💎 AMD $8M Put Sale - Bullish LEAPS Bet on AI Chip Dominance! 🚀

📅 January 7, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just collected $8 MILLION in premium by selling 1,000 long-dated puts on AMD at the $250 strike expiring January 2028! This is a massively bullish LEAPS position where a sophisticated trader is betting AMD stays above $250 (19% higher than current price of $210.25) over the next 2 years. With a Z-score of 29.25 marking this as EXTREMELY UNUSUAL activity and AMD positioning for major AI chip deployments in 2026-2027, this whale is collecting huge premium while expressing confidence in the long-term AI growth story. Translation: Smart money is selling insurance at premium prices, betting AMD's AI revolution keeps the stock elevated!

📊 Company Overview

Advanced Micro Devices (AMD) is a global semiconductor powerhouse leading the charge in AI accelerators, competing directly with Nvidia for dominance in the exploding data center GPU market:

- Market Cap: $347.31 Billion (as of January 6, 2026)1

- Industry: Semiconductors & Related Devices

- Sector: Technology

- Current Price: $210.25

- Primary Business: AMD designs digital semiconductors for PCs, gaming consoles, data centers (including AI accelerators), industrial, and automotive applications. The company's Instinct MI series GPUs compete with Nvidia for AI training and inference workloads, while EPYC processors have captured over 50% share in hyperscaler data centers.

💰 The Option Flow Breakdown

The Tape (January 7, 2026 @ 11:02:11):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:02:11 | AMD | MID | SELL | PUT $250 | 2028-01-21 | $8M | $250 | 1,000 | 541 | 1,000 | $210.25 | $80.22 |

🤓 What This Actually Means

This is a bullish short put position - someone is SELLING puts for massive premium! Here's the breakdown:

- 💸 Premium collected: $8M ($80.22 per contract × 1,000 contracts) - that's immediate cash in pocket

- 🎯 Strike positioned: $250 is 19% ABOVE current price of $210.25 - this is aggressive bullishness!

- ⏰ Time horizon: 745 days until January 2028 expiration - this is a long-term strategic bet

- 📊 Contract size: 1,000 contracts represents 100,000 shares worth ~$21M at current prices

- 🏦 Institutional confidence: This trader is expressing maximum conviction that AMD won't crash below $250

What's really happening here:

This trader is running the "sell puts, keep premium" playbook at maximum scale. By selling $250 strike puts expiring January 2028, they collect $8M TODAY. As long as AMD stays above $250 over the next two years, they keep the entire $8M premium with zero obligation. Think of it like being an insurance company - they're selling "crash protection" to nervous traders, but they're confident the crash won't happen.

If AMD drops below $250 by January 2028: They'd be obligated to buy 100,000 shares at $250 each (total cost: $25M). But they already collected $8M premium, so their effective cost basis would be $170 per share ($250 strike - $80.22 premium). That's still 19% BELOW today's price of $210.25, giving them a massive safety cushion.

The bullish thesis: This position only makes sense if they believe AMD will trade significantly higher than $250 over the next 2 years, driven by the OpenAI 6-gigawatt GPU partnership, MI400/MI500 series GPU deployments, and continued AI market share gains from Nvidia.

Unusual Score: 🔥 EXTREMELY UNUSUAL (29.25x Z-score) - This is massive institutional positioning that happens a few times per year. The 1.848 Vol/OI ratio shows HIGH_ACTIVITY with volume nearly 2x open interest, signaling fresh conviction rather than existing position management.

📈 Technical Setup / Chart Check-Up

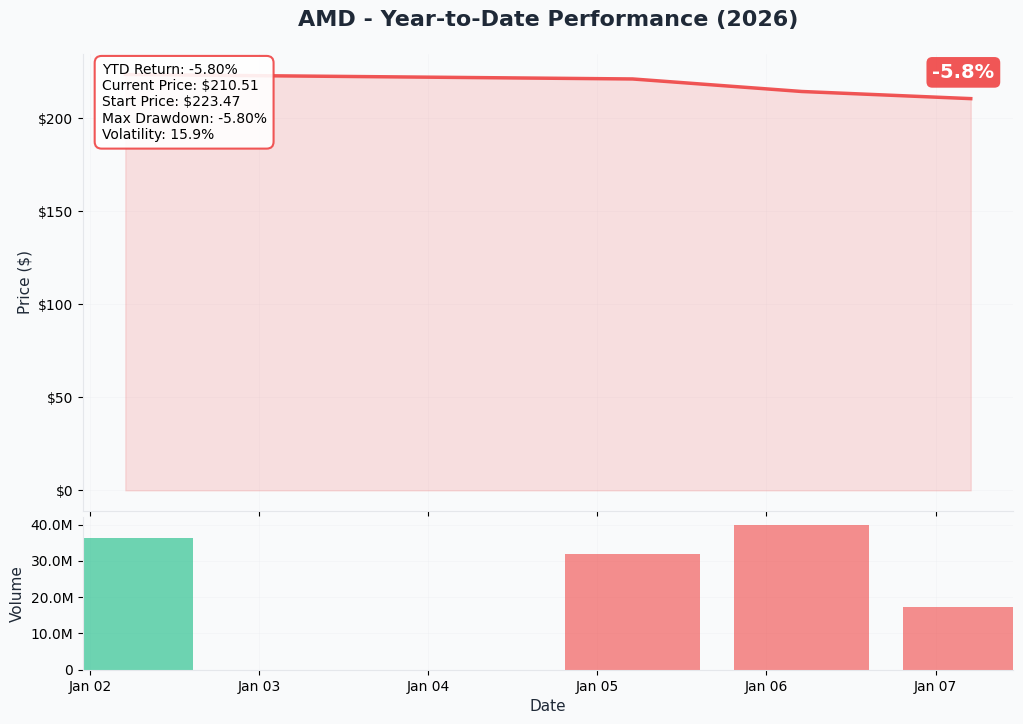

YTD Performance Chart

AMD has had a rollercoaster ride - after surging 77% in 2025 on the back of the landmark OpenAI partnership announcement in October, the stock hit an all-time high of $267.08 before pulling back 21% to current levels around $210. The recent 3-month decline from $264 reflects profit-taking and broader tech sector weakness, but the stock remains up substantially from the $125 lows seen in early 2025.

