💊 $BMY $6.3M Call Sweep - Big Pharma Bull Loads Up Ahead of FDA Decision!

📅 March 3, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $6.3 MILLION on 15,000 Bristol-Myers Squibb $57.50 calls expiring March 20th - with the stock trading at $61.50, this in-the-money bet screams high conviction. The Z-Score of 12.43 makes this an extremely unusual trade, the kind of size that shows up only a handful of times per year on $BMY. With an FDA PDUFA date for Opdivo in Hodgkin lymphoma on April 8 and the stock riding a 30% three-month rally, this institution is buying leveraged upside exposure heading into a dense catalyst window.

📊 Company Overview

Bristol-Myers Squibb Co. (BMY) discovers, develops, and markets drugs across cardiovascular, oncology, and immunology therapeutic areas:

- Market Cap: ~$127.0B

- Industry: Pharmaceutical Preparations (SIC 2834)

- Exchange: NYSE

- Current Price: $61.50 (near 52-week high of $63.33)

- Employees: 32,500

- Primary Business: Immuno-oncology leader (Opdivo), cardiovascular (Eliquis, Camzyos), neuroscience (Cobenfy), hematology (Reblozyl, Breyanzi)

Bristol-Myers derives close to 70% of total sales from the US and is navigating one of the largest patent cliffs in pharma history, with ~$38B in revenue at risk from Eliquis and Opdivo exclusivity losses over the next few years. The Growth Portfolio (Opdualag, Reblozyl, Camzyos, Breyanzi, Cobenfy) now represents ~60% of quarterly revenue and grew 17% in full-year 2025.

💰 The Option Flow Breakdown

The Tape (March 3, 2026 @ 10:56:38):

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order Type | Strategy | Z-Score | Vol/OI Ratio |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:56:38 | BMY | BUY | CALL | 2026-03-20 | $57.50 | 15,000 | $6.3M | BTO | Long Call | 12.43 | 0.75 |

🤓 What This Actually Means

This is a buy-to-open (BTO) long call - a straight-up bullish bet! Here's the breakdown:

- 💸 Premium paid: $6.3M ($4.20 per contract x 15,000 contracts x 100 shares)

- 🎯 In-the-money by $4.00: $57.50 strike with $BMY trading at $61.50

- ⏰ Minimal time value: Only $0.20 of extrinsic value per contract - this buyer wants delta exposure, not a speculative lottery ticket

- 📊 Position size: 15,000 contracts = 1,500,000 shares worth ~$92.3M notional exposure

- 🐋 Institutional footprint: Vol/OI ratio of 0.75 confirms heavy activity relative to existing open interest

What's really happening here:

This deep in-the-money call behaves almost like a synthetic long stock position. With only $0.20 of time value at risk per contract ($300K total), the buyer is essentially leveraging up ~$92M worth of $BMY exposure for $6.3M. The March 20 expiration puts this trade right in front of the April 8 FDA PDUFA date for Opdivo in Hodgkin lymphoma - any positive pre-announcement chatter or pipeline newsflow could push this stock to new 52-week highs.

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-Score: 12.43) - A 12.4x Z-Score means this trade is far beyond normal activity for $BMY. Trades of this magnitude on this ticker show up only a few times per year. The 15,000-contract clip is a clear institutional stamp.

