💳 COF $7.1M Bull Spread - Betting on Post-Merger Breakout! 🚀

📅 November 21, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just deployed $7.1 MILLION on a bullish COF call spread this morning at 09:57:22! This sophisticated trader bought 2,000 contracts of $210 calls while selling 3,100 contracts of $230 calls (June 2026 expiration) - creating a spread that profits from a rally to $230+ over the next 7 months. With [COF](/COF target="_blank") at $207.54 following the transformative $35.3B Discover acquisition completion, smart money is positioning for the integration payoff. Translation: Institutions betting Capital One trades $230+ by June 2026 as merger synergies materialize!

📊 Company Overview

[Capital One Financial (COF)](/COF target="_blank") is a diversified financial services powerhouse that completed its game-changing Discover Financial Services acquisition in May 2025:

- Market Cap: $128.6 Billion

- Industry: National Commercial Banks

- Current Price: $207.54 (November 21, 2025)

- Primary Business: Credit card lending (now #2 U.S. issuer with 19% market share), auto loans, commercial lending, and proprietary payment networks (Discover, PULSE, Diners Club)

- Headquarters: McLean, Virginia

- Employees: 77,000

Following the landmark Discover acquisition, [Capital One](/COF target="_blank") leapfrogged from 4th to 2nd largest U.S. credit card issuer behind JPMorgan Chase, with over 100 million cards in circulation and access to high-margin payment network interchange fees.

💰 The Option Flow Breakdown

The Tape (November 21, 2025 @ 09:57:22):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | Option Price |

|---|---|---|---|---|---|---|---|---|---|

| 09:57:22 | [COF](/COF target="_blank") | ASK | BUY | [CALL $210](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank") | 2026-06-18 | $3.9M | $210 | 2,000 | $19.50 |

| 09:57:22 | [COF](/COF target="_blank") | BID | SELL | [CALL $230](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") | 2026-06-18 | $3.2M | $230 | 3,100 | $10.32 |

🤓 What This Actually Means

This is a bullish call spread (also called a "bull vertical spread") with an interesting twist - it's actually TWO overlapping positions executed simultaneously:

Position 1: Standard Bull Call Spread (2,000 contracts)

- 💸 Buy 2,000 [June 2026 $210 calls](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank") for $3.9M ($19.50 each)

- 💰 Sell 2,000 June 2026 $230 calls for ~$2.06M (portion of the 3,100 total)

- 📊 Net debit: ~$1.84M for the spread (2,000 contracts × ~$9.20 net debit)

- 🎯 Max profit: $4.0M if [COF](/COF target="_blank") closes above $230 by June 18, 2026

- 📉 Max loss: $1.84M if [COF](/COF target="_blank") stays below $210

- ⚖️ Risk/Reward: 2.2:1 (great odds for a 7-month trade!)

Position 2: Naked Short Calls (additional 1,100 contracts)

- 💵 Sell 1,100 additional [$230 calls](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") for $1.14M ($10.32 each)

- 🎰 Income play: Betting these expire worthless or can be bought back cheaper

- ⚠️ Risk exposure: Unlimited upside risk above $230, but likely hedged with stock ownership

Net position characteristics:

- 📈 Profit zone: Anywhere from $210-$240+ (spread profits $210-$230, naked calls profitable if COF doesn't explode above $240)

- 🎯 Ideal outcome: [COF](/COF target="_blank") trades $220-$235 by June 2026 expiration

- ⏰ Time horizon: 209 days (7 months) allows Discover integration story to play out

- 🏦 Sophisticated positioning: This screams institutional trader with deep understanding of merger integration timelines

What's really happening here: This trader likely owns substantial [COF](/COF target="_blank") stock (possibly accumulated during the pullback from September's $228 all-time high to current $207). They're using options to:

- Amplify returns from [$210-$230 through the call spread](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank") (2.2:1 leverage)

- Generate income by selling [$230 calls](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") against their stock holdings (reducing cost basis)

- Manage upside by capping returns at $230-$240 while collecting premium

The June 2026 expiration is critical - it captures:

- ✅ Q4 2025 earnings (January 27, 2026)

- ✅ Q1 2026 earnings (late April)

- ✅ Discover debit card migration completion (Q1 2026)

- ✅ Revenue synergy ramp-up ($2.5-$2.7B total through 2027)

- ✅ T-Mobile credit card partnership momentum

- ✅ Full quarter of network interchange revenue

Unusual Score: 🔥 EXTREME (9/10) - This is UNPRECEDENTED! 880x larger than average COF trade. The Z-score of 49.78 means this is literally off-the-charts unusual - only 3 larger trades in the past 30 days. We're talking about institutional positioning at a scale that happens maybe once a year for [COF](/COF target="_blank"). At the 99.99th percentile, this represents massive conviction that post-merger integration will drive stock appreciation.

