🔋 CORZ $1.1M Call Close - Smart Money Exits Bitcoin-to-AI Transition Play! 📊

📅 December 23, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just closed $1.1 MILLION worth of CORZ call options this afternoon at 12:52:22! A trader sold to close 5,000 contracts of March $17 strike calls - unwinding a bullish position on Core Scientific (CORZ) at $15.68, locking in gains or cutting losses before the 87-day expiration. With CORZ navigating a complex transformation from pure Bitcoin mining to AI/HPC infrastructure, this institutional exit signals profit-taking or reduced conviction in the near-term rally despite the company's $8.7 billion CoreWeave partnership.

📊 Company Overview

Core Scientific, Inc. (CORZ) is executing one of the most aggressive business pivots in the crypto mining sector - transforming from a struggling Bitcoin miner into an AI data center infrastructure provider:

- Market Cap: $4.9 Billion (emerged from bankruptcy Jan 2024)

- Industry: Digital Infrastructure for High-Performance Computing

- Current Price: $15.68 (off 34% from November 2024 all-time high of $23.63)

- Primary Business:

- Digital Asset Self-Mining: Bitcoin mining operations (currently 85% of revenue, declining)

- HPC Hosting: GPU infrastructure for AI/ML workloads (future growth driver)

- Hosted Mining: Third-party mining hosting services

The transformation story: CORZ is converting 900 MW of its 1.3 GW total power capacity to AI/HPC hosting, anchored by a $8.7 billion 12-year contract with CoreWeave to host NVIDIA GPUs for OpenAI and other hyperscale customers. This pivot has driven a 260% YTD gain despite recent pullbacks.

💰 The Option Flow Breakdown

The Tape (December 23, 2025 @ 12:52:22):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:52:22 | CORZ | BID | SELL | CALL $17 | 2026-03-20 | $1.1M | $17 | 5K | - | 5,000 | $15.68 | $2.20 |

🤓 What This Actually Means

This is a position closing trade - someone who previously bought these calls is now EXITING:

- 💸 Premium collected: $1.1M ($2.20 per contract × 5,000 contracts) sold

- 🎯 Strike significance: $17 is 8.4% above current price - moderately out-of-the-money

- ⏰ Time remaining: 87 days to March 20 expiration (quarterly triple witch)

- 📊 Position size: Represents 500,000 shares worth ~$7.8M

- 🏦 Institutional unwinding: This is a sophisticated trader taking profits or cutting losses

What's really happening here: This trader likely entered these $17 calls weeks or months ago when CORZ was climbing toward its November highs around $23. Now, with the stock consolidating at $15.68 (down 34% from peak) and the strike sitting 8.4% out-of-the-money, they're closing out rather than holding through March expiration. The timing suggests either:

- Profit-taking scenario: They bought these calls much cheaper when stock was at $12-13 and are booking gains before further decay

- Loss-cutting scenario: They bought near the top ($20-23) and are exiting before calls go to zero

- Opportunity cost: Reallocating capital to better opportunities as CORZ momentum has stalled

Unusual Score: 🔥 MODERATE (0.85 Z-score = "Typical" activity) - While $1.1M is a significant amount, this size is actually NORMAL for CORZ's recent trading patterns. We've seen larger institutional flows, so this isn't screaming "emergency exit" but rather orderly profit-taking or position management.

Key distinction: This is a SELL TO CLOSE (BTC) not a sell-to-open. The trader is shutting down a bullish bet, not initiating a new bearish position. It's a defensive move, not an aggressive short.

