🐻 AMZN $4.2M Deep OTM LEAP Put - Someone Just Bought Crash Insurance on Amazon Through 2028!

📅 February 26, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $4.2 MILLION on deep out-of-the-money LEAP puts on Amazon (AMZN) - buying 2,500 $150 puts expiring December 2028, a full 34 months out. With AMZN trading at $208.38, this is a bet that Amazon drops 28%+ from here over the next nearly three years. This isn't a day trade - this is structural crash insurance from a big-money player who sees serious downside risk as Amazon burns through $200B in AI capex with negative free cash flow, insiders selling hand over fist, and AWS losing ground to Azure and Google Cloud.

📊 Company Overview

Amazon.com Inc (AMZN) is the everything-store turned cloud computing and advertising juggernaut:

- 🛒 What they do: The world's largest online retailer, dominant cloud platform (AWS), and the third-largest digital advertising business in the US - plus satellite internet (Kuiper), AI assistants (Alexa+), streaming (Prime Video), and more

- 💰 Market Cap: ~$2.26T

- 🏢 Sector: Retail - Catalog & Mail-Order Houses

- 📈 Exchange: NASDAQ

- 📊 Current Price: $208.38

- 🔑 Key Story: Amazon is making the largest single-year infrastructure bet in corporate history ($200B capex in 2026) while free cash flow collapses, insiders sell aggressively, and AWS faces accelerating competition from Azure and Google Cloud

💰 The Option Flow Breakdown

📊 The Tape

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Strategy |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:23:55 | AMZN | - | BUY | PUT $150 | 2028-12-15 | $4.2M | $150 | 2,500 | 1,500 | 2,500 | $208.38 | STANDALONE (BTO) |

Net Premium: $4.2M DEBIT 💸

🤓 What This Actually Means

Let me break this down - because this is a fascinating and unusual trade.

One leg, one massive bet: Amazon could be in serious trouble by late 2028.

- 💸 $4.2 million in premium for protection: At $16.82 per contract, this trader paid $4.2M for the right to sell AMZN at $150 through December 2028. That is 28% below today's price. This isn't someone hedging a small dip - this is crash insurance.

- 📊 1.67x Vol/OI (2,500 volume vs. 1,500 open interest) - volume exceeds open interest, indicating this is fresh capital entering the position, not a roll or adjustment

- 🐋 $4.2M on a single put leg is serious money - this is not retail. This is an institution or ultra-high-net-worth individual protecting a concentrated long AMZN position, or outright expressing a structural bearish thesis

- ⏰ 34 months to expiration (December 2028) - this is one of the longest-dated option trades you'll see. It covers multiple earnings cycles, the full $200B capex deployment, the FTC antitrust trial (February 2027), and the Kuiper satellite deadline (July 2026)

- 🎯 $150 strike = pre-2024 levels - AMZN hasn't traded at $150 since early 2024. Getting there would mean a roughly $875B wipeout from the current market cap

What's the actual strategy here?

This is a Long Put (Buy-to-Open) - the simplest and most direct way to bet on or hedge against a major decline. Here's what makes it interesting:

- 🛡️ Portfolio hedge interpretation: If this trader owns a massive AMZN stock position (say, $100M+), spending $4.2M (~4% of position value) on 34-month crash insurance is a perfectly rational risk management move. Think of it like buying fire insurance on your house - you hope you never need it, but you sleep better at night.

- 🐻 Directional bear thesis: Alternatively, this could be a pure directional bet. If AMZN drops to $130 by late 2028 (not impossible if the AI capex bet fails), these puts would be worth $50+ each - a 3x return on the $16.82 entry.

- 📈 Breakeven at $133.18 - AMZN needs to fall to ~$133 for this trade to profit at expiration. That is a 36% decline from today's price.

- 🎯 Aligns with DA Davidson's $175 bear target - and goes even further. DA Davidson downgraded AMZN to Neutral with a $175 PT on February 6, citing AWS losing its lead. This trader's $150 strike implies an even more severe outcome.

Bottom line on the trade: Whether this is a hedge or a bet, the message is clear - someone with deep pockets thinks AMZN has meaningful downside risk over the next 3 years, and they're willing to spend $4.2M on that view.

