AMZN $4.7M Call Bet - Institutional Bull Positions for Earnings Breakout

January 29, 2026 | Unusual Activity Detected

The Quick Take

A trader just spent $4.7 MILLION on AMZN calls at 12:30:11 today! They bought 4,999 contracts of the $245 strike calls expiring February 27th - a direct bullish bet on Amazon pushing through resistance just 7 days before Q4 2025 earnings on February 5th. With AMZN up +8.8% YTD at ~$240 and the $245 strike sitting right at a gamma resistance level, this is a clear signal: someone expects earnings to launch the stock through $245 and toward $255+. Translation: Institutional money is betting big on an AMZN earnings beat and breakout!

Company Overview

Amazon.com Inc. (AMZN) is the world's leading e-commerce, cloud computing, and AI infrastructure company:

- Market Cap: $2,597.8 Billion (one of the largest companies on Earth)

- Industry: Retail-Catalog & Mail-Order Houses

- Current Price: ~$239.53 (trading 6% below Nov 2025 ATH of $254)

- Primary Business: E-commerce (~74% revenue), AWS cloud (~17%), Digital advertising (~9%)

The Option Flow Breakdown

The Tape (January 29, 2026 @ 12:30:11):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:30:11 | AMZN | MID | BUY | CALL $245 | 2026-02-27 | $4.7M | $245 | 6,200 | 4,000 | 4,999 | $240.05 | $9.50 |

What This Actually Means

This is a directional bullish bet targeting a move above $245 within 29 days. Here is the breakdown:

- Significant premium committed: $4.7M ($9.50 per contract x 4,999 contracts)

- Strike selection: $245 is 2.1% out-of-the-money from current price of ~$240 -- not deep OTM, showing confidence in a near-term move

- Opening position: Volume of 6,200 vs open interest of 4,000 confirms this is overwhelmingly NEW positioning, not closing an existing trade

- Break-even at expiration: $254.50 ($245 strike + $9.50 premium) -- needs a 6% move from current levels

- Earnings capture: Feb 27 expiration is 22 days AFTER Q4 earnings on Feb 5th -- this trade is built around the earnings catalyst

- Execution at mid-price: Filled between the bid and ask, suggesting a patient institutional buyer negotiating with market makers

What is really happening here: This trader is making a calculated bet that AMZN will beat Q4 2025 earnings expectations on February 5th and rally through the $245 gamma resistance level. The break-even of $254.50 is almost exactly at Amazon's November 2025 all-time high of $254, meaning the trader needs a retest of highs to profit. The monthly implied move upper bound of $257.70 puts this break-even well within the options market's expected range -- this is not an unreasonable bet.

Why $245 matters: The $245 strike sits exactly at a gamma resistance level. Market makers holding call positions at this strike will sell into rallies as price approaches $245, creating a natural ceiling. The buyer of this $4.7M position is betting that earnings momentum will be strong enough to bulldoze through that resistance. Once $245 breaks and holds, the next resistance levels at $250 and $255 become targets.