📈 Technical Setup / Chart Check-Up

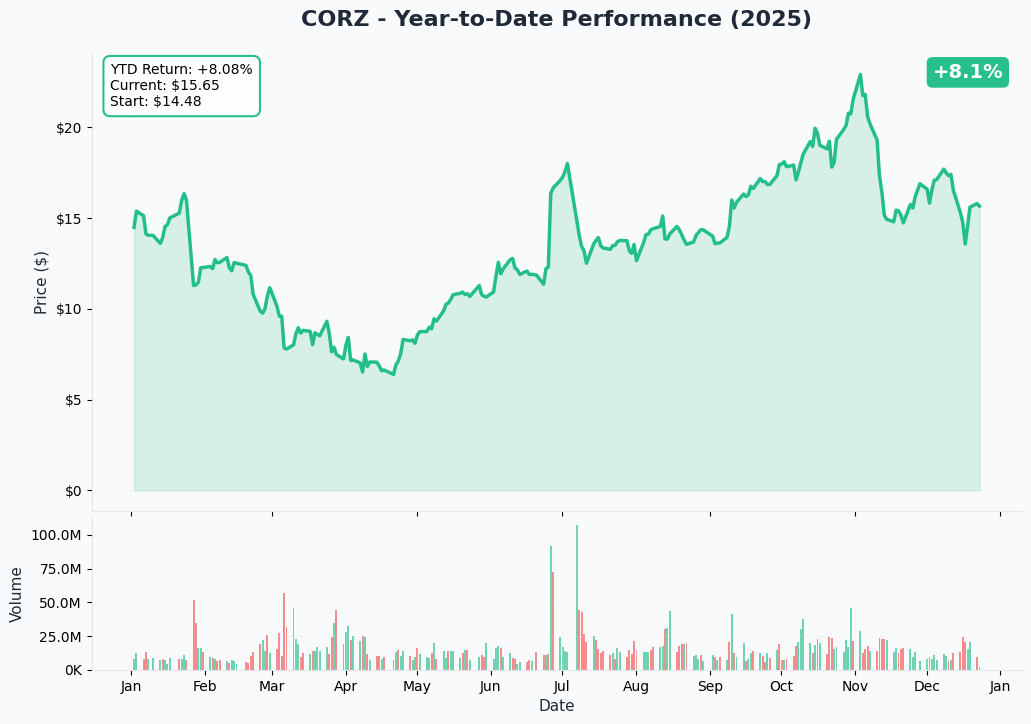

YTD Performance Chart

Core Scientific (CORZ) has delivered a wild ride in 2024 - up +260% YTD from around $4.40 in January to current $15.68, but that headline number hides serious volatility. The stock exploded from bankruptcy emergence in January through November, hitting an all-time high of $23.63 on November 3rd as the CoreWeave AI narrative reached peak euphoria.

Key observations:

- 🚀 Bankruptcy to billions: Emerged from Chapter 11 in January 2024 and immediately began rally

- 📈 Peak AI hype: August-November surge from $10 to $23 on OpenAI/CoreWeave partnership announcements

- 📉 Reality check pullback: Down 34% from November highs as execution challenges emerged

- 🎢 High beta Bitcoin exposure: Price action correlates with Bitcoin moves (currently 85% mining revenue)

- ⚠️ Failed merger hangover: October CoreWeave acquisition vote failure at $21+ still weighing on sentiment

- 💀 Max drawdown: Despite YTD gains, intraday swings have been brutal with 40-50% pullbacks common

The chart pattern shows a classic "buy the rumor, sell the news" setup - massive rally into the CoreWeave deal announcements, then consolidation and profit-taking as construction delays and revenue guidance cuts became public.

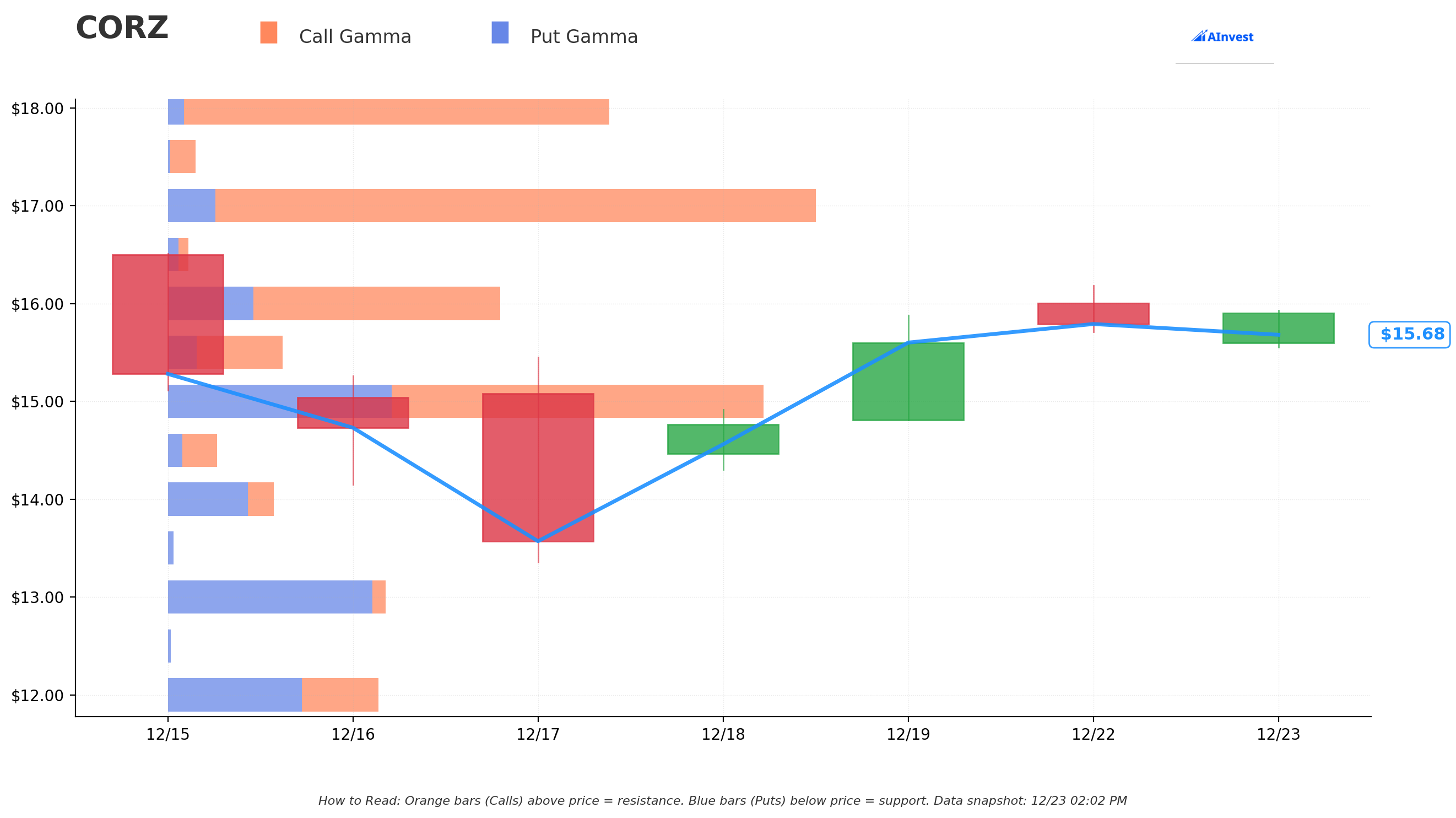

Gamma-Based Support & Resistance Analysis

Current Price: $15.68

The gamma exposure map reveals a stock caught in no-man's-land between major support below and resistance above:

