🚨 AVGO: $20M Call Bet Before Earnings! Institutional Money Loads Up on Broadcom

📅 December 11, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $20 MILLION on AVGO call options with the stock at $399, betting on a move to $360 by January 2026! This massive 4,000-contract position hit the tape just hours before Broadcom's Q4 earnings report (after market close today). With the stock up 74% year-to-date and Wall Street pricing in a 5.5% move for earnings, big money is positioning for continued AI infrastructure dominance.

💼 Company Overview

Broadcom Inc. (NASDAQ: AVGO)

- Market Cap: $1.95 Trillion (6th largest company globally)

- Sector: Semiconductors & Infrastructure Software

- Employees: 37,000

- Headquarters: Palo Alto, California

What They Do: Broadcom is a semiconductor powerhouse that designs custom AI chips (ASICs) for tech giants like Google, Meta, and OpenAI, while also owning VMware - the dominant enterprise virtualization software platform. Think of them as the arms dealer of the AI infrastructure buildout, providing both the chips and the software that power modern data centers.

💰 The Option Flow Breakdown

📊 What Just Happened

Here's the actual trade that crossed the tape this morning:

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Spot Price | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|

| 2025-12-11 | 10:16:32 | AVGO | BUY | CALL | 2026-01-16 | $360 | 4,000 | $20,000,000 | $399.32 | $49.90 |

🔥 Track this option live on Ainvest

🤓 What This Actually Means

Translation for us regular folks:

🐋 Whale Activity: This is institutional money, not retail. A $20M bet is roughly 555 times the average option trade size - you don't see this every day. This level of conviction screams hedge fund or family office positioning.

💡 The Strategy: Buying deep in-the-money calls ($360 strike vs $399 stock price) is a bullish bet with built-in downside protection. The buyer gets $39.32 of intrinsic value immediately, meaning the stock could drop to $360 and they'd still have value. This is Long Call strategy - pure directional bullish play.

⏰ Timing Matters: This trade hit 8 hours before Broadcom reports Q4 earnings. Either this trader has steel nerves or they're positioning for a post-earnings rally based on AI chip guidance.

📈 Unusualness Score: With a Z-Score of 1.34 (above average), volume of 4,000 contracts on open interest of just 350, and a volume-to-OI ratio of 11.4x, this trade ranks as high activity for AVGO options. Not once-in-a-lifetime, but definitely a few-times-per-year occurrence that demands attention.

📈 Technical Setup / Chart Check-Up

YTD Chart Analysis

What We're Seeing:

The chart tells a powerful story of 2025: AVGO has absolutely crushed it, rising from ~$230 in January to an all-time high of $412.97 on December 10th. That's a 74% gain in 11 months, powered by AI infrastructure euphoria and analyst upgrades.

Key Observations:

- 📊 Parabolic Move: The stock went nearly vertical starting in October, gaining 70% in just 3 months

- 🎯 At All-Time Highs: Currently trading at $406, just 1.7% below the December 10th peak

- 💪 Strong Support: Multiple tests of the $380-390 zone have held firm

- ⚡ Momentum: Clear uptrend with higher highs and higher lows throughout 2024

Risk Note: Parabolic moves like this can reverse violently if earnings disappoint. The stock has limited historical resistance levels to slow down a sell-off since we're in price discovery mode.

