💳 XLY $5.7M LEAPS Bet - Smart Money Loading Up on Consumer Discretionary Recovery! 🛍️

📅 December 23, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $5.7 MILLION on XLY call LEAPS this morning in two quick trades! This massive bullish bet bought 9,000 contracts of $127.50 strike calls expiring December 18, 2026 - a full-year bet that consumer discretionary names will rally 4.5% from current levels. With XLY trading at $121.94 and struggling to break through resistance, smart money is positioning for a major consumer spending recovery through 2026. Translation: Institutional investors are betting big that Amazon, Tesla, and the broader consumer discretionary sector will power higher over the next year!

📊 ETF Overview

Consumer Discretionary Select Sector SPDR Fund (XLY) is the premier vehicle for capturing consumer discretionary sector exposure:

- Net Assets: $23.26 billion AUM

- Expense Ratio: 0.08% (ultra-low cost)

- Dividend Yield: 0.76%

- Total Holdings: 52 stocks from the S&P 500

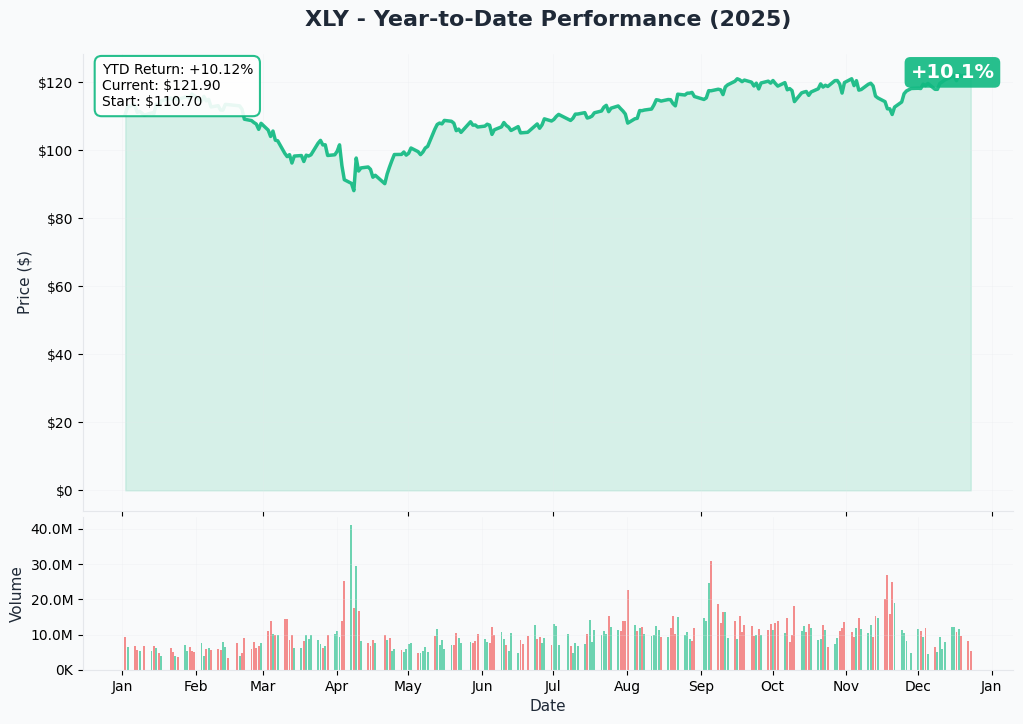

- Current Price: $121.94 (near 52-week high of $123.63)

- YTD Performance: +8.30% (significantly underperforming S&P 500)

Top Holdings (Concentration Risk Alert!):

- Amazon (AMZN): 22.91% - E-commerce and cloud computing giant

- Tesla (TSLA): 20.25% - Electric vehicles and AI/robotics

- Home Depot (HD): 5.96% - Home improvement retail

- McDonald's (MCD) - Quick service restaurants

- Nike (NKE) - Athletic footwear and apparel

- Starbucks (SBUX) - Coffee chain turnaround story

- Lowe's (LOW) - Home improvement

- TJX Companies (TJX) - Off-price retail

Important: The top 2 holdings (Amazon + Tesla) account for 43% of the entire fund - this creates massive concentration risk and means XLY's performance is heavily driven by just two mega-cap names.

💰 The Option Flow Breakdown

The Tape (December 23, 2025):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|

| 11:20:10 | XLY | ASK | BUY | CALL $127.50 | 2026-12-18 | $2.9M | $127.50 | 3,000 | $121.94 | ~$9.67 |

| 11:21:49 | XLY | ASK | BUY | CALL $127.50 | 2026-12-18 | $2.8M | $127.50 | 6,000 | $121.94 | ~$9.33 |

🤓 What This Actually Means

This is a massive bullish LEAPS position that screams institutional conviction! Here's what went down:

- 💸 Total premium deployed: $5.7M combined across both trades (likely a single order split)

- 🎯 Strike selection: $127.50 is 4.5% above current price - betting on multi-expansion rally

- ⏰ Time horizon: 360 days to expiration gives PLENTY of time for thesis to play out

- 📊 Size matters: 9,000 contracts represents 900,000 shares worth ~$109M of XLY exposure

- 🏦 Execution pattern: Split into two trades 99 seconds apart - classic institutional block order

What's really happening here:

This trader is making a multi-month bet that consumer discretionary stocks will significantly outperform through 2026. They're paying an average of ~$9.50 per contract for $127.50 December 2026 calls, which means they need XLY above $137 to profit at expiration - that's a 12.3% rally required for breakeven. But here's the kicker: they're not holding to expiration. This is a 2026 growth thesis play banking on:

- Amazon Q4 earnings blowout (January 29, 2026) driving the ETF higher

- Tesla delivery numbers (early January) beating depressed expectations

- Consumer spending resilience through holiday season and into 2026

- Fed rate cuts boosting discretionary spending power

- Sector rotation from defensive to cyclical as recession fears fade

The $127.50 strike is positioned exactly at a major gamma resistance level according to our data - they're betting the ETF breaks through that ceiling and runs higher through 2026.

