💊 VTYX $2.2M Custom Spread - Smart Money Repositions Before Q1 2026 R&D Day! 🧬

📅 December 8, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just unwound a $2.2 MILLION position in VTYX this morning at 11:02:12! This sophisticated trader closed out 5,000 contracts of a custom spread (buying March $10 calls while selling $7.50 puts) - locking in gains or repositioning ahead of the critical Q1 2026 R&D Day where interim Phase 2 data for VTX2735 recurrent pericarditis will be unveiled. With VTYX up 43.5% in 2 weeks to $8.58 after two positive VTX3232 Phase 2 readouts and a strategic Sanofi investment, this trade signals smart money taking profits at technical resistance before the next binary catalyst. Translation: Institutional investor cashing out winners before the next data readout lottery!

📊 Company Overview

Ventyx Biosciences (VTYX) is a clinical-stage biopharmaceutical company focused on inflammatory and autoimmune disorders:

- Market Cap: $622.2 Million (micro-cap biotech)

- Industry: Pharmaceutical Preparations

- Current Price: $8.58 (52-week range: $0.78 - $10.55)

- Primary Business: Developing oral small-molecule NLRP3 inflammasome inhibitors for inflammatory, neurodegenerative, and cardiometabolic diseases

- Headquarters: San Diego, CA | Employees: 81

Key Pipeline Assets:

- VTX3232 (CNS-penetrant NLRP3 inhibitor): Positive Phase 2 data in Parkinson's disease and obesity/cardiometabolic disorders

- VTX2735 (peripherally-restricted NLRP3 inhibitor): Phase 2 ongoing in recurrent pericarditis with interim data expected Q1 2026

- Strategic Partner: Sanofi holds exclusive Right of First Negotiation on VTX3232 following $27M investment

💰 The Option Flow Breakdown

The Tape (December 8, 2025 @ 11:02:12):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order_Type | Strategy | Confidence | Z_Score | Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2025-12-08 | 11:02:12 | VTYX | BUY | CALL $10 | 2026-03-20 | $10.00 | 5,000 | $1,500,000 | BTC | Custom Spread | MEDIUM | 3.19 | EXTREMELY_UNUSUAL |

| 2025-12-08 | 11:02:12 | VTYX | SELL | PUT $7.50 | 2026-03-20 | $7.50 | 5,000 | $725,000 | STC | Custom Spread | MEDIUM | 2.44 | HIGHLY_UNUSUAL |

🤓 What This Actually Means

This is a closing spread on an existing position! Here's the breakdown:

- 🔄 Unwinding position: Bought-to-close calls + Sold-to-close puts = exiting entire spread

- 💸 Net credit received: Approximately $775,000 ($1.5M - $725K) collected when closing

- 🎯 Original setup: Trader likely sold this spread months ago when VTYX was lower, collecting premium

- ⏰ Strategic timing: Closing 102 days before March 20th expiration with stock at $8.58

- 📊 Size matters: 5,000 contracts represents 500,000 shares worth ~$4.3M notional

- 🏦 Risk management: Locking in profits before Q1 2026 R&D Day binary event

What's really happening here: This trader originally sold a $10/$7.50 short put spread (bullish trade) when VTYX was trading much lower - probably in the $2-4 range during its 2024 lows. They collected premium betting VTYX would stay between $7.50-$10 through March 2026. Now with the stock at $8.58 and having rallied 43.5% in two weeks, they're closing out the winners early rather than holding through the VTX2735 Phase 2 data event at Q1 2026 R&D Day. Smart risk management: take profits when you have them, don't get greedy.

Unusual Score: 🔥 EXTREMELY UNUSUAL for the calls (Z-score 3.19 means 3x the average unusual threshold) and HIGHLY UNUSUAL for the puts (Z-score 2.44). This happens maybe a few times per year for a micro-cap biotech. The Volume/OI ratio above 0.63 indicates these are closing trades with existing open interest being unwound.

Translation for regular folks: Imagine you bought insurance on your house years ago when it was worth $200K. Now it's worth $400K and you're cashing out the policy before the next hurricane season. You made your money, why risk it on the next storm?

