🏥 CI Massive $1.76M Short Call Bet - Smart Money Caps Healthcare Rally! 📉

📅 December 15, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just sold $1.76 MILLION in naked calls on Cigna Group this morning at 10:42:37! This whale dumped 6,000 contracts of March 2026 $320 strike calls in two massive blocks - capping upside on a stock trading at $275. With CI down -22.6% from September highs despite strong Q1 2025 earnings, smart money is betting this healthcare giant stays pinned below $320 through March. Translation: Institutional players think CI's rally is over, and they're collecting premium betting on consolidation or further downside!

📊 Company Overview

The Cigna Group (CI) is a global healthcare services powerhouse with integrated pharmacy benefits and health insurance operations:

- Market Cap: $73.38 Billion (8th largest healthcare company)

- Industry: Hospital & Medical Service Plans

- Current Price: $275.23 (down from $357.96 all-time high in September 2024)

- Primary Business: Express Scripts PBM (120M pharmacy customers), Cigna Healthcare (17M US medical members), Medicare/Medicaid plans (recently divested), specialty pharmacy (Accredo)

- Key Segment: Evernorth Health Services (including Express Scripts) is the crown jewel driving profitability

💰 The Option Flow Breakdown

The Tape (December 15, 2025 @ 10:42:37):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:42:37 | CI | BID | SELL | CALL $320 | 2026-03-20 | $869K | $320 | 4,000 | 108 | 4,000 | $275.23 | $4.29 |

| 10:42:37 | CI | BID | SELL | CALL $320 | 2026-03-20 | $888K | $320 | 2,000 | 108 | 2,000 | $275.23 | $4.50 |

Total Premium Collected: $1,757,000 across 6,000 contracts

🤓 What This Actually Means

This is a bearish-to-neutral covered call strategy or potentially naked short calls! Here's the breakdown:

- 💸 Massive premium collected: $1.76M total ($4.29 + $4.50 average = ~$4.36 per contract × 6,000 contracts)

- 📉 Cap on upside: $320 strike is 16.3% above current price - seller betting stock can't break $320 by March

- ⏰ Time horizon: 95 days to expiration (March 20, 2026) captures full Q4 2025 earnings cycle and regulatory developments

- 📊 Size matters: 6,000 contracts represents 600,000 shares worth ~$165M at current prices

- 🎯 Strategic positioning: Extremely low open interest (only 108 contracts before this trade!) means this trader is CREATING a new position, not closing

What's really happening here: This sophisticated trader is either:

- Covered call overwrite: Owns 600K shares of CI (worth ~$165M) and selling calls to generate $1.76M income while capping upside at $320

- Naked short calls: Betting CI won't rally 16%+ by March, collecting premium with defined risk above $320

The strategy says: "CI isn't going above $320 by March 20th. I'll collect $4.36/share right now and cap my gains at $320 if it somehow rallies 16%+."

Unusual Score: 🔥 EXTREMELY UNUSUAL (146x and 73x average size) - These are the 2 largest CI option trades in the past 30 days! Z-scores of 146.09 and 72.85 indicate this happens only a few times per year. When someone sells $1.76M in calls at specific strikes, they have STRONG conviction the stock is capped.

📈 Technical Setup / Chart Check-Up

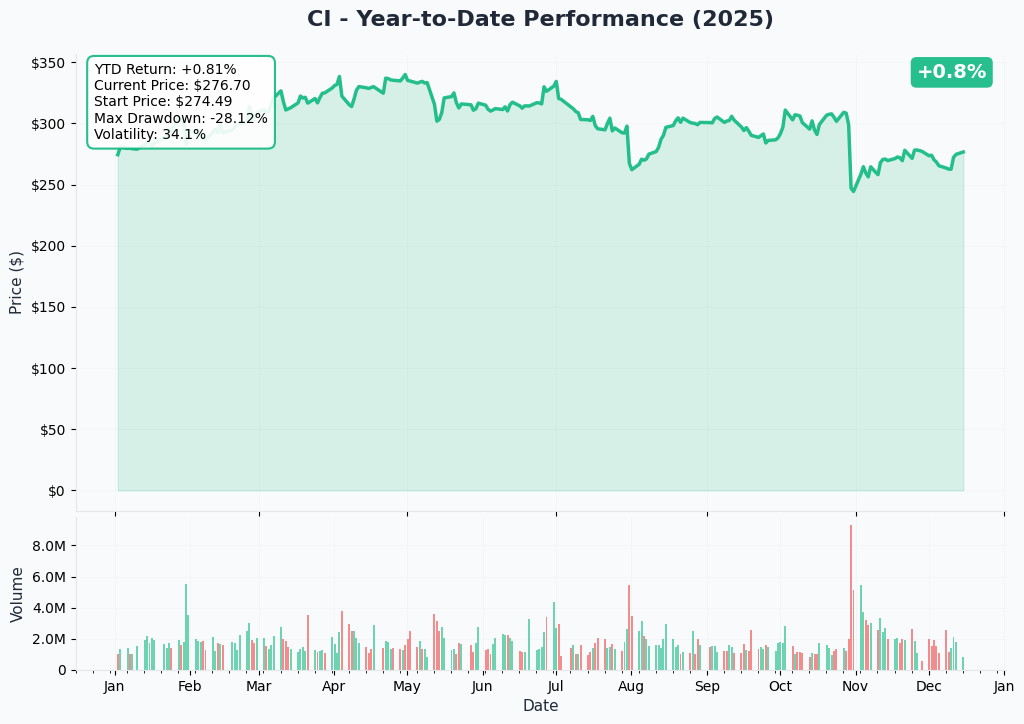

YTD Performance Chart

CI has had a brutal 2025 despite solid fundamentals. Starting the year around $320, the stock hit an all-time high of $357.96 in September 2024, then collapsed -22.6% to current levels around $275. The chart tells a story of regulatory overhang and PBM scrutiny destroying sentiment.

