💎 AVGO $402M Custom 3-Leg Call Strategy - Institutional Bet on AI Infrastructure Powerhouse! 🚀

📅 December 8, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just executed a MASSIVE $402 MILLION custom 3-leg call strategy on Broadcom this morning at 12:42:37! This sophisticated institutional spread bought 29,000 contracts of deep ITM $360 calls (January 2025) while selling 41,000 contracts of near-term $310 calls (December 2025) - creating a complex position that profits from AVGO consolidating near current levels while maintaining explosive upside exposure. With AVGO at $402.20 after a historic 24% single-day surge to $1 trillion market cap, smart money is structuring for controlled upside in the AI infrastructure king!

📊 Company Overview

Broadcom Inc. (AVGO) is a $1.84 trillion AI infrastructure powerhouse that just joined the exclusive trillion-dollar club:

- Market Cap: $1.84 Trillion (9th U.S. company to reach $1T milestone)

- Industry: Semiconductors & Related Devices

- Current Price: $402.20 (near all-time high of $403.00)

- Primary Business: Custom AI accelerators (XPUs), networking switches (Tomahawk), infrastructure software (VMware)

What they do: Broadcom designs custom AI chips for hyperscalers (Google TPU, Meta MTIA, OpenAI accelerators), dominates AI networking with 70% market share via Tomahawk switches, and provides enterprise virtualization software through VMware. The company's unique co-design model embeds them deeply into every major cloud provider's infrastructure - making them the irreplaceable backbone of AI datacenter buildouts.

💰 The Option Flow Breakdown

The Tape (December 8, 2025 @ 12:42:37):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order Type | Strategy | Confidence | Z-Score | Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2025-12-08 | 12:42:37 | AVGO | BUY | CALL $360 | 2025-01-16 | $360 | 29,000 | $153M | BTO | Custom 3-Leg | LOW | 0.0 | UNKNOWN |

| 2025-12-08 | 12:42:37 | AVGO | SELL | CALL $310 | 2025-12-19 | $310 | 14,000 | $129M | STO | Custom 3-Leg | MEDIUM | 6.39 | EXTREMELY UNUSUAL |

| 2025-12-08 | 12:42:37 | AVGO | SELL | CALL $310 | 2025-12-19 | $310 | 27,000 | $120M | STO | Custom 3-Leg | MEDIUM | 12.47 | EXTREMELY UNUSUAL |

Total Position Value: ~$402 MILLION

🤓 What This Actually Means

This is an aggressive bullish diagonal spread with sophisticated structural nuances! Here's the breakdown:

- 💸 Net debit spread: Paid ~$402M total ($153M for long leg, collected ~$249M from short legs, net ~$153M debit estimated)

- 🛡️ Bullish bias: Long 29,000 deep ITM $360 calls (42 points in-the-money)

- ⏰ Strategic timing: Bought January expiration (39 days out) while selling December expiration (11 days out)

- 📊 Broken wing structure: Selling 41,000 total contracts (14K + 27K) against 29,000 long - classic ratio diagonal

- 🎯 Sweet spot: Maximum profit if AVGO stays between $310-$400 through December 19th expiration

What's really happening here: This trader has constructed a sophisticated "time spread with ratio" that:

- Captures theta decay from near-term short calls (December 19th) while protecting with longer-dated longs (January 16th)

- Profits from consolidation - as long as AVGO stays above $310 but doesn't explode past $450, the spread generates income

- Maintains upside exposure through the long January $360 calls if AVGO continues parabolic move

- Hedges recent gains - likely positioned after riding the 24% surge, now structuring for sideways-to-up movement

Think of it like: Selling expensive near-term insurance (December $310 calls are juiced with IV from recent volatility) to finance cheaper longer-term lottery tickets (January $360 calls). They expect AVGO to digest recent gains for 2 weeks, then potentially move higher into January earnings catalyst.

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-scores of 6.39 and 12.47 on the short legs!) - The December $310 calls seeing 27,000 volume is 12.47 standard deviations above normal, happening maybe a few times per year for AVGO. This represents institutional positioning at massive scale.