Why LEAPS instead of shorter-term options? The one-year expiration provides insurance against near-term volatility around earnings, tariff announcements, and macro uncertainty. They can ride through bumpy periods knowing they have 360 days for the consumer discretionary recovery thesis to materialize.

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

XLY is showing a choppy but ultimately positive 2025 - up +8.3% YTD trading at $121.94 (started the year around $112). The chart reveals a tale of two halves: early 2025 struggled with discretionary underperforming staples significantly through March, then a powerful rally from $95 in April to near all-time highs of $123.63 by December.

Key observations:

- 🚀 H2 Rally: XLY surged 24.2% over six months starting mid-2025, dramatically outpacing consumer staples (XLP) which fell 3.3%

- 📈 Relative strength: The XLY:XLP ratio hit fresh highs not seen since February 2025, signaling robust risk-on sentiment

- 🎢 Volatility: 4.08% volatility vs consumer staples' 2.74% - this isn't a boring defensive play

- 📊 Concentration impact: Late 2025 rally driven heavily by Tesla's 50% H2 surge and Amazon approaching $260

- ⚠️ Recent consolidation: Trading in tight range at resistance - breakout or breakdown coming?

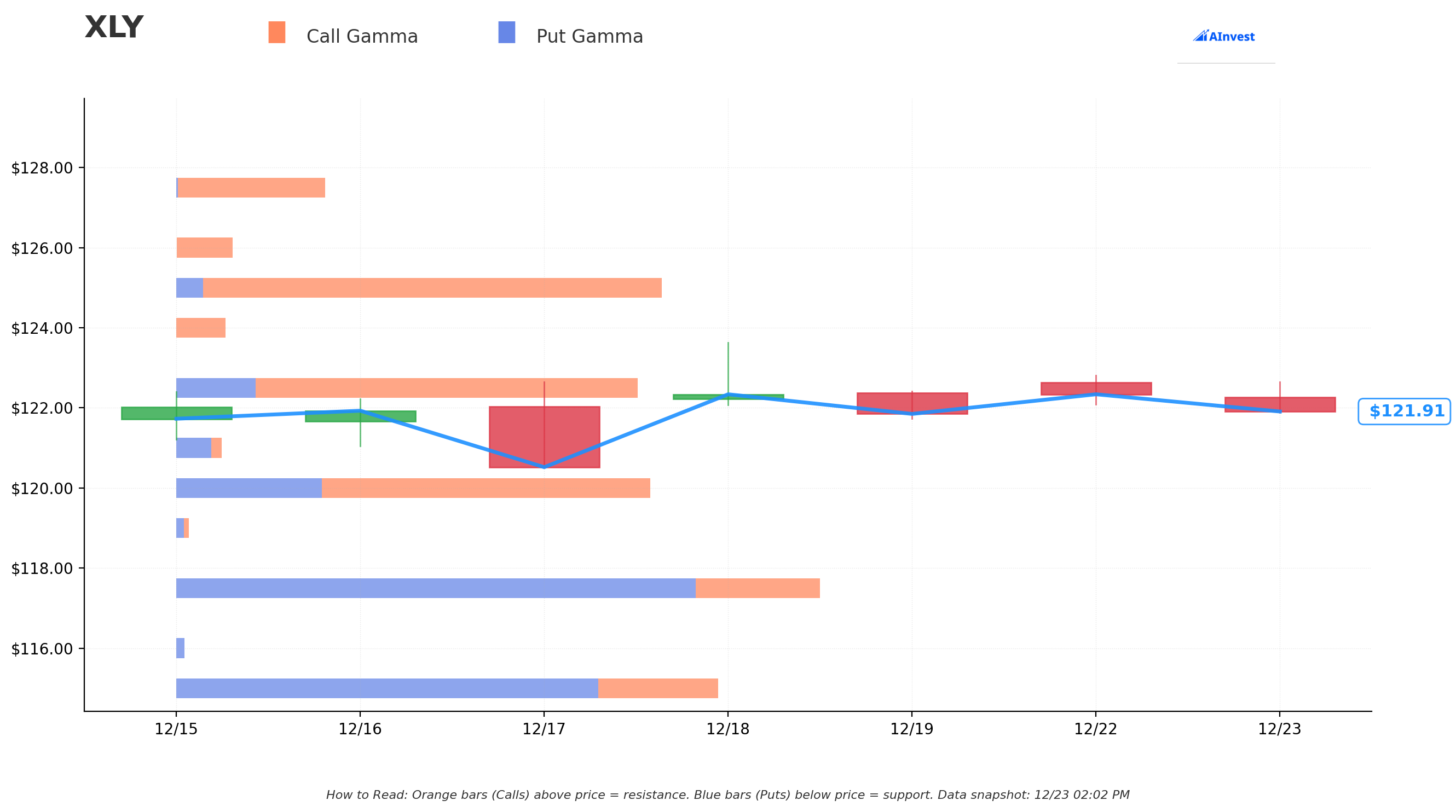

Gamma-Based Support & Resistance Analysis

Current Price: $121.94

The gamma exposure map reveals critical price magnets and barriers for XLY's near-term trajectory:

🔵 Support Levels (Put Gamma Below Price):

- $121.25 - Put Wall with strong 0.57 put gamma (IMMEDIATE FLOOR - must hold!)