🔵 Support Levels (Put Gamma Below Price):

- $13.50 - STRONGEST support with 0.516 put gamma vs 0.405 call gamma (net bearish -0.111) - This is the PUT WALL and HVL (High Volatility Level)

- $13.00 - Secondary support at 0.570 put gamma (net bearish -0.082)

- $12.00 - Deep support floor at 0.443 put gamma (net bearish -0.101)

- $11.50 - Minor support zone at 0.239 put gamma

- $11.00 - Extended floor at 0.296 put gamma

- $9.00 - Disaster scenario at 0.167 put gamma

- $8.00 - Absolute floor at 0.155 put gamma

🟠 Resistance Levels (Call Gamma Above Price):

- $16.00 - Immediate ceiling with MASSIVE 1.346 call gamma vs 1.284 put gamma (slight bullish net +0.062) - This is a major battleground

- $18.50 - Major resistance CALL WALL at 0.546 call gamma (net bullish +0.062) - Dealers will fight rallies here

- $21.00 - Extended upside target at 0.459 call gamma (net bearish -0.034 from put pressure)

What this means for traders: CORZ is trading in a tight no-man's-land at $15.68, sitting right BETWEEN the massive $16.00 gamma ceiling (1.346 call gamma - highest absolute level on the board) and the $13.50 put wall support. This creates a compression zone where the stock lacks strong directional bias.

Critical insight for this trade: The March $17 calls that were sold are struck ABOVE the $16 resistance zone. For these calls to finish in-the-money at expiration, CORZ needs to break through both the $16.00 ceiling AND push above $17 - requiring a 8.4% rally while fighting dealer hedging pressure at multiple levels. The trader who exited clearly doesn't see that path materializing in the next 87 days.

Net GEX Bias: Mixed/Neutral - The put wall at $13.50 is defensive (bearish net gamma) while resistance at $16 is also slightly bullish. This signals a consolidation range rather than directional momentum.

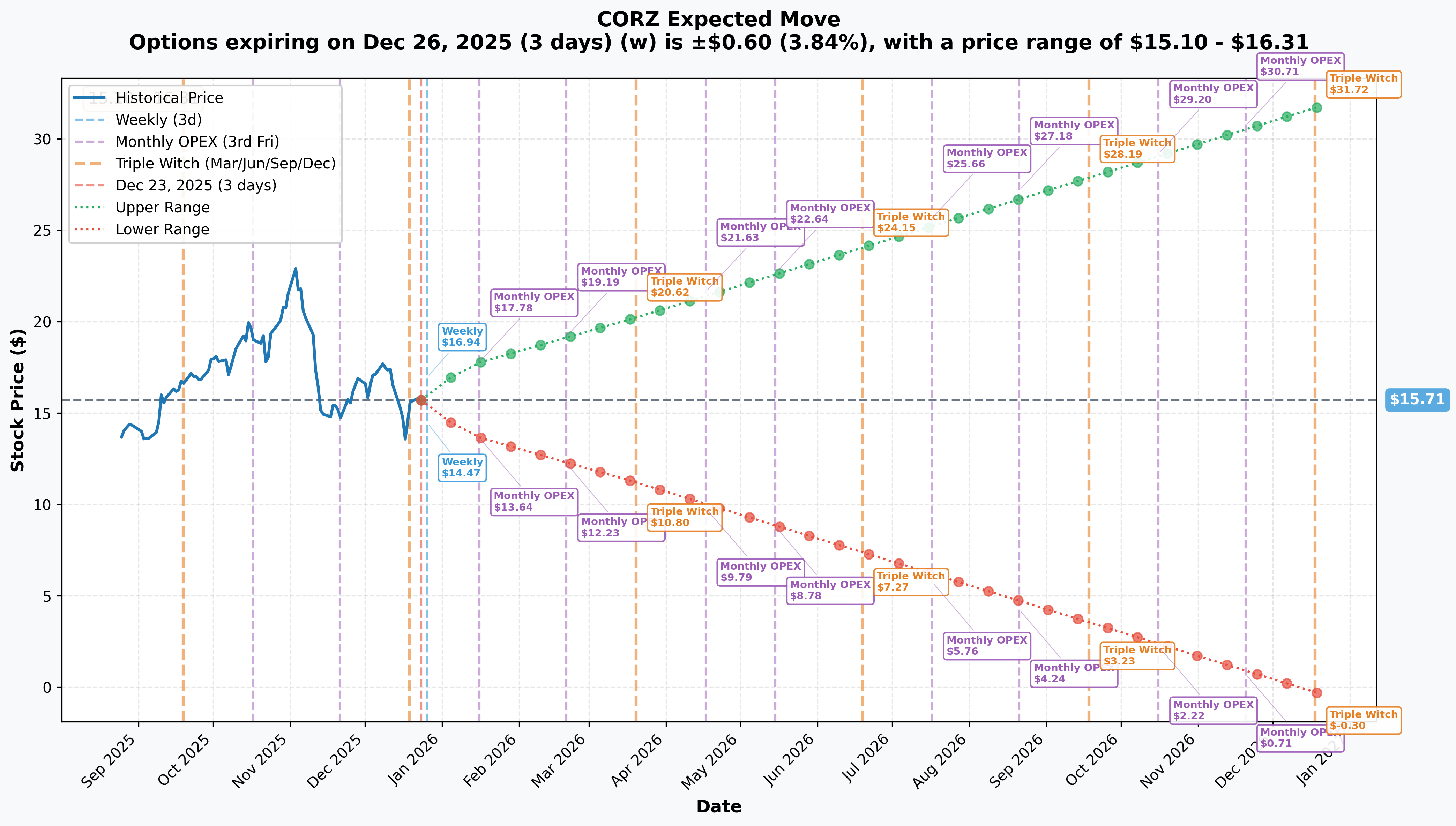

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 26 - 3 days): ±$0.60 (±3.84%) → Range: $15.10 - $16.31

