🔥 AAP Massive $4.1M Call Bet - Smart Money Betting on Turnaround Rally! 🚀

📅 December 18, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Two MONSTER call trades totaling $4.1 MILLION just hit Advance Auto Parts (AAP) this morning! An aggressive buyer swept 15,000 contracts of $40 January 2026 calls in two separate blocks at 10:31 and 10:36 - that's $4.1M in premium on a stock trading just $42. Translation: Someone's making a HUGE bet that AAP's aggressive turnaround plan drives the stock higher by 20%+ over the next 5 weeks! With CEO Shane O'Kelly executing a radical restructuring (700+ store closures, $1.5B Worldpac sale, supply chain overhaul), this is institutional money betting the cleanup finally works.

📊 Company Overview

Advance Auto Parts (AAP) is a leading auto-parts retailer fighting its way back from years of underperformance:

- Market Cap: $2.57 Billion (down from peak of $10B+ in 2015)

- Industry: Retail Auto & Home Supply Stores

- Current Price: $42.17 (52-week range: $28.89 - $70.00)

- Primary Business: 4,000+ store locations serving professional installers (50% of revenue) and DIY consumers (50%)

- Competitive Position: #3 nationally with 18.0% market share, trailing AutoZone (32.3%) and O'Reilly (18.3%)

AAP operates in the "rational oligopoly" of auto parts retail - competing against two best-performing stocks over decades (AutoZone and O'Reilly). After a brutal decade of operational missteps following the 2013 General Parts acquisition, new CEO Shane O'Kelly is executing the most aggressive turnaround plan in company history.

💰 The Option Flow Breakdown

The Tape (December 18, 2025):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:31:35 | AAP | ASK | BUY | CALL $40 | 2026-01-23 | $2.1M | $40 | 5K | 2 | 5,000 | $42.17 | $4.15 |

| 10:36:25 | AAP | ASK | BUY | CALL $40 | 2026-01-23 | $2.0M | $40 | 15K | 2 | 10,000 | $42.22 | $4.10 |

Combined Position: 15,000 contracts at average price of $4.12 per share = $4.12M total premium

🤓 What This Actually Means

This is AGGRESSIVE BULLISH POSITIONING with institutional fingerprints all over it:

- 💸 Massive premium: $4.1M on a $2.57B market cap stock (0.16% of entire company!)

- 🎯 Strike selection: $40 is just 5.1% below current price ($42.17) - buyer expects stock to move QUICKLY

- ⏰ Tight expiration: Only 36 days to January 23rd - this is NOT a long-term bet, it's a catalyst play

- 📊 Size matters: 15,000 contracts = 1.5 MILLION shares (2.5% of total float!)

- 🏦 Two-tranche execution: Breaking into 5K + 10K blocks suggests institutional desk trying to minimize market impact

- 🔥 Open interest tiny: Only 2 contracts OI before this trade - this created the ENTIRE position

What's really happening here: This trader is paying $4.12 per share for the right to buy AAP at $40 through January 23rd. With stock at $42.17, these calls are $2.17 in-the-money - meaning they're paying $1.95 in pure time value. For this to profit, AAP needs to be above $44.12 by expiration (4.6% rally). But the REAL upside comes if the stock explodes toward $50-55 range (18-30% gains) - which would turn $4.1M into $10-15M+.

Unusual Score: 🔥🔥🔥 EXTREMELY HIGH (2,500x average size for AAP) - This is a handful of times per year type of activity. The Z-score of 0 indicates this is a new position (no historical comparison), but the Vol/OI ratio of 7,500x shows this is MASSIVE relative to existing positioning. Someone is putting serious money behind a near-term turnaround thesis.

📈 Technical Setup / Chart Check-Up

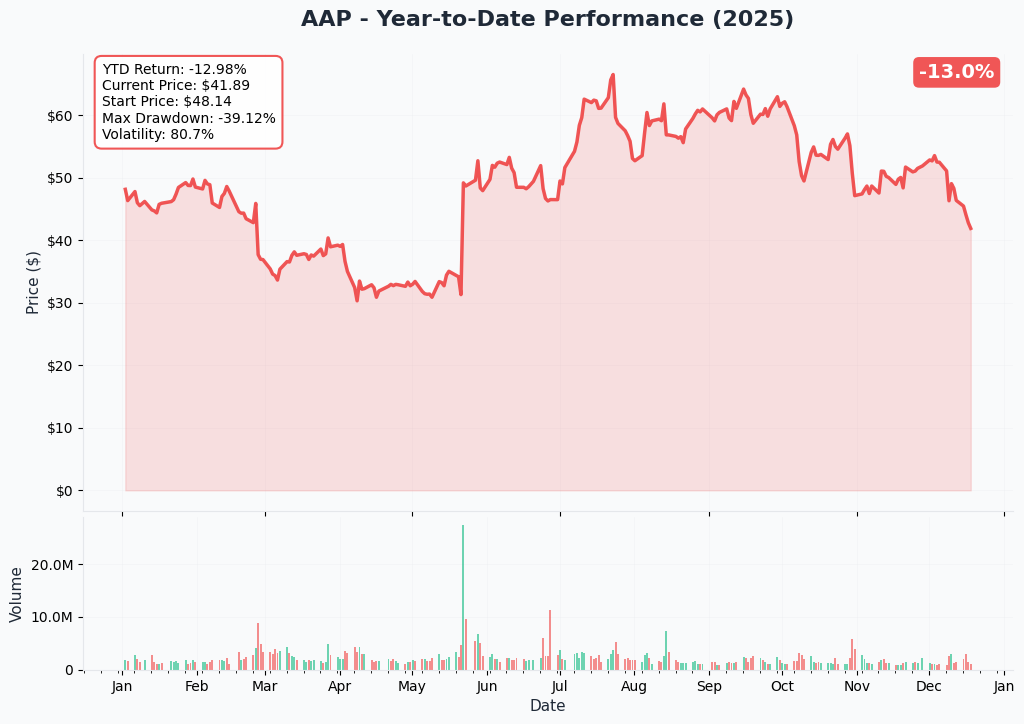

YTD Performance Chart

AAP has had a BRUTAL year - down -35.9% YTD with current price at $42.17 (started year at $65.87). But here's the interesting part: the chart shows signs of potential bottoming after hitting $28.89 lows in mid-year.