📈 Technical Setup / Chart Check-Up

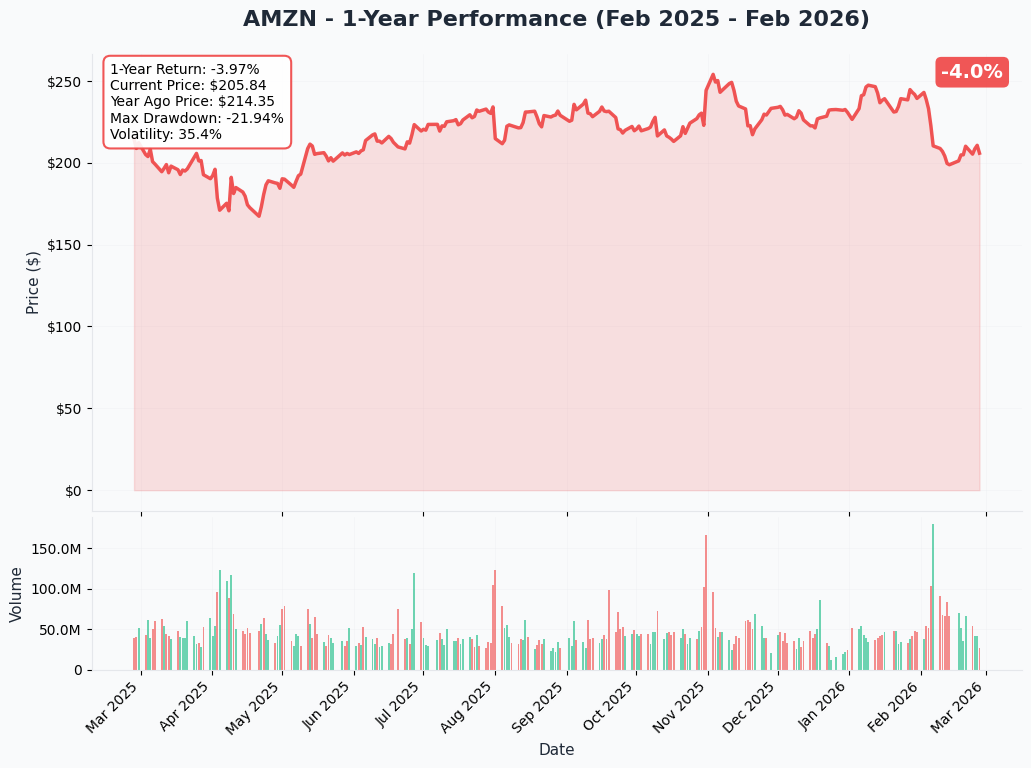

YTD Performance

AMZN has been in a world of pain since the capex bombshell dropped on February 5:

- 📉 Down ~22% from all-time highs: The stock peaked near $268 in late 2025 before the selloff began

- 📉 9-day losing streak in February: Amazon shed more than $450 billion in market value during its worst streak since 2006 before snapping it on February 17

- 💸 The $200B capex announcement was the catalyst that broke the stock: Investors were expecting ~$147B in 2026 capex. Amazon guided to $200B - a 36% overshoot that crushed sentiment

- 📊 Valuation compression: Forward P/E has dropped to ~27-29x, near 5-year lows and below the peer average of 30.2x

- 🔄 Recent bounce: AMZN rallied 2.6% on February 20 after the Supreme Court struck down IEEPA-based tariffs, a tailwind for e-commerce

Key takeaway: The stock is oversold on capex sticker shock and AWS competition fears, but the business actually beat on revenue ($213.4B, +14% YoY) and operating income ($25B). The question is whether the market will reward Amazon for investing aggressively in AI or punish it for burning cash. This $4.2M put buyer is betting on punishment.

