🍎 AAPL $20M Call Bet - Big Money Loading Up After Blockbuster Earnings!

📅 February 2, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $20 MILLION on AAPL calls this morning -- 6,500 contracts of the May 15th $240 strike bought on the ask! Just 4 days after Apple posted its best quarter EVER ($143.8B revenue, 23% iPhone growth), institutional money is making a confident bullish bet that AAPL keeps climbing. With the stock at $263.15 and these calls already deep in-the-money, this looks like a leveraged long position from someone who believes Apple's momentum has legs through spring. Translation: Smart money is betting big that the iPhone super-cycle and AI catalyst story pushes AAPL higher over the next 3+ months.

📊 Company Overview

Apple Inc. (AAPL) is one of the largest companies on the planet, building the hardware and software ecosystem that billions of people use every day:

- 💰 Market Cap: $3.81 Trillion (one of the top 2 most valuable companies globally)

- 🏭 Industry: Electronic Computers

- 📱 Current Price: $263.15 (near 52-week high of $288.62)

- 🎯 Primary Business: iPhone, Mac, iPad, Services (App Store, iCloud, Apple Music, Apple TV+), Wearables, and a growing AI/smart home strategy

Apple just reported $143.8B in quarterly revenue (up 16% YoY), with an installed base of 2.5 billion active devices and over 1 billion paid subscriptions. Services alone are running at a $120B annual pace.

💰 The Option Flow Breakdown

The Tape (February 2, 2026 @ 11:13:07):

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:13:07 | AAPL | BUY | CALL | 2026-05-15 | $20M | $240 | 6,600 | 34,000 | 6,500 | $263.15 | $31.20 | AAPL20260515C240 |

🤓 What This Actually Means

This is a bullish leveraged long position on Apple. Let me break it down:

- 💸 Massive premium: $20M ($31.20 per contract x 6,500 contracts) -- this is NOT your neighbor's Robinhood account

- 📈 Deep in-the-money: $240 strike is $23.15 below current price, meaning ~$23 of intrinsic value + ~$8 of time value

- ⏰ Strategic timing: 102 days to expiration captures Q2 earnings (April 30), smart home product launch (March-April), and enhanced Siri rollout

- 📊 Size matters: 6,500 contracts = 650,000 shares worth ~$171M in exposure -- leveraged 8.5x on the $20M invested

- 🏦 Institutional conviction: Buying on the ASK means they wanted IN immediately, willing to pay up

- 🔥 Z-Score of 2.24 (HIGHLY UNUSUAL): This level of activity happens only a few times per month -- roughly 10x more active than the typical AAPL session

What's really happening here: This trader is using deep in-the-money calls as a stock replacement strategy with built-in leverage. Instead of buying $171M worth of AAPL shares, they're getting the same upside exposure for $20M. The May 15th $240 calls have a delta around 0.80-0.85, meaning they move nearly dollar-for-dollar with the stock. If AAPL rallies to $290 by May, these calls would be worth ~$50 each -- a 60% return on the $20M. They're positioned for continuation of the post-earnings momentum into multiple spring catalysts.

Classification: STANDALONE - Long Call (BTO) -- this is NEW bullish positioning, not closing an existing trade.

