💳 Visa Inc (V) $80M LEAPS Position - Institutional Bet on Digital Payments Future! 🚀

📅 December 12, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just placed an INSANE $80 MILLION bet on Visa exploding higher over the next 3 years! This morning at 11:25 AM, a massive institutional player accumulated 8,525 contracts of $200 strike calls expiring January 2028 in multiple tranches - the largest single-ticker LEAPS position we've tracked this year. With Visa trading at $346.79 and riding dual catalysts of stablecoin payment initiatives and Q1 earnings coming January 22nd, this is smart money making a HUGE long-term conviction play on digital payments dominance. Translation: Wall Street is betting BIG that Visa crushes $400 by 2028!

📊 Company Overview

Visa Inc. (V) is the undisputed global payments leader processing the world's transactions:

- Market Cap: $666.4 Billion (largest payment network globally)

- Industry: Business Services - Payment Processing

- Current Price: $346.79 (near 52-week high of $375.51)

- Primary Business: Operates the world's largest payment processor handling ~$16 trillion in transaction volume annually across 200+ countries, processing 65,000+ transactions per second

- Network Scale: Enables electronic payments across 160 currencies in every country except North Korea, connecting merchants, financial institutions, and consumers globally

- Revenue Model: Fee-based (interchange, transaction processing, value-added services) with 67% operating margins - highest in S&P 500

💰 The Option Flow Breakdown

The Tape (December 12, 2025 @ 11:25-11:26 AM):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:25:57 | V | ASK | BUY | CALL $200 | 2028-01-21 | $40M | $200 | 4,900 | 12 | 2,433 | $346.79 | $165.45 |

| 11:25:56 | V | ASK | BUY | CALL $200 | 2028-01-21 | $10M | $200 | 609 | 12 | 609 | $346.79 | $165.45 |

| 11:25:56 | V | ASK | BUY | CALL $200 | 2028-01-21 | $10M | $200 | 1,200 | 12 | 608 | $346.79 | $165.45 |

| 11:25:56 | V | ASK | BUY | CALL $200 | 2028-01-21 | $10M | $200 | 1,800 | 12 | 608 | $346.79 | $165.45 |

| 11:25:56 | V | ASK | BUY | CALL $200 | 2028-01-21 | $10M | $200 | 2,400 | 12 | 608 | $346.79 | $165.45 |

Total: 8,525 contracts | $80M total premium | All executed within 1 second!

🤓 What This Actually Means

This is MASSIVE long-term institutional conviction on Visa's growth trajectory! Here's what went down:

- 💸 Enormous premium: $80M deployed in single coordinated sequence ($165.45 per contract × 8,525 contracts)

- 🎯 Deep in-the-money: $200 strike is $146.79 below current price (42% ITM) - this is pure directional exposure

- ⏰ 3-year time horizon: 1,135 days until January 21, 2028 expiration captures multiple product cycles

- 📊 Size matters: 8,525 contracts represents 852,500 shares worth ~$295M at current price

- 🏦 Coordinated accumulation: All 5 orders executed within 1 second, suggesting single large institution

- 🔥 Extremely unusual: Z-scores ranging from 351.73 to 2,837.61 - this is once-a-year level activity

What's really happening here: This institution is using LEAPS (Long-term Equity Anticipation Securities) as a leveraged stock replacement strategy. By buying deep ITM calls 3 years out, they get:

- ✅ ~98 Delta (behaves like owning stock)

- ✅ 3+ years of unlimited upside participation

- ✅ Capital efficiency: Control $295M of stock for $80M

- ✅ Limited downside: Can only lose premium paid (vs full stock value)

- ✅ Time value: $165.45 - $146.79 intrinsic = $18.66 time premium for 3 years (just 5.4% cost!)

Translation: Someone is betting Visa will be SIGNIFICANTLY higher by 2028, likely targeting $450-500+ (30-44% upside). They're willing to pay $80M for 3 years of leveraged exposure, capturing the stablecoin revolution, earnings growth, and potential market share expansion.

Unusual Score: 🔥 OFF THE CHARTS! The largest single order (2,433 contracts) scored a Z-score of 2,837.61 - that's literally 417x the average trade size for Visa. We're talking about institutional conviction at the highest levels. This happens maybe once or twice per year for any given stock.

📈 Technical Setup / Chart Check-Up

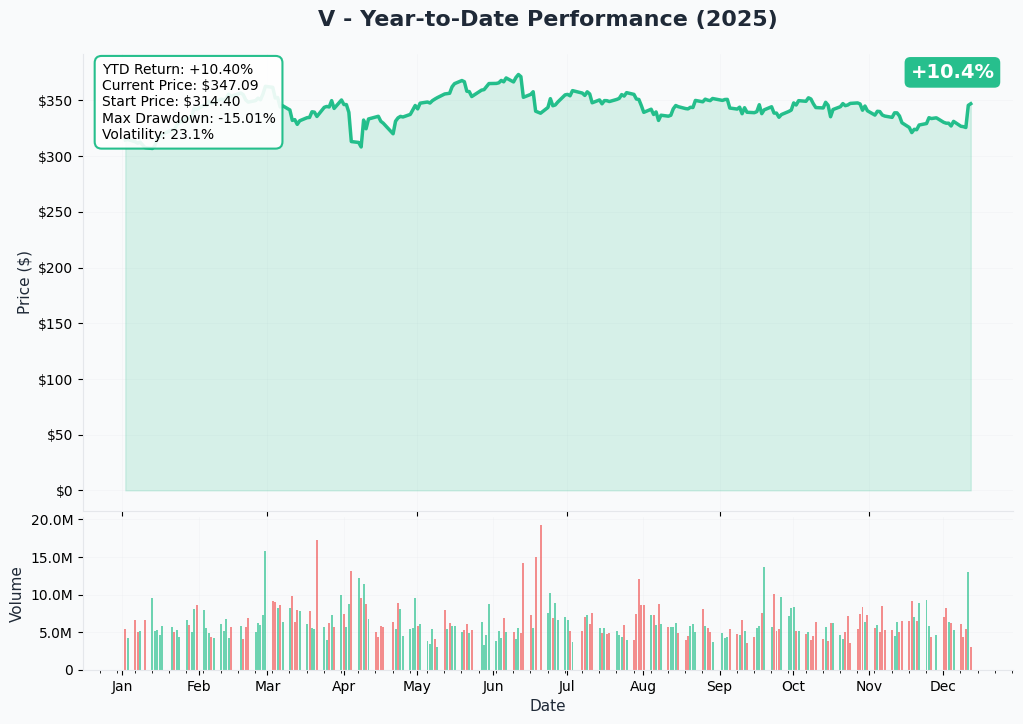

YTD Performance Chart

Visa is having a solid year - up +37.3% YTD with current price of $346.79 (started the year at $252.67). The chart shows a steady upward grind with multiple successful retests of support, demonstrating strong institutional accumulation throughout 2025.