Key observations:

- 📉 Massive selloff: Peak-to-trough decline from $358 to $270 represents $24B in market cap destruction

- 🏥 Medicare divestiture impact: $3.3B sale to HCSC closed March 2025, removing revenue but adding buyback firepower

- ⚖️ PBM reform fears: FTC lawsuit and potential forced Express Scripts divestiture weighing heavily

- 📊 Q4 2024 earnings miss: MCR of 87.9% exceeded guidance, triggering analyst downgrades across Street

- 💔 Broken momentum: Failed to hold $300 support in November, now consolidating at $275 support zone

- 📈 Bullish Q1 2025: Beat by $0.39 and raised guidance to $29.60 EPS, but stock didn't respond positively

The technical setup shows a stock in no-man's land - not crashing but unable to rally despite strong fundamentals. This is EXACTLY the environment where selling covered calls makes sense.

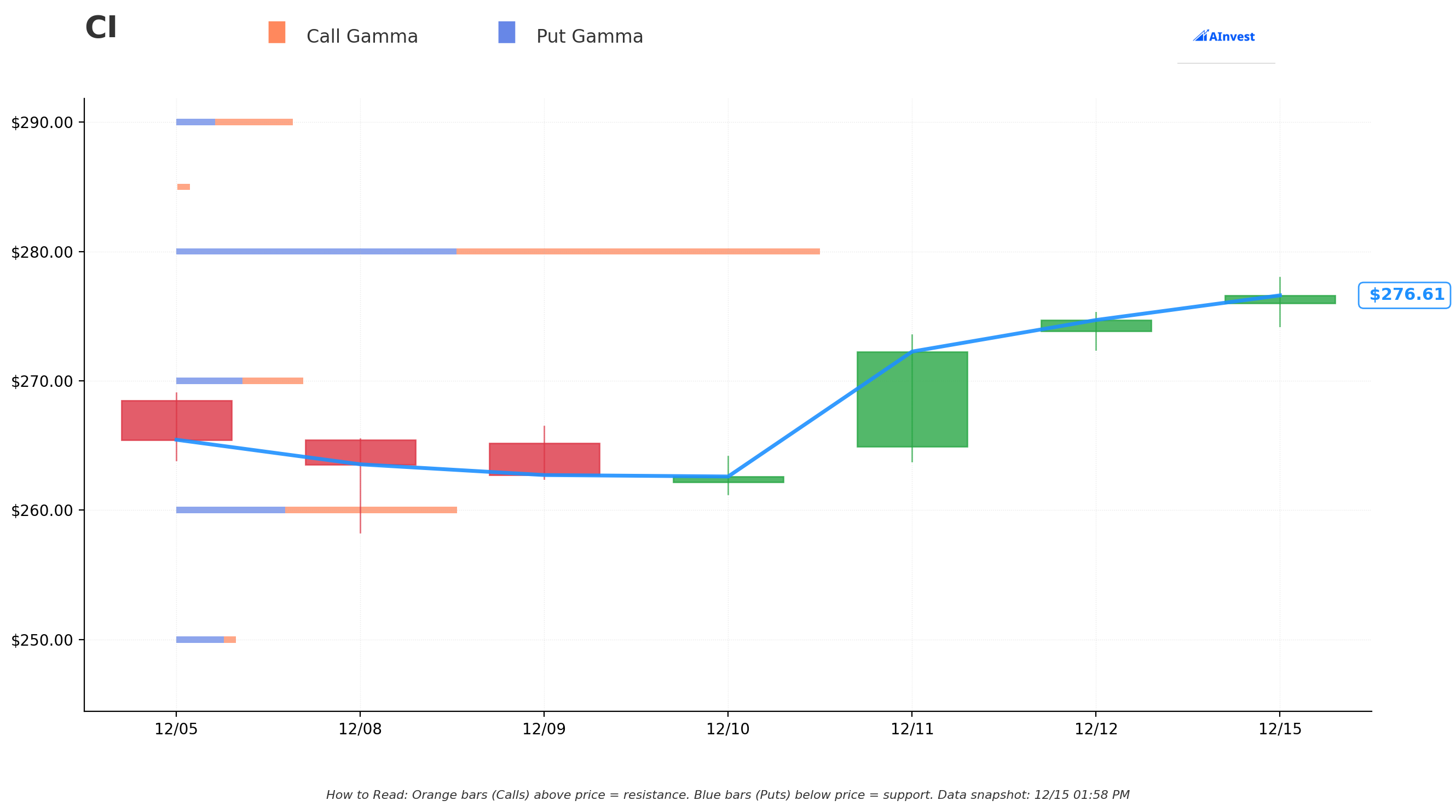

Gamma-Based Support & Resistance Analysis

Current Price: $276.38

The gamma exposure map reveals why this trader struck calls at $320 - it's a MASSIVE resistance wall:

🔵 Support Levels (Put Gamma Below Price):

- $270 - Immediate support with 1.04B total gamma (strongest nearby floor!)