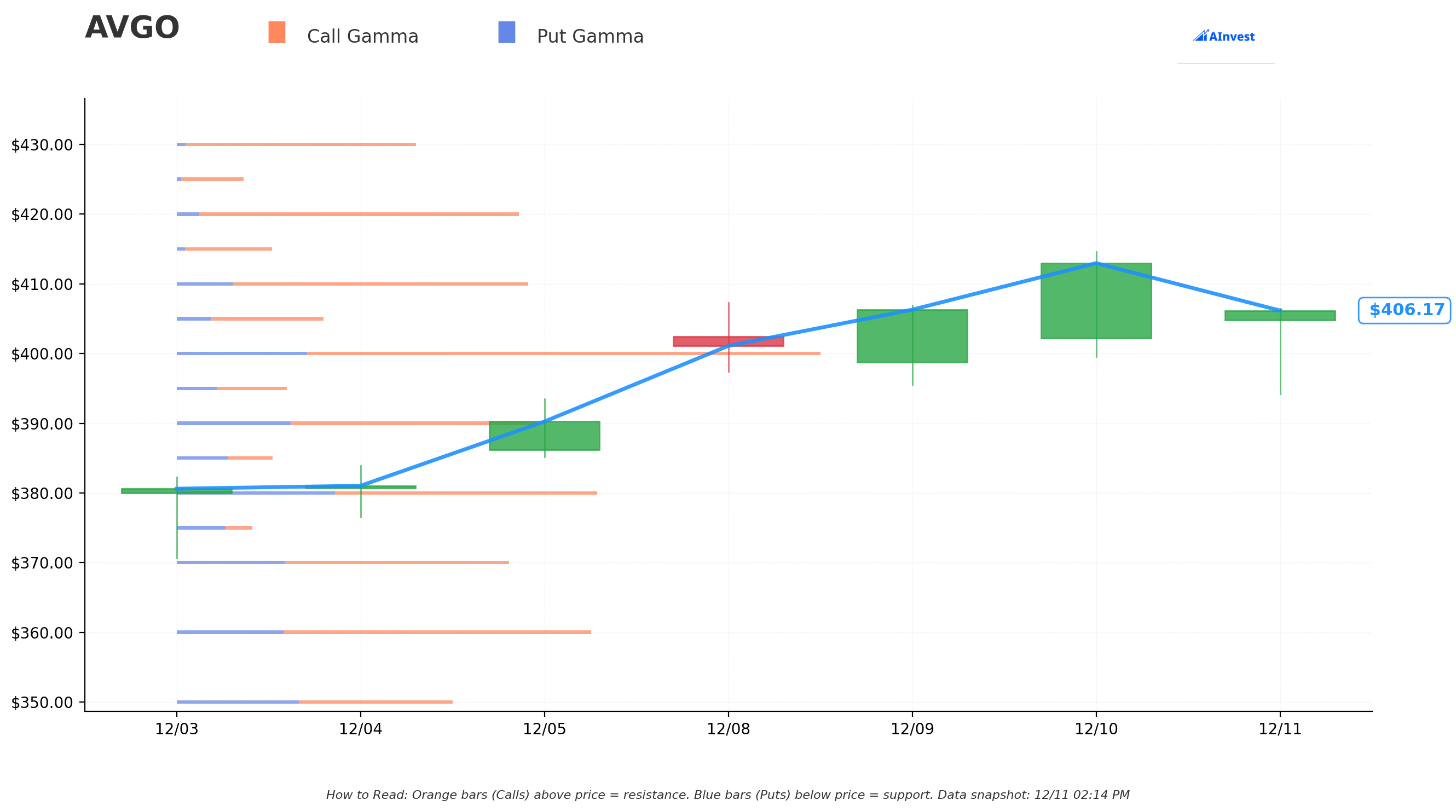

🎯 Gamma-Based Support & Resistance Analysis

What Are Gamma Levels? These are price zones where options dealers have massive exposure. Think of them as invisible force fields - the stock tends to get "sticky" at these levels because market makers have to buy/sell tons of shares to hedge their options positions.

Current Gamma Setup (as of December 11, 2:16 PM ET):

🔴 Resistance Levels (Orange Bars = Call Gamma Above Price):

| Strike | Net GEX | Distance from Current | Strength |

|---|---|---|---|

| $410 | $6.17B | +0.9% | 🔥 Strongest Resistance |

| $420 | $7.67B | +3.4% | 🔥 Very Strong |

| $430 | $5.75B | +5.8% | Strong |

| $450 | $5.13B | +10.7% | Moderate |

🟢 Support Levels (Blue Bars = Put Gamma Below Price):

| Strike | Net GEX | Distance from Current | Strength |

|---|---|---|---|

| $400 | $9.89B | -1.6% | 🔥 Strongest Support |

| $390 | $3.43B | -4.0% | Strong |

| $380 | $2.68B | -6.5% | Moderate |

| $370 | $3.01B | -8.9% | Moderate |

| $360 | $5.16B | -11.4% | Strong |

What This Tells Us:

🎯 Bullish Bias: Net gamma exposure is $65.3B in calls vs $52.4B in puts - that's a clear bullish tilt. Options dealers are positioned for upside.

💪 Near-Term Range: The stock is sandwiched between massive gamma walls at $400 support and $410 resistance. Expect choppy trading between these levels until earnings provides a catalyst.

🚀 Breakout Targets: If earnings beat and we clear $410, the next major resistance doesn't appear until $420 (+3.4%) and then $430 (+5.8%). That's a clear runway for bulls.

😰 Downside Cushion: The $400 strike has the strongest support with $9.89B in net GEX. If we break below $400, the next safety net is $390 (-4% from current levels).

Note: These levels are dynamic and change throughout the day as options are bought/sold. But they give us excellent clues about where big money expects the stock to gravitate.