Key observations:

- 📉 Carnage in H1: Stock crashed from $65 to $28 (-57% max drawdown) as turnaround doubts mounted

- 🔄 Recovery attempt: Rallied from $28 lows to $70 in October (+142% move!) on restructuring announcement

- ⚠️ Recent pullback: Gave back gains to $42 level (-40% from October highs) - profit-taking or renewed doubts?

- 🎢 High volatility: 39.6% annualized vol shows this is a headline-driven battleground stock

- 📊 Volume spike zones: Huge volume around $40-45 level suggests strong institutional interest here

- 💡 Technical setup: Currently testing support at $40-42 range where this call buyer is positioned

The call buyer is essentially saying: "The October rally to $70 wasn't wrong - it was early. Fundamentals catching up now."

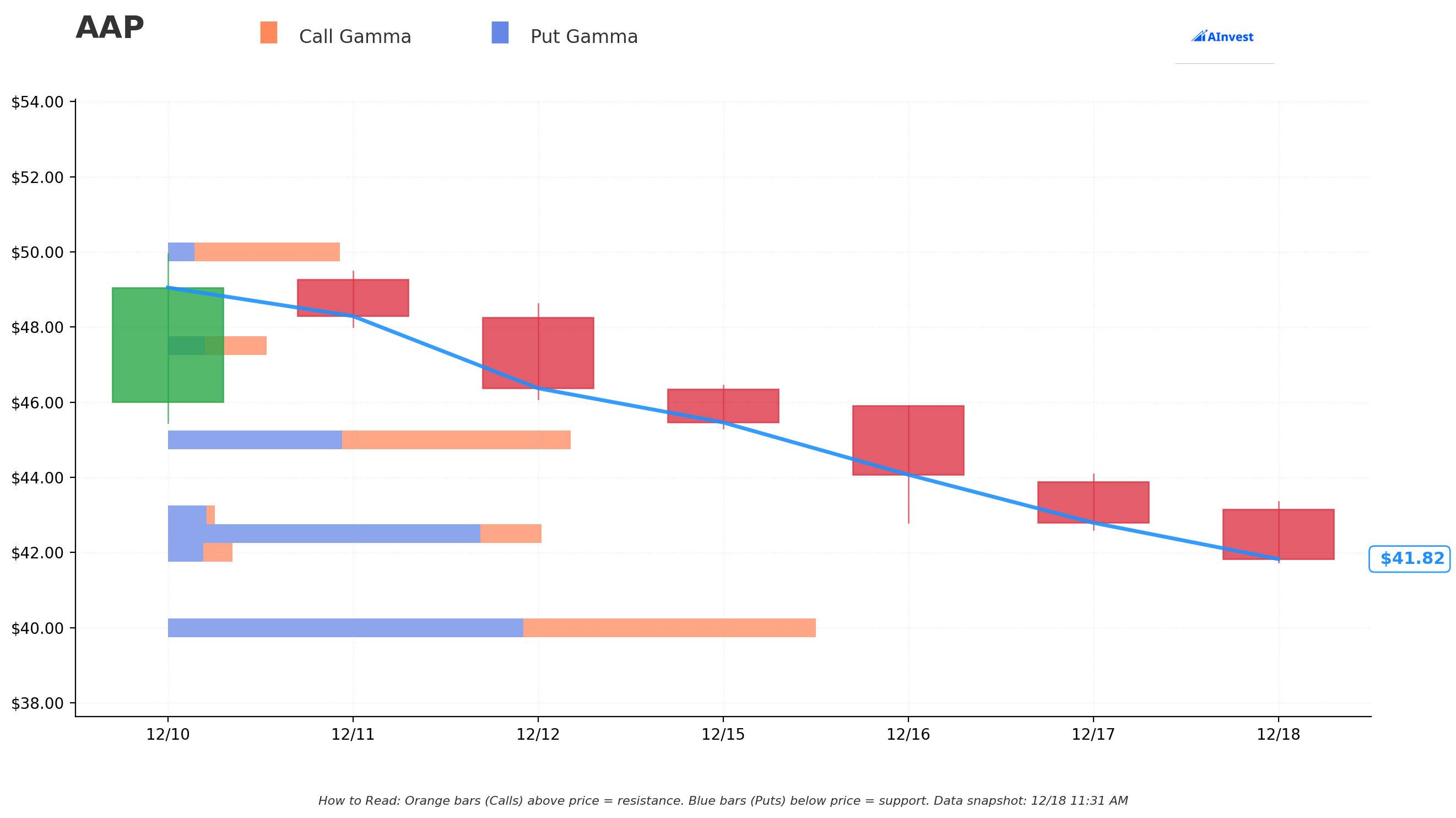

Gamma-Based Support & Resistance Analysis

Current Price: $41.79

The gamma exposure map reveals critical price levels that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $40.00 - STRONGEST SUPPORT with 1.83B total gamma (THIS IS THE LINE! Exactly where calls are struck)