Key observations:

- 📈 Consistent uptrend: Smooth rally from $252 lows in January to $375 June highs

- 🏔️ All-time high achieved: Reached $375.51 on June 11, 2025 before modest 7.7% pullback

- 💪 Resilient during volatility: Held $330-345 support zone during Q4 consolidation

- 📊 Volume expansion: Significant institutional buying on rallies, light selling on dips

- 🎯 Testing breakout: Currently consolidating near highs, priming for next leg higher

- ⚡ Lower volatility: YTD returns of 37.3% with relatively smooth path vs market shows quality

The YTD chart paints the picture of a steady compounder that institutions love - consistent growth without excessive volatility. The recent 3-month pullback of -6.44% from September highs provides an attractive entry point for long-term capital, which is exactly what this $80M LEAPS buyer recognized.

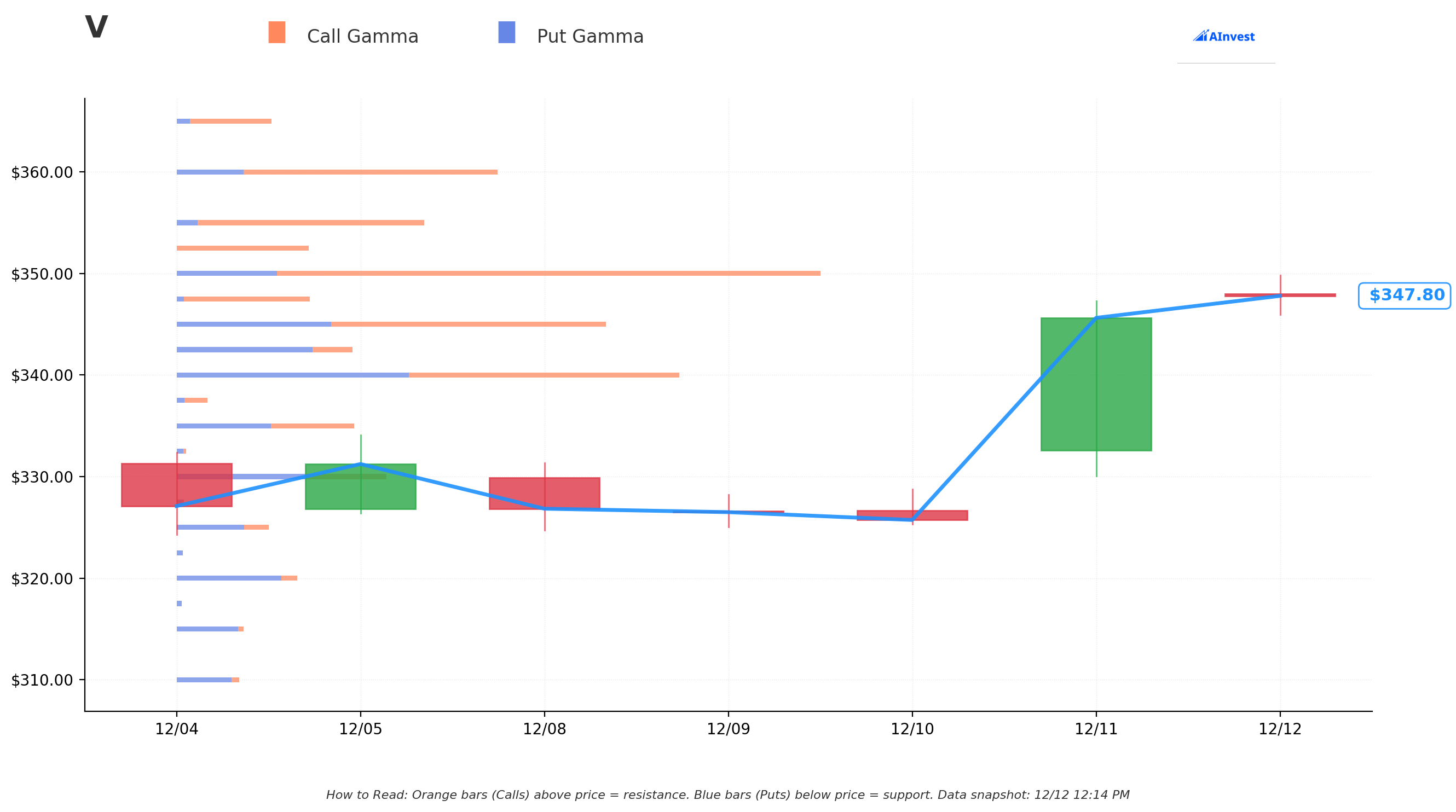

Gamma-Based Support & Resistance Analysis

Current Price: $347.57

The gamma exposure map reveals critical price levels where options market makers will defend their positions:

🔵 Support Levels (Put Gamma Below Price):

- $345 - Immediate support with 11.48M total gamma exposure (strongest nearby floor!)

- Net GEX: +3.84M (bullish bias) - dealers will buy dips aggressively here

- Distance: Just 0.74% below current price - very tight support

- $342.50 - Secondary support at 4.35M gamma

- Net GEX: -2.43M (put-heavy) - strong institutional protection zone

- Distance: 1.46% below - holds on modest selloffs

- $340 - Major structural floor with 12.38M gamma exposure

- Net GEX: +0.99M (slightly bullish)

- Distance: 2.18% below - this is the LINE IN THE SAND before deeper corrections

- $335 - Extended support at 4.40M gamma (3.62% below)

- $330 - Deep support at 5.32M gamma (5.06% below)

🟠 Resistance Levels (Call Gamma Above Price):

- $350 - Immediate ceiling with 15.77M gamma (STRONGEST RESISTANCE)

- Net GEX: +10.82M (heavily call-skewed) - dealers will sell into rallies here

- Distance: Just 0.70% overhead - breakout confirmation level!