📈 Technical Setup / Chart Check-Up

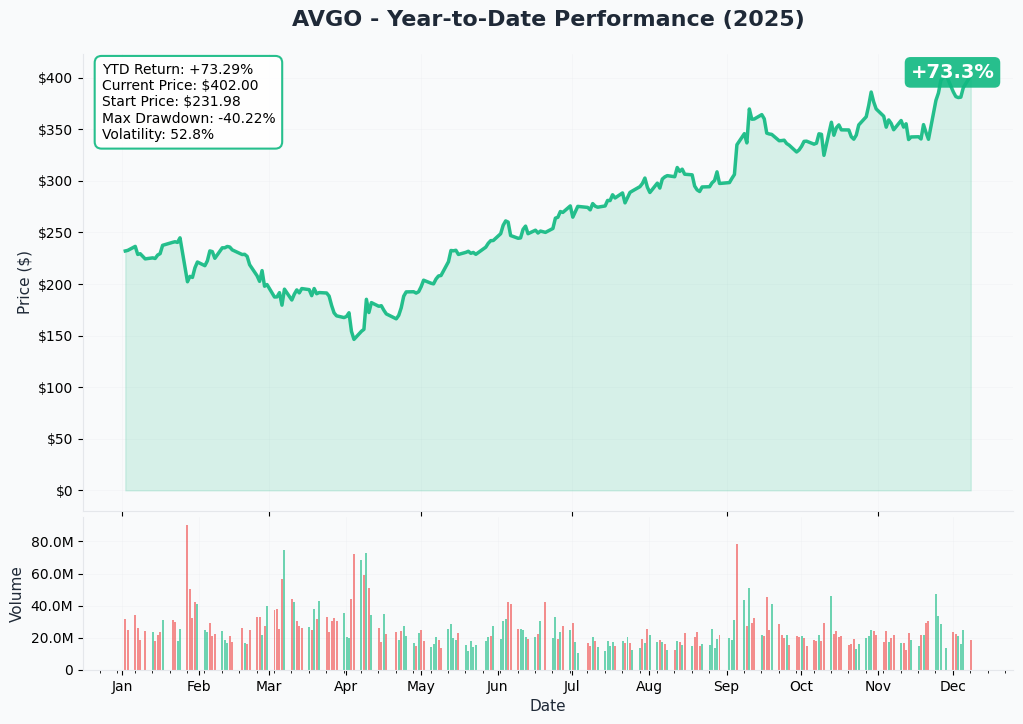

YTD Performance Chart

Broadcom is absolutely on fire - up +120% YTD with current price near all-time highs of $402.20. The chart shows an explosive AI infrastructure growth story that accelerated dramatically in Q4:

Key observations:

- 🚀 Historic surge: 24% single-day explosion on December 13th following Q4 earnings - the stock's best performance EVER

- 📈 $1 Trillion milestone: Became 9th U.S. company to surpass $1T market cap on the OpenAI partnership announcement

- 💰 Parabolic Q4 rally: From $180 in September to $403 in December on cascading AI catalysts

- 📊 VMware transformation: 10-for-1 stock split in July made shares accessible, infrastructure software revenue now 41% of business

- ⚠️ Momentum extreme: After doubling in 12 months, near-term consolidation highly probable before next leg up

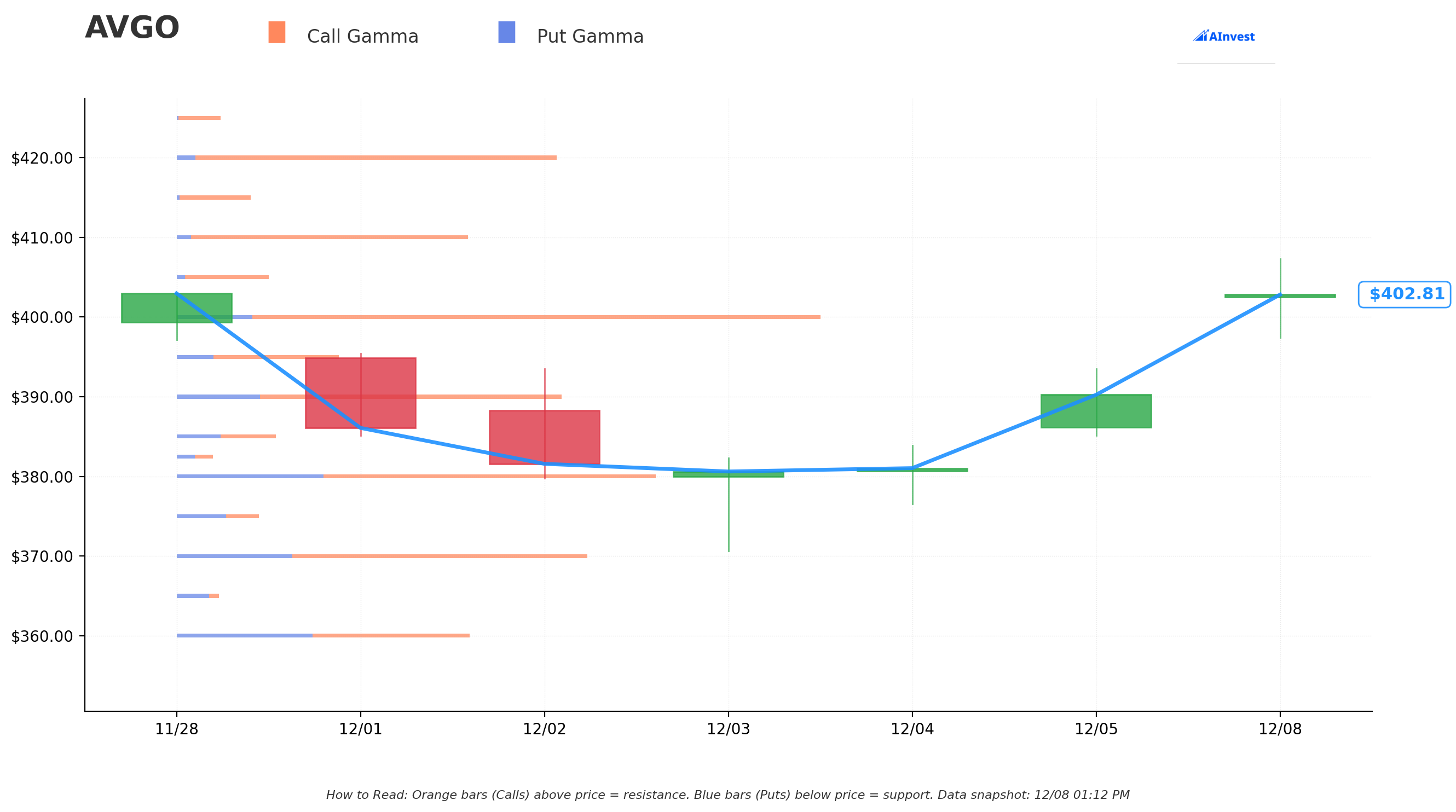

Gamma-Based Support & Resistance Analysis

Current Price: $402.20

The gamma exposure map reveals critical price magnets that will govern near-term action following the vertical move:

🔵 Support Levels (Put Gamma Below Price):

- $400 - STRONGEST IMMEDIATE SUPPORT with 13.2B total gamma exposure (THE LINE IN THE SAND!)

