💊 CAPR $6.2M Deep ITM LEAP Call Sale - Insider-Level Profit-Taking Before Critical FDA Catalyst! 💰

📅 March 6, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dumped $6.2 MILLION in deep in-the-money CAPR LEAP calls this morning - selling 3,000 contracts of the $7 strike January 2028 calls while the stock trades at $25.48. This is a massive profit-harvesting trade from someone who likely rode CAPR's epic run from ~$4 to $25+, cashing out just 5 days before the MDA Conference late-breaking HOPE-3 presentation on March 11. Translation: A big winner is taking chips off the table right before the next binary event.

📊 Company Overview

Capricor Therapeutics (CAPR) is a clinical-stage biotech company focused on transformative cell and exosome-based therapeutics, with its entire valuation riding on one drug:

- Market Cap: ~$1.4 Billion

- Industry: Pharmaceutical Preparations (Biotechnology)

- Current Price: $25.48 (down ~12.6% today from prior close of ~$28.32)

- Primary Business: Developing Deramiocel (CAP-1002), an allogeneic cardiac-derived cell therapy for Duchenne muscular dystrophy (DMD) - a devastating rare disease that causes progressive muscle degeneration

- Employees: ~160 | Headquarters: San Diego, CA

- Key Partner: Nippon Shinyaku - exclusive commercialization partner for U.S., Japan, and Europe

This is as binary as biotech gets. No approved products. No revenue from drug sales. Everything depends on whether the FDA approves Deramiocel - which would make it the first cell therapy ever approved for DMD.

💰 The Option Flow Breakdown

The Tape (March 6, 2026 @ 11:24:08):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:24:08 | CAPR | MID | SELL | CALL $7 | 2028-01-21 | $6.2M | $7 | 3K | 208 | 3,000 | $25.48 | $20.50 |

🤓 What This Actually Means

This is a massive profit-taking trade on deep-in-the-money LEAP calls. Let me break this down:

- 💸 Huge premium collected: $6.2M ($20.50 per contract x 3,000 contracts)

- 🎯 Extremely deep ITM: $7 strike with stock at $25.48 = $18.48 of intrinsic value baked in

- ⏰ Minimal time value for a LEAP: Only ~$2.02 of time value remaining on a 22-month option - that's unusual. This person isn't paying for hope; they're monetizing a winner

- 📊 Volume vs Open Interest: 3,000 contracts traded vs only 208 open interest = 14.4x Vol/OI ratio - this is overwhelmingly a closing/liquidating trade

- 🏦 Classified as Sell-to-Open with MEDIUM confidence, but the Vol/OI ratio screaming at 14.4x strongly suggests this is actually a Sell-to-Close - someone unwinding a winning position they've held for months

What's really happening here:

Think about who buys $7 strike LEAP calls on a biotech. This was almost certainly purchased when CAPR was trading in the $4-8 range - before the Phase 3 HOPE-3 positive topline results in December 2025 sent the stock rocketing 439%. At that time, these calls might have cost $2-4 each. Now they're worth $20.50. That's a 5-10x return being harvested.

The timing is telling: selling 5 days before the MDA Conference presentation on March 11 and with the stock already down 12.6% today. This trader has decided the risk/reward of holding through another binary event no longer makes sense when they're already sitting on life-changing gains.

Unusual Score: 🔥 Z-Score of 72.82 (EXTREMELY UNUSUAL) - For context, anything above 3.0 is considered unusual. A z-score of 72.82 means this trade is roughly 73 standard deviations above CAPR's normal daily options activity. This kind of single-trade dominance happens maybe a handful of times per year across the entire biotech sector. The Vol/OI ratio of 14.4x confirms this is not routine hedging - this is a major position exit.

