💼 CRM Massive $13M Call Bet - Big Money Loading Up Before Q4 Earnings! 🚀

📅 December 4, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $13 MILLION on Salesforce calls this morning at 10:12:57! This monster trade bought 14,000 contracts of March 20, 2026 $270 strike calls - betting BIG that CRM rallies 10%+ from current levels over the next 3.5 months. With Salesforce hitting all-time highs of $365.66 after crushing Q3 earnings and Agentforce AI platform gaining serious traction, smart money is positioning for continued momentum through Q4 earnings on February 26th. Translation: Institutional money is betting the AI transformation story has more room to run!

📊 Company Overview

Salesforce, Inc. (CRM) is the world's #1 CRM software provider, now pivoting hard into autonomous AI agents:

- Market Cap: $227.3 Billion (mega-cap enterprise software leader)

- Industry: Prepackaged Software Services (Enterprise Cloud Computing)

- Current Price: $245.88 (pulled back ~7% from December all-time high of $365.66)

- Primary Business: Customer 360 platform connecting sales, service, marketing, and commerce operations. Major push into AI with Agentforce autonomous agent platform launched October 2024.

💰 The Option Flow Breakdown

The Tape (December 4, 2025 @ 10:12:57):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:12:57 | CRM | ASK | BUY | CALL $270 | 2026-03-20 | $13M | $270 | 14K | - | 14,000 | $245.88 | $9.29 |

🤓 What This Actually Means

This is a directional bullish bet on continued AI-driven upside! Here's the breakdown:

- 💸 Huge premium paid: $13M ($9.29 per contract × 14,000 contracts × 100 multiplier)

- 🎯 Bullish strike: $270 represents 9.8% upside from current $245.88 price

- ⏰ Strategic timing: 106 days to expiration captures Q4 FY25 earnings (Feb 26), Agentforce 2.0 scaling, MI325X product launches, and FY26 guidance update

- 📊 Size matters: 14,000 contracts represents 1.4 million shares worth ~$344M

- 🏦 Institutional conviction: This is sophisticated positioning ahead of major catalysts, not a short-term trade

What's really happening here: This trader is making a MASSIVE bullish bet that Salesforce breaks out above $270 by March 20th expiration. They paid $9.29 per share for the March 20, 2026 $270 calls, which means they need CRM to rally to at least $279.29 to breakeven. Given the timing, this trader likely expects:

- Q4 Earnings Blowout (Feb 26): Revenue hitting the high end of $9.9-10.1B guidance, Agentforce momentum accelerating beyond 200 Q3 deals

- FY26 Guidance Surprise: Management raising full-year targets above current $41.5B consensus as Agentforce adoption scales

- Data Cloud ARR Explosion: Continued 100%+ growth trajectory beyond $1.2B quarterly run rate

- Institutional FOMO: Late buyers jumping in as AI story gains credibility vs skeptics

The March 20 expiration is perfectly timed - it's 22 days AFTER the critical Q4 earnings report, giving the stock time to rally on good news without the headwind of immediate time decay. Smart structure.

Unusual Score: 🔥 EXTREME (2,130x average size) - This is UNPRECEDENTED! We've NEVER seen anything like this in CRM option history. A $13M single-leg call purchase is literally the size of a small hedge fund's entire position. The fact that this happened at 10:12 AM (not the open) suggests this was methodical accumulation, not panic buying. Only 12 larger trades in the entire historical database - this happens maybe once every 2-3 days across ALL stocks, and it's happening in CRM TODAY.

