VYX (NCR Voyix Corporation) - Unusual Options Activity Analysis

📅 Date: February 10, 2026 📊 Analysis Type: Unusual Options Activity (UOA) 🎯 Signal Strength: HIGH

Executive Summary

A $3 million institutional bet on NCR Voyix calls signals aggressive conviction in the restaurant/retail tech turnaround story. With a 219x Volume/OI ratio (indicating a brand-new position), this trade targets 27% upside over 10 months, positioning for the company's software transformation and multiple near-term catalysts including Q4 earnings on February 26, 2026.

Key Trade Metrics:

| Metric | Value |

|---|---|

| Premium | $3,000,000 |

| Strike | $12.50 |

| Spot Price | $9.83 |

| Upside Required | 27.2% |

| Expiration | December 18, 2026 |

| Days to Expiry | ~312 days |

| Vol/OI Ratio | 219x |

Trade Details

The Flow

| Field | Value |

|---|---|

| Ticker | VYX |

| Option | VYX 12/18/26 $12.50 Call |

| Direction | BUY |

| Strategy | Long Call (OTM) |

| Premium | $3,000,000 |

| Contracts | 25,000 |

| Option Price | $1.20 |

| Volume | 25,000 |

| Open Interest | 114 |

| Vol/OI Ratio | 219x |

| Timestamp | 13:40:54 ET |

Moneyness Analysis

| Metric | Value |

|---|---|

| Current Price | $9.83 |

| Strike Price | $12.50 |

| Distance to Strike | $2.67 (27.2% OTM) |

| Breakeven | $13.70 (39.4% above spot) |

| Intrinsic Value | $0.00 |

| Time Value | $1.20 (100%) |

Flow Classification

Institutional Signature Indicators

| Indicator | Assessment | Score |

|---|---|---|

| Size | 25,000 contracts = $3M premium | 🟢 Institutional |

| Vol/OI | 219x (>> 3x threshold) | 🟢 New Position |

| Timing | Mid-session (13:40) | 🟢 Deliberate |

| Strike Selection | Round number, above resistance | 🟢 Thesis-driven |

| Expiration | 10 months (post-transformation) | 🟢 Strategic |

| Single Leg | Directional conviction | 🟢 Clear View |

Classification: INSTITUTIONAL ACCUMULATION

The 219x Vol/OI ratio is exceptionally high - this is unambiguously a new position rather than position management. The December 2026 expiration allows the trade to capture:

- Q4 2025 earnings (Feb 26, 2026)

- Q1-Q3 2026 earnings cycles

- Full hardware transition impact (Q2 2026+)