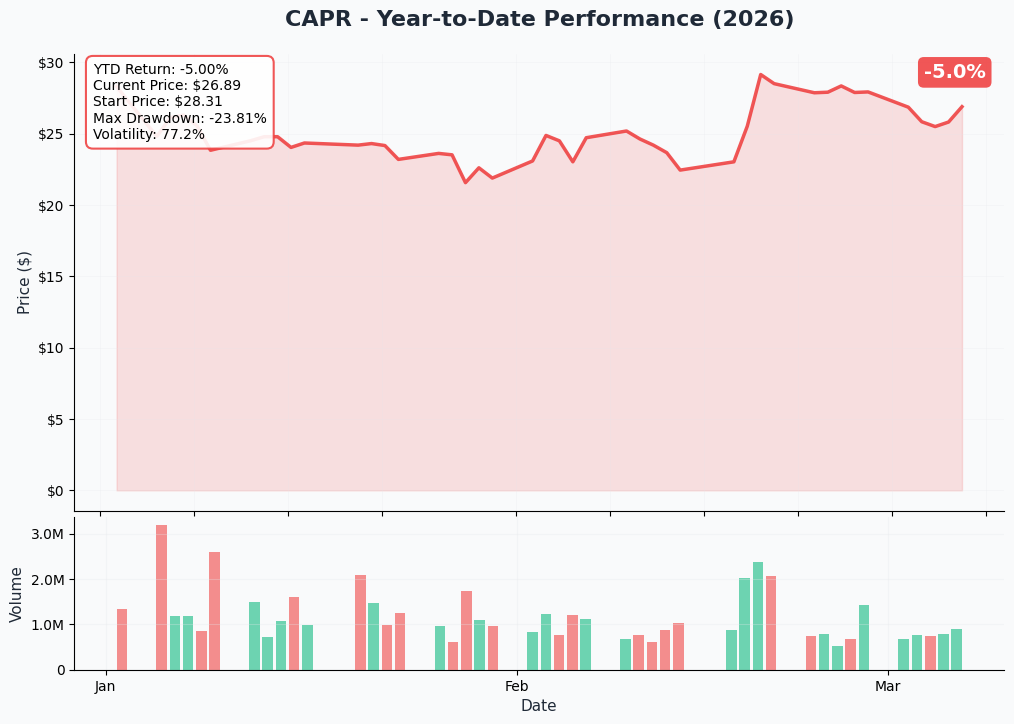

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

CAPR has had an absolutely wild ride. The stock traded as low as $4.30 in 2025 before the HOPE-3 Phase 3 data catapulted it over 400% in December. After reaching a 52-week high of $40.37, the stock has been consolidating and is currently down to $25.48 - a pullback of roughly 37% from those highs.

Key observations:

- 📈 Monster rally: From ~$4.30 to $40.37 driven by positive Phase 3 data and FDA pathway clarity

- 📉 Significant pullback: Down ~37% from highs, now finding potential support in the mid-$20s

- 🎢 Extreme volatility: This is a clinical-stage biotech - swings of 10-20% in a single day are not uncommon (case in point: down 12.6% TODAY)

- 💸 Dilution event: The $150M stock offering in December 2025 at $25.00/share put a near-term ceiling on the stock and explains the pullback from $40+ highs

- 📊 Three straight down days heading into today per StockTwits reporting, with retail sentiment turning bearish