📈 Technical Setup / Chart Check-Up

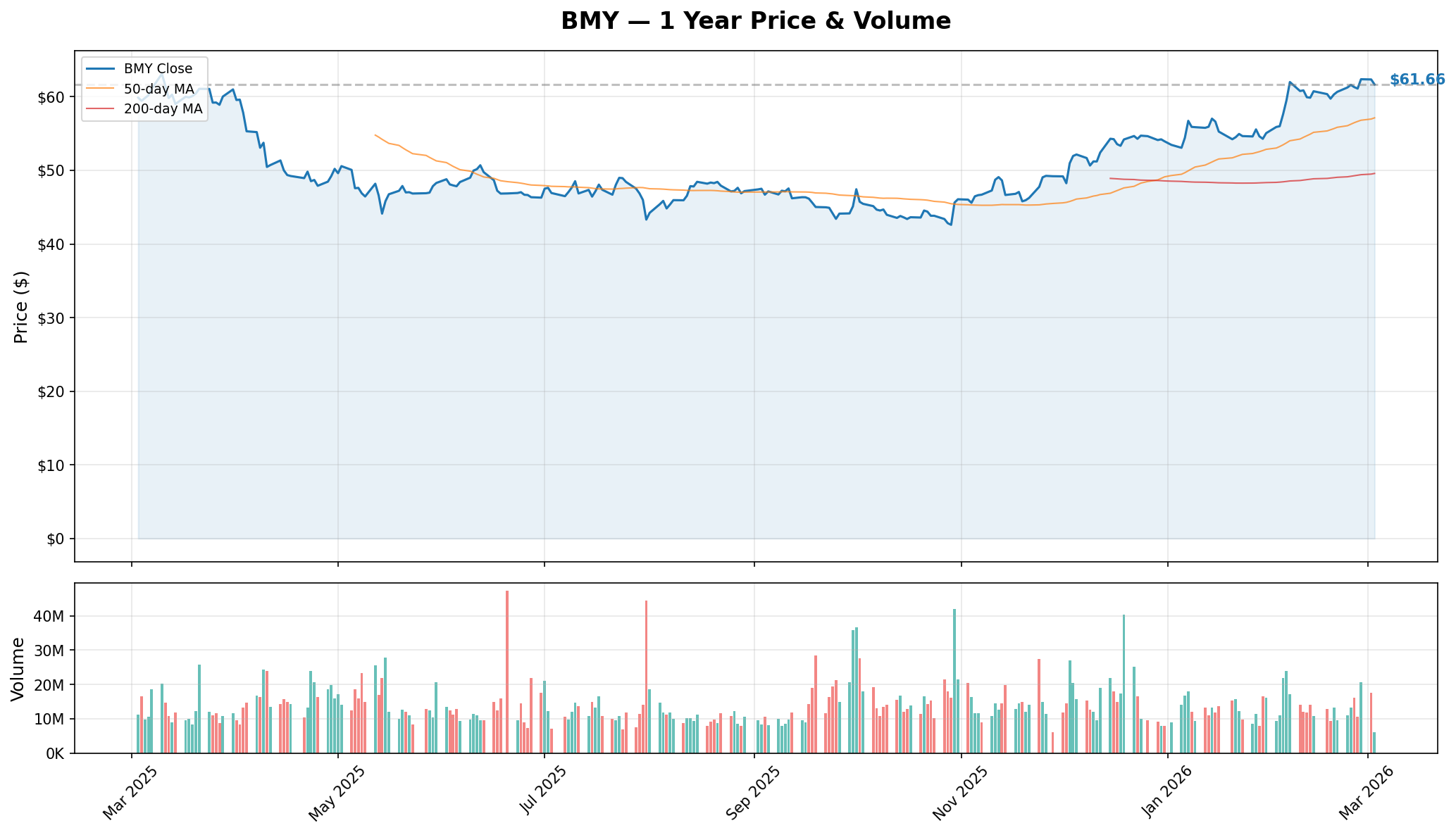

YTD Performance Chart

Bristol-Myers Squibb has been on a tear - the stock is up roughly 30% over the past three months, climbing from ~$47 in early December 2025 to $61.50 today. It's now trading near its 52-week high of $63.33, a dramatic turnaround from the $42.52 low hit last year.

Key observations:

- 📈 Strong uptrend: Consistent higher highs and higher lows since December 2025

- 💹 $60 breakout: Stock recently cleared the $60 psychological level and is holding above it

- 🎢 February earnings catalyst: The Q4 beat on February 5 launched the stock from the mid-$50s to the low $60s

- 📊 Near 52-week highs: Only $1.83 below the all-time high of $63.33 - a breakout could trigger fresh momentum