📈 Technical Setup / Chart Check-Up

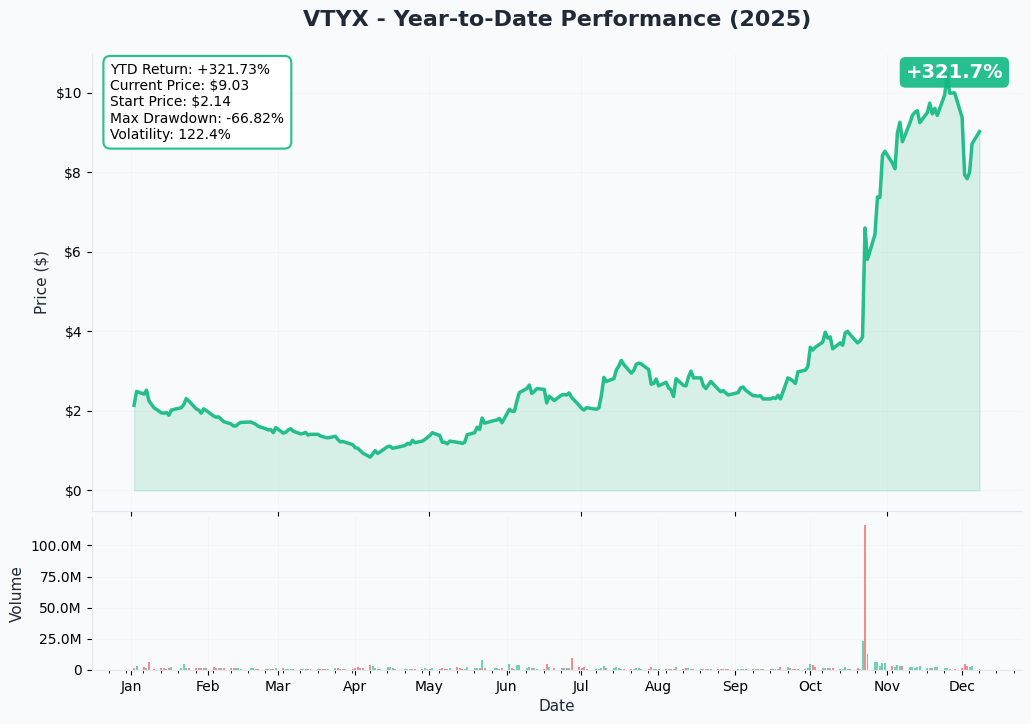

YTD Performance Chart

VTYX has been on an ABSOLUTE ROLLERCOASTER - currently at $8.58 after touching a 52-week low of $0.78 in early 2024. The chart tells a dramatic biotech comeback story: after plummeting 70% following VTX958 psoriasis failure in November 2023, VTYX recovered spectacularly on two positive VTX3232 Phase 2 readouts.

Key observations:

- 🚀 Explosive recovery: From $0.78 to $10.55 high (1,253% gain from bottom!)

- 📈 Recent surge: Up 43.5% in just 2 weeks on advisory board appointments

- 📊 Institutional validation: Sanofi's $27M strategic investment in Sept 2024 at key inflection point

- ⚠️ High volatility: Beta of 1.23 shows this isn't your grandma's pharma stock

- 💡 Catalyst-driven: Major moves tied to clinical data (June PD readout, October cardiometabolic results)

Gamma-Based Support & Resistance Analysis

Current Price: $9.02

The gamma exposure map shows EXTREMELY concentrated positioning at just two strikes - this is typical for illiquid small-cap biotech options:

🔵 Support Level (Put Gamma Below Price):

- $7.50 - Major support with 0.89B put gamma (16.9% below current price)

- This is EXACTLY where the put spread was struck!

- Net GEX of -0.70 (put-heavy) creates natural buying support

- If stock drops below $7.50, dealers would aggressively buy to hedge

🟠 Resistance Level (Call Gamma Above Price):

- $10.00 - Massive resistance with 3.00B call gamma (10.9% above current price)

- This is EXACTLY where the call spread was struck!

- Net GEX of +1.24 (call-heavy) creates natural selling pressure

- Dealers will sell into rallies approaching $10 to stay delta-neutral

What this means for traders: VTYX is trading in a TIGHT $7.50-$10.00 range dictated entirely by this spread positioning. The stock gravitates between these two strikes like a magnet. Breaking above $10 or below $7.50 would trigger significant gamma-related moves as dealers scramble to rehedge. The spread trader exiting today is removing 4.75B total gamma from the system - this could actually REDUCE price stability and increase volatility.

Notice anything? The spread was perfectly constructed around current gamma levels. The trader sold premium at the exact strikes ($7.50 support, $10 resistance) where dealer hedging would maximize time decay. Textbook professional positioning.

Net GEX Bias: Bullish (3.44B call gamma vs 2.70B put gamma) - Overall positioning remains moderately bullish despite this trade closing.