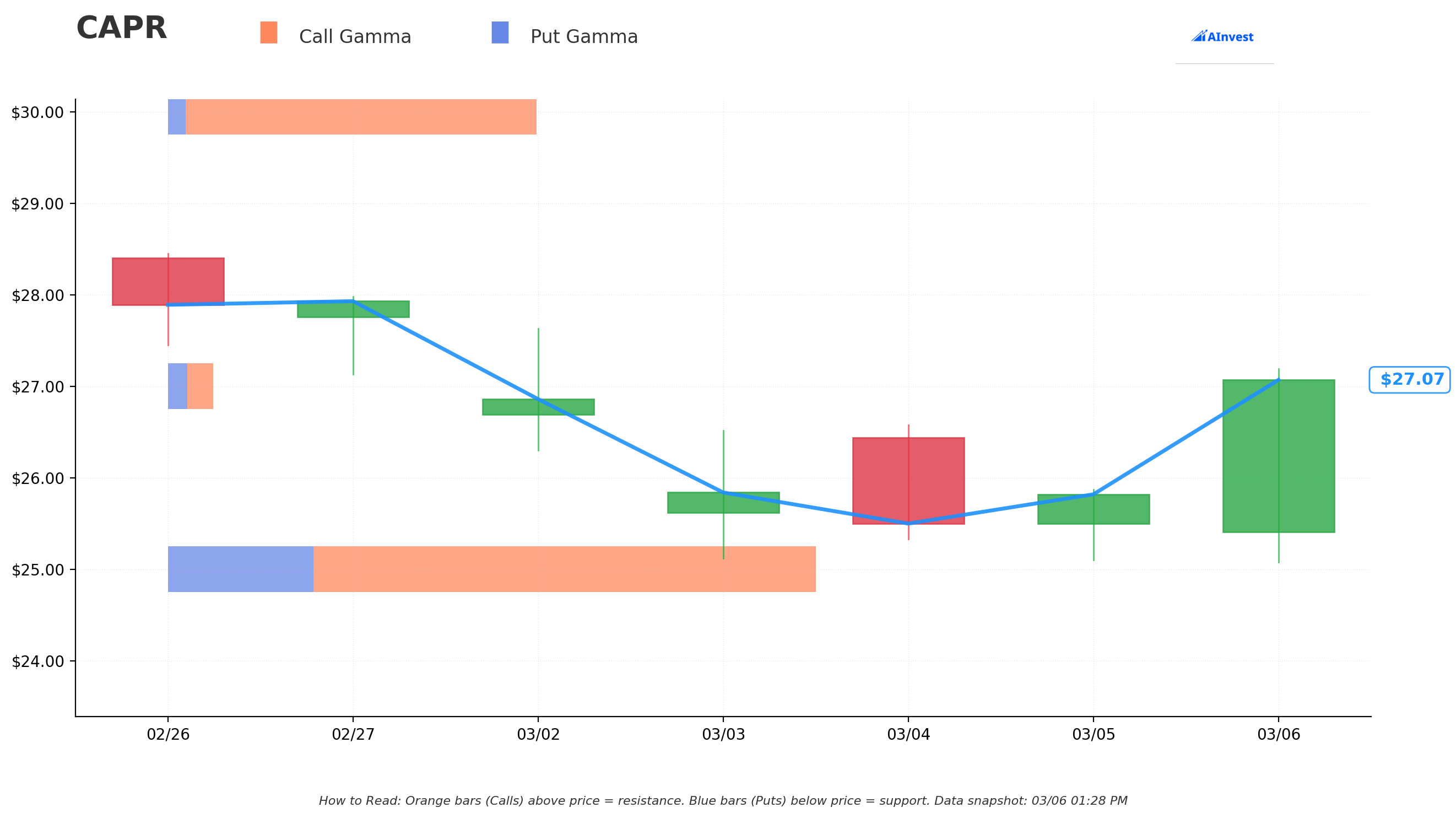

Gamma-Based Support & Resistance Analysis

Current Price: $25.48 (intraday at time of trade)

The gamma exposure map reveals where dealer hedging activity creates natural price magnets and walls:

🔵 Support Levels (Below Price):

- $26.00 - Nearby support with call gamma dominance (net GEX +0.011) - this is the first line of defense

- $25.00 - MAJOR support floor with 1.69 total gamma exposure (the STRONGEST gamma level on the board!) - dealers will aggressively buy dips here. This also aligns with the $150M offering price from December

- $24.00 - Secondary support, though weaker (net GEX slightly negative at -0.001)

- $22.50 - Deep support level with positive net gamma

🟠 Resistance Levels (Above Price):

- $27.00 - Immediate overhead resistance with 0.12 total gamma (modest ceiling)

- $28.00 - Secondary resistance at 0.061 total gamma

- $30.00 - MAJOR resistance wall with 0.95 total gamma (second strongest level!) - this is where sellers will pile in

- $32.00 - Extended resistance at 0.057 total gamma

What this means for traders:

The gamma map is screaming one thing: $25 is the floor, $30 is the ceiling. The massive gamma concentration at $25 (1.69 total - by far the highest) means market makers have enormous hedging exposure here. They'll buy aggressively if the stock dips toward $25, creating a natural floor. On the upside, the $30 strike has the second-largest gamma wall, meaning dealers will sell into any rally approaching that level.

Notice how today's price action is hovering right between the $25 mega-support and $27 first resistance. The stock is essentially pinned in a $25-$27 range by dealer hedging flows.

Net GEX Bias: Bullish (3.91 total call gamma vs 0.84 total put gamma) - Overall positioning leans bullish, suggesting market makers are net short calls and will buy stock on dips to hedge. This should provide a floor around $25.