📈 Technical Setup / Chart Check-Up

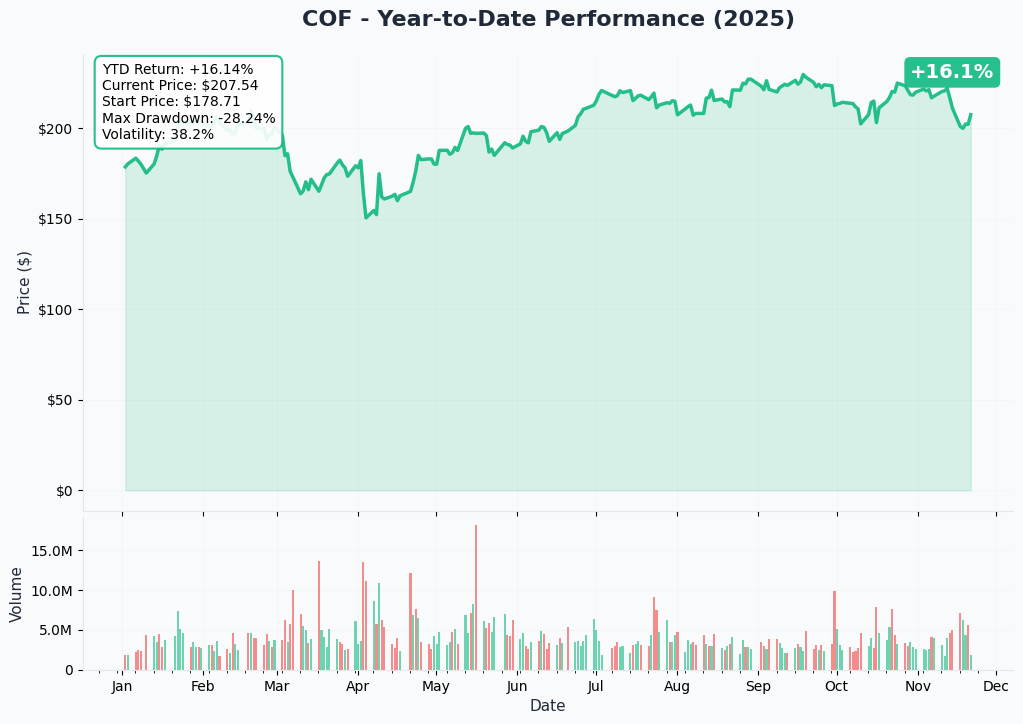

YTD Performance Chart

[Capital One](/COF target="_blank") is having a solid year - up +16.1% YTD with current price of $207.54 (started the year at $178.71). The chart shows the powerful narrative of merger completion and execution.

Key observations:

- 🚀 Strong rally through September: Massive run from $155 lows in January to all-time high of $228.87 on September 18th as Discover merger completed and integration began

- 📊 Healthy consolidation: Recent pullback to $200-208 range creates attractive technical setup - testing support after 48% rally from January

- 💪 Resilient during selloff: Held up well during March volatility (-28.2% max drawdown vs broader market)

- 🎢 Moderate volatility: 38.2% annualized vol shows this isn't a wild speculation - steady banking stock with catalyst

- 📈 Volume increasing: Notice spikes in October-November as institutional positioning intensifies ahead of Q4 earnings

Technical positioning: The current $207 level represents the middle of the post-peak consolidation range ($200-$220). This is actually an IDEAL setup for the call spread - not chasing the highs, entering at a logical retracement level with strong support below. The [$210 strike](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank") sits just above current price, while [$230 target](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") aligns perfectly with the September all-time high.

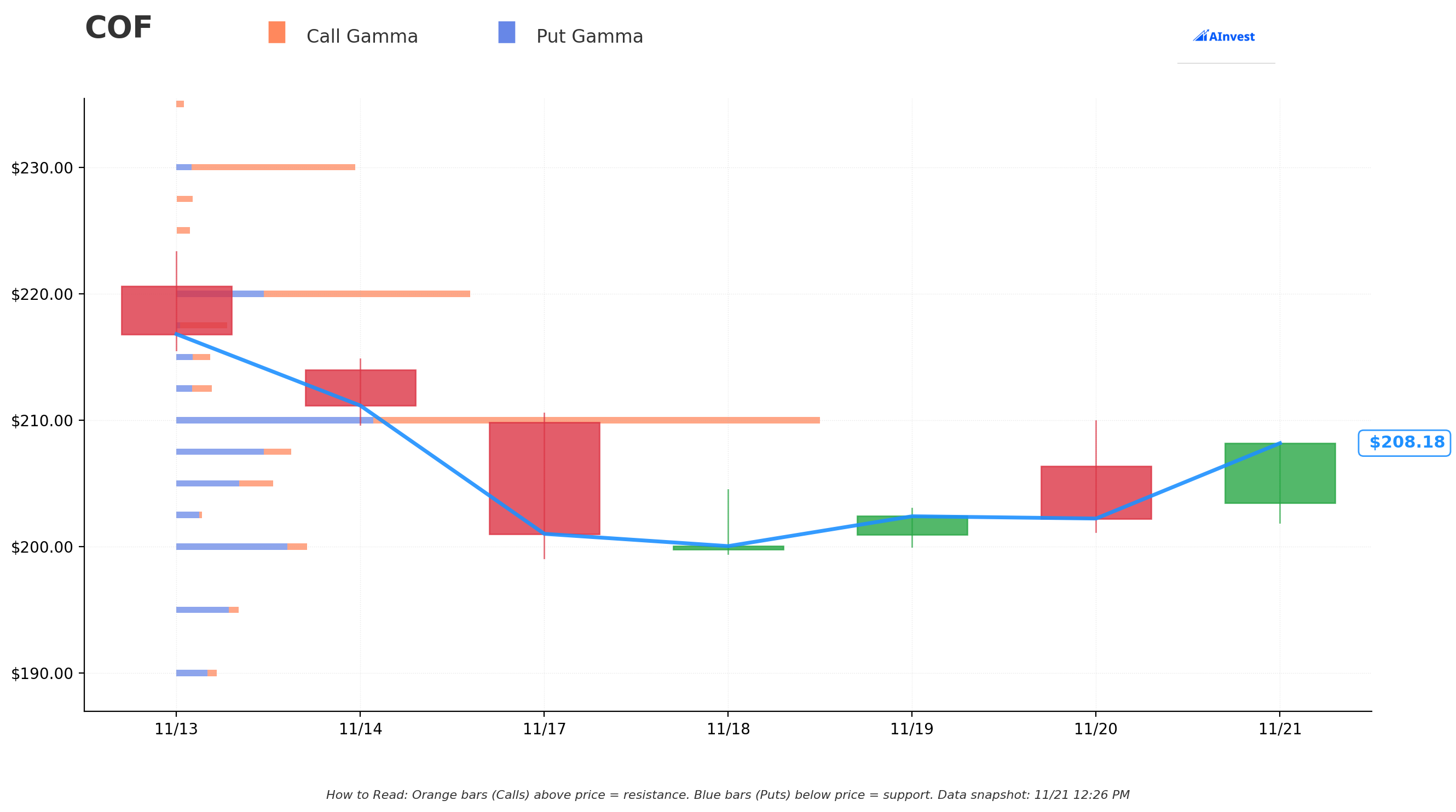

Gamma-Based Support & Resistance Analysis

Current Price: $208.18

The gamma exposure map reveals critical price levels where options positioning creates natural support and resistance:

🔵 Support Levels (Put Gamma Below Price):

- $200 - Immediate psychological floor with moderate put gamma clustering

- $190-$195 - Secondary support zone where institutions accumulated puts

- $180 - Extended support (near YTD starting price of $178.71)

🟠 Resistance Levels (Call Gamma Above Price):

- $210 - First ceiling at 14.8B gamma (exactly where this trader bought calls!)