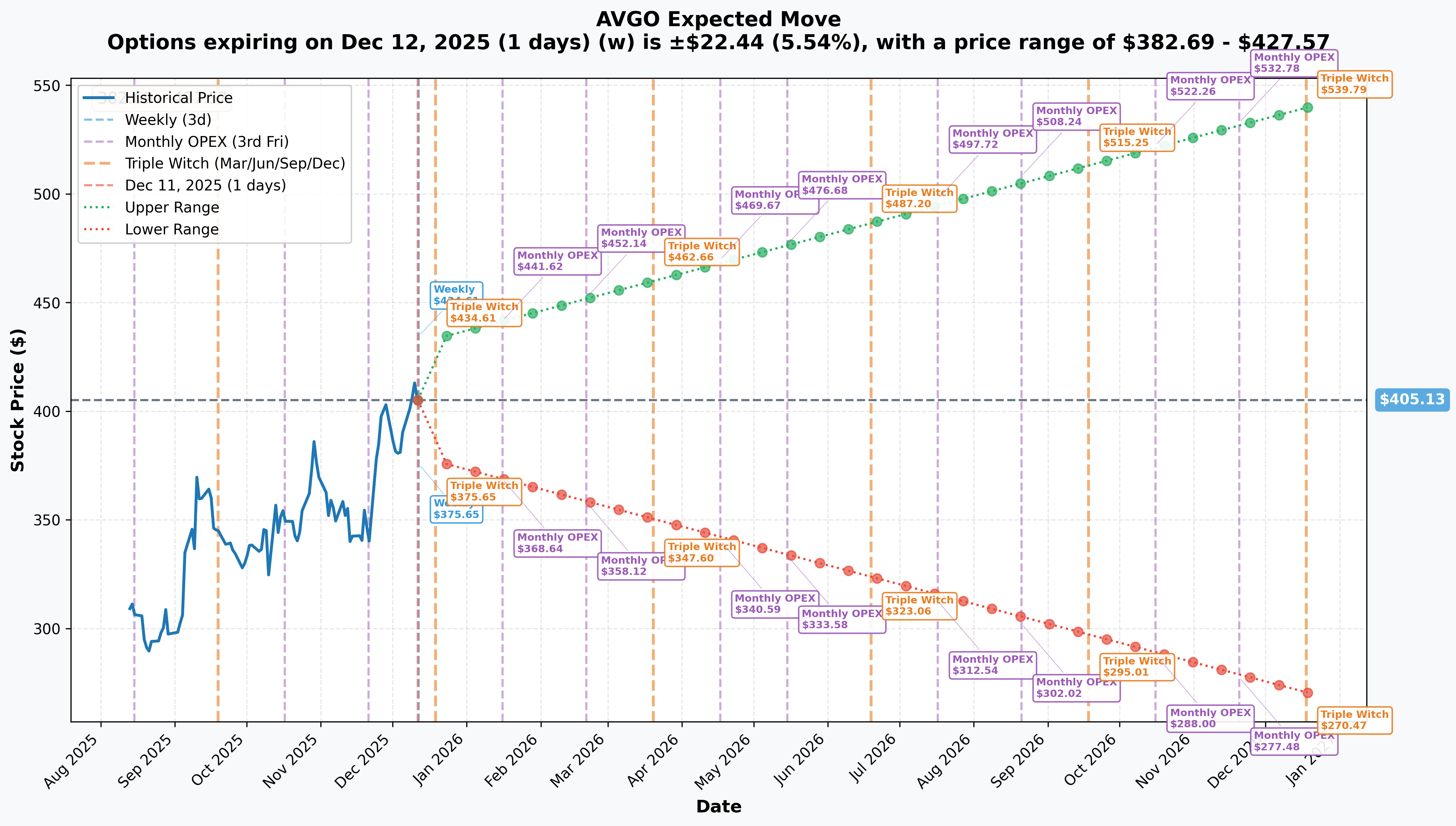

📊 Implied Move Analysis

What Is Implied Move? This shows how much the options market expects the stock to move by various expiration dates. It's basically the market's "best guess" baked into option prices.

Current Implied Moves (Based on $405 Stock Price):

📅 Weekly (December 12 Expiry - Tomorrow!):

- Implied Move: ±5.54% or ±$22.44

- Expected Range: $382.69 to $427.57

- Translation: Options traders are pricing in a $22 move just for tonight's earnings reaction. That's massive volatility!

📅 Monthly OPEX (December 19 - Next Week):

- Implied Move: ±6.99% or ±$28.30

- Expected Range: $376.82 to $433.44

- Translation: By next Friday's option expiration, the market expects a $28 range. This accounts for earnings plus any follow-through volatility.

📅 January 2026 LEAPS (Our $20M Trade Expiration!):

- Implied Move: ±9.04% or ±$36.62

- Expected Range: $368.64 to $441.62

- Translation: For the January 16 expiration (where our whale positioned), the market expects a $37 range. The $360 strike sits comfortably at the lower boundary.