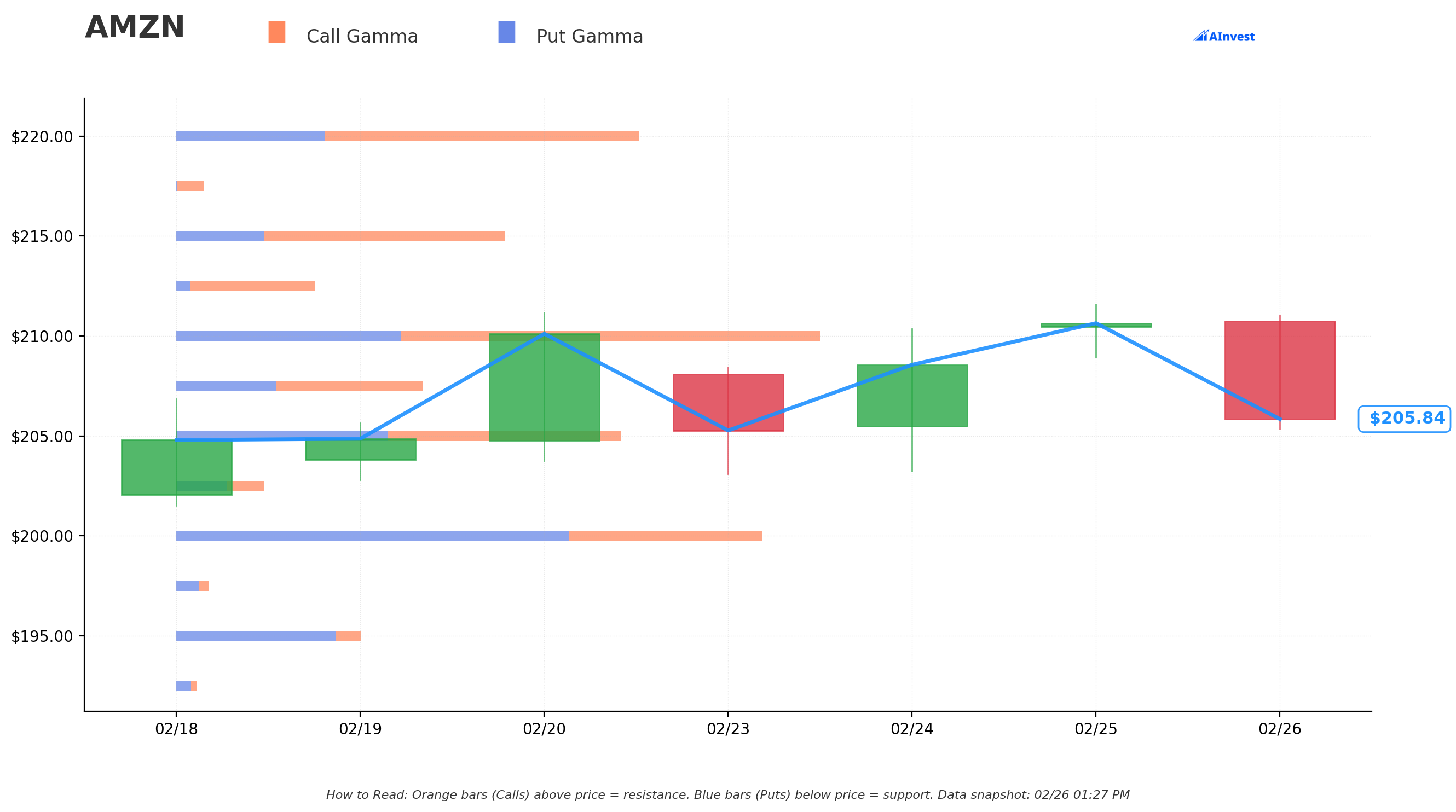

Gamma-Based Support & Resistance Analysis

Current Price: $205.60

The gamma exposure (GEX) map shows where options market maker positioning creates natural price magnets, floors, and ceilings. Think of these like invisible walls where the stock tends to slow down or bounce:

🔵 Support Levels (Put Gamma Below Price):

- $205 - MASSIVE immediate support with 61.2B total gamma (only 0.3% below current price). This is the biggest gamma concentration near the stock and acts as a strong near-term floor. Net GEX is slightly positive here, meaning dealers will buy the dip, reinforcing the support.

- $200 - Heavy structural support with 81.1B total gamma (2.7% below). This is the single strongest gamma level on the entire board. Net GEX is negative (-27.0B), meaning put gamma dominates - if AMZN breaks $200, dealer hedging could accelerate the selloff.

- $195 - Secondary support at 25.3B gamma (5.2% below). Put-dominated with -18.1B net GEX.

- $190 - Extended floor at 27.1B gamma (7.6% below). Another put-heavy level (-12.5B net GEX).

🟠 Resistance Levels (Call Gamma Above Price):

- $207.50 - First resistance at 33.6B gamma (0.9% above). Net GEX is positive (+6.3B), meaning call gamma dominates - dealers will sell into strength here, creating a near-term cap.

- $210 - MAJOR resistance at 87.3B total gamma (2.1% above). This is the strongest resistance level on the board with +26.1B net GEX. AMZN needs significant buying pressure to clear this.

- $215 - Strong resistance at 44.8B gamma (4.6% above). Call-dominated with +20.9B net GEX.

- $220 - Heavy resistance at 63.0B gamma (7.0% above). Call-dominated with +22.7B net GEX.

- $225 - Moderate resistance at 26.5B gamma (9.4% above).

- $230 - Extended resistance at 35.5B gamma (11.9% above). Call-dominated with +20.9B net GEX.

What this means for traders: AMZN is sitting just above the $205 gamma support floor with the first real resistance at $207.50 and a wall at $210. The $200 level is absolutely critical - it's the strongest gamma level on the entire board at 81.1B total. If $200 breaks, the next support doesn't kick in until $195 and $190, which means a break below $200 could trigger a fast slide. On the upside, $210 is a formidable wall that AMZN needs to clear to change the narrative.

Net GEX Bias: Bullish (438.7B total call gamma vs 309.9B total put gamma) - dealer positioning leans net bullish, which means market makers will tend to buy dips and sell rallies, keeping AMZN in a range near current levels unless a catalyst forces a breakout.