Key observations:

- 📈 Strong 2025 performance: +77% YTD in 20252 driven by OpenAI partnership and AI GPU momentum

- 📉 Recent pullback: Down ~20% from October 2025 peak of $2643, creating potential entry opportunity

- 💪 Consolidation zone: Trading in the $200-215 range as market digests Q4 earnings ahead of February 3 release

- 🎯 Critical support: Holding above $200 psychological level and key gamma support zones

- 🚀 Major catalysts ahead: Q4 earnings (Feb 3), MI400 deployments (2026), OpenAI 1-GW deployment (H2 2026)

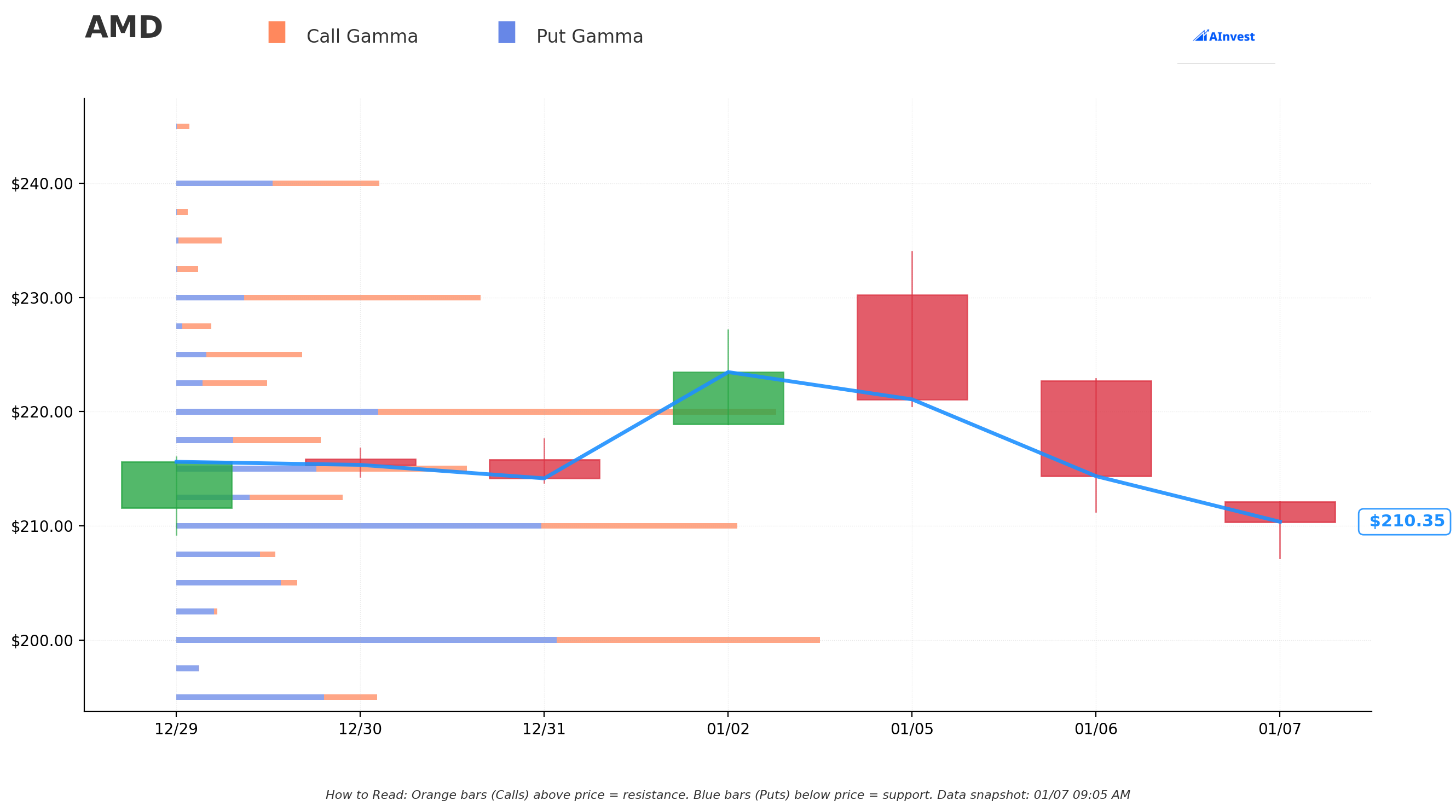

Gamma-Based Support & Resistance Analysis

Current Price: $210.25

The gamma exposure map reveals critical price magnets where options market activity creates natural support and resistance:

🔵 Support Levels (Put Gamma Below Price):

- $210 - Immediate support right at current price (strong gamma concentration)

- $205 - Secondary support with solid put gamma wall (2.4% downside cushion)

- $200 - Major psychological and gamma support floor (5.2% below current - LINE IN THE SAND)

- $190 - Extended support if $200 breaks (9.6% downside)

🟠 Resistance Levels (Call Gamma Above Price):

- $215 - Immediate resistance overhead (2.3% above current)

- $220 - Secondary resistance zone (4.6% above current price)

- $225 - Major resistance barrier (7.0% rally required to reach)

- $230 - Extended upside target (9.4% above current)

What this means for traders:

AMD is consolidating in a tight $200-220 range with strong gamma support at the $200-210 levels and resistance at $215-225. The options market is effectively creating a "price prison" where dealers' hedging activity will dampen moves in either direction. This consolidation pattern typically precedes a major breakout once a catalyst (like earnings) provides directional momentum.

Notice the put seller's strategy? They struck at $250 - a full 19% above current price and well above all resistance levels shown on the gamma chart. They're betting AMD breaks out of this consolidation range over the next 2 years and establishes a new trading range in the $250-300 zone as AI GPU deployments ramp.