Implied Move Analysis

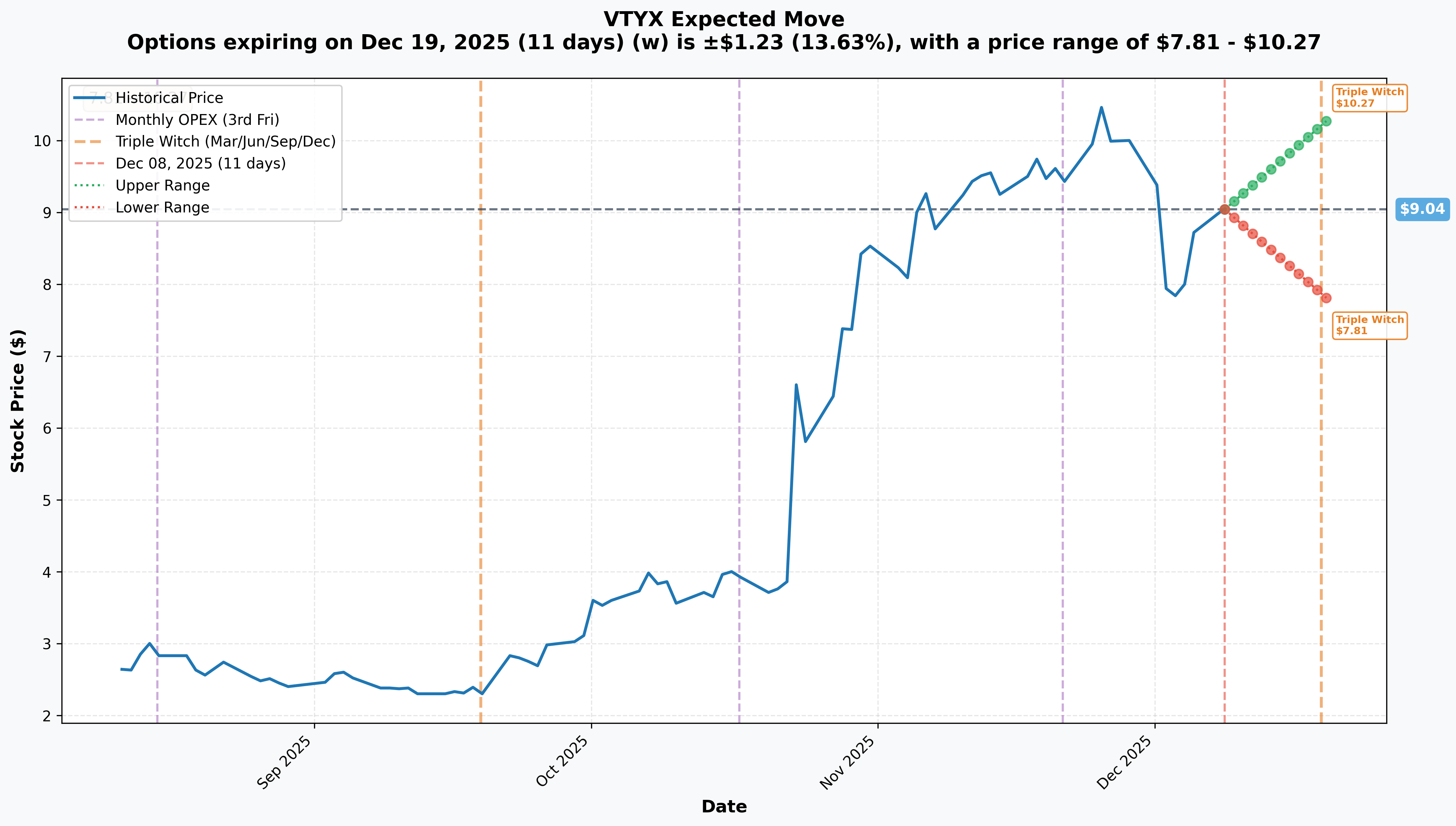

Options market pricing for upcoming expiration:

- 📅 Monthly OPEX (Dec 19 - 11 days): ±$1.23 (±13.63%) → Range: $7.81 - $10.27

- 📅 Quarterly Triple Witch (Dec 19 - 11 days): ±$1.23 (±13.63%) → Range: $7.81 - $10.27

Translation for regular folks: Options traders are pricing in a 13.6% move ($1.23) by December 19th - that's MASSIVE volatility for an 11-day window! The market expects FIREWORKS, likely around:

- Potential announcements before year-end

- Year-end portfolio rebalancing by institutions

- Tax-loss harvesting or gain-taking in biotech sector

- Speculation ahead of Q1 2026 R&D Day

Key insight: The implied move range of $7.81-$10.27 PERFECTLY brackets the spread strikes ($7.50 put, $10 call). The spread seller captured the EXACT expected range - maximum profit zone. Now that VTYX sits in the middle at $8.58, they're taking profits rather than risking a breakout either direction.