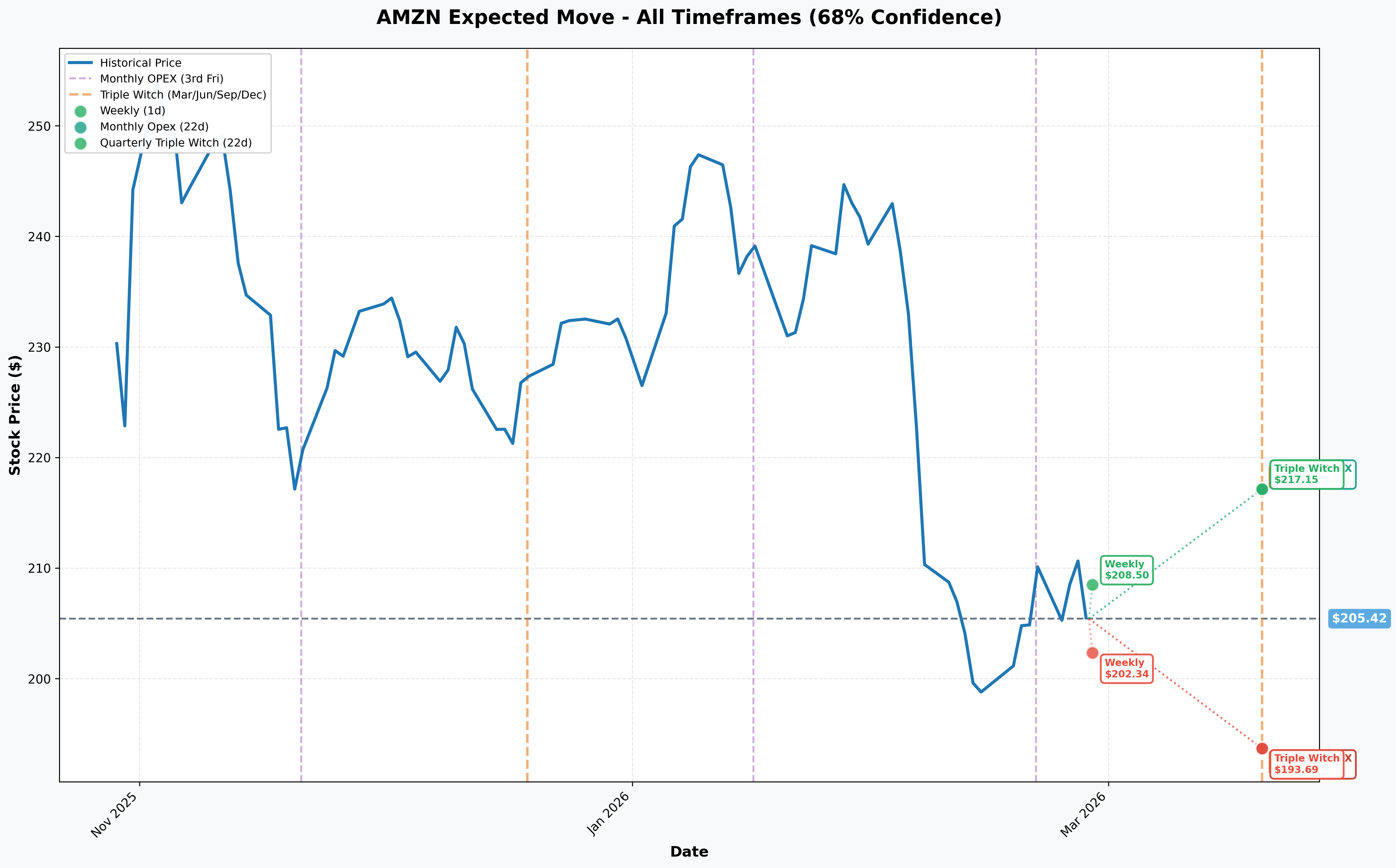

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Feb 27 - 1 day): ±$3.08 (±1.5%) --> Range: $202.34 - $208.50

- 📅 Monthly OPEX / Triple Witch (Mar 20 - 22 days): ±$11.73 (±5.7%) --> Range: $193.69 - $217.15

- 📅 December 2028 (THIS TRADE!): ~34 months out, extrapolated range roughly $130 - $300+

Translation: The options market expects AMZN could move ±1.5% this week and ±5.7% through the March 20 Triple Witch OPEX. That monthly range of $193.69 to $217.15 is significant - it tells you the market sees AMZN potentially testing both $194 on the downside and $217 on the upside within the next 3 weeks.

The $150 strike on this LEAP put sits WAY below even the monthly implied downside of $193.69. That confirms this is NOT a near-term trade. The buyer is positioning for a multi-year structural decline scenario - the kind that plays out over earnings cycles, not weeks.

Key insight: The tight weekly range ($202-$209) suggests near-term stability, but the wider monthly range ($194-$217) reflects elevated uncertainty heading into Q1 earnings season. For the LEAP put buyer, none of this near-term noise matters - they are playing a 34-month game.

