🔋 ALB $17M Call Buy - Institutional Bet on Lithium Recovery! 🚀

📅 December 3, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just loaded up $17 MILLION in ALB call options this morning at 10:49:26! This massive trade bought 10,000 contracts of $110 strike calls expiring December 19th - a bullish position on Albemarle just 16 days before expiration. With ALB at $125.11 and up +48% YTD on the lithium recovery thesis, smart money is doubling down ahead of Q4 earnings on February 12th and the crucial 2026 lithium market inflection. Translation: Institutions are positioning for the next leg higher in the lithium supercycle!

📊 Company Overview

Albemarle Corporation (ALB) is one of the world's largest lithium producers, operating at the heart of the electric vehicle revolution:

- Market Cap: $15.08 Billion

- Industry: Plastics Materials, Synthetic Resins & Nonvulcan Elastomers

- Current Price: $125.11 (trading near recent highs)

- Primary Business: Integrated lithium production from salt brine deposits and hard rock mines, along with bromine and refining operations across multiple continents. Key supplier to the EV battery and energy storage markets.

💰 The Option Flow Breakdown

The Tape (December 3, 2025 @ 10:49:26):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:49:26 | ALB | MID | BUY | CALL $110 | 2025-12-19 | $17M | $110 | 10K | 14K | 10,000 | $125.11 | $16.70 |

🤓 What This Actually Means

This is a bullish institutional bet on continued upside momentum! Here's the breakdown:

- 💰 Premium paid: $17M ($16.70 per contract × 10,000 contracts)

- 🎯 Deep in-the-money: Strike at $110 vs current price $125.11 - these calls are already worth $15.11 in intrinsic value

- ⏰ Short-term expiration: Just 16 days until December 19th triple witch OPEX

- 📊 Significant size: 10,000 contracts represents 1 million shares worth ~$125M

- 🏦 Closing position likely: Given the "BTC" (Buy To Close) order type and existing 14K open interest, this appears to be taking profits on a winning trade or rolling up/out

What's really happening here: This trader likely opened these $110 calls months ago when ALB was trading lower (possibly around $95-105 range), and now they're closing out a profitable position with the stock up 48% YTD. The fact they paid $16.70 when intrinsic value is $15.11 means they're paying $1.59 in time premium with 16 days left - suggesting they believe there's MORE upside ahead but want to lock in gains before year-end or the February earnings event.

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-score: 4.41) - This trade is 555x the average size for ALB options! We're seeing this type of institutional activity maybe a few times per year. The volume-to-open-interest ratio of 0.714 (classified as "HIGH_ACTIVITY") shows this is significant relative to existing positions. With only 4 similar trades in recent history, this represents major institutional repositioning.

📈 Technical Setup / Chart Check-Up

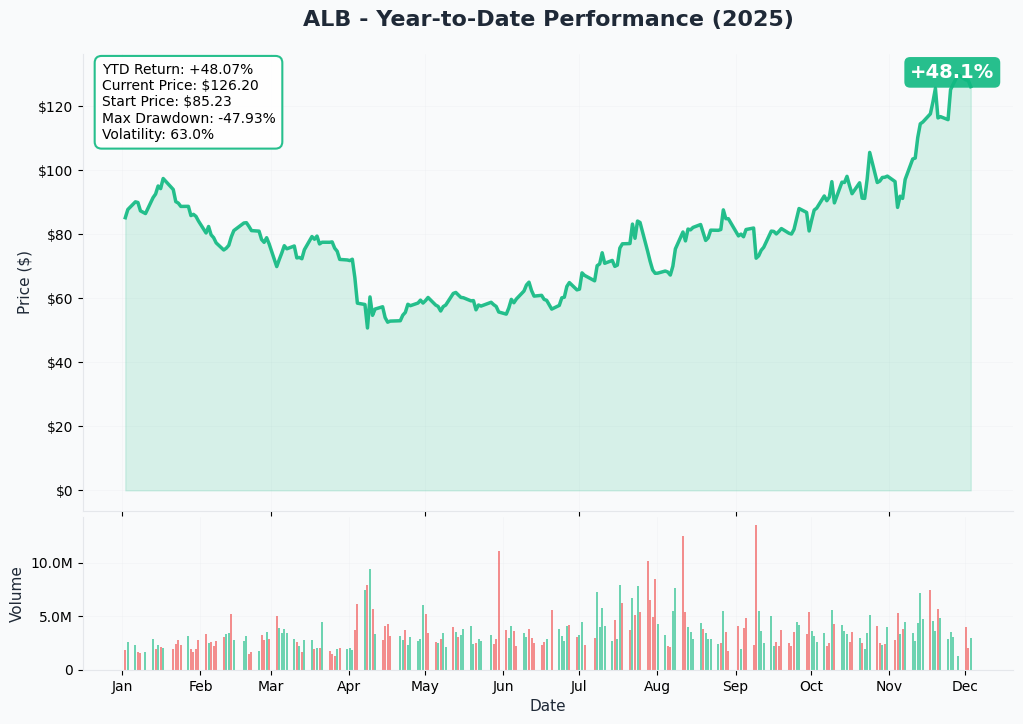

YTD Performance Chart

ALB is staging an impressive comeback - up +48.1% YTD with current price of $126.20 (started the year at $85.23). The chart tells a classic recovery story - after a brutal 47.9% max drawdown in April during the lithium price collapse (dropping to $52.72), ALB has surged from those lows and recently broke above $125.