📈 Technical Setup / Chart Check-Up

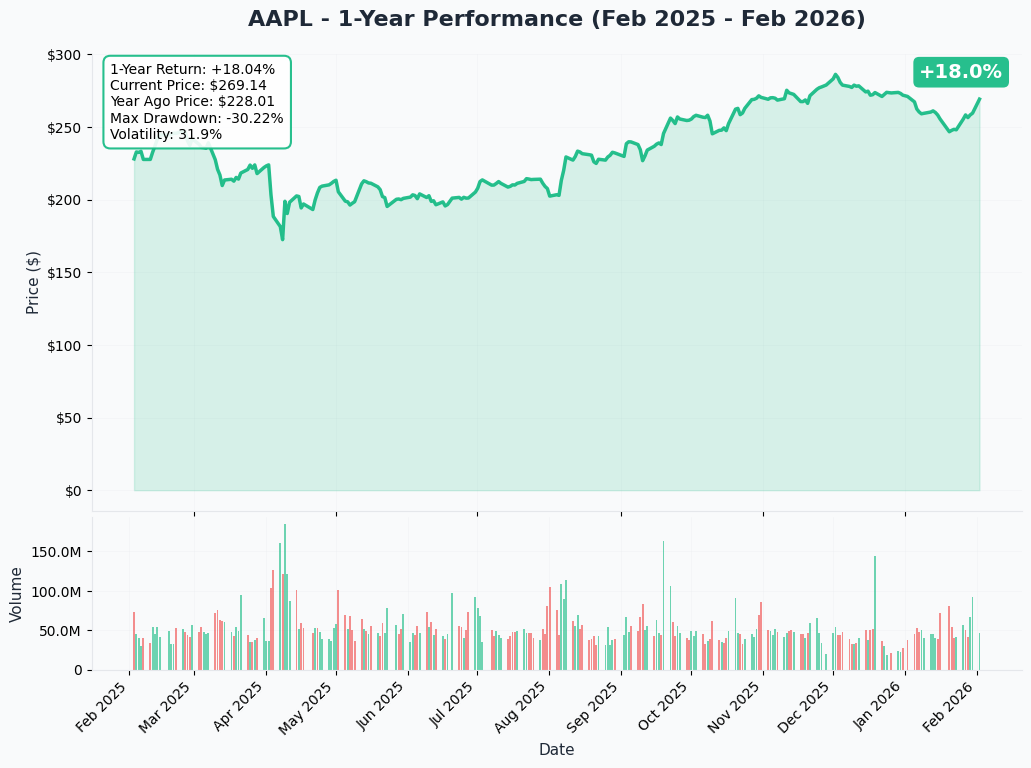

YTD Performance Chart

AAPL is having a strong run, trading at $263.15 after surging ~3% today on post-earnings analyst upgrades. The stock sits about 7% below its 52-week high of $288.62, with the 52-week low at $169.21. The recent Q1 FY2026 earnings blowout has reignited bullish momentum after some sideways action in late 2025.

Key observations:

- 🚀 Post-earnings surge: Stock up 3% today as analysts raise price targets to $290-$320

- 📈 Uptrend intact: Trading well above major moving averages after the earnings beat

- 💪 Strong support built: The $240 level (this trade's strike) aligns with pre-earnings price floor

- 📊 Volume confirmed: Institutional buying evident with large call flow today

- ⚠️ Near resistance: $270 is the key level to watch (massive gamma wall overhead)