🎪 Catalysts

🔥 Upcoming Catalysts

Q1 2026 Earnings Report - Late April 2026 📊

Expected around April 23-30, this will be the first earnings report under the $200B annual capex run rate. Key things to watch:

- 📊 Revenue guidance: $173.5B - $178.5B (11-15% YoY growth)

- 📊 Operating income guidance: $16.5B - $21.5B (includes ~$1B in higher Amazon Leo costs)

- ☁️ AWS growth rate: will it re-accelerate above 24%, or keep losing share to Azure (39%) and GCP (48%)?

- 💸 Free cash flow trajectory: first full quarter under the $200B annual capex run rate

- 🤖 Alexa+ adoption metrics: first full quarter of national availability

FCC Kuiper Half-Constellation Deadline - July 30, 2026 🛰️

This is a high-stakes binary catalyst. Amazon must launch and operate 1,500+ satellites by this date or risk losing its FCC spectrum licenses - worth billions. The constellation currently has 200+ satellites. Amazon has filed for an extension and contracted 10 additional Falcon 9 and 12 New Glenn launches, but the timeline is extremely aggressive.

FTC Antitrust Trial - February 9, 2027 ⚖️

The FTC plus 17 state attorneys general allege Amazon maintains an illegal monopoly. The trial was pushed back from October 2026 to February 2027 (bench trial). Throughout 2026, pre-trial motions and discovery will generate headlines and uncertainty. Potential remedies could include marketplace restructuring - a nightmare scenario for the stock.

AWS re:Invent 2026 - November 30 to December 4, 2026 🤖

Major product announcements expected with AI/ML focus. New Agentic AI categories in AWS AI Specialization launching in 2026. This is typically a positive catalyst for AMZN.

Capex Transparency - Throughout 2026 🔍

Every quarterly report will be scrutinized for capex execution and ROI signals. The market is demanding more granular breakdown of the $200B allocation. If Amazon can show clear AI revenue tied to spending, the stock re-rates higher. If not, the bleeding continues.

Prime Video Advertising Scale-Up - 2026 📺

Prime Video reaches 315M+ monthly viewers worldwide. Industry analysts project ad revenue could reach $7-10B annually by year-end. Freevee projected to grow 22% in 2026 to ~$2.2B. More interactive ad formats planned.

✅ Recent Catalysts (Already Happened)

Q4 2025 Results - February 5, 2026 📊

The earnings that shook the market:

- 💰 Revenue: $213.4B (+14% YoY) vs $211.33B consensus - beat

- ❌ EPS: $1.95 vs $1.97 consensus - slight miss

- ☁️ AWS Revenue: $35.58B (+24% YoY) vs $34.93B expected

- 📺 Advertising Revenue: $21.32B (+23% YoY)

- 💸 Full-Year 2025 Revenue: crossed the $700B milestone

- 💥 THE BOMBSHELL: 2026 capex guided to ~$200B vs $146.6B Wall Street expected - this is what crushed the stock

Free Cash Flow Collapse 💸

- 2025 FCF collapsed to $11.2B from $38.2B in 2024

- Capex consumed 94.5 cents of every dollar of operating cash flow in 2025

- 2026 FCF expected to be negative given $200B capex plan

Supreme Court Tariff Ruling - February 20, 2026 ⚖️

SCOTUS ruled 6-3 that IEEPA does not authorize the President to impose tariffs. AMZN rallied 2.6% to $210.11 on the news. Particularly beneficial given 24% of Amazon's net sales come from third-party sellers, many China-based. Caveat: de minimis rule remains shelved and legislative tariffs still possible.

DA Davidson Downgrade - February 6, 2026 📉

Gil Luria downgraded AMZN from Buy to Neutral, PT slashed from $300 to $175. Thesis: AWS is "losing its lead" - Google Cloud grew 48%, Azure 39%, vs. AWS 24%. Warned Amazon "may not have a choice but to follow through with a $50B investment in OpenAI" to remain competitive.

Alexa+ National Launch - February 4, 2026 🤖

AI-powered Alexa+ made available to all US users; free for Prime members, $19.99/month otherwise. Powered by Amazon Nova LLMs + Anthropic Claude. New personality options added February 25.

Amazon Leo Satellite Deployment - February 12, 2026 🛰️

First heavy-lift launch deploying 32 satellites via Ariane 6. Constellation now exceeds 200+ satellites. Service availability in 5 markets by end of March 2026.

FTC Prime Settlement - $2.5B 💰

$1.5B in customer refunds + $1.0B civil penalty for unlawful Prime enrollment/cancellation practices. Claim notices began going out January 2026.