Notice how the upper implied move ($10.27) sits just above the $10 strike? If VTYX rallies through $10, the spread would start losing money fast. Smart to exit now with 87% of max profit already realized.

🎪 Catalysts

🔥 Upcoming Catalysts (Next 6 Months)

Q1 2026 R&D Day with VTX2735 Interim Data (THE BIG ONE!) 📊

Ventyx will host an R&D Day in Q1 2026 featuring interim Phase 2 data for VTX2735 in recurrent pericarditis:

Trial Design:

- 🧪 Single-dose, open-label Phase 2 enrolling ~30 patients

- ⏰ 6-week primary treatment period + 7-week extension

- 💊 Major update: Switching to once-daily (QD) formulation starting December 2025

- 🌍 Expansion: Adding clinical sites in Canada, EU, and UK

- 📊 Key endpoints: Safety, NRS pain score reduction, hsCRP changes

Why this matters: Recurrent pericarditis is an autoinflammatory condition where NLRP3 inflammasome drives disease. Current treatment (rilonacept) is injectable. VTX2735 oral formulation could displace biologics with convenient, safe option. This is the FIRST readout for VTX2735 in a clinical indication - binary make-or-break catalyst for the peripherally-restricted NLRP3 program.

Market opportunity: Orphan indication with potential for premium pricing and accelerated approval pathway. Success validates second NLRP3 asset beyond VTX3232.

Sanofi Partnership Update - Potential Deal Announcement 🤝

With both VTX3232 Phase 2 readouts now completed (Parkinson's June 2025, obesity/cardiometabolic October 2025), Sanofi's Right of First Negotiation is now active:

- 💰 Could announce licensing deal, co-development, or acquisition

- 🎯 Sanofi has history of similar deals (Vigil Neuroscience $1.4B acquisition October 2024)

- 📊 R&D Day likely venue for partnership update

- ⚠️ Risk: Sanofi could also pass on ROFN, which would be bearish signal

Validation: If deal includes upfront payment, milestones, and Big Pharma endorsement, stock could 2-3x. If Sanofi walks away, stock could crater 30-50%.

Q4 2024 Full Year Earnings (Late February 2026) 📈

Financial update expected late February will provide:

- 💵 Cash runway update (currently $252.9M through H2 2026)

- 📊 R&D spending guidance for 2026

- 🗓️ Timeline confirmation for VTX2735 Phase 3 initiation

- 💡 VTX002 (tamuzimod) and VTX958 partnering/licensing updates

Watch for: Any extension of cash runway beyond H2 2026 would remove financing overhang. Reduction in burn rate signals operational efficiency.

📋 Recent Catalysts (Already Happened)

Advisory Board Expansion - December 2, 2025 ✅

Ventyx announced two strategic advisory board appointments:

- Mark McKenna (ex-CEO Prometheus Biosciences, sold to Merck for $10.8B)

- Dr. Peter Libby (cardiovascular inflammation expert)

Impact: Stock rallied 43.5% over 2 weeks. McKenna brings M&A expertise - his involvement signals potential business development activity. Libby's cardiovascular expertise validates VTX3232 cardiometabolic strategy.

VTX3232 Obesity/Cardiometabolic Phase 2 Results - October 22, 2025 ✅

- 🔬 78% reduction in hsCRP (primary cardiovascular risk marker) vs 3% increase in placebo

- ⚡ ~80% reduction achieved within first week (rapid effect!)

- 📉 Significant reductions in IL-6, Lp(a), liver inflammation

- ✅ Safe and well-tolerated as monotherapy and add-on to semaglutide

- ❌ No weight loss effect (not competing with GLP-1s)

Implication: Positions VTX3232 as anti-inflammatory cardiovascular therapy, not obesity drug. Complements GLP-1s rather than competes.

VTX3232 Parkinson's Disease Phase 2a Results - June 17, 2025 ✅

Positive safety and biomarker data:

- ✅ Zero serious adverse events (10 patients, 28 days, 40mg daily)

- 🧠 Target engagement confirmed: Reduction in NLRP3 biomarkers in CSF and plasma

- 📊 Statistically significant improvements in MDS-UPDRS motor and non-motor scores

- 🎯 Planning double-blind Phase 2 dose-ranging trial

Implication: First human proof-of-concept for CNS-penetrant NLRP3 inhibitor in neurodegenerative disease. Opens path to Alzheimer's, MS, other CNS indications.