Technical Setup / Chart Check-Up

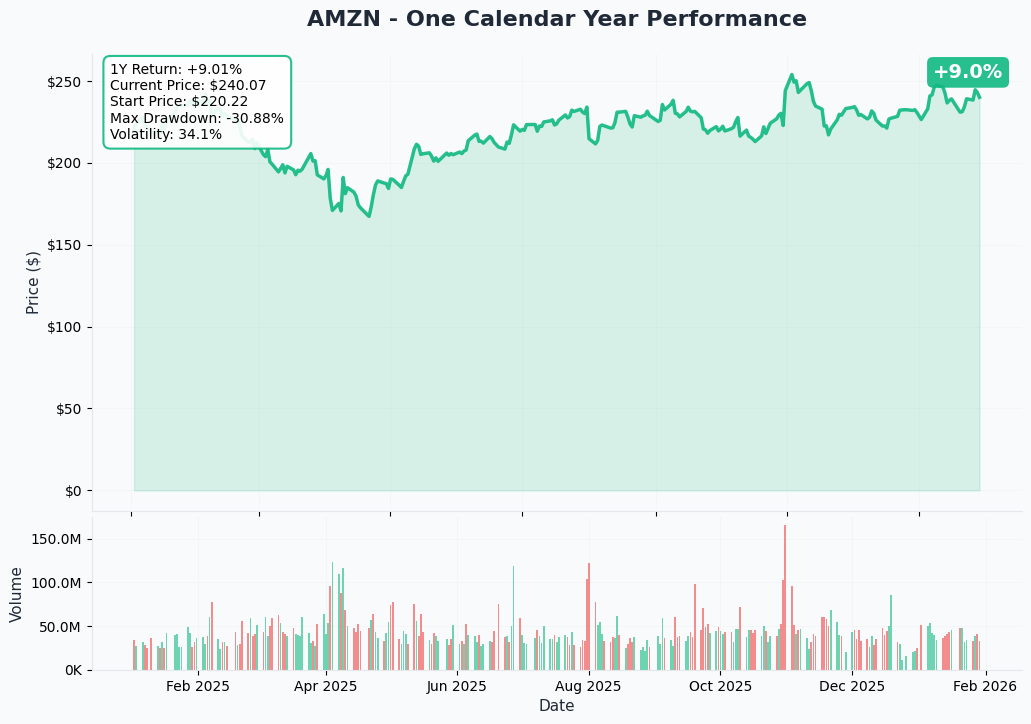

One Calendar Year Chart

AMZN is up +8.8% YTD with a current price of ~$239.53. The stock hit its all-time high of $254 in November 2025 following strong Q3 earnings and AWS re:Invent announcements, but has pulled back roughly 6% since then amid broader market rotation, "Project Dawn" layoff headlines, and concerns about the company's massive $125B capex plan for 2026.

Key observations:

- Pullback from highs: Trading $15 below the November ATH of $254, creating potential for a mean-reversion rally on positive earnings

- Consolidation range: Stock has been range-bound between $230-$245 through January, building a base

- Strong yearly context: Up 8.8% YTD despite negative headlines around layoffs and capex concerns

- Volume patterns: Institutional positioning has been active in the $235-$245 range ahead of earnings

- 52-week range: $161.38 to $258.60 shows the stock has already moved substantially from its lows