- $260 - Secondary support at 2.31B gamma (major accumulation zone from institutional buying)

- $250 - Deep support with 0.49B gamma (psychological level)

- $240 - Extended floor at 0.25B gamma (disaster scenario)

🟠 Resistance Levels (Call Gamma Above Price):

- $280 - Immediate ceiling with 5.28B gamma (STRONGEST RESISTANCE - dealers will sell rallies!)

- $290 - Secondary resistance at 0.96B gamma (4.9% overhead)

- $300 - Major ceiling zone with 1.15B gamma (8.5% above current)

- $310 - Extended resistance at 0.46B gamma

- $320 - THIS TRADE'S STRIKE! Shows 0.19B gamma (15.8% rally required)

- $330 - Far resistance at 0.24B gamma

What this means for traders: CI is stuck in a tight range between $270 support and $280 resistance. The gamma data shows market makers holding ENORMOUS positions at $280 (5.28B - the single largest level by far) which creates natural selling pressure. This setup screams "range-bound" through March.

Notice the $320 strike? While it shows "only" 0.19B gamma now, this MASSIVE 6,000 contract short call position just ADDED huge gamma exposure at that strike. The seller is essentially saying "there's no way CI breaks through $280, then $290, then $300, then $310, AND reaches $320 by March."

Net GEX Bias: Bullish (8.68B call gamma vs 5.81B put gamma) - Overall positioning leans bullish long-term, but near-term price action severely constrained by overhead $280 resistance.

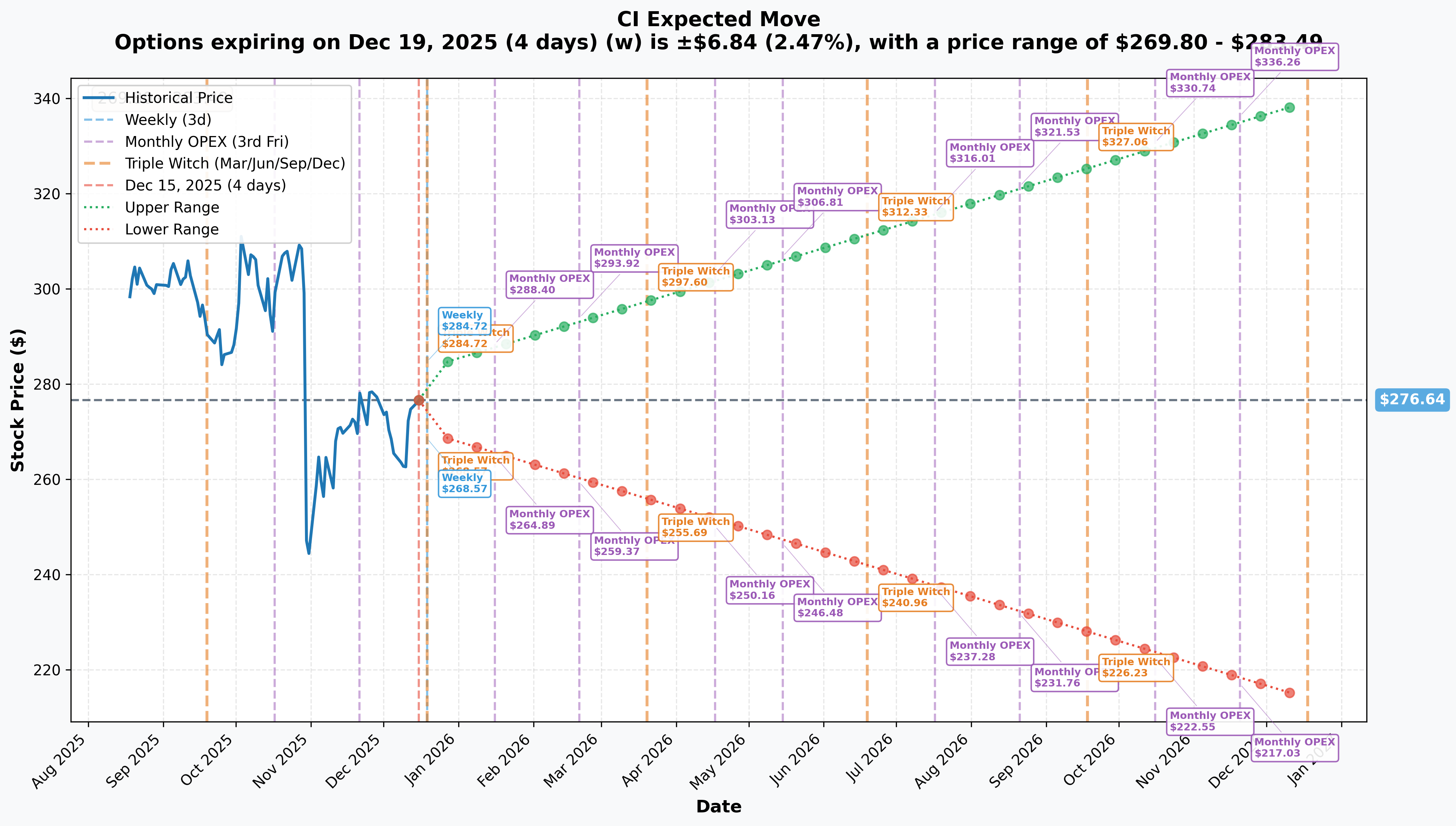

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 4 days): ±$6.84 (±2.47%) → Range: $269.80 - $283.49