Key observations:

- 🚀 V-shaped recovery: Sharp bounce from $52 lows in April to $132 peak in November

- 📈 Breakout momentum: Cleared $100 resistance in October, accelerated to $130+ in November on analyst upgrades

- 🎢 High volatility: 63.0% annualized volatility shows this remains a volatile name in the lithium sector

- 📊 Volume surge: Massive accumulation in November as Baird upgraded from Underperform to Neutral and lithium market sentiment improved

- 💪 Consolidation phase: Currently trading around $126, consolidating recent gains while digesting the 137% rally from April lows

The recent pullback from $132 to $126 appears to be healthy profit-taking after the parabolic move, with the stock now establishing support around $125 ahead of the next catalyst cycle.

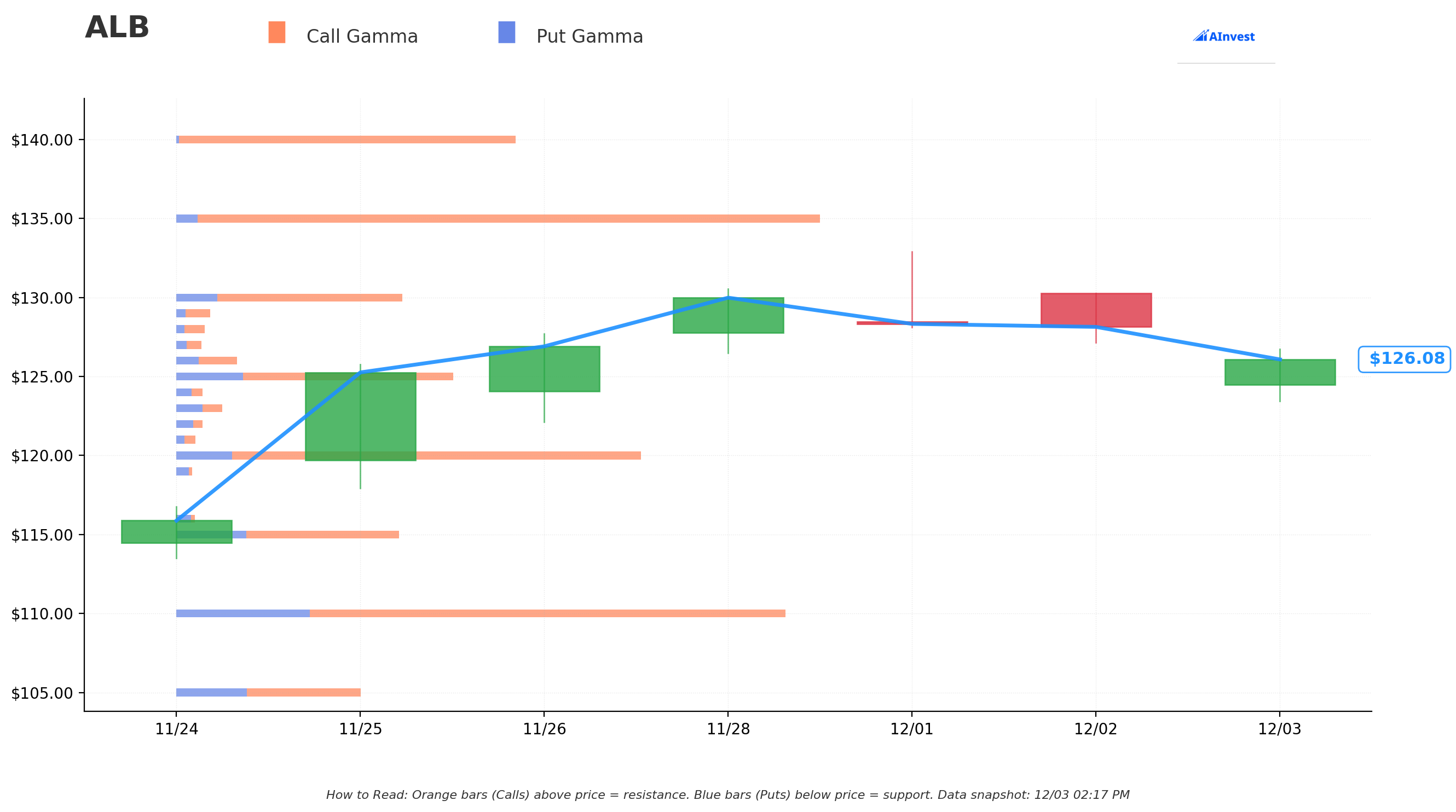

Gamma-Based Support & Resistance Analysis

Current Price: $126.08

The gamma exposure map shows critical inflection points, though notably the GEX data appears neutral (0.0 across all strikes) suggesting limited dealer hedging pressure currently. Let me interpret the chart's visual gamma bars:

🔵 Support Levels (Put Gamma Below Price):

- $125 - Immediate support zone where stock is currently trading

- $120 - Secondary support level

- $115 - Deeper support floor

- $110 - Major structural support (exactly where this call trade is struck! Not coincidental)

- $105 - Extended downside floor

🟠 Resistance Levels (Call Gamma Above Price):

- $130 - Immediate resistance ceiling (recent highs tested here)

- $135 - Secondary resistance

- $140 - Major resistance zone

- $145-150 - Extended upside targets if momentum continues

What this means for traders: ALB is consolidating in a $125-130 range after the strong November rally. The lack of significant gamma pressure (0.0 GEX readings) suggests reduced dealer hedging activity, which could mean more directional volatility is possible - the stock isn't "pinned" to any particular strike. The $130 level represents the recent high from late November/early December and will be the key breakout level to watch.

