💎 ASTS $1.3M Call Close - Smart Money Exits Ahead of Critical BlueBird 6 Launch! 🛡️

📅 December 23, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just closed $1.3 MILLION worth of ASTS calls this morning at 10:05:50 - buying back 3,500 contracts of January $100 strike calls in a BTC (Buy to Close) order. With ASTS trading at $85.20 and the stock down from its October all-time high of $102.79, this trader is locking in profits or cutting losses ahead of TODAY'S critical BlueBird 6 satellite launch at 10:24 PM EST. Translation: Institutional money is derisking before the most important catalyst in company history!

📊 Company Overview

AST SpaceMobile (ASTS) is pioneering the satellite-to-phone revolution, building the infrastructure to deliver cellular broadband directly to unmodified smartphones from space:

- Market Cap: $24.04 Billion

- Industry: Communications Services (Satellite Technology)

- Current Price: $85.20 (down 17% from October ATH of $102.79)

- Primary Business: Space-based cellular broadband networks connecting standard mobile phones without device modifications

- Core Technology: Massive phased array satellites (2,400 sq ft) with 100x bandwidth advantage over competitors

What they do: ASTS manufactures and deploys satellites featuring the largest commercial communications arrays in low Earth orbit. Their spaceMobile Service targets the 5+ billion mobile subscribers globally who experience connectivity gaps, partnering with 45+ mobile network operators serving 2.8 billion total subscribers. Think of it as turning space into a giant cell tower that works with your existing iPhone or Android.

💰 The Option Flow Breakdown

The Tape (December 23, 2025 @ 10:05:50):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | Spot Price | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|

| 10:05:50 | ASTS | BTC | BUY | CALL $100 | 2026-01-16 | $1.3M | $100 | 3,500 | $85.20 | ~$371 |

🤓 What This Actually Means

This is a CLOSING TRADE - someone who previously sold these calls is now buying them back to exit the position! Here's the breakdown:

- 💸 Large premium paid: $1.3M to close 3,500 contracts ($371 per contract approximately)

- 🎯 Strike selection: $100 strike sits 17.4% above current $85.20 price - way out of the money

- ⏰ Critical timing: Executed just 12 hours before BlueBird 6 launch (10:24 PM EST tonight!)

- 📊 Position type: BTC (Buy to Close) means exiting a previously opened short call position

- 🛡️ Risk management: Trader is unwinding exposure before binary catalyst event

- 📈 Z-Score 1.12: Above average activity but not extreme - represents 211x typical daily volume

What's really happening here: This trader likely SOLD these $100 calls when ASTS was trading near its $102.79 all-time high in October. At that point, with the stock above $100, these calls were in-the-money or near-the-money. Now with ASTS at $85.20, the calls are worth much less (out-of-the-money), so closing them locks in profit from the premium collected when selling.

BUT - why close TODAY, 24 days before expiration? BlueBird 6 launches TONIGHT. If the launch succeeds spectacularly, ASTS could gap higher 20-30% tomorrow, putting these $100 calls back in play. Rather than risk getting assigned or watching profits evaporate on a launch success rally, this trader is taking chips off the table BEFORE the binary event.

Unusual Score: 🔥 ABOVE AVERAGE (211x typical size) - This happens maybe once a week. Z-score of 1.12 shows elevated but not extreme positioning. The timing is more notable than the size - closing 12 hours before the most important catalyst in company history sends a clear message: smart money doesn't want exposure to tonight's launch outcome.

📈 Technical Setup / Chart Check-Up

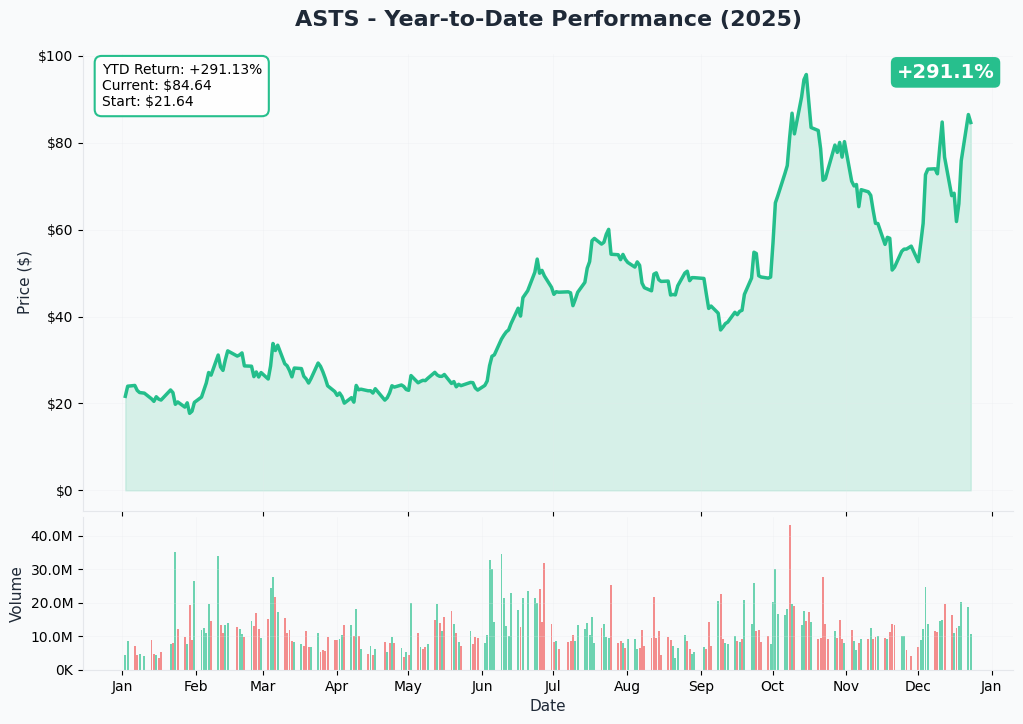

YTD Performance Chart

ASTS has delivered explosive returns - up +250% YTD through 2024, though currently trading 17% below its October 2025 peak. The chart tells a volatile space-race story - the stock surged from $17.50 lows in early 2024 to an all-time high of $102.79 on October 16, 2025, before pulling back to the current $85 range.