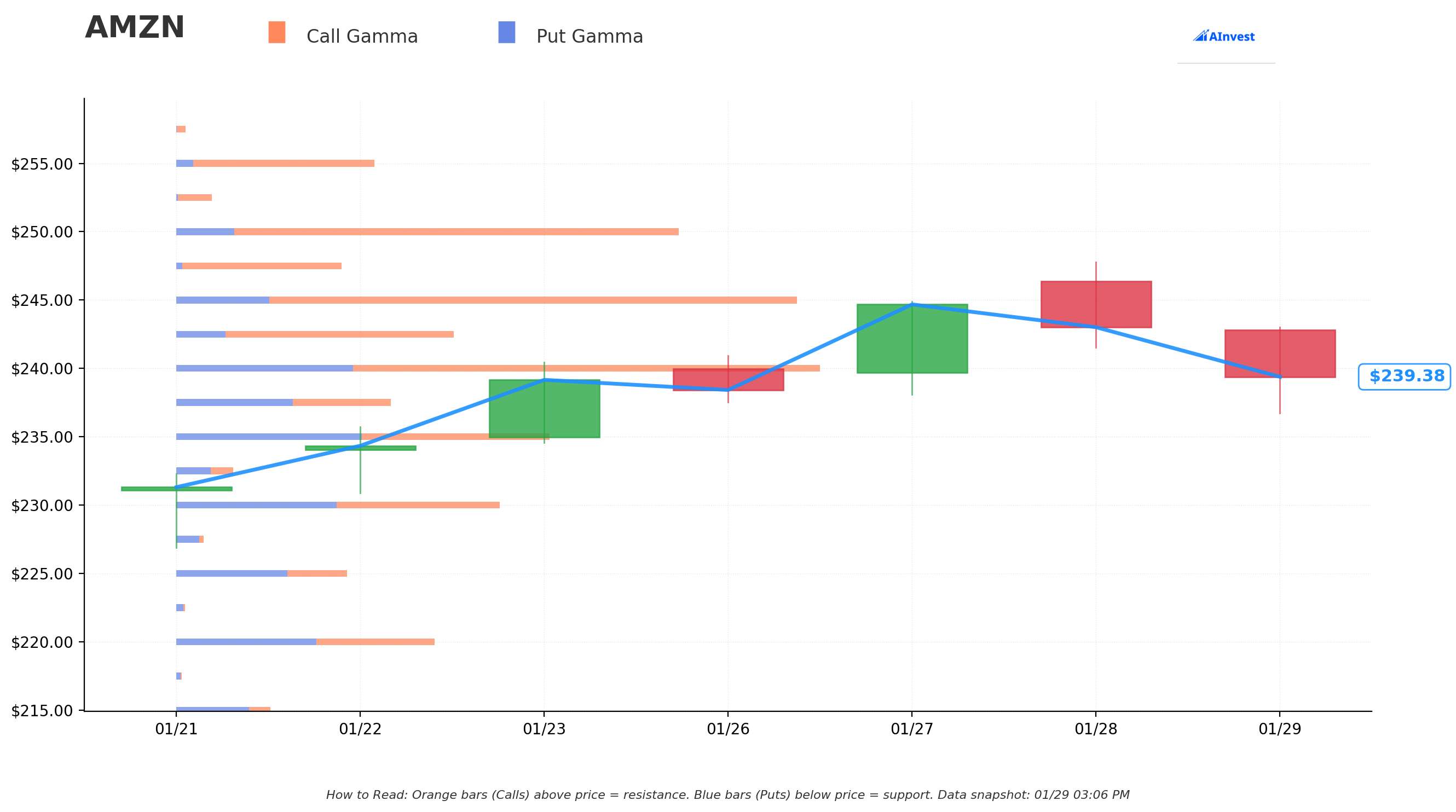

Gamma-Based Support & Resistance Analysis

Current Price: $239.49

The gamma exposure map reveals the key price levels that will govern near-term price action around earnings:

Support Levels (Below Price):

- $237.50 - Immediate support (first line of defense on any pullback)

- $235 - Secondary support (this is where dip-buyers have been active in January)

- $230 - Major structural floor (round number with significant put gamma -- a break below here shifts the entire narrative bearish)

- $220 - Deep support / disaster scenario level (16% below current price)

Resistance Levels (Above Price):

- $240 - Immediate overhead resistance (round number, stock has been struggling here)

- $242.50 - Near-term hurdle before the critical strike

- $245 - KEY LEVEL: This is exactly where the call buyer struck! Significant call gamma here creates natural selling pressure that needs to be overcome

- $250 - Major psychological barrier and round-number resistance

- $255 - Near the November ATH of $254 -- breakout above confirms new all-time high territory

- $260 - Extended upside target

What this means for traders: AMZN is trading just below the $240 round-number resistance with significant call gamma building at $245 and $250. The gamma setup creates a "coiled spring" scenario: if earnings provide enough momentum to push through $245, the forced dealer hedging (buying stock to cover short gamma) could accelerate the move toward $250-$255. However, if earnings disappoint, the $235 and $230 support levels become critical.

The $245 call buyer's thesis is clear: They believe earnings will provide the catalyst to break through the $240-$245 resistance zone. Once above $245, reduced overhead gamma and dealer hedging flows could create a quick move toward the $250-$255 range, where the trade becomes meaningfully profitable.

Net GEX Bias: Bullish -- overall call gamma exceeds put gamma, meaning market maker hedging flows favor upside moves.