- $120 - Secondary support zone

- $118.50 - Major support cluster aligning with monthly implied move lower range

🟠 Resistance Levels (Call Gamma Above Price):

- $123.75 - First resistance with 0.42 call gamma (fighting through now)

- $125.00 - MASSIVE Call Wall with 0.65 call gamma (STRONGEST RESISTANCE LEVEL!)

- This is the HVL (High Volatility Level) - maximum gamma exposure

- Also the exact call wall - dealers will sell aggressively here

- $127.50 - Secondary resistance at 0.42 call gamma (EXACT STRIKE OF THIS TRADE!)

- $130.00 - Extended resistance with 0.39 call gamma

- $132.50+ - Clear air above if $130 breaks

What this means for traders:

XLY is currently trading in a tight compression zone between $121.25 support and $125.00 resistance. The gamma data shows market makers holding HUGE positions at $125 (0.65 call gamma - the single largest level), which creates natural selling pressure as price approaches. This is textbook resistance.

Notice the trade positioning? The call buyer struck at exactly $127.50 - they're positioning for a breakout ABOVE the massive $125 call wall. They expect that once XLY clears $125, it accelerates through $127.50 toward $130+. Smart positioning above the major resistance cluster.

Net GEX Bias: Moderately bullish with call gamma dominating strikes above $125, but the immediate $125 wall creates short-term headwinds. The put wall at $121.25 provides a safety net just below current price.

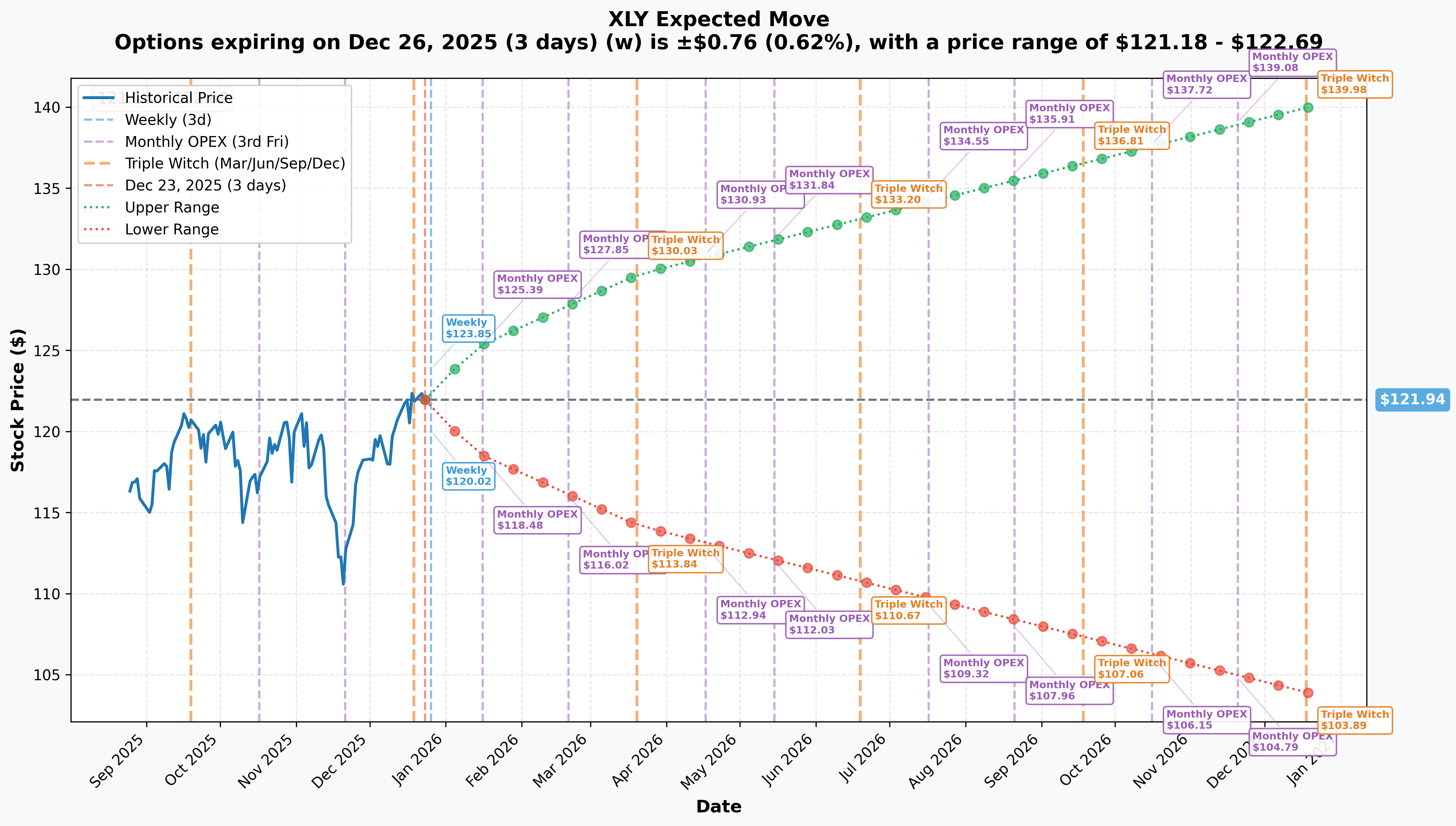

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 26 - 3 days): ±$0.76 (±0.62%) → Range: $121.18 - $122.69