Key observations:

- 🚀 Parabolic rally: Vertical move from $20s in August to $100+ in October on Verizon partnership and satellite deployment news

- 📈 Extreme volatility: 52-week range of $17.50-$102.79 (488% spread!) shows this isn't for the faint of heart

- 🎢 Whipsaw action: October +64%, November -30% demonstrates wild sentiment swings

- 📊 Current consolidation: Trading in $80-90 range for past 6 weeks as market awaits BlueBird 6 catalyst

- ⚠️ Pre-revenue valuation: $24B market cap on minimal revenue creates massive risk/reward asymmetry

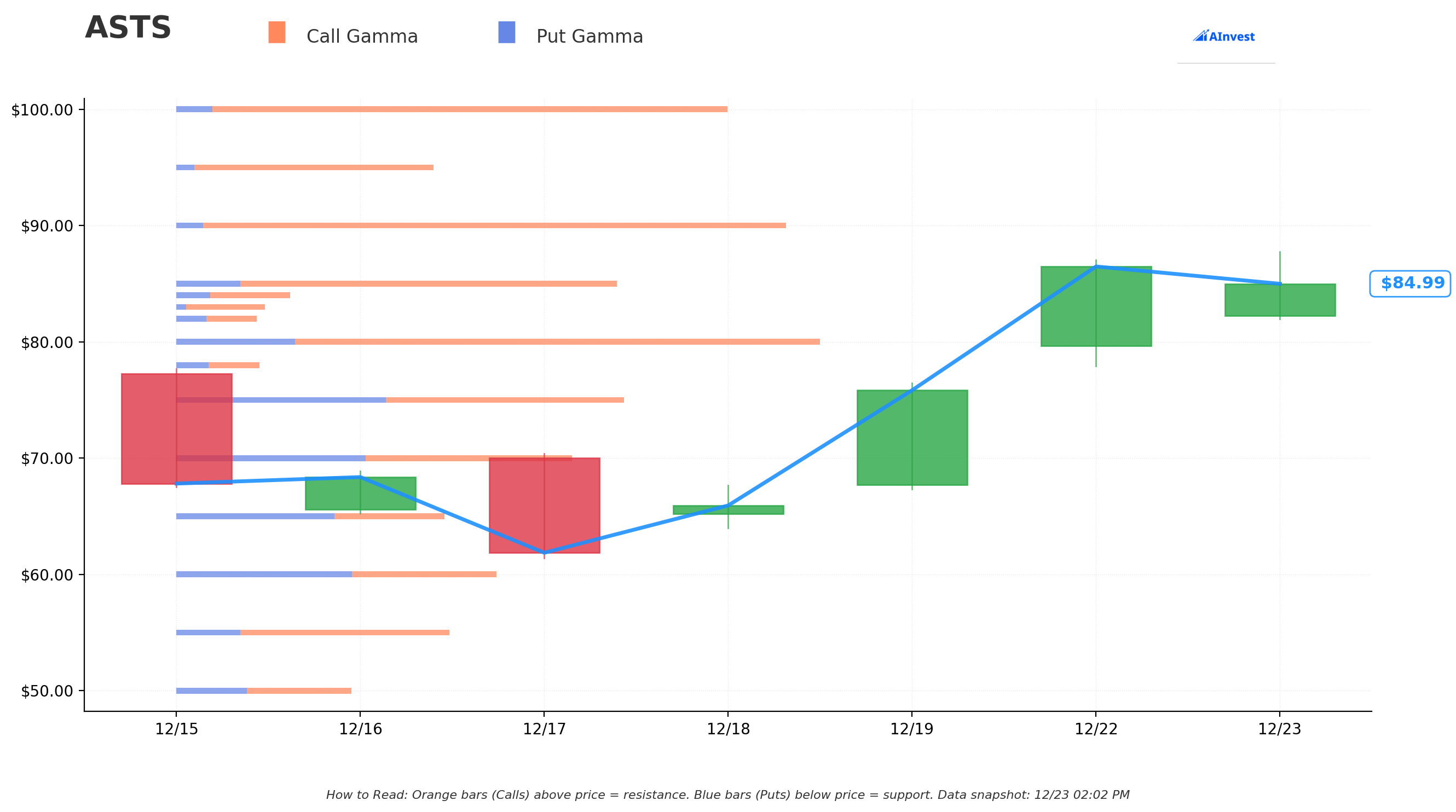

Gamma-Based Support & Resistance Analysis

Current Price: $85.20

The gamma exposure map reveals critical price magnets where options activity concentrates:

🔵 Support Levels (Put Gamma Below Price):

- $66.00 - Put Wall (major floor with heaviest put concentration)

- $64.00 - Secondary support level

- $63.00 - Additional put gamma accumulation

- $62.00 - Extended support zone

- $61.00 - Deep support floor

🟠 Resistance Levels (Call Gamma Above Price):

- $80.00 - Call Wall (heaviest call concentration - currently trading ABOVE this!)

- Minimal resistance above $85 - Limited options activity capping upside

What this means for traders: ASTS has already broken ABOVE the major $80 Call Wall, which typically would create selling pressure. This suggests institutional buyers absorbed supply and cleared the technical resistance. However, the lack of significant call gamma above $85 means there's no natural ceiling - the stock can move violently in either direction post-launch without options market makers providing stability.

The massive Put Wall at $66 (22.5% below current price) represents catastrophic downside protection. If BlueBird 6 launch fails or encounters major issues, that's likely the initial panic-selling target. The clustering of put strikes at $61-66 shows sophisticated players hedging for a potential 25-30% crash scenario.

Net GEX Bias: Bearish (negative net gamma at key levels) - This creates unstable price action where moves in either direction can accelerate. With limited dealer hedging activity, retail speculation dominates, amplifying volatility.