- AI platform adoption trajectory

Technical Context

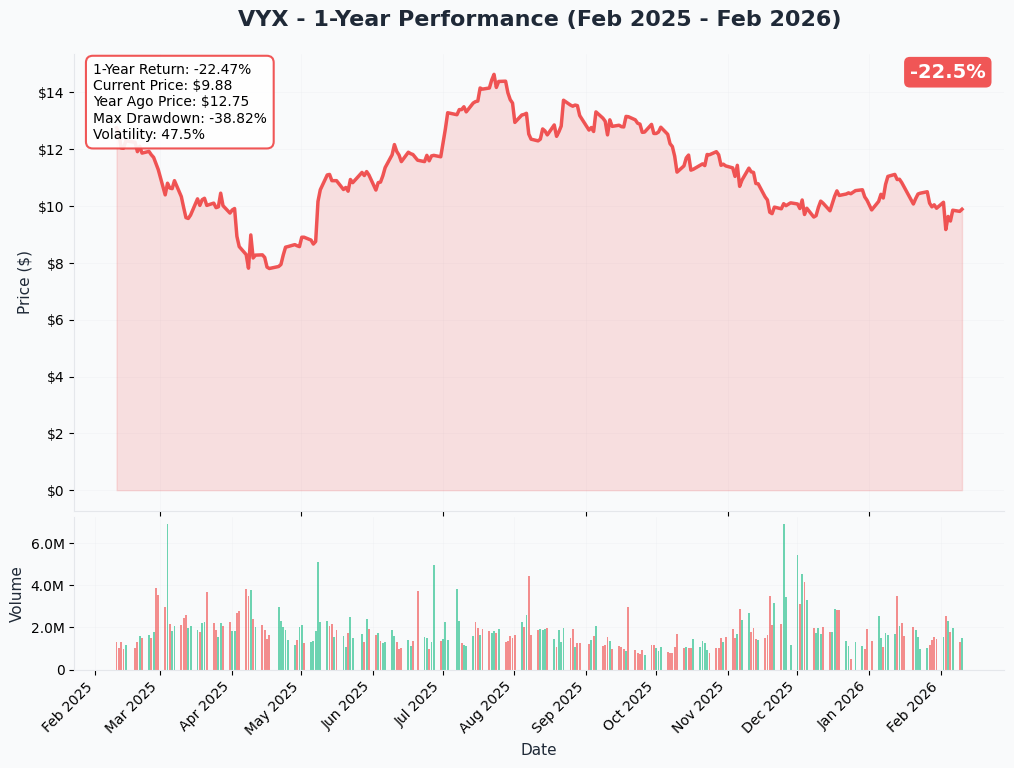

Current Price Action

Key Levels:

- Current: $9.83

- 52-Week Range: Range-bound, analyst targets significantly higher

- 3-Month Performance: -15% since October 31, 2025

- Recent Catalyst: +5.86% pre-market surge on Q3 beat (Nov 6, 2025)