- 📅 Monthly OPEX (Jan 16 - 24 days): ±$3.46 (±2.84%) → Range: $118.48 - $125.39

- 📅 Quarterly Triple Witch (Mar 20 - 87 days): ±$7.76 (±6.36%) → Range: $114.18 - $129.69

- 📅 Yearly LEAPS (Dec 18, 2026 - 360 days - THIS TRADE!): ±$18.04 (±14.8%) → Range: $103.89 - $139.98

Translation for regular folks:

Options traders are pricing in a TINY 0.6% move ($0.76) through year-end - basically expecting nothing through Christmas week. But looking out to January monthly OPEX, the market expects a 2.8% move ($3.46) which captures Amazon earnings on January 29th and Tesla Q4 deliveries in early January. That's where the real action begins!

The December 2026 expiration (when this $5.7M trade expires) has an upper range of $139.98 - meaning the market thinks there's a possibility XLY could trade 14.8% higher over the next year. At $139.98, the $127.50 calls would be worth $12.48 intrinsically - a nice profit from the ~$9.50 entry.

Key insight: The sharp increase in implied volatility from 0.6% (weekly) to 2.8% (monthly) reflects massive earnings uncertainty around Amazon and Tesla in January. The call buyer is positioning BEFORE these catalysts hit, expecting positive surprises to propel XLY higher through 2026.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Amazon Q4 2025 Earnings - January 29, 2026 (37 DAYS AWAY!) 📊

With Amazon comprising 22.91% of XLY, this single earnings report will massively impact the ETF's trajectory. Wall Street expects blockbuster results driven by holiday shopping and AWS growth:

- 📊 Revenue Consensus: $211.26B (range: $206B-$214.46B) - would be all-time record

- 💰 EPS Consensus: $1.95 (range: $1.61-$2.23)

- 🤖 AWS Critical: Q3 showed robust 20.2% YoY growth to $132B annualized run rate - sustainability key

- 🛍️ Holiday Season: Record-breaking 2025 holiday sales with $14.25B Cyber Monday should boost Amazon

- 📱 AI Impact: Generative AI drove 670% YoY traffic increase to retail sites on Cyber Monday, benefiting Amazon's platform

- 💸 Advertising Revenue: Q3 hit $17.6B (+22% YoY) - continued strength expected

Analyst Expectations: Average price target $296.12 (+30% upside from recent $229 level), with Street expecting management to guide toward $213B sales for Q4. Any beat and raise would ignite XLY rally.

Tesla Q4 2025 Delivery Report - Early January 2026 (WITHIN 2 WEEKS!) 🚗

Tesla's 20.25% weighting makes delivery numbers make-or-break for XLY. Expected first week of January:

- 📊 Delivery Consensus: 450,000-455,000 units for Q4 2025

- ⚠️ Bear Case Risk: Some analysts warn of potential miss as low as 405,000 units

- 📈 Q3 Comparison: Q3 delivered record 497,000 vehicles - Q4 could show sequential decline

- 🚀 Stock Momentum: TSLA surged 50% in H2 2025 to record $495, driven by AI/robotics narrative beyond automotive fundamentals

- 💰 Valuation Disconnect: Stock trading on future optionality, not current deliveries - beat/miss may not matter as much

2025 Holiday Shopping Season - JUST REPORTED! 🎁

Strong holiday results just confirmed, providing immediate tailwind for consumer discretionary:

- 💳 Total Spending: 202.9 million US consumers shopped Thanksgiving through Cyber Monday - largest turnout since NRF began tracking in 2017

- 📈 Growth Rate: Holiday retail spending rose 4.2% this season, with full Nov-Dec projected to exceed $1 trillion for first time

- 💻 E-commerce Dominance: Cyber Monday hit record $14.25B (+7.1% YoY), with mobile at record 56.1% of online spend

- 🎮 Category Leaders: Electronics led with 5.8% sales growth driven by "high-performance devices in the AI era"

This validates the consumer discretionary thesis heading into 2026!

🚀 Near-Term Catalysts (Q1-Q2 2026)

Federal Reserve Rate Policy - Next Meeting January 29, 2026 💰

The Fed delivered its third consecutive 25bp rate cut in December, bringing rates to 3.50%-3.75%, but forward guidance turned hawkish:

- 📊 2026 Outlook: Dot plot signals just ONE more rate cut in 2026 (vs market hoping for 3-4 cuts)

- 🎯 January Meeting: 75.6% probability Fed holds rates steady (up from 65% a week prior)

- 💳 Consumer Impact: Average 30-year mortgage at 6.19% vs 6.69% year ago - providing hundreds in annual savings

- ⚠️ Inflation Concern: PCE at 2.8%, well above 2% target, with Powell attributing bulk to Trump tariffs

Positive for discretionary: Lower rates boost big-ticket purchases (homes, autos, appliances), but tariff inflation could offset benefits.

Tariff Policy Implementation Risk - Ongoing Through Q1 2026 🚨

Trump administration tariffs pose significant headwind for consumer discretionary in 2026:

- 💸 Household Impact: Average tax increase of $1,400 per US household in 2026 (up from $1,100 in 2025)

- 📉 Margin Pressure: Retailers face 20% YoY average cost increases, with early 2026 margin compression expected as they discount to clear inventory

- 🛍️ Spring 2026 Risk: NRF warns Q1 2026 shipments "will undoubtedly be impacted" with higher costs and reduced product availability

- 📊 XLY fell 7.2% in one week during tariff shockwaves vs just 2.4% for staples - high sensitivity confirmed

Winners & Losers: Citi flagged Best Buy as top tariff casualty; Goldman highlights Target and Dick's Sporting Goods for pricing power resilience

Company-Specific Turnaround Narratives:

-

Nike (NKE) - Multi-Year Restructuring: Stock down 22% in 2025 after disappointing Q2 fiscal 2026 results (EPS down 32%) with sixth consecutive quarter of China sales declines (-17%). Analysts describe "slow grind" recovery rather than quick turnaround.