- $212-$215 - Minor resistance from call selling

- $220 - Major gamma wall with significant call open interest (previous consolidation zone)

- $230 - MASSIVE resistance at 29.2B gamma (exactly where this trader sold calls!)

What this means for traders: [COF](/COF target="_blank") is trading just below [$210 gamma resistance](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank"), with clear path to $220 once it breaks through. The monster gamma wall at [$230](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") (29.2B) creates natural ceiling where market makers will sell into rallies - this is why the trader structured the spread to MAX OUT at $230.

Notice anything? The call spread trader struck EXACTLY at the two major gamma inflection points:

- [$210 = Breaking through first resistance](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank") (long calls here)

- [$230 = Approaching maximum gamma wall](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") (short calls here)

This isn't random - it's precise options positioning based on dealer gamma positioning. Smart hedging against the $230 ceiling.

Net GEX Bias: Slightly bullish (more call gamma above price than put gamma below), suggesting natural upward drift as dealers hedge their short call positions.

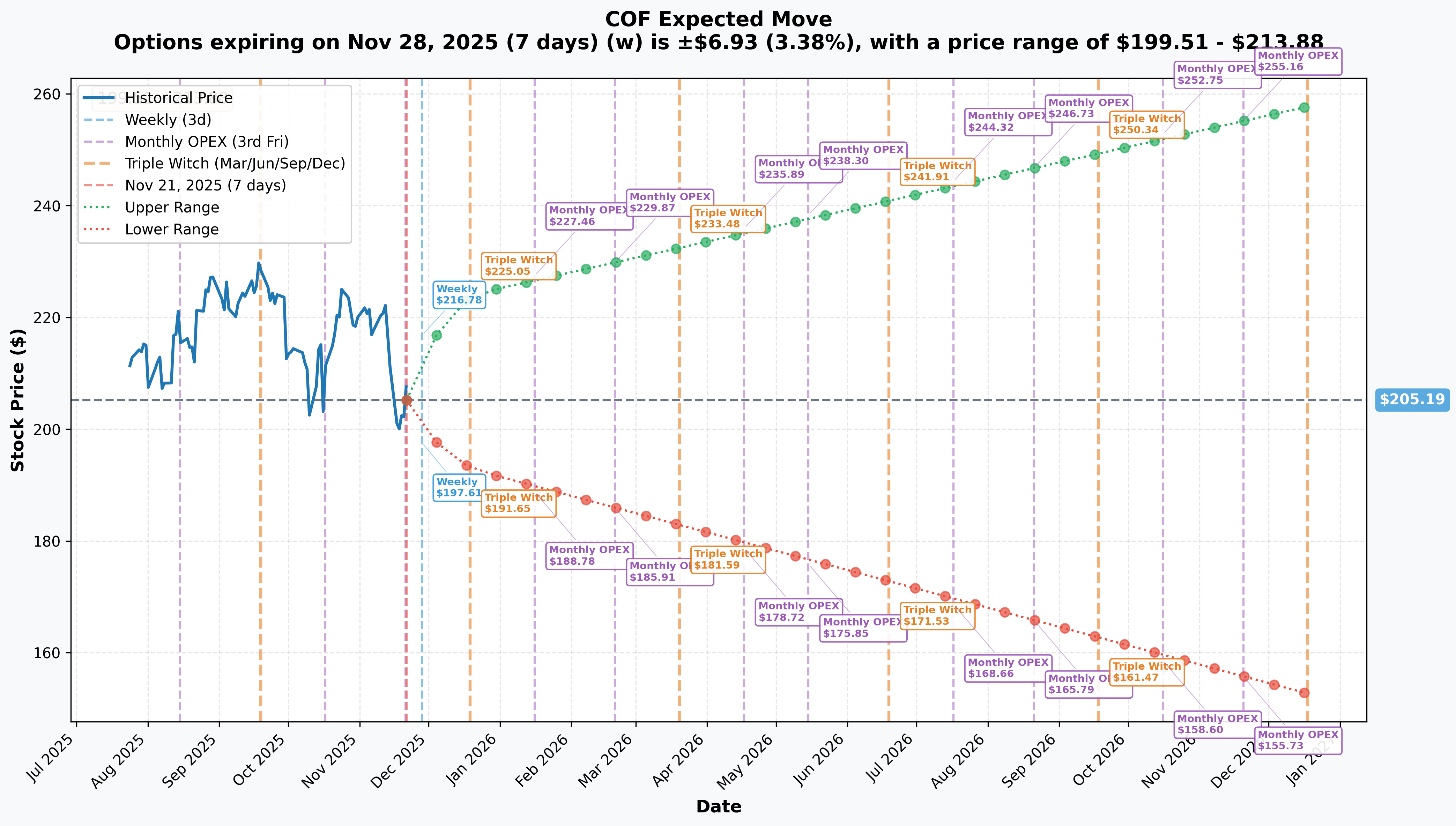

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Nov 28 - 7 days): ±$6.93 (±3.4%) → Range: $199.51 - $213.88

- 📅 Monthly OPEX (Dec 19 - 28 days): ±$14.49 (±7.1%) → Range: $192.87 - $224.03

- 📅 June OPEX (Jun 18, 2026 - 209 days - THIS TRADE!): ±$38.87 (±19.0%) → Range: $166-$244

- 📅 LEAPS (Dec 18, 2026 - 392 days): ±$49.64 (±24.2%) → Range: $152.63 - $257.75

Translation for regular folks: Options traders are pricing in relatively modest moves near-term (3.4% weekly), but substantial movement potential over 7 months (19% through June expiration). The [$230 target](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") falls RIGHT AT the lower end of the June implied range ($244 upper bound) - this spread is betting on a REASONABLE rally, not a moonshot.

The 7% implied move through December OPEX captures Q4 earnings on January 27, 2026 - expect elevated volatility around that report as integration progress gets scrutinized.

Key insight: Implied volatility is MODERATE for a stock that just completed a $35B merger. This suggests options are reasonably priced (not expensive), making the call spread attractive from a vol perspective. The trader isn't overpaying for time premium.