Implied Move Analysis

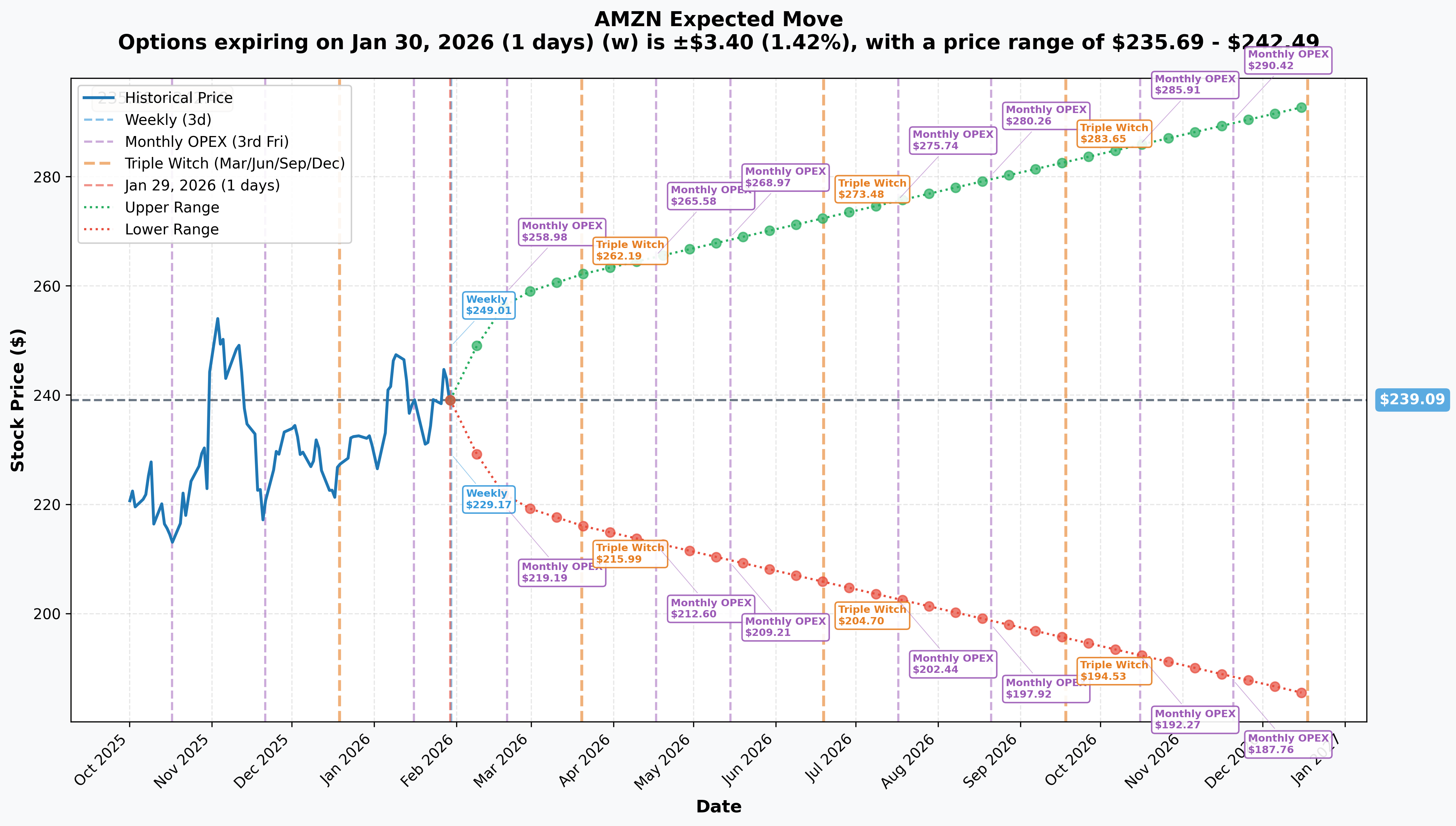

Options market pricing for upcoming expirations:

- Weekly (Jan 30 - 1 day): +/-1.4% (+/-$3.40) --> Range: $235.69 - $242.49

- Monthly OPEX (Feb 20 - 22 days): +/-7.8% (+/-$18.61) --> Range: $220.47 - $257.70

- Quarterly (Mar 20 - 50 days): +/-9.7% (+/-$23.10) --> Range: $215.99 - $262.19

Translation for regular folks: The options market is pricing in a modest 1.4% move by tomorrow, but a significant 7.8% move (+/-$18.61) through February OPEX -- which captures the February 5th earnings report. That means the market expects AMZN could trade anywhere from $220 to $258 over the next three weeks. For a $2.6 TRILLION company, that is a wide range and reflects genuine uncertainty around earnings quality and 2026 guidance.

How this relates to the trade: The call buyer's break-even of $254.50 sits WITHIN the monthly implied move upper range of $257.70. This means the options market itself is saying there is a reasonable probability AMZN reaches $254.50 by February OPEX. The trader is not making an outlandish bet -- they are positioning for the upper end of the expected range, which requires a strong earnings beat and positive guidance. The quarterly implied move to $262.19 on the upside shows that if the earnings catalyst hits, there is room to run well beyond the break-even.

Catalysts

Immediate Catalysts (Next 7 Days)

Q4 2025 Earnings - February 5, 2026 (7 DAYS AWAY!)

AMZN reports fiscal Q4 2025 results on Thursday, February 5, 2026 at 2:00 PM PT. This is THE catalyst this trade is built around. Wall Street consensus and key expectations:

- Revenue: $206B - $213B (+13% YoY) -- Q4 includes the massive holiday shopping season

- EPS: $1.97 (+5.9% YoY from $1.86) -- importantly, Amazon has beaten bottom-line estimates in each of the last 4 quarters

- Full-Year 2025 EPS: $7.17 (consensus, +29.7% YoY from $5.53)

- AWS Revenue: Re-acceleration is critical -- Q3 showed improved growth rates and the market wants to see this continue

- Advertising Revenue: Tracking at $65-70.8B full-year run rate after $17.7B (+24% YoY) in Q3

- 2026 Capex Guidance: $125B guided -- any upward revision could pressure the stock despite bullish fundamentals

Upside surprise potential: Bank of America named AMZN their top mega-cap pick with a $286 price target, citing AI deals, AWS growth, and Trainium chip adoption. Amazon's consistent beat history (4 straight quarters) and the compounding benefits from "Project Dawn" cost cuts could drive an upside surprise.