Notice anything? The call buyer structured their position at the $110 strike, which provides a significant cushion (12% below current price). This deep in-the-money positioning suggests they want delta exposure close to owning stock, while maintaining the leverage and defined risk of options. If ALB dips to $110, these calls still have $0 intrinsic value as a floor.

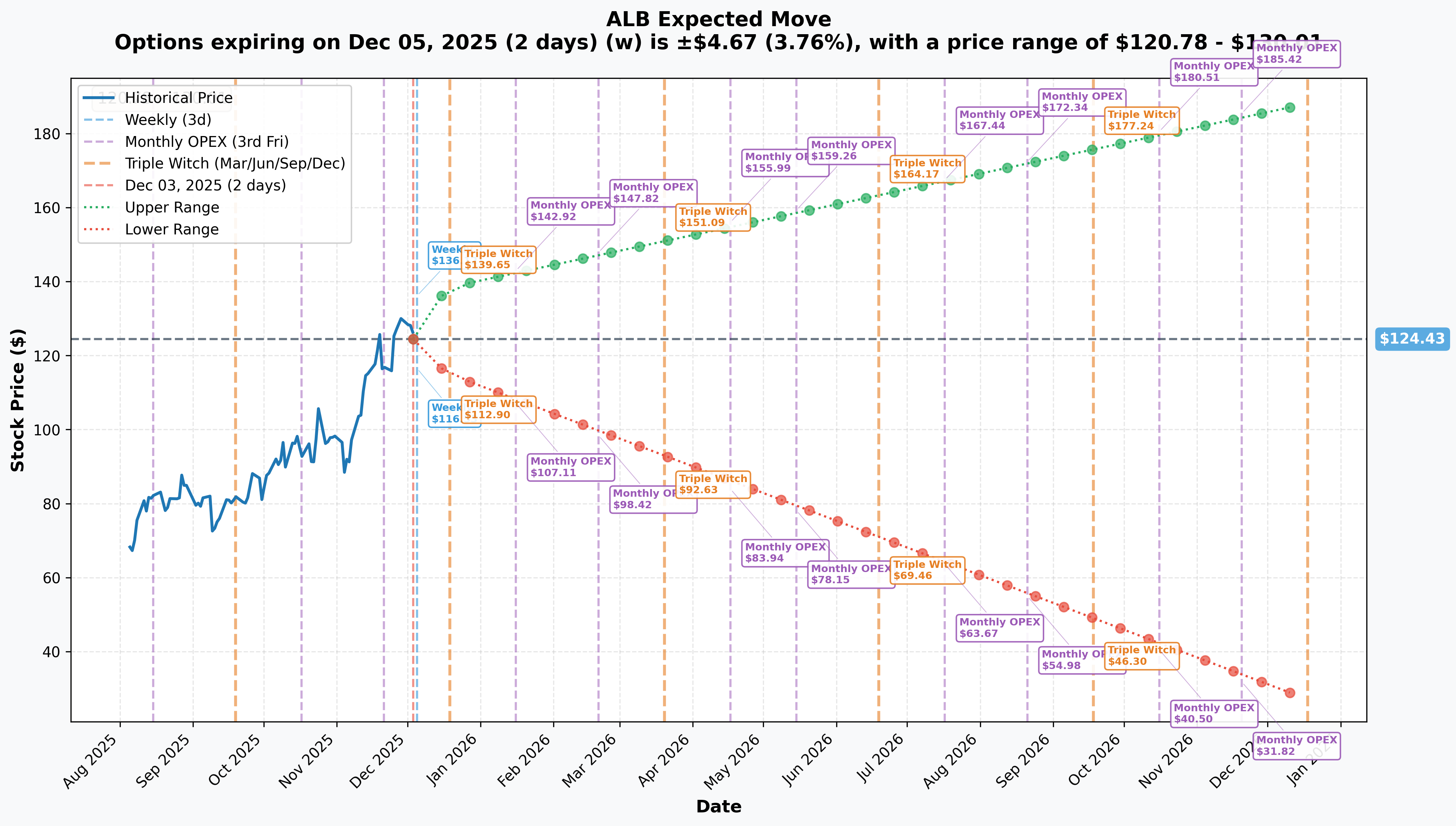

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 5 - 2 days): ±$4.67 (±3.76%) → Range: $120.78 - $130.01

- 📅 Monthly OPEX (Dec 19 - 16 days - THIS TRADE!): ±$11.11 (±8.93%) → Range: $114.83 - $138.56

- 📅 January OPEX (Jan 16 - 44 days): ±$14.72 (±11.83%) → Range: $109.71 - $139.15

- 📅 Yearly LEAPS (Dec 18, 2026 - 380 days): ±$70.78 (±56.89%) → Range: $26.99 - $188.14

Translation for regular folks: Options traders are pricing in a 3.8% move ($5) by Friday for weekly expiration, but a much larger 8.9% move ($11) through December 19th triple witch when this call position expires. The market expects decent volatility heading into year-end, with an upper range of $138.56 by December 19th - nearly 10% upside from current levels.

The January expiration shows an upper range of $139.15, while the longer-term LEAPS pricing reflects the extreme uncertainty in lithium markets - with a 380-day range spanning from $27 to $188! This massive spread captures the binary nature of the lithium thesis: either prices recover and ALB surges toward $150-200, or the oversupply persists and the stock revisits cycle lows.

Key insight: The relatively modest 8.9% implied move through December 19th (upper target $138.56) aligns perfectly with this call buyer's thesis. With the strike at $110 and current price at $125, they need the stock to simply hold above $110 (12% cushion) to maintain value, while any move toward $135-140 would generate significant gains on the remaining time premium.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

December 19, 2025 - Triple Witch OPEX (16 DAYS!) 🎢

The option expiration date coincides with quarterly triple witching, which historically creates increased volatility as large positions get closed or rolled. With 10,000 contracts at $110 strike representing $125M in notional exposure, this expiration could see significant stock movement as market makers hedge or unwind positions.