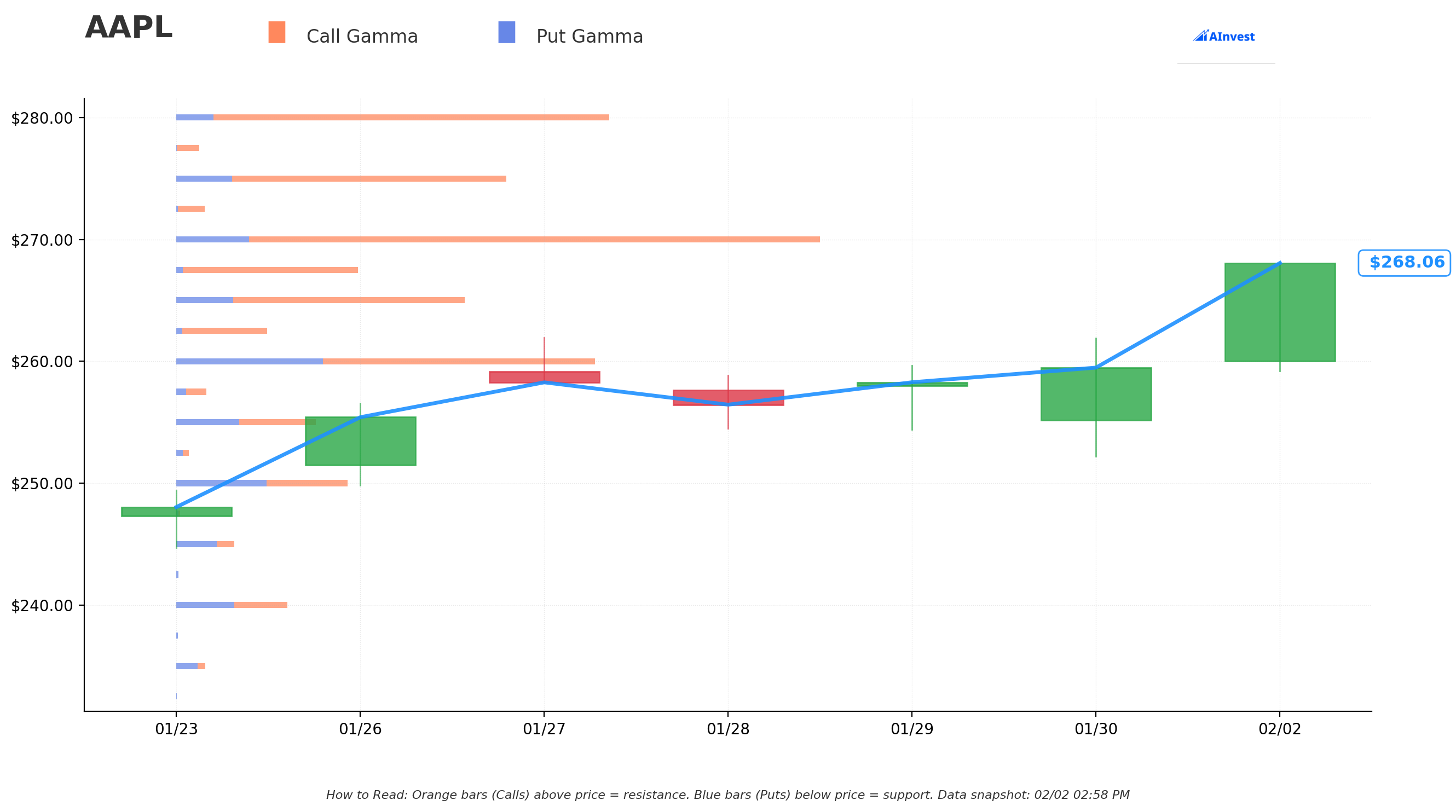

Gamma-Based Support & Resistance Analysis

Current Price: $268.03

The gamma exposure (GEX) map shows where market makers have the biggest positions -- think of these as price magnets and barriers that influence where the stock gravitates:

🔵 Support Levels (Floors Below Price):

- $267.50 - Immediate support with 46B total gamma (nearest cushion, just 0.2% below)

- $265 - Strong secondary floor with 72B gamma (1.1% below -- dealers buy dips here aggressively)

- $260 - Major structural support at 103B gamma (3.0% below -- this is THE line in the sand)

- $255 - Deeper support at 35B gamma (4.9% below)

- $250 - Extended floor with 43B gamma (6.7% below -- would need a major shock to reach)

🟠 Resistance Levels (Ceilings Above Price):

- $270 - STRONGEST resistance with 156B gamma (0.7% above -- THE wall to break!)

- $275 - Secondary ceiling at 80B gamma (2.6% above)

- $280 - Major overhead resistance at 106B gamma (4.5% above)

- $285 - Extended resistance at 51B gamma (6.3% above)

- $300 - Big round-number target at 47B gamma (11.9% above -- the dream scenario)

What this means for traders: AAPL is sitting just below a MASSIVE $270 gamma wall (156B -- by far the largest level on the board). Market makers hold enormous positions here, creating natural selling pressure as the stock approaches $270. A breakout above $270 would likely trigger a rapid move to $275-$280 as dealers scramble to hedge. On the flip side, $265-$267.50 provides a solid cushion with strong gamma support.

Net GEX Bias: Bullish (760B call gamma vs 215B put gamma) -- Overall positioning is heavily skewed bullish, which means the path of least resistance is UP once $270 breaks.