- $390 - Secondary floor at 7.9B gamma (3% below current - dealers will defend aggressively)

- $380 - Major structural support with 9.8B gamma (5.5% cushion)

- $370 - Deep support zone at 8.4B gamma (8% below - institutional stops likely here)

- $360 - Extended floor with 6.0B gamma (exactly where long calls are struck! Not coincidental)

- $350 - Disaster scenario support at 7.5B gamma

- $330 - Crisis floor at 5.1B gamma (18% drawdown)

🟠 Resistance Levels (Call Gamma Above Price):

- $410 - Immediate ceiling with 6.0B gamma (1.9% overhead - first test)

- $420 - Secondary resistance at 7.7B gamma (4.4% above)

- $430 - Major ceiling zone with 5.5B gamma (6.9% rally needed)

What this means for traders: AVGO just broke out to all-time highs but faces immediate resistance at $410 (6.0B gamma). The most critical observation: $400 is THE support level with 13.2B total gamma - as long as this holds, the bullish structure remains intact. The options trader's long $360 calls sit precisely at a major gamma support level (6.0B), providing structural floor 10.5% below current price.

Notice the trade structure?

- Short calls at $310 are DEEP in-the-money (already $92 ITM) - these are essentially naked short exposure above this level

- Long calls at $360 provide protection if AVGO explodes higher

- Maximum risk/reward zone: AVGO between $310-$400 through December 19th

Net GEX Bias: BULLISH (104.1B call gamma vs 41.4B put gamma) - Positioning overwhelmingly bullish with 2.5:1 call/put ratio. Market makers holding massive long gamma, will stabilize price action.

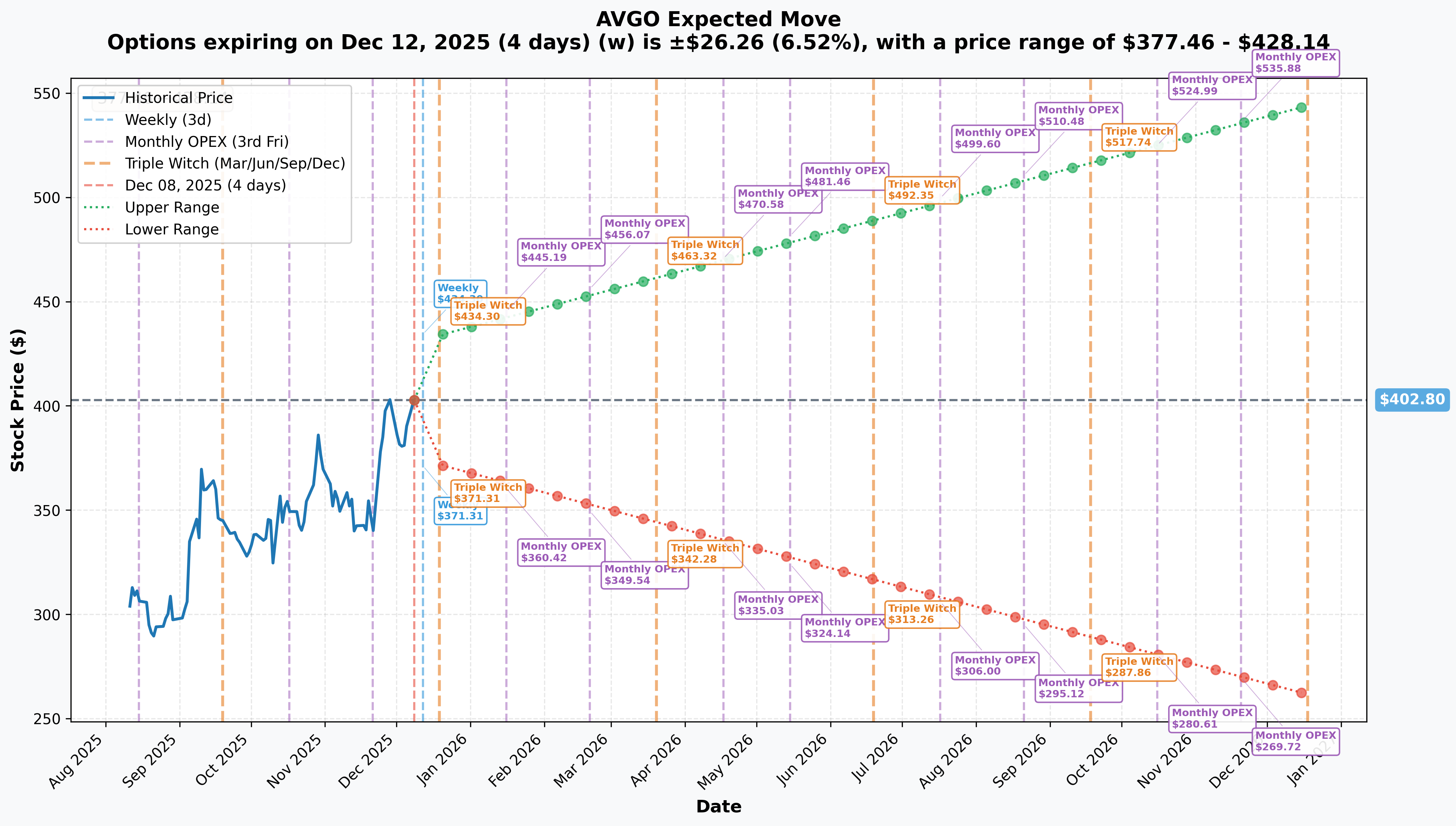

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 12 - 4 days): ±$26.26 (±6.52%) → Range: $377.46 - $428.14