- $37.50 - Secondary support at 0.63B gamma (10.3% below current)

- $35.00 - Deep support at 0.68B gamma (16.2% below current)

🟠 Resistance Levels (Call Gamma Above Price):

- $42.00 - Immediate ceiling with 0.17B gamma (0.5% overhead - minor resistance)

- $42.50 - Secondary resistance at 1.02B gamma (1.7% above current - first real test)

- $43.00 - Next ceiling at 0.13B gamma (2.9% overhead)

- $44.00 - Important barrier at 0.09B gamma (5.3% above - call buyer's breakeven zone)

- $45.00 - Major resistance at 1.19B gamma (7.7% above - key profit target)

- $47.50 - Extended target at 0.28B gamma (13.7% rally)

- $50.00 - Big upside target at 0.49B gamma (19.6% rally)

What this means for traders: AAP is sitting RIGHT ON TOP of massive $40 support (1.83B gamma - the strongest single level). This creates a natural floor - if stock dips to $40, market makers will aggressively buy to hedge their put exposure. The call buyer positioned EXACTLY at this critical support level - smart positioning!

The path higher faces resistance at $42.50 (1.02B) and $45.00 (1.19B), but these aren't insurmountable. If the stock breaks above $45, there's open road to $50 with limited gamma resistance. The setup screams: "Defend $40, grind to $45, then explosive move to $50+."

Net GEX Bias: Slightly Bearish (4.35B call gamma vs 4.40B put gamma) - Very balanced positioning suggests market is UNCERTAIN about direction. This creates opportunity for big moves in either direction if catalysts materialize.

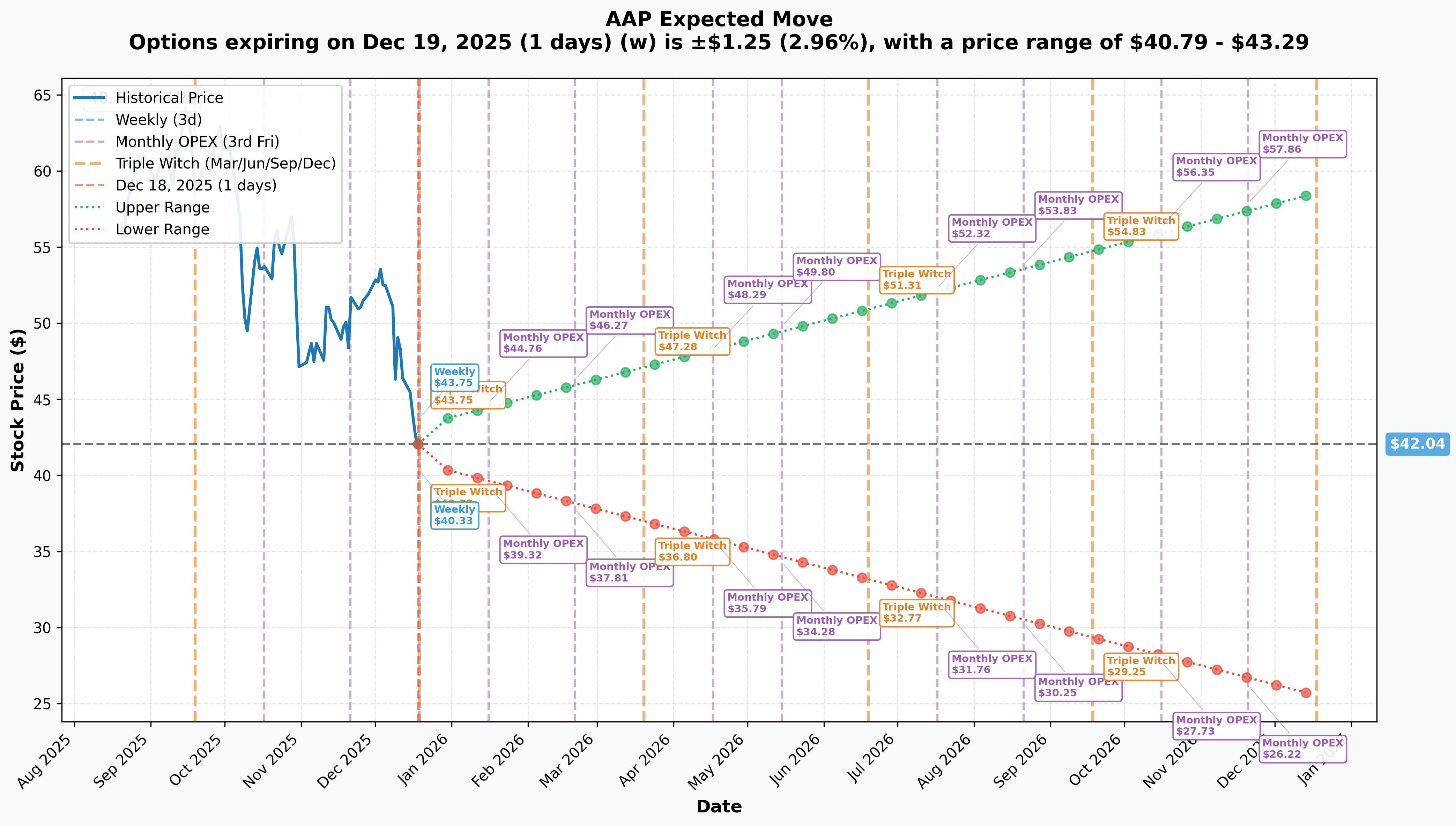

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 1 day - TOMORROW!): ±$1.25 (±2.96%) → Range: $40.79 - $43.29

- 📅 Monthly OPEX (Jan 16 - 29 days): ±$2.72 (±6.48%) → Range: $39.32 - $44.76

- 📅 Quarterly Triple Witch (Dec 19 - 1 day): ±$1.25 (±2.96%) → Range: $40.79 - $43.29

- 📅 January 23 (36 days - THIS TRADE!): ±$3.10 (±7.35%) → Range: $38.94 - $45.14

Translation for regular folks: The market is pricing a 3% move ($1.25) by TOMORROW for weekly expiration - not expecting much volatility near-term. But over the next month, implied volatility suggests a bigger 6.5% move ($2.72) through January OPEX.