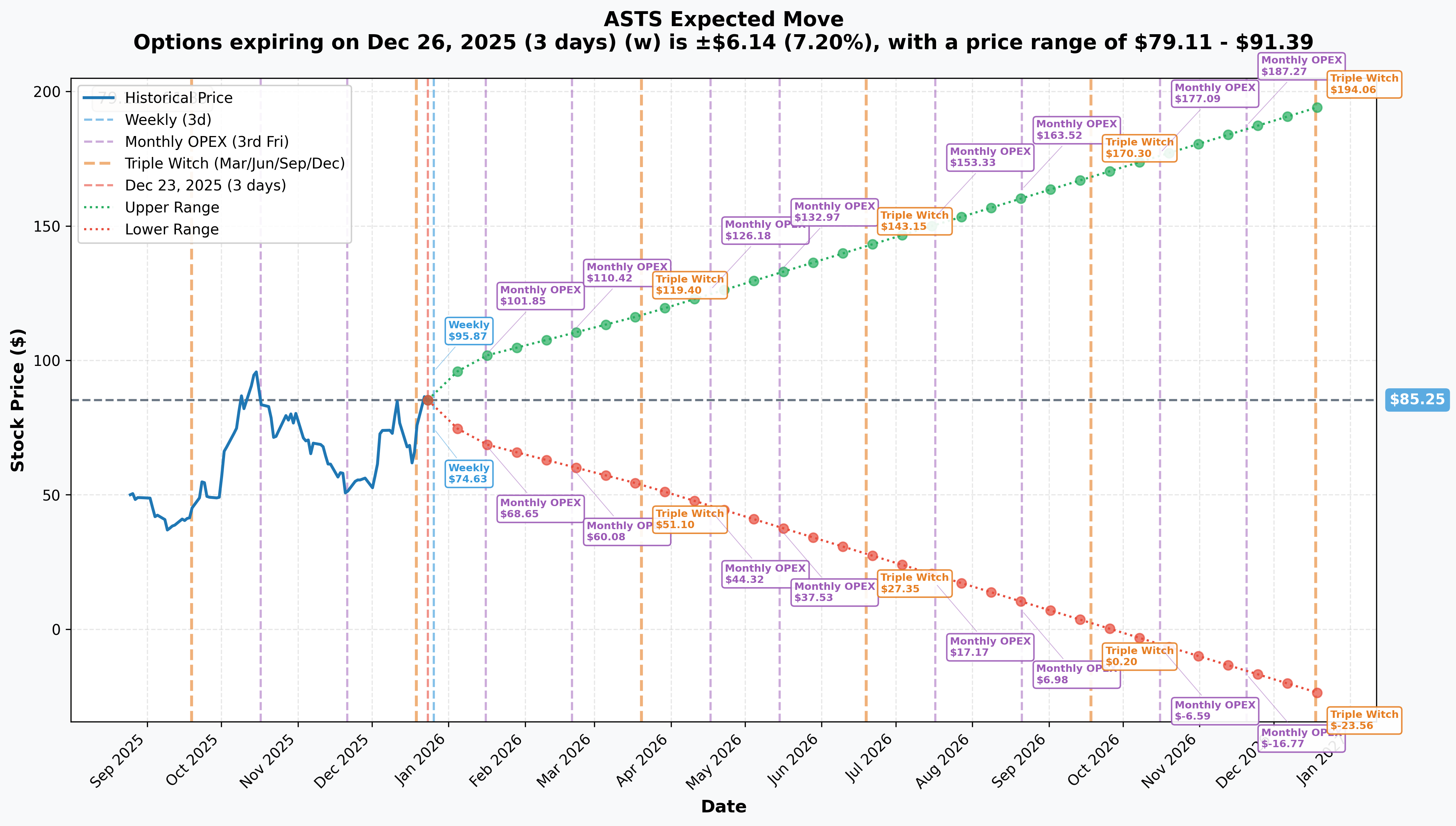

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 26 - 3 days): ±$6.14 (±7.2%) → Range: $79.11 - $91.39

- 📅 Monthly OPEX (Jan 16 - 24 days - THIS TRADE!): ±$16.60 (±19.47%) → Range: $68.65 - $101.85

- 📅 Quarterly (Mar 20 - 87 days): ±$31.60 (±37.07%) → Range: $53.65 - $116.85

Translation for regular folks: Options traders are pricing in a 7.2% move ($6) by this Friday - that's HUGE for just 3 days and reflects BlueBird 6 launch volatility expectations. The market expects ASTS could trade anywhere from $79 to $91 by week-end based on launch outcome and initial satellite performance data.

For the January 16th expiration (when this $100 call expires), implied volatility prices in a 19.5% move - with the upper range at $101.85. This means the options market gives meaningful probability to ASTS reclaiming $100+ if BlueBird 6 launch succeeds AND beta testing with AT&T/Verizon shows commercial promise.

Key insight: The 7.2% weekly implied move is exceptional for a $24B market cap stock. This is binary event volatility typically reserved for biotech FDA decisions or earnings from early-stage growth companies. The market is pricing in 50/50 odds of SIGNIFICANT movement tonight.

🎪 Catalysts

🔥 Immediate Catalysts (Next 7 Days)

BlueBird 6 Launch - TONIGHT! December 23, 2025, 10:24 PM EST 🚀

ASTS's most critical catalyst in company history happens in just 12 hours. BlueBird 6 launches tonight from India's Satish Dhawan Space Centre aboard an LVM3 rocket, marking the transition from Block 1 demonstration satellites to next-generation Block 2 commercial satellites.

Why this matters SO MUCH:

- 🛰️ Technology leap: 2,400 sq ft phased array (3.5x larger than BlueBird 1-5 satellites launched in September)

- 💪 10x capacity: Each Block 2 satellite delivers 10x the data throughput vs Block 1 satellites

- 🎯 Commercial readiness: Block 2 represents the production design for the 45-60 satellite constellation planned by end-2026

- 💰 Capital efficiency validation: At $22M per satellite (vs competitors' costs), successful deployment proves manufacturing scalability

- 📊 Institutional confidence test: Multiple launch delays (Dec 15 → Dec 21 → Dec 23) have tested investor patience - successful launch critical for credibility

What to watch for:

- ✅ Successful liftoff and orbital insertion: Confirmation within 1-2 hours of launch

- 📡 Array deployment: Unfolding of massive 2,400 sq ft phased array over next 2-4 weeks (BlueBird 1-5 took 3 weeks)

- 📞 First signal acquisition: Successful communication with ground stations

- 🎯 Initial performance metrics: Early data on throughput capacity and connection quality

Historical context: When BlueBird 1-5 deployed successfully ahead of schedule in October 2024, the stock surged 64% in a single month. However, when delays were announced in December, the stock dropped 11.6% in one day. This binary sensitivity shows why the BTC call trade makes sense - traders don't want exposure to this volatility.