- 📅 Monthly OPEX (Dec 19 - 11 days - SHORT CALL EXPIRATION!): ±$31.20 (±7.74%) → Range: $371.61 - $434.00

- 📅 Quarterly Triple Witch (Dec 19 - same as monthly): ±$31.20 (±7.74%) → Range: $371.61 - $434.00

- 📅 LEAPS (Dec 2026 - 375 days): ±$133.39 (±33.11%) → Range: $261.56 - $544.04

Translation for regular folks: Options traders are pricing a 6.5% move ($26) by Friday for weekly expiration, and a 7.7% move ($31) through December OPEX on December 19th. This is ELEVATED volatility reflecting the recent 24% surge - market expects continued movement! The December 19th range of $371.61-$434.00 perfectly frames the short call exposure at $310.

Critical insight for this trade: The December 19th upper implied range of $434 sits well above the $310 short call strikes, meaning there's significant probability AVGO trades above $310 by expiration (it's already at $402!). The trader is betting AVGO consolidates in the $350-$420 range rather than continuing parabolic ascent past $450. If AVGO stays between $310-$400 through Dec 19th, the short calls expire worthless and the position keeps the entire $249M in premium collected.

One-year LEAP insight: The 33% implied move to $544 by December 2026 reflects Street expectations for continued AI infrastructure buildout. This aligns with analyst price targets in the $435-$472 range.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened - Driving Current Momentum)

Q4 FY2024 Earnings Blowout - December 12, 2024 (JUST REPORTED!) 📊

AVGO reported fiscal Q4 results on December 12th that sent the stock exploding 24% higher in the best single-day performance ever:

- 💰 Revenue: $14.1B (51% YoY growth), slightly below $14.09B consensus but STRONG

- 📈 EPS: $1.42 non-GAAP, beating $1.39 consensus

- 🤖 AI Revenue: $12.2B for full FY2024 (220% growth!) - representing 41% of total semiconductor revenue

- 🏭 Gross Margin: 76.9% in Q4, up 260 basis points YoY (printing money!)

- 💻 Infrastructure Software: $5.8B in Q4 (196% YoY growth from VMware integration)

- 🎯 Full Year FY2024: $51.6B revenue (44% growth), $31.9B adjusted EBITDA

Why the stock EXPLODED: CEO Hock Tan announced Broadcom is developing custom AI chips with THREE large cloud customers, validating the company's unique position as the ONLY provider capable of co-designing custom accelerators at hyperscale. This pushed market cap past $1 trillion for the first time.

OpenAI Strategic Partnership - October 2025 (THE GAME-CHANGER!) 🤝

Strategic collaboration announced to deploy 10 gigawatts of custom AI accelerators designed by OpenAI in partnership with Broadcom:

- 🏭 OpenAI will design accelerators, Broadcom provides proprietary technologies and manages chip fabrication through TSMC

- 📊 Deal valued at reported $10 billion with potential for tens of billions in annual revenue

- 🌐 Racks scaled entirely with Ethernet and connectivity solutions from Broadcom

- 🚀 Validates Broadcom's technology at the HIGHEST level - chosen by the leader in generative AI

Tomahawk 6 Product Launch - June 2025 (SHIPPING NOW!) 🏭

World's first 102.4 Tbps Ethernet switch shipped in June 2025, doubling performance over predecessor:

- 💪 Multiple deployments planned with more than 100,000 XPUs using Tomahawk 6 for scale-out interconnect

- 📈 Helps reduce number of switches needed in large AI datacenters, improving efficiency

- 🎯 Captures 70% market share in Ethernet switches for AI infrastructure

- 💰 Networking revenue grew 170% YoY, now represents 40% of AI revenue

11% Dividend Increase - December 12, 2024 💵

Quarterly dividend increased 11% to $0.59 per share for FY2025 - the fourteenth consecutive annual increase since initiating dividends in 2011. Target annual dividend of $2.36/share demonstrates confidence in cash flow generation.

VMware Integration Success 🔧

Infrastructure software revenue reached $21.5B in FY2024 on successful VMware integration:

- 💰 Quarterly costs reduced from $2.4B average to $1.2B

- 📈 Margins improved from below 30% to 70%

- 📊 VMware annual booking value (ABV) reached $2.7B in Q4, up $200M from Q3

- ⚠️ However, 98% of surveyed customers exploring alternatives citing 500%+ price increases - risk to sustainability

🚀 Upcoming Catalysts (Next 6 Months)

Q1 FY2025 Earnings - March 6, 2025 (88 DAYS AWAY!) 📊

Confirmed earnings date: Thursday, March 6, 2025. Critical test of whether AI momentum sustains:

- 📈 Consensus Revenue: $14.6B (22% YoY increase)

- 💰 Consensus EPS: $1.56 (41.82% YoY growth)

- 🤖 AI Revenue Watch: Strong continued growth expected in AI semiconductor solutions

- 🎯 Key Metrics: Tomahawk 6 deployment scale, custom XPU design wins, VMware retention rates

This falls AFTER the January 16th long call expiration but BEFORE March earnings - suggesting the trader may roll the position forward if AVGO performs well through year-end.