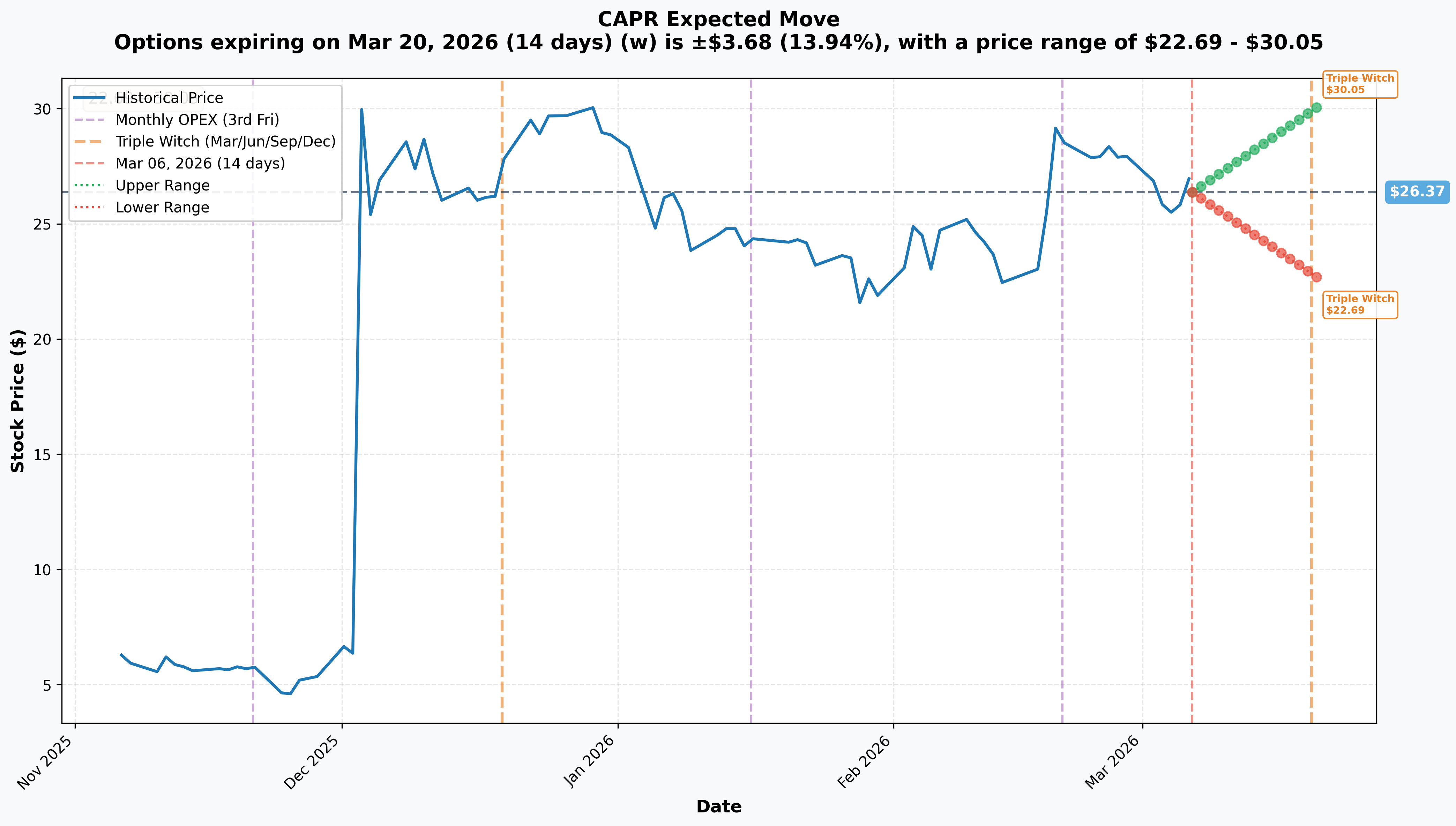

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Monthly OPEX / Triple Witch (March 20 - 14 days): ±$3.68 (±13.94%) → Range: $22.69 - $30.05

Translation for regular folks:

The options market is pricing in a nearly 14% move in either direction over the next two weeks. For a $26 stock, that's a $3.68 swing - meaning the market thinks CAPR could trade anywhere from $22.69 to $30.05 by March 20th OPEX.

That's a MASSIVE implied move for a two-week window, and it makes total sense when you consider the MDA Conference HOPE-3 presentation on March 11 falls right in the middle of this period. The market is pricing in significant event risk.

