🐋 AMZN $26M Institutional Call Sweep - Big Money Loading Up on Amazon AI Recovery!

📅 March 16, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $26 MILLION on Amazon call options in two rapid-fire buys this morning, scooping up nearly 19,500 contracts of the May 2026 $210 calls while AMZN trades at $208-209. This isn't retail dabbling - a single institutional player accumulated a massive bullish position in less than a minute, betting Amazon pushes above $210 before May 15th expiration. Translation: Smart money is calling the bottom and loading up on one of the most catalyst-rich tech stocks heading into Q1 earnings season.

📊 Company Overview

Amazon.com Inc (AMZN) is the world's dominant e-commerce and cloud computing platform, with three major revenue engines powering its $2.23 Trillion market cap:

- Market Cap: $2.23 Trillion

- Industry: Retail - Catalog & Mail-Order Houses (AWS, E-Commerce, Advertising)

- Current Price: ~$208.96 (March 16, 2026)

- Primary Business: AWS cloud computing (~31% global market share), North America e-commerce, third-party marketplace, Prime Video/streaming, and a rapidly growing $68.6B/year advertising business

Amazon just completed a $53B record bond offering to fund its $200B capex plan for 2026, partnered with Cerebras for 5x faster AI inference, and launched Alexa+ to all U.S. Prime members. The stock is down ~7.6% YTD from a November 2025 all-time high of $258.60 - and apparently, someone big thinks that discount isn't going to last.

💰 The Option Flow Breakdown

📊 The Tape (March 16, 2026)

| Time | Symbol | Side | Buy/Sell | C/P | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:38:37 | AMZN | ASK | BUY | CALL | 2026-05-15 | $13.2M | $210 | 9,745 | 8,300 | 9,745 | $208.96 | $13.55 | AMZN20260515C210 |

| 10:39:30 | AMZN | ASK | BUY | CALL | 2026-05-15 | $13.1M | $210 | 9,745 | 18,045 | 9,745 | $208.70 | $13.45 | AMZN20260515C210 |

Total combined premium: ~$26.3M across 19,490 contracts (9,745 + 9,745 split execution over 53 seconds)

🤓 What This Actually Means

This is a textbook institutional accumulation pattern - BTO (Buy to Open) in two tranches, hitting the ASK both times, same contract, 53 seconds apart. Here's what stands out:

- 💸 Massive conviction bet: $26M in premium for a position that controls roughly 1.95 million shares worth ~$407M of AMZN exposure

- 🐋 Volume vs OI tells the story: Combined volume of ~19,490 hit into open interest of only 8,300 - this player more than doubled the existing open interest in one shot, strongly confirming new long position opened

- 🎯 Split execution: Breaking the buy into two legs (9,745 each) is a classic institutional tactic to minimize market impact while still accumulating size quickly

- ⏰ 60-day runway: The May 15, 2026 expiration gives ~60 days for the thesis to play out - capturing Q1 2026 earnings (estimated late April), the Cerebras/Bedrock AI launch, and Prime Video Ultra price hike revenue

- 📊 Near-the-money strike: $210 calls bought with AMZN at $208.70-$208.96 means the position is essentially at-the-money - no hiding, this trader needs the stock to move up and fast

What's really happening here: This institutional player is making a direct bullish bet on AMZN recovering from its YTD drawdown. With AMZN sitting ~18% below its November all-time high of $258.60 and analysts holding a strong buy consensus with an average target of $282-$287, they're positioning before Q1 earnings expected late April. The AWS-Cerebras partnership announced March 13th for 5x faster AI inference and the fresh $53B bond offering signal management is firmly committed to accelerating AI infrastructure. This trade is betting those catalysts translate to price recovery.

Unusualness: This is a significant block - hitting into 8,300 OI with 19,490 combined volume means this single player accounts for 2x+ the existing open interest in one session. Trades of this size and structure in AMZN options are relatively infrequent, perhaps a handful of times per quarter at most.