- 📅 Monthly OPEX (Jan 16 - 24 days): ±$2.07 (±13.18%) → Range: $13.64 - $17.78

- 📅 Quarterly Triple Witch (Mar 20 - 87 days - THIS TRADE!): ±$4.53 (±28.84%) → Range: $11.18 - $20.24

- 📅 Yearly LEAPS (Dec 18 2026 - 360 days): ±$16.01 (±101.91%) → Range: -$0.30 - $31.72

Translation for regular folks: The options market is pricing in relatively modest movement near-term (3.8% weekly), but EXPLOSIVE volatility over longer timeframes. The quarterly move of ±28.8% reflects massive uncertainty around the AI transition execution. That's saying the stock could be anywhere from $11 to $20 by March - a HUGE range for a $5B company.

Key insight for this trade: The March 20th $17 calls expire exactly on quarterly triple witch. The implied move upper range is $20.24, meaning these $17 calls are within the probability cone but NOT at the high end. The market is pricing only a ~35-40% chance the stock trades above $17 by expiration. The seller clearly doesn't like those odds and wants to redeploy capital elsewhere.

Notice anything? The massive ±102% yearly implied move (range from effectively $0 to $32) shows the market sees CORZ as a binary bet - either the AI pivot works and stock explodes to $25-30+, or it fails and stock crashes back toward bankruptcy levels. This isn't a stable, predictable business - it's a high-risk transformation play.

🎪 Catalysts

🔥 Recent Catalysts (Last 3 Months - Already Happened)

Failed CoreWeave Merger Vote (October 30, 2024) ❌

Shareholders voted down CoreWeave's all-stock acquisition proposal citing valuation concerns, with stock declining 2% on termination announcement. While Core Scientific maintains operational independence and existing $8.7B CoreWeave contracts, the failed vote exposed relationship friction and may have strained trust between the partners. Stock was trading at $21+ when the vote failed and has since declined to $15.68 - a 25% drop suggesting market confidence was shaken.

Q3 2024 Earnings Miss (November 6, 2024) 📉

Core Scientific reported mixed Q3 results with massive $455M net loss (vs $41M prior year) driven by $408.5M non-cash warrant adjustment. Key metrics:

- Revenue: $95.4M vs $112.9M YoY (-15.5% decline)

- Digital asset mining revenue down 62% due to Bitcoin halving

- HPC hosting capacity increased to 800 MW but revenue still only $15M (+45% YoY but tiny base)

- Direct cash cost per Bitcoin: $42,351 (unsustainable at current prices)

- 85% of revenue still from volatile Bitcoin mining vs promised AI pivot

The earnings revealed the AI transition is proceeding MUCH slower than bulls hoped. Despite the massive CoreWeave contracts, actual HPC revenue is negligible.

Construction Delays at Denton Site (December 2024) 🚧

CoreWeave and Core Scientific's Denton, TX facility was delayed 60+ days due to heavy summer 2024 rains affecting concrete pouring and construction schedules. This 70 MW site (intended for OpenAI as end-customer) had completion dates pushed back "several months," raising concerns about ability to execute the broader 500 MW CoreWeave buildout on time. Stock declined from $17.50 to $15.50 on the delay news.

Revenue Guidance Cut (December 2024) 💔

2025 revenue estimate cut to $325.8M from prior $428.2M (-24% reduction) citing "challenges in energization timelines and operational efficiency." This was a MAJOR credibility hit as management had been promising accelerating AI revenue ramp. The market is now questioning whether the company can execute the AI pivot at all.

Debt Refinancing Success (August-December 2024) ✅

Issued $1.085 billion in convertible notes ($460M at 3% in August, $625M at 0% in December), reducing interest expense from 12.5% to effectively 3% and providing runway for AI infrastructure buildout. This improved the balance sheet but also created dilution risk (conversion price at $11.00 for August notes is well in-the-money at current $15.68).

🚀 Upcoming Catalysts (Next 6 Months)

Q4 2024 Earnings - February 26, 2025 (64 DAYS!) 📊

Core Scientific will report fiscal Q4 and full-year 2024 results on Wednesday, February 26, 2025 after market close, with conference call at 4:30 PM EST. This is THE critical catalyst that could make or break the near-term thesis.

What to watch:

- 🤖 AI/HPC revenue growth: Needs to show acceleration from Q3's $15M run rate toward $50M+ quarterly to justify valuation

- 💰 Bitcoin economics post-halving: With production down 62% and costs at $42,351/BTC, margin profile is challenged

- 🏭 CoreWeave energization progress: Management promised 250 MW online by year-end 2024 - did they deliver?

- 📊 2025 guidance revision: After cutting estimates once, will they cut again or stabilize expectations?