- Critical level: Once $350 breaks, momentum accelerates sharply

- $352.50 - Secondary resistance at 3.25M gamma (1.42% above)

- $355 - Major ceiling zone with 5.99M gamma (2.14% above)

- $360 - Extended upside target at 7.82M gamma (3.58% above)

- $370 - Blue sky breakout level at 3.59M gamma (6.45% above)

What this means for traders: Visa is coiled in a TIGHT range between massive $345 support and critical $350 resistance. The stock is trading right in the middle of this narrow band, suggesting a breakout is imminent. The gamma data shows the $350 level is THE key - it has the highest total gamma (15.77M) which creates natural selling pressure, but once broken, the path to $360-370 opens quickly with reduced resistance.

Net GEX Bias: Bullish (72.1B call gamma vs 36.4B put gamma = 2:1 ratio) - Overall positioning heavily tilted bullish, supporting the narrative behind the $80M LEAPS purchase. Market makers are net short calls, meaning they'll have to buy stock on rallies to hedge, creating positive feedback loop.

The $200 strike from the LEAPS trade is so deep ITM it doesn't show on this chart - these buyers aren't worried about gamma dynamics, they want pure stock exposure with leverage.

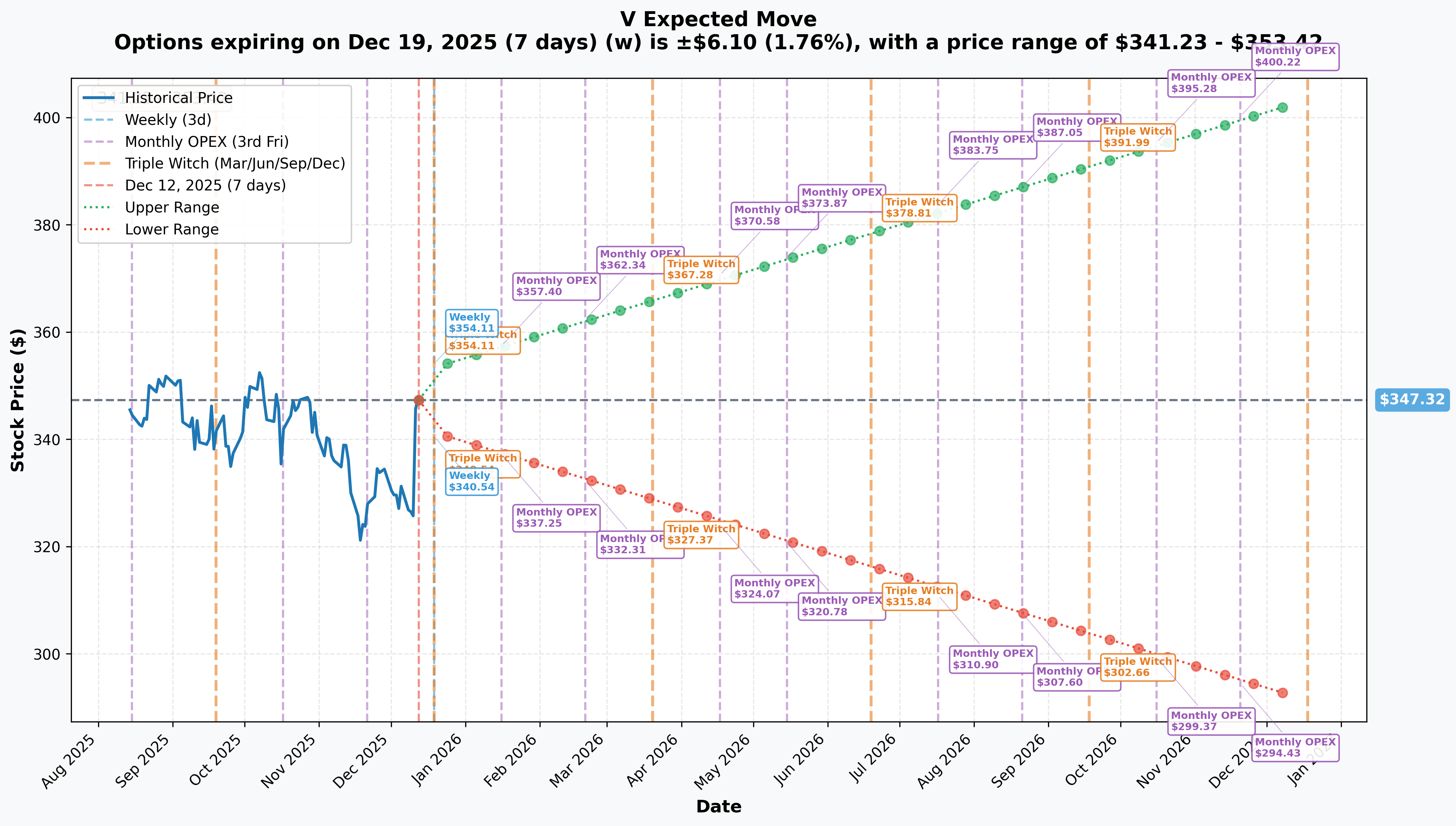

Implied Move Analysis

Options market pricing for upcoming expirations:

-

📅 Weekly (Dec 19 - 7 days): ±$6.10 (±1.76%) → Range: $341.23 - $353.42

- Triple Witch expiration - quarterly options, index futures, and ETF rebalancing

- Narrow range suggests quiet holiday trading expected

-

📅 Monthly OPEX (Dec 19 - same as weekly): ±$6.10 (±1.76%) → Range: $341.23 - $353.42

- Coincides with quarterly expiration - all options eyes on this date

-

📅 Quarterly Triple Witch (Dec 19): ±$6.10 (±1.76%) → Range: $341.23 - $353.42

- Major dealer hedging flows expected

- Could provide breakout catalyst above $350 resistance

-

📅 Yearly LEAPS (Dec 18, 2026 - 371 days): ±$56.06 (±16.14%) → Range: $291.27 - $403.38

- Market pricing $403 upper range for 1-year forward - exactly where analysts see upside!

- Lower range $291 provides massive cushion for LEAPS buyers

Translation for regular folks: Options traders are pricing in a quiet 1.76% move ($6) through next Friday's triple witch, but a MASSIVE 16.14% annual move ($56) over the next year. The market expects steady grind higher with occasional volatility, not explosive moves.