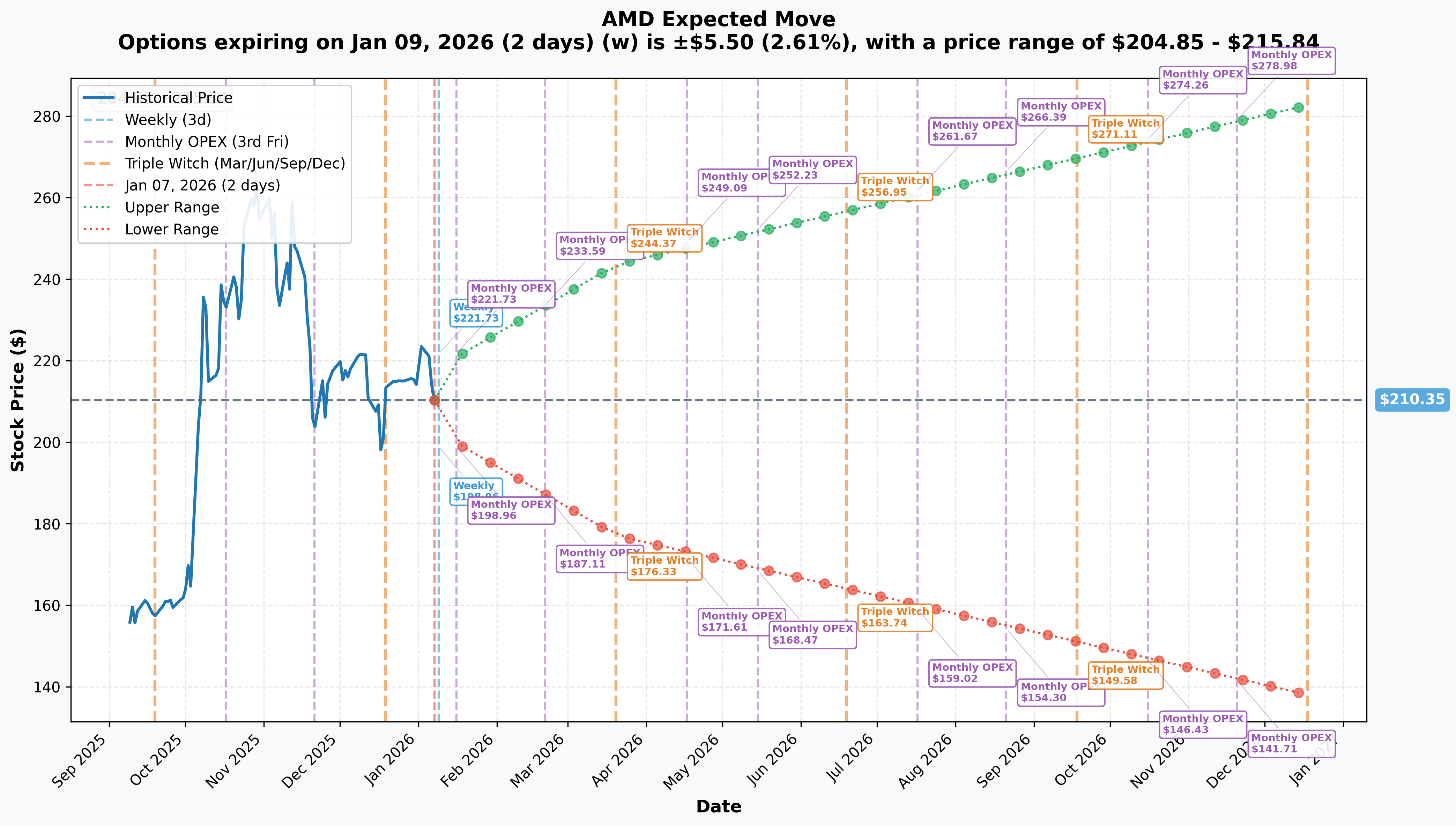

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 9 - 2 days): ±$5.50 (±2.61%) → Range: $204.85 - $215.84

- 📅 Monthly OPEX (Jan 16 - 9 days): ±$10.67 (±5.07%) → Range: $199.68 - $221.01

- 📅 Quarterly Triple Witch (Mar 20 - 72 days): ±$33.30 (±15.83%) → Range: $177.05 - $243.65

- 📅 Yearly LEAPS (Dec 18 - 345 days): ±$72.36 (±34.4%) → Range: $137.99 - $282.70

Translation for regular folks:

Options traders are pricing in a quiet 2.6% move ($5.50) over the next week, but a much larger 5% move through monthly OPEX on January 16. The real action starts with the quarterly expiration showing a 15.8% implied move, reflecting uncertainty around Q4 earnings on February 3 and MI400 deployment updates.

The LEAPS expiration shows a massive 34.4% implied range ($137.99 - $282.70), meaning the market sees significant two-way risk over the next year. However, notice that even the lower bound of $137.99 is still BELOW the put seller's $250 strike minus the $80 premium collected (effective cost basis of $170). This trade is positioned for worst-case scenarios while betting on best-case outcomes.

Key insight: The widening implied moves from 2.6% (weekly) to 34.4% (yearly) reflect massive uncertainty about AI chip market dynamics, competitive positioning vs Nvidia, and execution on the OpenAI partnership. The put seller is essentially betting they can predict the longer-term trend (up) better than the market can price near-term volatility.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Q4 2025 Earnings Release - February 3, 20264

AMD reports fiscal Q4 2025 results on Tuesday, February 3, 2026 after market close. This is the critical catalyst that will either validate or challenge the recent pullback. Wall Street consensus and key expectations:

- 📊 Revenue: ~$9.6B (+/- $300M), representing ~25% YoY growth5

- 💰 EPS: $1.31 consensus4

- 🤖 Data Center Segment: Expected ~$4.5-5B, watching for MI350 volume shipment commentary

- 📈 Q1 2026 Guidance: Critical for validating $44.6B full-year 2026 revenue target (31% growth)6

Key metrics to watch:

- MI350 series GPU ramp status and customer adoption

- OpenAI deployment timeline updates (H2 2026 target)

- China export license application status (MI308 currently restricted)

- Gross margin trajectory toward 54%+ target

- Data center revenue growth acceleration

Upside surprise potential: If AMD reports strong MI350 adoption with major hyperscaler wins (Meta, Microsoft Azure) and provides confident Q1 guidance above $10B, stock could gap back toward $230-240 resistance levels.

Downside risk factors: Any delays in MI400 timeline, weak China revenue commentary, or conservative guidance citing competitive pressure from Nvidia's Rubin platform7 could trigger another leg down toward $190-200 support.