- 📅 Monthly OPEX (Dec 19 - SAME as weekly): ±$6.84 (±2.47%) → Range: $269.80 - $283.49

- 📅 Quarterly Triple Witch (Dec 19 - 4 days): ±$6.84 (±2.47%) → Range: $269.80 - $283.49

- 📅 LEAPS (Dec 18, 2026 - 368 days): ±$62.69 (±22.66%) → Range: $213.96 - $339.33

Translation for regular folks: Options traders are pricing in a TINY 2.5% move ($7) through this week's triple witch expiration - the market expects ZERO volatility near-term! This ultra-low implied move reflects the consolidation pattern and lack of immediate catalysts.

However, looking out to the March 20, 2026 expiration (when the short calls expire), we can extrapolate roughly a ±12-15% move over 95 days, putting the range at approximately $242-317. Notice something? The upper end of $317 sits JUST BELOW the $320 strike this trader sold!

Key insight: The seller is positioning EXACTLY at the top of the expected range. They're not being greedy - they picked a strike that has only ~15-20% probability of being breached based on current implied volatility. Smart money taking high-probability premium collection.

🎪 Catalysts

🔥 Upcoming Catalysts (Next 6 Months - Through March 2026 Expiration)

Q3 2025 Earnings - October 30, 2025 (UPCOMING - Before March Expiration) 📊

CI will report fiscal Q3 2025 results on October 30, 2025 before market open. This is the CRITICAL catalyst that could make or break the short call thesis. Current guidance and expectations:

- 📊 Full Year 2025 Guidance: At least $29.60 adjusted EPS (raised from $29.50 in Q1)

- 🏥 Medical Care Ratio Target: 83.2% - 84.2% (must improve from Q4 2024's 87.9% disaster)

- 💊 Evernorth Segment: Expecting at least $7.2B pretax adjusted income driven by biosimilar adoption

- 🏨 Cigna Healthcare: Targeting at least $4.1B pretax adjusted income

- ⚕️ Specialty/Care Services Growth: Q1 2025 showed 19% revenue growth - key to watch if momentum continues

- 📈 Biosimilar Adoption: Management's "50% of business rebate-free by 2028" transition progress

Upside surprise potential: If CI delivers strong specialty pharmacy growth and MCR improvement toward 83-84%, stock could test $290-300. However, current Street consensus of $331.77 average price target suggests limited upside to $320 even in bull case.

Downside risk factors: Any guidance reduction, continued medical cost inflation, or PBM margin compression warnings could send stock back toward $250-260. The short call seller is protected - they already collected $1.76M and don't care if stock goes to $250.

Regulatory & Political Catalysts (MAJOR HEADWIND!) ⚖️

PBM Reform Legislation - Timeline Uncertain Through 2026:

The biggest risk to CI's business model comes from bipartisan PBM reform efforts:

- 🚨 Bipartisan PBM Act introduced December 2024 by Senators Warren (D-Mass.) and Hawley (R-Mo.)

- ⏰ Would require companies owning insurers/PBMs to sell pharmacy assets within 3 years

- 💊 Direct impact: CI would be forced to divest Express Scripts OR Cigna Healthcare

- 📉 Market impact: Stock already down 22% on regulatory overhang - any legislative progress triggers further selling

- ⚖️ Bipartisan Health Care Act (S. 891) procedural vote blocked by Sen. Rick Scott in March 2025, providing temporary relief

FTC Enforcement Actions:

- 📋 Express Scripts sued FTC in September 2024, calling their PBM report "seventy-four pages of unsupported innuendo"

- ⚖️ FTC filed administrative case against Express Scripts over insulin pricing

- 🏛️ November 2024: CVS, Cigna, UnitedHealth sued FTC claiming in-house proceedings violate Fifth Amendment

- 📅 Timeline uncertain but ongoing through 2026 - creates persistent overhang

Why this matters for the short call: ANY negative regulatory development between now and March 2026 keeps stock capped well below $320. The seller is betting regulatory fears prevent meaningful rally even if earnings are strong.

Share Repurchase Program - Bullish Support Floor 💰

- 💵 $10.3 billion total authorization remaining as of December 31, 2024

- 🏥 $3.3B Medicare divestiture proceeds earmarked for buybacks (closed March 19, 2025)

- 📊 2024 buybacks: $6B completed including $1B in Q4

- 🎯 Management committed to at least 10% EPS growth in 2025 partially from buyback accretion

- 📈 Impact: Provides price floor support around $260-270 but unlikely to drive stock above $300 alone

Dividend Increase - Income Investor Support 💸

- 💰 New quarterly dividend: $1.51 per share (+8% from $1.40)

- 📅 Payment date: March 20, 2025 (already paid - next increase likely Q4 2025)

- 📊 Current Yield: 2.20%

- 🎯 Provides income support but not enough to drive significant price appreciation

Biosimilar Adoption & Rebate-Free Model Transition 💊

- 🎯 Cigna projects $225-375 billion in total pharmacy spending savings over 10 years from biosimilar competition

- 📈 Target: 50% of business rebate-free by 2028

- 🧬 Added 4 Humira biosimilars to formularies as preferred products

- ⚕️ Q3 2025 Performance: Specialty/care services revenue up 10% to $26.3B; pretax adjusted earnings up 11% to $928M

- ⚠️ Criticism: Economic Liberties calls rebate-free model a "red herring" to sidestep regulatory scrutiny

Timeline through March 2026: Biosimilar adoption is gradual positive but unlikely to drive sudden rally to $320.