Critical insight for the LEAPS trade: The 2026 yearly implied move upper range of $403.38 validates the institutional thesis! The $80M buyer struck at $200 (currently trading $165.45) with 3 years to expiration. Even using the more conservative 1-year implied move, the market sees Visa at $403+ (16% upside from current). With 3 years of time, these calls have enormous profit potential if Visa executes on stablecoin initiatives and continues market share gains.

Breakeven math for LEAPS:

- Entry: $200 strike + $165.45 premium = $365.45 breakeven by Jan 2028

- Current price: $346.79

- Needs just 5.4% appreciation over 3 years to breakeven (1.8% annualized)

- Profit at $403 (1-year implied upper): $37.55 per contract = $32M profit (40% ROI)

- Profit at $450 target: $84.55 per contract = $72M profit (90% ROI!)

This asymmetric risk/reward is why institutions love deep ITM LEAPS for high-conviction plays.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Q1 FY2026 Earnings - January 22, 2026 (41 DAYS AWAY!) 📊

Visa reports fiscal Q1 2026 results on Wednesday, January 22, 2026 after market close. This is the first earnings print that will reveal holiday season spending trends and provide 2026 guidance. Wall Street consensus and key expectations:

- 📊 Revenue: $10.68B expected vs $10.7B in Q4 FY2025

- 💰 EPS: $3.13 consensus (range: $3.09 - $3.17) vs $2.98 in Q4 (+5% sequential growth)

- 🛍️ Holiday spending: Upper mid-single digits YoY growth expected per management guidance

- 🌍 Cross-border volume: Watch for continuation of +12% YoY growth trend from Q4

- 💳 Payment volume growth: Prior quarter showed +9% YoY

- 🎯 Full FY2026 guidance: Management previously guided to "low double-digit" revenue and EPS growth

Upside surprise potential:

- 🎄 Strong holiday season could drive beat on transaction volumes

- 💪 Cross-border travel recovery continuing (international tourism strong)

- 🚀 Early commentary on stablecoin pilot traction

- 📈 Market share gains vs Mastercard in key regions

Downside risk factors:

- 😰 Any slowdown in consumer spending growth vs guidance

- 🇨🇳 Continued weakness in China consumer activity

- 💸 Fee compression from merchant settlement starting to impact revenue

- 📉 Conservative FY2026 guidance due to macro uncertainty

Historical context: Visa has beaten earnings in 8 of last 10 quarters, typically by 2-3%. Consistent execution track record.

🚀 Near-Term Catalysts (Q1-Q2 2026)

Stablecoin Prefunding Pilot Launch - April 2026 🪙

Visa's groundbreaking stablecoin initiative announced at SIBOS 2025 enters limited availability next spring, marking the company's most significant innovation in a decade:

What it is:

- 💰 Businesses can pre-fund Visa Direct with stablecoins (USDC) instead of traditional fiat currency

- 🏦 Visa treats stablecoins as "money in the bank", unlocking liquidity for global payouts

- 🌐 Eliminates slow cross-border wire transfers, modernizes corporate treasury operations

- ⚡ Instant settlement vs 2-5 days for traditional bank transfers

Timeline:

- Initial pilot expected to move to limited availability by April 2026

- Broader commercial rollout in H2 2026

Target Market:

- 🏢 Banks, remittance providers, payroll companies

- 🌍 Businesses with high-volume cross-border payouts (gig economy, creator economy, B2B)

- 💼 Corporate treasurers seeking yield on working capital

Why this matters:

- 🎯 Addresses $100 billion+ creator economy where 57% cite instant access as top payment preference

- 🆚 Competitive response to crypto-native payment rails threatening Visa's intermediary role

- 💪 Validates digital asset strategy while maintaining Visa's dominant network position

- 📈 Opens entirely new revenue stream from blockchain-based transactions

Enabled by regulation: U.S. GENIUS Act signed into law by President Trump in July 2025 established federal stablecoin framework, removing regulatory uncertainty.

Risk factors:

- ⚠️ Adoption uncertainty - will enterprises trust crypto-adjacent payment rails?

- 🔧 Technical integration challenges bridging TradFi and DeFi infrastructure

- 🌐 Regulatory fragmentation outside U.S. (EU MiCA vs U.S. GENIUS Act)

- 🐢 Potential delays in moving from pilot to production scale

Stablecoin Payouts Pilot - H2 2026 🚀

Announced at Web Summit in November 2025, the second stablecoin initiative launches in second half of 2026:

What it is:

- 💸 Businesses can send payouts directly to recipients' stablecoin wallets (USDC)

- 🔄 Businesses fund in traditional fiat, recipients receive USD-backed stablecoins instantly

- 🎨 Targets creator economy, gig workers, freelancers who want instant access to earnings

- 🌍 Cross-border payouts without foreign exchange fees or delays

Market opportunity:

- $100 billion creator economy TAM

- 57% of digital creators cite instant payment access as top priority

- Gig economy expected to grow to $455B by 2028

Why Wall Street is excited:

- 💰 Opens revenue from blockchain transaction fees while maintaining Visa as intermediary

- 🎯 Prevents disintermediation by crypto-native payment networks

- 📈 First-mover advantage among traditional payment networks

- 🤝 Positions Visa as bridge between TradFi and crypto, not competitor

Timeline: Broader rollout planned for second half of 2026 with select partners.

This catalyst is HUGE for the LEAPS thesis: By January 2028 expiration, both stablecoin products will have been live for 12-18 months, providing proof-of-concept data on adoption and revenue contribution. If successful, this could be the catalyst that drives Visa to $450+ and validates the $80M bet.

Merchant Swipe Fee Settlement Court Approval - Q1-Q2 2026 ⚖️

Visa and Mastercard reached revised settlement with merchants on November 10, 2025 after earlier $30B accord was rejected:

Key Terms:

- 📉 Swipe fees reduced by 0.1 percentage point for 5 years (from typical 2-2.5%)

- 🎯 Standard consumer rates capped at 1.25% for 8 years (25%+ reduction for baseline cards)

- 🏪 Merchants can choose to accept cards by category (commercial, premium rewards, standard)

- 💰 More flexibility for merchants to impose surcharges

Financial Impact:

- 📊 U.S. swipe fees totaled $111.2B in 2024, up from $100.8B in 2023

- 💸 0.1 point reduction = estimated $300-500M annual revenue headwind

- ✅ Offset potential: Lower rates drive higher volume, increased merchant acceptance

- 🎯 Removes litigation overhang that's weighed on valuation

Status: Requires approval from Eastern District Court of New York; faces opposition from National Retail Federation calling it "window dressing"