Downside risk: Supply chain issues caused previous delays with production problems affecting solar panel and antenna "Microns" components. Any anomaly during launch, deployment, or initial testing could trigger 20-30% selloff toward that $66 Put Wall.

🚀 Near-Term Catalysts (Next 3-6 Months)

Commercial Beta Service Launch with AT&T & Verizon (Late December 2025)

ASTS plans to initiate beta testing of direct-to-device cellular service by year-end 2025 using the BlueBird 1-5 constellation. This represents the first revenue-generating commercial service in company history.

What's involved:

- 📱 Service capabilities: 4G/5G voice, data, and video directly to unmodified smartphones

- 📊 Coverage area: Approximately 100% nationwide coverage with 5,600+ coverage cells across the U.S.

- 🚀 Peak speeds: Up to 120 Mbps demonstrated in testing

- 💰 Carrier partnerships: Sharing 700-850 MHz spectrum from AT&T and Verizon

- 🎯 FCC status: Operating under Special Temporary Authority granted in January 2025 - full commercial approval pending

Revenue implications: While beta services generate limited revenue, they provide critical proof-of-concept data validating the $50-75M H2 2025 revenue guidance. Successful beta testing with paying carrier partners would be the first evidence that the business model works at commercial scale.

Key risks: Beta testing launches before BlueBird 6 deploys, meaning initial service uses just the Block 1 satellites with 1/10th the capacity of Block 2. Customer experience may not reflect full network capabilities, creating uncertainty around final service quality and pricing power.

Q1 2025 Earnings - Expected April 7, 2025 📊

First quarter with potential beta testing revenue showing up in financials. This earnings report will provide critical visibility into:

- 💵 Revenue trajectory: Progress toward $50-75M H2 2025 guidance

- 🏭 Manufacturing execution: Status of 40 Block 2 satellite production at Midland, Texas facility

- 💸 Burn rate management: Q3 2024 showed $66.6M quarterly operating expenses vs $14.74M revenue - investors watching for path to profitability

- 🚀 2026 launch cadence: Confirmation of "every 45 days" satellite deployment schedule

- 📡 Service metrics: Customer acquisition, network performance, carrier feedback from beta testing

Aggressive 2026 Launch Schedule (Every 45 Days Starting Q1)

Management targets deploying 45-60 satellites by end-2026 through an aggressive launch cadence unprecedented for the company.

The execution challenge:

- 🏭 Production ramp: Manufacturing 40+ satellites in 12-18 months vs 5 satellites over prior 2+ years (8x acceleration!)

- 🚀 Launch dependency: Secured SpaceX launch contracts but competing for Falcon 9 capacity with Starlink, NASA, and commercial customers

- 💰 Capital intensity: $22M per satellite × 40 satellites = $880M capex requirement through 2026

- 🛠️ Supply chain risk: Previous delays stemmed from component supplier issues - scaling 8x increases dependency on third parties

Why this matters: The entire bull thesis depends on achieving scale. With just 5-6 satellites, ASTS can provide limited beta coverage. With 25+ satellites, they claim path to free cash flow positive. With 45-60 satellites, they can deliver continuous global coverage supporting the $2.2B revenue projection for 2028.

Any delays to this launch cadence would push out revenue ramps and require additional dilutive capital raises, potentially cutting the current $85 stock price in half.

📊 Strategic Revenue Catalysts

H2 2025 Revenue Guidance: $50-75M

Management projects first meaningful commercial revenue in second half of 2025, a massive inflection from Q3 2024's $14.74M quarterly revenue.

Revenue composition:

- 🏛️ Government contracts: $43M Space Development Agency (SDA) contract provides base revenue

- 📡 Gateway installations: Telecom partners paying for ground infrastructure (stc Group building 3 gateways in Saudi Arabia)

- 📱 Service revenues: Early beta/commercial revenue from AT&T, Verizon, and potentially international carriers

- 💼 Equipment sales: Hardware and licensing to carrier partners

Why this is CRITICAL: Current $24B market cap prices in aggressive growth expectations. Missing the $50-75M target or showing weak margins would validate bears' claims of "excessive valuation" and could trigger 30-40% correction.

Vodafone 10-Year Commercial Agreement (Through 2034)

Announced December 8, 2024, Vodafone committed to a 10-year contract with $25M minimum revenue commitment covering Europe, Africa, and Vodafone partner markets.

Strategic significance:

- 🌍 Geographic expansion: Validates ASTS technology for international markets beyond U.S. carriers

- 💰 Revenue floor: $25M minimum guarantees baseline revenue stream

- 🤝 Three-time investor: Vodafone has been strategic partner/investor since 2018 - contract demonstrates long-term confidence

- 📈 Upside potential: Agreement structured with usage-based pricing above minimums - could generate $50M+ annually at scale

stc Group Saudi Arabia Partnership: $175M Prepayment + $1.87B Potential

Massive October 30, 2024 deal with stc Group represents ASTS's largest commercial contract:

- 💵 Upfront capital: $175M prepayment for future services (non-dilutive funding!)

- 🎯 Total contract value: Revenue-sharing model potentially exceeding $1.87B over 10 years

- 🌍 Exclusive territories: Libya, Syria, Lebanon, Djibouti, Tunisia, Sudan

- 🏗️ Infrastructure buildout: Three ground gateways in Saudi Arabia with Network Operations Center in Riyadh

- 📅 Service launch: Q4 2026 targeted commercial service activation

Why this changes everything: The $175M prepayment alone funds 8+ satellites ($22M each), demonstrating that carrier partners are willing to pre-fund network buildout. This reduces ASTS's need for dilutive equity raises and validates that carriers see strategic value worth billions.

⚠️ Risk Catalysts (Negative)

Continued Capital Raises & Dilution Risk 💸

ASTS burns cash at alarming rates while pursuing the most capital-intensive satellite constellation buildout in commercial space history.