Here's the critical insight: The January 23rd calls need AAP above $44.12 to profit (4.6% rally). The implied move upper range of $45.14 gives the call buyer a realistic shot IF the stock moves as the options market expects. However, the buyer is betting on a BIGGER move (toward $48-50) than implied volatility suggests - that's the speculative element.

Key insight: Relatively LOW implied volatility (under 10% for monthly) means options are CHEAP right now. The call buyer is taking advantage of low premium costs to make a leveraged bet on the turnaround story accelerating.

🎪 Catalysts

🔥 Already Happened (Supporting Turnaround Thesis)

$1.5 Billion Worldpac Sale Closed - November 1, 2024 💰

AAP completed the sale of its Worldpac wholesale distribution unit to Carlyle for $1.5B, netting ~$1.2B after taxes:

- 🏦 Balance sheet transformation: Used proceeds to pay down debt, strengthen liquidity to $1.9B

- 🎯 Strategic refocus: Exit lower-margin wholesale business to focus on higher-ROI "blended-box" model serving both professional and DIY customers

- 📊 Management stated this allows focus on "where we win" - the core domestic retail business

- ⚠️ However: Removes $1B+ in annual revenue, creating near-term top-line headwind

700+ Store Closures Approved - November 13, 2024 🏬

Board approved aggressive 2024 Restructuring Plan with massive footprint reduction:

- 📉 Closing: 523 corporate stores, 204 independent locations, 4 distribution centers by mid-2025

- 🚪 California exit: Complete withdrawal from California - 137 stores closing by March 2025 affecting 1,600+ workers

- 💰 Expected savings: $50M annualized cost reduction

- 🎯 Margin improvement potential: Management targeting 500+ basis points margin expansion through FY2027

- 💸 Restructuring costs: $300-750M total (trending toward low end)

- 📈 Strategic rationale: Exit low-density Western markets, consolidate resources in high-density Eastern markets where AAP has competitive advantages

This is the CORE catalyst - if execution delivers, margins expand dramatically. If it fails, AAP stays stuck in no-man's-land.

Supply Chain Transformation Progress - Ongoing Through 2025 🏭

AAP is consolidating U.S. distribution centers from 38 to 16 by end of 2025:

- ✅ Progress: 9 DC closures/conversions completed in Q2 2025, on track for 12 by year-end

- 📦 Market hub expansion: Growing from 19 to 29 locations by end of 2025, targeting 60 by mid-2027

- 💻 Tech upgrade: New warehouse management system completed July 2024 covering 300,000+ SKUs

- 📈 Results showing: Store availability improved to mid-90% range vs low-90% in FY2024

- 🎯 Efficiency gains: Management expects "low single-digit increase in product throughput (lines per hour)"

Q3 2024 Results - November 14, 2024 📊

Q3 delivered strongest quarterly performance in two years:

- 💰 Revenue: $2.1B (down 3% YoY but beat expectations)

- 📈 Comparable sales growth: 3.0% - STRONGEST in two years

- 💸 Adjusted operating income: $16.7M (80 bps margin)

- 📉 Adjusted diluted loss: -$0.04 per share vs -$1.19 prior year (HUGE improvement)

- ⚠️ Results impacted by hurricanes and CrowdStrike IT outage (one-time items)

Analyst Upgrades - October 2024 ✅

Multiple analysts turned positive after Q3 results and restructuring announcement:

- 🚀 Wedbush upgraded from Neutral to Outperform with $55 price target (30% upside from current $42)

- 📈 Roth Capital raised to Hold rating (October 15)

- 💹 J.P. Morgan raised target to $62 from $44 (47% upside!)

- 📊 BMO Capital raised to $55 citing turnaround progress

However, other analysts remain cautious:

- 📉 Goldman Sachs cut to $43, Wells Fargo to $40, Truist to $39

- ⚖️ Consensus remains "Hold" with 43 Hold vs only 2 Buy ratings

- 📊 Average price target: $52.34 (24% upside from $42)

🚀 Upcoming Catalysts (Next 6 Weeks Through Call Expiration)

Q1 Fiscal 2026 Earnings - Expected Late February 2025 📊

This is likely the PRIMARY catalyst for the call trade! Earnings should fall within the January 23rd expiration window:

- 📅 Previous Q1 2025 date: May 22, 2025 (but this is fiscal Q1 FY2026, likely reports late Feb)

- 💰 Consensus revenue: $1.97B expected

- 📈 Consensus EPS: $0.68 expected

- 🎯 Key metrics to watch:

- Comparable store sales trend (need sustained 2-3%+ growth)

- Gross margin expansion (targeting 54%+ long-term)

- Holiday selling season results (Q4 calendar = Q1 fiscal)

- Supply chain efficiency improvements showing in metrics

- Progress on 2025 new store openings (targeting 30 in 2025)

Why earnings matter so much: If AAP reports strong holiday results with margin improvement and raises guidance, the stock could easily pop 15-20% (taking $42 to $48-50 range). The call buyer is positioned PERFECTLY for this scenario. However, any disappointment could send stock back toward $35-37.