Key insight: The implied upper range of $30.05 lines up almost perfectly with the major gamma resistance at $30. And the lower range of $22.69 sits just below the $24 gamma support. The options market and the gamma map are telling the same story: $23-$30 is the battlefield for the next two weeks.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened)

Phase 3 HOPE-3 Positive Topline Results - December 3, 2025 📊

This was THE game-changer. Capricor announced that HOPE-3 met BOTH its primary skeletal muscle endpoint and key secondary cardiac endpoint:

- 💪 Skeletal muscle: Deramiocel showed a 1.2 point absolute difference from placebo on the PUL 2.0 test - representing a nearly 54% slowing of skeletal muscle disease progression

- ❤️ Cardiac function: 91% preservation of left ventricular ejection fraction (LVEF) vs placebo (p=0.041) - statistically significant

- 📊 106 subjects randomized across ambulatory and non-ambulatory cohorts

- 🚀 Stock surged 439% in December following this announcement per Motley Fool reporting

FDA Did NOT Request Additional Studies - January 2026 ✅

After reviewing the HOPE-3 topline data, the FDA formally requested only the full clinical study report (CSR) - and critically, did NOT request any additional clinical studies or new patient data. This was a hugely positive signal that the existing data package may be sufficient for approval.

CSR Submitted to FDA - February 2026 📝

Capricor submitted the HOPE-3 clinical study report to the FDA to address items in the prior Complete Response Letter from July 2025. The company now expects assignment of a new PDUFA target action date.

$150M Stock Offering at $25.00 - December 2025 💰

Following the Phase 3 data readout, Capricor priced a $150M public offering of 6M shares at $25.00 to fund commercialization preparation. This dilution event created a natural price ceiling and explains the pullback from $40+ highs.

Piper Sandler Price Target Raise to $45 🎯

Piper Sandler raised its price target from $20 to $45, maintained Overweight rating, and named CAPR a 2026 top pick. They anticipate potential FDA Priority Review with approval possible by mid-2026.

🚀 Upcoming Catalysts

MDA Conference HOPE-3 Late-Breaker - March 11, 2026 (5 DAYS AWAY!) 🧬

The full HOPE-3 data will be presented as a late-breaking oral presentation at the MDA Clinical and Scientific Conference at 2:45 PM ET on March 11:

- 🔬 Will include detailed musculoskeletal AND cardiac benefit data beyond topline results

- 📊 Could reveal secondary endpoint details, subgroup analyses, and safety data not previously disclosed

- 🐻 Risk: If full data shows any weaknesses vs topline results, stock could sell off hard

- 🚀 Upside: Stronger-than-expected detailed data could reignite rally toward $30+

- 👀 Investor attention is already building heading into this event

Q4 2025 / FY2025 Earnings - March 25, 2026 📊

- 💰 Will update cash position following the $150M offering - key for runway into potential FDA approval

- 📈 Management commentary on FDA engagement and PDUFA timeline expectations

- 🔬 Pipeline updates on exosome technology (StealthX platform)

FDA PDUFA Date Assignment - TBD (Expected Q1-Q2 2026) 📋

This is the BIG ONE. Following CSR submission in February, the FDA should assign a new PDUFA target action date for the Deramiocel BLA:

- ⏰ Piper Sandler expects a Type II 6-month review, putting potential approval around mid-2026

- 🏆 If approved, Deramiocel would be the first cell therapy ever approved for DMD - a landmark event

- 💊 Orphan Drug Designation, RMAT designation, and Rare Pediatric Disease designation could accelerate review

- 🎫 Potential Priority Review Voucher upon approval - worth $100M+ if sold

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, analyst targets, and the upcoming catalyst calendar, here are the scenarios through June 2026:

📈 Bull Case (25% probability)

Target: $35-$45

How we get there:

- 🚀 MDA Conference presentation reveals even stronger detailed data (subgroup wins, safety profile, etc.)

- 📋 FDA assigns PDUFA date with Priority Review timeline (6 months from submission)

- 🎯 Analyst upgrades cascade as Street models approval probability >80%

- 💰 Short covering and momentum buying push through $30 gamma resistance, then $32

- 🏆 Community and patient advocacy amplify positive data narrative

- 📈 Stock breaks above post-offering resistance and approaches Piper Sandler's $45 target

Key metrics needed: Clean detailed data at MDA, PDUFA date announced within 30 days, no CMC issues

🎯 Base Case (50% probability)

Target: $24-$30 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ MDA presentation confirms topline results without major surprises (positive but priced in)

- 📊 Stock bounces between $25 gamma floor and $30 gamma ceiling

- ⏰ Market waits for PDUFA date assignment as the next true catalyst

- 💤 Volatility compresses post-MDA as event risk dissipates

- 📈 Earnings on March 25 provides modest update but no major stock-moving news

- 🔄 Offering overhang at $25 continues to create natural support/floor

This is exactly what the LEAP seller is betting on. The stock consolidates in a range, their massive gains are already banked, and they avoid the risk of holding through more binary events. Smart play.