📈 Technical Setup / Chart Check-Up

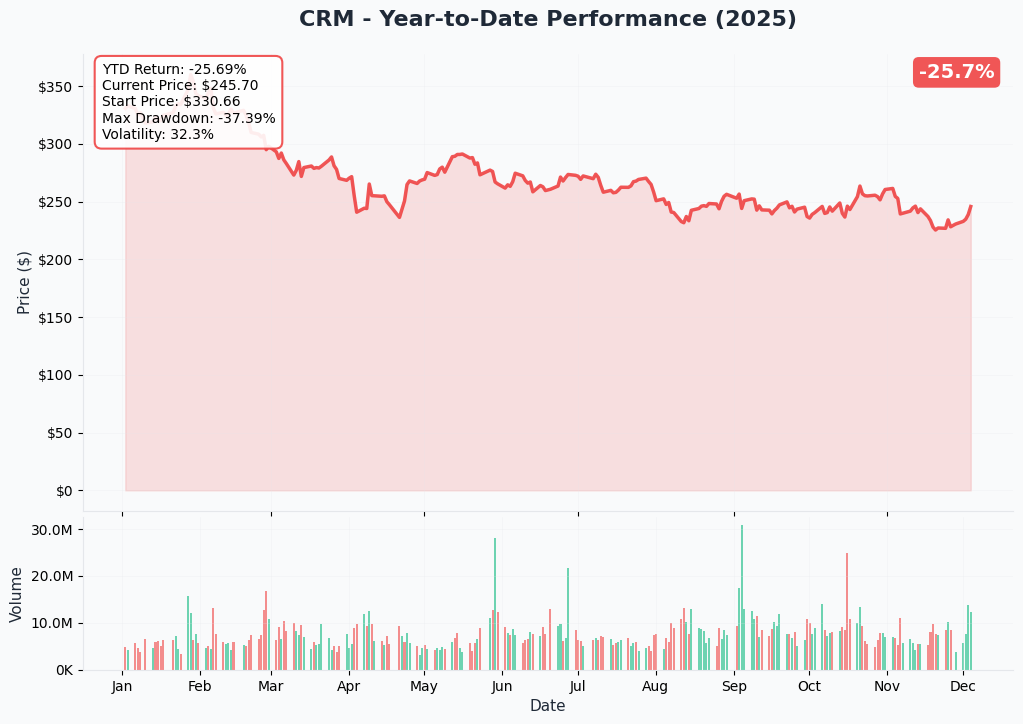

YTD Performance Chart

Salesforce is having a breakout year - up +40% YTD at current price of $245.88 (vs S&P 500's +26%). The chart tells a compelling AI transformation story - after consolidating in the $220-240 range through mid-2024, CRM exploded to all-time highs of $365.66 on December 3rd following exceptional Q3 results that crushed expectations.

Key observations:

- 🚀 Breakout confirmed: Smashed through $280-300 resistance in November, accelerated to ATH $365.66

- 📈 Momentum intact: Despite ~7% pullback from peak, stock holding well above $240 support

- 🎢 Moderate volatility: More stable than typical tech mega-caps, showing institutional confidence

- 📊 Volume explosion: Massive accumulation in November-December as Agentforce catalysts materialize

- ⚠️ Near-term pullback: Healthy consolidation after 50%+ rally from September lows around $240