Restructuring Milestone Updates - Through Mid-2025 🏗️

Multiple operational milestones hit during the January expiration window:

- 🚪 California exit completion: All 137 California stores closing by March 2025

- 📦 Final DC closures: 12th distribution center closure/conversion by end of 2024

- 💰 Restructuring cost updates: Management should provide updated guidance on total costs vs $300-750M range

- 📊 $50M cost savings: Should start showing up in financial results

- 🎯 2025 store opening progress: 30 new stores planned - early progress updates expected

Analyst Day or Strategic Update - Possible Q1 2025 📈

Given the magnitude of transformation, AAP may host an analyst day or major strategic update in early 2025:

- 🎯 2025 full-year guidance: Currently guiding to $8.4-8.6B revenue, 2-3% operating margin, $1.20-2.20 EPS

- 📊 2027 targets update: $9B revenue, 7% operating margin - may provide detailed roadmap

- 💡 Technology initiatives: New CTO hired to lead transformation - could unveil digital strategy

- 🏪 Store format evolution: Plans for 100+ annual store openings by 2027 - what's the concept?

Any positive surprise on strategy or guidance would be rocket fuel for the stock.

⚠️ Risk Catalysts (What Could Kill This Trade)

Macro Headwinds - Consumer Weakness 📉

DIY sales remain soft under ongoing inflation pressure:

- 💸 Consumers cutting back on discretionary vehicle maintenance spending

- 📊 If Q1 results show continued DIY weakness despite Pro channel strength, stock could sell off

- ⚠️ Broader retail environment weak heading into 2025 - discretionary spending under pressure

Competitive Pressure - Losing Ground 🏆

AutoZone and O'Reilly continue expanding while AAP shrinks footprint:

- 📉 AAP market share stuck at 18.0% while already trailing AutoZone (32.3%) and O'Reilly (18.3%)

- 🚪 700+ store closures concede territory to competitors permanently

- 💰 California exit hands entire state to rivals

- ⚠️ If professional customers defect during restructuring, recovery becomes much harder

Execution Risk - History of Failed Turnarounds 😰

Multiple prior restructuring attempts have failed over past decade:

- 📉 2013 General Parts acquisition STILL causing operational issues 12 years later

- 🔄 Previous CEOs attempted turnarounds that failed to close gap vs AutoZone/O'Reilly

- ⚠️ Current plan is most aggressive ever - higher risk, higher reward

- 📊 If execution stumbles (supply chain issues, technology problems, talent loss), credibility destroyed

Credit Rating and Financial Stress 💳

S&P downgraded AAP to 'BB' in September 2024:

- 📉 High leverage relative to earnings

- 💸 $300-750M restructuring costs pressure near-term cash flow

- 📊 Free cash flow still negative through Q3 2024

- ⚠️ If liquidity becomes constrained or debt covenants tighten, stock could crater

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts through January 23rd expiration:

📈 Bull Case (35% probability)

Target: $48-$55

How we get there:

- 🎄 Holiday season delivers: Q1 (fiscal) earnings in late Feb show strong holiday comp sales growth of 4-5%+

- 💪 Margin expansion visible: Gross margins tick up to 53-54% range as restructuring savings flow through

- 🏪 Store closure execution flawless: No major operational disruptions, Professional customers stay loyal

- 📦 Supply chain improvements: Store availability hits high-90% range, inventory turns improve

- 📈 Guidance raise: Management increases full-year 2025 targets based on Q1 momentum

- 🎯 Analyst upgrades accelerate: More firms move to Buy ratings, price targets lifted to $55-65 range

- 📊 Technical breakout: Stock clears $45 gamma resistance, momentum carries to $48-50

- 💚 Short covering rally: 16.8% short interest provides fuel for squeeze if bulls gain control

Key metrics needed:

- Comparable sales growth sustained at 3%+ (preferably accelerating to 4-5%)

- Gross margin up 100+ basis points YoY

- Operating margin improving toward 3-4% range (from current 2-3% guidance)

- Free cash flow turning positive

- Professional channel market share stable or growing

Call P&L in Bull Case:

- Stock at $48 on Jan 23: Calls worth $8.00, profit = $3.88/share × 15,000 = $5.82M gain (141% ROI!)

- Stock at $52 on Jan 23: Calls worth $12.00, profit = $7.88/share × 15,000 = $11.82M gain (287% ROI!!)

- Stock at $55 on Jan 23: Calls worth $15.00, profit = $10.88/share × 15,000 = $16.32M gain (396% ROI!!!)

Probability assessment: 35% because it requires multiple things going right simultaneously, but the pieces are in place. Restructuring on track, Q3 showed improvement, supply chain delivering results. Not a moonshot - realistic if execution continues.

🎯 Base Case (45% probability)

Target: $40-$45 range (MODEST GAINS)

Most likely scenario:

- ✅ Q1 earnings meet expectations: Solid but not spectacular results, in-line with guidance

- 📊 Restructuring progressing but not complete: California closures on track but benefits not fully visible yet

- 💰 Margins improving slowly: Gross margins up 50-75 bps, not the 100+ bulls hope for

- 🏪 Competitive environment stable: Not gaining share, but not losing ground either

- 📈 Guidance maintained: Management reaffirms full-year targets, doesn't raise or cut

- 📊 Stock grinds higher: Moves from $42 to $44-45 range on modest fundamental improvement

- 💤 Market remains skeptical: Consensus stays "Hold" - institutions waiting for more proof

This is breakeven-to-modest-profit territory for call buyer: Stock needs to be above $44.12 for calls to profit. In base case, stock reaches $44-45 by expiration, delivering 0-15% gains on the position. Not a home run, but not a total loss either.