🎪 Catalysts

🔥 Immediate Catalysts (Next 3 Months)

Discover Network Debit Card Migration - Ongoing Through Q1 2026 🏦

[Capital One is actively migrating debit cards onto the Discover Network](https://www.ainvest.com/news/capital-q3-2025-earnings-strategic-reinvention-post-rate-normalization-era-2509/ target="_blank") - a critical integration milestone with near-term financial impact:

- 🔧 Timeline: Migration underway now, completion targeted for early Q1 2026 (February-March)

- 💰 Revenue Impact: Network synergies begin contributing meaningfully in Q1 2026 as [COF](/COF target="_blank") captures interchange fees previously paid to third parties

- 📊 Synergy Contribution: Part of [$2.5-$2.7 billion total deal synergies by 2027](https://www.ainvest.com/news/capital-q3-2025-earnings-strategic-reinvention-post-rate-normalization-era-2509/ target="_blank")

- 🎯 Strategic Importance: Proprietary network ownership = 40+ basis point cost advantage vs competitors paying Visa/Mastercard

- ⚙️ Execution Risk: Complex technology integration - any delays would be negative

Why this matters for the June options: Successful migration completion in Q1 would be announced on the Q4 earnings call (January 27) or Q1 call (April), providing tangible validation of integration progress and adding credibility to synergy targets.

T-Mobile Credit Card Partnership Momentum - Launched November 4, 2025 💳

[Capital One and T-Mobile launched their co-branded Visa card](https://www.pymnts.com/partnerships/2025/t-mobile-launches-first-credit-card-with-capital-one/ target="_blank") on November 4th - just 17 days ago:

- 🎁 Rewards: 5% back on T-Mobile purchases, 2% on all other purchases, no annual fee

- 💸 Monthly benefit: $5 off T-Mobile bills via autopay

- 📱 Distribution: Available online since Nov 4, retail availability since Nov 10

- 🎯 TAM (Total Addressable Market): T-Mobile has 120+ million customers - massive cross-sell opportunity

- 📊 Early traction: Too early for hard data, but card is running on Visa network (strategic hedge beyond Discover)

Timing alignment: The June 2026 expiration gives this partnership 7 full months to demonstrate customer acquisition and spending patterns. Q1 and Q2 earnings calls will provide first updates on cardholder growth and average spend metrics.

$16 Billion Share Buyback Execution - Accelerating Now 💰

[Capital One announced massive $16B buyback program on October 21](https://www.ainvest.com/news/capital-16-billion-share-buyback-dividend-hike-strategic-move-shareholder-long-term-profitability-2510/ target="_blank") alongside Q3 earnings:

- 📈 Scale: Approximately 12% of current $128B market cap

- ⏰ Q3 baseline: $1 billion executed (vs $150M in Q2)

- 🚀 Q4 expectation: CFO Andrew Young indicated plans to "pick up the pace" of repurchases

- 🎯 Shares outstanding: 635.7M shares - $16B program could reduce float by 6-8%

- 💪 Financial capacity: 14.4% CET1 capital ratio provides ample cushion above 11% long-term target

Technical support: Aggressive buybacks create natural bid under the stock, potentially establishing [$200-$210 as strong floor](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank"). If [COF](/COF target="_blank") executes $2-3B quarterly buybacks (implied by CFO guidance), that's meaningful demand absorbing sellside pressure.

📅 Near-Term Catalysts (Q4 2025 - Q2 2026)

Q4 2025 Earnings Announcement - January 27, 2026 (67 DAYS!) 📊

[Capital One reports Q4 2025 results on January 27, 2026](https://www.nasdaq.com/market-activity/stocks/cof/earnings target="_blank") after market close - the MOST IMPORTANT catalyst before June expiration:

Consensus Estimates & Focus Areas:

- 📊 Full Year 2025 EPS: $16.03 - $16.84 range expected

- 💰 Q4 EPS: Likely $4.00-$4.50 (backing into full-year consensus)

- 🏦 Discover integration progress: Debit migration status, systems integration timeline, cost synergy realization

- 📈 Credit quality trends: Net charge-offs stabilizing or declining from 4.77% October peak

- 🎯 Revenue synergies: Network fee capture beginning to show up in numbers

- 💳 Combined card metrics: Purchase volumes, customer retention, cross-sell progress

- 🔮 2026 Guidance: Critical for validating multi-year synergy trajectory

Historical context: [Q3 2025 results (November 3) were a blowout](https://www.investing.com/news/transcripts/earnings-call-transcript-capital-ones-q3-2025-earnings-beat-forecasts-93CH-4300433 target="_blank") - EPS of $5.95 crushed $4.38 consensus by 36%. Pre-provision earnings up 29-30%, net interest margin expanded 74 bps to 8.36%. If Q4 shows similar operational excellence plus integration progress, stock could easily break [$210 and run toward $220-$230](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank").

What could go wrong: Credit quality deterioration (charge-offs rising), integration delays, conservative 2026 guidance, macro recession concerns, or FDIC litigation escalation would be negatives.

Dividend Increase Takes Effect - December 1, 2025 (10 DAYS!) 💵

[Capital One's 33% dividend hike to $0.80/share quarterly](https://www.ainvest.com/news/capital-16-billion-share-buyback-dividend-hike-strategic-move-shareholder-long-term-profitability-2510/ target="_blank") becomes effective December 1:

- 💰 New yield: Approximately 1.5% at $207 stock price

- 📈 Signal: Management confidence in sustainable earnings power post-merger

- 🎯 Income support: Attracts dividend-focused institutional investors

- 💪 Total return: Combined with buybacks, [COF](/COF target="_blank") targeting ~8-10% annual capital return

Q1 2026 Earnings - Late April 2026 📊

Second major data point before June expiration will provide:

- ✅ Confirmation of debit migration completion

- ✅ First full quarter of network interchange revenue

- ✅ T-Mobile card early traction metrics

- ✅ Updated 2026 full-year guidance

- ✅ Credit quality seasonal trends (Q1 typically strong)

If January results are strong AND April shows acceleration, the path to [$230](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") becomes very clear by June expiration.