Insider Selling - Relentless 📉

37 insider transactions over last 90 days, ALL sells, totaling $56.4M. Zero insider purchases. Notable sellers include the CEO of AWS (Matthew Garman), CEO of Worldwide Amazon Stores (Douglas Herrington), and SVP David Zapolsky.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, analyst targets, and the dense catalyst calendar, here are the scenarios for AMZN:

📈 Bull Case (35% probability)

Target: $230-$280

How we get there:

- ☁️ AWS growth re-accelerates above 25-30% as AI workloads scale, proving the $200B capex bet is working

- 📊 Q1 and Q2 earnings beat on revenue and operating income, with management providing granular capex ROI breakdowns

- ⚖️ SCOTUS tariff ruling provides sustained tailwind; Amazon gains e-commerce share under tariff uncertainty

- 📺 Advertising revenue continues growing 20%+, approaching $80B+ annual run-rate

- 🛰️ Kuiper clears the FCC deadline, opening a new revenue stream

- 📈 Forward P/E re-rates from 28x back toward the 35-40x historical range on improving cash flow visibility

- 🎯 Stock breaks through $210 gamma resistance and targets $220, $225, $230 levels

- 📊 Analyst consensus target of $279-$287 gets validated with upgrades

At $230: Stock clears all gamma resistance levels. The $150 LEAP put would be worth roughly $4-5 (mostly time value), a loss of ~$12/contract (-70%). At $280: puts worth near-zero. The LEAP put buyer loses most or all of the $4.2M premium.

🎯 Base Case (40% probability)

Target: $195-$220 range

Most likely scenario:

- ✅ AMZN treads water in the $195-$220 range as the market digests the capex plan quarter by quarter

- 📊 Earnings meet guidance but don't blow away estimates; AWS growth stays in the 22-26% range

- ☁️ The $200B capex story slowly gets priced in as "the new normal" for hyperscalers

- 🔄 Stock bounces between the $200 mega-support (81.1B gamma) and $210 resistance (87.3B gamma) for months

- 💸 Free cash flow goes negative in 2026 as expected, keeping value investors cautious

- ⚖️ FTC pre-trial proceedings generate intermittent headline risk but no resolution

At $205: The $150 put would retain meaningful time value ($8-10 with 2+ years to go) but no intrinsic value. Position roughly breakeven to a modest loss. At $195: puts gain some additional time value ($10-13), nearing breakeven for the trade.

📉 Bear Case (25% probability)

Target: $150-$185

What could go wrong:

- 😰 AI capex ROI fails to materialize - the $200B bet turns out to be Amazon's biggest mistake

- ☁️ AWS growth decelerates below 20% as Azure and GCP continue taking share, and CoreWeave erodes GPU workload share

- 💸 Negative FCF in 2026 extends into 2027, forcing Amazon to issue debt or cut spending

- ⚖️ FTC antitrust trial results in meaningful marketplace restructuring remedies

- 🛰️ Kuiper misses the FCC half-constellation deadline, jeopardizing spectrum licenses worth billions

- 📉 Consumer spending recession + tariff creep compress retail margins

- 📉 Broader AI spending skepticism hits all hyperscalers, dragging AMZN into a multi-year de-rating

- 📉 Stock breaks below the $200 mega-gamma support, triggering accelerated selling to $195, $190, and beyond

- 🎯 DA Davidson's $175 target gets tested; in the severe scenario, the $150 strike comes into play

At $175: The $150 put would be worth roughly $30-35 with time value remaining. That is a 2x return on the $16.82 entry. At $150: puts are at-the-money, worth roughly $20-25+ in time value alone - a 1.2-1.5x return with potential for much more if the decline continues.

At $130 (extreme bear): The $150 put would be worth $20+ intrinsic plus time value = roughly $30-40. That is a 2-2.4x return on the $4.2M investment.

This is exactly the scenario the LEAP put buyer is positioning for - a multi-year deterioration where the $200B AI capex gamble doesn't pay off and the stock revisits pre-2024 levels.

💡 Trading Ideas

🛡️ Conservative: "Sleep Well With Amazon" - Put Spread Hedge

Play: Buy the AMZN June 2026 $195 put, sell the June 2026 $180 put

Structure: $195/$180 put spread, ~4 months to expiration

Why this works:

- 🛡️ Defined risk: you can only lose the net debit (~$3-4 per spread)

- 💰 Max profit: $15 per spread minus debit (~$11-12 gain) if AMZN below $180 at June expiry

- 📊 The $195 strike aligns with the third gamma support level (25.3B) and sits near the monthly implied move lower bound of $193.69

- ⏰ Captures Q1 earnings (late April) and Kuiper FCC deadline anticipation

- 📈 If AMZN holds above $195, your defined loss is small. If the bear thesis accelerates, the payoff is meaningful

- 🎯 Great for protecting an existing AMZN long position through the next earnings cycle without spending $4.2M like the whale

Position sizing: Risk no more than 2-3% of portfolio. 10 spreads at ~$3.50 each = ~$3,500 risk for ~$11,500 max profit.