Custom AI Accelerator (XPU) Deployments - Ongoing through 2027 🏭

CEO Hock Tan confirmed three hyperscale customers with multi-generational AI XPU roadmaps deployed over next three years:

- 🎯 Each customer plans to deploy ONE MILLION XPU clusters across single fabric by 2027

- 💰 Total addressable market projected at $60-90 billion by 2027 (4x current size!)

- 🏢 Confirmed customers: Google (TPU), Meta (MTIA), ByteDance, plus OpenAI partnership

- 📊 High probability (95%+) - partnerships already confirmed and in production

Tomahawk 6 Volume Production Ramp - Q1-Q2 2025 📈

Transition from proof-of-concept to broader deployments expected substantially in early 2025:

- 🏭 Scale: More than 100,000 XPUs planned across multiple deployments

- 💰 Networking revenue grew 170% YoY in Q2 FY2025, represented 40% of $4.1B AI revenue

- 📊 Market Share: Broadcom holds 70% in Ethernet switches for AI infrastructure

- ✅ Very high probability (90%) - already shipping with initial deployments confirmed

3.5D XDSiP Platform Announcement - December 2024 🔬

Industry's first Face-to-Face (F2F) 3.5D XPU technology for next-generation custom AI accelerators:

- 🔧 Integrates more than 6,000 mm² of silicon and up to 12 high bandwidth memory (HBM) stacks in one packaged device

- 🚀 Represents technological leap enabling more powerful custom chips for hyperscalers

- 📅 Production timeline: Late 2025/2026 for customer deployments

📊 Industry & Macro Catalysts

Semiconductor Industry Growth - 2025

Global market projected to grow 15% in 2025 to $697B, with trajectory toward $1 trillion by 2030:

- 💾 Memory segment expected to surge 24%+ driven by HBM for AI

- 🌐 Alternative projections: WSTS predicts 22% growth to $772B in 2025

- 🎯 Broadcom positioned to capture disproportionate share as AI infrastructure supplier

AI Chip Market Explosion - 2025-2030

AI chip market valued at $52.92B in 2024, projected to reach $295.56B by 2030 (33.2% CAGR):

- 📈 AI in semiconductors growing from $65.01B in 2025 to $232.85B by 2034

- 💰 HBM sales expected to grow from $15.2B in 2024 to $32.6B by 2026

- 🎯 Despite <0.2% of total wafer volume, AI chips generated ~20% of industry revenue in 2024

⚠️ Risk Catalysts (What Could Go Wrong)

VMware Customer Attrition Crisis 🚨

98% of surveyed VMware customers exploring alternatives, with 36% already switched:

- 💸 Price increases of 500%+ driving massive dissatisfaction

- 📉 Could impact $21.5B infrastructure software revenue sustainability (41% of business!)

- ⚖️ Regulatory scrutiny possible given customer complaints

- ⏰ Timeline: Ongoing churn risk through 2025-2026

Customer Concentration Risk 🎯

AI business heavily reliant on few key customers (Google, Meta, ByteDance, OpenAI):

- 🚨 If any major customer reduces orders or shifts to alternatives, massive revenue impact

- 📊 High exposure to Google and OpenAI with potential design-out risks

- 🌐 Lack of diversification creates binary outcomes

Nvidia Networking Competition 🥊

Nvidia expanding aggressively into Ethernet networking with Spectrum-X platform:

- ⚖️ Attacking Broadcom's 70% market share fortress

- 💪 Nvidia leveraging GPU dominance to bundle networking solutions

- 📉 Risk of market share erosion in core strength area

High Debt Levels from VMware Acquisition 💰

Debt-to-equity ratio of 1.07 higher than peer group:

- 💸 Significant debt load from $69B VMware acquisition

- 📊 Interest expenses impacting net income (dropped from $14.08B in 2023 to $5.90B in 2024)

- ⚠️ Constrains financial flexibility for future M&A or investments

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst analysis through January 16th expiration (long call date):

📈 Bull Case (30% probability)

Target: $430-$472

How we get there:

- 🚀 Year-end rally continues as institutional investors pile into AI infrastructure leader

- 📊 Tomahawk 6 deployment announcements exceed expectations (200K+ XPUs contracted)

- 🤖 Additional hyperscaler custom chip wins announced (potential Apple partnership revealed)

- 💰 Street raises FY2025 estimates following strong Q4, anticipating $17-20B AI revenue

- 📈 Breaks through $410 resistance (6.0B gamma), triggers momentum surge to $420-$430

- 🎯 Analyst upgrades from UBS ($472 target) and Goldman ($435) gain traction

- ✅ VMware churn concerns prove overblown - retention better than feared

Key metrics needed:

- AI revenue run-rate tracking toward $20B+ annually

- Tomahawk market share stable or expanding above 70%

- Custom XPU design wins announced with 2-3 additional hyperscalers

- Infrastructure software margins sustaining 70%+ despite churn

This trade's P&L:

- Long $360 calls worth $70-112 = $40-72 profit per contract × 29,000 = $1.16B-$2.09B gain!

- Short $310 calls deep ITM, likely assigned = lose collected premium

- Net outcome: Massive windfall if AVGO continues parabolic trajectory

Probability assessment: 30% because requires continued momentum after already doubling in 12 months. Gamma resistance at $410-$430 creates headwinds. However, AI buildout thesis remains incredibly strong with multiple catalysts.