Year-End Portfolio Rebalancing (December 2025) 📊

Institutional funds typically rebalance portfolios in late December, which can drive significant flows in names like ALB that have moved 48% YTD. Given the strong recovery from April lows, many funds may be underweight and could add exposure, while others may trim to lock in gains. The stock's inclusion in multiple ESG and clean energy indices could amplify these flows.

🚀 Near-Term Catalysts (Q1 2026)

Q4 2024 Earnings - February 12, 2025 (71 DAYS) 📈

ALB reports fiscal Q4 2024 results on February 12, 2025 with conference call on February 13th at 8:00 AM ET. This is THE major catalyst that will validate whether the lithium recovery thesis is playing out:

Key metrics to watch:

- 📊 2025 Guidance: Management expected to provide full-year 2025 guidance at upper end of $9/kg lithium price scenario

- 📈 Energy Storage Volume: Strong growth already noted; Q4 will show if momentum continues

- 💰 Cost Savings Execution: Progress on $300-400M annual cost reduction program implemented November 1st

- 🎯 Lithium Pricing Realization: Whether the company is seeing stabilization or improvement from current ~$9.50/kg levels

- 💸 EPS Consensus: $1.75 for 2025 (up 217.5% YoY)

Why this matters: The Q3 results in November showed a devastating $1.1B net loss including $861M in asset write-downs. Q4 guidance will reveal management's confidence in the 2026 recovery narrative. Any positive surprise on lithium demand or cost savings could send the stock toward $140-150 resistance levels.

Ketjen Business Divestiture - H1 2026 (Expected within 180 days) 💵

ALB announced the sale of 51% controlling stake in Ketjen to KPS Capital Partners generating ~$660M in pre-tax cash proceeds. Expected close in first half of 2026 pending regulatory approvals.

Strategic impact:

- 💰 Balance sheet improvement: Proceeds earmarked for debt reduction (currently $3.6B debt with 3.5x leverage ratio)

- 🎯 Focus on core business: Allows ALB to concentrate on lithium and bromine, reducing portfolio complexity

- 📈 Shareholder value: Unlocks value in non-core asset while retaining 49% minority stake for upside participation

- ⚠️ De-risking: Strengthens financial position ahead of lithium market recovery

The timing of this transaction (H1 2026) means the cash infusion should arrive right as the lithium market shifts from oversupply to deficit, positioning ALB with a fortress balance sheet to capitalize on the recovery.

Lithium Market Inflection Point - 2026 (THE BIG ONE!) 🌍

Multiple industry forecasts point to 2026 as the year lithium supply-demand fundamentals flip from bearish to bullish:

Supply-Demand Dynamics:

- 📉 2025 Forecast: ~10,000 tonnes oversupply (keeping prices suppressed)

- 📈 2026 Forecast: Shift to 1,500-tonne deficit (first deficit since 2022!)

- 🚀 2030 Projection: 97,000-tonne deficit with supply at 373Kt vs demand of 472Kt

Lithium Pricing Outlook:

- 💸 Current (End 2024): ~$9,655 per tonne (down 87% from $77,041 peak in late 2022)

- 📊 2025 Expected: ~$9.50/kg average based on ALB's guidance scenarios

- 🎯 Recovery Trajectory: Reached 11-month high of $12,067/tonne in August 2025 before settling at $11,186

- 💰 Long-term (2027-2040): Structural bull market driven by widening supply-demand gap

Demand Drivers:

- 🚗 EV Sales: 17M units in 2024, projected >20M in 2025 (+22% growth)

- 🔋 Grid Storage: Exceeded 90 GWh in 2024, costs expected to fall 40% by 2030

- 📈 Global Demand: ALB forecasts 1.8M tonnes LCE in 2025, doubling to 3.7M tonnes by 2030

- 🌐 Clean Energy Transition: IEA projects 5x increase in lithium demand by 2040

Why this matters for ALB: The company has been bleeding cash during the 2023-2024 downturn (-$1.1B net loss in Q3), but has used this time to cut costs ($300-400M savings program), reduce capex from $1.7B to $0.7B, and improve operational efficiency. When the 2026 deficit materializes and prices recover toward $15-20/kg, ALB will be positioned as the low-cost producer with a clean balance sheet (post-Ketjen sale) to capture massive margin expansion. This is the setup institutional buyers are positioning for with deep ITM call options.

📊 Recent Developments (Last 90 Days)

Analyst Upgrades and Price Target Changes (November-December 2024) 📈

The Street is coming around on ALB after brutal 2023-2024 downgrades:

- 💚 Baird (December 2, 2024): Upgraded from Underperform to Neutral, raised PT from $81 to $113 - Major sentiment shift!

- 📊 Oppenheimer: Cut PT to $123 from $170, maintained Outperform - Still sees upside despite reduction

- 📈 Evercore ISI: Raised PT to $100 from $88 - Seeing improving fundamentals

- 💰 Wells Fargo: Raised PT to $100 from $90 - Incrementally more positive

- ⚖️ Mizuho Securities: Lowered PT from $105 to $90, maintained Neutral - Still cautious

- 📉 Truist Securities: Initiated coverage with Hold rating and $96 PT - Wait-and-see approach

Current Consensus:

- 📊 Rating Distribution: 6 Buy, 10 Hold, 2 Sell

- 💰 Average Price Target: $104.27 (range: $58-$136)

- 🎯 Consensus Rating: Hold

- 📈 Sentiment: Moderately bullish with caution on near-term lithium pricing

The Baird upgrade from Underperform to Neutral on December 2nd was particularly notable - it came just ONE DAY before this $17M call trade, suggesting smart money front-ran the broader market's recognition of improving fundamentals. Analyst coverage is shifting from "avoid" to "show me" mode, with multiple upgrades in late November as lithium demand outlook improves.