📈 Technical Setup / Chart Check-Up

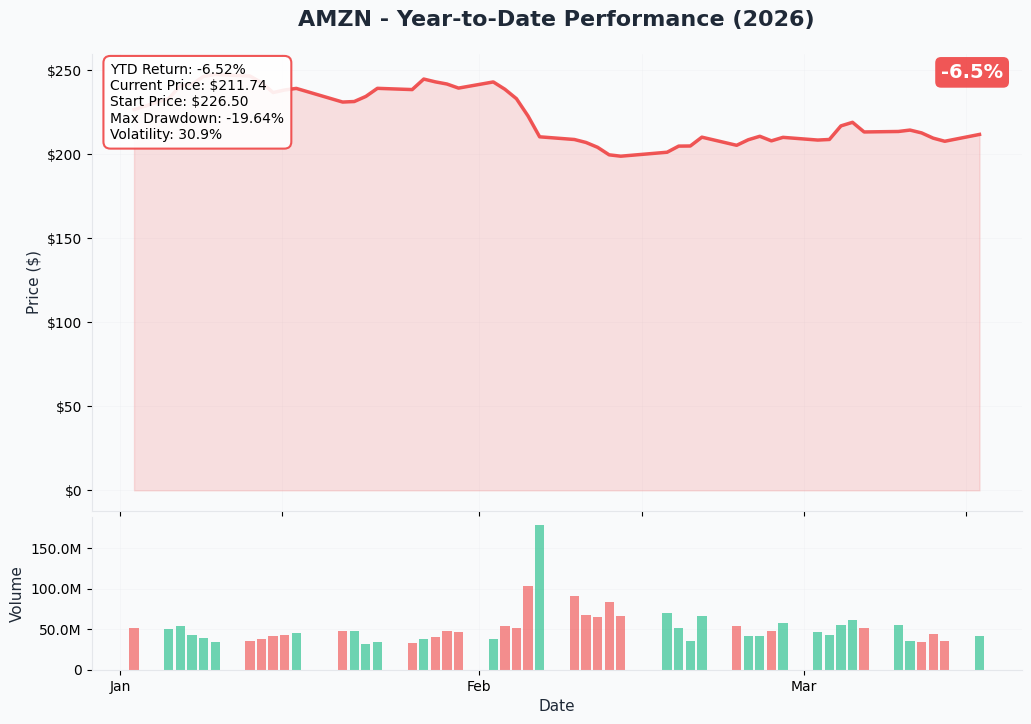

YTD Performance Chart

AMZN has had a rough start to 2026 - down approximately 7.6% YTD from the start of the year, and sitting about 18% below its all-time high of $258.60 set on November 3, 2025. The stock has been under pressure since Q4 earnings on February 5th when the $200B capex guidance spooked investors who had penciled in ~$147B. The stock fell hard post-earnings and has been grinding sideways in the $200-215 range.

Key chart observations:

- 📉 Post-earnings gap down: The $200B capex shock created a distribution zone in the $215-$225 range that now acts as resistance

- 🔄 Stabilization zone: AMZN has been consolidating around $205-$215, suggesting the initial shock selling has absorbed

- 🎯 52-week range: The $161.38 low (April 7, 2025) to $258.60 high shows the full picture - current price is in the middle of the annual range

- 📊 1-year still positive: Despite YTD weakness, the stock is +9.81% over 12 months, which means long-term holders are still in profit

- ⚠️ Needs a catalyst: Without a fresh positive development, the stock risks drifting back toward the $200 gamma support floor