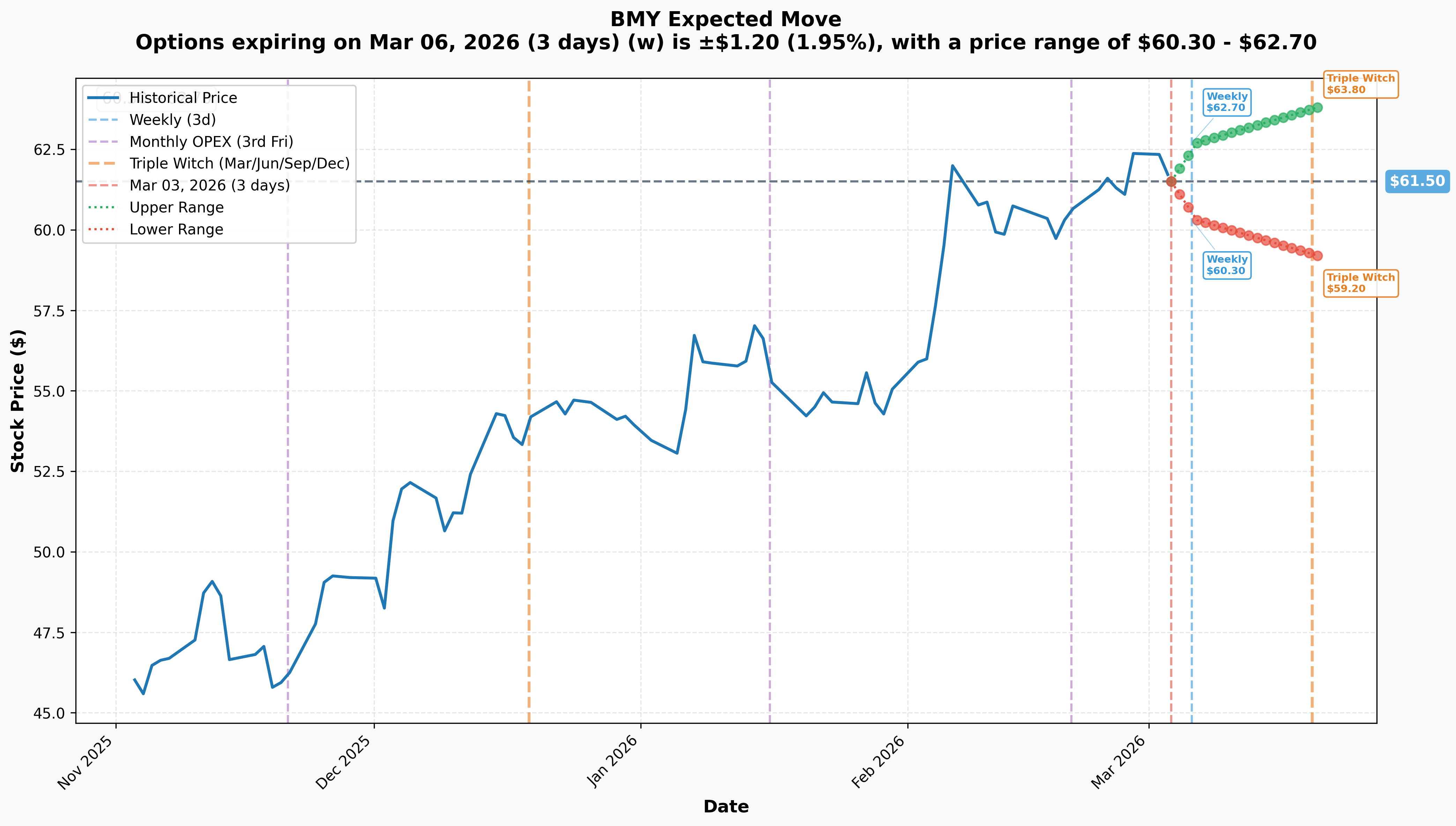

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Mar 6 - 3 days): +/-$1.20 (+/-1.95%) --> Range: $60.30 - $62.70

- 📅 Monthly OPEX / Triple Witch (Mar 20 - 17 days): +/-$2.30 (+/-3.74%) --> Range: $59.20 - $63.80

Translation for regular folks:

Options traders are pricing in a 1.95% move ($1.20) by Friday and a 3.74% move ($2.30) through March expiration. That's relatively tame for a pharma stock heading into a major FDA catalyst window. The upper implied move target of $63.80 would push $BMY to a new 52-week high. The lower bound at $59.20 aligns with the pre-earnings breakout zone that should act as support.