Legal Settlement with Chilean Indigenous Community (December 2024) 🇨🇱

ALB reached conciliation agreement with Atacameño people in Chile providing compensation for damages to meadows and lakes (Tilopozo, La Punta, La Brava). This removes a significant regulatory overhang in ALB's critical Chilean lithium operations, which supply substantial portions of global lithium from salt brine deposits. Reduces tail risk of operational shutdowns or production curtailments.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through December 19th expiration:

📈 Bull Case (35% probability)

Target: $135-145

How we get there:

- 🎯 Year-end institutional rebalancing drives momentum as funds add ESG/clean energy exposure

- 📈 Lithium spot prices continue recovery toward $12-13/kg from current $9.50 levels

- 💚 Additional analyst upgrades follow Baird's lead as fundamentals improve

- 🌍 Positive industry data on Q4 EV sales and energy storage deployments

- 📊 Technical breakout above $130 resistance triggers momentum buying toward $135-140

- 🇨🇳 Any positive developments on China demand or export policy

- 💰 Speculation builds ahead of February 12th earnings and strong 2025 guidance expectations

- ✅ Ketjen deal progress announced, providing visibility on $660M cash infusion timing

Key metrics needed:

- Lithium carbonate prices holding above $11,000/tonne

- No major production curtailments or delays announced

- Macro environment remains supportive (no recession fears)

- Technical momentum indicators stay positive (RSI >50, MACD bullish)

Probability assessment: 35% because it requires sustained positive newsflow and absence of negative surprises. The December 19th timeline is short (16 days) to reach $135-145 from $125, requiring 8-16% rally. However, the stock has shown it can make these moves quickly (rallied $20 in November alone). The implied move upper range of $138.56 suggests options market gives it reasonable odds.

Call P&L in Bull Case:

- Stock at $135 on Dec 19: Calls worth $25.00 intrinsic, gain = $25.00 - $16.70 = $8.30/share × 10,000 = $8.3M profit (49% ROI)

- Stock at $140 on Dec 19: Calls worth $30.00 intrinsic, gain = $30.00 - $16.70 = $13.30/share × 10,000 = $13.3M profit (78% ROI)

- Stock at $145 on Dec 19: Calls worth $35.00 intrinsic, gain = $35.00 - $16.70 = $18.30/share × 10,000 = $18.3M profit (108% ROI!)

🎯 Base Case (45% probability)

Target: $120-130 range (CONSOLIDATION)

Most likely scenario:

- ⚖️ Stock consolidates recent gains in $120-130 channel through December OPEX

- 📊 Lithium prices remain range-bound around $9-11/kg as 2025 oversupply persists

- 🎄 Holiday-thinned trading volumes create choppy, directionless price action

- 💤 Market in "wait and see" mode ahead of February 12th earnings catalyst

- 📈 No major positive OR negative surprises - steady as she goes

- 🔄 Technical range trading between $125 support and $130 resistance

- 💰 Time decay gradually erodes call premium but intrinsic value maintained

- 🎯 Triple witch volatility on December 19th but no sustained breakout

This scenario keeps the call buyer profitable: With the $110 strike and stock at $120-130, intrinsic value ranges from $10-20, so even losing the entire $1.59 time premium paid, they're still capturing $8.41-18.41/share in gains vs the $16.70 cost. Most likely they close early in this range to lock in profits or roll to January/February expiration to hold through earnings.

Why 45% probability: This is the path of least resistance - stock holding ground after 48% YTD rally, market waiting for next catalyst, no major surprises either way. Consolidation is the healthy, expected outcome after a big move. The gamma data showing neutral positioning supports this range-bound thesis.

Call P&L in Base Case:

- Stock at $125 on Dec 19: Calls worth $15.00 intrinsic, loss = $15.00 - $16.70 = -$1.70/share × 10,000 = -$1.7M loss (10% loss)

- Stock at $130 on Dec 19: Calls worth $20.00 intrinsic, gain = $20.00 - $16.70 = $3.30/share × 10,000 = $3.3M profit (19% ROI)

Even in the consolidation scenario, if stock stays above $127, the call buyer breaks even or makes modest gains.

📉 Bear Case (20% probability)

Target: $110-120 (TEST THE STRIKE!)

What could go wrong:

- 😰 Lithium spot prices roll over again, breaking below $9,000/tonne on renewed China oversupply fears

- 🇨🇳 Weak China economic data suggests EV demand slowdown in world's largest market

- 📉 Broader market selloff or risk-off environment ahead of year-end (tax loss selling)

- ⚠️ Negative pre-announcement or analyst downgrade ahead of February earnings

- 💸 Ketjen deal regulatory delays or complications announced

- 🏭 Unexpected production issues or cost overruns at key facilities

- 📊 Technical breakdown below $120 support triggers stop losses and momentum selling

- 💔 Institutional profit-taking accelerates after 48% YTD gain (lock in wins before year-end)

Critical support levels:

- 🛡️ $120: Secondary support from implied move lower range

- 🛡️ $115: Deeper support floor from gamma analysis

- 🛡️ $110: MAJOR SUPPORT (exactly where this call is struck!) - line in the sand

Probability assessment: Only 20% because fundamentals are improving (restructuring complete, costs down, 2026 recovery thesis intact), recent analyst upgrades show improving sentiment, and stock has shown resilience holding $120+ after pullback from $132. Would require multiple negative catalysts to break down to $110. However, lithium remains a volatile sector and ALB has 63% annualized volatility - so $15 downmoves (12%) are within normal range.