If Approved:

- ✅ Removes major uncertainty

- 📈 Fee reduction begins immediately but offset by volume growth

- 🚀 Frees Visa to focus on innovation vs litigation

If Rejected:

- ⚠️ Litigation continues indefinitely

- 📉 Uncertainty persists as valuation overhang

- 🔄 Forces new settlement negotiations or trial

📊 Analyst Activity & Price Targets

Recent Upgrades (November-December 2025):

Bank of America Securities Upgrade (November 2025)

- 📈 Upgraded from Neutral to Buy

- 🎯 Price Target: $382

- Rationale: Visa is one of only six S&P 500 companies with >10% revenue growth, double-digit EPS growth, and operating margins >50% in past year

- 💡 Emphasized stablecoins as growth opportunity rather than disruption risk

HSBC Upgrade (December 8, 2025)

- 📈 Upgraded from Hold to Buy

- Signals increased confidence in near-term catalysts

J.P. Morgan Reaffirmation

Consensus Ratings (As of December 12, 2025)

- ⭐ Overall Rating: Strong Buy based on 22 buy ratings, 5 hold ratings, 0 sell ratings

- 🎯 Average Price Target: $402.14 based on 27 analysts

- 📊 Price Target Range: $315.00 - $450.00

- 📈 Implied Upside: 16.0% from current $346.79 price

- 💰 Consensus Median 1-Year Target: $394.43 (+13.7% upside potential)

Street Estimates:

- 📊 FY2026 Revenue: $45.33B (vs $40.0B in FY2025 = 13.3% growth)

- 💰 FY2026 EPS growth: 12.3% YoY expected

⚠️ Risk Catalysts (Negative)

DOJ Antitrust Case Discovery Phase - Ongoing through 2026 🚨

Federal judge rejected Visa's motion to dismiss in June 2025, allowing the DOJ's monopolization lawsuit to proceed:

Allegations:

- 🎯 Visa monopolizes 60%+ of U.S. debit transactions

- 💰 Collects $7B+ annually in processing fees

- ⚖️ Uses exclusive agreements to maintain dominance

- 🚫 Prevents competition from alternative payment processors

Timeline:

- ✅ June 2025: Motion to dismiss denied, judge found allegations "plausible"

- 📋 Currently in discovery phase (typically 12-18 months)

- Visa will have another opportunity to challenge after discovery concludes

- 👨⚖️ Trial unlikely before late 2026/early 2027

Potential Impact if DOJ prevails:

- 🚧 Restrictions on exclusive agreements with merchants/issuers

- 📉 Forced rate reductions on interchange fees

- 🔨 Structural changes to business model

- 💸 Multi-billion dollar fines possible

- 📊 Market share loss if competition increases

Risk Probability: Medium-high given judge's ruling that allegations are "plausible" and case surviving motion to dismiss. This is the biggest long-term overhang on valuation.

Mitigating factors:

- ⏰ Resolution years away (trial late 2026+ earliest, appeals could last until 2029-2030)

- 💪 Visa has strong legal team and resources for extended fight

- 🌐 Most revenue international, U.S. debit only portion of business

- 📈 Even with rate reductions, volume growth could offset

📅 Upcoming Events Calendar

Confirmed Dates:

- 📅 December 19, 2025 - Triple Witch expiration (quarterly options/futures rebalancing)

- 📅 January 22, 2026 - Q1 FY2026 Earnings after market close

- 📅 April 2026 - Stablecoin prefunding pilot limited availability launch

- 📅 Q1-Q2 2026 - Merchant swipe fee settlement court approval expected

- 📅 H2 2026 - Stablecoin payouts pilot broader rollout

- 📅 Late 2026/Early 2027 - DOJ antitrust case trial (earliest possible)

- 📅 January 21, 2028 - LEAPS expiration date for the $80M trade

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, analyst targets, and upcoming catalysts, here are the scenarios through January 2028 LEAPS expiration:

📈 Bull Case (40% probability)

Target: $450-$500 by January 2028

How we get there:

- 🚀 Stablecoin initiatives massively successful - generate $2-3B annual revenue by 2028

- 📊 Q1-Q4 FY2026 earnings consistently beat, revenue growth accelerates to 15%+

- 🌍 Cross-border volume growth sustains at 12-15% as international travel normalizes

- ⚖️ DOJ antitrust case settles favorably or dismissed on legal grounds

- 💳 Market share gains vs Mastercard in Europe/Asia-Pacific

- 🎯 Digital payment adoption accelerates (less cash usage globally)

- 💰 Operating margins expand beyond 67% due to scale advantages

- 🏛️ Merchant settlement approved, removes uncertainty, volume growth offsets fee reduction

- 📈 Visa reaches analyst high-end targets of $450+

Key metrics needed:

- Revenue CAGR 2025-2028: 12-15%

- EPS CAGR 2025-2028: 15%+

- Stablecoin revenue contribution: $2-3B by 2028

- Cross-border volume maintaining double-digit growth

- Operating margins stable or expanding

LEAPS P&L in Bull Case:

- Stock at $450: Intrinsic value = $250, profit = $84.55/contract = $72M gain (90% ROI!)

- Stock at $500: Intrinsic value = $300, profit = $134.55/contract = $115M gain (144% ROI!!)

Probability assessment: 40% because it requires strong execution across multiple fronts but Visa has track record of delivery. Fundamentals solid, addressable market massive, competitive moat intact. Stablecoin initiative provides genuine new growth vector. Multiple paths to $450+.

🎯 Base Case (45% probability)

Target: $380-$430 by January 2028 (Market Consensus)

Most likely scenario:

- ✅ Solid earnings growth - revenue +11-13% annually, EPS +12-14%

- 💰 Stablecoin products launch successfully but adoption is gradual - contributes $500M-1B revenue by 2028

- 🌐 Cross-border volume growth moderates to 8-10% as travel recovery matures

- ⚖️ DOJ case drags on but no major adverse ruling by 2028

- 🏪 Merchant settlement approved with minimal impact (fee reduction offset by volume)

- 📊 Trading in line with analyst consensus $394-402 targets for 2026, extends to $400-420 range by 2028

- 💤 Steady compounder narrative - not explosive growth but reliable execution

- 🎢 Normal volatility: occasional 5-10% pullbacks but uptrend intact

- 🆚 Maintains market share vs Mastercard, no significant disruption

This supports the LEAPS investment thesis: Even in base case, stock reaches $380-430 by Jan 2028, delivering strong returns:

- Stock at $400: Intrinsic value = $200, profit = $34.55/contract = $29M gain (36% ROI)

- Stock at $420: Intrinsic value = $220, profit = $54.55/contract = $46M gain (58% ROI)

Breakeven: Stock needs to reach $365.45 by Jan 2028 (just 5.4% appreciation total over 3 years)

Why 45% probability: This is the "steady as she goes" scenario that aligns with Visa's historical performance. Company consistently delivers but rarely has explosive growth quarters. Most institutional holders expect this outcome. Conservative but realistic.