Downside risk factors: Free cash flow collapsed 69% to $14.8B TTM due to massive capex. Any hint that the $125B 2026 spend is growing further, or that AWS growth is decelerating, could trigger a selloff. The Project Dawn layoffs create negative sentiment even if they improve margins long-term.

Near-Term Catalysts (Q1 2026)

AWS re:Invent 2025 Momentum and Trainium3 Ramp

Amazon's December 2025 AWS re:Invent conference delivered a wave of product announcements that are just now translating into customer deployments:

- Trainium3 Chips: AWS's first 3nm AI chip; EC2 Trn3 UltraServers pack 144 chips with 4.4x more compute, 4x energy efficiency vs. Trainium2

- Amazon Nova AI Models: Nova 2 family launched including Nova 2 Sonic (speech-to-speech), Nova 2 Lite (reasoning), Nova 2 Omni (multimodal), Nova Forge (custom frontier models), and Nova Act (browser agent automation with 90%+ reliability)

- AWS AI Factories: Dedicated AI infrastructure for enterprise and government, combining NVIDIA GPUs, Trainium, and AWS services

- Key Customers: Anthropic, Karakuri, Metagenomi, Decart using Trainium; up to 50% cost reduction vs. GPUs

- Graviton5: Most powerful and efficient AWS CPU

Trainium3 customer deployments ramping through H1 2026 could re-accelerate AWS cloud growth to 20%+, which would be a significant re-rating catalyst.

Amazon Leo (Project Kuiper) Commercial Launch - Q1 2026

Amazon's satellite internet constellation is entering its commercial phase:

- Rebranded as "Amazon Leo" in November 2025 with 150+ satellites in orbit

- Commercial service launching in US, Canada, France, Germany, UK by end of Q1 2026

- Next launch: Ariane 64 on Feb 12, 2026, carrying 32 satellites

- FCC deadline: ~1,618 satellites must be operational by July 30, 2026 -- extremely ambitious with only ~150+ currently in orbit

- 92 rocket launches contracted from ULA, ArianeGroup, Blue Origin (>$10B total)

Project Dawn Cost Savings - Completion by May 2026

Amazon's massive restructuring will drive margin improvement:

- 16,000 workers laid off on Jan 28, 2026 across AWS, retail, Prime Video, and HR

- Broader restructuring targeting up to 30,000 corporate positions by May 2026

- 78% of eliminated roles were mid-level managers (L5-L7) -- this is about flattening the org, not desperation

- CEO Andy Jassy stated AI efficiency gains will cause corporate headcount to fall

- Short-term negative sentiment but could meaningfully boost operating margins in Q1-Q2 2026

Medium-Term Catalysts (Q2-Q3 2026)

Advertising Acceleration

Amazon's advertising business continues to be an underappreciated profit engine:

- Ad revenue grew 24% to $17.7B in Q3 2025, third consecutive quarter of accelerating growth

- Projected $65-70.8B for full-year 2025

- Expanding into Prime Video, Twitch, live sports, and third-party partnerships

- Third-largest U.S. digital ad platform, growing faster than the overall market

India Expansion

- $35B investment by 2030 in AI, data centers, and infrastructure in India -- massive long-term growth runway

Analyst Sentiment

Wall Street is overwhelmingly bullish on AMZN:

| Firm | Rating | Price Target | Date |

|---|---|---|---|

| Bank of America | Top Pick | $286 | Jan 27, 2026 |

| Wells Fargo | Overweight | $295 | Jan 2026 |

| Oppenheimer | Outperform | $305 | Jan 2026 |

| KeyBanc | Overweight | $308 | Jan 2026 |

- Consensus: 57 analysts: 49 Strong Buy, 5 Moderate Buy, 3 Hold

- Average Price Target: $285 - $294 (+19-23% upside from current price)

- Price Target Range: $195 - $340

Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through the February 27th expiration:

Bull Case (30% probability)

Target: $255-$270

How we get there:

- Earnings CRUSH expectations with revenue toward the $213B high end and EPS well above $1.97 consensus

- AWS growth re-accelerates to 20%+ on Trainium3 adoption and AI workload demand

- 2026 capex guidance stays at $125B or comes in lower, easing FCF compression fears