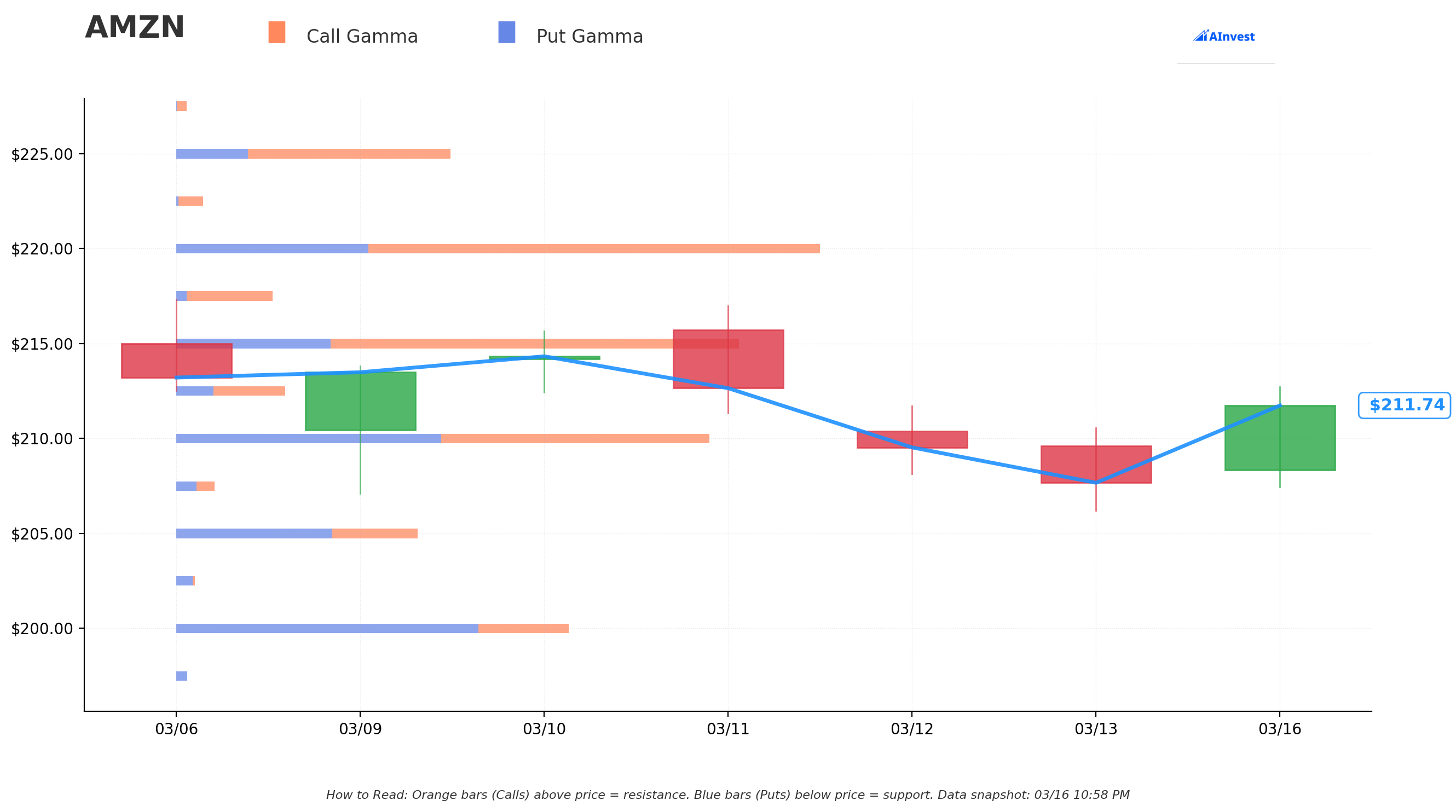

Gamma-Based Support & Resistance Analysis

Current Price: $211.40

The gamma exposure map tells us exactly where the big money in options is parked - and those levels act like magnets and walls for the stock price. Here's the plain-English breakdown:

🔵 Support Levels (Put Gamma Below Price - These are your floors):

- $210 - The single strongest nearby support level with 75.65 total GEX and almost perfectly balanced call/put gamma (38.1 call vs 37.5 put). This is THE key level right now - the $210 calls bought today sit right at this critical gamma cluster. Dealers have massive positioning here which creates a natural cushion.

- $205 - Secondary support at 34.2 total GEX with put-heavy gamma (-9.96 net), meaning dealers will be buyers of stock if price falls to this zone

- $200 - Deep support floor at 55.6 total GEX with heavily put-dominated positioning (-30.1 net GEX). The $200 round number is a psychological AND gamma-based magnet if the stock breaks lower

- $190 - Extended floor at 22.9 total GEX - the disaster scenario level

🟠 Resistance Levels (Call Gamma Above Price - These are your ceilings):

- $215 - Nearest ceiling with the highest total GEX at 79.8 (strongest single level!), net positive 36.1 from call-heavy positioning. This is the first wall the call buyer needs to break through. Once AMZN clears $215, the next leg becomes easier.

- $220 - Second major ceiling at 91.3 total GEX with +36.9 net GEX - actually the largest total gamma level in the picture. A break above $215 doesn't automatically take you to $220; this is another wall to grind through.

- $225 - Third ceiling at 38.9 total GEX (+18.7 net) - lighter resistance, more of a speed bump

- $230 - Fourth ceiling at 43.9 total GEX (+25.8 net) - the zone where Q1 earnings bears/bulls settle their score

- $235 - Lighter resistance at 24.8 total GEX

- $250 - Extended upside target with 27.8 total GEX - the pre-earnings all-time recovery zone

Net GEX Bias: Bullish (430.9 call gamma vs 290.7 put gamma) - The broader positioning across all strikes leans bullish, which is consistent with this institutional call buyer's view.