📅 Year Ahead (December 2026 LEAPS):

- Implied Move: ±33.24% or ±$134.66

- Expected Range: $270.47 to $539.79

- Translation: Over the next year, options price in potential moves to either $540 (bull case) or $270 (bear case). That's the full spectrum.

What This Tells Us:

⚡ High Volatility Event: Tonight's earnings is expected to move the stock 5.5% - that's about $22 in either direction. For a $1.95 trillion company, that's huge.

🎯 Our Trade Makes Sense: The $20M call buyer's $360 strike sits well within the implied range for January expiration. Even if earnings disappoint and the stock drops to the lower boundary ($368), they're only $8 away from their strike.

💰 Volatility Premium: Options are expensive right now because of earnings uncertainty. After tonight, implied volatility will "crush" and option prices will drop sharply - even if the stock stays flat. Our whale paid up for this privilege.

📊 Risk/Reward Setup: Bulls have a clear path to $428+ if earnings beat (weekly upper range), while bears could push to $383 if guidance disappoints (weekly lower range).

🎪 Catalysts

🔥 Happening TODAY (December 11, 2025)

Q4 FY2025 Earnings Report (After Market Close):

Wall Street is watching this one closely. Here's what analysts expect:

📊 Consensus Estimates:

- Revenue: $17.49 billion (+24% YoY from $14.05B)

- EPS: $1.86 (+31% YoY from $1.42)

- AI Semiconductor Revenue: $6.2 billion (+66% YoY)

🎯 Key Items to Watch:

-

AI Revenue Guidance: Management previously guided to 60% AI growth into FY2026. Any confirmation or raise would be rocket fuel. According to StocksToTrade's analysis, the target is $40B+ in AI revenue for next fiscal year.

-

VMware Customer Retention: After 800-1,500% price increases alienated customers, investors want to know if the remaining 90% are sticking around. VMware generates $6.8B/quarter at 93% margins - any defection would hurt.

-

Hyperscaler Partnership Updates: Google, Meta, OpenAI, and rumored Microsoft partnerships represent $60-90 billion addressable market. Commentary on new design wins matters.

-

$110 Billion Backlog: Investors want visibility on this massive order book and when it converts to revenue.

Options Market Expectations: The market is pricing a 5.54% move (about $22) for tomorrow's reaction. That's volatility typically reserved for high-growth tech, not trillion-dollar semiconductor companies.

📅 Upcoming Catalysts (Next 6 Months)

1. Q1 FY2026 Earnings (Expected: Late February to Early March 2026)

- Consensus: $1.56 EPS (+41.82% YoY)

- First glimpse of FY2026 AI revenue trajectory

- Critical for validating the 60% growth story

2. Jericho4 Production Ramp (Q1-Q2 2026)

- According to Broadcom's press release, volume shipments to hyperscalers for distributed AI infrastructure

- Targets interconnecting 1M+ XPUs across multiple data centers

- Key product for AI networking dominance

3. OpenAI "Titan" XPU Deliveries (Q3 2026)

- First rack deliveries of $10 billion custom chip order

- Validates Broadcom's XPU competitiveness vs Nvidia GPUs

- Part of decade-long partnership through 2029

4. Apple "Baltra" AI Chip Production (2026)

- Per ainvest's research, mass production expected in 2026

- First Apple server chip for AI infrastructure

- Could significantly expand Broadcom's custom ASIC TAM

5. Potential Microsoft AI Chip Agreement (H1 2026)

- CoinCentral reports discussions for custom ASIC partnership

- Would add another $20-30 billion to addressable market

- Formal announcement could be major catalyst

⚖️ Regulatory Catalysts (Risk Factors)

1. EU CISPE Antitrust Lawsuit (2026 Developments)

- Cloud providers filed legal challenge to annul VMware acquisition approval

- Court hearings expected in 2026

- Low probability but high impact if successful

2. Japan Fair Trade Commission Investigation

- Investigation into VMware bundling practices

- Findings expected Q1-Q2 2026

- Potential fines or licensing restrictions

3. Fidelity Lawsuit (Ongoing)

- High-profile case affecting 50 million Fidelity clients

- Could encourage other enterprise customers to sue

- Discovery and hearings throughout 2026

📊 Analyst Activity (Recent Updates)

Major Upgrades in December 2025:

Wall Street is getting more bullish heading into earnings:

- HSBC: $535 target (highest on Street) - Buy rating on ASIC momentum

- UBS: $472 target (raised from $415) - Bullish on custom AI chips

- BofA Securities: $460 target (raised from $400) - Buy on Google partnership potential

- Morgan Stanley: $443 target (raised from $409) - Overweight on AI supply chain

- Susquehanna: $450 target (raised from $400)