📉 Bear Case (25% probability)

Target: $15-$22

What could go wrong:

- 😰 MDA detailed data reveals weaknesses not apparent in topline results (effect size smaller in subgroups, safety signals, etc.)

- 🚨 FDA requests additional data or studies beyond CSR - delays PDUFA by 6-12 months

- 💸 CMC (manufacturing) issues flagged in BLA review - common for cell therapies

- 📉 Broader biotech selloff drags small-cap names lower

- 🐻 Break below $25 gamma support triggers cascade selling toward $22.50, then $20

- 💰 Offering participants who bought at $25 start dumping if stock breaks below their entry

Critical support levels:

- 🛡️ $25: THE line in the sand (strongest gamma floor at 1.69 total GEX + offering price)

- 🛡️ $22.50: Deep gamma support - if this breaks, things get ugly fast

- 🛡️ $20: Psychological round number and potential capitulation level

💡 Trading Ideas

🛡️ Conservative: Wait for MDA Data, Then Reassess

Play: Stay on the sidelines until after the March 11 MDA Conference presentation at 2:45 PM ET

Why this works:

- ⏰ Major binary event in 5 days - the detailed HOPE-3 data presentation could swing the stock 10-20% in either direction

- 💸 Options are EXPENSIVE right now (13.94% implied move = high IV premium) - you're paying through the nose

- 📉 Stock already down 12.6% today - catching a falling knife before a binary event is risky

- 🎯 Better entry likely post-MDA after the event risk premium evaporates (IV crush)

- 🤔 Even the $6.2M LEAP seller decided this wasn't worth holding through - why should you be more aggressive than someone with $6M+ at stake?

Action plan:

- 👀 Watch the MDA Conference presentation on March 11 at 2:45 PM ET

- 🎯 If data is clean and strong: look for entry on any post-presentation pullback toward $25-26 (gamma support)

- ❌ If data shows any weakness: stay away and wait for dust to settle at $20-22

- ✅ After MDA clarity, the NEXT catalyst to position for is the PDUFA date assignment

- 📊 Monitor earnings March 25 for cash position update and management confidence level

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

⚖️ Balanced: Post-MDA Bull Put Spread at Gamma Support

Play: After March 11 MDA data (assuming positive), sell a bull put spread at the $25 gamma wall

Structure: Sell $25 puts / Buy $22.50 puts (April 17 expiration, ~5 weeks out)

Why this works:

- 🛡️ The $25 strike is THE strongest gamma level (1.69 total GEX) - dealers will defend this level

- 💰 Also aligns with the $150M offering price ($25.00) - institutional buyers have skin in the game here

- 📊 Defined risk: $2.50 wide spread = $250 max loss per contract

- 🎢 IV crush after MDA data means you sell expensive premium to opening buyers

- ⏰ 5 weeks gives time for PDUFA date catalyst to potentially push stock higher

- 🤝 You're essentially betting that $25 holds as a floor - which gamma, offering price, and institutional positioning all support

Estimated P&L (adjust after MDA data):

- 💰 Collect ~$0.80-$1.20 credit per spread (post-MDA, depending on data quality)

- 📈 Max profit: Keep full credit if CAPR stays above $25 at April expiration

- 📉 Max loss: $1.30-$1.70 per spread if CAPR below $22.50

- 🎯 Breakeven: ~$23.80-$24.20

- 📊 Probability of profit: ~65-70% given gamma support and offering price floor

Entry timing: Only enter AFTER March 11 MDA data - confirm data is clean before selling puts

Position sizing: Risk 2-3% of portfolio max - this is still a binary biotech

Risk level: Moderate (defined risk, bullish at support) | Skill level: Intermediate

🚀 Aggressive: Pre-MDA Call Butterfly Targeting $30 Breakout

Play: Buy a call butterfly centered at the $30 gamma resistance for a cheap lottery ticket into MDA data

Structure: Buy 1x $27 call / Sell 2x $30 calls / Buy 1x $33 call (March 20 expiration)

Why this works:

- 💸 Butterflies are CHEAP - probably costs $0.50-$1.00 per spread given current IV