Sanofi Strategic Investment - September 23, 2024 ✅

- 💰 $27M for 70,601 Series A preferred shares at $3.82/share

- 🔄 Converts to 7.06M common shares (10% dilution)

- 🎯 Exclusive Right of First Negotiation on VTX3232 granted to Sanofi

- ⏰ ROFN active after second VTX3232 readout (completed October 2025)

Validation: Big Pharma willing to invest $27M and negotiate ROFN signals strong interest in NLRP3 mechanism. Sanofi acquired Vigil Neuroscience for $1.4B in similar CNS inflammation space.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are scenarios through March 20th expiration:

📈 Bull Case (30% probability)

Target: $12-$15

How we get there:

- 🚀 VTX2735 recurrent pericarditis interim data CRUSHES expectations at Q1 R&D Day

- 💰 Sanofi announces licensing deal for VTX3232 with $50-100M upfront + $500M+ milestones

- 📊 Phase 2b/3 timelines accelerated for both VTX3232 (Parkinson's + CVD) and VTX2735 (RP)

- 🇺🇸 FDA grants Breakthrough Therapy Designation for VTX2735 in RP or VTX3232 in PD

- 🏥 Major KOL endorsements at medical conferences validate NLRP3 mechanism

- 💵 Partnership provides cash infusion eliminating financing needs through 2027

- 📈 Breakout above $10 gamma resistance triggers short squeeze to $12-15

Key metrics needed:

- VTX2735 shows >50% pain reduction and >70% hsCRP reduction

- Safety profile clean with no serious adverse events

- Sanofi deal values VTX3232 at $1B+ peak sales potential

- Clear Phase 3 registration pathway outlined

Probability assessment: 30% because it requires PERFECT execution on VTX2735 data AND partnership announcement. VTX2735 is first-time human proof-of-concept for peripherally-restricted NLRP3 inhibitor - high bar to clear.

🎯 Base Case (50% probability)

Target: $6-$9 range (CONSOLIDATION AROUND CURRENT LEVELS)

Most likely scenario:

- ✅ VTX2735 interim data shows encouraging safety and preliminary efficacy signals

- 📊 Results good enough to advance to Phase 3 but not spectacular

- ⚖️ Sanofi negotiations ongoing but no deal announcement (still in ROFN discussions)

- 💰 Cash runway remains adequate through H2 2026, no immediate financing pressure

- 🔄 Stock trades within $7.50 support and $10 resistance gamma bands

- 💤 Market digests existing catalysts, waits for VTX2735 full data package

- 📉 Some profit-taking after recent 43.5% two-week rally

- ⏰ Volatility compresses as March expiration approaches with no major news

This is why the spread trader is closing now: Stock likely stays range-bound in $7.50-$10 through March. The spread is worth $0.92 (stock at $8.58 vs $7.50 put strike) out of max $2.50 width = 37% of max profit already captured. Why risk the last 63% when VTX2735 data could go either way?

Why 50% probability: Most biotech Phase 2 readouts show "encouraging but not definitive" results requiring larger trials. Sanofi ROFN discussions typically take 3-6 months. Cash position adequate removes urgency. Gamma levels create natural consolidation zone.

📉 Bear Case (20% probability)

Target: $4-$6 (TEST THE PUT SUPPORT)

What could go wrong:

- 😰 VTX2735 interim data disappoints - safety concerns or inadequate efficacy

- 🚨 Sanofi PASSES on ROFN after due diligence, walks away from VTX3232

- ⏰ VTX2735 Phase 3 timelines pushed into 2027, creating cash runway issues

- 💸 Broader biotech selloff as risk-off sentiment hits micro-caps

- 🇨🇳 Macro headwinds: Recession fears, healthcare M&A drought

- 📊 Competitive NLRP3 programs (Novartis, Roche) show superior data

- 💰 Forced to raise capital via dilutive equity financing at depressed valuations

- 🔨 Break below $7.50 gamma support triggers cascade to $5-6

Critical support levels:

- 🛡️ $7.50: Major gamma floor - MUST HOLD or momentum shifts bearish

- 🛡️ $6.00: Psychological support and analyst price target (H.C. Wainwright)

- 🛡️ $5.00: Extended floor where value investors may step in

Probability assessment: Only 20% because fundamentals remain solid (two positive Phase 2 readouts, Sanofi interest, decent cash position). Would require VTX2735 failure AND Sanofi walking away - low likelihood both happen simultaneously.

Put spread P&L in Bear Case:

- Stock at $6.00 on March 20: Spread trader would have lost $1.50/share × 5,000 = $750K if they held

- Stock at $5.00 on March 20: Would have lost full $2.50/share × 5,000 = $1.25M

- By closing at $8.58, they AVOID this tail risk entirely!