For this specific trade (March 20 expiration), the breakeven at $61.70 ($57.50 strike + $4.20 premium) is just $0.20 above the current price. This buyer barely needs the stock to move to break even - they're positioned for any upside from here to deliver leveraged gains.

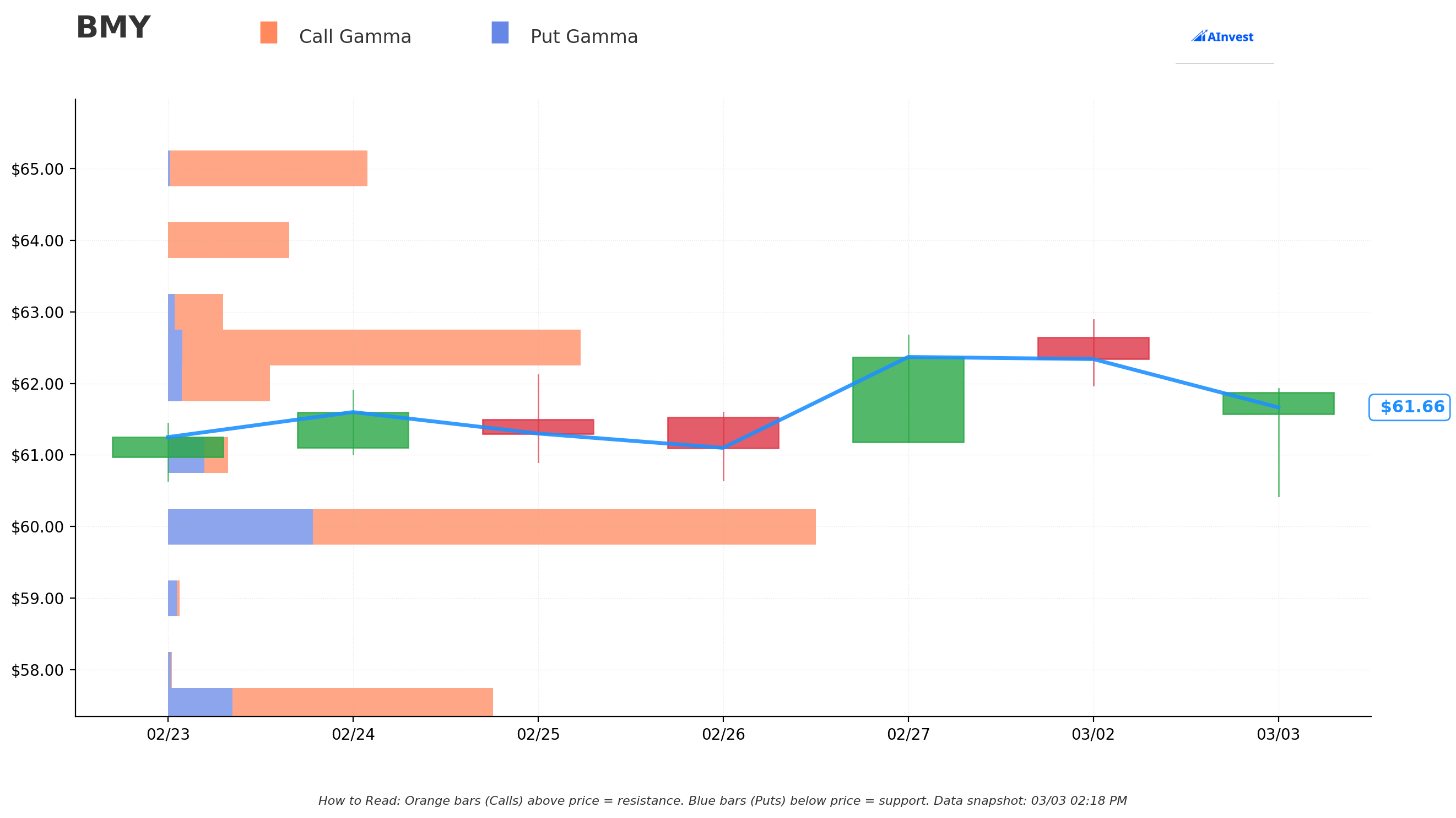

Gamma-Based Support & Resistance Analysis

🔵 Support Levels (Put Gamma):