The brutal math:

- 🔥 Current burn: Q3 2024 operating expenses $66.6M vs revenue $14.74M = -$51.9M quarterly cash burn

- 💰 Cash position: $518.9M as of Q3 2024 - provides ~10 quarters of runway at current burn

- 📊 Capital requirements: $1.32B needed for 60 satellites through end-2026 (vs $518.9M cash)

- 🎯 Funding gap: Needs $800M+ in additional capital over next 24 months

Recent dilutive activities:

- 💵 $800M At-The-Market (ATM) program active allowing ongoing share sales

- 📄 May 2025: $500M prospectus filed for potential equity offering

- 💳 November 2025: $23.9M follow-on offering

- 🔄 Convertible notes from AT&T ($110M), Verizon ($35M), Google ($110M) will add shares when converted

Dilution impact: With 277.6M shares outstanding and $800M+ of potential raises ahead at $85/share, existing shareholders could face 10-15% additional dilution over next 12-18 months. Every equity raise at depressed prices (vs the $102 peak) accelerates dilution and reduces per-share value of future cash flows.

FCC Commercial Approval Uncertainty 📡

Despite FCC granting Special Temporary Authority in January 2025, full commercial authorization for terrestrial spectrum use (700 MHz/850 MHz) remains pending.

The regulatory challenge:

- ⏰ Timeline unknown: FCC deferred decision on commercial satellite-to-cell services in terrestrial frequencies as of November 2024 - no clarity on final approval timing

- 📻 Amateur radio opposition: Concerns raised about interference on 430-440 MHz frequencies

- 🛰️ Collision risk: NASA filed letter in October 2020 expressing collision concerns with A-train satellite constellation

- 🌍 International approvals: Each market (Europe, Japan, Saudi Arabia, etc.) requires separate regulatory authorization

Why this matters: Beta testing under temporary authority is fine for proof-of-concept, but scaled commercial service generating $50-75M H2 2025 revenue REQUIRES full FCC approval. Any delays or restrictions on spectrum usage could push revenue timelines right and force additional capital raises, cratering the stock 30-50%.

Starlink Direct-to-Cell Competition 🚀

SpaceX announced direct-to-device satellite service with T-Mobile, creating a formidable competitor with massive resource advantages.

Starlink's competitive threats:

- 🏭 Vertical integration: SpaceX manufactures satellites AND launches them on Falcon 9 - no third-party dependencies

- 🚀 Launch capacity: Can deploy satellites faster given control of launch schedule

- 📡 Installed base: Thousands of Starlink satellites already in orbit provide infrastructure base

- 💰 Capital access: SpaceX valuation >$150B provides unlimited funding for satellite buildout

- 🤝 T-Mobile partnership: Third-largest U.S. carrier provides instant distribution and spectrum access

ASTS's counterarguments:

- 💪 100x bandwidth advantage: 2,400 sq ft arrays deliver ~100x the capacity per satellite vs Starlink's smaller direct-to-cell satellites

- 📱 Full broadband capability: Voice, data, video from day one vs Starlink's phased rollout starting with text messaging

- 🌍 MNO partnerships: 45+ carriers serving 2.8B subscribers vs Starlink's 7 carrier deals

- 📜 Patent portfolio: 3,450+ patents may create IP moat

Reality check: In a race between the tortoise (ASTS's superior technology but slower deployment) and the hare (Starlink's faster execution but lower per-satellite capability), SpaceX's track record of aggressive execution poses existential risk. If Starlink achieves critical mass first, carrier partners may pivot away from ASTS, stranding invested capital.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through January 16th expiration:

📈 Bull Case (30% probability)

Target: $100-$116

How we get there:

- 🚀 BlueBird 6 launch PERFECT tonight - flawless liftoff, orbital insertion, and initial telemetry

- 📡 Array deployment completes ahead of schedule (within 2-3 weeks vs 4-week estimate)

- 💪 Initial performance tests show 10x capacity improvement validated - full 2,400 sq ft array functioning

- 📱 Beta testing with AT&T/Verizon launches successfully by year-end with positive customer feedback

- 💰 Q1 2025 earnings show strong progress toward H2 2025 $50-75M revenue guidance

- 🤝 Additional carrier partnership announcements (Japan's Rakuten, Bell Canada service launches)

- 🏭 Manufacturing ramp confirmed with next 3-4 satellites on schedule for Q1 2026 launches

- 🎯 FCC signals imminent full commercial approval for terrestrial spectrum usage

Key metrics needed:

- BlueBird 6 operational within 30 days of launch

- Beta service peak speeds >100 Mbps demonstrated

- Q1 revenue >$20M showing acceleration

- Zero additional launch delays announced

- Manufacturing capacity validated at 1 satellite/month production rate

Technical setup: Break above $90-95 triggers squeeze toward old $102.79 all-time high. Quarterly implied move upper range of $116.85 represents the moonshot scenario if everything goes right AND market re-rates the stock on commercial validation.

Probability assessment: Only 30% because it requires FLAWLESS execution across multiple vectors with zero setbacks. ASTS has history of delays and execution challenges. Current $24B market cap already prices in significant success, leaving limited margin for "meets expectations" scenarios.

🎯 Base Case (45% probability)

Target: $70-$90 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ BlueBird 6 launches successfully with nominal orbital insertion and initial communications

- 📡 Array deployment takes 3-4 weeks (in-line with expectations, not ahead of schedule)

- 📊 Initial performance data promising but needs 60-90 days of testing for full validation

- 📱 Beta testing launches but limited initial scale - hundreds of users, not thousands

- ⚖️ Q1 2025 earnings show progress but revenue still minimal ($15-20M) - path to H2 guidance unclear

- 🏭 Manufacturing progressing but with typical supply chain hiccups delaying 1-2 satellites

- 💸 Additional capital raise announced ($200-300M) causing modest dilution fears

- 📉 Stock trades sideways $70-90 range as market digests progress and awaits next catalysts

- 🎢 Volatility persists with ±10-15% swings on news flow

This is the BTC call trader's target scenario: Stock consolidates below $100 strike, calls expire worthless or with minimal value, and trader pockets the original premium from selling the calls. The $1.3M paid to close is far less than potential loss if stock rallies to $110-120 on launch success.