- 💸 Cash burn rate: With negative $581M net cash position, runway is limited without revenue growth

Upside scenario: CoreWeave sites coming online ahead of schedule, AI revenue doubling sequentially, conservative 2025 guidance beat expectations → Stock to $20-22

Downside scenario: Further delays disclosed, AI revenue flat, more guidance cuts, cash concerns → Stock to $12-13 support levels

CoreWeave Site Energization (Q1-Q2 2025) 🏭

The 200 MW initial CoreWeave sites expected operational in H1 2025 represent the PROOF POINT for the entire AI thesis. These sites began modifications in H2 2024 and should start generating $290M+ annual revenue once fully operational.

Milestones to watch:

- February/March 2025: First major site goes live (likely Austin or Denton once weather delays clear)

- Q2 2025: Revenue inflection begins showing in monthly reports

- Mid-2025: 70 MW additional capacity expected operational (bringing total to ~270 MW)

Risk: Any further construction delays, technical issues with GPU deployments, or customer pushback on performance would devastate the story. The Denton delay already showed execution challenges are real.

MI350 Series Launch Impact (Mid-2025) 🚀

While Core Scientific isn't directly involved, AMD's accelerated MI350 launch timeline affects CORZ since CoreWeave hosts NVIDIA GPUs. If AMD gains meaningful market share, it could pressure NVIDIA pricing or create alternative deployment opportunities. However, the CoreWeave contracts are NVIDIA-specific, so limited direct impact.

Bitcoin Halving Anniversary (April 2025) ⛏️

One year post-halving provides assessment window for Core Scientific's mining economics. With hash rate at 20.1 EH/s and costs at $42,351/BTC, the company needs Bitcoin above $50K to be profitable on mining. The strategic question: how fast can they pivot the remaining 400 MW from mining to AI before mining becomes totally unprofitable?

OpenAI Deployment Timing (H2 2026) 🤝

While far out, CoreWeave plans to lease Denton capacity to OpenAI once operational. Any updates on OpenAI's AI compute needs or alternative supplier announcements could impact CORZ sentiment. If OpenAI diversifies away from CoreWeave/Core Scientific infrastructure, the entire thesis crumbles.

⚠️ Risk Catalysts (Negative)

Further Construction Delays Beyond Denton 🚧

The 60-day Denton weather delay may be just the tip of the iceberg. Converting Bitcoin mining facilities to GPU data centers is complex - power delivery, cooling infrastructure, network connectivity all need major upgrades. Other sites could face similar or worse delays, pushing revenue realization into 2026 or beyond.

Bitcoin Price Collapse Below $40K 💔

With 85% of revenue still from mining and costs at $42,351/BTC, any Bitcoin drop below $40K makes mining operations loss-making. This would force accelerated facility conversions (capital intensive) while bleeding cash from core business. Bitcoin currently at ~$95K provides cushion, but crypto volatility means $40K is not impossible.

CoreWeave Relationship Deterioration 🤝

The failed merger attempt may have damaged trust. CoreWeave could slow buildout pace, renegotiate contract terms, or even pivot to alternative infrastructure providers (like building their own facilities or partnering with established data center REITs). Since CoreWeave represents substantially ALL HPC revenue, any relationship issues are existential risk.

Competitive Pressure from Established Players 🏢

Traditional data center operators (Equinix, Digital Realty, CyrusOne) are rapidly building AI-specific facilities with decades of experience, better locations, superior network connectivity, and existing customer relationships. Core Scientific's advantage is speed-to-market using existing infrastructure, but that advantage narrows every quarter. If CoreWeave or other hyperscalers decide purpose-built facilities are superior, CORZ loses its differentiation.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timeline through March 20th expiration, here are the scenarios:

📈 Bull Case (20% probability)

Target: $19-$22

How we get there:

- 💪 Q4 earnings BEAT expectations with AI revenue exceeding $25M (vs $15M in Q3)

- 🏭 CoreWeave sites energizing ON SCHEDULE with first major facility live by March

- 🤖 2025 guidance RAISED back toward $400M+ revenue citing accelerating AI ramp

- ⛏️ Bitcoin holds $80K+ providing cash flow buffer from mining operations

- 📊 Customer wins announced beyond CoreWeave (diversification reduces single-customer risk)

- 📈 Break above $16 gamma resistance triggers short covering rally to $18.50 call wall

- 🚀 Momentum builds into OpenAI deployment narrative for H2 2026

What needs to happen: The company needs to EXECUTE FLAWLESSLY across all fronts while also getting lucky on Bitcoin price support. CoreWeave buildout needs to accelerate despite recent delays, and management needs to restore credibility after guidance cuts.

Probability assessment: Only 20% because it requires multiple positive catalysts WITHOUT any negative surprises, and the company has proven execution challenges are real. The recent track record (failed merger, earnings miss, delays, guidance cuts) makes bulls skeptical.