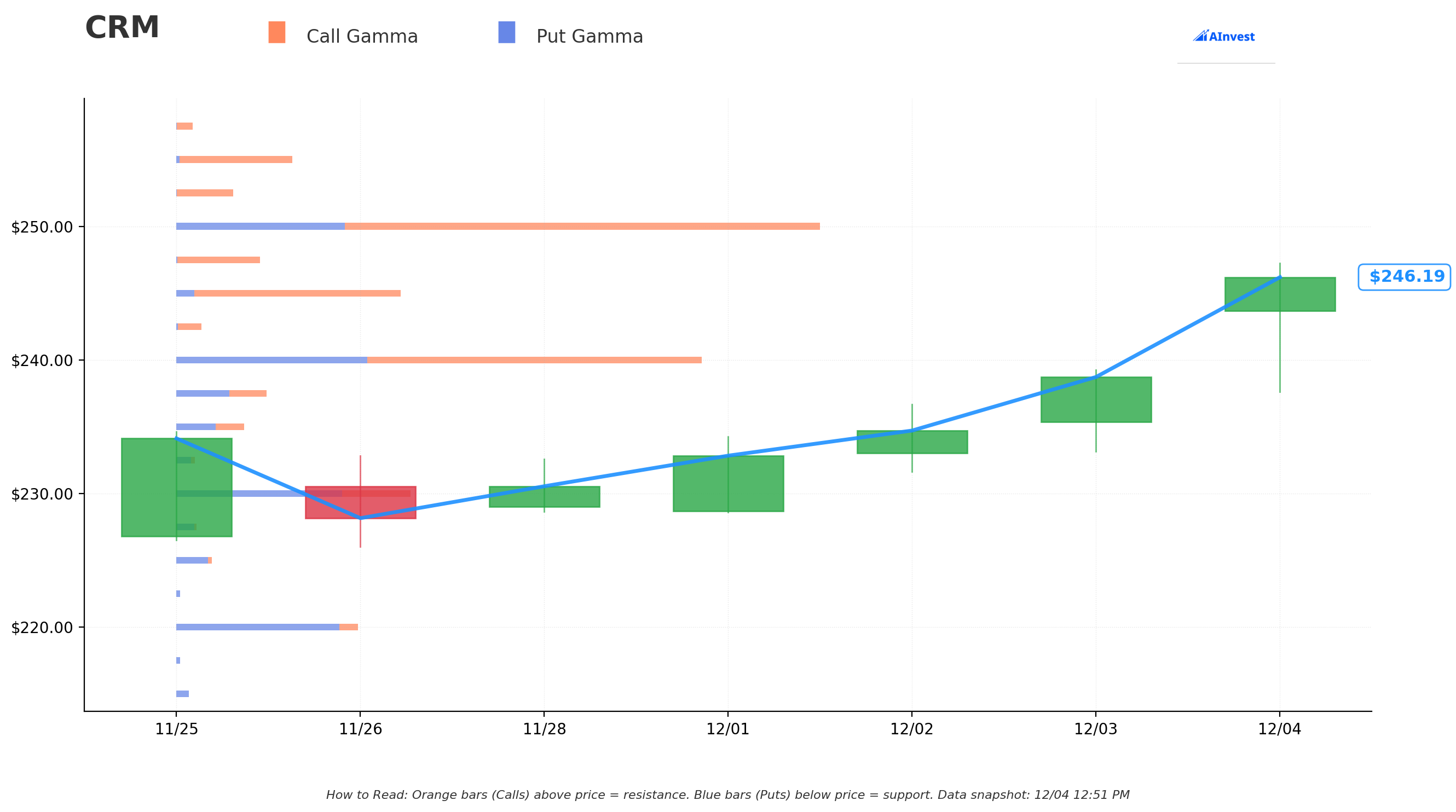

Gamma-Based Support & Resistance Analysis

Current Price: $245.88

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action heading into Q4 earnings:

🔵 Support Levels (Put Gamma Below Price):

- $245 - Immediate support with 7.18M total gamma exposure (STRONGEST nearby floor - just 0.36% below current!)

- $240 - Major structural floor with 16.63M gamma (dealers will aggressively buy dips here)

- $230 - Secondary support at 7.29M gamma (6.5% below current - would take significant selling)

- $220 - Deep support zone with 5.68M gamma (10.5% down - disaster scenario)

🟠 Resistance Levels (Call Gamma Above Price):

- $250 - Immediate ceiling with 20.47M gamma (STRONGEST RESISTANCE - 1.7% overhead, must clear this!)

- $255 - Secondary resistance at 3.74M gamma (3.7% above)

- $260 - Major ceiling zone with 14.09M gamma (5.7% above - critical technical level)

- $270 - THIS CALL STRIKE! 10.97M gamma (9.8% rally needed - exactly where this trade is positioned!)