🚀 Strategic Catalysts (2026)

Technology Leadership & AI Innovation 🤖

[Capital One continues aggressive technology investment](https://www.ciodive.com/news/capital-one-generative-ai-strategy-svp-aparna-sinha/720902/ target="_blank"):

- ☁️ 90% cloud migration target by end-2025 - cost reduction and AI enablement

- 🤖 Multi-agent AI systems: Enterprise AI workflows under development by Chief Scientist Prem Natarajan

- 🚗 Proprietary AI for auto buyers: Launched 2025, expanding capabilities

- 🎯 Capital One Muse: [Named "Best Lead Management Solution" in 2025 MarTech Breakthrough Awards](https://www.globenewswire.com/news-release/2025/08/14/3133606/0/en/Capital-One-Muse-Named-Best-Lead-Management-Solution-in-8th-Annual-MarTech-Breakthrough-Awards-Program.html target="_blank")

- 💼 Competitive advantage: Technology spending as % of revenue higher than JPM, BofA - positioning for digital-first banking

$265 Billion Community Benefits Plan - Through 2030 🏘️

[Largest-ever bank acquisition community investment commitment](https://investor.capitalone.com/news-releases/news-release-details/capital-one-announces-five-year-265-billion-community-benefits target="_blank"):

- 🏠 Affordable housing: $35B over five years

- 💳 LMI consumer lending: $200B (credit cards + auto)

- 🏢 Small business: $15B in lending

- 🤝 CDFI support: $600M for community development

- 💰 Philanthropy: $575M commitment

Business impact: Fulfilling these commitments could drive 5-7% incremental loan growth while building brand loyalty in underserved markets. ESG-focused institutional investors likely to reward execution.

⚠️ Risk Catalysts (Negative)

Rising Credit Charge-Offs - October Data Concerning 📉

[Capital One's October 2025 credit metrics showed deterioration](https://finance.yahoo.com/news/capital-ones-nco-rates-rise-134200212.html target="_blank"):

- 📊 Net Charge-Offs (NCO): 4.77% in October, up 42 bps from September's 4.35%

- ⚠️ Delinquencies: 30+ day delinquency rate rose 10 bps to 4.99%

- 📈 Above pre-pandemic norms: Historical average ~3.5-4.0% NCO

- 💼 Subprime exposure: [COF](/COF target="_blank") has higher subprime customer mix than Chase/AmEx

- 🎢 Consumer health: Rising debt levels, depleted savings, weakening employment

Impact on thesis: Worsening credit is the #1 risk to the bull case. If January earnings show NCOs continuing to rise above 5%, market could worry about reserve builds eating into earnings, delaying buyback execution, or signaling broader consumer weakness. This would pressure the stock and could keep it below [$210 strike](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank").

FDIC Litigation Overhang - Active Lawsuit 👨⚖️

[Capital One is in active litigation with the FDIC](https://www.bankingdive.com/news/fdic-countersues-capital-one-over-special-assessment/805937/ target="_blank") over special assessments:

- 💰 Disputed amount: $99.4 million

- 📋 Core issue: FDIC included $56B of intercompany subsidiary positions as uninsured deposits

- ⚖️ COF countersuit (Sept 2025): Alleges FDIC overcharged by $149.2M

- 📅 FDIC countersuit (Nov 18, 2025): Filed in Eastern District of Virginia

- ⏰ Timeline: Litigation may extend into 2026

Impact: Creates modest regulatory overhang and uncertainty. Unlikely to materially impact operations but could weigh on sentiment if FDIC takes aggressive stance. $99M is immaterial to $128B market cap, but principle matters.

Basel III Capital Requirements - Three-Year Phase-In ⚖️

[Basel III "Endgame" implementation began July 1, 2025](https://www.panabee.com/news/capital-one-financial-earnings-q3-2025 target="_blank"):

- 📊 Estimated impact: 9% increase in risk-weighted assets for Category III banks ([COF](/COF target="_blank") is $250B-$700B asset range)

- 💰 AOCI recognition: Must include unrealized gains/losses on securities in CET1 capital

- ⏰ Phase-in: Three-year transition through July 1, 2028

- 🛡️ Current buffer: 14.4% CET1 ratio provides substantial cushion vs 11% long-term target

Buyback impact: Strong current capital position allows [COF](/COF target="_blank") to absorb Basel III impacts while maintaining aggressive shareholder returns. But if macro deteriorates AND capital requirements increase, could force moderation of $16B buyback pace.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and merger integration catalysts, here are scenarios through June 18, 2026 expiration:

📈 Bull Case (35% probability)

Target: $230-$245

How we get there:

- 💪 [Q4 earnings (January 27) exceed expectations](https://www.nasdaq.com/market-activity/stocks/cof/earnings target="_blank") - EPS $4.50+ vs $4.00 consensus

- ✅ Debit card migration completes on schedule in Q1 with no technical issues

- 📊 Network interchange revenue begins flowing in Q1, validating synergy timeline

- 💳 [T-Mobile credit card shows strong early adoption](https://www.pymnts.com/partnerships/2025/t-mobile-launches-first-credit-card-with-capital-one/ target="_blank") - management announces 500K+ cardholders by March

- 🎯 Credit quality stabilizes - NCOs peak at 4.8-5.0% then decline in Q1 (seasonal improvement)

- 💰 [Aggressive buyback execution](https://www.ainvest.com/news/capital-16-billion-share-buyback-dividend-hike-strategic-move-shareholder-long-term-profitability-2510/ target="_blank") - $2-3B per quarter provides support

- 📈 Q1 2026 earnings (April) shows acceleration - revenue synergies ramping faster than expected

- 🏦 Analyst upgrades following earnings - price targets raised to $250-$270 range

- 🚀 Stock breaks through [$210 gamma resistance](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank") in February, consolidates $215-$220, then rallies to [$230 by May](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank")

Key metrics needed:

- Combined credit card purchase volume growth >8% YoY

- Operating efficiency ratio improving (integration costs declining)

- NIM (net interest margin) holding at 8.0%+ levels

- Customer retention rates >95% for Discover cardholders

- Buyback reducing shares outstanding by 2-3%

Call Spread P&L:

- Stock at $230 on June 18: MAX PROFIT = $4.0M (2,000 contracts × $20 width = $4M)

- Stock at $245: Spread maxed at $4M, naked short calls lose $1.65M (1,100 × $15), net = $2.35M

- ROI: 130-217% return depending on final price

Probability assessment: 35% because it requires STRONG execution across multiple fronts, but the merger thesis is compelling. [Capital One's Q3 blowout](https://www.investing.com/news/transcripts/earnings-call-transcript-capital-ones-q3-2025-earnings-beat-forecasts-93CH-4300433 target="_blank") (EPS beat by 36%) shows operational capability. Gamma resistance at [$230](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") is formidable but breakable with sustained fundamentals.