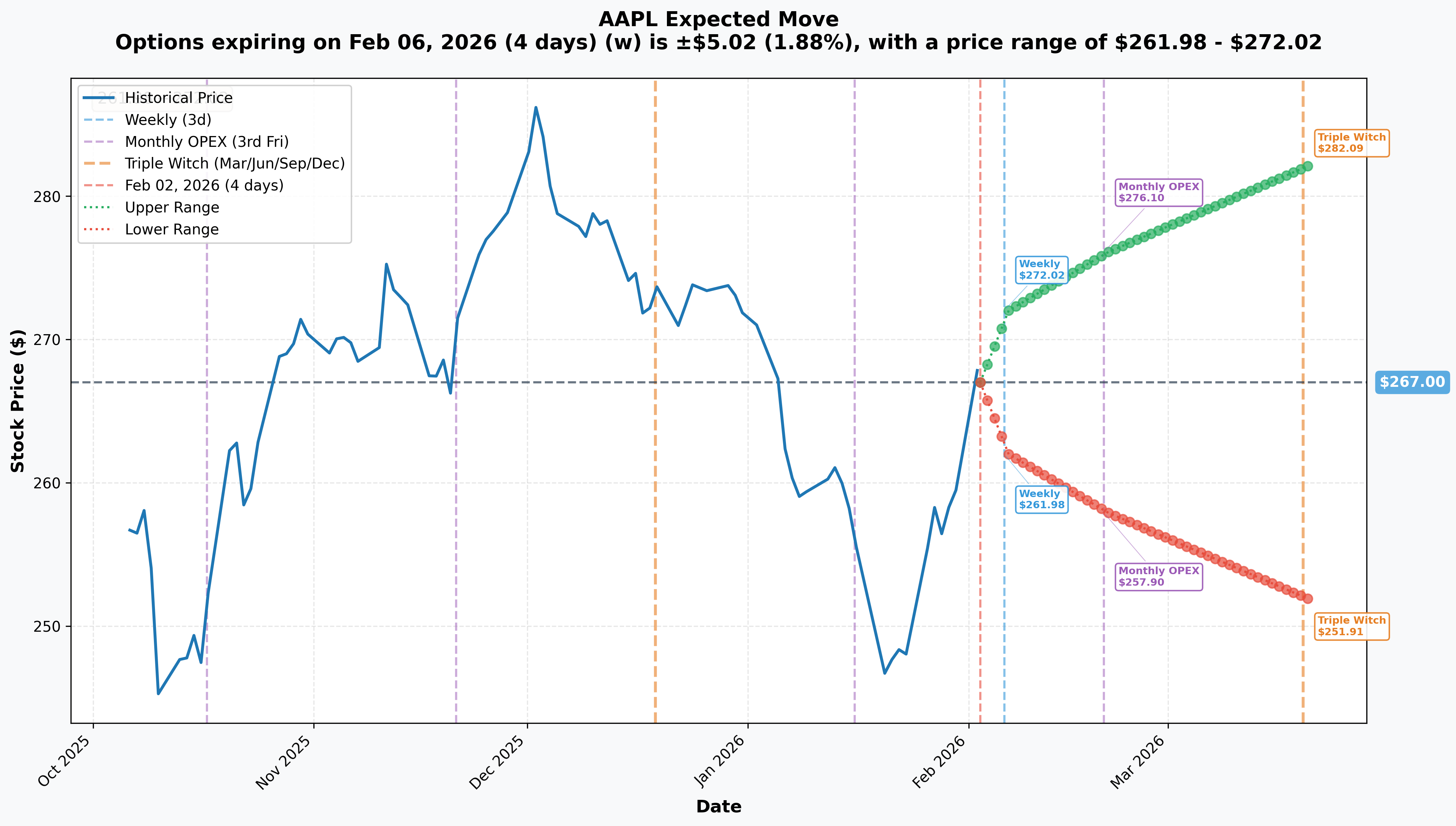

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Feb 6 - 4 days): +/-$5.02 (+/-1.9%) -- Range: $261.98 - $272.02

- 📅 Monthly OPEX (Feb 20 - 18 days): +/-$9.09 (+/-3.4%) -- Range: $257.90 - $276.10

- 📅 Quarterly Triple Witch (Mar 20 - 46 days): +/-$15.09 (+/-5.7%) -- Range: $251.91 - $282.09

Translation for regular folks: The options market is pricing in a modest 1.9% move ($5) by this Friday and a 3.4% move ($9) by February monthly OPEX. For a $3.8T mega-cap stock, this is relatively calm -- earnings are behind us, so implied volatility has compressed. The quarterly expiration in March prices in a wider 5.7% move ($15), which captures the smart home product launch window and potential Siri overhaul news.