Call P&L in Bull Case: The trader who closed their $17 calls would have regretted it:

- Stock at $22 on Mar 20: Calls worth $5.00, missed profit = $2.80/share × 5,000 = $14M opportunity cost

- Stock at $19 on Mar 20: Calls worth $2.00, missed profit = -$0.20/share × 5,000 = -$1M (still would have lost by holding)

🎯 Base Case (55% probability)

Target: $13.50-$17.50 range (CHOPPY SIDEWAYS ACTION)

Most likely scenario:

- ✅ Q4 earnings MEET lowered expectations ($325M 2025 guidance confirmed)

- 📱 CoreWeave sites progress but with continued delays - partial operations by Q2 2025

- ⚖️ AI revenue grows modestly to $20-30M quarterly but not spectacular

- 💰 Bitcoin stays range-bound $70-90K, mining remains marginally profitable

- 🔄 Stock trades within gamma support ($13.50) and resistance ($16.00-$18.50) bands

- 📊 Market remains skeptical but doesn't completely abandon thesis

- 💤 Trading range consolidation as investors wait for REAL revenue proof

This is why the trader exited: In this scenario, the $17 calls expire worthless or with minimal value as stock consolidates in $14-16 range. Rather than watch theta decay eat the remaining premium, they're booking whatever value is left and redeploying capital to better risk/reward opportunities.

Why 55% probability: This is the path of least resistance. Company isn't going bankrupt (strong balance sheet, CoreWeave contracts are real), but also isn't executing well enough to justify premium valuation. Consolidation and time is the likely outcome.

Call P&L in Base Case:

- Stock at $16.50 on Mar 20: Calls expire worthless (below $17 strike), loss = -$2.20/share × 5,000 = -$11M (smart to exit early and save whatever premium remains)

- Stock at $14.00 on Mar 20: Calls expire worthless, loss = -$2.20/share × 5,000 = -$11M (even worse if held)

📉 Bear Case (25% probability)

Target: $9-$12 (TEST THE PUT WALL!)

What could go wrong:

- 😰 Q4 earnings DISAPPOINT with more guidance cuts and cash burn concerns

- 🚨 CoreWeave delays extend into H2 2025 or beyond - no material revenue until 2026

- ⏰ Additional sites experience construction issues beyond Denton

- 💸 Bitcoin crashes below $50K, making mining operations deeply unprofitable

- 🤝 CoreWeave relationship fractures - slowdown or cancellation of expansion plans

- 💰 Cash position deteriorates requiring dilutive capital raise

- 📊 Competitive losses - hyperscalers choose traditional data center operators over CORZ

- 🔨 Break below $13.50 gamma support triggers cascade to $12, then $9

Critical support levels:

- 🛡️ $13.50: PUT WALL and HVL - MUST HOLD or sentiment turns fully bearish

- 🛡️ $12.00: Secondary support - breakdown below signals thesis failure

- 🛡️ $9.00: Disaster scenario returning to mid-2024 levels

Probability assessment: 25% because while execution risks are real and track record is poor, the CoreWeave contracts ARE signed and company has adequate financing. Complete thesis failure requires multiple severe negative catalysts. However, the recent pattern of disappointments makes this scenario more likely than bulls want to admit.

Call P&L in Bear Case:

- Stock at $10 on Mar 20: Calls expire worthless, loss = -$2.20/share × 5,000 = -$11M (but early exit at least stopped the bleeding)

- Stock at $8 on Mar 20: Calls expire worthless, loss = -$2.20/share × 5,000 = -$11M (disaster scenario)

💡 Trading Ideas

🛡️ Conservative: Avoid Until Execution Proof

Play: Stay on sidelines until February 26th Q4 earnings provides clarity on AI revenue trajectory

Why this works:

- ⏰ Too many unanswered questions about CoreWeave buildout timing and customer reception

- 💸 Recent track record (failed merger, delays, guidance cuts) shows management credibility issues

- 📊 Stock in no-man's-land at $15.68 - not clearly breaking out or breaking down

- 🎯 Better entry likely post-earnings if AI revenue accelerates OR at $12-13 support if it doesn't

- 🤔 The professional trader who just closed $1.1M in calls is signaling poor risk/reward here

- 📉 Gamma levels show $13.50-$16.00 consolidation range likely for months

Action plan:

- 👀 Monitor Q4 earnings closely for AI revenue ($25M+ would be bullish), CoreWeave progress, cash position

- 🎯 If earnings beat and stock breaks $16-$18 on volume, consider entry at $17-18 breakout

- 📊 If earnings disappoint, wait for pullback to $12-13 support for value entry

- ⏰ Don't chase here at $15.68 in dead zone between support and resistance

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 20-30% drawdown if execution stumbles. Get better entry at technical inflection points (breakout above $18 or breakdown to $12).

⚖️ Balanced: Post-Earnings Put Spread (Protect The Downside)

Play: After Q4 earnings volatility settles, sell put spread to capture premium while defining risk

Structure: Buy $14 puts, Sell $12 puts (March 20 expiration - SAME as the call trade)

Why this works:

- 🎢 IV crush after earnings makes spreads cheaper - enter AFTER volatility drops

- 📊 Defined risk spread ($2 wide = $200 max risk per spread)

- 🎯 Targets the $12-14 gamma support zone where put walls are strongest

- 🛡️ Betting on consolidation NOT collapse - collect premium if stock stays above $12

- ⏰ 30+ days post-earnings gives time for AI revenue trajectory to become clearer

- 📈 Works if stock stabilizes, rallies, or only modestly declines

Estimated P&L (adjust based on post-earnings IV):

- 💰 Collect ~$0.60-0.80 credit per spread (selling the $12 puts, buying $14 puts for protection)

- 📈 Max profit: $60-80 if CORZ stays above $14 at March expiration

- 📉 Max loss: $120-140 if CORZ below $12 (defined and limited)

- 🎯 Breakeven: ~$13.20-13.40

- 📊 Risk/Reward: ~1:2 (risking $140 to make $60) but high probability of success if put wall holds

Entry timing:

- ⏰ Wait 3-5 days after Feb 26 earnings for IV to fully collapse

- 🎯 Only enter if stock trading $14.50+ (gives cushion to breakeven)

- ❌ Skip if stock already below $13 (too close to max loss zone)

Position sizing: Risk only 2-3% of portfolio (this is a defined-risk income play)

Risk level: Moderate (defined risk, neutral-to-bullish bias) | Skill level: Intermediate

🚀 Aggressive: Strangle Betting on Breakout OR Breakdown (ADVANCED!)