Call P&L in Bear Case:

- Stock at $120 on Dec 19: Calls worth $10.00 intrinsic, loss = $10.00 - $16.70 = -$6.70/share × 10,000 = -$6.7M loss (40% loss)

- Stock at $115 on Dec 19: Calls worth $5.00 intrinsic, loss = $5.00 - $16.70 = -$11.70/share × 10,000 = -$11.7M loss (70% loss)

- Stock at $110 on Dec 19: Calls worth $0 (at-the-money), loss = $0 - $16.70 = -$16.70/share × 10,000 = -$16.7M loss (98% loss!)

The $110 strike provides a floor - below that level, losses accelerate rapidly as calls move out-of-the-money.

Breakeven Analysis: The call buyer's breakeven is $126.70 at expiration ($110 strike + $16.70 premium paid). With current price at $125.11, they're already close to breakeven territory, suggesting they either got in at better prices earlier and are taking profits now, or they're confident the stock will stay above $127 through December 19th.

💡 Trading Ideas

🛡️ Conservative: Wait for February Earnings Setup

Play: Stay on sidelines until post-earnings volatility in February provides clearer setup

Why this works:

- ⏰ With Q4 earnings on February 12th being the major catalyst, the December 19th expiration captures minimal fundamental catalysts

- 📊 Better risk/reward waiting for earnings clarity on 2025 guidance, lithium pricing outlook, and cost savings execution

- 💸 Options premiums expensive pre-earnings - let IV crush work in your favor

- 🎯 Post-earnings pullback (even on good news) often provides better entry points with lower implied volatility

- 🔮 Lithium market inflection into 2026 is the real thesis - no need to rush into short-dated options

- ⚠️ December is illiquid holiday trading - better to wait for January institutional flows

Action plan:

- 👀 Monitor lithium spot prices at Investing News lithium forecast for any acceleration toward $12-13/kg

- 📈 Watch for $120 support to hold - that's the key level for maintaining bullish structure

- 🎯 Look for entry on any pullback to $115-120 range in January ahead of February earnings

- 📊 Review Q4 earnings results and 2025 guidance to assess whether lithium recovery thesis remains intact

- ⏰ Consider March or April options (post-earnings) for longer-dated exposure with less time decay risk

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid getting chopped up in pre-holiday volatility. Get better entry point post-earnings with clearer fundamental visibility. Maintain flexibility.

⚖️ Balanced: Bull Put Spread (Copy The Setup)

Play: Sell put spread targeting $120-115 support zone

Structure: Sell $120 puts, Buy $115 puts (December 19 expiration - SAME as the call trade)

Why this works:

- 💰 Collect premium betting stock stays above $120 (implied move lower range support)

- 📊 Defined risk spread ($5 wide = $500 max risk per spread)

- 🎯 Aligns with bullish institutional positioning shown by the $17M call trade

- ⏰ Short 16-day timeframe benefits from rapid time decay (theta works FOR you)

- 🛡️ $120 support has held multiple times recently - solid technical floor

- 📈 Fundamentals improving (restructuring done, analyst upgrades, 2026 recovery thesis)

- 💸 High implied volatility (63%) means premiums are juicy for sellers

Estimated P&L:

- 💰 Collect ~$2.00-2.50 credit per spread (check current pricing)

- 📈 Max profit: $200-250 if ALB above $120 at December 19 expiration (keep full credit)

- 📉 Max loss: $250-300 if ALB below $115 (defined and limited to width minus credit)

- 🎯 Breakeven: ~$117.50-118 depending on credit received

- 📊 Probability of profit: ~60-65% (stock needs to stay above $118)

Entry timing:

- 🎯 Enter if stock pulls back to $123-125 range (gives some cushion above $120 floor)

- ✅ Confirm $120 support holding on any test

- ❌ Skip if stock already approaching $120 or below (too close to strike)

- 📊 Ensure credit received is at least $2.00 (40% of spread width for adequate risk/reward)

Position sizing: Risk only 2-3% of portfolio (this is income strategy, not speculation)

Management:

- 🎯 Take profit at 50% of max gain ($100-125 per spread) if achieved quickly

- ⚠️ Close early if stock breaks $118 with 5+ days remaining (don't wait for expiration)

- 📈 Let expire worthless for full profit if stock solidly above $122 on expiration day

Risk level: Moderate (defined risk, bullish bias) | Skill level: Intermediate

🚀 Aggressive: January Call Calendar Spread (ADVANCED!)