- Rosenblatt: $440 target (raised from $400)

Consensus:

- 24 Buy ratings, 2 Hold ratings = Strong Buy

- Average target: $427.41 (+5.2% from current levels)

- Range: $210 (low) to $535 (high)

🎲 Price Targets & Probabilities

Based on gamma levels, implied move analysis, catalyst timing, and analyst targets:

🚀 Bull Case: $440-460 (8-13% Upside)

Timeline: 30-45 days Probability: 35%

What Needs to Happen:

- ✅ Q4 earnings beat on AI revenue ($6.2B+ semiconductor sales)

- ✅ FY2026 guidance confirms 60% AI growth trajectory ($40B+ AI revenue)

- ✅ VMware customer retention holds at 90%+ despite pricing backlash

- ✅ New hyperscaler partnership announcement (Microsoft or unnamed fourth customer)

- ✅ Breakthrough of $410 gamma resistance triggers momentum buying

Why This Works: The stock has clear runway to $420 and $430 gamma resistance levels once it clears the $410 wall. With 24 analysts rating it Strong Buy and average target of $427, there's institutional support for upside. The OpenAI $10B order and potential Microsoft partnership provide fundamental catalysts.

Key Levels:

- First target: $420 (December monthly upper range)

- Stretch target: $443 (Morgan Stanley target)

- Moonshot: $472 (UBS bull case)

⚖️ Base Case: $395-415 (Stay Range-Bound)

Timeline: 2-4 weeks Probability: 45%

What Needs to Happen:

- ✅ Earnings meet expectations but guidance is cautious

- ✅ Stock oscillates between $400 support and $410 resistance

- ✅ VMware concerns balance against AI optimism

- ✅ Regulatory investigations drag on without resolution

- ✅ Volatility crush post-earnings keeps stock pinned

Why This Makes Sense: AVGO is sitting at $406, right in the middle of the $400-410 gamma pocket. With $117.7B in call gamma vs $52.4B in put gamma, market makers will fight to keep the stock near these max pain levels through December OPEX (December 19). The implied move of 5.54% suggests a range of $383-428, centering around current levels.

Trading Strategy: This scenario favors theta decay. Selling premium (covered calls, cash-secured puts) at the $400 and $410 strikes would profit from range-bound action. Avoid directional bets until we break out of this gamma trap.

Key Levels:

- Support: $400 (strongest gamma support)

- Midpoint: $405 (current price)

- Resistance: $410 (strongest gamma resistance)

😰 Bear Case: $360-385 (5-11% Downside)

Timeline: 1-3 weeks Probability: 20%

What Needs to Happen:

- ❌ Earnings miss or guidance disappoints on AI growth trajectory

- ❌ VMware customer defections accelerate beyond management's expectations

- ❌ Regulatory action in EU or Japan forces pricing changes

- ❌ Broader tech sector sell-off on Fed hawkishness or recession fears

- ❌ Nvidia's Blackwell GPUs prove superior, shrinking ASIC TAM

What Could Go Wrong: Gartner expects VMware to lose 35% of workloads over 3 years - any acceleration would hurt the $6.8B quarterly software revenue. The stock trades at 47x forward P/E, pricing in flawless execution. Marvell's 58% revenue growth vs AVGO's 22% suggests market share losses in custom ASICs.

Meanwhile, Nvidia maintains 80%+ AI chip market share, and if hyperscalers decide general-purpose GPUs work better than custom ASICs, Broadcom's growth thesis unravels fast.

Key Levels:

- First support: $390 (gamma support #2)

- Critical support: $383 (weekly implied move lower bound)

- Major support: $360 (monthly gamma support & our whale's strike)

Protection Strategy: The $360 put strike shows strong gamma support ($5.16B net GEX). If we're headed down, this is where market makers will defend. Not coincidentally, this is exactly where our $20M whale positioned their call strike - even smart money expects this level to hold.

💡 Trading Ideas

🛡️ Conservative: The "Sleep Well" Iron Condor

For traders who want income without the stress

Strategy: Sell Dec 19 $390 Put / Buy Dec 19 $380 Put + Sell Dec 19 $420 Call / Buy Dec 19 $430 Call

The Setup:

- Collect premium by selling options at $390 and $420

- Buy protection at $380 and $430 to limit losses

- Max profit if AVGO stays between $390-$420 by December 19

Cost/Risk:

- Credit received: ~$200-250 per contract

- Max loss: $750-800 per contract

- Max profit: $200-250 per contract

- Probability of profit: ~65%

Why This Works: You're playing the gamma trap. The stock is pinned between $400 support and $410 resistance, and even post-earnings volatility should keep it within your $390-420 range. Both strikes sit outside the weekly implied move of $383-428, giving you buffer room.