Call P&L in Base Case:

- Stock at $43 on Jan 23: Calls worth $3.00, loss = -$1.12/share × 15,000 = -$1.68M loss (-41% ROI)

- Stock at $44.12 on Jan 23: Calls worth $4.12, breakeven (0% ROI)

- Stock at $45 on Jan 23: Calls worth $5.00, profit = $0.88/share × 15,000 = $1.32M gain (32% ROI)

Why 45% probability: Most realistic outcome given current trajectory. Company improving but slowly. Market needs more evidence before getting excited. Turnaround takes time.

📉 Bear Case (20% probability)

Target: $35-$40 (TEST THE $40 STRIKE!)

What could go wrong:

- 😰 Q1 earnings disappoint: Holiday sales weaker than expected, margins don't improve as hoped

- 🚨 Restructuring complications: Store closures create service disruptions, customers defect to competitors

- 💸 Costs higher than expected: Restructuring expenses trend toward $750M high-end vs $300M low-end

- 📉 DIY channel deteriorates: Consumer spending weakness accelerates, 40% of business under pressure

- 🇨🇳 Tariff headwinds: Current guidance assumes tariffs remain stable - escalation would compress margins

- 🏪 Professional customer defection: Commercial accounts switch to AutoZone/O'Reilly during transition period

- 📊 Guidance cut: Management forced to lower 2025 targets, pushes out 2027 margin goals

- 🔨 Break below $40 support: Cracks major gamma floor (1.83B), triggers cascade to $37.50 then $35

Critical support levels:

- 🛡️ $40.00: MUST HOLD or call trade dies (1.83B gamma floor)

- 🛡️ $37.50: Secondary support (0.63B gamma) - disaster scenario

- 🛡️ $35.00: Deep floor (0.68B gamma) - turnaround thesis dead

Call P&L in Bear Case:

- Stock at $40 on Jan 23: Calls worth $0 (expire worthless), loss = -$4.12/share × 15,000 = -$6.18M loss (-100% ROI)

- Stock at $37 on Jan 23: Calls worth $0 (expire worthless), loss = -$4.12/share × 15,000 = -$6.18M loss (-100% ROI)

- Stock at $35 on Jan 23: Calls worth $0 (expire worthless), loss = -$4.12/share × 15,000 = -$6.18M loss (-100% ROI)

Probability assessment: Only 20% because fundamentals ARE improving (Q3 showed it), restructuring plan is logical, and management has board/activist support. Would require multiple negative surprises to derail. But history of failed turnarounds can't be ignored - this is AAP's 4th or 5th attempt in a decade.

💡 Trading Ideas

🛡️ Conservative: Watch from Sidelines (Wait for Confirmation)

Play: Stay in cash until Q1 earnings prove the turnaround is real

Why this works:

- ⏰ Earnings timing uncertainty: Q1 fiscal results likely late February - options expire Jan 23, so you might miss the catalyst entirely

- 📊 Execution risk too high: Multiple prior turnarounds failed - why bet on this one working without more proof?

- 💸 Options expensive relative to probability: Paying $4.12 for calls on $42 stock = 9.8% of stock price for 36 days

- 🎯 Better entry likely: If turnaround works, stock will be $55+ by mid-2025 - plenty of time to participate

- 📉 Downside protection: Avoid -50% to -100% loss if thesis doesn't play out

Action plan:

- 👀 Monitor Q1 earnings closely (likely late February) for:

- Comparable sales growth 3%+ sustained

- Gross margin expansion 50+ basis points

- Operating margin improving toward 3-4%

- Free cash flow turning positive

- Guidance maintained or raised

- ✅ IF earnings deliver: Buy stock at $45-48 with confirmed fundamental improvement

- ❌ IF earnings disappoint: Stay away - another failed turnaround attempt

- 🎯 Risk/reward improves: Wait for $48-50 breakout with earnings confirmation, then ride to $55-60

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -50% to -100% loss. Miss out on leveraged gains if bull case plays out, but preserve capital for better opportunity with more evidence.

⚖️ Balanced: Small Stock Position with Tight Stop

Play: Buy small AAP stock position at $41-42 with stop-loss at $39

Why this works:

- 📊 Gamma support at $40: Massive 1.83B gamma floor provides natural buying pressure

- 🎯 Defined risk: 7% downside to stop-loss vs 15-30% upside potential to $48-55

- 💰 Better risk/reward than options: Don't pay $4.12 time premium for uncertain timing

- 📈 Participate in upside: Still capture 15-30% gains if bull case plays out

- 🛡️ Less time decay: Stock doesn't expire like options do

- ⏰ Flexibility: Can hold through Q1 earnings even if they report after Jan 23

Position sizing & entry:

- 💰 Risk 2-3% of portfolio maximum

- 🎯 Buy zone: $41.00-42.50 (current levels)

- ❌ HARD STOP: $39.00 (just below $40 gamma support)

- 📈 First target: $45 (7% gain)

- 🚀 Second target: $48-50 (15-20% gain)

- 💎 Moon shot: $55 (30% gain)

Management rules:

- 📊 If stock drops to $40.50, consider adding small amount (average down once only)

- ❌ If stop hit at $39, exit immediately - support broken, thesis wrong

- ✅ If stock hits $45, take 50% profit, let rest run with trailing stop

- 📈 If stock breaks $48, move stop to $45 (protect gains)

Risk level: Moderate (directional equity, tight stop) | Skill level: Intermediate

Expected outcome: Small loss (-7%) if thesis wrong, moderate gains (+15-30%) if thesis right. Better probability-adjusted return than options due to timing flexibility.