Key insight: The call buyer chose a May 15th expiration that goes WELL BEYOND all these near-term expirations. They're positioned for a multi-month move, not a quick trade. By May, AAPL could have reported Q2 earnings (April 30), launched the smart home hub, and revealed the Gemini-powered Siri. That's a LOT of potential catalysts.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened -- Building Momentum)

Q1 FY2026 Earnings Blowout (January 29, 2026) Apple crushed it. Revenue hit $143.8B (up 16% YoY, beat by $5.4B), EPS of $2.84 (beat by $0.17), and iPhone revenue surged 23% to $85.3B. Greater China rebounded 38% -- the bears' biggest concern has flipped bullish. Services hit $30B quarterly (all-time record). Management guided Q2 at 13-16% revenue growth. This was a statement quarter.

Apple-Google Gemini AI Partnership (January 12, 2026) Apple picked Google's Gemini to power the next-generation Siri, in a deal reportedly worth up to $5B for Google. This positions Apple to close the AI gap with competitors and could drive a major upgrade cycle if the new Siri delivers.

iPhone 17 Super-Cycle Continues Apple captured 25% global smartphone market share in Q4 2025 -- the highest-ever quarterly share. iPhone ASP hit $1,000 for the first time. Apple is the world's #1 smartphone vendor for the third straight year.

Analyst Upgrades Galore (Post-Earnings)

- JPMorgan: $315 target

- Morgan Stanley: $315 target

- Goldman Sachs: $320 target

- Melius Research: $290 target

- Median consensus: ~$300 across 36 analysts

🚀 Upcoming Catalysts (Next 3-6 Months -- Why This Trade Was Made)

Smart Home Product Launch (March-April 2026) Apple is expected to launch its first smart home display hub ("HomePad") -- a 7-inch touchscreen with A18 processor at ~$350. This enters a new product category and leverages Apple's 2.5B device ecosystem. Part of a broader push including HomeKit cameras and updated HomePod.

Enhanced Siri with Gemini (Spring 2026) The overhauled Gemini-powered Siri debuts in iOS 26.4 with ChatGPT-like conversational abilities. This is arguably Apple's most important AI catalyst -- success here drives upgrade cycles AND Services revenue. Apple waited to launch the smart home hub specifically to pair it with the smarter Siri.

Q2 FY2026 Earnings (Expected April 30, 2026) Consensus expects ~$1.89 EPS on $107-111B revenue. The call buyer's May 15th expiration captures this report perfectly -- if Apple delivers another beat with strong iPhone demand commentary, these calls could be worth significantly more.

WWDC 2026 (June 8, 2026) Apple's developer conference previews iOS 27, potential Health+ subscription service, and AI strategy updates. While after the May expiration, any early leaks or previews could lift sentiment.

iPhone Fold & iPhone 18 (September 2026) Apple's first foldable iPhone targeting September 2026 at $2,000-$2,500 with a crease-free display. This is further out but builds the long-term narrative that keeps institutions buying.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and the catalyst calendar, here's what could happen for AAPL through the May 15th expiration:

📈 Bull Case (30% probability)

Target: $290-$310

How we get there:

- 💪 Q2 earnings on April 30th delivers another beat (revenue above $111B guided range, strong iPhone 17 demand)

- 🤖 Gemini-powered Siri launches to positive reviews, sparking upgrade cycle buzz

- 🏠 Smart home hub sells well, validates new product category

- 📊 Analysts raise targets further toward $320-$350 as AI narrative takes hold

- 🚀 Breakout above $270 gamma wall triggers momentum to $280, then $300 (major gamma level at 47B)

- 📈 Implied move upper range for quarterly expiration ($282) gets blown through on catalyst stack

Key metrics needed:

- iPhone demand sustained through spring (no post-holiday cliff)

- Services growth acceleration above 14%

- China revenue holds above $20B quarterly

- Siri overhaul receives positive developer/media reception

Why 30%: Apple just delivered a blowout quarter, multiple catalysts line up perfectly through May, and analyst consensus is clustered at $300+. The $270 gamma wall is the main obstacle -- once broken, momentum accelerates fast.