Risk Management:

- Size this to risk no more than 2% of your portfolio

- Exit if the stock breaks $395 (lower) or $415 (upper) with conviction

- Take profits at 50% max gain (around $100-125 credit remaining)

Best For: Traders who believe earnings will be "fine" but not explosive, expecting range-bound trading through December OPEX.

⚖️ Balanced: The "Whale Copy" Call Spread

For traders who want upside but don't have $2M lying around

Strategy: Buy Jan 16 $380 Call / Sell Jan 16 $420 Call

The Setup:

- Similar thesis to the $20M whale trade (bullish into January)

- Use a spread to reduce cost and cap risk

- Different strike ($380 vs $360) to reduce premium

Cost/Risk:

- Net debit: ~$25-28 per contract ($2,500-$2,800 total)

- Max loss: $2,500-$2,800 per contract

- Max profit: ~$1,200-1,500 per contract (if stock at $420+)

- Breakeven: ~$408 (debit paid + lower strike)

Why This Works: You're riding the AI infrastructure wave with defined risk. If AVGO clears $410 resistance post-earnings and heads toward the $420-430 targets analysts are forecasting, you profit handsomely. The January expiration gives you 5+ weeks for the thesis to play out, including Q1 guidance and any CES 2026 announcements.

Profit Scenarios:

- Stock at $420 by January = +48% gain ($1,200 profit on $2,500 risk)

- Stock at $430 by January = +48% gain (capped by short call)

- Stock at $400 by January = -60% loss (about $1,500 loss)

- Stock at $360 by January = -100% loss (full $2,500 loss)

Risk Management:

- Exit if stock breaks below $390 and stays there (cut losses ~40%)

- Take profits at $415-418 (don't wait for $420, greed kills)

- Consider rolling up the short call if stock rips past $420 early

Best For: Traders moderately bullish on AI chip growth who want to piggyback the whale's thesis without the whale-sized capital requirement.

🚀 Aggressive: The "YOLO with Training Wheels" Call Butterfly

For traders who want home run potential with capped risk

Strategy: Buy 1x Jan 16 $410 Call / Sell 2x Jan 16 $430 Call / Buy 1x Jan 16 $450 Call

The Setup:

- This is a precision bet that AVGO lands between $420-440 by January

- Extremely low cost due to selling 2 calls at $430

- Massive profit if your target zone hits

- Capped loss even if you're completely wrong

Cost/Risk:

- Net debit: ~$150-250 per butterfly ($150-$250 total cost)

- Max loss: $150-250 (occurs if stock below $410 or above $450)

- Max profit: ~$1,750-1,850 (occurs if stock exactly at $430)

- Breakeven: $410.50 and $449.50 (approximately)

- Probability of profit: ~40%

Why This Is Aggressive But Smart: You're targeting the Morgan Stanley ($443) and Susquehanna ($450) price targets. If AVGO beats earnings, raises FY2026 guidance to $40B+ AI revenue, and announces a Microsoft partnership, the stock could easily hit $430-440. You risk just $150-250 to make $1,750-1,850 - that's a 7x to 12x return.

Profit Scenarios:

- Stock at $430 by Jan 16 = +700% to 1,100% gain (max profit)

- Stock at $425 by Jan 16 = +500% to 700% gain

- Stock at $420 by Jan 16 = +200% to 300% gain

- Stock at $415 by Jan 16 = -50% to -60% loss

- Stock at $405 by Jan 16 = -100% loss (but only $150-250)

Risk Management:

- Only risk what you can lose completely - this is a lotto ticket, not an investment

- Exit at 200%+ profit (take $500+ gain and run)

- Don't overthink it - this is a binary bet on earnings/guidance surprise

Best For: Traders with high risk tolerance who believe the AI chip supercycle is real and AVGO will blow out numbers. You're betting on a specific landing zone ($420-440), not just "up."

⚠️ Risk Factors

Let's keep it real - here's what could mess up the bullish thesis:

📉 Execution Risks

1. VMware Customer Exodus (HIGH RISK) The 800-1,500% price increases have customers furious. Gartner predicts 35% workload loss over 3 years. VMware generates $6.8B per quarter at 93% margins - lose 20% of customers and you're talking $1.36B quarterly revenue hit. That's not pocket change, even for a trillion-dollar company.

Why It Matters: Software revenue is the cash cow funding AI chip R&D. If VMware bleeds customers faster than expected, it constrains investment in the high-growth semiconductor business.

2. AI Revenue Growth Deceleration Management is guiding 60% AI growth into FY2026, targeting $40B+ in AI revenue. But comps get tougher as the base grows. Q4 expects $6.2B in AI semiconductor revenue - that's already a $25B annual run rate. Growing 60% from there requires enormous hyperscaler capex.