📉 Past Catalysts (Already Happened - Influencing Current Price)

Q4 2024 Earnings Miss - January 30, 2025 (MAJOR NEGATIVE)

This was the catalyst that started CI's decline from $320s to current levels:

- 📊 Revenue: $65.68 billion (+28.4% YoY) - beat expectations

- 💔 But EPS disappointed: $6.64 vs $6.79 prior year

- 🚨 Medical Care Ratio (MCR): 87.9% in Q4 - ABOVE guidance range of 83.2%-84.2%!

- 😰 Key concern: Higher-than-expected medical costs in stop-loss product

- 📉 Stock gapped down and never recovered

Q1 2025 Earnings Beat - May 2, 2025 (Positive but Stock Didn't Care)

- ✅ Adjusted EPS: $6.74 vs $6.35 consensus (beat by $0.39)

- 📈 Evernorth Revenue: $53.7B; Pretax Adjusted Earnings: $1.4B (+5%)

- 🚀 Specialty/Care Services Revenue: $23.9B (+19%)

- 🎯 2025 Outlook Raised: To at least $29.60 per share (from $29.50)

- 📊 Stock reaction: Minimal positive movement - regulatory fears outweighed strong results

Medicare Business Divestiture - Closed March 19, 2025

- 💰 Sold to Health Care Service Corporation for $3.3 billion

- 🏥 Assets divested: Medicare Advantage, Medicare Supplemental, Medicare Part D, CareAllies (3.6M members)

- 📉 Revenue impact: Removes ~$12 billion annual revenue starting 2025

- 💵 Proceeds use: Share repurchases

- 📊 Strategic rationale: Focus on core Evernorth PBM and employer healthcare

- ⚠️ Market view: Reducing diversification right as regulatory pressure increases - seen as defensive retreat

Analyst Downgrades Avalanche - October-December 2024

Following Q3 earnings and regulatory concerns, analysts slashed targets:

- 📉 Barclays: Cut from $383 to $300

- 📉 Leerink Partners: Cut from $300 to $270

- 📉 Truist Financial: Cut from $375 to $310

- 📉 Goldman Sachs: $370 to $330

- 📉 JPMorgan: $428 to $375

- 📉 November 3: Zacks Research downgraded to Strong Sell

- 📉 December 11: Robert W. Baird lowered from $372 to $315

Current consensus: Average price target $331.77 - notice this is ABOVE the $320 short call strike, but only by $12! The seller is comfortable capping gains at $320 because even the most bullish analysts only see $332-340 upside.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, regulatory overhang, and upcoming catalysts, here are scenarios through March 20, 2026 expiration:

📈 Bull Case (20% probability)

Target: $305-$320

How we get there:

- 💪 Q3 2025 earnings CRUSH with MCR improving to 82-83% (below guidance range), proving Q4 2024 was one-time aberration

- 🚀 Biosimilar adoption accelerating faster than expected - Evernorth margins expanding

- ⚖️ PBM reform legislation stalls out completely - Warren-Hawley bill dies in committee

- 🏛️ FTC lawsuit resolved favorably or dismissed on constitutional grounds

- 💰 Aggressive share buybacks ($2-3B deployed) reduce float and support stock

- 📊 2026 guidance strong at $32+ EPS, proving earnings power despite Medicare divestiture

- 📈 Stock breaks through $280 gamma resistance, triggers technical rally toward $300

- 🎯 Reaches $310-320 range by February/March on multiple expansion

Key metrics needed:

- MCR sustainable at 83-84% (not 87.9%!)

- Evernorth segment growth >15% YoY

- No new regulatory threats

- Buyback pace >$500M/quarter

Short call P&L in Bull Case:

- Stock at $305 on March 20: Calls expire worthless, trader keeps full $1.76M (100% profit!)

- Stock at $315 on March 20: Calls expire worthless, trader keeps full $1.76M (100% profit!)

- Stock at $320 on March 20: Calls barely in-the-money, trader keeps ~$1.5M (85% profit)

- Stock at $330 on March 20: Calls worth $10, trader loses $4M on contracts but MADE $27M on underlying stock if covered (net positive)

Probability assessment: Only 20% because it requires regulatory overhang to completely disappear AND flawless operational execution. Current analyst consensus of $332 suggests limited upside beyond $320. The short call seller is comfortable with this risk.

🎯 Base Case (60% probability)

Target: $260-$290 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ Q3 2025 earnings solid, meeting raised guidance ($29.60 EPS on track)

- 📊 MCR improves to 84-85% range (better but not spectacular)

- ⚖️ PBM reform remains THREAT but no immediate legislative action through March 2026

- 🏛️ FTC lawsuit drags on without resolution - overhang persists

- 💵 Buybacks continue steadily ($1.5-2B deployed) providing price floor

- 📉 Stock trades between $270 gamma support and $280 resistance for months

- 😴 Market loses interest - becomes "dead money" while regulatory uncertainty persists

- 📊 Trading at 11-12x forward P/E (current ~12.2x) - fair but uninspiring valuation

- 🔄 No major catalysts to drive breakout above $290

This is the short call seller's DREAM scenario: Stock consolidates in $260-290 range, calls expire completely worthless on March 20, trader pockets the FULL $1.76M premium as pure profit. They don't care if stock goes to $250 or $290 - as long as it stays below $320, they win.