Play: Buy time while selling near-term premium into December OPEX

Structure: Sell December 19 $130 calls, Buy January 16 $130 calls

Why this could work:

- 📅 Sell expensive near-term premium (16 days) while buying cheaper longer-dated option (44 days)

- 🎯 Targets $130 resistance as the "sweet spot" - not too far out-of-money

- ⏰ December expiration captures triple witch volatility, then you own January call through earnings

- 💸 Time decay works in your favor - short option loses value faster than long option

- 📊 If stock consolidates around $125-128 through Dec 19, short call expires worthless and you own January call at reduced cost

- 🚀 Positions you for February 12th earnings catalyst with minimal upfront capital

Why this could blow up (SERIOUS RISKS):

- 📈 Early assignment risk: If stock rallies hard above $130 before Dec 19, short call could be assigned early

- 💥 Gap risk: If major catalyst causes stock to gap to $140+, you're short the upside and stuck with losses

- 🎢 Volatility risk: If IV collapses after December OPEX, both calls lose value (vega risk)

- ⏰ Complexity: Calendar spreads require active management - not set-and-forget

- 💸 Capital inefficiency: Tying up margin for spread that has limited profit potential vs outright directional trade

Estimated P&L:

- 💰 Net debit: ~$2-3 per spread (buying Jan $130 call for ~$5-6, selling Dec $130 call for ~$2-3)

- 📈 Max profit: ~$4-5 if stock at exactly $130 on Dec 19 (short expires worthless, long has max value)

- 📉 Max loss: ~$2-3 net debit paid if stock drops significantly (both calls become worthless)

- 🎯 Ideal outcome: Stock at $128-132 on Dec 19, then rallies to $140+ by January expiration

Breakeven analysis: This spread profits if:

- Stock stays below $130 through Dec 19 (short call expires worthless)

- Stock then rallies above $130 by January 16 (long call gains value)

- Implied volatility stays elevated or increases into February earnings

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand calendar spread mechanics and time decay dynamics

- ✅ Can monitor position daily and adjust if needed

- ✅ Have experience with early assignment risk management

- ✅ Accept that max profit zone is very narrow ($128-132 range)

- ✅ Understand volatility risk (vega) and how IV changes affect both legs

- ⏰ Are willing to close the spread early if stock moves against you (above $135 or below $120)

Risk level: HIGH (complex spread, multiple risk factors) | Skill level: Advanced only

Probability of profit: ~40% (narrow profit zone, requires precision)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💸 Lithium price volatility remains extreme: Current spot prices around $9,655/tonne are down 87% from $77,041 peak in late 2022. While forecasts show 2026 deficit emerging, Chinese oversupply continues to pressure prices in 2025. Any renewed price collapse toward $7-8/kg levels would crater ALB stock back toward $80-90 range. The recovery thesis is NOT guaranteed - timing is uncertain.

-

🇨🇳 China dominates global lithium market (63% share vs ALB's 13%): Chinese competitors have surged production 55% from 2023-2025 and are projected to overtake Australia as world's top producer by 2026. CEO Kent Masters acknowledged "we're being a little more cautious and investing behind the market, so there's a risk we lose that share". If China floods market with cheap lithium, the recovery could be delayed by years. Geopolitical tensions add uncertainty.

-

💰 Balance sheet stress with $3.6B debt and covenant waivers: ALB required covenant waiver extension through Q2 2026 due to 3.5x net debt/EBITDA ratio. While liquidity is $3.4B, the company is burning cash during downturn. Any further deterioration in lithium prices or operational issues could force additional asset sales, equity raises, or production curtailments. The Ketjen sale generating $660M helps but doesn't eliminate leverage concerns.

-

📉 Massive losses continue: -$1.1B net loss in Q3 including $861M asset write-downs: The Q3 2024 results showed devastating charges primarily for capital project write-offs. Revenue dropped 41% YoY to $1.4B from $2.3B. While adjusted EBITDA of $211M shows core operations remain positive, the company is nowhere near profitable at current lithium prices. Path to sustained profitability entirely dependent on lithium price recovery that may not materialize until late 2026 or beyond.

-

🏭 Aggressive CapEx cuts risk missing the recovery: ALB slashed 2024 CapEx to $600M (65% reduction) and 2025 to $700-800M (down >50%) with capacity expansion projects like Nevada Silver Peak and South Carolina facilities delayed. While prudent during downturn, this conservative approach means ALB may be capacity-constrained when demand surges in 2026-2027. Chinese competitors investing aggressively could capture incremental market share.

-

⚖️ Valuation still expensive despite pullback: At current $125 price with $15.08B market cap, ALB trades at -80.25x P/E (negative due to losses) but consensus 2025 EPS of $1.75 implies forward multiple of ~71x. This is RICH pricing for a cyclical materials company, requiring perfect execution on 2026 recovery thesis. Any disappointment magnified at this valuation. No margin of safety.

-

📊 High short interest (12.34M shares, 13.32% of float) reflects skepticism: Short interest declined 9.5% in November following restructuring announcements and analyst upgrades, but remains elevated at 5.0 days-to-cover. This is 5x the peer group average of 2.74%, indicating sophisticated investors remain bearish despite recent rally. While this creates short squeeze potential, it also signals genuine fundamental concerns about the timing/magnitude of lithium recovery.

-

🎢 Extreme volatility (63%) creates whipsaw risk: YTD volatility of 63% with 47.9% max drawdown means ALB can easily move $10-15 (8-12%) on NO NEWS. This isn't a stable dividend aristocrat - it's a leveraged play on lithium prices with massive daily swings. Recent $52 low in April to $132 high in November represents 150% rally in 7 months, showing how quickly sentiment shifts. Stock dropped from $132 to $125 just in the past week.

-

🚗 EV adoption pace uncertainty impacts demand forecasts: While projections show EV sales growing from 17M in 2024 to >20M in 2025, consumer demand has been softer than expected in key markets. Affordability concerns, charging infrastructure gaps, and competition from plug-in hybrids could slow EV penetration. If demand disappoints, ALB's 2026 deficit thesis falls apart.

-

⚠️ Alternative battery technologies pose long-term threat: Solid-state batteries, sodium-ion alternatives, and improved battery recycling could reduce lithium intensity per vehicle over time. While not imminent (5-10 year timeframe), these technologies represent tail risk to structural lithium bull thesis. ALB's high debt load and current losses mean company has limited runway if demand disappoints structurally.