🎯 Base Case (50% probability)

Target: $260-$280 (Grind Higher With Pullbacks)

Most likely scenario:

- ✅ Stock consolidates the post-earnings gains between $265-$275 near-term

- 📱 Smart home launch gets decent reviews but isn't a game-changer for the stock

- 🤖 Siri improvements are incremental, not revolutionary -- market says "show me more"

- ⚖️ Q2 earnings roughly in-line with guidance ($107-111B range, no major surprise)

- 🔄 Trades between gamma support at $265 and resistance at $270-$280

- 📊 Call buyer's position gains modestly -- stock at $275 means calls worth ~$35 (12% gain)

- 💤 Volatility stays low as mega-cap stability attracts steady institutional flows

This is the call buyer's minimum-win scenario. With the stock already $23 above their $240 strike, they profit as long as AAPL stays above $271.20 (strike + premium paid). Given the strong fundamental backdrop, that's a reasonable bet.

Why 50%: Apple is a $3.8T battleship -- it doesn't move 20% in a quarter without a major catalyst. The earnings beat is already priced in, and the next catalyst (Siri/smart home) is months away. Steady grind higher is the most likely path.

📉 Bear Case (20% probability)

Target: $240-$260

What could go wrong:

- 😰 Tariff escalation -- Apple faces $900M+ quarterly tariff costs with 145% US tariffs on Chinese imports still in effect

- 🇨🇳 China demand fades after initial iPhone 17 surge -- one-quarter wonder

- 🤖 Siri overhaul delayed again or reviews highlight unacceptable error rates -- AI narrative crumbles

- 📉 Rising memory costs (40-50% in Q1) squeeze margins below expectations

- ⚖️ DOJ antitrust case or EU DMA enforcement headlines spook investors

- 💸 Broader market selloff drags mega-caps lower (macro recession fears, rate uncertainty)

- 📊 Break below $260 gamma support (103B) opens path to $255, then $250

Critical support levels:

- 🛡️ $265: Strong gamma floor (72B) -- first line of defense

- 🛡️ $260: Major structural support (103B gamma) -- THE must-hold level

- 🛡️ $250: Extended floor (43B gamma) -- implied move quarterly lower bound at $252

- 🛡️ $240: The trade's strike price -- call buyer would be underwater below here

Call P&L in Bear Case:

- Stock at $260: Calls worth ~$20, loss = -$11.20/contract = -$7.3M (-36%)

- Stock at $250: Calls worth ~$10, loss = -$21.20/contract = -$13.8M (-69%)

- Stock at $240: Calls worth ~$1-2, loss = -$29-30/contract = -$19M+ (-95%)

Why only 20%: Apple just proved the business is firing on all cylinders. A drop below $260 would require multiple negative catalysts stacking simultaneously. The $3.8T market cap and 2.5B device installed base provide a fundamental floor that limits downside.

💡 Trading Ideas

🛡️ Conservative: The "Ride Apple's Coattails" Stock Purchase

Play: Buy AAPL shares on any pullback to $260-$265 gamma support zone

Why this works:

- 📈 Apple just posted its best quarter ever -- momentum is real, not speculative

- 🛡️ $260-$265 has massive gamma support (72-103B) -- dealers buy dips here automatically

- 💰 Upcoming catalysts (smart home, Siri, Q2 earnings) provide multiple shots on goal

- 📊 Analyst consensus at $300 gives 12-15% upside from entry

- ⏰ No time decay -- unlike options, shares don't expire worthless

- 💵 Collect the $0.26/quarter dividend while you wait

Action plan:

- 🎯 Set limit buy at $262-265 (gamma support zone)

- 📊 Position size: 2-5% of portfolio (this is still a $3.8T mega-cap, not a lottery ticket)

- ⛔ Stop loss: $250 (below major gamma floor and implied move quarterly lower bound)

- 🎯 Profit targets: $280 (trim 1/3), $290 (trim 1/3), hold remainder for $300+

- ⏰ Time horizon: 3-6 months

Risk level: Low | Skill level: Beginner-friendly | Expected outcome: 10-15% gain if base case plays out

⚖️ Balanced: May Bull Call Spread (Follow The Flow)

Play: Buy AAPL May 15th $265/$285 call spread

Structure: Buy $265 call, Sell $285 call (May 15th expiration -- SAME expiry as the $20M trade)

Why this works:

- 🎯 Defined risk -- you know your max loss upfront

- 📊 Capitalizes on same thesis as the $20M institutional buyer, but with capped risk

- 💪 $265 call starts near-the-money with high delta (~0.55-0.60)