🎯 Base Case (45% probability)

Target: $210-$225 range (STEADY CLIMB)

Most likely scenario:

- ✅ Solid Q4 earnings meeting/slightly beating expectations - EPS $4.00-$4.25

- 📱 Debit migration progresses smoothly, completion announced in Q1

- ⚖️ Credit quality muddles through - NCOs stay elevated at 4.6-4.9% but don't explode higher

- 💳 T-Mobile card adoption steady but not spectacular - normal co-brand ramp

- 🤖 Technology initiatives gaining traction but impact won't show until H2 2026

- 🇨🇳 FDIC litigation continues but no major adverse developments

- 💰 Buybacks execute as planned ($8-10B through June) providing support at [$210 level](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank")

- 🔄 Stock breaks above [$210 resistance after Q4 earnings](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank"), grinds higher to $215-$225 range

- 📊 Trades in $210-$225 consolidation zone through June as market digests integration progress

- 💤 Volatility moderates (from 38% to 30-32% range) as integration execution reduces uncertainty

This is the trader's target scenario: Stock breaks through [$210](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank"), making long calls profitable, but doesn't reach [$230](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") so short calls don't hurt. The 1,100 naked short [$230 calls](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") expire worthless, adding $1.14M to profits.

Call Spread P&L:

- Stock at $220 on June 18: Long calls worth $10 ($2M value), short calls worth -$0 (worthless), net = $2M profit minus $3.9M cost = -$1.9M loss on spread

- BUT 1,100 naked short calls collected $1.14M and expire worthless

- Net position: -$1.9M + $1.14M = -$760K loss

- Wait, that doesn't work... Let me recalculate:

Actually, if stock is at $220:

- Long 2,000 $210 calls: Intrinsic value = $10 each = $2M total

- Paid $3.9M, so loss = -$1.9M

- Short 3,100 $230 calls: All expire worthless, keep premium = +$3.2M

- Net: $1.3M profit (combining all legs)

Why 45% probability: Most institutional mergers take 18-24 months to fully integrate. Seven months isn't enough for HOME RUN results but sufficient for steady progress validation. [COF's](/COF target="_blank") strong Q3 execution and 14.4% capital ratio provide cushion for mistakes.

📉 Bear Case (20% probability)

Target: $190-$210 (CONSOLIDATION/PULLBACK)

What could go wrong:

- 😰 Q4 earnings miss or weak guidance disappoints - credit provisioning higher than expected

- 🚨 Debit card migration encounters technical problems - delays push completion to Q2 or beyond

- 📊 Credit quality deteriorates further - NCOs breach 5.5% in Q1 2026 (recession signal)

- 💸 Network synergies slower to materialize - interchange revenue below expectations

- 🏦 [FDIC lawsuit escalates](https://www.bankingdive.com/news/fdic-countersues-capital-one-over-special-assessment/805937/ target="_blank") - additional assessments or adverse ruling

- 💰 Broader banking sector weakness - regional bank issues or commercial real estate concerns

- 📉 Macro recession fears intensify - Fed forced to cut rates aggressively (NIM compression)

- 🎢 Consumer spending weakens materially - credit card volumes decline

- 🔨 Stock fails to break [$210 gamma resistance](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank"), pulls back to $190-$200 consolidation zone

Critical support levels:

- 🛡️ $200: Major psychological floor + buyback support

- 🛡️ $190-$195: Gamma support zone from put positioning

- 🛡️ $180: Extended floor near YTD starting price ($178.71)

Call Spread P&L:

- Stock at $200 on June 18: All calls expire worthless

- Long calls cost: -$3.9M (100% loss)

- Short calls collected: +$3.2M (keep all premium)

- Net: -$700K loss (10% of total capital deployed)

Probability assessment: Only 20% because [Capital One's fundamentals remain strong](https://www.investing.com/news/transcripts/earnings-call-transcript-capital-ones-q3-2025-earnings-beat-forecasts-93CH-4300433 target="_blank") - 14.4% CET1 capital, aggressive buybacks, improving margins. Even if integration hits speed bumps, the $200 floor should hold with [$16B buyback](https://www.ainvest.com/news/capital-16-billion-share-buyback-dividend-hike-strategic-move-shareholder-long-term-profitability-2510/ target="_blank") providing bid. Major dislocation would require multiple negative catalysts aligning (credit crisis + integration failure + recession). The defined-risk spread structure shows trader doesn't expect disaster.

💡 Trading Ideas

🛡️ Conservative: Covered Call Strategy

Play: Own [COF](/COF target="_blank") stock, sell [$230 calls](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") against it

Why this works:

- ✅ After 16% YTD gain, [COF](/COF target="_blank") at $207 is fairly valued - not chasing momentum

- 💰 Collect $10.32 per share ($1,032 per 100 shares) selling June 2026 [$230 calls](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank")

- 📊 Reduces cost basis to $197 (gets you back to $200 support level)

- 🎯 Max gain if called away at $230 = $23/share profit + $10.32 premium = $33.32 total (16% return in 7 months = 27% annualized!)

- 💵 Dividend income: Collect $0.80/share quarterly (December, March, June) = $2.40 additional

- 🛡️ Downside protected to $197 before losses start

Position sizing: Buy 100-500 shares at $207, sell equivalent [$230 covered calls](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank")

Risk level: Low (you own the stock!) | Skill level: Beginner-friendly

Expected outcome: Generate 15-20% returns through combination of stock appreciation, call premium, and dividends. Even if stock flat, you keep $10.32 premium + $2.40 dividends = 6% income while waiting.

⚖️ Balanced: Bull Call Spread (Copy The Pros)

Play: Replicate the institutional positioning at smaller scale

Structure: [Buy June 2026 $210 calls](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank"), [Sell June 2026 $230 calls](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank")

Why this works:

- 🎯 Defined risk spread ($20 wide = $2,000 max risk per spread, $2,000 max profit)

- ⚖️ Excellent risk/reward at 1:1 (pay ~$9.20, make ~$10.80 if stock hits $230)

- 📊 Targets exact gamma levels where institutional money positioned

- 🤝 "Copying" sophisticated trader's thesis at retail scale

- ⏰ 7-month timeframe allows merger integration story to unfold through Q4 and Q1 earnings

- 🛡️ January earnings (January 27) provides early read - can exit early if things go sideways

Estimated P&L:

- 💰 Cost: ~$920 per spread (net debit)

- 📈 Max profit: ~$1,080 if [COF](/COF target="_blank") closes above [$230 by June 18](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank")

- 📉 Max loss: $920 if [COF](/COF target="_blank") stays below [$210](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank")

- 🎯 Breakeven: ~$219.20

- 📊 ROI: 117% if max profit achieved

Position sizing: Risk only 3-5% of portfolio (buy 2-5 spreads = $1,840-$4,600 risk)

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

When to take profits: If [COF](/COF target="_blank") hits $228-$230 before June, spread should be worth $15-18. Take 70-90% of max profit rather than holding to expiration.