- $60.00 - Round number and recent breakout level; heavy psychological support

- $59.20 - Implied move lower bound for March OPEX

- $57.50 - The call trade strike level; significant institutional interest anchored here

- $55.00 - Major gamma concentration and prior resistance-turned-support

- $50.00 - Maximum gamma strike; strongest structural support floor

🟠 Resistance Levels (Call Gamma):

- $62.70 - Implied move upper bound for weekly expiration

- $63.33 - Current 52-week high; the line in the sand for a breakout

- $63.80 - Implied move upper bound for March OPEX

- $65.00 - Next round-number target above the 52-week high

What this means for traders:

$BMY is coiled right below its 52-week high with strong support underneath. The gamma data shows heavy concentration at the $50 and $55 strikes, creating a solid floor well below current prices. The major decision point is whether $BMY can break above $63.33 - if it does, there's relatively little resistance until $65+. The institutional buyer at $57.50 has positioned themselves perfectly to capture that breakout move while having deep ITM protection if the stock pulls back.

🎪 Catalysts

🔥 Upcoming Catalysts

FDA PDUFA: Opdivo in Hodgkin Lymphoma - April 8, 2026 🏥

The FDA granted Priority Review for Opdivo plus chemotherapy in classical Hodgkin lymphoma (adults and pediatric). If approved, this expands Opdivo into a significant new front-line oncology indication. Opdivo is already generating $2.69B per quarter - this label expansion supports franchise durability ahead of the 2028 patent expiry. This is the catalyst the $6.3M call buyer is likely positioning for.

Dividend Ex-Date - April 2, 2026 💰

$0.63 per share quarterly dividend payable May 1, 2026. That's a 4.1% annualized yield providing a valuation floor.

Q1 2026 Earnings - April 30, 2026 📊

Next earnings report expected April 30. Key metrics to watch:

- 📊 Cobenfy ramp trajectory (Q4 was $51M - can it accelerate?)

- 💊 Eliquis volume post-IRA price reset ($231 vs. $521 list price)

- 🏥 Opdivo Qvantig subcutaneous conversion rate

- 🌍 Camzyos international expansion progress

FDA PDUFA: Iberdomide in Multiple Myeloma - August 17, 2026 🧬

FDA accepted BMS's application for iberdomide with Breakthrough Therapy Designation and Priority Review. This first-in-class CELMoD agent could be a blockbuster in the $20B+ multiple myeloma market and a direct successor to the declining Revlimid franchise.

Milvexian Phase 3 Data - 2026 📋

The Librexia AF and Librexia STROKE trials are studying 50,000+ patients. If positive, milvexian becomes a next-gen anticoagulant replacement for Eliquis with reduced bleeding risk - representing multi-billion-dollar revenue potential.

Cobenfy ADEPT Program Readouts - End of 2026 🧠

ADEPT-2 data in Alzheimer's psychosis expected by year-end 2026. If positive, opens a large underserved market of 2.5M+ Alzheimer's patients with psychosis symptoms.

Triple Witch OPEX - March 20, 2026 📅

Major options expiration (same day as this call trade's expiry) could create elevated volatility and hedging flows. Implied move prices a $59.20-$63.80 range through this date.

⏪ Recent Catalysts (Already Happened)

Q4 2025 Earnings Beat (February 5, 2026) 📈

Bristol-Myers crushed Q4 estimates - revenue of $12.5B beat the $11.93B consensus by 4.8%, and adjusted EPS of $1.26 beat $1.20 by 4.6%. The Growth Portfolio delivered $7.4B (+16% YoY), and management raised 2026 guidance above consensus to $46.0B-$47.5B in revenue.

Analyst Price Target Increases (February-March 2026) 📊

Multiple firms raised targets after the earnings beat: Guggenheim to $72, Bank of America to $68, Citigroup to $64, Wells Fargo to $60. Consensus average is $60.71 across 9 Buy, 12 Hold, and 1 Sell ratings.