- 📈 $285 short call collects premium, reducing cost basis

- ⏰ 102 days captures smart home launch, Siri update, AND Q2 earnings

- 🤝 You're essentially "copying" institutional positioning at a fraction of the cost

Estimated P&L:

- 💰 Cost: ~$8-10 per spread ($800-$1,000 per contract)

- 📈 Max profit: $20 - cost = ~$10-12 per spread if AAPL above $285 ($1,000-$1,200)

- 📉 Max loss: Premium paid ($800-$1,000)

- 🎯 Breakeven: ~$273-275

- 📊 Risk/Reward: ~1:1.2 with 50%+ probability of profit

Position sizing: 1-3% of portfolio | Risk 2-5 spreads max

Risk level: Moderate | Skill level: Intermediate

🚀 Aggressive: Ride The $270 Gamma Breakout

Play: Buy AAPL March 20th $270 calls -- betting on a gamma squeeze above the $270 wall

Why this could work:

- 💥 $270 is the STRONGEST gamma level on the board (156B) -- a breakout triggers dealer hedging that ACCELERATES the move higher

- 📊 Once through $270, next resistance is $275 (only 80B gamma) and $280 (106B) -- less dense resistance

- 🏠 Smart home launch catalyst in March-April could be the spark

- 🤖 Any positive Siri/Gemini headlines add fuel

- ⚡ Implied move for quarterly expiration already prices $282 upside -- $270 calls would be deep in-the-money there

Why this could blow up (REAL RISKS):

- 💸 Options near gamma walls can be expensive due to elevated IV at key strikes

- ⏰ 46 days to expiration means meaningful theta decay (~$0.15-0.20/day)

- 😱 $270 wall could REPEL price repeatedly before breaking -- death by a thousand cuts

- 📉 If broader market sells off, even a strong Apple can't fight the tide

- 🚨 Cost ~$6-8 per contract ($600-800) with real chance of total loss if AAPL stays below $270

Estimated P&L:

- 💰 Cost: ~$6-8 per contract

- 📈 Profit at $280: ~$10 value, gain of $2-4 (25-67% return)

- 🚀 Profit at $290: ~$20 value, gain of $12-14 (150-230% return!)

- 📉 Loss at $268: Worth ~$3-4, loss of $2-5 (30-60% loss)

- 💀 Total loss: Stock below $270 at March 20th expiration

Position sizing: 1% of portfolio MAX -- this is a directional bet, not a core position

Risk level: HIGH | Skill level: Advanced only | Probability of profit: ~40%

⚠️ Risk Factors

Don't get caught off guard by these potential headwinds:

-

💸 Tariff exposure is REAL: Apple still manufactures ~80% of products in China. The 145% US tariff on Chinese imports costs an extra $900M+ per quarter. Any tariff escalation could crush margins. Apple is shifting iPhone production to India, but it's a multi-year transition.

-

📊 Valuation isn't cheap at ~33x forward P/E: After the earnings blowout, AAPL trades at a meaningful premium to most mega-cap peers. The stock needs CONTINUED execution on iPhone demand, Services growth, and AI momentum to justify the multiple. Limited margin for error at these levels.

-

🤖 AI execution risk -- Siri has disappointed before: The Gemini-powered Siri overhaul has been delayed multiple times with internal testing revealing error rate issues. If the spring 2026 launch underwhelms, the "Apple AI catch-up" narrative collapses and could weigh on sentiment heading into iPhone 18 season.

-

💾 Rising memory costs squeeze margins: DRAM/NAND costs expected up 40-50% in Q1 2026. Apple flagged this on the earnings call. If component costs spike faster than expected, the 48.2% gross margin could compress.

-

⚖️ Regulatory threats across 4 continents: DOJ antitrust case proceeding in the US, EU DMA non-compliance finding, UK 1.5B pound App Store ruling on appeal, and Brazil requiring alternative app distribution. Any adverse ruling threatens the high-margin Services business.

-

📉 Berkshire Hathaway keeps selling: Warren Buffett trimmed Apple holdings to 238M shares from 915M shares in 2023. When the world's most famous value investor reduces a position by 74%, it's worth paying attention -- even if Apple remains his largest holding.