🚀 Aggressive: Copy the Whale Trade (Advanced Only!)

Play: Buy $40 January 23 calls to mirror institutional positioning

Why this could work:

- 🐋 Follow the smart money: Someone with $4.1M saw enough conviction to make this bet

- 🎯 Positioned at key support: $40 strike sits exactly at 1.83B gamma floor

- 📊 Asymmetric payoff: Risk $4.12, make $8-12+ if stock hits $48-52 (200-300% ROI potential)

- ⏰ Tight timeline creates urgency: 36 days forces quick resolution - not slow bleed

- 💰 Relatively low dollar risk: Can participate with 10-20 contracts ($4,120-8,240) vs $4.1M whale trade

- 📈 Earnings catalyst: If Q1 results report before Jan 23 expiration and beat, calls explode higher

Why this could blow up (SERIOUS RISKS):

- ⏰ TIME DECAY KILLER: Burning -$0.11 per day right now - that's $1,650/day on 15,000 contracts!

- 📅 Earnings timing risk: If Q1 earnings report AFTER Jan 23, you miss the catalyst entirely

- 💸 Already in-the-money: Paying $4.12 for $2.17 intrinsic = $1.95 time premium (47% of position)

- 😱 Can lose 100%: If stock at or below $40 on Jan 23, calls expire worthless

- 📊 Need 4.6% move just to breakeven: Stock must reach $44.12 (not guaranteed)

- ⚠️ Turnaround may not be fast enough: Even if thesis is right long-term, 36 days may not be enough

Position structure:

- 💰 Cost: $4.12 per share = $412 per contract

- 📊 Suggested size: 10-20 contracts = $4,120-8,240 total risk

- ⚠️ DO NOT risk more than 3-5% of portfolio (this is pure speculation)

Estimated P&L:

- 💀 Total loss scenario: Stock at $40 or below = lose entire $4,120-8,240 (-100%)

- 😰 Partial loss: Stock at $43 = calls worth $3.00 = lose $1.12 per contract (-27%)

- ✅ Breakeven: Stock at $44.12 = calls worth $4.12 (0% gain)

- 💚 Modest win: Stock at $46 = calls worth $6.00 = gain $1.88 per contract (+46%)

- 🚀 Big win: Stock at $50 = calls worth $10.00 = gain $5.88 per contract (+143%)

- 🌙 Home run: Stock at $55 = calls worth $15.00 = gain $10.88 per contract (+264%)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand you can lose 100% of premium (REAL possibility!)

- ✅ Have traded options through earnings before

- ✅ Can afford to lose entire investment

- ✅ Understand theta decay will erode position $40-80 per day

- ✅ Accept that earnings may report AFTER expiration (timing risk)

- ✅ Have researched AAP turnaround plan thoroughly

- ⏰ Plan to actively manage position (take profits at $46-48, cut losses at $40)

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~40% (stock must reach $44.12+ in 36 days while avoiding sub-$40 collapse)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Earnings timing uncertainty: Q1 fiscal results historically report late February - that's AFTER Jan 23 expiration! The call buyer may be banking on early release or preliminary guidance, but if earnings hit Feb 25-28, the options expire worthless before the catalyst. This is MASSIVE risk that retail traders often miss.

-

📉 History of failed turnarounds: AAP has attempted multiple restructurings over past decade, all falling short of closing the gap with AutoZone and O'Reilly. The 2013 General Parts acquisition still causing integration issues 12 years later. Why should this attempt succeed when others failed? Market skepticism is justified.

-

🏆 Competing against two legends: AutoZone (32.3% share) and O'Reilly (18.3% share) are among best-performing stocks over past 20+ years. AAP stuck at 18.0% and losing ground. Closing 700+ stores CONCEDES territory permanently to competitors who will happily take the market share. Very hard to regain once lost.

-

💸 Consumer discretionary spending pressure: DIY sales remain soft as consumers cut back on vehicle maintenance under inflation pressure. This represents 50% of AAP revenue base. If consumer spending deteriorates further into 2025, even perfect execution won't save financial results.

-

🚪 Execution risk during transition: Closing 700+ locations while maintaining customer service is HARD. Professional customers (50% of revenue) may defect to AutoZone/O'Reilly if service quality slips during restructuring. Supply chain consolidation from 38 to 16 DCs creates inventory availability risk. Any major operational hiccup destroys credibility.

-

💳 Financial stress and credit downgrade: S&P cut rating to 'BB' in September 2024 citing high leverage. $300-750M restructuring costs pressure cash flow. Free cash flow still negative through Q3 2024. If liquidity tightens or debt covenants become an issue, forced asset sales or equity dilution could crater stock.

-

📊 Analyst consensus skeptical: 43 Hold ratings vs only 2 Buy ratings shows Wall Street unconvinced. Recent guidance cut from $1.20-2.50 EPS to $1.20-2.20 signals execution challenges. Multiple analysts recently LOWERED price targets (Goldman to $43, Wells Fargo to $40). Smart money may be fading this rally.

-

🎯 $40 support is critical: If stock breaks below 1.83B gamma floor at $40, the call trade dies instantly (100% loss). Next support isn't until $37.50 (-10.8% drop). A single bad news item (weak sales update, guidance cut, competitive pressure) could trigger collapse through this level.

-

🇨🇳 Tariff risk: 2025 guidance assumes current tariffs remain in place. Any tariff escalation on auto parts imports would compress already-thin margins (currently guiding to just 2-3% operating margin). AAP has less pricing power than AutoZone/O'Reilly, so can't pass through costs as easily.