- Project Dawn cost savings clearly reflected in operating margins

- Advertising momentum continues at 24%+ growth rate

- Stock breaks through $245 gamma resistance, triggers dealer hedging buying to $250-$255

- Analysts raise price targets above $300, creating further buying momentum

Key metrics needed:

- Revenue above $210B (top half of guidance range)

- AWS growth re-acceleration (sequential improvement)

- Operating margin expansion driven by ads + cost cuts

- Constructive 2026 commentary on FCF trajectory

For the call trade: Stock at $260 by Feb 27 = calls worth $15.00, profit of $5.50/contract x 4,999 = $2.75M gain (58% ROI). Stock at $270 = calls worth $25.00, profit of $15.50/contract x 4,999 = $7.75M gain (165% ROI).

Base Case (45% probability)

Target: $240-$255 range (CONSOLIDATION THEN GRIND HIGHER)

Most likely scenario:

- Solid earnings meeting or slightly beating consensus (~$208-210B revenue, $1.95-2.05 EPS)

- AWS growth stable but not spectacular -- market wants more proof of re-acceleration

- Capex guidance confirmed at $125B, creating mixed reactions (bullish on AI investment, bearish on FCF)

- Stock initially pops on earnings beat, tests $245-$250 resistance, then consolidates

- Analysts maintain targets in $285-$305 range, providing long-term upside narrative

- Project Dawn layoffs create short-term noise but market ultimately focuses on fundamentals

- Trading range of $240-$255 through February as market digests results

For the call trade: Stock at $250 by Feb 27 = calls worth $5.00, loss of $4.50/contract x 4,999 = $2.25M loss (47% loss on premium). Stock at $255 = calls worth $10.00, profit of $0.50/contract x 4,999 = $250K modest gain (5% ROI). This is the "break-even zone" for the trade.

Bear Case (25% probability)

Target: $215-$235

What could go wrong:

- Earnings miss on revenue or EPS -- even a small miss at this juncture could trigger aggressive selling

- AWS growth decelerates, raising concerns about Azure and Google Cloud taking share

- 2026 capex guidance revised UPWARD from $125B, sending FCF bears into a frenzy

- Free cash flow continues collapsing from the already-69% decline

- Project Dawn layoffs (30,000 total) create execution risk and negative headlines

- Amazon Leo faces impossible FCC deadline -- write-down risk if constellation deployment fails

- Broader tech selloff on macro fears drags mega-caps lower

- Break below $235 gamma support triggers cascade to $230, then $220

For the call trade: Stock at $230 by Feb 27 = calls expire worthless = $4.7M total loss (100%). Stock at $240 = calls worth $0 (OTM at expiration) = $4.7M total loss.

Trading Ideas

Conservative: Wait for Post-Earnings Clarity

Play: Stay on the sidelines until after February 5th earnings, then look for a pullback entry in shares or longer-dated calls

Why this works:

- Earnings in 7 days creates binary event risk -- options premiums are elevated and you are paying for uncertainty

- Implied volatility will crush 30-50% post-earnings, making options significantly cheaper after the event

- AMZN has beaten estimates 4 straight quarters but guidance quality (especially capex and FCF) matters more than the beat itself

- Average analyst price target of $285-$294 implies 19-23% upside from current levels -- there is no rush to chase

- Project Dawn layoffs may create additional noise in the next few days, potentially offering a better entry

Action plan:

- Watch February 5th earnings closely for: revenue ($210B+ target), AWS growth rate (re-acceleration needed), operating margins, 2026 capex guidance, and FCF trajectory commentary

- If stock pulls back to $230-$235 post-earnings (gamma support zone), that is an excellent entry for shares with 20-25% upside to analyst targets

- If stock rallies through $250+ on strong results, wait for a pullback to $245 support before entering

- Consider April or June 2026 expiration calls for longer runway to capture AWS and Trainium3 catalysts

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Balanced: Post-Earnings Call Spread Targeting ATH Retest

Play: After earnings (Feb 6+), buy a bull call spread targeting a move back to all-time highs

Structure: Buy $245 calls / Sell $260 calls (March 20 expiration for 43 days of runway)

Why this works:

- IV crush after earnings makes the spread significantly cheaper -- buy AFTER volatility drops

- Defined risk: maximum loss is the net debit paid (likely $4-$6 per spread post-IV crush vs $7-$9 now)

- Maximum profit: $15 wide spread minus cost = $9-$11 potential gain per spread if AMZN above $260 at March expiration