🚀 Near-Term Catalysts (Q1-Q2 2026)

MI400 Series Volume Production Ramp (Throughout 2026)89

AMD's next-generation Instinct MI400 series represents the company's most ambitious AI accelerator lineup:

- 🖥️ MI455X flagship: 432GB HBM4 memory, 20 petaflops FP8 performance, 19.6Tbps bandwidth

- 🏢 MI440X enterprise: On-premise deployments for corporate data centers

- 🔬 MI430X: HPC and scientific computing workloads

- 💪 Key capability: Designed for trillion-parameter model training

- 🎯 Competitive positioning: Targeting Nvidia's Blackwell/Rubin platforms with superior memory capacity

Why this matters: Volume production beginning in 2026 is critical for AMD to prove they can compete at scale. The MI400 needs to deliver on the claimed 10x performance improvement vs MI355X and win major customer deployments to justify current valuation and this put seller's $250 strike conviction.

Helios Platform General Availability (Q3 2026)10

AMD unveiled the revolutionary Helios rack-scale platform at CES 2026:

- 🏭 Massive scale: 72 MI455X accelerators per double-wide rack configuration

- 💾 Unprecedented capacity: 31TB HBM4 memory, 4,600 CPU cores

- 🚀 Performance target: Up to 3 AI exaflops per rack

- ⚖️ Competitive necessity: Directly competes with Nvidia's NVL72 Rubin system

Critical timing: Q3 2026 general availability puts AMD on track to fulfill OpenAI deployment commitments and compete for hyperscaler refreshes in H2 2026. Any delays would significantly damage the bull thesis.

OpenAI First 1-Gigawatt Deployment (H2 2026)1112

The game-changing catalyst for AMD's long-term trajectory:

- 🤝 Partnership scope: 6-gigawatt total deployment over multiple years

- 🏭 First milestone: 1-GW deployment of MI450 series begins H2 2026

- 💰 Revenue magnitude: Expected to generate tens of billions annually; $100B+ over 4 years13

- 📈 Warrant structure: OpenAI receives up to 10% stake with final vesting at $600/share14

- ✅ Validation effect: Proves AMD is a credible Nvidia alternative at hyperscale

Why the put seller cares: This deployment beginning in H2 2026 (within the LEAPS timeframe) represents the ultimate validation of AMD's AI strategy. If successful, it unlocks multiple follow-on deployments from other hyperscalers and validates the $250+ stock price thesis through 2028.

📊 Medium-Term Catalysts (H2 2026 - 2027)

China Export License Resolution1516

AMD took an $800M inventory charge in Q2 2025 related to MI308 export restrictions:

- 📝 Current status: License application "in progress" per CEO Lisa Su

- ⏰ Timeline: Resolution could take "a few quarters"

- 💰 Upside potential: $1.5B-$1.8B annual revenue if approved

- 🚨 Downside risk: Permanent loss of China market share to domestic competitors

Impact on put position: License approval would be a significant catalyst supporting higher stock prices. Denial would create near-term weakness but likely wouldn't threaten the $250 strike given the 2-year timeframe and diversified revenue from US/EU sovereign AI projects.

Oracle MI450 Deployment (Beginning 2026)17

Oracle announced plans to deploy 50,000 AMD Instinct MI450 chips in its cloud infrastructure:

- 🏢 Customer validation: Major hyperscaler choosing AMD over Nvidia for massive deployment

- 📈 Revenue contribution: Multi-hundred million dollar contract

- 🎯 Competitive proof point: Demonstrates AMD's ecosystem maturity and TCO advantage

MI500 Series Preview (2027)18

AMD previewed the MI500 series at CES 2026 with jaw-dropping claims:

- 🚀 Performance leap: Claimed 1,000x performance improvement vs MI300X

- 🔬 Future positioning: Maintains AMD's roadmap leadership through 2027

- ⚠️ Execution risk: Aggressive timeline and performance targets create credibility challenges

Relevance to 2028 put: The MI500 preview shows AMD's long-term commitment to AI leadership, but the 2027 timeline means it's less relevant to the January 2028 expiration. The trade hinges more on MI400/MI450 execution in 2026.

⚠️ Risk Catalysts (Negative)

Nvidia Competitive Pressure Intensifies719

Nvidia maintains overwhelming market dominance and continues to innovate:

- 📊 Market share: Nvidia still commands 80-92% of data center GPU market20

- 🏭 Rubin platform: Full production availability H2 2026 with claimed 10x inference token cost reduction21

- 💰 OpenAI relationship: Nvidia announced $100B investment in OpenAI (vs AMD's equity-based deal)14

- 🔒 CUDA moat: Ecosystem lock-in remains AMD's biggest challenge despite ROCm improvements

Why this matters: If Nvidia's Rubin platform significantly outperforms MI400 or if hyperscalers delay AMD deployments to wait for Nvidia, AMD's market share gains could stall, threatening the $250 long-term price target.

Broadcom Custom ASIC Competition22

Broadcom's custom chip strategy is fragmenting the AI accelerator market:

- 🎯 Customer wins: Google TPU and Meta custom chip partnerships

- 💰 Anthropic orders: $21B in custom ASIC orders announced22

- 💸 TCO advantage: Lower total cost of ownership vs standard GPUs for specific workloads

Impact: Broadcom's success reduces the total addressable market for AMD's standard GPUs, potentially capping upside even if execution is flawless.

Valuation Compressed at 109 P/E23

At current prices, AMD trades at elevated multiples reflecting aggressive growth expectations:

- 📊 P/E ratio: 109.2623 vs historical 25-35x range

- 🎯 Embedded expectations: Market pricing 60%+ data center CAGR, 40% AI revenue mix by 2027

- ⚠️ Limited cushion: Any execution miss or guidance disappointment could trigger 20-30% correction

- 📉 Multiple compression risk: Even with good growth, PE reversion toward 60-70x would imply $150-180 price

Put seller perspective: The elevated valuation is actually GOOD for this trade - high IV means they collected massive $80.22 premium per contract. If valuation normalizes but fundamentals remain solid, stock could trade $180-220 range and puts still expire worthless.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst analysis, here are the scenarios through January 2028 expiration:

📈 Bull Case (35% probability)

Target: $280-$350

How we get there:

- 🚀 OpenAI deployment flawless: First 1-GW deployment in H2 2026 exceeds performance expectations, leading to accelerated 2-GW and 3-GW phases

- 💪 MI400/Helios dominance: AMD wins 15-20% data center GPU market share by 2027, up from current <10%20

- 📊 Revenue explosion: Data center segment reaches $22.9B in 2026 and $33.9B in 202724, validating >60% CAGR targets

- 🇨🇳 China resolution positive: MI308 export licenses approved, adding $1.5-1.8B annual revenue

- 🏆 Market share inflection: Meta, Microsoft Azure, Google announce major MI400 deployments beyond OpenAI

- 📈 Margin expansion: Gross margins reach 55%+ as AMD proves pricing power vs Nvidia

- ✅ Analyst upgrades cascade: Street raises targets to $350-380 range as AI revenue visibility improves

Key milestones needed:

- Q4 2025 earnings beat with confident Q1 2026 guidance

- MI400 production volumes meet or exceed plan throughout 2026

- OpenAI H2 2026 deployment begins on schedule

- At least 2-3 additional hyperscaler wins announced by mid-2026

Breakout levels: Stock needs to reclaim $230 resistance (Mar 2026 timeframe), then break through old highs at $267 (Q3 2026), establishing new trading range $280-320 by late 2026 and potentially reaching $350 by 2027 if all cylinders fire.