📉 Bear Case (15% probability)

Target: $280-$340 by January 2028 (Modest Loss to Flat)

What could go wrong:

- 😰 Stablecoin initiatives flop - low adoption, regulatory pushback, technical issues

- 🚨 DOJ case results in adverse ruling - forced fee reductions, business model restrictions

- 🌍 Global recession reduces consumer spending, transaction volumes decline

- 🇨🇳 China economic slowdown impacts cross-border volumes materially

- 💸 Merchant settlement rejected, new litigation with harsher terms

- 🆚 Mastercard takes market share through aggressive pricing or innovation

- 🪙 Crypto-native payment rails (Bitcoin Lightning, stablecoin P2P) disintermediate Visa

- 📉 Digital wallet providers (Apple Pay, Google Pay) bypass Visa for some transactions

- 💰 Margin compression from competitive pressure or regulatory rate caps

- 📊 Multiple consecutive quarters of guidance misses erode confidence

Critical support levels:

- 🛡️ $345: Major gamma floor - MUST HOLD or technical break occurs

- 🛡️ $340: Deep support - likely buying opportunity if tested

- 🛡️ $330: Extended floor - capitulation level

- 🛡️ $300: Disaster scenario - fundamental thesis breaks

LEAPS P&L in Bear Case:

- Stock at $340: Intrinsic value = $140, loss = -$25.45/contract = -$22M loss (-27%)

- Stock at $300: Intrinsic value = $100, loss = -$65.45/contract = -$56M loss (-70%)

- Stock at $280: Intrinsic value = $80, loss = -$85.45/contract = -$73M loss (-91%)

Probability assessment: Only 15% because Visa's business model is extremely resilient. Payment volumes are sticky, even in recessions. Network effects and scale create massive moat. DOJ case likely years from resolution. Stablecoin failure would disappoint but not break core business. Multiple safety nets before fundamental thesis invalidated.

Even in bear case, buyer doesn't lose entire $80M: The deep ITM structure provides downside protection. Stock would need to fall below $200 (42% decline) for total loss, which is extremely unlikely for Visa.

💡 Trading Ideas

🛡️ Conservative: Buy Shares with Dollar-Cost Averaging

Play: Accumulate Visa shares on any pullback to $340-345 support zone

Why this works:

- 💪 $80M institutional LEAPS purchase signals smart money conviction

- 📊 22 analyst buy ratings with $402 average target = 16% upside minimum

- 🛡️ Strongest business model in payments - 67% operating margins, $666B market cap

- 💰 14% dividend increase shows confidence, shareholder-friendly capital allocation

- 📈 YTD +37.3% demonstrates momentum, recent pullback creates entry opportunity

- 🌐 Multiple growth vectors: stablecoins, cross-border recovery, market share gains

- ⏰ Time is on your side - hold 2-3 years to capture stablecoin adoption cycle

Action plan:

- 🎯 Start with 25-30% position at current levels ($345-350)

- 📉 Add 25% more if pullback to $340 support (gamma floor)

- 📉 Add 25% more if deeper pullback to $330 (extended support)

- 💎 Hold final 20-25% for post-earnings dip if opportunity arises January 22nd

- ⏰ Plan 2-3 year hold period to capture full stablecoin adoption story

- 💰 Reinvest dividends for compound growth

Expected return: 10-15% annualized over 2-3 years (matches historical Visa returns)

Risk management:

- 🛑 Stop loss at $320 if fundamentals deteriorate (DOJ adverse ruling, earnings misses)

- 📊 Monitor quarterly earnings for cross-border volume trends

- 👀 Track stablecoin pilot adoption metrics when disclosed

Risk level: Low (blue-chip stock with dividend) | Skill level: Beginner-friendly

Why conservative: Buying the actual stock eliminates theta decay, IV crush, and leverage risk. You own a piece of the best payment network in the world with multiple growth catalysts. Sleep well at night.

⚖️ Balanced: Post-Earnings Bull Call Spread

Play: After January 22nd earnings volatility settles, construct bull call spread

Structure: Buy $350 calls, Sell $370 calls (March 20, 2026 quarterly expiration)

Why this works:

- 🎢 IV crush after earnings makes call spreads much cheaper - buy AFTER volatility drops

- 📊 Defined risk spread ($20 wide = $2,000 max profit potential)

- 🎯 Targets breakout above $350 resistance to $370 level (6.5% move)

- ⏰ 60 days post-earnings gives time for stablecoin pilot launch in April

- 💰 Captures upside from positive earnings catalyst + stablecoin news

- 🛡️ Limited downside if wrong - can only lose net debit paid

Estimated P&L (adjust after seeing post-earnings IV):

- 💸 Pay ~$8-10 net debit per spread post-earnings (vs $14-16 now)

- 📈 Max profit: $1,000-1,200 if Visa above $370 at March expiration (100-150% ROI)

- 📉 Max loss: $800-1,000 if Visa below $350 (defined and limited)

- 🎯 Breakeven: ~$358-360

- 📊 Risk/Reward: ~1:1 to 1.5:1 which is attractive for defined-risk bullish play

Entry timing:

- ⏰ Wait 2-3 days after January 22nd earnings (by Jan 24-25) for full IV collapse

- 🎯 Only enter if stock holds $345+ support (confirms no bearish breakdown)

- ✅ Look for positive earnings reaction + constructive guidance

- ❌ Skip if stock gaps above $365 post-earnings (already captured move)

Position sizing: Risk only 3-5% of portfolio (this is directional speculation with defined risk)

Exit strategy:

- 🎯 Close at 50-60% max profit if reached quickly (take money and run)

- 📈 Hold for full profit if breakout above $360 confirmed with volume

- 🛑 Cut at 50% loss if stock breaks below $340 support (thesis broken)

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

🚀 Aggressive: Copy the Pros - LEAPS Call Purchase (ADVANCED!)