- 🎯 Max profit zone at $30 - exactly where the second-largest gamma wall sits

- 📊 Implied move upper range is $30.05 - options market thinks $30 is achievable

- 🚀 If MDA detailed data is a blowout positive, $30 is a realistic target within 2 weeks

- 🎰 Risk/reward skewed heavily: risk $50-100 to potentially make $200-250 (2-5x return)

Why this could blow up (SERIOUS RISKS):

- ❌ If MDA data disappoints or matches expectations (priced in), stock stays at $25-27 and butterfly expires worthless

- ⏰ Only 14 days to expiration - time decay is brutal

- 📉 Stock already down 12.6% today - momentum is AGAINST you

- 💸 Biotech options are expensive - butterfly may cost more than expected

- 🎢 Could lose 100% of premium (though it's a small amount)

Estimated P&L:

- 💰 Cost: ~$0.50-$1.00 per butterfly ($50-$100 risk per spread)

- 📈 Max profit: ~$2.50-$3.00 at $30 ($250-$300 per spread)

- 📉 Max loss: 100% of premium paid if CAPR below $27 or above $33

- 🎯 Breakeven: ~$27.50 on downside, ~$32.50 on upside

CRITICAL WARNING: This is a speculative bet on a biotech data event. Only use money you can afford to lose entirely. The butterfly structure limits your risk, but the probability of max profit is LOW (maybe 15-20%). Think of it as buying a lottery ticket, not making an investment.

Risk level: HIGH (can lose 100% of premium, but premium is small) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🧬 MDA Conference data risk in 5 days: The March 11 late-breaking presentation will reveal detailed HOPE-3 data beyond topline results. Subgroup analyses, secondary endpoints, and safety data could change the narrative in either direction. Topline data showed a 1.2-point absolute difference on PUL 2.0 - if detailed data shows this effect was concentrated in a small subgroup or came with safety signals, the stock could gap down 15-25%.

-

📋 FDA regulatory uncertainty remains HIGH: Despite positive HOPE-3 data and a Clean CSR submission, the prior Complete Response Letter cited that the BLA "does not meet the statutory requirement for substantial evidence of effectiveness." The FDA's request for only the CSR (no additional studies) is encouraging, but FDA approval is never guaranteed - they could still request more data, an advisory committee meeting, or issue a second CRL.

-

🎲 Ultimate binary stock - no revenue, no products: CAPR is a clinical-stage biotech with ZERO approved products and ZERO product revenue. The entire $1.4B market cap is a bet on Deramiocel getting approved. If the FDA says no, this stock could lose 60-80% of its value overnight. That's not fear-mongering - it's the reality of pre-revenue biotech investing.

-

💸 Recent dilution and offering overhang: The $150M offering at $25.00/share in December added 6 million shares (plus up to 900K overallotment). Investors who bought at $25 may become sellers on rallies to break even. This creates natural resistance near current levels.

-

📉 Stock down 37% from highs with bearish momentum: From $40.37 high to $25.48 today (including a 12.6% single-day drop), CAPR is in a clear downtrend. Three consecutive down days with increasing bearish sentiment on social media. Momentum traders may continue to sell into any bounce.

-

🐋 $6.2M smart money exit signals caution: When someone with a multi-million dollar winning position decides to cash out RIGHT BEFORE a major catalyst, it's worth paying attention. They clearly believe the risk of holding through the MDA presentation outweighs the potential upside. This isn't necessarily bearish on the long-term story, but it IS a warning about near-term risk/reward.

-

💊 Cell therapy manufacturing complexity: Even with a positive FDA decision, cell therapies are notoriously difficult to manufacture at scale. The original CRL cited CMC (Chemistry, Manufacturing, and Controls) issues alongside efficacy questions. Manufacturing problems could delay even a favorable regulatory outcome.

-

📊 Small market cap = big swings: At ~$1.4B, CAPR is a small-cap stock with ~54M weighted shares outstanding. It takes relatively small amounts of buying or selling to move the stock 5-10%. This cuts both ways but makes position sizing critical - one bad headline and you could be down 20% before your limit order even fills.

-

🌎 52-week range tells the story: $4.30 to $40.37. That's a nearly 10x range in 12 months. This is not a stock for the faint of heart. If you can't stomach watching your position drop 30-40% over a few weeks (like the recent decline from $40 to $25), CAPR is probably not for you.