-

Starbucks (SBUX) - "Back to Starbucks" Strategy: CEO Brian Niccol's turnaround showing early progress with first comparable sales gains in 1.5 years, but facing open-ended union strikes and intense competition. Analysts forecast fiscal 2026 EPS of $2.44 (+50% from 2025).

-

Home Depot (HD) - Continued Pressure: Q3 sales up just 0.2% comp with EPS miss ($3.74 vs $3.84 expected). CFO cited "ongoing consumer uncertainty and continued pressure in housing" with full-year EPS forecast cut to -5% decline from prior -2% expectation.

📊 Medium-Term Catalysts (H2 2026)

Consumer Confidence Trajectory 📉

Multiple indicators signal deteriorating consumer sentiment heading into 2026:

- 📊 Conference Board Index (December 2025): Fell to 89.1 vs expected 91.0, fifth consecutive monthly decline

- 🚨 Expectations Index: Held at 70.7, remaining below critical 80.0 recession threshold for 11 consecutive months - historically reliable recession indicator

- ⚠️ Present Situation: Index plummeted 9.5 points to 116.8, sharpest drop since September 2024

However, positive datapoint: Prosper Insights December 2025 snapshot shows US consumer closing year on "more positive footing" with confidence rising

2026 Spending Outlook:

- Real consumer spending growth expected to expand 2.2% in 2026, down from 2.6% in 2025

- Bifurcated Economy: Higher-income consumers spending strongly boost XLY, while lower-income cutting back - creates "two-speed" economy

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, Amazon/Tesla earnings catalysts, and sector dynamics, here are scenarios through December 2026 expiration:

📈 Bull Case (35% probability)

Target: $135-$140

How we get there:

- 🚀 Amazon crushes Q4 earnings (Jan 29) with revenue toward $214B high-end, AWS growth acceleration to 22%+, and strong Q1 guidance

- 🔋 Tesla Q4 deliveries beat 460K+ units, stock holds $500+ on AI/robotics narrative

- 💳 Consumer spending resilience: Holiday momentum ($1T+ spending) carries into Q1-Q2 2026

- 💰 Fed delivers 2 more cuts in 2026 (vs current 1-cut expectation), boosting discretionary spending

- 📊 Tariff relief: Trump administration moderates tariff implementation or provides exemptions for key categories

- 🎯 Sector rotation: XLY:XLP ratio extends to fresh multi-year highs as recession fears fade completely

- 📈 Technical breakout: XLY clears $125 call wall, then $127.50, accelerating to $130+ on momentum

- 🔄 Turnaround execution: Starbucks and Nike show tangible progress in H1 2026

Key metrics needed:

- Amazon Q4 revenue >$212B with Q1 guide >$155B

- Tesla full-year 2025 deliveries >1.8M (implying strong Q4)

- Consumer discretionary earnings growth hits double-digit targets for 2026

- XLY trading above $125 for sustained period breaks resistance

Call P&L in Bull Case:

- XLY at $137 by Dec 2026: Calls worth $9.50 intrinsically, breakeven (0% ROI)

- XLY at $140 by Dec 2026: Calls worth $12.50, profit = $3.00/share × 9,000 = $2.7M gain (47% ROI)

- XLY at $145 by Dec 2026: Calls worth $17.50, profit = $8.00/share × 9,000 = $7.2M gain (126% ROI!)

Probability assessment: 35% because it requires strong execution from Amazon/Tesla AND macro cooperation (Fed cuts, tariff relief). The sector is projected for double-digit earnings growth in 2026, supporting this scenario.

🎯 Base Case (45% probability)

Target: $125-$132 range (MODEST APPRECIATION)

Most likely scenario:

- ✅ Amazon meets expectations with solid Q4 (~$211B revenue, $1.95 EPS) and conservative Q1 guidance

- 📊 Tesla delivers in-line 450-455K Q4 units, stock consolidates $450-500 range on mixed sentiment

- 🛍️ Consumer spending moderates but doesn't collapse - 2.2% real spending growth in 2026 as expected

- 💰 Fed delivers 1 cut in 2026 as currently projected, maintaining restrictive stance

- 🚨 Tariffs implemented gradually with some pain but manageable margin compression

- 📈 XLY grinds higher slowly breaking through $125 call wall by Q2 2026, consolidating at $127.50 area

- ⚖️ Mixed company performance: Amazon/Tesla carry the load, offsetting weakness in Nike/Home Depot

- 🎢 Volatility persists: XLY's 4.08% volatility creates choppy path higher

Call P&L in Base Case:

- XLY at $130 by Dec 2026: Calls worth $2.50 intrinsically, loss = -$7.00/share × 9,000 = -$6.3M loss (-110% - total loss with some recovery)

- XLY at $132 by Dec 2026: Calls worth $4.50 intrinsically, loss = -$5.00/share × 9,000 = -$4.5M loss (-79%)

Why 45% probability: Most realistic outcome given current setup. XLY slowly appreciates but not enough to make LEAPS profitable at these strikes. The call buyer likely plans to sell earlier if XLY hits $128-130 in H1 2026 for 30-50% gain, not holding to expiration.