TD Cowen Healthcare Conference (March 2, 2026) 🎤

CEO Chris Boerner presented strategic vision emphasizing BMS's goal to be the "fastest-growing pharmaceutical firm by the end of the decade," highlighting Camzyos, Cobenfy, and Opdivo Qvantig as key growth drivers.

Milvexian ACS Trial Discontinuation (December 2025) ❌

BMS and J&J stopped the Phase 3 Librexia ACS trial after an interim analysis determined it was unlikely to meet the primary efficacy endpoint. The AF and stroke prevention trials continue.

Microsoft AI Collaboration (March 2026) 🤖

BMS announced a collaboration with Microsoft to deploy AI algorithms for early detection of lung cancer in underserved communities.

🎲 Price Targets & Probabilities

Using implied move data, gamma levels, analyst targets, and upcoming catalysts:

📈 Bull Case (30% probability)

Target: $65-$72

How we get there:

- 🏥 April 8 Opdivo PDUFA approval in Hodgkin lymphoma extends the franchise runway and boosts sentiment

- 📈 Stock breaks above the $63.33 52-week high, triggering breakout momentum and short covering

- 📊 Analyst upgrades follow the breakout - Guggenheim's $72 target becomes the consensus pull

- 💊 Eliquis volume growth proves stronger than expected under IRA pricing, validating the "lower price = more volume" thesis

- 🤝 Additional business development deals (CEO Boerner said BD remains a top priority) add pipeline excitement

- 📈 The Growth Portfolio narrative strengthens as Camzyos, Breyanzi, and Reblozyl all exceed quarterly expectations

Impact on the trade: This is the home run scenario. At $65, the $57.50 calls are worth $7.50 intrinsic ($11.25M value on $6.3M invested = 79% return). At $72 (Guggenheim target), the calls are worth $14.50 ($21.75M = 245% return).

🎯 Base Case (50% probability)

Target: $59-$64 range-bound

Most likely scenario:

- ✅ Stock consolidates near 52-week highs, digesting the 30% three-month rally

- 📊 Pre-PDUFA positioning keeps a bid under the stock ahead of April 8

- 💰 4.1% dividend yield and 9.75x forward P/E provide valuation support

- ⚖️ Market waits for Q1 earnings (April 30) to validate the above-consensus 2026 guidance

- 🔄 Implied move range of $59.20-$63.80 captures the most probable trading band

Impact on the trade: At the current price of $61.50, the $57.50 calls are already $4.00 ITM. The buyer breaks even at $61.70 and profits on any move higher. Even in a sideways scenario, the deep ITM structure means minimal time decay erosion.

📉 Bear Case (20% probability)

Target: $52-$57

What could go wrong:

- 😰 Opdivo PDUFA gets a Complete Response Letter (CRL) or is delayed - would shake confidence in the franchise

- 📉 Cobenfy adoption continues to disappoint (Q4 sales of $51M missed expectations), and ADEPT-2 trial integrity concerns grow

- ⚖️ Morgan Stanley's $40 target and Underweight rating gains traction if growth stalls

- 💊 Eliquis EU patent expiry in H2 2026 starts weighing on sentiment earlier than expected

- 📉 Broad pharma sector rotation or macro headwinds (tariffs, rate environment) drag the stock back toward $55 support

Impact on the trade: Below $57.50, the calls expire worthless and the buyer loses the full $6.3M. However, the $55 gamma support level and 4.1% dividend yield should limit downside.

💡 Trading Ideas

🛡️ Conservative: The "Pharma Dividend Shield" Put Sell

Play: Sell April 17 $57.50 puts on $BMY to collect premium at a strike you'd be happy owning the stock

Why this works:

- 💰 $57.50 is the same strike the institutional buyer chose - significant interest at this level

- 📊 That's 6.5% below current price, providing a solid cushion

- 💊 If assigned, you own $BMY at an effective cost basis below $56 (strike minus premium) with a 4.5%+ dividend yield

- 🛡️ Multiple support levels ($59.20 implied move, $57.50 strike, $55 gamma level) sit above your risk zone