Why 35% probability: Requires very strong execution across multiple fronts, but the catalyst pipeline (OpenAI, MI400, Oracle, sovereign AI) is real and well-timed. AMD has proven ability to execute on product roadmaps. The 77% rally in 2025 shows market will reward success. Main risks are Nvidia competitive response and macro conditions.

Put seller outcome: Massive win - collects full $8M premium, puts expire worthless, potentially sells more puts at $300-350 strikes to repeat the strategy.

🎯 Base Case (45% probability)

Target: $220-$270 range (CHOPPY BUT ELEVATED)

Most likely scenario:

- ✅ Solid execution, not spectacular: MI400 ramps on schedule but adoption steady rather than explosive

- 📱 OpenAI deployment proceeds: H2 2026 milestone hit but no major acceleration announced

- ⚖️ Market share grind: AMD reaches 12-15% data center GPU share by 2027, up from <10% but not the 20%+ bulls hope for

- 🇨🇳 China status quo: Export licenses remain in limbo, excluding this revenue from forecasts

- 🤖 Revenue growth solid: Data center reaches $20-22B in 2026, $28-32B in 2027 (good but below Street's most optimistic targets)

- 💰 Valuation normalizes: PE compresses from 109x toward 70-80x on 2027 estimates as growth moderates

- 🔄 Trading range establishes: Stock consolidates $220-270 as market balances strong fundamentals against Nvidia's maintained dominance

- 📊 Quarterly volatility: Earnings create 10-15% swings but stock maintains elevated plateau

Why this is the most probable path:

AMD's fundamentals are genuinely strong - Financial Analyst Day targets of >35% revenue CAGR and >35% operating margins25 are achievable even without "beating" Nvidia. The $400B AI accelerator TAM by 2027 provides room for multiple winners. However, Nvidia's ecosystem advantages and Broadcom's custom ASICs prevent AMD from capturing the massive 30-40% market share needed to justify $300+ sustained prices.

What happens to stock price: After Q4 earnings (Feb 3), stock rallies to $230-240 on solid results and guidance. Throughout 2026, trades $220-260 range with volatility around product launches and competitive announcements. By late 2026/early 2027, establishes new "fair value" range $240-270 as AI GPU revenue ramp becomes clear but not transformational. Occasional dips to $220 support on macro selloffs, occasional pops to $270 on positive catalysts.

Put seller outcome: Strong win - stock stays comfortably above $250 for majority of the 2-year period. Even if there are temporary dips to $220-240, the puts are out-of-the-money at expiration in Jan 2028, allowing them to keep the full $8M premium. This is exactly what the trade is designed for.

Why 45% probability: Balances AMD's proven execution (product roadmaps, share gains vs Intel) against the reality of competing with Nvidia's massive moat. Most institutional analysts have $250-280 price targets for 12-18 month horizon, aligning with this scenario.

📉 Bear Case (20% probability)

Target: $150-$200 (PUTS THREATENED)

What could go wrong:

- 😰 MI400/Helios delays or underperformance: Production issues, performance below claims, or ROCm software gaps limit customer adoption

- 🚨 OpenAI deployment delayed or scaled back: Technical issues, cost overruns, or OpenAI shifts strategy toward Nvidia/custom silicon

- 💔 Major hyperscaler defection: Meta or Microsoft announce reducing AMD deployments in favor of Nvidia Rubin or Broadcom custom ASICs

- 🇨🇳 China export licenses permanently denied: Loss of $1.5-1.8B revenue opportunity, market share captured by Huawei/Biren

- 📉 Nvidia widens gap: Rubin platform delivers 15-20x performance advantages, making AMD's value proposition obsolete for frontier model training

- 💸 Macro recession: 2026-2027 economic downturn cuts enterprise IT budgets, delaying datacenter refresh cycles

- 📊 Revenue growth disappoints: Data center reaches only $16-18B in 2026 (vs $22B+ targets), missing the >60% CAGR commitment

- 💰 Margin compression: Forced to cut prices aggressively to win share, gross margins fall to 48-50% range

- 🔨 Valuation resets violently: PE compresses from 109x to 40-50x on slower growth, implying $120-180 price range

- ⚠️ Multiple negative catalysts align: 2-3 of above scenarios occur simultaneously

Critical support levels:

- 🛡️ $200: Major gamma and psychological support - MUST HOLD or sentiment shifts bearish

- 🛡️ $180: Extended support from yearly implied move lower bound - heavy technical damage if broken

- 🛡️ $150: Disaster scenario floor - would imply complete AI strategy failure

How low could it go: In a true bear case with multiple execution failures and macro headwinds, stock could revisit $150-170 range (where it traded in early 2025 before OpenAI partnership). This would represent a 28-35% decline from current $210 levels.

Path there: Q4 earnings disappoint (Feb 3) with weak Q1 guidance, stock gaps down to $190. MI400 production delays announced in Q2 2026, drops to $170. OpenAI pushes out deployment timeline in Q3, falls to $155. Macro recession fears in late 2026 drive final leg down to $150 lows by early 2027.

Put seller outcomes in Bear Case:

- 📍 Stock at $200 in Jan 2028: Puts worth $50, showing $50K loss vs $80.22 premium received. Net profit still $30.22 per contract × 1,000 = $3M profit (38% ROI)

- 📍 Stock at $180 in Jan 2028: Puts worth $70, loss $70K vs $80.22 premium. Net profit $10.22 × 1,000 = $1M profit (13% ROI)

- 📍 Stock at $150 in Jan 2028: Puts worth $100, loss $100K vs $80.22 premium. Net loss -$19.78 × 1,000 = -$2M loss (-25% ROI)

- 📍 Stock below $170 in Jan 2028: This is the breakeven ($250 strike - $80 premium = $170). Below this, trade loses money.