Strategic insight: This isn't a "hold to expiration" trade - it's a 6-9 month position where they take profits if XLY rallies 5-8% by mid-2026 around Amazon's strong guidance and consumer resilience confirmation.

📉 Bear Case (20% probability)

Target: $110-$118 (TEST MONTHLY SUPPORT)

What could go wrong:

- 😰 Amazon disappoints with Q4 revenue <$208B or weak Q1 guidance citing consumer slowdown - stock drops to $200-210

- 🚗 Tesla Q4 delivery miss to 430-440K range, raising concerns about 2026 growth trajectory - stock falls to $400s

- 📉 Consumer spending cracks: Conference Board Expectations Index below 80 for 11 months finally manifests in actual spending decline

- 💸 Tariff shock: Full $1,400/household tax increase hits in Q1 2026, crushing discretionary purchases

- 🏚️ Housing market deterioration: Home Depot's "ongoing pressure" worsens as high rates persist

- 🌍 Recession fears resurge: Macro data weakens, Fed can't cut despite slowing growth (stagflation scenario)

- 📊 Valuation compression: XLY's 30.56x trailing P/E and 28.6x forward P/E collapses as growth disappoints

- 🔨 Technical breakdown: XLY breaks $121.25 put wall, cascades to $118.50 monthly support, then $114-115

Critical support levels:

- 🛡️ $121.25: Put wall (0.57 gamma) - MUST HOLD or momentum shifts bearish

- 🛡️ $118.48: Monthly OPEX implied move lower range - strong technical support

- 🛡️ $114.18: Quarterly implied move floor - disaster scenario

Call P&L in Bear Case:

- XLY at $118 by Dec 2026: Calls expire worthless, loss = -$9.50/share × 9,000 = -$8.55M (150% - total wipeout with premium loss)

- XLY at $110 by Dec 2026: Calls expire worthless, loss = -$9.50/share × 9,000 = -$8.55M (150% - same total loss)

Probability assessment: Only 20% because it requires multiple negative catalysts to align. Consumer discretionary fundamentals remain supported by affluent consumer spending and holiday season strength just confirmed. However, XLY's concentration in Amazon/Tesla creates outsized downside risk if either disappoints materially.

💡 Trading Ideas

🛡️ Conservative: Wait for Amazon/Tesla Earnings Clarity

Play: Stay on sidelines until after January 29th Amazon earnings and early January Tesla deliveries

Why this works:

- ⏰ Binary events ahead: Amazon earnings (Jan 29) and Tesla deliveries (early Jan) will determine 43% of XLY's direction

- 💸 Avoid concentration risk: Top 2 holdings account for 43% of fund - too much single-stock dependency

- 📊 **XLY at resistance:** Trading just below $125 call wall with 0.65 gamma - breakout uncertain

- 🎯 Better entry post-earnings: If Amazon beats and guides well, buy the confirmed strength; if disappoints, buy the pullback to $118-120

- ⚠️ **Tariff uncertainty:** Q1 2026 implementation risk still unquantified

- 💰 Valuation stretched: 28.6x forward P/E ties for highest in S&P 500 - limited margin of safety

Action plan:

- 👀 Watch Amazon Q4 earnings January 29th for revenue ($211B+ target), AWS growth (20%+ needed), Q1 guidance quality

- 🚗 Monitor Tesla Q4 deliveries early January for beat/miss vs 450-455K consensus

- 📊 Track consumer confidence data - need Expectations Index back above 80.0 for sustainable recovery

- 🎯 If XLY breaks $125 on strong earnings, enter on confirmation; if pulls back to $118-120, buy the dip

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 5-10% drawdown if earnings disappoint. Get better entry with more clarity on 2026 consumer trajectory.

⚖️ Balanced: April $125 Calls (Ride the Amazon Wave)

Play: Buy April 2026 $125 calls after Amazon earnings (assuming beat)

Structure: Buy XLY April 17, 2026 $125 calls

Why this works:

- 🎯 Strike at key resistance: $125 is the massive call wall - if it breaks, momentum accelerates

- ⏰ Timeline: 3.5 months to expiration captures Amazon Q1 earnings, consumer spending data, Fed policy updates

- 💰 Lower cost: Shorter duration means cheaper premium than December LEAPS (~$4-5 vs $9.50)

- 📈 Defined catalyst path: Amazon earnings → Valentine's/President's Day shopping → Q1 earnings preview

- 🎢 Manageable risk: Can risk 3-5% of portfolio vs 10%+ for LEAPS position

- 🛡️ Natural stop: If XLY fails at $125 resistance after earnings, exit for small loss

Estimated P&L (enter post-Amazon earnings):

- 💰 Pay ~$4.50-5.00 per contract for April $125 calls

- 📈 Profit scenario: XLY rallies to $130 by April expiration = $5.00 intrinsic value, breakeven to small gain

- 🚀 Home run: XLY hits $132-135 by April = $7-10 value, 40-100% ROI

- 📉 Loss scenario: XLY stays below $123 = lose 50-80% of premium

- 💀 Max loss: XLY below $125 at expiration = lose full premium ($4.50-5.00)

Entry conditions:

- ✅ ONLY enter if Amazon beats Q4 with revenue >$211B and guides Q1 >$155B

- ✅ Wait 1-2 days post-earnings for initial volatility to settle

- ✅ Look for XLY holding above $122.50 showing strength

- ❌ Skip if Amazon disappoints or guides conservatively

Position sizing: Risk 3-5% of portfolio maximum

Exit strategy:

- 🎯 Take 50% off at 50% gain ($6.75-7.50 level) to lock profits

- 🚀 Let remaining 50% run toward $130+ target

- 🛡️ Hard stop if XLY breaks below $121.25 put wall (cut loss at -30 to -40%)

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

🚀 Aggressive: Copy the LEAPS Trade - December $127.50 Calls (ADVANCED!)