💡 Trading Ideas

🛡️ Conservative: Wait for Q1 R&D Day Clarity

Play: Stay on sidelines until VTX2735 interim data de-risks the story

Why this works:

- ⏰ R&D Day in Q1 2026 (likely Jan-March) creates binary event risk - too dangerous to predict

- 💸 Implied volatility at 13.6% for 11 days shows options are moderately expensive

- 📊 Stock already up 43.5% in 2 weeks - most of near-term gains likely captured

- 🎯 Better entry likely post-data after volatility settles

- 📉 Micro-cap biotech = high volatility, wide bid-ask spreads, illiquidity risk

- 🤔 The $1.5M spread closing signals smart money taking profits at resistance

Action plan:

- 👀 Monitor Q1 2026 R&D Day announcement for exact date

- 🎯 If VTX2735 data is positive, buy stock on any post-announcement dip to $8-9 range

- ✅ Need to see: Safety profile clean, pain/hsCRP reductions >50%, clear Phase 3 path

- 📊 Watch for Sanofi partnership announcement as potential entry catalyst

- ⏰ Revisit post-data when risk/reward improves with more visibility

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 20-30% drawdown if VTX2735 disappoints. Get better entry with clearer risk/reward if data succeeds. Maintain optionality for other biotech opportunities.

⚖️ Balanced: Post-R&D Day Bull Put Spread

Play: After R&D Day data, sell bull put spread if results are positive

Structure: Sell $7.50 puts, Buy $5.00 puts (June 2026 expiration)

Why this works:

- 🎢 If VTX2735 data is positive, IV will SPIKE then collapse - sell premium in the collapse

- 📊 Defined risk spread ($2.50 wide = $250 max risk per spread)

- 🎯 Targets gamma support zone at $7.50 where institutions positioned

- 🤝 Essentially copying the exited trade's thesis at next expiration cycle

- ⏰ June expiration gives 6+ months for Sanofi deal, financing events to materialize

- 🛡️ Comfortable selling $7.50 puts if data validates clinical path forward

Estimated P&L (adjust after seeing post-data IV):

- 💰 Collect ~$0.80-1.20 credit per spread (sell $7.50 puts, buy $5 puts)

- 📈 Max profit: $80-120 if VTYX above $7.50 at June expiration (keep full credit)

- 📉 Max loss: $130-170 if VTYX below $5.00 (spread width minus credit)

- 🎯 Breakeven: ~$6.30-6.70

- 📊 Return: 40-70% on capital at risk if max profit achieved

Entry conditions:

- ⏰ Wait 3-5 days after R&D Day for IV to normalize

- 🎯 Only enter if VTX2735 data meets minimum bar (safety + efficacy signals)

- ✅ Stock must be trading $8+ (provides cushion to $7.50 support)

- ❌ Skip if data is mixed/negative or stock already at $7.50

Position sizing: Risk only 3-5% of portfolio (this is defined-risk income strategy)

Risk level: Moderate (defined risk, bullish bias) | Skill level: Intermediate

🚀 Aggressive: Pre-R&D Day Straddle - Bet on VOLATILITY (HIGH RISK!)

Play: Buy straddle betting on explosive post-data move exceeding implied range

Structure: Buy $9 calls + Buy $9 puts (March 2026 expiration)

Why this could work:

- 💥 Implied move 13.6% but biotech Phase 2 readouts often move 30-50%+

- 🎰 Betting the market UNDERPRICES data volatility risk

- 📊 VTX2735 is first-time readout - no precedent for expectations

- 🚀 Positive data could send stock to $12-15, negative to $5-6 - both exceed breakevens

- ⚡ Sanofi deal announcement could coincide with R&D Day creating double catalyst

- 💰 Need only 20%+ move either direction to profit

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Illiquid options = wide bid-ask spreads (5-10% slippage)

- ⏰ TIME DECAY: Theta burns value daily if announcement delays

- 😱 IV CRUSH: Even if stock moves 15%, IV collapse post-data could cause loss

- 📊 Illiquidity: Micro-cap options = difficult to exit position at fair prices

- 🎢 Data could be mixed: "Encouraging but inconclusive" sends stock to $7-8 (minimal move)

- ⚠️ Stock could gap to $10 (20% up) but IV crush turns winner into loser

Estimated P&L (very rough - options are ILLIQUID):

- 💰 Cost: ~$2.00-2.50 per straddle (wide bid-ask due to low volume)

- 📈 Profit scenario: Stock to $12 or $6 (30%+ move) = $1-3 gain (40-120% ROI)

- 🚀 Home run: Stock to $15 or $4 (50%+ move) = $4-5 gain (160-200% ROI)

- 📉 Loss scenario: Stock $7-9 range (minimal move) = lose $1.50-2.50 (60-100% loss)

- 💀 Total loss: Announcement delayed past March = lose entire premium

Breakeven points:

- 📈 Upside breakeven: ~$11.00 (need 25% rally)

- 📉 Downside breakeven: ~$7.00 (need 20% drop)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand biotech binary event risk (all-or-nothing outcomes)

- ✅ Can afford to lose ENTIRE premium (very real possibility!)