- Risk/reward of roughly 2:1 on a stock where 49 of 57 analysts rate Strong Buy

- 43 days captures the post-earnings momentum period plus Amazon Leo commercial launch and Trainium3 ramp news

- $260 short strike sits just above ATH -- realistic target if fundamentals confirm

Entry timing:

- Wait 1-2 days post-earnings (Feb 6-9) for IV to settle and initial reaction to stabilize

- Only enter if stock trades $240+ (confirms positive earnings reception)

- Skip if stock drops below $230 (bear case unfolding -- thesis invalidated)

Position sizing: Risk only 3-5% of portfolio on any single spread trade

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

Aggressive: Pre-Earnings Momentum Call (HIGH RISK)

Play: Buy short-dated calls betting on a pre-earnings run-up and earnings beat

Structure: Buy AMZN $245 calls expiring February 27 -- essentially mimicking the institutional flow detected today

Why this could work:

- Following $4.7M of institutional flow -- someone with deep pockets and likely strong conviction is leading the way

- AMZN has beaten EPS estimates 4 consecutive quarters -- the beat streak is real

- 49 of 57 analysts rate Strong Buy with average PT of $285-$294 -- massive upside consensus

- Stock is 6% below its ATH -- a reversion to highs alone would put the trade near break-even

- AWS Trainium3 ramp, advertising acceleration, and Project Dawn cost savings provide multiple tailwinds

- Break-even of $254.50 is within the monthly implied move upper range of $257.70

Why this could blow up (SERIOUS RISKS):

- EXPENSIVE: $9.50 per contract with only 29 days to expiration -- time decay is aggressive

- BINARY EVENT: Earnings on Feb 5 is make-or-break; a miss or weak guidance means these go to zero

- CAPEX OVERHANG: $125B capex guidance could spook investors even on a revenue beat

- FCF CONCERNS: 69% decline in free cash flow is a legitimate bear case

- LAYOFF SENTIMENT: 30,000 job cuts create negative headlines right before the report

- NEEDS 6% MOVE: Break-even at $254.50 requires a significant rally from $240

CRITICAL WARNING -- DO NOT attempt unless you:

- Can afford to lose the ENTIRE premium (real possibility)

- Understand earnings binary risk and IV crush mechanics

- Have experience trading short-dated options around earnings

- Plan to manage the position actively -- consider taking partial profits on any pre-earnings run-up

- Accept that even a small earnings miss means these calls could lose 80-100% of value overnight

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced only

Risk Factors

Do not ignore these potential landmines:

-

Earnings binary event in 7 days: Q4 2025 results on February 5th will determine the near-term direction of AMZN. The stock is priced for a beat based on the trailing 4-quarter streak, meaning a miss or even an in-line result could trigger a 5-10% selloff. Revenue guidance quality ($206-213B range) means the difference between the low and high end is $7B -- that spread alone moves the stock.

-

Free cash flow compression is real: FCF plummeted 69% to $14.8B TTM driven by a $50.9B YoY surge in capital expenditure. With $125B capex guided for 2026 and a $15B bond offering in November 2025 (first US dollar debt issuance in 3 years), Amazon is spending at unprecedented levels. The market needs to see a clear path to FCF recovery or the stock stays range-bound.

-

Project Dawn layoffs create execution risk: Up to 30,000 corporate positions being eliminated by May 2026, with 78% of cuts targeting mid-level managers. While this boosts margins, losing institutional knowledge and management depth during a critical AI infrastructure buildout is a real concern. The premature "Project Dawn" email leak was also an embarrassing operational stumble.

-

Amazon Leo faces near-impossible FCC deadline: Only ~150+ satellites in orbit vs ~1,618 required by July 30, 2026. SpaceX Starlink has ~7,000+ satellites and a massive head start. $10B+ in launch contracts are at risk if the constellation falls behind schedule. Missing the FCC deadline could require a new application and write-downs.

-

Cloud competition intensifying: Azure growing at a similar rate to AWS while Google Cloud is growing faster at 33.5%. Microsoft's enterprise distribution advantage and Google's AI-native approach both threaten AWS market share. NVIDIA GPU ecosystem dominance may limit Trainium chip adoption despite the 50% cost reduction claims.

-

E-commerce headwinds: Competition from Temu, Shein, and Walmart+ is pressuring the core retail business. UPS reducing Amazon daily volume by 1M packages as part of $3B cost savings signals shifting logistics dynamics. Amazon shuttered Fresh and Go grocery chains, admitting defeat in physical retail.