Play: Replicate the institutional LEAPS position in smaller size

Structure: Buy XLY December 18, 2026 $127.50 calls

Why this could work:

- 📊 Following smart money: $5.7M institutional bet suggests strong conviction in 2026 consumer recovery

- ⏰ Full year to work: 360 days provides cushion for thesis to materialize despite near-term volatility

- 🎯 Strategic strike: $127.50 positioned above major $125 resistance - betting on breakout AND continuation

- 💰 Amazon/Tesla double catalyst: Both report within weeks - potential for massive January rally

- 📈 **Sector tailwinds:** Consumer discretionary projected for double-digit earnings growth in 2026

- 🔄 Multiple exit opportunities: Can take profits at $128-130 (6-8 months) or hold for larger move

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: ~$9.50 per contract ($950 per lot) ties up significant capital

- 📊 High breakeven: Need XLY above $137 (12.3% rally) to profit at expiration

- ⏰ Time decay: Theta burns value steadily if XLY doesn't move

- 🚨 **Concentration risk:** 43% in Amazon/Tesla means earnings disappointments crush position

- 💸 **Tariff wildcard:** $1,400/household tax could derail consumer spending unpredictably

- 📉 **Valuation risk:** 28.6x P/E vulnerable to multiple compression if growth disappoints

- 🎢 Could lose 100% if XLY trades sideways or lower through 2026

Estimated P&L:

- 💰 Cost: ~$9.50 per contract (current market)

- 📈 Profit scenario: XLY at $135 by mid-2026 = sell at ~$10-12 (5-25% gain), then reassess

- 🚀 Home run: XLY at $140 by Dec 2026 = $12.50 intrinsic (32% ROI)

- 🎯 Max gain: XLY at $145+ by Dec 2026 = $17.50+ intrinsic (84%+ ROI)

- 📉 Partial loss: XLY at $130 by Dec 2026 = $2.50 intrinsic (-74% loss)

- 💀 Total loss: XLY below $127.50 at expiration = expire worthless (-100%)

CRITICAL REQUIREMENTS - DO NOT attempt unless you:

- ✅ Have 12+ months investment horizon and won't panic on short-term volatility

- ✅ Can afford to lose ENTIRE premium (real possibility if consumer spending collapses)

- ✅ Understand LEAPS require patience - not a quick flip trade

- ✅ Plan to take partial profits at $130-132 levels (don't be greedy)

- ✅ Have conviction in Amazon/Tesla executing through 2026

- ✅ Can mentally handle 40-60% drawdowns during consolidation periods

- ⏰ Monitor quarterly and take profits incrementally rather than holding to expiration

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced only

Probability of profit at expiration: ~30-35% (but most traders will exit earlier at profit/loss thresholds)

Smart execution: Buy 1/3 position now, 1/3 after Amazon earnings if bullish, 1/3 if XLY breaks $125. Scale in to reduce risk.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🎯 Extreme concentration in Amazon (22.91%) and Tesla (20.25%): Combined 43% weighting means XLY is essentially a leveraged bet on these two mega-caps. Any disappointment from either company tanks the ETF regardless of other holdings. This creates "sketchy" fundamental analysis according to analysts. Amazon earnings January 29th and Tesla deliveries early January are make-or-break events.

-

💸 Tariff implementation could crush margins and consumer spending in Q1 2026: Average household faces $1,400 tax increase in 2026 with retailers seeing 20% YoY cost increases and forced to discount heavily. NRF warns Q1 2026 shipments "will undoubtedly be impacted" with higher costs and reduced availability. Historical precedent: XLY fell 7.2% in one week during tariff shockwaves vs just 2.4% for staples.

-

📉 Consumer confidence at recessionary levels despite strong holiday spending: Conference Board Expectations Index below 80.0 for 11 consecutive months - historically reliable recession indicator. Present Situation Index plummeted 9.5 points in December, sharpest drop since September 2024. This creates "two-speed economy" where only affluent consumers drive discretionary spending while lower/middle-income households severely strained.

-

💰 Valuation at nosebleed levels with 28.6x forward P/E: Consumer discretionary ties with tech for highest valuation among all S&P 500 sectors at 28.6x, while XLY trades at 30.56x trailing P/E. This is priced for PERFECT execution with operating margin expectations that "may be overly optimistic" per LPL Research given slowing spending and tariff pressures.

-

📊 Company-specific execution risks in major holdings: Home Depot Q3 comp sales up just 0.2% with full-year EPS cut to -5% decline citing "ongoing consumer uncertainty and pressure in housing". Nike down 22% in 2025 after sixth consecutive quarter of China declines (-17%) with gross margins expected to fall 175-225 basis points in Q3.

-

🚨 Fed turning hawkish despite rate cuts: December dot plot signals only ONE more 2026 rate cut vs market hoping for 3-4. 75.6% probability Fed holds steady at January meeting with PCE inflation at 2.8% well above 2% target. Higher-for-longer rates pressure big-ticket discretionary purchases (autos, appliances, home improvement).

-

📉 Recent institutional outflows signal profit-taking: 3-month outflows of -$571.78M and 1-month outflows of -$102.03M suggest smart money taking chips off the table near all-time highs. Only 5-day inflows of $418M provide recent support.