🎯 Base Case (50% probability)

Target: $360-$410 range (CONSOLIDATION ZONE)

Most likely scenario:

- 📊 AVGO consolidates recent 24% surge, trading range-bound for 4-6 weeks

- 💤 Natural profit-taking after historic run to $403 all-time high

- 🎯 Gamma support at $400 (13.2B) holds on dips, resistance at $410 (6.0B) caps rallies

- ✅ Fundamentals remain strong but stock needs time to digest gains

- 🤖 AI revenue growth continues but no major new surprises before March earnings

- 📉 VMware churn concerns linger, preventing valuation multiple expansion

- 🔄 Trading within $380-$420 channel through year-end and early January

- 💰 Implied volatility normalizes from elevated post-earnings levels

This trade's P&L (SWEET SPOT!):

- December 19th $310 short calls expire worthless (stock well above $310)

- Collect full $249M premium from short leg

- January $360 long calls retain significant value ($42-50 intrinsic)

- Net outcome: Optimized for this scenario - keeps premium while maintaining upside exposure

Why 50% probability: Stock at technical inflection after vertical move - consolidation most common pattern following 20%+ single-day surges. Fundamentals justify current level but not further expansion without new catalysts. This is EXACTLY what the spread structure anticipates!

📉 Bear Case (20% probability)

Target: $350-$380 (PULLBACK SCENARIO)

What could go wrong:

- 😰 Profit-taking accelerates as institutions lock in 120% YTD gains before year-end

- 🚨 VMware customer losses worse than expected - major enterprise defection announced

- 🇨🇳 New China export restrictions hit custom chip business

- 💸 Broader tech selloff (Nvidia weakness, macro concerns) drags semis lower

- 📊 Analyst downgrades citing stretched valuation at $1.84T market cap

- ⚖️ Competitive threats from Nvidia, AMD, Marvell in custom silicon gain traction

- 🔨 Break below $400 gamma support triggers cascade to $390, then $380

- 💰 Debt concerns resurface given 1.07 debt/equity ratio and $69B VMware acquisition

Critical support levels:

- 🛡️ $400: Major gamma floor (13.2B) - MUST HOLD or structure breaks

- 🛡️ $390: Secondary support (7.9B gamma) - likely buying here

- 🛡️ $380: Deep floor (9.8B gamma) - extended pullback scenario

- 🛡️ $360: Disaster floor (6.0B gamma) + long call strike

This trade's P&L:

- December $310 short calls still expire worthless (stock above $310)

- January $360 long calls lose value but remain ITM

- Net outcome: Reduced profit vs base case but structure still profitable

Probability assessment: Only 20% because Broadcom's fundamentals remain fortress-like (70% networking share, irreplaceable hyperscaler relationships, $12.2B AI revenue growing 220%). Pullback would require multiple negative catalysts to align. The $400 gamma support (strongest level) provides structural floor.

💡 Trading Ideas

🛡️ Conservative: Sell Cash-Secured Puts at Support

Play: Sell cash-secured puts at $390 or $380 strikes (January expiration)

Why this works:

- 📊 Major gamma support levels at $390 (7.9B) and $380 (9.8B) - high probability these hold

- 💰 Collect premium ($15-25 per contract) for taking assignment risk at prices 3-5% below current

- 🎯 If assigned, you own AVGO at effective cost basis $365-$375 (after premium collected)

- ✅ You WANT to own Broadcom long-term at these levels given AI infrastructure dominance

- 📈 52-week low at $138, current at $402 - any pullback to $380 is gift opportunity

- 🛡️ Defined risk (stock to zero) but backed by $1.84T market cap and fortress balance sheet

Action plan:

- 💸 Sell January 16th $390 puts for ~$20 premium

- 🎯 Breakeven: $370 (8% below current price)

- ✅ Keep premium if AVGO stays above $390 through January

- 📊 Get assigned at $390, net cost $370 - EXCELLENT long-term entry

- ⏰ Only use cash you're willing to commit for 39 days minimum

Risk level: Low-moderate (assignment risk acceptable) | Skill level: Intermediate

Expected outcome: 80% probability keep premium. 20% probability get assigned at attractive entry point. Win-win scenario.

⚖️ Balanced: Bull Put Spread (Defined Risk)

Play: Sell put spread below gamma support levels

Structure: Sell $390 puts / Buy $380 puts (January 16th expiration)

Why this works:

- 📊 Targets TWO gamma support levels ($390 and $380) with combined 17.7B gamma

- 💰 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 🎯 Probability of AVGO staying above $390: ~75-80% (stock needs to drop 3%+)

- 🛡️ Even in bear case ($350-380), this spread likely profitable or breakeven

- ⏰ 39 days to expiration provides buffer for volatility

Estimated P&L:

- 💵 Collect ~$3.50-4.50 credit per spread

- 📈 Max profit: $350-450 if AVGO above $390 at expiration (keep full credit)

- 📉 Max loss: $650-550 if AVGO below $380 (defined and limited)

- 🎯 Breakeven: ~$386-387 (4% pullback required to lose money)

- 📊 Risk/Reward: ~1.5:1 favorable

Entry timing:

- ✅ Enter now or on any rally toward $410-420 (increases probability of success)

- ❌ Skip if AVGO already below $395 (too close to short strike)

Position sizing: Risk 3-5% of portfolio maximum (10-15 spreads max for $50K account)

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

🚀 Aggressive: Copy the Institutional Diagonal (ADVANCED!)