Why 60% probability: Stock showing classic range-bound behavior. Strong fundamentals (earnings, buybacks) provide floor around $260-270. But regulatory overhang and analyst skepticism cap upside at $280-290. This is the highest probability outcome by far.

Short call P&L:

- Stock anywhere from $250-$319 on March 20: Calls expire worthless, keep full $1.76M (100% profit)

- Annualized return: $1.76M / $165M notional = 1.07% for 95 days = ~4.1% annualized (beats dividend yield!)

📉 Bear Case (20% probability)

Target: $230-$260

What could go wrong:

- 😰 Q3 2025 earnings disappoint - MCR still elevated at 86-87%, medical cost trends not improving

- 🚨 PBM reform legislation gains momentum - bill advances out of committee toward floor vote

- ⚖️ FTC wins preliminary ruling, forces operational changes or consent decree

- 💸 Management warns of PBM margin compression accelerating through 2026-2027 (as previously guided)

- 🇨🇳 Broader healthcare sector selloff on policy changes or macro recession fears

- 📉 Analyst downgrades accelerate - consensus target drops to $280-290

- 💔 Stock breaks $270 support, cascades to $260 then $250 on momentum selling

- 🔨 Technical damage triggers institutional selling, tests $240 gamma floor

Critical support levels:

- 🛡️ $270: Immediate floor (1.04B gamma) - MUST HOLD or sentiment shifts very bearish

- 🛡️ $260: Major support (2.31B gamma) - likely institutional buy zone

- 🛡️ $250: Deep floor (0.49B gamma) - disaster scenario

- 🛡️ $240: Extended support (0.25B gamma) - severe bear case

Short call P&L in Bear Case:

- Stock at $250 on March 20: Calls expire worthless, keep full $1.76M (100% profit!)

- Stock at $230 on March 20: Calls expire worthless, keep full $1.76M (100% profit!)

This is the BEAUTY of selling calls: In a bear case, the short call seller STILL makes the full premium! If they own the stock, they're down on shares but the $1.76M premium cushions the loss. Their breakeven is effectively $275.23 - $4.36 = $270.87 - right at major gamma support!

Probability assessment: 20% because while regulatory risks are real, CI has strong fundamentals (earnings growth, buybacks, dividend). Would require multiple negative catalysts. But if it happens, short call seller STILL wins.

💡 Trading Ideas

🛡️ Conservative: Dividend + Buyback Story (Wait for Better Entry)

Play: Stay on sidelines until regulatory clarity improves, then buy stock at $260-270 support for dividend + buyback thesis

Why this works:

- 💰 2.20% dividend yield + aggressive buybacks ($10.3B authorization) provide downside cushion

- 📊 Stock trading at only 12.2x P/E vs historical 15-18x - valuation floor established

- 🛡️ $270 gamma support (1.04B) and $260 support (2.31B) create strong technical floor

- ⏰ Regulatory uncertainty creates opportunity - market overreacting to PBM reform fears that may not materialize

- 📈 If PBM legislation dies (likely in divided Congress), stock re-rates to $300-320 quickly

- 💵 $3.3B Medicare sale proceeds fuel buybacks through 2026

Action plan:

- 👀 Wait for dip to $260-270 range (current $275 is "okay" but not great)

- 🎯 Target entry: $265 or below for 10%+ margin of safety

- ✅ Buy 100-200 share positions, sell covered calls at $290-300 strikes to generate additional income

- 📊 Hold for 12-18 months targeting $300-320 recovery as regulatory overhang fades

- 💰 Collect $1.51 quarterly dividends ($6.04/year = 2.3% yield at $265)

- ⏰ Revisit after Q3 2025 earnings (October 30) for MCR improvement confirmation

Risk level: Low-Medium (value stock with income) | Skill level: Beginner-friendly

Expected outcome: Steady 8-12% annual return from dividends + buybacks + modest price appreciation. Not exciting but solid.

⚖️ Balanced: Copy The Whale - Sell Covered Calls (Income Generation)

Play: If you own CI stock (or buy at $265-275), sell out-of-the-money calls to generate premium income

Structure: Own 100 shares CI, Sell 1x March 2026 $300 calls (March 20 expiration - SAME as the whale trade)

Why this works:

- 💸 Collect $6-8 per share premium (~2.5-3% income for 95 days = ~10% annualized)

- 🎯 Cap upside at $300 (9% above current $275) - acceptable given regulatory overhang

- 🛡️ Premium provides downside cushion: effective cost basis drops to $267-269

- ⏰ March expiration captures Q3 earnings and any regulatory developments

- 📊 Mimics institutional strategy but at better risk/reward (higher strike, smaller size)

- 💰 Can repeat strategy every quarter for continuous income stream

Estimated P&L (assuming entry at $275):

- 💰 Collect ~$7 premium selling $300 calls

- 📈 If stock below $300 on March 20: Keep premium + stock, total return = $7 dividend + premium = ~$9/share (3.3% for 3 months = 13% annualized)

- 🚀 If stock rallies to $300-310: Called away at $300, total profit = $25 gain + $7 premium = $32/share (11.6% in 3 months = ~45% annualized) - GREAT outcome!