🎯 The Bottom Line

Real talk: Someone rode CAPR from the $4-8 range to $25+ and just banked a $6.2M payday selling their deep ITM LEAP calls. That's a legendary trade - possibly a 5-10x return. And they're cashing out 5 days before the MDA Conference detailed data presentation, right as the stock drops 12.6% in a single session.

What this trade tells us:

- 🎯 A sophisticated player decided that ~500%+ gains are enough - they're not getting greedy ahead of a binary event

- 💰 The $7 strike LEAP with $20.50 price means only $2 of time value on a 22-month option - this is pure profit extraction, not strategy repositioning

- ⚖️ The 72.82 z-score (EXTREMELY UNUSUAL) reflects the sheer size of this exit relative to CAPR's normal activity

- 📊 Selling into a 12.6% down day suggests urgency - they wanted OUT today, not tomorrow

This is NOT a "CAPR is done" signal - it's a "the easy money has been made" signal.

If you own CAPR:

- ✅ Consider trimming 30-50% of your position before March 11 MDA data

- 🛡️ The $25 gamma level (strongest on the board) should provide support - set a mental stop just below at $24

- ⏰ If holding through MDA: understand you're making a binary bet on detailed data quality

- 📊 Keep core position if your thesis is FDA approval by mid-2026 per Piper Sandler's analysis

- 💰 Remember: the stock offering was priced at $25 - institutions have a floor here

If you're watching from the sidelines:

- ⏰ March 11 at 2:45 PM ET is the moment of truth - MDA Conference late-breaking oral presentation

- 🎯 Post-MDA pullback to $24-25 (if data is good but "priced in") would be a strong entry with gamma support

- 📈 Looking for: Clean safety profile, consistent subgroup effects, strong cardiac data - these would de-risk the FDA approval narrative

- 🚀 The REAL catalyst is the PDUFA date assignment - that's when the approval clock officially starts ticking

- ⚠️ Do NOT buy before MDA data unless you understand this is a binary event bet on a volatile biotech

If you're bearish:

- 🎯 Wait for MDA data before shorting - if data disappoints, the stock will come to you

- 📊 Key levels to watch: break below $25 gamma support opens path to $22.50, then $20

- ⚠️ Put spreads ($25/$22.50 or $25/$20) after MDA offer defined risk bearish plays

- 📉 Don't short a biotech ahead of a data catalyst - the upside surprise can be brutal

- ⏰ Shorting after a strong MDA presentation could be a better entry if stock pops to $28-30 resistance

Mark your calendar - Key dates:

- 📅 March 11 (Wednesday) at 2:45 PM ET - MDA Conference HOPE-3 late-breaking oral presentation - THIS IS THE BIG ONE

- 📅 March 20 - Monthly OPEX / Triple Witch (±13.94% implied move window)

- 📅 March 25 - Q4 2025 / FY2025 earnings report

- 📅 Q1-Q2 2026 (TBD) - FDA PDUFA date assignment for Deramiocel BLA

- 📅 Mid-2026 (estimated) - Potential FDA approval decision (if Priority Review granted)

Final verdict: CAPR sits at a fascinating crossroads. The Phase 3 data is legitimately positive - a 54% slowing of DMD progression with cardiac benefits is clinically meaningful. The FDA pathway looks cleaner than it did post-CRL. Analysts see $41+ per share if approval comes through. BUT - the stock has already rallied 400%+ from its lows, the detailed data presentation in 5 days creates binary risk, and smart money is cashing out $6.2M in gains RIGHT NOW.

The Deramiocel approval story is real, but the timing for new entries is tricky. Let the MDA data settle the near-term uncertainty. If the detailed results hold up, the PDUFA date catalyst will be the next major inflection point - and you'll want to be positioned before THAT, not before a conference presentation where most of the topline data is already known.

Patience pays in biotech. The approval story will still be there in a week. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. CAPR is a clinical-stage biotech with no approved products - the stock could lose 50-80% of its value on a negative FDA decision. The z-score of 72.82 reflects this specific trade's unusualness relative to CAPR's recent history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Binary biotech events create extreme risk with potential for 20%+ gaps in either direction.

About Capricor Therapeutics: Capricor Therapeutics is a clinical-stage biotechnology company with a $1.4 billion market cap, focused on developing Deramiocel, a first-in-class cell therapy for Duchenne muscular dystrophy (DMD). The company has partnerships with Nippon Shinyaku for U.S., Japan, and European commercialization, and its proprietary StealthX exosome platform for future therapeutic applications in the Pharmaceutical Preparations industry.