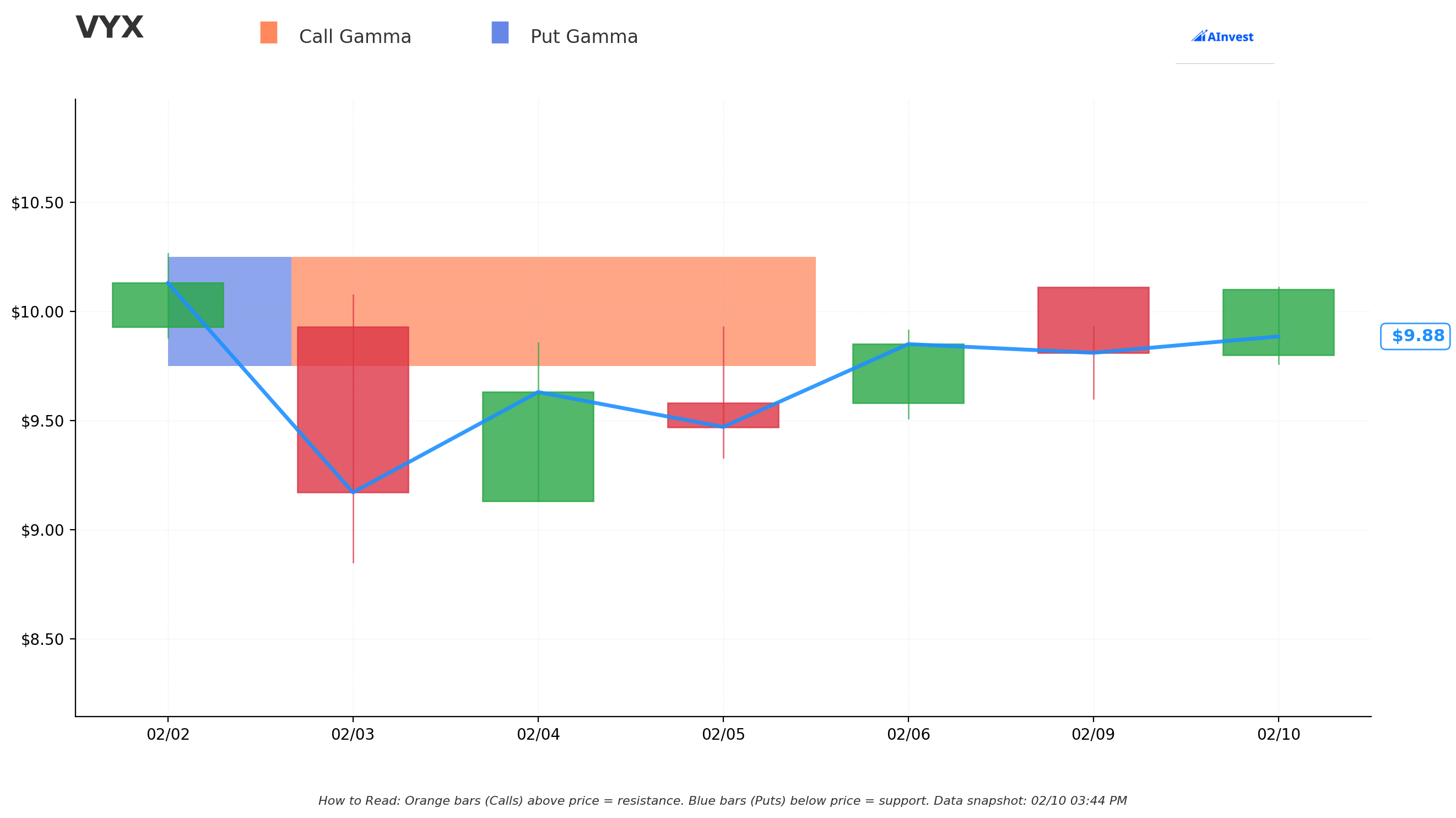

Gamma Support/Resistance

The $12.50 strike selection sits above current resistance levels, suggesting the buyer expects a catalyst-driven move through technical barriers rather than gradual appreciation.