What this means for traders: AMZN is sandwiched between $210 support (where today's trade is struck - not a coincidence!) and the $215 first resistance wall. The call buyer needs $215 to give way to get real momentum going. The good news: net GEX is bullish, the overall positioning favors upward drift, and the $200 put wall provides strong downside cushion.

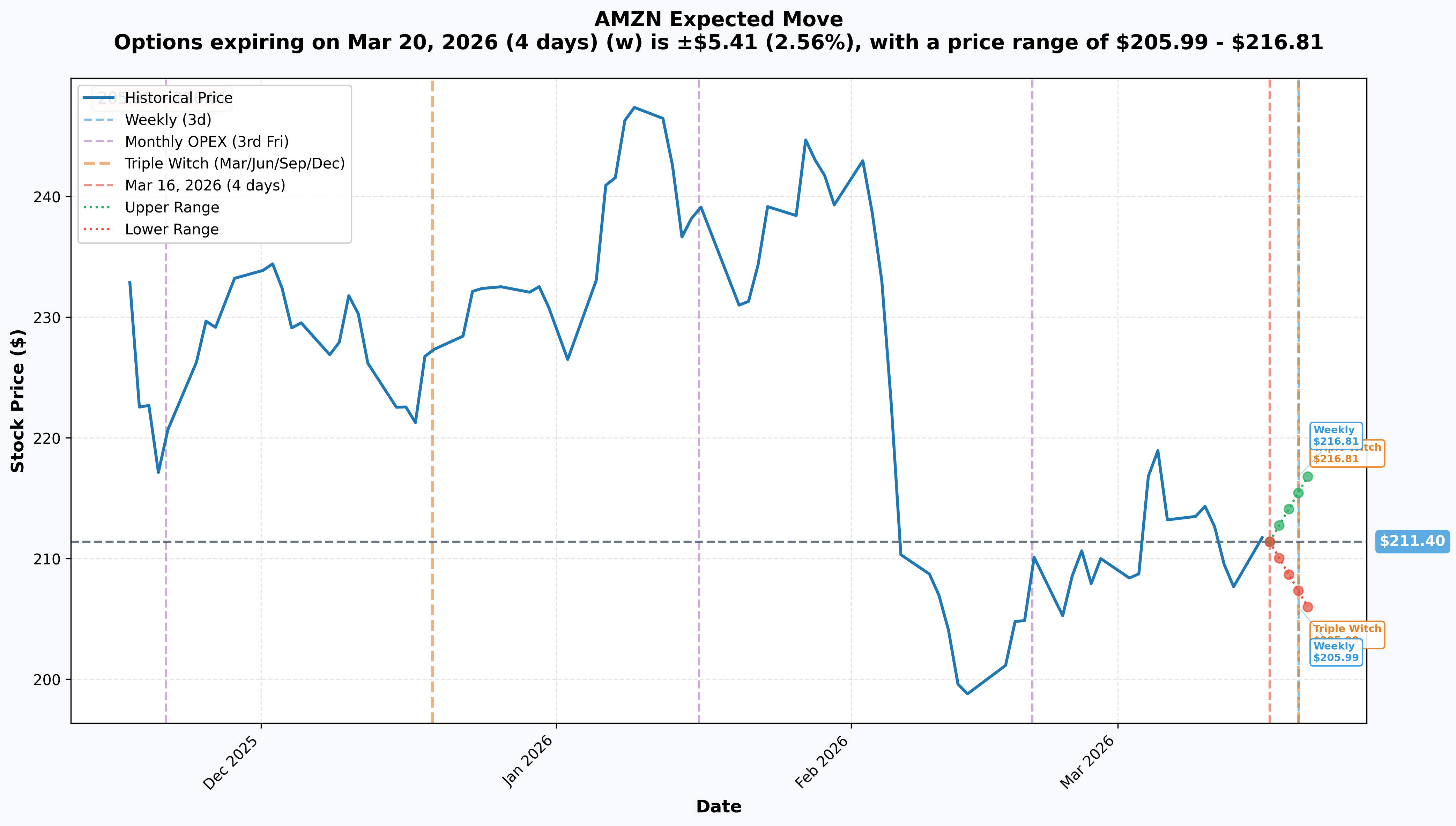

Implied Move Analysis

Options market pricing for March 20, 2026 Triple Witch expiration (4 days away):

- 📅 Weekly / Monthly OPEX / Quarterly Triple Witch (March 20, 4 days): ±$5.41 (±2.56%) → Range: $205.99 - $216.81

This week coincides with Quarterly Triple Witch expiration on March 20 - one of the highest-volume expiration days of the year. The market is pricing in a 2.56% move in either direction by Friday, which tightly frames the action around the gamma support/resistance levels identified above.