Play: Buy strangle betting stock breaks out of $13.50-$18.50 consolidation range violently

Structure: Buy $12 puts + Buy $19 calls (March 20 expiration)

Why this could work:

- 💥 Implied move of ±28.8% ($11-$20 range) suggests violent movement possible

- 🎰 Binary catalyst (Q4 earnings Feb 26) could trigger explosive move either direction

- 📊 CoreWeave buildout is pass/fail - either works and stock to $22+, or fails and stock to $10

- ⚡ Strangle positioned OUTSIDE the gamma walls to capture breakout momentum

- 📈 Only need stock to break $20 OR $11 to profit - covers both scenarios

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Strangle costs ~$3.50-4.50 total ($350-450 per strangle)

- ⏰ TIME DECAY: Theta burns -$20-30/day approaching earnings

- 😱 IV CRUSH: Post-earnings collapse could crush both legs even if stock moves

- 📊 Stuck in the middle: Most likely outcome is stock stays $13-17 and both legs expire worthless

- 🎢 Need 30%+ move from current level to breakeven

- ⚠️ Consolidation scenario (55% probability!) results in 80-100% loss

Estimated P&L:

- 💰 Cost: ~$4.00 per strangle ($400 total investment)

- 📈 Profit scenario: Stock moves to $23+ or $9- = $3-5 gain per strangle (75-125% ROI)

- 🚀 Home run: Stock to $25 or $7 = $5-7 gain (125-175% ROI)

- 📉 Loss scenario: Stock ends $12-19 range = lose $2-4 (50-100% loss)

- 💀 Total loss: Stock at $14-16 at expiration = lose entire $4.00 (100% wipeout)

Breakeven points:

- 📈 Upside breakeven: ~$23 (47% rally from current)

- 📉 Downside breakeven: ~$8 (49% drop from current)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can afford to lose ENTIRE premium (very realistic possibility!)

- ✅ Understand you need a 30-50% move to profit - not a 10-15% move

- ✅ Have traded strangles before and understand IV dynamics

- ✅ Accept 55% probability scenario (consolidation) means total loss

- ⏰ Plan to adjust after earnings - potentially close one leg and let winner run

- 📊 Recognize this is pure speculation on binary catalyst outcome

Risk level: EXTREME (can lose 100%) | Skill level: Advanced only

Probability of profit: ~30% (lower than implied 50% due to consolidation bias)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q4 earnings binary event in 64 days: Results February 26th after market close could gap stock 20-30% either way based on AI revenue trajectory, CoreWeave progress, and guidance. Recent history shows management struggling with execution (guidance cuts, delays) so credibility is challenged. Market will demand PROOF not promises.

-

💸 Execution track record is TERRIBLE: In past 3 months alone we've seen: failed CoreWeave merger vote, Q3 earnings miss with $455M loss, 60+ day construction delay at Denton, and 24% revenue guidance cut. This is NOT a well-oiled machine - this is a company struggling to transform its business model while fighting headwinds on all fronts.

-

🇨🇳 85% revenue exposure to volatile Bitcoin mining: Despite the AI narrative, actual operations are still overwhelmingly Bitcoin mining with only $15M quarterly AI revenue in Q3. With costs at $42,351 per Bitcoin, any Bitcoin drop below $50K makes core business loss-making. The AI transition is real but SLOW - revenue won't flip to majority-AI until 2026 at earliest.

-

🤝 CoreWeave customer concentration is EXISTENTIAL risk: CoreWeave represents substantially all HPC revenue and future growth. The failed merger attempt in October may have damaged the relationship - what if CoreWeave slows buildout, renegotiates terms, or pivots to alternative infrastructure providers? There's ZERO diversification - it's CoreWeave or bust.

-

🚧 Construction delays proving harder than expected: The Denton 60-day weather delay shows converting Bitcoin mining facilities to GPU data centers is COMPLEX. Heavy rains delayed concrete pouring, but the real issue is this: power delivery, cooling, network infrastructure all need major upgrades. If one site faced 60-day delays from weather, how many other sites will face technical delays, permitting issues, equipment shortages? The 500 MW buildout timeline is at serious risk.

-

🏢 Valuation stretched at $4.9B with negative cash flow: Trading at 15x forward revenue (using optimistic 2025 estimates) while burning cash with -$581M net debt position and pretax margins of -189%. The stock is priced for PERFECT execution on the AI transition. Any stumble and there's 40-50% downside to $9-10 levels where value investors might step in.

-

💰 Dilution risk from convertible notes: Issued $1.085B in convertibles with August notes having $11.00 conversion price (42% in-the-money at current $15.68). While this strengthened balance sheet, it also creates significant share dilution if notes convert. Shares outstanding already grew 67.5% in past year - further dilution from converts could pressure stock.