Risk level: Low-Moderate (defined risk, directional) | Skill level: Beginner-Intermediate

⚖️ Balanced: "Range Rider" - Iron Condor Through Earnings

Play: Sell the AMZN May 2, 2026 $195/$190 put spread AND sell the May 2, 2026 $220/$225 call spread

Structure: Iron condor capturing the $195-$220 range through Q1 earnings

Why this works:

- 💰 You collect premium from both sides - betting AMZN stays in the $195-$220 range through the next earnings cycle

- 📊 The gamma map shows $200 as massive support and $210 as major resistance - the iron condor range wraps around these gravity zones

- 🔄 Net GEX is bullish, meaning dealers buy dips and sell rallies - perfect for a range-bound thesis

- 📅 The weekly implied move of ±1.5% and monthly of ±5.7% suggest the market expects moderate, not explosive, movement

- ⏰ ~2 months of runway captures earnings volatility crush (sell the event)

- 🎯 Max profit if AMZN stays between $195 and $220 at expiration

- 🛡️ Max loss is defined at $500/spread minus premium collected

Position sizing: 5 iron condors collecting ~$2.00 each = ~$1,000 collected, max risk ~$1,500.

Risk level: Moderate (range-bound bet, risk defined) | Skill level: Intermediate

🚀 Aggressive: "Follow the Whale" - LEAP Put

Play: Buy the AMZN January 2028 $170 put outright - a cheaper version of the whale's crash insurance

Structure: Long LEAP put, 23 months to expiration

Why this works (and why it's risky):

- 🐋 You are expressing the SAME thesis as the $4.2M whale - structural downside risk over the next 2+ years - but at a fraction of the cost

- 📊 The $170 strike is 18% below current price, giving more room than the whale's $150 but still a deep OTM bet

- ⏰ 23 months captures Q1 2026 earnings, Kuiper deadline (July 2026), FTC antitrust trial (February 2027), and multiple capex checkpoints

- 💸 Cost: roughly $8-10 per contract = ~$800-$1,000 per contract (accessible for retail)

- 📉 If AMZN drops to $150, these puts would be worth $20+ intrinsic, roughly a 2x return

- 🎯 Aligns with DA Davidson's $175 bear thesis and negative FCF trajectory through 2026-2027

Why it could blow up:

- 📈 If AI capex pays off and AWS re-accelerates, AMZN could re-rate to $250+ and these puts expire worthless

- 📊 44 analysts rate AMZN Strong Buy with an average PT of $279-$287 - Wall Street consensus is overwhelmingly bullish

- ⏰ 23 months of time decay eating at your premium every single day

- 🔄 Bullish net gamma positioning means dealers will fight the decline

Position sizing: Risk ONLY what you can afford to lose completely. 5 contracts at ~$900 each = ~$4,500 at risk.

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

⚠️ Risk Factors

Whether you're bullish or bearish on AMZN, these are the landmines to watch:

-

💸 $200B capex is the largest corporate infrastructure bet in history: No guarantee AI workloads will materialize at the pace needed to justify the spend. If AI demand disappoints, Amazon will have burned through cash with nothing to show for it. Depreciation from $131.8B (2025) + $200B (2026) will compress operating income for years.

-

📉 Negative free cash flow in 2026 is confirmed: FCF collapsed from $38.2B in 2024 to $11.2B in 2025, and is expected to go negative in 2026. For a $2.2 trillion company, negative FCF is a red flag that can trigger institutional selling.

-

☁️ AWS is demonstrably losing growth momentum: 24% growth vs. Azure at 39% and Google Cloud at 48%. Market share has declined from ~33% in 2021 to ~30% today. Emerging threats like CoreWeave are generating $1B+ quarterly revenue from GPU-intensive AI workloads, directly attacking AWS's moat.

-

⚖️ FTC antitrust trial (February 2027) is a structural overhang: 17 state AGs joined the FTC alleging illegal monopoly. Discovery and pre-trial proceedings throughout 2026 will generate negative headlines. Worst case: marketplace restructuring remedies.

-

🛰️ FCC Kuiper deadline (July 2026) is a binary event: Missing the half-constellation milestone could jeopardize spectrum licenses worth billions. With only 200+ satellites deployed and 1,500 needed, the gap is enormous.

-

👤 Insider selling is aggressive and one-directional: 37 sells, zero purchases, $56.4M sold in the last 90 days. The CEO of AWS, CEO of Worldwide Stores, and SVP are all selling. When the people who know the business best are all heading for the exits, that is worth noting.

-

🌍 Macro risks compound everything: Consumer trade-down behavior under tariff pressure, broader AI capex skepticism weighing on all hyperscalers, and high interest rates increasing the cost of capital for a $200B buildout.

-

📈 For bears: the bull case is also strong. 44 analysts with a Strong Buy consensus and average PT of $279-$287. AMZN at ~28x forward P/E is near 5-year lows. AWS backlog is $244B. Advertising is growing 23%. If the capex bet pays off in 2027-2028, AMZN could double from here and the put buyer loses $4.2M.