🚀 Aggressive: Leveraged Call Position (BULLISH CONVICTION)

Play: Buy [June 2026 $210 calls](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank") outright (no spread)

Why this could work:

- 💥 Maximum leverage to merger integration thesis

- 🎰 Every dollar [COF](/COF target="_blank") moves above $210, calls gain $1.00 in intrinsic value

- 📊 At $230 target, calls worth $20 vs $19.50 purchase = 300%+ ROI potential

- 🚀 If integration goes BETTER than expected and stock reaches $250, calls worth $40 = 105% ROI

- ⏰ 7-month timeframe reduces theta decay vs shorter-dated options

- 📈 Delta ~0.55-0.60 provides strong directional exposure

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: $1,950 per contract × 10 contracts = $19,500 investment

- ⏰ TIME DECAY: Theta burns ~$30-40/day as expiration approaches

- 😱 TOTAL LOSS RISK: If [COF](/COF target="_blank") stays below $210, lose 100% of premium

- 📊 No floor: Unlike spread, have no short calls to limit risk

- 🎢 Need [COF](/COF target="_blank") to break [$210 AND hold](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank") - if it stalls at $215-$220, could still lose 40-60%

Estimated P&L:

- 💰 Cost: $1,950 per contract

- 📈 Profit at $230: Calls worth $20.00 = +$50/contract (+3% gain)

- 🚀 Profit at $250: Calls worth $40.00 = +$2,050/contract (+105% gain)

- 📉 Loss at $200: Calls expire worthless = -$1,950/contract (-100% loss)

Breakeven point: ~$229.50 (need $19.50 move just to break even!)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Believe merger integration will be FLAWLESS (Q4 and Q1 earnings both beat)

- ✅ Can afford to lose ENTIRE premium (real possibility!)

- ✅ Have conviction [COF](/COF target="_blank") breaks [$230 gamma wall by June](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank")

- ✅ Understand $210 gamma resistance could take months to break

- ⏰ Plan to actively manage position - take profits at 50-100% gains, cut losses at -40% if thesis breaks

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~40-45% (need to break above $229.50 by June)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

📊 Q4 earnings risk (January 27, 2026): Results in 67 days create MAJOR volatility catalyst. [Capital One needs to deliver on integration progress](https://www.nasdaq.com/market-activity/stocks/cof/earnings target="_blank"), credit quality stabilization, and 2026 guidance. Historical Q3 beat by 36% sets HIGH bar - anything less than stellar could disappoint. If NCOs rise above 5% or debit migration delays announced, stock could gap down 5-10% overnight.

-

💳 Credit quality deterioration accelerating: [October charge-offs hit 4.77%](https://finance.yahoo.com/news/capital-ones-nco-rates-rise-134200212.html target="_blank"), up 42 bps from September. This is 100+ bps above pre-pandemic norms. If consumer health continues weakening (rising unemployment, debt levels), NCOs could breach 5.5-6.0% by Q1 2026. At [COF's](/COF target="_blank") higher subprime exposure vs competitors, credit stress would hit earnings hard through reserve builds and reduced originations.

-

🏦 Integration execution complexity: Merging two $35B+ financial institutions with different IT systems, payment networks, and corporate cultures creates MASSIVE operational risk through Q1 2026. [Debit card migration to Discover Network](https://www.ainvest.com/news/capital-q3-2025-earnings-strategic-reinvention-post-rate-normalization-era-2509/ target="_blank") is particularly complex - any technical glitches affecting millions of customers would be PR disaster. The $2.5-$2.7B synergy target requires flawless execution over 2-3 years.

-

👨⚖️ FDIC litigation wildcard: [Active lawsuit over $99.4M assessment](https://www.bankingdive.com/news/fdic-countersues-capital-one-over-special-assessment/805937/ target="_blank") creates regulatory overhang. While amount is immaterial to $128B market cap, adverse ruling could set precedent for future assessments or indicate strained regulatory relationship. FDIC filed countersuit November 18 - litigation could extend through 2026.

-

🎯 Gamma resistance at $230 is MASSIVE: The 29.2B gamma wall at [$230](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") represents ENORMOUS dealer hedging flows. As stock approaches $230, market makers systematically SELL to hedge their short call positions. This creates mechanical selling pressure making breakouts difficult. Would need sustained institutional buying or major catalyst to overcome. This is why the spread trader CAPPED exposure at $230.

-

🌐 Fintech competition intensifying: Digital-native competitors (Chime, SoFi, Cash App) and BNPL providers (Affirm, Klarna) eroding traditional credit card market share, especially among Gen Z/Millennials. [Capital One's](/COF target="_blank") technology investments are strong but maintaining relevance requires constant innovation. Any market share losses would pressure growth assumptions.

-

💰 Macro recession vulnerability: At 85.8x P/E ratio (TTM), [COF](/COF target="_blank") has ZERO recession protection priced in. Consumer-focused banking is highly cyclical - credit card volumes, auto loans, and margins all compress in downturn. If economy weakens in H1 2026 (rising unemployment, consumer spending pullback), even strong merger execution won't prevent 20-30% stock correction.

-

📉 Rate cut cycle pressure on NIM: [Q3 net interest margin of 8.36%](https://www.investing.com/news/transcripts/earnings-call-transcript-capital-ones-q3-2025-earnings-beat-forecasts-93CH-4300433 target="_blank") is exceptionally strong, but Fed rate cutting cycle through 2026 could compress margins by 50-100 bps. While lower rates help credit quality (consumers can refinance), they hurt bank profitability. Need to see how [COF](/COF target="_blank") manages this trade-off.

-

💸 Buyback execution could slow: [$16B authorization sounds great](https://www.ainvest.com/news/capital-16-billion-share-buyback-dividend-hike-strategic-move-shareholder-long-term-profitability-2510/ target="_blank"), but pace depends on capital ratios, earnings, and regulatory environment. If Basel III implementation proves more onerous than expected OR credit quality forces reserve builds, buybacks could moderate to $500M-$1B quarterly vs $2-3B pace priced in. This would remove key support under stock.