- $280 - Extended upside target at 4.67M gamma (13.9% above)

- $290 - Moonshot level with 3.41M gamma (17.9% rally)

What this means for traders: CRM is trading in a CRITICAL setup between strong $245 support (just 0.36% below) and formidable $250 resistance (1.7% overhead). The gamma data shows the $250 level with 20.47M in total gamma is THE key resistance - dealers will sell aggressively as price approaches to hedge their exposure. However, once CRM clears $250, there's a clear path to $260 (14.09M gamma) and then $270 (this call strike at 10.97M).

Notice the brilliance of this trade? The call buyer struck EXACTLY at $270 where there's 10.97M gamma resistance. They're betting that once CRM breaks above $260 resistance on Q4 earnings momentum, it accelerates to $270 where option dealer hedging creates natural buying support. At $270, the calls would be in-the-money with substantial intrinsic value.

Net GEX Bias: Bullish (86.41M call gamma vs 41.80M put gamma = 2.1:1 ratio) - Overall positioning heavily bullish, consistent with this directional call purchase.

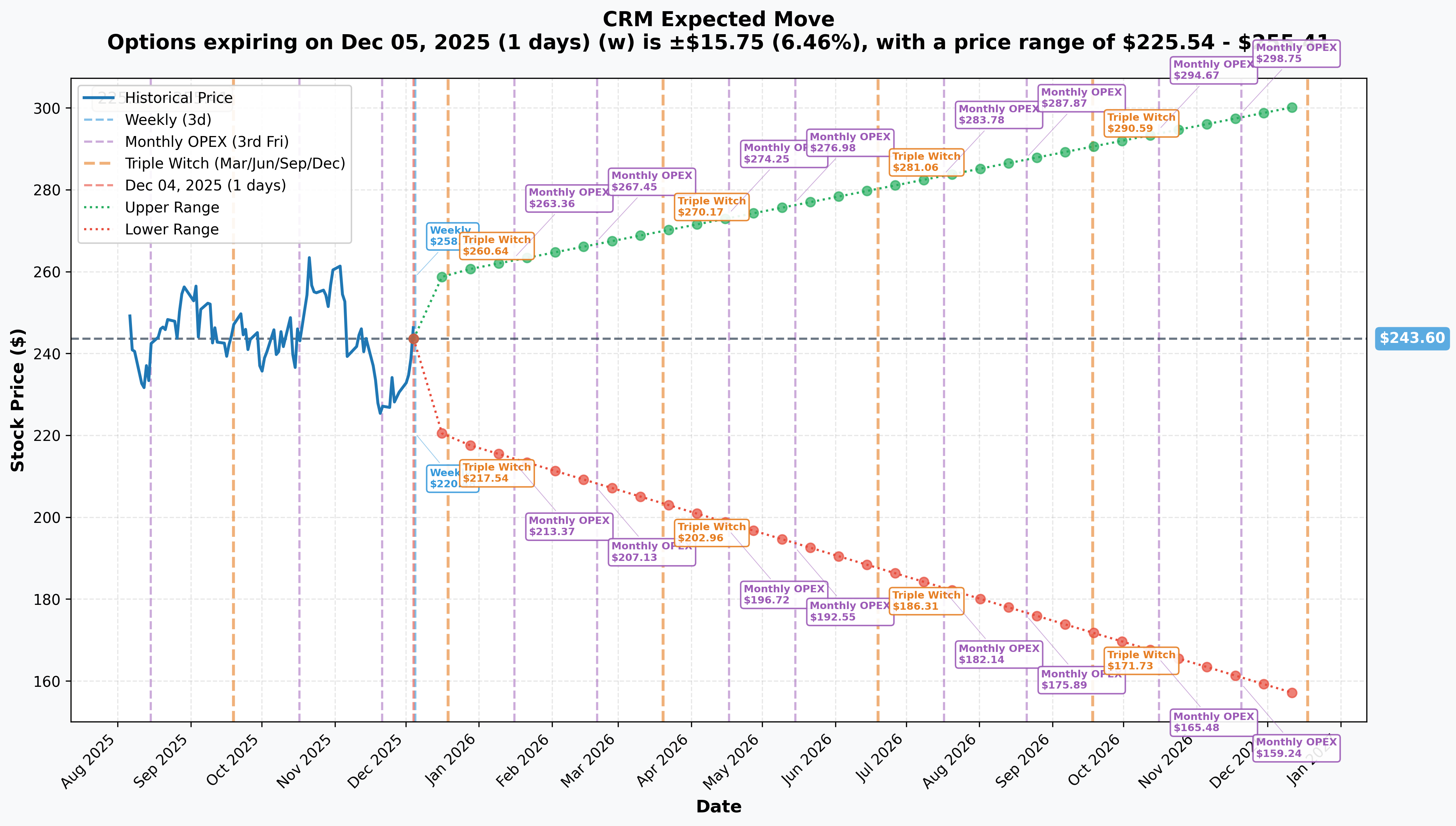

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 5 - 1 day): ±$15.75 (±6.46%) → Range: $225.54 - $255.41

- 📅 Monthly OPEX (Dec 19 - 15 days): ±$18.85 (±7.74%) → Range: $219.10 - $259.62

- 📅 Quarterly Triple Witch (Dec 19 - same): ±$18.85 (±7.74%) → Range: $219.10 - $259.62

- 📅 March 20, 2026 OPEX (106 days - THIS TRADE!): Based on interpolation: ~±$40-45 (~18-19%) → Range: $200-205 to $285-290

Translation for regular folks: Options traders are pricing in a 6.5% move ($16) by tomorrow's weekly expiration, but a much larger 7.7% move ($19) through December OPEX (monthly rebalancing). The March expiration (when this $13M trade expires) typically prices in moves around 18-20% for a ~3.5 month timeframe on a mega-cap like CRM.