Why only 20% probability: Requires multiple major negative catalysts to align over 2 years. AMD's product roadmap is solid, financial position is strong ($7.4B cash), and management has track record of execution under CEO Lisa Su. Even in scenarios where they don't "win" against Nvidia, the company remains highly profitable and growing. The $150-170 downside requires assuming complete AI strategy failure, which contradicts the Oracle 50,000 chip order and OpenAI partnership already secured.

Also, put seller has significant cushion - breakeven is $170 (19% below current price). Stock would need to fall AND stay down through Jan 2028 for trade to lose meaningful money.

💡 Trading Ideas

🛡️ Conservative: Wait for Earnings Clarity, Then Reassess

Play: Stay in cash until after February 3 earnings, then evaluate entry points based on Q1 guidance and MI400 commentary

Why this works:

- ⏰ Catalyst imminent: Q4 earnings on Feb 3 (27 days away) is a binary event that could move stock 10-15% either direction

- 💸 IV elevated: Implied volatility reflecting earnings uncertainty - better to wait for IV crush and clearer direction

- 📊 Consolidation range: Stock in $200-220 range with no urgency to chase - better entries likely post-earnings

- 🎯 Defined trigger points: Can create a shopping list based on earnings outcomes

- 🤔 Let the whale do the heavy lifting: The $8M put seller clearly has 2-year conviction, but you don't need to match their risk horizon

Action plan after Feb 3 earnings:

- ✅ If earnings beat + strong guidance: Look for pullback to $220-225 support (gamma resistance levels) for stock entry with stop loss at $210

- ⚖️ If earnings in-line: Wait for $205-210 retest to enter long stock or sell cash-secured puts at $200 strike (March/April expiration)

- 📉 If earnings disappoint: Let stock find bottom at $190-200, then evaluate if fundamental thesis remains intact before entering

- 👀 Watch for: MI400 production timeline updates, OpenAI deployment confirmation, China export license status

Position sizing: Start with 2-3% portfolio allocation if entering stock, scale up to 5-7% on proven execution

Risk level: Minimal (cash position preserves optionality) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 10-15% drawdown if earnings disappoint. Get better entry with defined catalyst visibility if earnings positive. Maintain flexibility.

⚖️ Balanced: Mimic the Whale with Smaller Put Sales (After Earnings)

Play: After Feb 3 earnings, sell cash-secured puts at $200 or $210 strikes, collecting premium while expressing bullish bias

Why this works:

- 🎢 IV crush post-earnings: Volatility will collapse after earnings, but puts will still pay decent premium given 2+ year time horizon

- 📊 Strong gamma support: $200 and $210 are major support levels with high options activity

- 🤝 Copying institutional logic: Mimicking the whale's strategy (sell puts, collect premium, willing to own at lower basis) at your scale

- ⏰ Flexibility: Can use shorter expirations (June/Sep 2026) vs whale's Jan 2028, reducing capital commitment

- 🛡️ Downside protection: Premium collected reduces your effective cost basis if assigned

- 💰 Multiple ways to win: Keep premium if stock stays flat/up, or get assigned at attractive basis if stock drops

Recommended structure (execute AFTER Feb 3 earnings):

- 📅 Expiration: June 2026 or September 2026 (gives 5-8 months vs whale's 24 months)

- 🎯 Strike selection: $200 puts if conservative (5% below current), $210 puts if confident (at current support)

- 💵 Expected premium: Approximately $15-25 per contract for June, $25-40 for September (adjust based on actual post-earnings IV)

- 📊 Position sizing: Sell 1 contract per $20,000 cash you're willing to commit (each put = obligation to buy 100 shares)

Estimated P&L for $200 strike June 2026 puts:

- 💰 Premium collected: ~$20/contract = $2,000 per contract

- 📈 Max profit: Keep full $2,000 if AMD above $200 at June expiration (80%+ probability based on support levels)

- 📉 Breakeven: $180 effective cost ($200 strike - $20 premium)

- ⚠️ Assignment scenario: If AMD at $185 in June, you buy 100 shares at $200 but received $20 premium = $180 basis (14% below current $210)

Why wait until after earnings:

- IV crush makes puts cheaper to sell (you collect less premium but have less risk)

- Fundamental clarity on MI400 roadmap and Q1 guidance de-risks the position

- Can adjust strikes based on where stock settles post-earnings

Risk management:

- Don't sell more puts than cash you have to cover assignment

- Use ~25% of available cash maximum (sell 1 put per $20K for $200 strike)

- Consider rolling puts out and down if stock drops below strike before expiration

- Set alerts if stock breaks $195 support to reassess

Risk level: Moderate (obligation to buy stock if assigned, but at favorable basis) | Skill level: Intermediate

Expected outcome: 70% probability of keeping full premium with no assignment. 25% probability of assignment at attractive entry price. 5% probability of getting assigned in a true bear market scenario but with premium cushion.

🚀 Aggressive: Leveraged Bull Spread Betting on $250+ by End of 2026 (ADVANCED)

Play: Buy call spreads betting AMD reclaims $250+ by December 2026, aligning with whale's conviction

Structure: Buy $240 calls, Sell $270 calls, December 2026 expiration

Why this could work:

- 💥 Defined risk leverage: Spend $15-20 per spread to control $30 of upside (2:1 reward/risk)

- 🎯 Aligns with whale thesis: Betting on same $250+ price target over similar timeframe (Dec 2026 vs Jan 2028)

- 📊 Multiple catalysts: Captures Q4 earnings, MI400 ramp, Oracle deployment, OpenAI updates over 11-month period

- 🚀 Asymmetric payoff: If AMD breakout occurs (bull case), spread maxes out at $30 value for 100-150% gain

- ⏰ Time to work: 11 months gives trade room to develop, not betting on immediate move

- 📈 Breakout probability: If stock reclaims $230 by Q2 and confirms uptrend, $250-270 by year-end becomes realistic

Estimated structure (enter AFTER Feb 3 earnings clarity):

- 🟢 Long leg: Buy Dec 2026 $240 calls @ ~$35-40

- 🔴 Short leg: Sell Dec 2026 $270 calls @ ~$20-25

- 💵 Net debit: $15-20 per spread (your max risk)