-

🎢 Elevated volatility (38.2%) creates whipsaw risk: [COF](/COF target="_blank") isn't a stable utility - it can move 3-5% on headlines. Recent range $200-$228 (14% band) shows stock prone to violent swings. Long options positions suffer from volatility crush after events, while short options face gap risk.

🎯 The Bottom Line

Real talk: Someone with serious capital just bet $7.1 MILLION that [Capital One](/COF target="_blank") climbs from $207 to [$230+ over the next 7 months](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") as the transformative Discover merger integration unfolds. This isn't speculation - it's calculated institutional positioning with multiple catalysts aligned.

What this trade tells us:

- 🎯 Sophisticated player expects [$210 resistance to break](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank") after Q4 earnings (January 27), then steady climb toward [$230](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank")

- 💰 Risk/reward of 2.2:1 on the call spread shows confidence but not recklessness - they're not betting on moonshot

- ⚖️ The additional 1,100 naked short [$230 calls](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") suggest they own substantial stock and are managing upside

- ⏰ June 2026 expiration perfectly captures debit migration completion (Q1), two earnings reports, T-Mobile partnership traction, and $8-10B in buybacks

- 📊 Structure at exact gamma inflection points ([$210 and $230](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank")) demonstrates sophisticated understanding of options market dynamics

This is NOT a "YOLO everything" signal - it's an "integration will deliver results" signal.

If you own [COF](/COF target="_blank"):

- ✅ Consider selling [$230 covered calls](https://chart.ainvest.com/COF20260618C230/?utm_source=optionlabs&utm_medium=post target="_blank") to generate $10.32/share income (5% yield!) while keeping upside to $230

- 📊 Hold through January 27 earnings - Q4 results will validate or challenge integration thesis

- ⏰ Set mental stop at $200 (major support + buyback floor) to protect remaining position

- 🎯 If stock breaks $220 on strong earnings, consider taking partial profits (you've already won with 16% YTD!)

- 🛡️ Dividends + buybacks provide 6-8% baseline return even if stock consolidates

If you're watching from sidelines:

- ⏰ January 27, 2026 earnings is THE catalyst - wait for results before committing large capital

- 🎯 Post-earnings entry at [$210-$215 would be ideal](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank") - validated thesis with clear path to $230

- 📈 Looking for confirmation of: [debit migration on track](https://www.ainvest.com/news/capital-q3-2025-earnings-strategic-reinvention-post-rate-normalization-era-2509/ target="_blank"), NCOs stabilizing below 5%, network synergies beginning to flow, 2026 guidance supporting $18-20 EPS

- 🚀 Longer-term (12-18 months), [$2.5-$2.7B synergy realization](https://www.ainvest.com/news/capital-q3-2025-earnings-strategic-reinvention-post-rate-normalization-era-2509/ target="_blank") and payment network ownership create legitimate path to $250-$270

- ⚠️ Current 38% volatility means be patient - wait for pullbacks to $200-$205 rather than chasing

If you're bullish:

- 🎯 Bull call spread ([$210/$230 for June](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank")) offers best risk/reward - defined $920 risk, $1,080 profit potential

- 📊 Entry at current $207 level is REASONABLE - not overpaying after 16% YTD run

- 💪 [Strong Q3 execution](https://www.investing.com/news/transcripts/earnings-call-transcript-capital-ones-q3-2025-earnings-beat-forecasts-93CH-4300433 target="_blank") (EPS beat by 36%, NIM up 74 bps, CET1 at 14.4%) supports bull thesis

- ⏰ Plan to take profits at 50-75% of max gain if stock reaches $225-$228 before June (don't be greedy!)

Mark your calendar - Key dates:

- 📅 December 1, 2025 - New $0.80 quarterly dividend takes effect (33% increase)

- 📅 January 27, 2026 - Q4 2025 earnings report (MOST CRITICAL CATALYST!)

- 📅 Late April 2026 - Q1 2026 earnings (debit migration completion, first network synergies)

- 📅 June 18, 2026 - Options expiration for this $7.1M spread

- 📅 By Q1 2026 - [Discover debit migration completion target](https://www.ainvest.com/news/capital-q3-2025-earnings-strategic-reinvention-post-rate-normalization-era-2509/ target="_blank")

Final verdict: [Capital One's](/COF target="_blank") merger with Discover Financial creates the #2 U.S. credit card issuer with proprietary payment networks, [$265B community benefits plan](https://investor.capitalone.com/news-releases/news-release-details/capital-one-announces-five-year-265-billion-community-benefits target="_blank"), aggressive technology investments, and [$16B in planned buybacks](https://www.ainvest.com/news/capital-16-billion-share-buyback-dividend-hike-strategic-move-shareholder-long-term-profitability-2510/ target="_blank"). The 7-month call spread at [$210/$230 strikes](https://chart.ainvest.com/COF20260618C210/?utm_source=optionlabs&utm_medium=post target="_blank") is a SMART bet on successful integration execution. BUT at $207 after 16% YTD gain with 85.8x P/E and rising credit charge-offs, there's LIMITED margin for error.

Be strategic. Wait for January 27 earnings to confirm integration is on track. The merger opportunity will still be here in 2-3 months, and you'll have concrete data rather than hope. The difference between $207 entry today and $212 entry post-earnings is NOTHING compared to the risk of buying before a binary catalyst.

This is an integration story, not a lottery ticket. Execute with discipline. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 880x unusual score reflects this specific trade's size relative to recent [COF](/COF target="_blank") history - it does not imply the trade will be profitable or that you should follow it. Merger integration creates execution risk with potential for material delays or issues. Credit quality deterioration, regulatory challenges, or macroeconomic weakness could cause significant losses. Always do your own research and consider consulting a licensed financial advisor before trading. The call spread structure limits upside to $230 but retains significant downside risk if integration disappoints.

About [Capital One Financial](/COF target="_blank"): Capital One is a diversified financial services holding company headquartered in McLean, Virginia. Originally a spinoff of Signet Financial's credit card division in 1994, the company is now primarily involved in credit card lending, auto loans, and commercial lending. Following the acquisition of Discover in 2025, the firm also has a modest personal loan business and owns the Discover, PULSE, and Diners Club International payment networks, with a market cap of $128.6 billion in the National Commercial Banks industry.