-

👥 Insider selling with zero insider buying is notable: Recent insider sales including CEO J Masters selling 2,525 shares in December and COO selling 1,060 shares in November with 0 buys vs 4 sells in past 12 months. While these are relatively small transactions typical of executive compensation liquidation, the absence of ANY insider buying during the 48% recovery rally suggests management isn't putting their own money to work at current levels. Red flag.

-

📅 Short 16-day timeframe for this trade adds execution risk: With expiration on December 19th, there's minimal time for the lithium recovery thesis to play out. This trade captures holiday-thinned trading, year-end rebalancing volatility, and triple witch OPEX - but misses the February 12th earnings catalyst and H1 2026 Ketjen proceeds. Makes sense for the institutional buyer closing a profitable position, but risky for new entries at these levels.

🎯 The Bottom Line

Real talk: Someone just deployed $17 MILLION to close or adjust a winning $110 call position on ALB with the stock near recent highs after a 48% YTD rally. This isn't a bearish signal - it's sophisticated profit-taking and position management by institutions who've captured massive gains from the April lows around $52 to current $125+ levels. The "BTC" (Buy To Close) order type suggests they're locking in a winning trade that likely cost them $5-8 per contract months ago and is now worth $16.70.

What this trade tells us:

- 💰 Institutions are TAKING PROFITS at current levels after the strong Q4 rally, not initiating new aggressive bullish bets

- 🎯 The deep ITM strike at $110 (12% below current price) shows these were delta-hedged positions, not speculative lottery tickets

- ⏰ December 19th expiration is BEFORE the major catalysts (February 12 earnings, H1 2026 Ketjen sale), suggesting they're trimming before year-end

- 📊 The timing one day after Baird's upgrade from Underperform to Neutral shows smart money selling into improving sentiment

- 🔄 This likely represents portfolio rebalancing, option roll strategies, or tax-loss harvesting considerations

This is NOT a "buy everything" signal - it's a "winners are taking money off the table" signal.

If you own ALB:

- ✅ Consider trimming 20-30% at $125+ levels to lock in gains from the $52 lows (137% rally!)

- 📊 Set mental stop at $115-120 (major support zone) to protect remaining position

- ⏰ Re-evaluate after February 12th earnings when management provides 2025 guidance and lithium pricing outlook

- 🎯 If holding for the 2026 lithium recovery thesis, use any pullback to $110-115 to add to position

- 💰 The long-term thesis (2026 deficit, $660M Ketjen proceeds, cost restructuring) remains intact despite near-term profit-taking

If you're watching from sidelines:

- ⏰ Wait for better entry point - don't chase at current levels after 48% YTD gain

- 🎯 Target $115-120 pullback zone for initial entry with 8-10% margin of safety

- 📈 Look for confirmation of: Lithium spot prices holding above $10,000/tonne, Q4 EV sales data strong, no negative China news

- 🚀 Post-February earnings may provide excellent entry if 2025 guidance confirms lithium recovery trajectory

- 📊 This is a 12-18 month thesis play (2026 lithium deficit), not a quick trade - be patient

If you're bearish:

- ⚠️ Don't fight the improving fundamentals - restructuring complete, analyst upgrades accelerating, 2026 supply deficit forecast

- 📊 First resistance at $130 (recent highs), major resistance at $135-140

- 🎯 Any breakdown below $120 could trigger cascade to $115, then $110 support

- 📉 Put spreads targeting $120/$115 offer defined-risk way to play near-term consolidation

- ⏰ Best shorting setup would be AFTER earnings disappointment in February, not now

Mark your calendar - Key dates:

- 📅 December 19 (Thursday) - Quarterly triple witch OPEX, expiration of this $17M call trade (16 DAYS!)

- 📅 December 31 - Year-end (tax considerations, portfolio rebalancing)

- 📅 February 12, 2025 (Wednesday after close) - Q4 FY2024 earnings report (71 days)

- 📅 February 13, 2025 (Thursday 8:00 AM ET) - Earnings conference call

- 📅 H1 2026 - Ketjen business divestiture close expected, $660M proceeds

- 📅 2026 - Lithium market projected shift from 10,000-tonne oversupply to 1,500-tonne deficit

Final verdict: ALB's long-term lithium recovery thesis remains compelling - 2026 supply deficit, $300-400M cost savings, $660M Ketjen proceeds for debt reduction, and positioned as low-cost producer when lithium prices recover toward $15-20/kg. BUT, at $125 after a 48% YTD rally with negative earnings and 99% institutional ownership, the risk/reward is NO LONGER favorable for aggressive new positioning at these levels. The $17M call buyback is smart money taking chips off the table after a great run.

Be patient. Let December triple witch pass. Look for better entry $115-120. The lithium supercycle will still be here in Q1 2026, and you'll sleep better at night paying $115 instead of $125.

This is a marathon, not a sprint. Protect your capital and wait for your pitch.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual score of 555x average size reflects this specific trade's volume relative to recent ALB history - it does not imply the trade will be profitable or that you should follow it. The "BTC" (Buy To Close) order type suggests this is closing an existing position, not opening a new bullish bet. Always do your own research and consider consulting a licensed financial advisor before trading. Lithium markets are highly volatile and speculative.

About Albemarle Corporation: Albemarle is one of the world's largest lithium producers with integrated operations spanning resource extraction, refining, and bromine production. The firm operates salt brine deposits across multiple continents and maintains joint venture hard rock mines in Australia, with a market cap of $15.08 billion in the Plastics Materials industry.