-

$4.7M call position is time-sensitive: With only 29 days to expiration, theta decay will erode the position's value rapidly if the stock does not move quickly above $245. Each day that passes without a move higher costs the position approximately $160K in time value decay. If earnings disappoint or the stock stays flat, this $4.7M evaporates.

The Bottom Line

Real talk: Someone just committed $4.7 MILLION to AMZN February $245 calls with earnings 7 days away. This is a clear, directional, bullish bet that Amazon will beat Q4 expectations on February 5th and rally through the $245 gamma resistance level toward its November all-time high of $254. The break-even of $254.50 is ambitious but within the implied move range.

What this trade tells us:

- Institutional money believes the earnings beat streak continues (4 straight quarters of EPS beats)

- The $245 strike at gamma resistance shows confidence that earnings momentum will be strong enough to overcome dealer selling pressure

- Feb 27 expiration gives 22 days of post-earnings runway -- enough time for the market to digest results and for follow-through buying to develop

- Volume of 6,200 vs OI of 4,000 confirms this is primarily NEW positioning, not rolling or closing an existing trade

The bull case is straightforward: AWS re-acceleration + advertising growth at 24% + Project Dawn cost savings + Trainium3 adoption = margin expansion and revenue beat. Average analyst target of $285-$294 implies this stock should be 19-23% higher. If earnings confirm the thesis, $245 breaks and $250-$255 is the next stop.

The bear case is equally clear: $125B capex, 69% FCF compression, 30,000 layoffs, and cloud competition headwinds could overshadow a revenue beat. At 34x P/E, AMZN is not cheap and requires flawless execution.

If you are considering following this trade:

- Understand this is a time-sensitive, earnings-dependent bet -- not a long-term investment

- The trader's break-even of $254.50 requires a 6% move in 29 days -- possible but not certain

- If you want to play AMZN bullishly with less risk, consider post-earnings entry in shares or longer-dated spreads

- Never risk more than you can afford to lose on any single options trade

If you own AMZN shares:

- Current price of $240 is 6% below the ATH -- you are NOT at the top, there is room to hold

- Earnings on Feb 5 is the next major catalyst -- decide BEFORE the report whether you want to hold through or trim

- Consider selling covered calls at $260-$270 (March expiration) to generate income while waiting for the breakout

- The $235 and $230 gamma support levels are your key downside markers

If you are watching from the sidelines:

- February 5th is the decision point -- do NOT chase before earnings with short-dated options unless you are experienced

- Post-earnings pullback to $230-$235 would be an excellent entry point for shares (20%+ upside to analyst consensus)

- If earnings beat and stock breaks $250, the January ATH of $254 and then $260+ become realistic targets

- Longer-term, AWS Trainium3 ramp, advertising scale, and Project Dawn margin improvement create a compelling 2026 story

Mark your calendar -- Key dates:

- Jan 28, 2026 - Project Dawn layoffs (16,000) announced

- Feb 5, 2026 - Q4 2025 earnings report (2:00 PM PT) -- THE catalyst

- Feb 12, 2026 - Amazon Leo Ariane 64 satellite launch (32 satellites)

- Feb 27, 2026 - This $4.7M call option expires

- Q1 2026 - Amazon Leo commercial service launch in 5 countries

- By May 2026 - Project Dawn layoffs completion (~30,000 total)

- Late Apr 2026 - Q1 2026 earnings (estimated)

- Jul 30, 2026 - FCC deadline: ~1,618 Kuiper satellites operational

Final verdict: AMZN's fundamental story is strong -- AWS leadership, advertising dominance, AI infrastructure investment, and cost discipline through restructuring all point to higher prices over the next 12 months. The $4.7M call buy is a reasonable if aggressive bet that earnings will be the catalyst to restart the rally. But at 34x P/E with $125B in capex commitments and 30,000 layoffs in progress, the near-term path is not guaranteed. The risk/reward favors being PATIENT: let earnings clear, then position for the next move with better information and lower implied volatility.

Smart money is getting bullish. The question is whether February 5th delivers the goods.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance does not guarantee future results. The $4.7M call trade reflects one trader's view and does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for significant gaps in either direction. Position sizing and risk management are critical.

About Amazon.com Inc.: Amazon is the leading online retailer and marketplace for third-party sellers. Revenue breakdown: Retail ~74%, AWS ~17%, Advertising ~9%. The company operates in e-commerce, cloud computing, AI, and digital streaming, with a market cap of $2,597.8 billion in the Retail-Catalog & Mail-Order Houses industry.