-

🎢 High volatility (4.08%) creates whipsaw risk: XLY's volatility nearly 50% higher than consumer staples (2.74%) with maximum drawdown since inception of -59.05% vs XLP's -35.89%. This isn't a stable defensive play - it's a cyclical growth bet that can gap violently.

-

⚠️ $125 gamma wall creates natural resistance: Massive 0.65 call gamma at $125 (highest single level) means market makers will systematically SELL into rallies to hedge exposure. Technical analysis shows strong resistance cluster at $123.29, $124.23, $124.84 before the $125 level. Would need sustained institutional buying to overcome.

-

🌍 Macro recession risk if consumer cracks in 2026: Real consumer spending growth expected to slow to 2.2% in 2026 from 2.6% in 2025 with discretionary spending intentions showing "sharp decline". If economy weakens materially, even strong Amazon/Tesla execution won't save XLY from 20-30% correction.

🎯 The Bottom Line

Real talk: Someone just bet $5.7 MILLION that consumer discretionary names will power significantly higher through 2026. This isn't a short-term earnings gamble - it's a strategic LEAPS position with a full year for the thesis to materialize. They're betting that Amazon's cloud dominance, Tesla's AI narrative, and record holiday shopping momentum will overcome tariff headwinds and consumer confidence concerns.

What this trade tells us:

- 🎯 Sophisticated player expects XLY to break through $125 resistance and run toward $130+ through 2026

- 💰 They're willing to pay $9.50/contract (8% of current ETF price) for 360-day optionality - that's conviction!

- ⏰ The timing (right before Amazon/Tesla January catalysts) shows they're positioning BEFORE major earnings events

- 📊 They structured at $127.50 strike just above the massive $125 gamma wall - betting on breakout AND continuation

- 🎪 This captures: Amazon Q4 (Jan 29), Tesla deliveries (early Jan), Fed meetings, consumer spending data, potential tariff relief, company turnarounds

This is NOT a "go all-in" signal - it's a "follow smart money IF catalysts confirm" signal.

If you own XLY or consumer discretionary stocks:

- ✅ Hold through Amazon earnings January 29th and Tesla deliveries early January

- 📊 Watch for breakout above $125 call wall - that's the trigger for acceleration

- ⏰ Set mental stop at $121.25 put wall to protect against breakdown

- 🎯 If both Amazon and Tesla deliver positive surprises, add to positions targeting $130-135

- 🛡️ Consider buying $125 April calls to leverage upside if earnings confirm strength

If you're watching from sidelines:

- ⏰ January 29th (Amazon earnings) and early January (Tesla deliveries) are decision points

- 🎯 Post-earnings rally through $125 would be BUY signal for momentum play

- 📈 Looking for: Amazon revenue >$211B with strong AWS growth, Tesla deliveries >455K, consumer confidence stabilizing

- 🚀 Longer-term (6-12 months), consumer discretionary double-digit earnings growth and sector rotation from staples support $130-135 targets

- ⚠️ Current 30.56x P/E valuation requires flawless execution - one stumble and it's back to $115-118

If you're bearish:

- 🎯 Wait for Amazon/Tesla to report before shorting - fighting 360-day LEAPS momentum is dangerous

- 📊 Key support at $121.25 put wall, then $118.48 monthly range - watch for breakdown

- ⚠️ Consumer confidence Expectations Index below 80 for 11 months supports bearish thesis

- 📉 Tariff implementation in Q1 2026 could be catalyst for 10-15% correction

- ⏰ Better to wait for failed breakout at $125 resistance than fight institutional LEAPS buying

Mark your calendar - Key dates:

- 📅 Early January 2026 - Tesla Q4 2025 delivery report (within 2 weeks!)

- 📅 January 29, 2026 - Amazon Q4 2025 earnings after market close (CRITICAL!)

- 📅 January 29, 2026 - FOMC meeting (same day as Amazon earnings)

- 📅 February-March 2026 - Q1 2026 consumer spending data showing tariff impact

- 📅 April 17, 2026 - Monthly OPEX (good timeframe for shorter-dated calls)

- 📅 Late April 2026 - Amazon Q1 2026 earnings

- 📅 December 18, 2026 - LEAPS expiration, triple witch

Final verdict: XLY's 2026 trajectory hinges entirely on Amazon and Tesla execution given their 43% combined weighting. The $5.7M LEAPS bet signals institutional conviction that record holiday spending and AI-driven e-commerce growth will overcome tariff headwinds and weakening consumer confidence. BUT at 28.6x forward P/E with massive concentration risk, there's ZERO margin for error.

Be patient. Let Amazon and Tesla report. If they deliver, join the party. If they disappoint, the $127.50 calls will get crushed and you'll get a better entry at $115-120.

The consumer discretionary recovery will still be there in February if it's real. Don't rush. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. LEAPS options can lose 100% of value if the underlying doesn't move as expected. ETF concentration in Amazon (22.91%) and Tesla (20.25%) creates significant single-stock risk. Always do your own research and consider consulting a licensed financial advisor before trading. The $5.7M institutional trade may represent portfolio hedging or complex positioning not applicable to retail traders.

About Consumer Discretionary Select Sector SPDR Fund (XLY): XLY provides liquid, low-cost (0.08% expense ratio) exposure to 52 consumer discretionary stocks from the S&P 500, with $23.26 billion in net assets. The fund tracks a market-cap-weighted index heavily concentrated in Amazon (22.91%), Tesla (20.25%), and Home Depot (5.96%), representing e-commerce, electric vehicles, and retail sectors.