The Risk: If any of the big three customers (Google, Meta, OpenAI) delay orders or OpenAI's Titan XPU delivery slips past Q3 2026, growth could disappoint. A guidance miss tonight could trigger a 15-25% correction given the 47x forward P/E.

3. Hyperscaler Concentration Three customers represent the $60-90 billion TAM. Lose one major partner and 30-40% of your addressable market evaporates. Google could bring chip design fully in-house. Meta could decide Nvidia GPUs work better. OpenAI could pivot strategies.

Mitigation: The rumored Microsoft partnership would add diversification, but it's not confirmed yet.

🤺 Competitive Threats

1. Nvidia's Blackwell Architecture Nvidia maintains 80%+ AI chip market share for good reason - their GPUs work incredibly well. If Blackwell proves superior for the workloads Broadcom targets (inference, specialized training), the custom ASIC market could shrink faster than expected.

The Competitive Wedge: Nvidia's CUDA ecosystem is deeply entrenched. Developers know how to code for GPUs. Custom ASICs require specialized expertise - not every hyperscaler wants that complexity.

2. Marvell's Faster Growth Marvell grew revenue 58% YoY vs Broadcom's 22%. They're targeting 20% of the $94B TAM by 2028. Similar capabilities, similar customer base, but growing 2.6x faster. That's not noise - that's market share loss.

What It Means: BofA's projection that Broadcom could reach 24% market share by 2027 assumes they defend current position. If Marvell steals points, that projection drops to 18-20%, materially impacting growth rates.

3. AMD's MI355X Acceleration AMD is on track for 40% server CPU market share by end of 2025. They're bundling AI accelerators with CPUs. If hyperscalers can get "good enough" AI performance from AMD's integrated approach, why pay Broadcom for custom silicon?

⚖️ Regulatory & Legal Landmines

1. EU CISPE Antitrust Lawsuit Cloud providers want to annul the VMware acquisition. If successful (15-25% probability), EU could force divestitures or behavioral remedies. Europe is a material market - can't ignore this risk.

2. Japan Fair Trade Commission Actively investigating VMware bundling practices. Japan has been aggressive on tech antitrust. A finding against Broadcom could result in fines or force licensing changes that hurt margins.

3. Fidelity Lawsuit Domino Effect Fidelity's high-profile case affects 50 million clients. If they win, every other enterprise customer will pile on with similar suits. Class action risk is real. Worst case: Broadcom is forced to roll back VMware pricing, destroying the margin expansion thesis.

4. Broadcom's Antitrust History They settled an FTC complaint in 2021 for monopoly abuse. Pattern of regulatory scrutiny means they're under a microscope. Any aggressive move draws immediate investigation.

📊 Valuation & Macro Risks

1. Premium Valuation Compression At 47x forward P/E and 101x trailing P/E, AVGO is priced for perfection. The semiconductor peer group averages 25-35x forward P/E. Any deceleration in AI growth expectations could trigger violent multiple compression. Think 20-30% correction in weeks, not months.

2. Interest Rate Sensitivity High-growth tech valuations get crushed when rates rise. If the Fed holds rates higher for longer or reverses course on cuts, AVGO's premium multiple won't hold. A 100-200 bps rate increase could drive 10-20% stock decline purely from valuation reset.

3. AI Infrastructure Spending Slowdown Hyperscaler capex is cyclical and depends on AI monetization. If enterprises don't adopt AI fast enough or ROI disappoints, infrastructure spending decelerates sharply. Leading indicators to watch: Microsoft/Google/Meta capex guidance, GPU utilization rates, cloud revenue growth.

The Scary Scenario: AI bubble pops, hyperscalers cut capex 40%, Broadcom's $110B backlog gets canceled/delayed, and we find out how much of the stock price was hype vs fundamentals.

4. Semiconductor Cyclicality Management expects U-shaped recovery for non-AI semis into late 2026. Broadband, wireless, and industrial segments are weak. Right now AI masks this weakness. If AI slows AND traditional businesses stay weak, earnings could miss materially.

🎯 Binary Event Risk (TODAY)

Tonight's Earnings Is Make-or-Break:

The options market is pricing a 5.54% move ($22). That's huge volatility for a $1.95 trillion company. You could wake up tomorrow with AVGO at $428 (if they crush it) or $383 (if they disappoint).

Bull Case Triggers:

- AI revenue beats $6.2B target

- FY2026 guidance confirms $40B+ AI revenue

- Microsoft partnership confirmed

- VMware retention above 90%

Bear Case Triggers:

- AI revenue misses or guidance is cautious

- VMware customer defections accelerate

- Hyperscaler order delays mentioned

- Margin pressure from competition

The Bottom Line on Risk: This isn't a "set and forget" stock. You need to watch earnings closely, monitor VMware customer retention quarterly, track competitive dynamics with Marvell/AMD/Nvidia, and keep an eye on regulatory developments. The upside is massive if the AI thesis plays out, but the downside is equally brutal if execution falters.