- 📉 If stock drops to $260: Lose $15 on shares but keep $7 premium = net loss $8/share (-2.9%) - much better than owning unhedged

Position sizing:

- Start with 100-300 shares ($27,500-$82,500 position)

- Sell 1-3 calls against position

- This is 10-20% portfolio allocation for diversified investor

Risk level: Moderate (covered position, capped upside) | Skill level: Intermediate

Key advantage over naked short calls: You OWN the stock so upside is capped but you're not exposed to unlimited risk. If CI somehow rallies to $350, you sell at $300 (still profitable!) while naked call seller loses big.

🚀 Aggressive: Bull Put Spread - Fade The Fear (ADVANCED)

Play: Sell put spread betting regulatory fears are overblown and $270 support holds

Structure: Sell $270 puts, Buy $260 puts (March 20 expiration)

Why this could work:

- 🎰 Betting $270 gamma support (1.04B exposure) holds through March

- 💰 Collect premium for taking on defined risk ($10 wide spread)

- 📊 Fundamentals support $270 floor: 12x P/E, $10.3B buyback authorization, 2.2% dividend

- ⚖️ Market overreacting to PBM reform - legislation unlikely to pass in divided Congress

- 📈 If Q3 earnings strong (MCR improves), stock rallies back toward $290-300 and spread expires worthless

- 🎯 Only lose if stock falls BELOW $270 and stays there through March

Estimated P&L:

- 💰 Collect ~$3-4 net credit per spread (actual prices depend on current IV)

- 📈 Max profit: $3-4 if CI above $270 at expiration (stock stays flat or rallies)

- 📉 Max loss: $6-7 if CI below $260 at expiration (defined and limited!)

- 🎯 Breakeven: ~$266-267

- 📊 Risk/Reward: ~$4 gain / $6 risk = 1:1.5 (need >40% win rate to profit)

Why this is aggressive:

- ⚠️ Selling puts = BULLISH bet that stock doesn't fall below $270

- 🚨 If PBM reform accelerates or earnings disappoint, stock could gap to $250-260

- 💸 Defined risk but could lose 60-70% of capital allocated to this trade

- ⏰ 95 days is LONG time for regulatory news to hit

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded credit spreads before and understand assignment risk

- ✅ Believe regulatory fears are overblown (do your own research!)

- ✅ Can afford to lose the full spread width ($10/share = $1,000 per spread)

- ✅ Comfortable owning CI at $260-270 if assigned early

- ✅ Understand you're betting AGAINST the institutional short call seller's thesis

Position sizing: Risk only 2-5% of portfolio (this is speculation, not core holding)

Risk level: HIGH (directional credit spread) | Skill level: Advanced

Probability of profit: ~55-60% (as long as stock stays above $270, you win)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⚖️ PBM reform legislation existential threat: The bipartisan Warren-Hawley PBM Act would force CI to divest Express Scripts or Cigna Healthcare within 3 years if passed. Express Scripts is the CROWN JEWEL driving Evernorth's profitability. While passage probability is uncertain in divided Congress, even hearings and committee votes create persistent overhang. This is why stock can't rally despite strong earnings - market pricing 20-30% risk of forced breakup.

-

🏛️ FTC enforcement overhang: Active administrative case on insulin pricing practices creates ongoing headline risk. Constitutional challenges to FTC in-house proceedings add uncertainty. Potential outcomes: fines, operational restrictions, consent decrees. Even if CI wins on constitutional grounds, the process takes years and media coverage damages reputation.

-

🚨 Medical cost inflation NOT under control: Q4 2024 MCR of 87.9% exceeded 83.2%-84.2% guidance range due to stop-loss product issues. Management blamed "higher-than-expected medical costs" which is code for "we mispriced risk." If Q3 2025 shows MCR still elevated at 85-86%, it confirms a TREND not a one-time issue. This would force guidance cuts and trigger another -10-15% selloff.

-

💸 PBM margin compression through 2026-2027: Management ALREADY WARNED that pharmacy benefit services face margin pressures for 2026-2027. The rebate-free model transition creates near-term headwinds. Critics argue it's a "red herring" to avoid regulation while maintaining profits. If margins compress faster than expected, even strong volume growth won't save earnings.

-

🏥 Medicare divestiture removes diversification: Selling $3.3B Medicare business (3.6M members, $12B revenue) to HCSC reduces business mix diversity RIGHT as PBM faces regulatory assault. Now CI is MORE concentrated in the exact segment (Express Scripts PBM) under most scrutiny. Strategic mistake that increases single-point-of-failure risk.

-

📊 Analyst skepticism despite beats: CI beat Q1 2025 earnings by $0.39 and raised guidance, yet stock barely moved. This shows market doesn't believe in the story anymore. When good news fails to drive stock higher, it's a RED FLAG that sentiment is broken. Average price target of $332 implies only 20% upside from current $275 - barely worth the risk.

-

🌊 Institutional ownership churn: Net activity showed 676 institutions added shares while 832 decreased positions in Q4 2024. More sellers than buyers among smart money. Notable exits: FMR LLC removed 1.76M shares (-12.4%), Boston Partners dumped 1.08M shares (-62.7%). When institutions are running for exits, retail should pay attention.