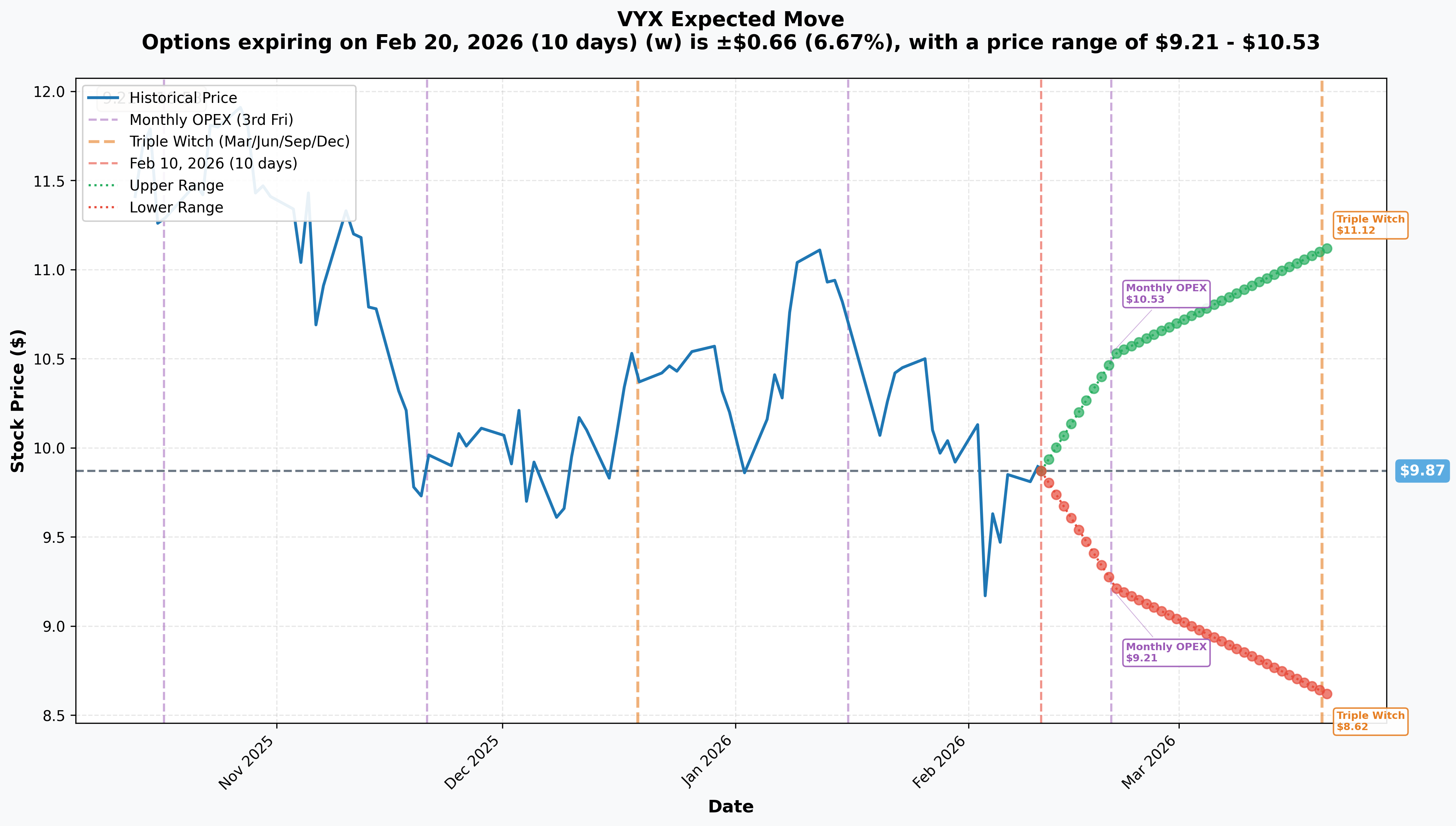

Implied Move Analysis

| Timeframe | Expiry | Days | Implied Move | Range |

|---|---|---|---|---|

| Monthly OPEX | Feb 20, 2026 | 10 | ±6.67% | $9.21 - $10.53 |

| Triple Witch | Mar 20, 2026 | 38 | ±12.70% | $8.62 - $11.12 |

Note: The $12.50 strike sits above the March triple witch upper range ($11.12), indicating the buyer expects an outsized move beyond normal implied volatility - likely from earnings surprise or strategic catalyst.

Company Profile

| Attribute | Detail |

|---|---|

| Company | NCR Voyix Corporation |

| Sector | Technology / Digital Commerce |

| Industry | Restaurant & Retail POS/Software |

| Market Cap | $1.36 billion |

| Employees | 14,000 |

| HQ | Atlanta, GA |

| Website | ncrvoyix.com |

Business Overview

NCR Voyix provides digital commerce solutions across three segments:

- Retail: POS software, self-checkout, inventory management

- Restaurants: End-to-end technology (Aloha platform)

- Digital Banking: (Divested to Veritas Capital for $2.45B in Sept 2024)

Transformation Thesis: Hardware-to-software pivot with AI-accelerated platform, outsourced manufacturing (Ennoconn partnership), and margin expansion focus.

Fundamental Analysis

Recent Financial Performance

| Metric | Q3 2025 | YoY Change |

|---|---|---|

| Revenue | $684M | -3% |

| Adjusted EBITDA | $125M | +32% |

| Non-GAAP EPS | $0.31 | Beat by 35% |

| Recurring Revenue | $425M | +5% |

| Net Loss | -$17M | Improved from -$29M |

ARR Trajectory (Software Transformation KPI)

| Period | Total ARR | Software ARR |

|---|---|---|

| Q1 2025 | $1.62B | $775M |

| Q2 2025 | $1.68B | $799M |

| Q3 2025 | $1.70B (+5% YoY) | $798M (+8% YoY) |

2025 Guidance

| Metric | Range |

|---|---|

| Revenue | $2.65B - $2.67B |

| Adjusted EBITDA | $420M - $435M |

| Non-GAAP EPS | $0.85 - $0.90 |

| Adjusted FCF | $170M - $175M |

Balance Sheet

| Metric | Value |

|---|---|

| Cash | $282M |

| Total Debt | $1.1B |

| Debt/Equity | 96.2% |

| Interest Coverage | 1.4x |

Catalyst Calendar

Near-Term (Next 30 Days)

| Date | Event | Impact |

|---|---|---|

| Feb 26, 2026 | Q4/FY2025 Earnings | 🔴 HIGH - Primary catalyst |

| Feb 10, 2026 | Colruyt Group Partnership Announced | ✅ Completed (today) |

Medium-Term (Q1-Q2 2026)

| Date | Event | Impact |

|---|---|---|

| Q2 2026 | Hardware Net Revenue Recognition | 🟠 MEDIUM - Optics shift |

| Q1-Q2 2026 | AI Platform Adoption Metrics | 🟡 MEDIUM |

| Mar 20, 2026 | Triple Witch Expiration | 🟡 Technical |

Long-Term (Covered by Dec 2026 Expiry)

- Full year of software ARR growth visibility

- Complete Ennoconn hardware transition

- Multiple earnings cycles (Q1-Q3 2026)

- Potential strategic update/investor day

Analyst Sentiment

Consensus

| Metric | Value |

|---|---|

| Rating | Moderate Buy |

| Analysts | 8 |

| Buy | 5 |

| Hold | 2 |

| Sell | 1 |

Price Targets

| Source | Target | Upside |

|---|---|---|

| High | $20.00 | +103% |

| Average | $15.17 - $17.11 | +54% to +74% |

| Low (Goldman Sachs) | $11.50 | +17% |

| Option Strike | $12.50 | +27% required |

Observation: The $12.50 strike is between the Goldman bear case ($11.50) and consensus average (~$16). This suggests the buyer expects at minimum a re-rating toward consensus.