🎯 The Bottom Line

Real talk: This $20M call position is a bold bet on Broadcom's AI dominance, but it's not reckless. The buyer chose deep in-the-money strikes ($360 vs $399 stock) with 5+ weeks to expiration, giving them downside protection and time for the thesis to play out.

Here's what I think is happening:

👀 The Whale's Thesis: This trader believes tonight's earnings will beat, FY2026 guidance will confirm the 60% AI growth trajectory, and AVGO breaks out to the $420-440 range over the next month. They're willing to pay $20M in premium (mostly intrinsic value) to gain leveraged exposure to that move. The $360 strike sits right at major gamma support - even if they're wrong and the stock tanks, that level should hold.

📊 What The Charts Say: Technically, AVGO is at all-time highs with clear momentum, sandwiched between $400 support (strongest gamma level) and $410 resistance (first barrier to break). The weekly implied move suggests $383-428 range post-earnings. If we clear $410, there's runway to $420-430 with limited resistance. If we break $400, there's air pocket down to $390.

🎪 Catalyst Calendar: The next 6 months are stacked: Q4 earnings tonight, Q1 earnings in March, Jericho4 production ramp, OpenAI Titan deliveries in Q3, potential Microsoft partnership announcement. Wall Street has 24 Buy ratings with $427 average target (+5% from here). The setup favors bulls IF execution is flawless.

⚠️ But Here's The Rub: AVGO trades at 47x forward P/E, pricing in perfect execution of a 60% AI growth roadmap dependent on 3-4 hyperscaler customers. VMware's 800-1,500% price increases risk customer defections that would hurt the high-margin cash cow. Marvell growing 58% vs AVGO's 22% suggests market share losses. Regulatory scrutiny in EU, Japan, and the Fidelity lawsuit create asymmetric downside risk.

My Take:

🚀 If You're Bullish (40% conviction): The AI infrastructure buildout is real, Broadcom is uniquely positioned with custom ASICs and networking gear, and the $110B backlog provides visibility. Play it with defined-risk spreads (like the Balanced strategy) rather than naked calls. Target $420-440 by January.

😐 If You're Neutral (40% conviction): Expect range-bound trading between $400-410 gamma levels through December OPEX. Sell premium (iron condors, covered calls) to profit from theta decay and volatility crush post-earnings. Don't fight the gamma trap.

😰 If You're Bearish (20% conviction): The stock is priced for perfection at all-time highs. Any guidance disappointment, VMware defection acceleration, or competitive loss triggers 15-25% correction to $360-385. Buy protective puts at $390-400 strikes or sit in cash until the picture clarifies.

What I'm Watching Tonight:

- AI semiconductor revenue: Beat $6.2B or bust

- FY2026 guidance: Needs to confirm $40B+ AI revenue target

- VMware retention rate: Must hold 90%+

- New customer announcements: Microsoft or fourth hyperscaler would be rocket fuel

- Margin commentary: Any pressure from competition is red flag

Mark Your Calendar:

- December 11 (TODAY) after close: Q4 earnings report

- December 12: Market reaction (expect volatility)

- December 19: Monthly OPEX (gamma levels reset)

- January 16, 2026: Expiration of the $20M whale trade

- Late Feb/Early March 2026: Q1 FY2026 earnings

Final Thought: The whale who dropped $20M isn't gambling - they're making a calculated bet with downside protection. You can play the same thesis with smaller size and defined risk using spreads. But respect the binary risk: tonight's earnings will likely move the stock $20+ in either direction. If you can't stomach that volatility, wait for the dust to settle.

This is high-stakes poker, not investing. Play accordingly.

⚖️ Disclaimer

Options trading involves substantial risk and is not suitable for all investors. The value of options can fluctuate rapidly, and you can lose your entire investment. Past performance does not guarantee future results.

This analysis is for informational and educational purposes only - it is NOT financial advice. The author may hold positions in securities mentioned. Always conduct your own research and consult with a licensed financial advisor before making investment decisions.

Key Risks:

- Options can expire worthless, resulting in total loss of premium paid

- High volatility can cause rapid price swings in either direction

- Earnings events create binary risk - the stock can gap up or down significantly

- Gamma exposure levels change throughout the day - they are not static

- Implied moves are estimates, not guarantees - actual moves can be larger or smaller

Do your own due diligence. Never risk more than you can afford to lose. Trade smart, not big. 🎯