- 📊 Max profit: $30 - $15 = $15/spread (if AMD above $270) = 100% ROI

- 🎯 Breakeven: $255 (well above current $210 but aligned with bull case)

P&L scenarios at December 2026 expiration:

- 🚀 AMD at $280+: Spread worth $30, profit $15 per spread (100% ROI)

- 📈 AMD at $260: Spread worth $20, profit $5 per spread (33% ROI)

- 📊 AMD at $240: Spread worth $0-5, loss of $10-15 per spread (50-100% loss)

- 📉 AMD below $230: Spread worthless, lose entire $15-20 debit (100% loss)

Why this is AGGRESSIVE and RISKY:

- ⚠️ Needs 20% rally: From $210 current to $255 breakeven requires significant bullish momentum

- 💸 High probability of loss: If base case ($220-240 range) plays out, you lose most/all of debit

- ⏰ Time decay enemy: Every month closer to expiration erodes value if stock doesn't move up

- 🎢 Volatility crush: Post-earnings IV drop will immediately reduce spread value 20-30%

- 📊 All-or-nothing: Unlike stock ownership, spreads can expire worthless with total loss

CRITICAL REQUIREMENTS - DO NOT attempt unless:

- ✅ You fully understand call spreads and have traded them before

- ✅ Can afford to lose 100% of capital allocated (serious possibility!)

- ✅ Believe bull case (35% probability) is actually 50%+ likely

- ✅ Plan to actively manage - take profits at 50-75% max gain, don't hold to expiration

- ✅ Will cut losses if stock breaks below $200 support (don't hope and pray)

- ⏰ Comfortable with illiquid December 2026 LEAPS (wide bid-ask spreads)

Entry timing:

- Wait until after Feb 3 earnings

- Only enter if stock holds $200+ and shows technical strength

- Look for confirmation above $220 before committing

- Consider scaling in 1/3 at a time if unsure

Position sizing: Risk only 5-10% of options portfolio on this trade (it's speculative directional bet, not core holding)

Risk level: HIGH (can lose 100% of premium, requires major bullish move) | Skill level: Advanced only

Probability of profit: ~35-40% (aligned with bull case probability, slightly higher than base case would suggest)

Why trade this vs just selling puts like the whale? You have smaller capital base and want leveraged upside participation. The whale can commit $25M to sell 1,000 puts; you probably can't. Call spreads give retail traders asymmetric upside exposure for defined risk. But understand you're fighting lower probability (40% vs whale's 80%) in exchange for higher potential ROI (100% vs their 50% annualized).

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q4 earnings binary event (Feb 3): Results after close could gap stock 10-15% either direction based on revenue quality ($9.6B guidance vs actual), MI400 production status, Q1 2026 guidance, and China export commentary. Options market pricing ±5% monthly move but actual volatility could exceed this given elevated expectations. Historical precedent shows AMD gaps 8-12% on earnings even when meeting consensus if guidance disappoints.

-

💸 Stretched valuation at 109x P/E: Trading at 109.26 P/E vs historical 25-35x average23 near recent highs after 77% 2025 gain. Stock is priced for near-perfect execution - requires 60%+ data center CAGR through 2027 and 40% of revenue from AI products to justify current multiple. Any disappointment in MI400 adoption, OpenAI timeline, or competitive positioning could trigger 20-30% multiple compression even if fundamentals remain "good." Zero margin of safety at current prices.

-

🚨 OpenAI deployment execution risk: First 1-GW deployment must begin H2 2026 to maintain credibility and unlock warrant tranches. Any delays due to MI450 production issues, power/cooling constraints at OpenAI facilities, or performance below expectations would severely damage bull thesis. OpenAI could also pivot strategy toward Nvidia or custom silicon if AMD underdelivers. This is a "bet the company" partnership that creates massive binary risk.

-

⚖️ Nvidia maintains crushing dominance: Despite AMD's progress, Nvidia still commands 80-92% data center GPU market share20 with the CUDA ecosystem creating powerful lock-in. Nvidia's Rubin platform launches H2 2026 with claimed 10x inference cost reduction21, potentially widening the performance gap just as AMD ramps MI400. Large enterprises are reluctant to switch AI infrastructure mid-deployment due to training costs and ecosystem dependencies. AMD might win 15-20% share but struggle to exceed that, capping long-term upside.

-

🏭 MI400/Helios production execution risk: AMD pulled forward MI350 and now MI400 timelines to improve competitive position. Compressed development schedules increase risk of delays, bugs, or performance shortfalls. The Helios platform with 72-GPU scale-out is unproven - any yield issues or interconnect problems could limit volume production in Q3 2026. Competing for same TSMC 3nm capacity as Apple and Nvidia creates supply constraints. Claimed 10x performance vs MI355X needs real-world validation across diverse workloads.

-

🇨🇳 China export restriction overhang: AMD took $800M charge in Q2 2025 from MI308 restrictions. License application remains "in progress" with resolution timeline of "a few quarters"16. Permanent denial would eliminate $1.5-1.8B annual revenue opportunity and cede market share to Huawei/Biren domestic alternatives. Even if approved, future export controls on MI400/MI500 could hit without warning given deteriorating US-China relations and 245% tariffs on Chinese goods. This represents 15-20% revenue wildcard that could swing either way.

-

💰 Broadcom custom ASIC fragmentation: Broadcom's custom chip strategy winning major hyperscaler contracts including $21B from Anthropic22. Google TPU and Meta custom designs reduce addressable market for AMD's standard GPUs. As AI models mature and workloads become more predictable, hyperscalers increasingly favor application-specific chips with better TCO. This structural shift could cap AMD's potential market share at 15-20% even with flawless execution, limiting upside to $250-280 vs the $350+ bull case.

-

📉 Macro recession scenario: At 109x P/E, AMD has zero recession protection. Fed Chairman Powell comments on potential 2026 economic slowdown raise concerns. If economy weakens in 2026-2027, enterprise IT budgets get cut first, delaying datacenter GPU refresh cycles by 12-18 months. Even if AMD's products are superior, customers will postpone purchases, crushing revenue growth. Historical precedent: semiconductor stocks drop 40-50% in recessions regardless of market position.