Why 45% probability: ASTS has demonstrated ability to execute satellite deployments (BlueBird 1-5 succeeded), but timelines consistently slip and scaling remains unproven. With multiple catalysts over next 30 days (launch, deployment, beta testing, Q1 earnings preview), some positive and some neutral news is most likely mix.

Trading pattern: Strong support at $66 Put Wall (22% below current) and resistance around $90-95 (previous consolidation zone). Range-bound action frustrates bulls and bears equally while market awaits commercial revenue proof.

📉 Bear Case (25% probability)

Target: $55-$70 (TEST THE PUT WALL)

What could go wrong:

- 😰 BlueBird 6 launch anomaly - either launch failure, orbital insertion issue, or array deployment problem

- 🚨 Array fails to fully deploy or shows technical issues (partial deployment, communication failures)

- ⏰ Manufacturing delays announced - next satellites slip from Q1 to Q2 2026

- 💸 Larger-than-expected capital raise required ($500M+) causing major dilution concerns

- 📉 Q1 2025 earnings disappoint with revenue <$15M and increased operating expenses

- 🇨🇳 FCC delays commercial approval citing interference concerns or additional testing requirements

- 🌐 Beta testing encounters technical problems - dropped calls, slow speeds, coverage gaps

- 🚀 Starlink announces accelerated direct-to-cell deployment stealing ASTS's narrative

- 💰 Analyst downgrades citing "excessive valuation" like Barclays's October downgrade

- 🔨 Break below $80 triggers technical selling cascade toward $66 Put Wall

Critical support levels:

- 🛡️ $80: Former Call Wall - now initial support (already broken in past)

- 🛡️ $66: Major Put Wall with heavy option concentration - MUST HOLD or panic accelerates

- 🛡️ $61-64: Extended support zone but represents 25-30% crash scenario

- 🛡️ $55: Disaster floor from quarterly implied move lower range ($53.65)

Probability assessment: 25% because ASTS has successfully launched and deployed BlueBird 1-5, showing technical capability exists. However, scaling risks, capital intensity, and regulatory uncertainty create multiple failure points. The market's 7.2% weekly implied move pricing suggests 25-30% odds of significant downside if launch/deployment encounters issues.

Put Wall significance: The massive concentration of puts at $66 (22.5% below current $85) represents catastrophic hedging by institutions. If the stock breaches $70, those puts come into play and market makers hedging their exposure could accelerate selling pressure, creating a feedback loop toward $66.

💡 Trading Ideas

🛡️ Conservative: Cash Gang Until Launch Outcome Clear

Play: Stay on sidelines until BlueBird 6 launch completes and initial data available (48-72 hours post-launch)

Why this works:

- ⏰ Launch happens TONIGHT at 10:24 PM EST - binary event risk with ±7.2% implied move

- 💸 Implied volatility at extreme levels - options massively expensive pre-launch

- 📊 Stock at $85 with no clear technical support until $66 - risking 22% downside for uncertain upside

- 🎯 Better entry likely post-launch after volatility crush reduces option premiums 40-60%

- 📉 Historical pattern: ASTS drops 11.6% on delay news, rallies 15% on positive news - wait for direction

- 🤔 The BTC call trader exiting signals smart money is derisking - why fight the flow?

Action plan:

- 👀 Watch launch livestream tonight for immediate success/failure indication

- 📡 Monitor company announcements Thursday-Friday for orbital insertion and initial telemetry confirmation

- 🎯 Look for entry on pullback to $75-80 range if launch succeeds (10-15% dip on profit-taking)

- ✅ Need to see: Successful launch, orbital insertion, first signal acquisition, no anomalies reported

- 📊 If launch fails: Wait for dust to settle around $60-66 Put Wall for distressed long-term entry

- ⏰ Revisit in early January 2026 when beta testing data and Q1 earnings preview provide fundamentals

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -15-25% drawdown if launch encounters issues. Preserve capital for better risk/reward entry after binary catalyst resolves. Maintain optionality.

⚖️ Balanced: Post-Launch Put Spread (IF Launch Succeeds)

Play: If BlueBird 6 launches successfully, sell put spread to capitalize on elevated volatility and support levels

Structure: Buy $70 puts, Sell $66 puts (January 16 expiration - SAME as the call trade)

Why this works:

- 🎢 IV crush after launch reduces put prices - buy AFTER volatility drops from current extremes

- 📊 Defined risk spread ($4 wide = $400 max risk per spread)

- 🎯 Targets Put Wall at $66 where institutions are heavily hedged - strong support level

- 🛡️ Collecting premium betting stock holds $66 floor over next 24 days

- ⏰ If launch succeeds, stock likely settles $80-90 range, keeping puts safely out-of-money

- 💰 Capitalize on "relief rally" premium after binary event passes

Entry requirements (CRITICAL - do NOT enter before these conditions):

- ✅ BlueBird 6 launches successfully with confirmed orbital insertion

- ✅ No major anomalies reported in first 24-48 hours

- ✅ Stock trading $82-90 range (gives cushion above $70 strike)

- ✅ Implied volatility drops below 60% (currently likely 80-100% pre-launch)

Estimated P&L (adjust after seeing post-launch IV):

- 💰 Collect ~$1.00-1.50 net credit per spread post-launch (vs $2.50-3.00 now)

- 📈 Max profit: $100-150 if ASTS above $70 at January expiration (25-40% ROI)

- 📉 Max loss: $250-300 if ASTS below $66 (defined and limited)

- 🎯 Breakeven: ~$68.50-69.00

Why January 16 expiration: Matches the BTC call trade timing, captures beta testing progress, and includes any Q1 earnings preview commentary. Provides 3+ weeks for stock to stabilize post-launch.

Position sizing: Risk only 3-5% of portfolio (this is directional speculation on support holding)

Exit plan:

- 🎯 Take profits at 50-60% max gain (don't be greedy)

- ⏰ Close 1 week before expiration to avoid gamma risk

- 🚨 If stock breaks $75, close immediately to prevent full loss

Risk level: Moderate (defined risk, bullish assumption) | Skill level: Intermediate

🚀 Aggressive: Post-Launch Straddle - Bet on CONTINUED VOLATILITY (ADVANCED ONLY!)