- ⏰ 45 days of theta decay working in your favor

Estimated P&L:

- 💰 Collect ~$0.80-1.20 per contract (~1.5-2.0% yield on capital at risk)

- 📈 Keep full premium if $BMY stays above $57.50 at April expiration

- 📉 Worst case: own $BMY at ~$56.50 effective cost with a great dividend yield

Risk level: Low | Skill level: Beginner-friendly

⚖️ Balanced: The "PDUFA Momentum" Call Spread

Play: Buy the April 17 $62.50/$67.50 call spread to position for the April 8 Opdivo PDUFA approval

Why this works:

- 🏥 The April 8 PDUFA date falls before April 17 expiration, so you capture the binary event

- 📈 $62.50 is just $1 above current price - modest move needed for profitability

- 🎯 $67.50 cap aligns with Bank of America's $68 target

- 📊 Defined risk: you know exactly what you can lose going in

- 💰 Bull spread structure keeps the cost reasonable vs. buying naked calls

Estimated P&L:

- 💰 Net debit: ~$1.50-2.00 per spread

- 📈 Max profit: $3.00-3.50 per spread ($500 width minus debit) if $BMY above $67.50

- 📉 Max loss: Premium paid (~$150-200 per spread) if $BMY below $62.50

- 🎯 Breakeven: ~$64-$64.50 (roughly the 52-week high area)

Risk level: Moderate (defined risk) | Skill level: Intermediate

🚀 Aggressive: The "Follow the Whale" ITM Call

Play: Mirror the institutional trade on a smaller scale - buy March 20 $60 calls

Why this works:

- 🐋 You're literally following a $6.3M institutional bet into the same expiration

- 📈 $60 strike is ITM by $1.50, giving you delta exposure with some time value

- ⏰ 17 days to expiration captures any pre-PDUFA momentum heading into April 8

- 📊 If $BMY breaks above $63.33 (52-week high), this call accelerates rapidly

- 💡 The implied move upper target of $63.80 is your realistic profit target

Why this could go wrong:

- 💥 17 days is short - theta decay accelerates as you approach expiration

- 📉 If the stock pulls back below $60, time value evaporates quickly

- ⚠️ Triple Witch OPEX on March 20 can create unpredictable pin risk and gamma effects

Estimated P&L:

- 💰 Cost: ~$2.30-2.80 per contract

- 📈 At $63.80 (implied upper bound): calls worth $3.80, roughly 35-65% return

- 📈 At $65 (bull case): calls worth $5.00, roughly 80-115% return

- 📉 At $59.20 (implied lower bound): calls worth ~$0, total loss of premium

- 🎯 Breakeven: ~$62.50 (about 1.6% above current price)

Risk level: High (short-dated, directional) | Skill level: Advanced

⚠️ Risk Factors

Don't overlook these potential headwinds:

-

💊 The $38B patent cliff is real: Eliquis (

$14B annualized) and Opdivo ($10.8B annualized) both face exclusivity losses over the next few years. Eliquis EU patent expiry hits in H2 2026, and US generic entry is expected April 2028. Even with a thriving Growth Portfolio, replacing $38B in revenue is a massive undertaking. -

😰 Cobenfy adoption disappointment: Q4 2025 sales of $51M missed analyst expectations. Overcoming deeply entrenched prescribing habits for generic antipsychotics in schizophrenia is proving harder than anticipated. If the Alzheimer's ADEPT trials also disappoint, a major growth pillar weakens.

-

📉 Milvexian execution risk heightened: After the ACS trial failure in December 2025, the remaining AF and stroke prevention trials carry elevated scrutiny. A second milvexian failure would seriously undermine the post-Eliquis replacement narrative.

-

⚖️ ADEPT-2 trial integrity concerns: BMS disclosed "irregularities" at study sites in the Cobenfy Alzheimer's psychosis trial. Data quality questions could complicate any future regulatory filing even if efficacy data look positive.

-

🏥 PDUFA rejection risk: While Opdivo's Priority Review in Hodgkin lymphoma is encouraging, FDA decisions are never guaranteed. A Complete Response Letter on April 8 would be a negative surprise for anyone positioned bullish into the date.