-

📊 Gamma ceiling at $16 creates mechanical resistance: The MASSIVE 1.346 call gamma at $16.00 (highest level on the entire board) means dealers will systematically SELL rallies to hedge exposure. This creates mechanical selling pressure making breakouts difficult. Would need sustained institutional buying to overcome - and the $1.1M call close suggests institutions are REDUCING not adding exposure.

-

🎢 High beta volatility creates whipsaw risk: Down 34% from November highs despite being up 260% YTD shows this stock moves FAST in both directions. Not suitable for conservative investors or those who can't handle 10-15% daily swings. The March implied move of ±28.8% is MASSIVE for a $5B company.

-

📉 Competition from established data center operators: Traditional players (Equinix, Digital Realty) have decades of experience, better locations, superior network connectivity, existing customer relationships, and are rapidly building AI-specific facilities. Core Scientific's ONLY advantage is speed-to-market using existing power infrastructure - but that advantage narrows every quarter. If hyperscalers decide purpose-built > converted mining facilities, the thesis is dead.

🎯 The Bottom Line

Real talk: A sophisticated trader just CLOSED $1.1 million in March $17 calls on Core Scientific rather than holding through the critical February 26th Q4 earnings and March expiration. This isn't a bearish attack - it's professional position management by someone who sees poor risk/reward at current levels.

What this trade tells us:

- 🎯 The trader doesn't believe CORZ can rally 8.4% from $15.68 to $17+ in next 87 days

- 💰 They'd rather take whatever premium remains ($2.20/contract = $1.1M) than risk theta decay to zero

- ⚖️ The timing (64 days before Q4 earnings) suggests they're skeptical of upcoming results

- 📊 With stock trapped between $16 resistance and $13.50 support, sideways action is most likely

- ⏰ They may redeploy capital to better opportunities with clearer catalysts

This is NOT a "sell everything" signal - it's a "risk/reward is poor here" signal.

If you own CORZ:

- ✅ Consider trimming 25-40% at $15-16 levels if you're sitting on big YTD gains (up 260%!)

- 📊 Set MENTAL STOP at $13.00 (below put wall support) to protect remaining position

- ⏰ Don't get greedy - recent track record (delays, guidance cuts, failed merger) shows execution is HARD

- 🎯 If earnings on Feb 26 beat AND AI revenue accelerates to $30M+ quarterly, could re-add on breakout above $18

- 🛡️ Consider defensive put spreads to protect against earnings disappointment

If you're watching from sidelines:

- ⏰ February 26th after close is the moment of truth - DO NOT enter before earnings clarity!

- 🎯 Post-earnings pullback to $12-13 support would be EXCELLENT risk/reward entry

- 📈 Looking for confirmation of: CoreWeave sites going live, AI revenue exceeding $25M quarterly, 2025 guidance stability

- 🚀 Longer-term (12-18 months), if CoreWeave buildout executes successfully, the $8.7B contract value could drive $25-30 stock price

- ⚠️ But current valuation ($4.9B market cap) already reflects a LOT of success - margin for error is THIN

If you're bearish:

- 🎯 Wait for breakdown below $13.50 put wall before initiating shorts

- 📊 First support at $13.50 (gamma), major support at $12.00, disaster at $9.00

- ⚠️ Post-earnings put spreads offer defined-risk way to play downside after IV crush

- 📉 Watch for break below $13 - that's the trigger for potential cascade to $10-12

- ⏰ Key risk: CoreWeave contracts ARE real - thesis failure requires multiple severe negative catalysts

Mark your calendar - Key dates:

- 📅 February 26, 2025 (Wednesday) after market close - Q4 FY2024 earnings (64 DAYS!)

- 📅 March 20, 2025 - Quarterly triple witch, expiration of this $1.1M call trade

- 📅 Q1-Q2 2025 - First CoreWeave sites expected operational (revenue inflection point)

- 📅 April 2025 - Bitcoin halving one-year anniversary (mining economics assessment)

- 📅 H2 2026 - CoreWeave/OpenAI deployment begins (ultimate proof point)

Final verdict: Core Scientific's AI transformation story remains REAL - the $8.7 billion CoreWeave partnership, government contracts, and infrastructure assets are legitimate. BUT, execution has been TERRIBLE (delays, guidance cuts, failed merger), the timeline keeps slipping, and 85% of revenue is still from volatile Bitcoin mining. At $15.68 in a consolidation range with Q4 earnings as the next major catalyst, the risk/reward is NEUTRAL at best.

Be patient. Let earnings provide clarity. If AI revenue accelerates and CoreWeave sites go live, there will be plenty of upside to capture at $17-18 breakout. If execution stumbles again, you'll get a MUCH better entry at $12-13 support. The AI revolution will still be here in 2-3 months.

Don't fight the tape - the professional who just closed $1.1M in calls is telling you something. Listen. 💡

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. The unusual score of 0.85 (Typical) indicates this trade size is normal for CORZ's recent patterns - it does not imply you should follow the trade or that it will be profitable. Past performance doesn't guarantee future results. Bitcoin mining is extremely volatile and AI infrastructure buildouts carry significant execution risk. Company has negative cash flow and recent history of missing targets. Always do your own research and consider consulting a licensed financial advisor before trading.

About Core Scientific, Inc.: Core Scientific operates digital infrastructure for high-performance computing across three segments: Digital Asset Self-Mining (Bitcoin mining for internal operations), Digital Asset Hosted Mining (third-party hosting services), and HPC Hosting (GPU infrastructure for AI/ML workloads). Market cap of $4.9 billion in the Finance Services industry.