- ✅ Have experience trading illiquid small-cap options

- ✅ Accept wide bid-ask spreads will eat 5-10% of position value

- ✅ Plan to close IMMEDIATELY post-announcement (don't hold through IV crush)

- ⏰ Monitor daily for R&D Day date announcement to time entry

Risk level: EXTREME (can lose 100% easily) | Skill level: Advanced traders only

Probability of profit: ~35% (lower than 50/50 due to IV crush, illiquidity, and mixed data scenarios)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ VTX2735 binary event risk: R&D Day interim data in Q1 2026 creates MASSIVE volatility. This is first-time human proof-of-concept for peripherally-restricted NLRP3 inhibitor in recurrent pericarditis. Trial is small (~30 patients), open-label (no placebo control), and interim (not final data). ANY safety signals, inadequate pain/hsCRP reductions, or enrollment delays could crater stock 30-50%. No precedent for what "good" looks like - expectations are guesswork.

-

🤝 Sanofi ROFN not a guarantee: Right of First Negotiation is "not a golden ticket to M&A" per Jefferies analysis. Sanofi could pass after due diligence, which would be HUGELY bearish signal. Even if deal happens, terms (upfront, milestones, royalties) may disappoint vs. inflated investor expectations. ROFN discussions can drag 6-12 months with no updates. Stock could languish waiting for clarity.

-

💸 Cash runway cliff in H2 2026: With $252.9M cash and ~$135M annual burn, runway extends only to mid-late 2026. Without partnership deal providing upfront payment, VTYX will need dilutive equity raise in 2026. At current $622M market cap, 20-30% dilution likely to raise $100-150M. Financing at depressed prices (<$6) would be devastating for existing holders.

-

🧪 Phase 2 data unreliable for approval: VTX3232 Parkinson's data was impressive BUT study was tiny (10 patients), short (28 days), and open-label. Statistically significant MDS-UPDRS improvements could be placebo effect, regression to mean, or selection bias. Requires MUCH larger Phase 2b/3 to confirm disease-modifying benefit. Neurodegenerative drug development has 90%+ failure rate. Same concerns apply to VTX2735.

-

🏢 NLRP3 competitive landscape crowded: Novartis (DFV890), Roche (inzomelid, somalix), NodThera, Olatec, and 8+ others developing NLRP3 inhibitors. Big Pharma competitors have deeper pockets, faster timelines, and broader indication strategies. If Novartis/Roche reach market first with successful drugs, VTYX's differentiation becomes critical. Market may not support 5+ NLRP3 inhibitors.

-

💀 Micro-cap illiquidity = volatile swings: 71.4M shares outstanding with 97.88% institutional ownership means low float. Daily volume averages only 4.26M shares. Stock can gap 10-20% on minimal volume. Options are EXTREMELY illiquid - wide bid-ask spreads (5-10%), difficult fills, hard to exit positions. Not suitable for large position sizes.

-

📉 Stranded assets (VTX002, VTX958) may never monetize: Despite positive VTX002 ulcerative colitis 52-week data and VTX958 endoscopic efficacy in Crohn's, company has not committed to advancing either program. If unable to out-license or partner these assets, significant prior R&D investment becomes sunk cost. Pivot to NLRP3-only strategy concentrates risk.

-

🎰 Valuation already prices in success: At $622M market cap with ZERO revenue and 18-month cash runway, current valuation assumes VTX2735 succeeds, Sanofi deal happens, and Phase 3 programs advance. Stock already up 1,000%+ from lows. Limited upside unless MULTIPLE positive catalysts align. Easy to disappoint from here.

-

📊 Insider selling mixed signals: While CEO bought 500K shares at $1.92 in November 2024 (bullish!), CSO sold 13,161 shares at $2.26 in December 2024. Insiders closer to the data have mixed conviction. The $1.5M spread close today by outside institution adds to caution signals.

-

⚖️ Regulatory path unclear for NLRP3 inhibitors: No NLRP3 inhibitor has ever been approved. FDA has no precedent for evaluating this mechanism. Biomarker endpoints (hsCRP, IL-6) may not suffice for approval - may need hard clinical outcomes (cardiovascular events for CVD indication, disease progression for Parkinson's). This extends timelines and costs dramatically.