-

🐻 Morgan Stanley bear case: The firm maintains an Underweight rating with a $40 price target, arguing patent cliff headwinds are insufficiently priced and pipeline execution is uncertain. That implies 35% downside from current levels.

-

💸 IRA drug pricing impact: The negotiated Eliquis price of $231 vs. $521 list effective January 1, 2026 is a significant revenue headwind. Management guides that volume growth will offset the price cut, but if volume uplift disappoints, Eliquis revenue could erode faster than expected.

🎯 The Bottom Line

Real talk: A big player just loaded up $6.3M in deep-in-the-money $BMY calls with only 17 days to expiration. This isn't speculation - it's conviction positioning. With only $0.20 per contract in time value, they're essentially buying leveraged stock exposure. The Z-Score of 12.43 tells us this kind of flow on $BMY is extremely rare, the sort of trade you see a few times a year at most.

What this trade tells us:

- 🎯 Institutional money is positioning for continued upside ahead of the April 8 Opdivo PDUFA

- 💰 The deep ITM structure says "I want delta exposure now" - not a speculative gamble

- 📊 The March 20 expiration captures pre-PDUFA momentum without taking the binary event risk itself

- 🐋 15,000 contracts = $92M notional - this is serious institutional capital at work

If you're bullish on $BMY:

- ✅ The fundamental story is strong: Growth Portfolio at 60% of revenue and growing 17%, above-consensus 2026 guidance, 9.75x forward P/E

- 📊 Multiple analyst upgrades target $64-$72 (Guggenheim at $72, BofA at $68)

- 📈 A breakout above $63.33 (52-week high) could trigger fresh momentum with limited resistance above

- 💊 Two FDA PDUFA dates (April 8 and August 17) provide binary upside catalysts

- 💰 4.1% dividend yield gives you a paycheck while you wait

If you're watching from the sidelines:

- 🎯 A pullback to $59-$60 (near the implied move lower bound) would be a strong entry point

- 📊 Wait for the April 8 PDUFA outcome if you want to reduce binary event risk

- 💡 The institutional ownership at 80.68% with Norges Bank initiating a ~$1.6B position signals smart money accumulation

If you're bearish:

- 📉 The patent cliff ($38B at risk) is a legitimate multi-year headwind

- 🎯 Morgan Stanley's $40 target represents the credible bear case

- ⚠️ Consider bear put spreads ($57.50/$52.50) for defined-risk downside plays

- ⏰ Wait for a failed breakout at $63.33 before pressing the short side - fighting a 30% rally with momentum is painful

Mark your calendar - Key dates:

- 📅 March 6 (Friday) - Weekly options expiration (implied range: $60.30-$62.70)

- 📅 March 20 - Triple Witch OPEX + This call trade expires (implied range: $59.20-$63.80)

- 📅 April 2 - Dividend ex-date ($0.63/share)

- 📅 April 8 - FDA PDUFA for Opdivo in Hodgkin lymphoma

- 📅 April 30 - Q1 2026 earnings report

- 📅 August 17 - FDA PDUFA for iberdomide in multiple myeloma

Final verdict: This $6.3M call trade is a strong signal that smart money expects $BMY to either hold its ground or push higher over the next 17 days. The deep ITM structure, massive size, and extreme Z-Score all point to a high-conviction institutional bet positioned ahead of a favorable catalyst window. $BMY's combination of a discounted valuation (9.75x forward P/E), accelerating Growth Portfolio, and dense upcoming catalysts makes this one of the more compelling pharma setups right now. The biggest risk? The stock has already rallied 30% in three months - you'd be buying near 52-week highs. But as this whale just showed us, sometimes the best trades are the ones that ride momentum into a catalyst.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-Score of 12.43 reflects this specific trade's unusualness relative to recent activity - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading.

About Bristol-Myers Squibb Co.: Bristol-Myers Squibb is a global biopharmaceutical company with a ~$127B market cap, focused on discovering, developing, and delivering medicines for cardiovascular, oncology, immunology, and neuroscience therapeutic areas. The company is a leader in immuno-oncology (Opdivo) and derives approximately 70% of sales from the US market.