-

🎢 Extreme two-year volatility risk: The $72 implied move (34.4%) for yearly LEAPS reflects massive uncertainty. Stock could trade anywhere from $138 to $283 over next 12 months based on options pricing. Recent 3-month pullback from $264 to $210 (-20%) shows how quickly sentiment can shift. For a 2-year position, expect multiple 15-25% drawdowns along the way even if long-term thesis proves correct. Weak hands will get shaken out.

-

🐋 Institutional positioning unclear: While this $8M put sale is bullish, we don't have visibility into the seller's full portfolio. They might be hedging a massive long stock position, running complex arbitrage, or expressing a view on IV rather than directional conviction. Retail traders shouldn't blindly follow institutional trades without understanding the complete strategy. Additionally, institutional ownership concentrated in top holders (Vanguard 8.2%, State Street 4.7%)26 means large redemptions could drive technical selling unrelated to fundamentals.

-

⚠️ Margin call risk for put sellers: If you follow the whale's strategy and sell cash-secured puts, understand that brokers require cash collateral. If you sell 10 contracts at $200 strike, you need $200,000 in cash locked up for months or years. This creates opportunity cost and capital inefficiency. If AMD crashes and you get assigned at $200 while stock trades at $150, you're sitting on a -$50K unrealized loss and your capital is tied up. Make sure you have sufficient liquidity and won't need that capital for other opportunities.

🎯 The Bottom Line

Real talk: Someone just collected $8 MILLION selling long-dated puts on AMD, expressing massive conviction that the stock stays above $250 (19% higher than current price) through January 2028. This isn't a bearish hedge - this is a bullish whale selling insurance at premium prices and betting AMD's AI revolution keeps the stock elevated for years.

What this trade tells us:

- 🎯 Long-term bull thesis: Sophisticated player believes the OpenAI 6-GW partnership, MI400/MI500 roadmap, and AI market share gains justify $250+ valuations through 2028

- 💰 Massive premium collection: $80.22 per contract (38% of current stock price) reflects elevated IV and 2-year time premium - they're getting paid handsomely for this conviction

- ⚖️ Downside cushion: Breakeven at $170 (19% below current $210) means they can withstand significant volatility and still profit

- 📊 Strategic timing: January 2028 expiration captures all major catalysts (Q4 earnings, MI400 ramp, OpenAI deployment H2 2026, MI500 preview) with maximum time decay in their favor

- ⏰ Willingness to own: If assigned, they're buying 100,000 shares at effective $170 basis - they genuinely want AMD exposure at those levels

This is NOT a "buy everything now" signal - it's a "2-year strategic positioning" signal that requires patience and risk management.

If you own AMD:

- ✅ Hold through Feb 3 earnings if you have conviction in MI400 story and can handle 10-15% volatility

- 📊 Set mental stops at $195-200 (major gamma support) to protect against bear case breakdown

- ⏰ Don't chase here at $210 - wait for either earnings confirmation or pullback to $200 support for adding

- 🎯 Take partial profits if stock rallies back to $230-240 (old resistance), lock in gains from wherever you entered

- 🛡️ Consider selling covered calls at $230-240 strikes if you want to generate income while holding

If you're watching from sidelines:

- ⏰ Wait for Feb 3 earnings clarity - this is only 27 days away and will define the next 6-month direction

- 🎯 Target entry at $200-210 if earnings confirm strong MI400 trajectory and Q1 guidance

- 📈 Looking for confirmation: Revenue beat, 60%+ data center CAGR visibility, OpenAI deployment on track, gross margins 54%+

- 🚀 Bull case requires: MI400 production volumes meet plan, at least 2-3 hyperscaler wins beyond OpenAI/Oracle, market share reaching 15%+ by 2027

- ⚠️ Bear case triggers: MI400 delays, OpenAI pushes out timeline, Nvidia Rubin dominates, China licenses denied permanently

If you're considering the put-selling strategy:

- 🎯 Wait until after earnings for IV crush and fundamental clarity

- 📊 Start with 1-2 contracts at $200 strike (June or Sept 2026 expiration) to test the waters

- ⚠️ Only commit cash you're willing to tie up for 6-12 months and can afford to use buying stock if assigned

- 📉 Understand assignment risk: If AMD crashes to $150, you'll own stock with $50/share unrealized loss

- ⏰ Plan to roll or close if stock approaches your strike 30-60 days before expiration

Mark your calendar - Key dates:

- 📅 February 3, 2026 - Q4 FY2025 earnings (THE catalyst for next 3-6 months)

- 📅 March 20, 2026 - Quarterly triple witch (15.8% implied move window)

- 📅 Q2-Q3 2026 - MI400 volume production ramp

- 📅 Q3 2026 - Helios platform general availability

- 📅 H2 2026 - OpenAI first 1-gigawatt MI450 deployment begins

- 📅 2027 - MI500 series launch, China export resolution likely

- 📅 January 21, 2028 - Expiration of this $8M put trade

Final verdict: AMD's 2-year setup is genuinely compelling - the OpenAI partnership worth $100B+ over 4 years, MI400/MI500 roadmap progression, Oracle's 50,000 chip order, and Financial Analyst Day targets of >35% revenue CAGR are all real catalysts. The put seller's $250 strike 19% above current price reflects informed optimism about execution over the next 24 months.

BUT - at 109x P/E after pulling back 20% from highs with Nvidia maintaining 80-92% market dominance and Broadcom fragmenting the market with custom ASICs, this is NOT a "buy blindly and hold" situation. The trade requires patience, waiting for Feb 3 earnings clarity, and accepting that the path to $250+ will include multiple 15-20% drawdowns along the way.

The whale can afford to wait 2 years and weather volatility. Can you? If yes, this pullback to $210 with strong catalysts ahead could be an opportunity. If you need shorter-term results or can't handle volatility, there are easier trades out there.

Be strategic. Be patient. Let earnings provide clarity. The AI revolution will still be here in a month. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Selling puts creates obligation to purchase stock at the strike price and requires sufficient capital to cover assignment. The 29.25x Z-score reflects this specific trade's statistical unusualness relative to recent AMD activity - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Q4 earnings on February 3 creates binary event risk with potential for 10-15% gaps either direction.

About Advanced Micro Devices: Advanced Micro Devices designs digital semiconductors for markets such as PCs, gaming consoles, data centers (including artificial intelligence), industrial, and automotive applications, with a market cap of $347.31 billion in the Semiconductors & Related Devices industry.