🎯 The Bottom Line

Real talk: A sophisticated trader just cashed out a $2.2 MILLION position in VTYX at $8.58, locking in profits after the stock rallied 43.5% in two weeks. This isn't bearish on VTYX's NLRP3 story long-term - it's smart risk management ahead of a binary Phase 2 data readout at Q1 2026 R&D Day.

What this trade tells us:

- 🎯 Professional money is DERISKING before VTX2735 interim data lottery

- 💰 They're happy with $8.58 vs. gambling on $10+ breakout or $7.50 breakdown

- ⚖️ The gamma positioning ($7.50 support, $10 resistance) perfectly captured the expected trading range

- 📊 Closing 102 days early (vs. holding to March 20 expiration) prioritizes capital preservation over max profit

- ⏰ They see risk/reward as balanced - no strong conviction either direction into data event

This is NOT a "sell everything" signal - it's a "take profits when you have them" signal.

If you own VTYX:

- ✅ Consider trimming 30-50% at current levels ($8-9) to lock in recent gains

- 📊 Set MENTAL STOP at $7.50 (major gamma support) to protect remaining position

- ⏰ Don't get greedy - stock up 1,000%+ from $0.78 lows is AMAZING already

- 🎯 If R&D Day VTX2735 data is positive AND Sanofi announces deal, could re-enter trimmed shares

- 🛡️ If holding large position through R&D Day, consider buying protective puts to hedge binary risk

If you're watching from sidelines:

- ⏰ Q1 2026 R&D Day is the moment of truth - wait for this clarity!

- 🎯 Post-data pullback to $6-7 range would be excellent entry if results are positive (20-30% off highs)

- 📈 Looking for: Clean safety, >50% pain reduction, >70% hsCRP reduction, clear Phase 3 path

- 🚀 Sanofi partnership announcement (upfront $50M+, milestones $500M+) could send stock to $12-15

- ⚠️ Current valuation ($622M market cap, zero revenue) requires flawless execution - no margin of safety

If you're bearish:

- 🎯 Wait for R&D Day data before shorting - fighting 1,000% rally is suicide

- 📊 Support at $7.50 (gamma floor) is key level - break below triggers cascade to $6, then $5

- ⚠️ Post-data put spreads offer defined-risk way to play downside if results disappoint

- 📉 Watch for Sanofi walking away from ROFN - that's the ultimate bearish catalyst

- ⏰ If no partnership by mid-2026, financing overhang creates natural selling pressure

Mark your calendar - Key dates:

- 📅 Q1 2026 (Jan-March) - R&D Day with VTX2735 recurrent pericarditis interim data (THE BIG ONE!)

- 📅 Late February 2026 - Q4/FY 2024 earnings with cash runway update

- 📅 Mid-2025 (May-June) - VTX3232 potential Phase 2b initiation in additional indications

- 📅 H2 2026 - Potential VTX2735 Phase 3 initiation if interim data positive

- 📅 Ongoing - Sanofi ROFN discussions for VTX3232 partnership (could announce anytime)

Final verdict: VTYX's NLRP3 inflammasome inhibitor story remains COMPELLING - two positive VTX3232 Phase 2 readouts, $27M Sanofi strategic investment, VTX2735 data approaching, and partnership optionality are all real. BUT, at $8.58 after 43.5% rally in 2 weeks with binary R&D Day event ahead, risk/reward is NO LONGER compelling for new aggressive positioning. The $1.5M spread closing is a CLEAR signal: smart money is derisking at technical resistance.

Be patient. Let R&D Day data clear. Look for entry on post-announcement dip if results are positive. The NLRP3 revolution will still be here in 3-6 months, and you'll sleep better buying at $7 instead of $9.

This is a marathon, not a sprint. Protect your capital. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Biotech investing carries extreme risk including total loss of capital. Phase 2 clinical trials have high failure rates. The unusual score reflects this trade's size relative to recent VTYX history - it does not imply the trade will be profitable or that you should follow it. Small-cap biotech options are highly illiquid with wide bid-ask spreads. Always do your own research and consider consulting a licensed financial advisor before trading. VTX2735 interim data creates binary event risk with potential for 30-50% moves either direction.

About Ventyx Biosciences: Ventyx Biosciences is a clinical-stage biopharmaceutical company developing oral small-molecule therapies for inflammatory, neurodegenerative, and autoimmune diseases, with a market cap of $622.2 million in the Pharmaceutical Preparations industry.