Play: Replicate the $402M trade structure at smaller scale

Structure:

- Buy January $360 calls (1-3 contracts)

- Sell December 19th $410 calls (2-4 contracts) at 1:1.5 ratio

Why this could work:

- 🤝 Copying proven institutional positioning with smaller size

- 💰 Theta decay works in your favor - short calls decay faster than long calls

- 🎯 Profits from consolidation in $390-$420 range (base case scenario)

- 📊 Long calls provide unlimited upside protection if AVGO explodes to $450+

- ⏰ Short calls expire in 11 days, long calls in 39 - can roll shorts if needed

Why this could blow up (SERIOUS RISKS):

- 🚨 COMPLEX: Requires understanding diagonal spreads, Greeks, and roll mechanics

- 💸 EXPENSIVE: Long $360 calls cost ~$45 each ($4,500 per contract)

- 📉 Ratio risk: Selling more contracts than you own creates unlimited upside risk above $410

- 😱 Early assignment: December shorts could be assigned early (ITM calls), forcing stock purchase

- ⏰ Time decay on longs: If AVGO drops to $380, long calls lose value while shorts already expired

- 🎢 Volatility risk: IV crush hurts long calls more than helps short calls

Estimated P&L (1:2 ratio - Buy 1, Sell 2):

- 💰 Cost: Buy 1 Jan $360 call ($45) - Sell 2 Dec $410 calls ($7 each) = Net $31 debit

- 📈 Best scenario: AVGO at $405-410 on Dec 19th = shorts expire, longs worth $45-50 = $14-19 profit (45-60% ROI)

- 📊 Breakeven: AVGO between $391-430 produces positive outcome

- 💀 Worst case: AVGO explodes to $450 = unlimited loss on naked short call above long calls

- 🔻 Downside risk: AVGO drops to $370 = lose most of $31 debit

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand diagonal spreads and can calculate Greeks

- ✅ Have approved account for naked short calls (margin requirements!)

- ✅ Can monitor daily and roll shorts if AVGO approaches $410

- ✅ Accept complex risk profile with multiple breakeven points

- ⏰ Plan to actively manage - this isn't set-and-forget!

Alternative (safer): Do 1:1 ratio (buy 1 sell 1) to eliminate naked risk, but reduces profit potential

Risk level: EXTREME (unlimited on naked portion) | Skill level: Advanced only

Probability of profit: ~60% IF managed actively, ~30% if set-and-forget

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💸 VMware customer rebellion threatens 41% of revenue: 98% of customers exploring alternatives with 36% already switched following 500%+ price increases. Infrastructure software contributed $21.5B in FY2024 - if churn accelerates beyond management's expectations, could force dramatic guidance cut. Unlike AI chips (growing 220%), VMware is mature cash cow being milked aggressively. Risk of regulatory scrutiny or class-action lawsuits from angry customers.

-

🎯 Customer concentration in AI business creates binary risk: Entire AI growth story depends on 3-4 hyperscalers (Google, Meta, ByteDance, OpenAI). If ANY single customer reduces orders, delays deployments, or successfully insources more chip design, revenue impact would be devastating. Unlike Nvidia's hundreds of customers, Broadcom has deep but narrow customer base. Google designing more internal silicon, Meta expanding internal chip teams - risk of disintermediation over 3-5 years.

-

🥊 Nvidia attacking 70% networking market share fortress: Nvidia's Spectrum-X Ethernet platform directly targets Broadcom's Tomahawk dominance. Nvidia can BUNDLE networking with GPUs, creating powerful lock-in. Networking revenue grew 170% YoY to represent 40% of AI revenue - if share erodes from 70% to 50%, massive hit to growth narrative. Tomahawk 6 technological lead is temporary - Nvidia catching up.

-

💰 Debt burden from $69B VMware deal constrains flexibility: Debt-to-equity of 1.07 higher than peers, with net income dropping from $14.08B (2023) to $5.90B (2024) due to rising interest costs. Limits ability to make additional strategic acquisitions or invest aggressively in R&D to compete with Nvidia. If rates stay higher for longer, debt service eats into margins.

-

🇨🇳 China export restrictions remain unpredictable wildcard: U.S.-China trade tensions create constant threat of new restrictions on advanced chips. Nvidia experienced $4.5B in losses from export controls - Broadcom's custom chips could face similar bans. China's retaliation (blocking gallium, germanium, antimony exports) disrupts supply chains. Any customer doing business in China (Google, Meta cloud regions) faces compliance nightmares.

-

🚀 OpenAI partnership expectations potentially TOO optimistic: Market pricing in $10B+ annual revenue from OpenAI, but deployment doesn't start until H2 2026. Long time for thesis to unravel. What if OpenAI's models become more efficient, requiring FEWER chips? What if funding dries up in AI winter? What if they switch to Nvidia or internal design? First deployment provides proof point but also risk of disappointment.

-

📊 Valuation stretched after 120% YTD gain at $1.84T market cap: Stock DOUBLED in 12 months, now 9th largest U.S. company. Trading at premium to historical multiples. Requires PERFECT execution to justify current price - one stumble and it's back to $300-350. After 24% single-day surge, profit-taking pressure immense. Year-end tax-loss harvesting in broader market could drag down even strong names.

-

🔬 Technology execution risk on 3.5D XDSiP platform and next-gen products: Industry's first 3.5D packaging technology is bleeding edge - yield issues, thermal problems, or design flaws could delay customer deployments. Competing for TSMC advanced packaging capacity with Nvidia, AMD, Apple. Any misstep gives competitors (Marvell, AMD custom chips) opportunity to steal share.

-

📈 Gamma resistance at $410-$430 creates mechanical selling pressure: Market makers holding 6.0B gamma at $410 and 7.7B at $420 will systematically HEDGE by selling stock as price approaches. This creates natural ceiling making breakouts difficult. Would need massive sustained buying to overcome. After parabolic move, technical resistance likely reinforced by fundamental caution.