Translation for regular folks: The options market is basically saying AMZN will stay between $206 and $217 through this Friday's expiration. Notice how that upper bound at $216.81 aligns almost perfectly with the $215 gamma resistance ceiling and the $220 secondary wall. This is the battleground for the rest of the week.

Key insight for the May trade: The institutional call buyer with a May 15 expiration has ~60 days to absorb this week's Triple Witch volatility and position for Q1 earnings. The near-term $205.99-$216.81 implied range is just the opening act - what matters for the $210 calls is the Q1 earnings print and AWS acceleration data in late April.

🎪 Catalysts

✅ Recent Catalysts (Already Happened)

Q4 2025 Earnings Beat + $200B Capex Shock (February 5, 2026)

Amazon's Q4 results were a tale of two reactions: revenue crushed at $213.4B (+14% YoY) and AWS hit $35.6B with 24% growth - fastest in 13 quarters. But the $200B capex plan for 2026 (vs ~$147B expected) sent the stock tumbling. Analysts noted this is the year Amazon either proves AI monetization is real, or burns cash on a massive bet. The current ~$209 price reflects maximum capex fear pricing.

Alexa+ Full U.S. Launch (February 4, 2026)

Amazon auto-enrolled all Prime members in Alexa+, the generative AI assistant powered by Amazon Nova and Anthropic Claude. Free for Prime subscribers, $19.99/month standalone. With 315M+ Prime Video viewers globally, this is a distribution moat no AI startup can replicate overnight.

$53B Record Bond Offering (March 10-11, 2026)

Amazon raised $37B in U.S. dollar bonds followed by €14.5B in euro bonds - the fourth-largest U.S. corporate bond sale ever, drawing $126B+ in orders. They got the money they needed at good rates. This removes near-term financing risk for the AI buildout.

AWS-Cerebras Partnership (March 13, 2026)

This is the one that likely triggered today's institutional buy. AWS will integrate Cerebras' WSE-3 wafer-scale chips into Amazon Bedrock, delivering 5x faster AI inference. Amazon is the first cloud provider to offer this disaggregated inference solution, with Amazon Bedrock integration expected within a few months. Speed matters enormously for enterprise AI adoption - this is a real competitive differentiator vs Azure and GCP.

Prime Video Ultra Rebrand (March 13, 2026)

Amazon rebranded its ad-free Prime Video tier as "Prime Video Ultra" with a 67% price increase from $2.99 to $4.99/month, effective April 10. New perks include 5 concurrent streams and 100 offline downloads. Pure margin expansion with minimal churn risk given the ecosystem lock-in.

$50B Government & Defense AI Expansion (2026)

Amazon committed up to $50 billion to expand AI and supercomputing capacity for AWS U.S. government customers, with construction beginning in 2026. The buildout adds approximately 1.3 GW of AI capacity across Top Secret, Secret, and GovCloud regions — a massive, locked-in revenue stream that insulates AWS growth from commercial market volatility.

🔥 Upcoming Catalysts (Key Dates Ahead)

| Date | Event | Why It Matters |

|---|---|---|

| March 20, 2026 | Quarterly Triple Witch expiration | High-volume options expiry; gamma dynamics shift significantly after this |

| April 10, 2026 | Prime Video Ultra launches | Immediate subscription revenue increase |

| Late April 2026 (est. Apr 23-30) | Q1 2026 Earnings | THE big event - AWS growth rate, capex cadence, tariff commentary. Consensus: $173.5-178.5B revenue |

| May-June 2026 | Cerebras/Bedrock AI inference live | Real-world 5x speed advantage starts converting enterprise customers |

| July 2026 | Prime Day 2026 | Major retail event catalyst |

| July 30, 2026 | Amazon Leo (Kuiper) FCC deadline | Must have half Gen1 satellite constellation operational |

| October 2026 | FTC Antitrust Trial begins | Major structural risk event |

The May 15 call expiration is positioned perfectly to capture Q1 earnings in late April - the single most important catalyst for validating (or deflating) Amazon's AI spending thesis.