-

🎢 $270 gamma wall creates near-term resistance: The MASSIVE 156B gamma exposure at $270 means market makers will aggressively sell into any approach. Failure to break $270 could lead to frustrating range-bound trading, slowly eroding call premiums through time decay.

-

📱 iPhone demand could normalize: The iPhone 17 super-cycle produced incredible Q1 numbers, but smartphone cycles historically fade after the initial launch quarter. If Q2 iPhone revenue disappoints, the "super-cycle" narrative weakens quickly.

🎯 The Bottom Line

Real talk: A $20 MILLION call buy on AAPL the week after Apple's best quarter ever? That's institutional conviction. This isn't some speculative YOLO -- deep in-the-money calls at the $240 strike are basically leveraged stock ownership. The buyer is saying: "I believe Apple keeps winning through spring, and I want 8.5x leverage on that thesis."

What this trade tells us:

- 🎯 Big money is ADDING to Apple exposure right after earnings, not selling the news

- 💰 The May 15th expiration is perfectly positioned to capture smart home launch, Siri overhaul, AND Q2 earnings

- ⚖️ Deep ITM structure ($240 strike with stock at $263) shows confidence in holding above $240, not betting on a moonshot

- 📊 The 6,500 contract size with a Z-Score of 2.24 puts this in the top ~1% of AAPL activity -- this is real institutional flow

If you're bullish on AAPL:

- ✅ Look for pullback entries in the $260-265 gamma support zone -- don't chase at the highs

- 📊 $270 is the KEY breakout level -- a clean break above triggers momentum to $275-$280 fast

- ⏰ Mark your calendar: Smart home launch (March-April), Siri overhaul (spring), Q2 earnings (April 30)

- 🎯 Analyst consensus at $300 gives you a roadmap -- realistic 12-15% upside from current levels

- 🛡️ Use $255-260 as your line in the sand -- if Apple breaks below there, something fundamental has changed

If you're watching from sidelines:

- ⏰ Best entry window: any dip to $260-265 over the next few weeks (gamma support + implied move lower bound)

- 📈 Or wait for confirmed $270 breakout with volume for momentum entry

- 🎯 Apple at $265 with a $300 analyst target is a better risk/reward than chasing at $270+

- 📊 The catalyst calendar through May is LOADED -- plenty of reasons for the stock to work higher

If you're cautious:

- ⚠️ Tariffs, rising memory costs, and AI execution risk are all real headwinds

- 📊 33x forward P/E means you're paying a premium -- any stumble gets punished

- 💸 Berkshire selling suggests the easy money has been made

- 🛡️ Consider a collar or protective put if you're sitting on significant gains

Key dates to mark:

- 📅 February 6 - Weekly OPEX (implied range: $262-$272)

- 📅 February 12 - Quarterly dividend payment ($0.26/share)

- 📅 February 20 - Monthly OPEX (implied range: $258-$276)

- 📅 March-April - Smart home hub launch expected

- 📅 March 20 - Quarterly triple witch OPEX (implied range: $252-$282)

- 📅 Spring 2026 - Enhanced Siri with Gemini debuts

- 📅 April 30 - Q2 FY2026 earnings (expected)

- 📅 May 15 - This $20M call trade EXPIRES

- 📅 June 8 - WWDC 2026 keynote

Final verdict: This $20M call buy is a high-conviction institutional bet that Apple's momentum continues through spring. With a blowout quarter in the books, multiple catalysts ahead, and analyst targets pointing to $300+, the bull case is well-supported. The main risk is the $270 gamma wall capping near-term upside and macro headwinds (tariffs, rates) derailing the broader market. If you share the bullish view, buy pullbacks to $260-265 support rather than chasing. The smart money just told you their thesis -- now it's about finding the right entry.

Stay patient. Buy support. Let the catalysts come to you. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-Score of 2.24 reflects this trade's unusual size relative to recent AAPL history -- it does not guarantee the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Deep in-the-money calls carry significant capital risk and the entire $20M premium could be lost if AAPL declines sharply below $240. Position sizing and risk management are essential.

About Apple Inc.: Apple is among the largest companies in the world, with a broad portfolio of hardware and software products targeted at consumers and businesses. Best known for its iPhone, Mac, iPad, and Services ecosystem, Apple has a market cap of $3.81 trillion in the Electronic Computers industry.