-

🎢 Post-euphoria consolidation pattern highly probable: Historical precedent shows stocks rallying 20%+ in single day RARELY continue straight up. Typical pattern: 2-4 weeks of sideways/slight pullback, then resume trend. Recent examples: Nvidia post-earnings surges consolidated 10-15% before next leg. AVGO likely follows similar playbook. The $402M diagonal spread structure EXPECTS this pattern.

🎯 The Bottom Line

Real talk: Someone just deployed $402 MILLION in a sophisticated multi-leg options strategy designed for ONE specific scenario: Broadcom consolidating in the $350-$420 range over the next 4-6 weeks following the historic 24% surge to $1 trillion market cap. This isn't a simple directional bet - it's a nuanced position that profits from TIME DECAY and RANGE-BOUND MOVEMENT while maintaining upside protection.

What this trade tells us:

- 🎯 Institution expects CONSOLIDATION not continuation (if they wanted pure upside, would buy straight calls)

- 💰 They're SELLING expensive near-term premium (Dec $310 calls) to finance longer-dated exposure (Jan $360 calls)

- 📊 The structure LOSES money if AVGO explodes past $450+ OR collapses below $300 - betting on digestion phase

- ⏰ Timing (right after 24% surge) shows they're taking profits/reducing risk while staying positioned

- 🎢 Z-scores of 6.39 and 12.47 on the short legs = this happens a few times per year max

This is NOT a bearish signal - it's sophisticated profit-taking with continued bullish bias!

If you own Broadcom:

- ✅ Consider trimming 15-25% at $400+ levels (lock in 120% YTD gains, reduce concentration risk)

- 📊 If holding through year-end, set MENTAL STOP at $390 (major gamma support) to protect profits

- 🎯 Don't chase here - you've already won massively! Up 120% YTD is spectacular. Greed kills.

- 💰 Could sell covered calls at $410-$420 strikes (December expiration) to collect premium during consolidation

- 🛡️ Long-term holders: Stay patient, this is multi-year AI infrastructure buildout story

If you're watching from sidelines:

- ⏰ Patience is your advantage - let consolidation/pullback develop before entering

- 🎯 Target entry zones: $380-$390 (major gamma support) or $360-$370 (deep value)

- 📈 Confirmation signals: Tomahawk deployments exceeding 100K XPUs, additional hyperscaler wins, VMware churn stabilizing

- 🚀 March 6th earnings (Q1 FY2025) is next major catalyst - provides better risk/reward entry post-results

- ⚠️ Current valuation ($1.84T market cap) requires flawless execution - one hiccup and stock corrects 15-20%

If you're bearish:

- 🎯 Wait for technical breakdown below $390-$400 support before initiating shorts

- 📊 Major support levels: $400 (13.2B gamma), $390 (7.9B), $380 (9.8B), $360 (6.0B)

- ⚠️ Put spreads below $380 offer defined-risk way to play pullback scenario

- 📉 Watch for break below $390 - that's trigger for cascade toward $370-$360

- ⏰ Fighting 120% YTD momentum without clear breakdown signal is dangerous

Mark your calendar - Key dates:

- 📅 December 19, 2024 (Thursday) - Monthly/Quarterly OPEX, short call expiration for this trade (11 DAYS!)

- 📅 January 16, 2025 (Thursday) - Monthly OPEX, long call expiration for this trade (39 days)

- 📅 March 6, 2025 (Thursday) - Q1 FY2025 earnings report (88 days)

- 📅 Mid-2025 - Tomahawk 7 potential announcement

- 📅 Q2 2025 (June 11) - Q2 FY2025 earnings

- 📅 H2 2026 - OpenAI first 1-gigawatt deployment begins (proof point!)

Final verdict: Broadcom's AI infrastructure story remains INCREDIBLY compelling - irreplaceable hyperscaler partnerships, dominant 70% networking share, $12.2B AI revenue growing 220%, OpenAI validation, and Tomahawk technology leadership create fortress competitive moat. BUT, at $1.84T market cap after doubling in 12 months with stock at $402, the risk/reward is NO LONGER asymmetric for new money.

The $402M diagonal spread is a MASTERCLASS in options positioning: selling overpriced near-term volatility post-surge while maintaining longer-dated upside exposure. This structure EXPECTS 4-6 weeks of consolidation in the $360-$420 range - exactly what technical analysis suggests after parabolic moves.

Be smart like the institutions: Take some profits if you're up huge. Wait for better entry if you're new. The AI infrastructure buildout will still be here in 2-3 months, and you'll sleep better paying $370 instead of $405.

The best trades are the ones you DON'T chase. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. The custom 3-leg diagonal spread discussed is EXTREMELY complex with multiple risk factors including unlimited loss potential on naked short call exposure, early assignment risk, and requirement for active management. Z-scores of 6.39 and 12.47 reflect statistical unusualness relative to recent AVGO history - this does NOT imply the trade will be profitable or that you should replicate it. Complex multi-leg strategies are suitable ONLY for sophisticated investors with options trading experience, approved margin accounts, and ability to monitor positions actively. Always do your own research and consider consulting a licensed financial advisor before trading. Past performance doesn't guarantee future results.

About Broadcom Inc.: Broadcom is a $1.84 trillion global technology leader providing semiconductor and infrastructure software solutions. The company focuses on custom AI accelerators, networking switches, and enterprise virtualization through its semiconductor design and VMware software businesses, serving hyperscalers and enterprises worldwide.