🎲 Price Targets & Probabilities

Using gamma levels, the implied move framework, upcoming catalysts, and current analyst consensus:

📈 Bull Case (35% probability) - Target: $225-$235

How we get there by May 15:

- 💪 Q1 2026 earnings in late April shows AWS holding or accelerating past 24% growth, squashing the "capex with no monetization" bear thesis

- 🚀 Cerebras/Bedrock launches on schedule in May-June window, attracting enterprise AI workload announcements

- 🎯 Prime Video Ultra launches April 10 with minimal subscriber churn, demonstrating pricing power

- 📊 Tariff commentary from Andy Jassy is measured - Amazon captures share from weaker competitors as Jassy suggested is possible

- 🔑 Gamma analysis: Break above $215 (79.8 GEX wall) triggers mechanical buying as dealers rehedge; next stop is the $220 zone (91.3 GEX)

- 📈 Analyst consensus target of $282-$287 gives plenty of room; even a partial re-rating toward $225-$235 returns strong profits on the $210 calls

Call P&L in Bull Case (on the $210 calls at ~$13.50 average cost):

- AMZN at $225 on May 15: Calls worth ~$15.00, gain of ~$1.50/share × 19,490 contracts × 100 = ~+$2.9M

- AMZN at $230 on May 15: Calls worth ~$20.00, gain of ~$6.50/share × 19,490 contracts × 100 = ~+$12.7M

- AMZN at $235 on May 15: Calls worth ~$25.00, gain of ~$11.50/share × 19,490 contracts × 100 = ~+$22.4M

🎯 Base Case (45% probability) - Target: $210-$220 (Range-Bound Through Earnings)

Most likely scenario:

- ✅ AMZN drifts between $210-$220 as the market waits for Q1 earnings clarity

- 📊 Triple Witch this Friday keeps stock pinned to the $205.99-$216.81 implied range

- 🔄 Q1 earnings meet consensus (not a blowout, not a disaster) - AWS stays at ~24%, capex commentary reaffirms $200B plan

- 💤 Options show $210-$215 as the gamma gravity zone - stock naturally gravitates here

- 📉 The $210 calls hover near breakeven through much of the 60-day period before an earnings pop gives them life near expiry

- ⚖️ The call buyer likely happy to hold through any consolidation given the 60-day window

📉 Bear Case (20% probability) - Target: $195-$205 (Support Tested)

What could go wrong:

- 😰 Q1 guidance disappoints - if operating income guidance comes in below $16.5B floor, the capex-drag thesis gets worse

- 🇺🇸 Tariff escalation hits North America e-commerce segment harder than expected; consumer trade-down accelerates

- ☁️ Azure or GCP announces major enterprise AI contract wins that cast doubt on AWS's Cerebras advantage

- 💸 Broader tech selloff in macro risk-off environment (recession fears, rate concerns) weighs on the entire sector

- 🔨 Break below $210 gamma support (75.6 GEX) leads to test of $205 and potentially $200 (the 55.6 GEX wall)

- 📊 At the $200 level, put gamma dominates strongly (-30.1 net GEX) and dealers become mechanical stock buyers, creating a natural floor

Call P&L in Bear Case:

- AMZN at $205 on May 15: Calls worth ~$2.00, loss of ~$11.50/share × 19,490 contracts × 100 = -$22.4M

- AMZN at $200 on May 15: Calls expire nearly worthless, loss approaches full $26M premium

💡 Trading Ideas

🛡️ Conservative: "Wait for the Wall Break"

Play: Watch for AMZN to break and close above $215 before entering any long options position

Why this works:

- 🎯 The $215 level carries the strongest nearby resistance (79.8 total GEX). A confirmed close above it would represent a real technical breakout and suggest the gamma headwinds have been overcome

- 📊 If you want stock exposure, a covered call or simply buying AMZN shares on a pullback to the $205-$210 support zone gives defined risk

- 💤 The "sleep well" version: wait until AFTER Q1 earnings to enter any bullish AMZN options, buying after the IV crush drops premiums significantly

- ✅ If you do enter early, consider buying the June 2026 $215 call (out-of-the-money, costs less premium, gives 30+ days post-earnings)

- 📉 Stop logic: if AMZN closes below $200 (breaks the major 55.6 GEX floor), the thesis is broken - exit

Risk level: Low-Moderate | Skill level: Beginner-friendly

Expected outcome: Lower probability of maximum profit, but significantly higher probability of preserving capital if the trade goes sideways.