🎯 The Bottom Line

Real talk: Someone with very deep pockets just spent $4.2 million buying crash insurance on Amazon through December 2028. A $150 put, 28% below today's price, with 34 months of runway. This is not a panic trade or a day trade - this is a calculated, institutional-grade bet that Amazon's $200B AI capex gamble could go wrong.

What this trade tells us:

- 🎯 Institutional money sees meaningful tail risk in AMZN over the next 3 years - the kind of risk that justifies spending $4.2M on far-OTM protection

- 💸 The trade aligns with the FCF collapse narrative: $38.2B in 2024 --> $11.2B in 2025 --> potentially negative in 2026

- ☁️ The AWS competitive deterioration thesis is gaining traction - even DA Davidson cut their PT to $175 on this concern

- ⏰ The 34-month duration covers every major catalyst: Q1 earnings, Kuiper deadline, FTC trial, multiple capex checkpoints, and the full realization of the 2026-2027 buildout

- 👤 The trade is consistent with 37 insider sells and zero purchases - the smart money appears to be de-risking

If you own AMZN:

- ✅ Consider protective puts or collars to hedge downside, especially through Q1 earnings and the Kuiper deadline

- 📊 The $200 gamma level (81.1B total gamma) is YOUR line in the sand - if it breaks, re-evaluate your position

- 📅 Mark late April (Q1 earnings) and July 30 (FCC Kuiper deadline) as make-or-break catalyst dates

- 💡 This $4.2M put trade doesn't mean AMZN is crashing tomorrow - but it means someone sophisticated sees enough multi-year risk to spend real money on protection

If you're watching from the sidelines:

- ⏰ AMZN at $205-210 is in no-man's-land between the $200 mega-support and $210 mega-resistance. Wait for a resolution before taking a big position

- 📊 Analyst consensus says Strong Buy with $279-$287 targets - but consensus was also bullish before the capex bombshell dropped

- 📈 A break above $210 gamma resistance opens the path to $215-$230; a break below $200 opens the trap door to $190 and below

- 💡 The monthly implied move of ±5.7% through March Triple Witch means significant range-bound opportunity for premium sellers

If you're bearish:

- 🐻 The whale's $150 put trade validates a multi-year bear thesis, but remember: breakeven is $133, a 36% decline

- 📉 Cheaper ways to express downside: shorter-dated put spreads targeting specific catalysts (earnings, Kuiper deadline) let you bet on individual events without paying 34 months of time decay

- ⚠️ Net gamma bias is bullish - dealers will buy dips. Bears need a catalyst to trigger real selling, not just momentum

- 📊 $200 is the level to watch: a break below the strongest gamma support on the board could trigger a cascade

Key dates to mark:

- 📅 February 27 (Friday) - Weekly OPEX (±1.5% implied move)

- 📅 March 20 (Friday) - Triple Witch OPEX (±5.7% implied move)

- 📅 Late April 2026 - Q1 2026 earnings report (THE capex reality check)

- 📅 July 30, 2026 - FCC Kuiper half-constellation deadline (binary catalyst)

- 📅 November 30 - December 4, 2026 - AWS re:Invent 2026

- 📅 February 9, 2027 - FTC antitrust trial begins

- 📅 December 15, 2028 - THIS TRADE EXPIRES - 34 months for the bear thesis to play out

Final verdict: Amazon is at a genuine inflection point. The business is growing ($213.4B revenue, +14% YoY, $68.6B ad revenue) but burning cash at an unprecedented rate to fund the AI buildout. The $4.2M LEAP put trade is a clear signal that at least one sophisticated player believes the risk/reward has meaningfully shifted to the downside over a multi-year horizon. This doesn't mean AMZN is a sell today - 44 analysts still say Strong Buy - but it means the distribution of outcomes is wider than normal. The $200B capex bet is either Amazon's masterstroke that cements its AI dominance, or it's a capital-destroying boondoggle that sends the stock back toward $150. The whale just spent $4.2M betting on the second outcome. Position accordingly.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance does not guarantee future results. LEAP puts can expire worthless, resulting in total loss of premium paid. The $4.2M institutional trade analyzed here may represent hedging, structured product, or portfolio objectives not applicable to retail traders. Amazon faces binary catalysts (FCC deadline, FTC trial, capex ROI) that could trigger significant stock moves in either direction. Always do your own research and consider consulting a licensed financial advisor before trading.

About Amazon.com Inc: Amazon is the world's largest online retailer, leading cloud computing platform (AWS), and third-largest digital advertising platform in the US. With a market cap of ~$2.26T in the Retail - Catalog & Mail-Order Houses sector, Amazon generated over $700B in revenue in 2025 while investing $131.8B in capex, with plans to deploy $200B in 2026 on AI infrastructure.