Play: After launch, buy straddle betting volatility remains elevated through beta testing and Q1 earnings

Structure: Buy $85 calls + Buy $85 puts (January 16 expiration)

Why this could work:

- 💥 Launch is just FIRST catalyst - beta testing, manufacturing updates, Q1 preview all create volatility

- 🎰 Betting launch outcome doesn't resolve uncertainty - execution questions remain

- 📊 Straddle profits if stock moves >15-20% either direction

- ⚡ ASTS has shown ±30% monthly swings (Oct +64%, Nov -30%) - volatility is the product

- 🚀 If launch succeeds spectacularly AND beta testing impresses, stock could run to $100-110

- 😱 If array deployment encounters issues or beta testing disappoints, stock could crash to $65-70

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Straddle costs ~$15-20 post-launch ($1,500-2,000 per straddle) at current $85 price

- ⏰ IV CRUSH RISK: If launch succeeds without drama and stock settles $80-90, IV collapses and straddle loses 30-50% immediately

- 😱 Theta decay: Losing $50-80/day in time decay as expiration approaches

- 📊 Needs BIG move: Stock must move outside $70-100 range to profit after IV crush

- 🎢 Launch is the MAIN catalyst - subsequent news may not move stock enough to overcome premium paid

Estimated P&L:

- 💰 Cost: ~$15-20 per straddle post-launch (vs $25-30 now - WAIT for IV crush!)

- 📈 Profit scenario: Stock moves to $105 or $65 = $5-20 gain (25-100% ROI)

- 🚀 Home run: Stock moves to $115 or $55 = $30 gain (150-200% ROI)

- 📉 Loss scenario: Stock stays $78-92 range = lose $10-18 (50-90% loss)

- 💀 Total loss: Stock flat at $85 = lose entire $15-20 (100% loss)

Breakeven points:

- 📈 Upside breakeven: ~$100-105 (need 18-23% rally from $85)

- 📉 Downside breakeven: ~$65-70 (need 18-23% drop from $85)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded straddles through binary events and understand IV dynamics

- ✅ Can afford to lose ENTIRE premium (real possibility!)

- ✅ Accept you're betting AGAINST the options market's probability estimates

- ✅ Can monitor position daily and take profits/cut losses quickly

- ⏰ Plan to close position within 5-7 days post-launch (don't hold to expiration)

- 💪 Understand ASTS's volatility history and can stomach ±20% daily moves

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~35% (lower than implied 50% due to IV crush effects)

Alternative for less risk: Instead of straddle at-the-money, buy out-of-money strangle (Buy $95 calls + Buy $75 puts) for ~$8-10 total cost. Requires bigger move to profit but cuts cost in half.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ BlueBird 6 launch TONIGHT creates binary event risk: Results available within 1-2 hours of 10:24 PM EST launch. Stock could gap ±15-25% either direction tomorrow based on launch outcome, orbital insertion success, and initial telemetry. Previous delays caused 11.6% single-day drops, while successful BlueBird 1-5 deployment drove 64% monthly surge. Options pricing ±7.2% weekly move but actual moves could exceed this. NO margin for error - any anomaly triggers panic selling.

-

💸 Extreme valuation at $24B market cap on minimal revenue: Trading at massive premium to fundamentals with Q3 2024 revenue just $14.74M quarterly while burning >$50M/quarter cash. Current valuation requires flawless execution achieving $2.2B revenue by 2028 (149x growth in 3 years!). Barclays called valuation "excessive" in October downgrade even after stock already declined from $102 peak. 43% of analysts rate Hold, 14% rate Sell despite momentum. Any execution stumble magnified 3-5x at this valuation. Zero margin of safety - priced for perfection.

-

🏭 Unproven manufacturing scale-up: Target of 40 Block 2 satellites by early 2026 represents 8x acceleration vs historical production of 5 satellites over 2+ years. Satellite costs increased 10% to $22M each while production timelines slip. Supply chain issues with component suppliers caused previous delays. Dependency on third-party vendors for solar panels, phased array "Microns," and electronics creates execution risk. Never demonstrated 1 satellite/month production rate needed for 2026 targets. ONE major delay cascades entire roadmap.

-

🚀 Starlink competitive threat with massive resource advantage: SpaceX can manufacture satellites AND launch them on Falcon 9 with vertical integration ASTS can't match. While ASTS satellites have ~100x bandwidth advantage per satellite, Starlink can deploy faster at lower cost. T-Mobile partnership provides instant U.S. distribution. If SpaceX achieves critical mass first (likely given their execution track record), carrier partners may pivot away from ASTS, stranding invested capital. Competitive moat based on technology lead, not execution capability.

-

📡 FCC commercial approval remains uncertain: Still operating under Special Temporary Authority with full commercial authorization for terrestrial spectrum (700/850 MHz) pending. FCC deferred decision on commercial satellite-to-cell services as of November 2024 with no clarity on approval timeline. Amateur radio concerns, NASA collision risk letters, and spectrum interference questions create regulatory overhang. Beta testing proceeds but scaled commercial service generating $50-75M H2 2025 revenue REQUIRES full approval. Delays push revenue right and force additional dilutive capital raises.

-

💰 Massive ongoing dilution from capital needs: Requires $1.32B through end-2026 for 60-satellite constellation vs $518.9M cash position. $800M ATM program active, $500M prospectus filed May 2025, plus convertible notes from AT&T, Verizon, Google will add significant share count. Every equity raise at depressed prices accelerates dilution. With 277.6M shares outstanding, could face 15-25% additional dilution over next 18 months. Per-share economics deteriorate with each raise.

-

🛰️ Array deployment execution risk: BlueBird 6's 2,400 sq ft array is 3.5x larger than BlueBird 1-5 and represents untested Block 2 design. BlueBird 1-5 took 3 weeks to fully deploy arrays - Block 2 could take longer. Mechanical deployment at this scale in space never attempted by ASTS. Partial deployment, communication failures, or structural issues would be catastrophic for technology validation. Investors watching for "ahead of schedule" deployment like BlueBird 1-5 - anything slower triggers concerns.

-

📊 Extreme 488% volatility (52-week range $17.50-$102.79): This isn't a stable blue chip - ASTS moves ±20-30% on headline news regularly. October: +64%, November: -30% demonstrates whipsaw risk. Pre-revenue space companies trade on narrative and sentiment, not fundamentals. Retail speculation dominates with 51% institutional ownership. Gamma and technical levels provide minimal support - stock can gap through levels on low volume. Position sizing critical - don't risk capital you can't lose 50% of overnight.