⚖️ Balanced: "Copy the Whale, Smaller Size"

Play: Buy the AMZN May 2026 $210 calls - same contract as today's institutional trade

Structure: Buy AMZN20260515C210 at market (currently ~$13.45-$13.55)

Why this works:

- 🤝 You're directly aligning with the institutional thesis - same strike, same expiry, with a known large player holding a $26M position in this exact contract

- 📅 The 60-day window captures Q1 earnings (the single biggest catalyst) plus early Cerebras/Bedrock momentum

- 🎯 At-the-money calls give you the most leverage per dollar if AMZN moves up; $215+ break by late April could easily double the option value

- 📊 Wells Fargo's $304 price target and Argus Research's $325 target mean the analyst community is firmly in the bull camp

- ⚖️ Cost: ~$1,355 per contract (manageable for most portfolios) - consider 1-3 contracts rather than 19,490!

P&L scenarios (per contract):

- 💰 AMZN at $225 by May 15: ~+$150 gain (+11%)

- 🚀 AMZN at $230 by May 15: ~+$650 gain (+48%)

- 💀 AMZN stays below $210 at May 15 expiry: -$1,355 (full premium lost)

Position sizing: Risk no more than 3-5% of portfolio. These are at-the-money calls with real time decay (~$15-20 theta per day per contract).

Risk level: Moderate | Skill level: Intermediate

🚀 Aggressive: "Bull Call Spread - Defined Risk to $230"

Play: Buy the May 2026 $210 call and sell the May 2026 $230 call to reduce cost

Structure: Long AMZN20260515C210 / Short AMZN20260515C230

Why this works:

- 💸 Cuts cost dramatically - selling the $230 call (approximately $6-7) brings the net debit down from ~$13.50 to ~$6.50-$7.50 per spread

- 🎯 $230 is a rational target - sits just below the $230 gamma resistance level (43.9 GEX) and represents a ~10% rally from current levels - very achievable in 60 days if earnings impress

- ⚖️ Max profit: $20 spread width minus ~$7 cost = ~$13 gain per spread at $230+, roughly 1.85x return

- 🛡️ Max loss: Limited to the ~$7 net debit per spread (vs $13.50 for the naked call)

- 📈 Breakeven: ~$217 (only needs 4% rally from current $208-209 to breakeven by expiry)

- 🎰 Can size up with the same dollar risk as a single naked call but get 2 spreads instead, improving capital efficiency

Estimated P&L per spread:

- 💰 AMZN at $220 on May 15: Spread worth ~$10.00, gain ~$3.00 (+43%)

- 🚀 AMZN at $230+ on May 15: Spread worth $20.00 (max), gain ~$13.00 (+186%)

- 💀 AMZN below $210 on May 15: Lose $7.00 (full spread premium)

IMPORTANT: This caps your upside at $230. If AMZN rips to $240 on blowout earnings, you don't participate above $230. For a stock with analyst targets of $282-$325, that's a real trade-off worth considering.

Risk level: High (but defined) | Skill level: Intermediate-Advanced

⚠️ Risk Factors

Don't go in without understanding what could go wrong:

-

📉 Q1 earnings disappointment is the single biggest risk: Consensus calls for $173.5-178.5B revenue and $16.5-21.5B operating income from Amazon's own guidance. If AWS growth decelerates below 20%, the stock could revisit its $195-200 zone and the calls expire significantly underwater.

-

💸 Time decay is relentless for ATM calls: At ~$13.50 for at-the-money options, AMZN is burning roughly $15-20/day in theta per contract just to stand still. If the stock goes nowhere for 30 days, you've lost roughly $450-600 per contract before anything else moves. The whale can afford to wait - make sure you can too.

-

🇺🇸 Tariff headwinds are real and escalating: CEO Andy Jassy explicitly said tariffs have started to "creep" into prices and third-party sellers (60%+ of marketplace) are seeing margin compression. If tariff policy escalates further before May, it hits AMZN's North America segment and could weigh on Q1 results.

-

💰 The $200B capex overhang won't disappear: The market has already repriced AMZN down ~18% from highs partly because of this. Unless Q1 shows demonstrable AI monetization (AWS growth accelerating further, Bedrock enterprise wins), the capex-skeptic narrative will persist through the option's life.

-

⚖️ FTC antitrust trial approaching (October 2026 / possibly February 2027): While outside this trade's timeframe, the bench trial on monopoly power allegations creates a structural overhang that could weigh on valuation multiples even before the verdict.

-

☁️ Cloud competition is intensifying: Azure with OpenAI and Google Cloud with TPU/Gemini are both closing the gap with AWS on AI workloads. The Cerebras partnership needs to demonstrably move the needle in enterprise AI wins before this becomes a consensus narrative.