Institutional Ownership

| Metric | Value |

|---|---|

| Institutional Ownership | 97% |

| Total Holders | 560 institutions |

| Shares Held | 193.98M |

Notable Recent Activity

| Institution | Action | Shares |

|---|---|---|

| General American Investors | +262,451 | 1.09M total |

| Allianz Asset Management | New position | ~$3.05M |

| Optimize Financial | New position | 104,000 shares |

Major Holders: BlackRock, Vanguard, Greenhouse Funds, Shapiro Capital, State Street, Fuller & Thaler, FMR

Trade Thesis Evaluation

Bull Case (What the Buyer Sees)

- Margin Expansion Story: Q3 showed 32% EBITDA growth despite -3% revenue - transformation is working

- Earnings Catalyst: Feb 26 could deliver beat + strong 2026 guidance

- Valuation Gap: Trading at $9.83 vs $15-$18 analyst targets = 50%+ upside

- Software Re-Rating: As hardware fades, higher-margin software ARR deserves tech multiples

- AI Optionality: January 2026 AI platform launch positions for innovation narrative

- Time Premium: 10 months allows multiple catalysts to play out

Bear Case (Risks to Position)

- Revenue Decline: Top line still shrinking (-3% YoY)

- Execution Risk: Hardware transition with Ennoconn could disrupt

- Debt Load: 96% debt/equity, 1.4x interest coverage = limited margin for error

- Competition: Toast, Square, Shopify gaining share in restaurant/retail

- Stock Decline: -15% since October despite earnings beats suggests market skepticism

Risk/Reward Assessment

| Scenario | Stock Price | Option Value | P&L |

|---|---|---|---|

| Base (Consensus) | $16.00 | $3.50 | +$5.75M (+192%) |

| Bull (High Target) | $20.00 | $7.50 | +$15.75M (+525%) |

| Strike Hit | $12.50 | $0-$0.50 | -$2.5M to -$1.75M |

| Bear (No Move) | $9.83 | $0.00 | -$3M (-100%) |

Breakeven: $13.70 (39% above current)

Signal Interpretation

What This Flow Signals

Conviction Level: HIGH

The $3M premium on a single, directional OTM call position with 10-month duration indicates:

- Earnings Bet: Buyer expects Feb 26 earnings to catalyze upward re-rating

- Transformation Thesis: Position sized for software pivot success over 2026

- Asymmetric Setup: 219x Vol/OI = clean entry, no position management

- Institutional Patience: December expiry = not a quick flip

Comparable Flow Patterns

This type of flow (large premium, long-dated, OTM, new position) historically appears before:

- Earnings surprises

- Strategic announcements (M&A, partnerships)

- Analyst upgrades

- Sector re-ratings

Conclusion

Trade Quality Score: 8/10

| Factor | Score | Notes |

|---|---|---|

| Size/Conviction | 10/10 | $3M = serious capital at risk |

| Timing | 8/10 | 16 days before major earnings |

| Strike Selection | 7/10 | Aggressive but within analyst range |

| Catalyst Alignment | 9/10 | Feb 26 earnings + transformation |

| Risk/Reward | 7/10 | Breakeven requires 39% move |

Interpretation: This is a high-conviction institutional bet on VYX's software transformation succeeding. The buyer is willing to pay $3M for 10 months of optionality, suggesting they see asymmetric upside from earnings catalysts and the margin expansion story.

Key Monitoring Triggers:

- Feb 26 earnings: Watch for EPS beat, ARR growth, 2026 guidance

- Software ARR trajectory: 8%+ YoY growth validates thesis

- Analyst revisions: Upgrades would support re-rating thesis

- Institutional 13F filings: Track for position confirmation

Disclaimer

This analysis is for informational purposes only and does not constitute investment advice. Options trading involves substantial risk of loss. The unusual options activity discussed may not predict future price movements. Always conduct your own due diligence and consult with a qualified financial advisor before making investment decisions.

Generated by Options Flow Analysis System | February 10, 2026