-

🎯 Smart money exiting via BTC call trade: The $1.3M closing trade signals institutional trader unwinding exposure 12 hours before biggest catalyst in company history. They're paying $1.3M to close rather than risk assignment or watching profits evaporate on launch success rally. When sophisticated players with better information than retail are derisking, it's a caution flag. They may know execution risks we don't - supply chain issues, technical concerns, regulatory delays.

-

💼 Beta testing limited to Block 1 satellites (1/10th capacity): Beta services with AT&T/Verizon launch using BlueBird 1-5 before BlueBird 6 deploys. Customer experience with 693 sq ft arrays won't reflect final Block 2 capabilities with 2,400 sq ft arrays and 10x capacity. If beta testing disappoints on speeds/coverage, market may miss that it's testing inferior technology. Conversely, good beta results may not translate to Block 2 economics or scalability.

-

🌍 International regulatory approval complexity: Each market requires separate authorization - Europe, Japan, Saudi Arabia, etc. stc Group service launch targeted Q4 2026 depends on MENA regulatory approvals. UK, Canada, Japan each have independent processes. Delays in ANY major market push revenue guidance right and reduce TAM. Cannot assume U.S. FCC approval guarantees international clearance.

🎯 The Bottom Line

Real talk: Someone just paid $1.3 MILLION to close ASTS call options 12 hours before the most important catalyst in company history. This isn't a bearish bet on the long-term story - it's smart risk management by a trader who doesn't want exposure to tonight's 10:24 PM EST BlueBird 6 launch outcome.

What this trade tells us:

- 🎯 Sophisticated player expects VOLATILITY through January (BTC timing suggests uncertainty about 24-day path, not just launch)

- 💰 They're unwilling to risk assignment or profit erosion if launch succeeds and stock rallies back toward $100-105

- ⚖️ The timing (literally morning of launch day) shows they see binary risk - outcome could swing either direction dramatically

- 📊 Closing at $85 when strike is $100 (out-of-money) suggests they originally sold these calls near October's $102 peak and are locking in profits

- ⏰ January 16th expiration captures beta testing progress, Q1 earnings preview, and manufacturing execution updates

This is NOT a "sell everything" signal - it's a "manage your risk before the binary event" signal.

If you own ASTS:

- ✅ Consider trimming 20-30% before tonight's launch to lock in +250% YTD gains

- 📊 If holding through launch, set MENTAL STOP at $75 (12% below current) to protect against catastrophic failure

- ⏰ Don't get greedy - already up massively from $17.50 lows. Protecting profits is smart.

- 🎯 If launch succeeds and stock rallies to $95-100, sell into strength - take chips off table

- 🛡️ Consider buying protective puts at $75-80 strikes if holding large position through launch

If you're watching from sidelines:

- ⏰ Tonight 10:24 PM EST is the moment of truth - DO NOT enter before launch outcome clear!

- 🎯 Post-launch pullback to $75-80 on profit-taking would be excellent entry if launch succeeds

- 📈 Looking for confirmation: Successful launch, orbital insertion, first signal acquisition, no anomalies

- 🚀 Longer-term (6-12 months), beta testing success and manufacturing scale-up validation could drive $120-150 if execution delivers

- ⚠️ Current $85 price offers poor risk/reward before binary catalyst - wait for clarity

If you're bearish:

- 🎯 Wait for launch outcome before initiating shorts - fighting momentum into catalysts is suicide

- 📊 First support at $80 (former Call Wall), major support at $66 Put Wall (22% below)

- ⚠️ If launch fails or array deployment issues emerge, $66 Put Wall is initial target for panic selling

- 📉 Watch for break below $70 - triggers cascade selling as institutions' put hedges activate

- ⏰ Timing matters: Post-launch provides better risk/reward for bearish positioning after IV crush

Mark your calendar - Key dates:

- 📅 December 23 (TONIGHT) 10:24 PM EST - BlueBird 6 launch from India

- 📅 December 24-26 - Initial orbital insertion and telemetry confirmation window

- 📅 Late December 2025 - Beta testing launch with AT&T/Verizon (targeted)

- 📅 January 16, 2026 - Monthly OPEX, expiration of this $1.3M call trade

- 📅 April 7, 2025 - Q1 2025 earnings (first quarter with potential beta revenue)

- 📅 Q1 2026 - Next satellite launches begin (every 45 days targeted cadence)

- 📅 Mid-2026 - Target for 25+ satellites deployed (path to free cash flow positive)

Final verdict: ASTS's long-term satellite-to-phone story is INCREDIBLY compelling - 45+ carrier partnerships, over $1B in contracted revenue, 100x bandwidth advantage vs competitors, and validated Block 1 satellite technology. BUT, at $85 with $24B market cap on minimal revenue 12 hours before the most important launch in company history, the risk/reward is NO LONGER favorable for aggressive new positioning.

The $1.3M BTC call trade is a CLEAR signal: smart money is derisking before tonight's binary catalyst.

Be patient. Let the launch resolve. Watch for better entry points $70-80 if launch succeeds. The satellite revolution will still be here tomorrow, and you'll sleep better at night buying at $75 post-launch instead of $85 pre-launch with ±7.2% volatility priced in.

This is a marathon, not a sprint. Protect your capital. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 211x unusual volume score reflects this trade's size relative to recent ASTS history - it does not imply the trade will be profitable or that you should follow it. BlueBird 6 launch tonight creates extreme binary event risk with potential for ±20-30% gaps either direction. The BTC call buyer may have complex hedging needs not applicable to retail traders. ASTS is a pre-revenue space company with significant execution, regulatory, and competitive risks. Always do your own research and consider consulting a licensed financial advisor before trading.

About AST SpaceMobile: AST SpaceMobile develops satellite technology to deliver cellular broadband services via space-based networks directly to unmodified mobile phones, with a market cap of $24.04 billion in the Communications Services industry. The company manufactures satellites featuring the largest commercial phased array antennas in low Earth orbit, partnering with 45+ mobile network operators serving 2.8 billion subscribers globally.