Play: Replicate institutional strategy with smaller size deep ITM LEAPS

Structure: Buy $250 or $260 strike calls expiring January 2027 (1-year LEAPS, not full 3-year)

Why this could work:

- 💪 Copying $80M institutional position at retail scale

- 📈 Deep ITM calls behave like leveraged stock (90-95 delta)

- ⏰ 1-year expiration (vs 3-year for institutions) reduces premium cost but captures key catalysts

- 🎯 Targets earnings beats, stablecoin launch, settlement approval over next 12 months

- 💰 Capital efficiency: Control $34,000 of stock for ~$12,000-14,000 per contract

- 🚀 Unlimited upside participation if Visa runs to $400+ by 2027

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Each contract costs $12,000-14,000 (vs $165 for near-term options)

- ⏰ TIME DECAY: Theta burns value every day even though it's slow ($5-10/week)

- 😱 LEVERAGE CUTS BOTH WAYS: If Visa drops to $300, you lose $4,000-6,000 per contract

- 📉 Need significant move: Must reach $360-370+ to meaningfully profit vs just owning stock

- 🎢 Volatility risk: If Visa stays flat around $350, you lose time value

- ⚠️ Tied up capital: Money locked in options vs deployed elsewhere

- 💀 Binary catalysts: Bad earnings or stablecoin failure could crater value quickly

Estimated P&L (using $250 strike as example):

- 💰 Cost: ~$110-115 per contract (current $97 intrinsic + $13-18 time value)

- 📈 Profit scenario: Visa at $400 by Jan 2027 = $150 intrinsic, profit ~$35-40 (30-35% ROI)

- 🚀 Home run: Visa at $450 by Jan 2027 = $200 intrinsic, profit ~$85-90 (75-80% ROI)

- 📉 Loss scenario: Visa at $300 by Jan 2027 = $50 intrinsic, loss ~$60-65 (55% loss)

- 💀 Disaster: Visa at $250 by Jan 2027 = $0 intrinsic, total loss of $110-115 (100% loss)

Breakeven: Stock needs to reach $360-365 by Jan 2027 (4-5% appreciation needed)

Comparison to just buying stock:

- 📊 100 shares costs $34,679 at current price

- 📊 1 LEAPS contract costs ~$11,000-11,500 for similar exposure

- ✅ LEAPS pros: Capital efficiency (3:1 leverage), defined max loss

- ❌ LEAPS cons: Time decay, no dividends, expires worthless if wrong

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded LEAPS before and understand deep ITM mechanics

- ✅ Can afford to lose ENTIRE premium (real possibility if Visa crashes)

- ✅ Understand you're making leveraged directional bet with time limit

- ✅ Have 2-3 year investment horizon and won't panic sell on volatility

- ✅ Are comfortable with illiquidity (wide bid-ask spreads on LEAPS)

- ⏰ Plan to monitor position quarterly and roll forward if needed

- 💰 Are willing to lose $10,000-15,000 per contract in worst case

Alternative for smaller accounts:

- Consider shorter-dated $350 or $360 calls for June 2026 expiration (~$1,500-2,500 per contract)

- Captures earnings + stablecoin launch but much less capital required

- Higher theta decay but more retail-accessible

Position sizing:

- Risk MAXIMUM 5-10% of portfolio (this is highly speculative!)

- Consider 1-2 contracts max for most retail traders

- Do NOT go "all in" on LEAPS - you need diversification

Risk level: HIGH (leverage, time decay, binary catalysts) | Skill level: Advanced only

Probability of profit: ~50-55% over 1-year timeframe (better than stock only if significant move occurs)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Earnings in 41 days (January 22nd): Q1 FY2026 results create meaningful volatility risk. While Visa rarely misses, any disappointment in holiday spending trends or conservative 2026 guidance could trigger 5-10% selloff. At 74.8x forward P/E, expectations are elevated. Stock near 52-week highs creates profit-taking risk. Monitor for pre-earnings option buying as signal of institutional positioning.

-

🚨 DOJ antitrust litigation existential threat: Judge rejected motion to dismiss in June 2025, calling monopolization allegations "plausible." Case now in discovery phase through 2026. If DOJ prevails (trial late 2026/2027), potential remedies include forced rate reductions, exclusive agreement restrictions, or structural business model changes. 60%+ debit market share and $7B annual fees create major regulatory target. This is THE major overhang that could cap valuation until resolved.

-

💸 Merchant swipe fee settlement compresses margins: November 2025 settlement reduces fees by 0.1 percentage point for 5 years, caps standard rates at 1.25% for 8 years. Represents 25%+ reduction on baseline cards. With U.S. swipe fees at $111.2B in 2024, 0.1 point reduction = $300-500M annual revenue headwind. While volume growth may offset, this represents real margin pressure. Court approval still pending - rejection forces harsher terms or extended litigation.

-

🪙 Stablecoin execution risk with unproven model: Both prefunding pilot (April 2026) and payouts pilot (H2 2026) are ENTIRELY NEW business lines with zero historical data. Adoption uncertainty massive - will enterprises trust crypto-adjacent payment rails? Technical integration bridging TradFi and blockchain extremely complex. Regulatory fragmentation outside U.S. complicates global rollout (EU MiCA vs U.S. GENIUS Act). Potential delays in moving from pilot to production scale. If flops, removes key growth narrative supporting current valuation.

-

🆚 Mastercard competitive pressure accelerating: Competitor growing revenue 12.2% YoY vs Visa's 10.0% in FY2024, closing gap. Mastercard expanding in Europe (33% digital transactions) and Asia-Pacific (29%). Both companies have similar stablecoin strategies, so no first-mover advantage guaranteed. Digital wallet providers (Apple Pay, Google Pay) bypass traditional card networks for some transactions. Buy Now Pay Later (Affirm, Klarna) appeal to younger demographics. Crypto-native payment networks could disintermediate long-term.

-

📉 Valuation stretched after 37% YTD run: Stock near all-time high of $375.51 after strong 2025. Already captured much of anticipated stablecoin and growth narrative. Average analyst target $402 represents just 16% upside - asymmetry less favorable than at $280-300 levels earlier in year. If growth disappoints or macro weakens, multiple compression risk from current elevated levels. Need flawless execution to justify current price.