-

⚖️ Valuation offers NO cushion: Stock trading at $42 with $52.34 consensus target implies just 24% upside IF turnaround succeeds. Compare to DOWNSIDE: Failed turnaround could send stock back to $28 lows (-33% from here). Risk/reward only attractive if probability of success is 60%+, but history suggests lower odds.

-

🔥 Massive option position creates volatility: The $4.1M call trade represents 15,000 contracts = 1.5M shares = 2.5% of total float. This large concentrated position could create violent price swings if position is unwound early (forced selling) or if dealer hedging amplifies moves. Retail traders can get whipsawed in this environment.

-

💼 Activist investors could flip bearish: Third Point and Saddle Point Management forced board changes in March 2024, each holding ~5% stakes. If they lose patience with turnaround execution, they could push for more drastic action (breakup, sale, management change) which creates uncertainty and volatility.

🎯 The Bottom Line

Real talk: Someone just bet $4.1 MILLION that Advance Auto Parts completes its turnaround story over the next 36 days. This isn't a long-term value play - it's a leveraged bet that CEO Shane O'Kelly's aggressive restructuring (700+ store closures, $1.5B Worldpac sale, supply chain overhaul) drives a 15-30% rally by late January.

What this trade tells us:

- 🎯 Sophisticated player sees near-term catalyst (likely Q1 earnings or strategic update)

- 💰 They're positioned EXACTLY at $40 gamma support level (1.83B floor) - smart technical setup

- ⏰ Tight 36-day timeframe suggests high conviction in timing, not just direction

- 📊 Willing to pay $4.1M for leverage shows real money behind the thesis

- 🏦 Two-tranche execution (5K + 10K) suggests institutional desk with serious capital

But here's what concerns me:

- ⚠️ AAP has failed multiple turnaround attempts over past decade - what makes this one different?

- 📅 Earnings timing risk: If Q1 results report AFTER Jan 23, calls expire before the catalyst

- 🏆 Competing against AutoZone/O'Reilly (two of best stocks ever) - closing 700+ stores concedes market share permanently

- 💸 Consumer spending weak, DIY segment soft - macro headwinds remain

- 📊 Analyst consensus skeptical: 43 Hold vs 2 Buy - Wall Street not convinced yet

This is HIGH RISK, HIGH REWARD - not a "safe" play.

If you own AAP stock already:

- ✅ Hold with tight stop at $39.50-40.00 (just below gamma support)

- 📊 Watch for Q1 earnings announcement date - if it's AFTER Jan 23, temper expectations

- 🎯 If stock breaks above $45, consider taking partial profits (lock in 7%+ gains)

- 📈 Let remaining position run toward $48-50 targets if momentum continues

- ❌ SELL immediately if stock breaks $40 - support broken means thesis wrong

If you're watching from sidelines:

- ⏰ DO NOT chase above $43 - risk/reward deteriorates rapidly

- 🎯 Best entry zone: $40.50-41.50 (near gamma support with tight stop)

- 📊 Wait for Q1 earnings confirmation before committing serious capital

- ✅ Looking for: Sustained 3%+ comp growth, 50+ bps margin expansion, positive free cash flow

- 🚀 If earnings deliver, stock could run to $48-55 over next 3-6 months

If you're considering the call trade:

- ⚠️ Understand you can lose 100% - this is speculation, not investment

- ⏰ Timing is EVERYTHING - earnings must report before Jan 23 OR stock must rally on other catalysts

- 💰 Position size: Risk only 2-3% of portfolio maximum (treat as lottery ticket)

- 📉 Cut losses at $40 - if stock breaks support, exit immediately

- 📈 Take profits at $46-48 - don't be greedy, lock in 50-100%+ gains if you get them

- ❌ DO NOT attempt unless you've traded options through earnings before

Mark your calendar - Key dates:

- 📅 December 19 (Tomorrow) - Weekly/Quarterly OPEX (±3% implied move)

- 📅 January 16, 2026 - Monthly OPEX

- 📅 January 23, 2026 - OPTION EXPIRATION DATE (36 days from now)

- 📅 Late February 2026 - Q1 Fiscal 2026 earnings (likely date)

- 📅 March 2025 - California exit completion (137 stores closed)

- 📅 Mid-2025 - Final restructuring milestones hit

Final verdict: The $4.1M call trade is a BOLD bet that AAP's turnaround story accelerates dramatically over next 5 weeks. The thesis has merit - Q3 showed improvement (3.0% comp growth, best in two years), restructuring plan is aggressive (700+ closures, $50M savings), supply chain improvements delivering results, and activist investors providing governance oversight.

BUT - timing risk is enormous. If Q1 earnings report after Jan 23 expiration, the entire thesis could be RIGHT and the options still expire worthless. History of failed turnarounds can't be ignored. Competing against two legends (AutoZone/O'Reilly) is HARD.

For retail traders: Stock position with tight stop at $39-40 offers better risk/reward than options due to timing flexibility. Wait for earnings confirmation before committing serious capital. Let the institutional whale take the timing risk with their $4.1M - you preserve yours.

This is a calculated gamble on execution, not a sure thing. Size accordingly. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 2,500x unusual score reflects this trade's size relative to recent AAP option activity - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Turnaround situations carry significant execution risk with potential for 100% loss if thesis fails to materialize within tight 36-day timeframe.

About Advance Auto Parts: Advance Auto Parts operates as a leading auto-parts retailer in North America with more than 4,000 store and branch locations, serving both professional installers (50% of revenue) and DIY consumers (50%), with a market cap of $2.57 billion in the Retail Auto & Home Supply Stores industry.