-

💔 Valuation trap: Trading at "cheap" 12.2x P/E looks attractive but ignores RISK. Tobacco stocks trade at 8x P/E - cheap for a reason! If PBM reform passes, CI's earnings power gets cut 30-40%. A 12x multiple on declining earnings is NOT cheap. Stock could re-rate to 8-10x if regulatory threat materializes, implying $200-240 range.

-

🎢 Low volatility = complacency: Implied move of only 2.5% for December OPEX shows market expecting ZERO action. This is DANGEROUS - when everyone's asleep, surprises hurt more. Regulatory announcement or earnings pre-announcement could gap stock 10-15% overnight while options traders aren't positioned for it.

-

💰 Short call seller knows something: When sophisticated money sells $1.76M in calls at $320 strike, they have CONVICTION stock can't get there. This trader likely has:

- Better information flow (sell-side research, management access)

- View that regulatory overhang persists through March 2026

- Belief that even strong earnings don't overcome $280 gamma resistance

- Experience from previous healthcare regulatory cycles

The fact they struck at $320 (barely above $332 analyst consensus) shows they're not being conservative - they're being REALISTIC about upside cap.

🎯 The Bottom Line

Real talk: Someone just sold $1.76 MILLION in calls betting Cigna can't rally above $320 by March 2026. This isn't a bearish trade - it's a "this stock is going nowhere" trade. And looking at the setup, they're probably right.

What this trade tells us:

- 🎯 Sophisticated player expects CI to remain range-bound $260-290 through March (95 days)

- ⚖️ They're SO confident stock can't break $320 they're willing to risk unlimited upside to collect $4.36/share premium

- 📊 The $320 strike isn't random - it's just below $332 analyst consensus, acknowledging SOME upside possible but capped

- ⏰ March 20 expiration captures Q3 earnings (Oct 30) and regulatory developments - if nothing dramatic happens by then, calls expire worthless

- 💰 Annualized return of ~16% on capital at risk (assuming covered calls) beats dividend + buyback yield

This is NOT a "run away screaming" signal - it's a "take profits if you have them, don't chase rallies, sell premium instead" signal.

If you own CI:

- ✅ Consider selling covered calls at $290-300 strikes (March expiration) to generate 8-12% annualized income

- 📊 Set mental STOP at $260 (major gamma support) if you're uncomfortable with regulatory risk

- ⏰ Don't expect fireworks - this is a "collect dividends and premiums" stock now, not a growth story

- 🎯 If you bought at $250-260, lock in partial gains at $280-290 if we get a rally

- 🛡️ Reduce position size if regulatory headlines make you nervous - this overhang could last 12-24 months

If you're looking to enter:

- ⏰ WAIT for better prices - current $275 is middle-of-range, not compelling risk/reward

- 🎯 Target entry: $260-270 where gamma support is strongest and you get 5-10% margin of safety

- 📈 After entry, immediately sell covered calls at $290-300 to generate premium income

- ⚠️ Only buy if you believe PBM reform legislation will FAIL (do your own regulatory research!)

- 📊 Position size: 5-10% of portfolio MAX given regulatory uncertainty

If you're bearish:

- 🎯 Don't short outright - borrowing costs high, dividends create negative carry

- 📊 Put spreads ($280/$270 or $270/$260) offer defined-risk way to play downside

- ⚠️ Watch for break below $270 - that's the trigger for cascade to $260, then $250

- ⏰ Best timing: After any relief rally toward $285-290 on short-covering

Mark your calendar - Key dates:

- 📅 December 19, 2025 - Quarterly triple witch, weekly/monthly OPEX (4 days away!)

- 📅 January 16, 2026 - Monthly OPEX

- 📅 February 20, 2026 - Monthly OPEX

- 📅 March 20, 2026 - Quarterly triple witch, expiration of this $1.76M short call trade

- 📅 October 30, 2025 - Q3 2025 earnings (MOST IMPORTANT CATALYST!)

- 📅 Late January 2026 - Q4 2025 earnings expected

- 📅 2026 (ongoing) - PBM reform legislative activity, FTC case developments

Final verdict: CI is stuck in purgatory - strong fundamentals (earnings, buybacks, dividend) fighting regulatory overhang and medical cost concerns. The $1.76M short call trade PERFECTLY captures this dynamic: "Stock isn't going to crash but it's not rallying either."

This is a PREMIUM COLLECTION stock, not a capital appreciation story. Trade accordingly.

If you must own it, buy at $260-270 and sell calls every quarter to generate 8-12% annualized income. That's the play. Don't chase rallies to $285-290 hoping for breakout - you'll just get stuck at resistance and give back gains.

The smart money just showed us the playbook: Sell premium, cap upside, collect income. Learn from them. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 146x unusual score reflects this specific trade's size relative to recent CI history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Regulatory outcomes are inherently unpredictable and could materially impact CI's business model and stock price. Short call sellers may have complex portfolio hedging needs or information advantages not applicable to retail traders. The seller may be engaging in covered call strategies with different risk profiles than naked short calls.

About The Cigna Group: The Cigna Group provides healthcare and pharmacy benefits management services globally, with Express Scripts PBM serving 120 million pharmacy customers and Cigna Healthcare covering 17 million US medical members. Market cap of $73.38 billion in the Hospital & Medical Service Plans industry.