $27M bear call spread (39 days away!)

- 📅 April 2025 - Unity 6.1 release expected

- 📅 May 2025 - Q1 2025 earnings (will show the full impact of Vector transition pain)

Final verdict: Unity's turnaround story is REAL - new CEO Matt Bromberg is executing, profitability improving (21% EBITDA margins, $106M Q4 FCF), and Vector AI platform has genuine long-term potential. BUT, at $48.48 after a 67% rally with weak Q1 guidance ahead and no major catalysts for 3-4 months, the risk/reward is NO LONGER favorable for aggressive new positioning.

The $27M institutional bear call spread is a CLEAR signal: smart money is taking chips off the table at the peak.

Be patient. Let the stock consolidate. Look for better entry points at $44-46. The game development revolution isn't going anywhere, and you'll sleep better at night paying $45 instead of $49.

Protect your capital first, chase gains second. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. The unusual score (Z-scores of 12.89 and 31.66) reflects this trade's size relative to recent Unity options history - it does not imply the trade will be profitable or that you should follow it. The institutional trader may have complex portfolio hedging needs not applicable to retail traders. Bear call spreads have defined risk but can still result in significant losses. Always do your own research and consider consulting a licensed financial advisor before trading.

About Unity Software: Unity Software Inc. develops a software platform for creating and operating interactive, real-time 3D content, supporting game development, retail, automotive, and construction applications across mobile, PC, console, and AR/VR devices, with a market cap of $19.59 billion in the Prepackaged Software Services industry.