-

📊 Gamma ceiling at $215 creates real friction: The strongest nearby resistance is at $215 (79.8 total GEX). Getting through that requires sustained institutional buying, not just a one-day pop. Expect multiple tests before a confirmed breakout.

🎯 The Bottom Line

Real talk: When a single player drops $26 million in two tranches 53 seconds apart, hitting the ASK both times in a near-the-money call that expires right after Q1 earnings - that's conviction, not coincidence. They did the math on AMZN's catalyst lineup: Q1 earnings, Cerebras/Bedrock launch, Prime Video Ultra revenue boost, and $53B in fresh capital already in the bank. They looked at the stock sitting 18% off all-time highs with a forward P/E of ~29x (well below Amazon's historical average of 81x) and decided this was the moment to load up.

What this trade tells us:

- 🎯 An institutional player has a specific timeline thesis: AMZN breaks higher before May 15, likely catalyzed by late April Q1 earnings

- 💰 The $210 strike sitting right on the $210 gamma support cluster is deliberate - they picked the inflection point where bulls and bears fight it out

- ⏰ The 60-day window is tight enough for urgency but long enough to absorb any near-term Q1 preview noise and Triple Witch this Friday

- 📊 Analyst consensus implies 33-36% upside from current levels - even a partial move toward targets turns these calls into a significant winner

If you're bullish on AMZN:

- ✅ Respect the $210 gamma support level - as long as AMZN holds above it, the path of least resistance is higher given the bullish net GEX bias

- 📊 Watch the $215 resistance break carefully - a confirmed close above it opens the door to $220 and beyond

- ⏰ Mark your calendar for late April Q1 earnings - that's the binary event that either validates or breaks this trade's thesis

- 🎯 Consider scaling in after Triple Witch Friday when near-term gamma dynamics reset

If you're watching from the sidelines:

- 👀 Wait for a confirmed break above $215 before entering - don't chase the first pop

- 📅 Earnings in late April is the true decision point; there may be a better entry (post-Triple Witch or after any Q1 preview newsflow)

- 🤔 If you want AMZN exposure without options complexity, the stock at ~$209 with $200 as a clear floor and analyst consensus at $282-$287 offers a reasonable risk/reward in the stock itself

If you're skeptical:

- ⚠️ The $200 level (55.6 total GEX with heavy put gamma) is your signal - a weekly close below $200 would indicate the bull thesis is materially broken

- 📉 The $200B capex plan without clear near-term monetization is a legitimate bear concern that won't resolve until Q1 earnings at the earliest

Mark your calendar for key dates:

- 📅 March 20, 2026 - Quarterly Triple Witch expiration (gamma dynamics reset)

- 📅 April 10, 2026 - Prime Video Ultra launches (revenue catalyst starts)

- 📅 Late April 2026 (est. Apr 23-30) - Q1 2026 earnings - THE moment of truth for this trade

- 📅 May 15, 2026 - This $26M call position expires; options holders need to see a move above ~$223-$224 to break even at the average $13.50 cost

Final verdict: Amazon's long-term story around AWS AI infrastructure, Alexa+, advertising growth, and Cerebras-powered inference leadership is as strong as it has been in years. The capex shock is real, but at ~$29x forward earnings vs an 81x historical average, a lot of fear is already baked in. Today's $26M institutional call buy says someone thinks the market is overly pessimistic. Whether they're right depends almost entirely on what AWS growth looks like when Q1 earnings hit.

Patience is the edge here. The trade is set. Now we watch the levels.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational and informational purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Past performance of institutional trades or options positions does not guarantee future results. The at-the-money call options described carry significant time decay risk and can expire worthless if the underlying stock does not move sufficiently in the required direction within the specified timeframe. Amazon stock is subject to earnings risk, macroeconomic risk, competitive risk, and regulatory risk as described above. Always do your own research, understand the full risk of any position, and consider consulting a licensed financial advisor before trading options.

About Amazon.com Inc: Amazon.com operates as a technology and retail conglomerate with three primary businesses: AWS cloud computing (~31% global cloud market share, $142B annualized revenue run rate), North American and international e-commerce (~38-40% U.S. e-commerce share), and a $68.6B advertising platform. The company is executing a $200B AI infrastructure investment in 2026, funded in part by a record $53B bond offering completed in March 2026. Market cap: $2.23 Trillion.