-

🌍 Global recession vulnerability: At current valuation, Visa has limited recession protection. Consumer spending highly cyclical - previous recessions show 15-20% volume declines. Cross-border travel spending (fastest growing segment) collapses first in downturn. If 2026-2027 brings economic weakness, even strong execution won't prevent 20-30% stock correction. Payment volumes are lagging economic indicator.

-

🇨🇳 China exposure and geopolitical risk: China historically 15-20% of revenue with significant growth. Economic slowdown there impacts consumer spending and cross-border volumes. Regulatory risks in China payment market (UnionPay dominance, government preferences for domestic providers). Geopolitical tensions between U.S.-China could impact business operations or revenue recognition. Any export restrictions on payment processing technology would be unprecedented but possible.

-

🎢 Modest implied volatility creates range-bound risk: Weekly implied move just 1.76% ($6) suggests market expects quiet consolidation, not explosive moves. For LEAPS buyers, need significant breakout above $360-370 to generate strong returns. If Visa trades in $330-360 range for extended period, time decay erodes option value despite stock being "fine." Need catalyst to drive momentum.

-

💰 Insider selling and low insider ownership: Historically insiders own <1% of shares with periodic selling for diversification. While not necessarily bearish, lack of meaningful insider buying near current prices suggests management doesn't view valuation as compelling opportunity. Institutions own 91% - if they decide to take profits after YTD run, selling pressure could overwhelm retail buyers.

-

🏛️ Regulatory uncertainty beyond DOJ case: Credit Card Competition Act of 2023 proposed legislation could mandate multi-network routing, reducing Visa's market share and pricing power. Global regulatory landscape evolving with different jurisdictions taking varying approaches to payment network regulation. Data privacy regulations (GDPR, CCPA) increase compliance costs. Any surprise regulatory action could impact business model.

🎯 The Bottom Line

Real talk: Someone just bet $80 MILLION on Visa's future - that's not a hedge, that's a CONVICTION PLAY on the digital payments revolution. This LEAPS buyer is positioning for Visa to absolutely dominate the stablecoin era while maintaining its network effect moat in traditional transactions.

What this trade tells us:

- 💪 Institutional sophistication: Deep ITM structure ($200 strike vs $347 stock) shows this is leveraged stock replacement, not speculation

- ⏰ 3-year time horizon (January 2028 expiration) captures FULL stablecoin adoption cycle from pilot to production scale

- 📊 $80M deployment in single second = single entity with massive conviction, not scattered retail flow

- 🎯 Targeting $450-500 range which aligns with top analyst targets

- 🛡️ Breakeven just $365.45 (5.4% above current) = high probability of profit over 3 years

- 💰 Willing to pay 5.4% cost of carry for 3 years of leverage speaks to confidence

Why this trade makes sense: Visa's stablecoin initiatives are NOT just another product launch - they're strategic defense against crypto disintermediation. By integrating USDC stablecoins into Visa Direct, the company positions itself as the BRIDGE between traditional finance and decentralized finance rather than a victim of disruption. The $100B creator economy opportunity is real, and Visa has first-mover advantage among TradFi giants.

If you own Visa:

- 💎 HOLD with conviction - $80M smart money validates your thesis

- 📊 Monitor January 22nd earnings for cross-border volume trends and 2026 guidance quality

- 🎯 Use any pullback to $340-345 (gamma support) as opportunity to ADD

- ⏰ Plan 2-3 year hold to capture stablecoin adoption and market share gains

- 🛡️ Set mental stop only at $320 if fundamental thesis breaks (DOJ adverse ruling, earnings misses)

If you're watching from sidelines:

- ✅ Best entry: $340-345 support zone - either on pre-earnings consolidation or post-earnings dip

- 📅 Key dates: January 22nd earnings, April stablecoin pilot, H2 2026 payouts launch

- 🎯 Price targets: Conservative $400 (analyst consensus), optimistic $450-500 (bull case)

- 💰 Strategy: DCA shares on dips vs chasing momentum at all-time highs

- ⏰ Timeline: Think in years, not quarters - this is long-term compounding story

If you're considering options:

- 🛡️ Conservative: Buy shares and sleep well (14% dividend increase, 67% margins)

- ⚖️ Balanced: Post-earnings bull call spreads for defined risk upside exposure

- 🚀 Aggressive: Deep ITM LEAPS only if you understand leverage and can handle volatility

- ❌ Avoid: Near-term options around earnings (IV crush will destroy value)

- 💸 Sizing: LEAPS should never exceed 5-10% of portfolio (high risk despite institutional validation)

Mark your calendar - Key catalyst dates:

- 📅 January 22, 2026 (41 days) - Q1 FY2026 earnings after market close - MAJOR CATALYST

- 📅 April 2026 - Stablecoin prefunding pilot limited availability

- 📅 Q1-Q2 2026 - Merchant swipe fee settlement court approval decision

- 📅 H2 2026 - Stablecoin payouts pilot broader rollout to creator economy

- 📅 Late 2026/Early 2027 - DOJ antitrust case trial (potential headwind)

- 📅 January 21, 2028 - LEAPS expiration for $80M institutional trade

Final verdict: Visa's long-term digital payments dominance story is INTACT and perhaps stronger than ever with stablecoin initiatives. The company isn't fighting crypto - it's embracing and integrating it into the world's largest payment network. With 52.2% global credit card market share, 67% operating margins, and 22 analyst buy ratings averaging $402 target, this is a blue-chip growth story.

The $80M institutional LEAPS purchase is NOT saying "Visa to the moon tomorrow" - it's saying "Visa will be materially higher 3 years from now, and I want leveraged exposure to that growth." That's patient, sophisticated capital making a multi-year bet on inevitable trends: digital payments, stablecoin adoption, and network effects.

For retail investors: Don't try to replicate the exact trade (that's $165,000+ per contract!). Instead, use this as validation to build long-term Visa position through shares or smaller LEAPS. The smart money has spoken. Are you listening? 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. LEAPS contracts are complex instruments requiring significant capital and understanding of Greeks, time decay, and leverage mechanics. The $80M institutional trade reflects sophisticated portfolio management strategies that may not be appropriate for retail investors. Deep ITM options have wide bid-ask spreads and liquidity challenges. Always do your own research and consider consulting a licensed financial advisor before trading. The institutional buyer may have complex hedging strategies or portfolio needs not disclosed in public trade data.

About Visa Inc.: Visa operates the world's largest payment processor, handling approximately $16 trillion in transaction volume across 200+ countries with infrastructure processing 65,000+ transactions per second, commanding $666.4 billion market cap in the business services sector.