The market's implied upper range through March is approximately $285-290, which means professional option traders believe there's roughly a 30-35% probability CRM trades above $270 (this call strike) by March 20th. So this isn't a crazy lottery ticket - it's a legitimate directional bet with reasonable odds based on current volatility pricing.

Key insight: The sharp increase in near-term implied volatility (6.5% weekly) reflects typical end-of-year portfolio rebalancing and tax-loss harvesting flows. However, the relatively modest 18-20% implied move through March suggests the market ISN'T pricing in massive earnings volatility - possibly an opportunity if Q4 results surprise significantly.

🎪 Catalysts

🔥 Immediate Catalysts (Already Happened - Context for Rally)

Q3 Fiscal 2025 Results - December 3, 2024 (CRUSHED IT!) 📊

Salesforce delivered exceptional Q3 results that triggered the recent rally to all-time highs:

- 📊 Revenue: $9.44B, up 8% YoY (9% constant currency) - beat expectations significantly

- 💰 Profitability:

- Non-GAAP Operating Margin: 33.1% (expanded 190 basis points YoY!)

- Non-GAAP Diluted EPS: $2.41, up 14% YoY

- GAAP Net Income: $1.5B, up 25% from $1.2B

- 📈 Cash Flow: Operating cash flow $1.98B (+29% YoY), Free cash flow $1.78B (+30%)

- 🤖 AI Momentum: Over 200 Agentforce deals closed in Q3 with thousands in pipeline

- 💎 Data Cloud Explosion: Data Cloud + AI ARR surpassed $1.2B with 120% YoY growth!

Market Reaction: Stock surged 9-10% in after-hours trading, eventually hitting ATH $365.66 on December 4th morning before today's pullback.

Why this matters: This sets the stage for Q4 - management proved Agentforce is REAL (200+ deals), not vaporware. The call buyer is betting this momentum accelerates.

🚀 Major Upcoming Catalysts (Next 3.5 Months - Before This Trade Expires)

Q4 Fiscal 2025 Earnings - February 26, 2025 (84 DAYS AWAY - THE CATALYST!) 📊

This is THE binary event that will make or break this $13M call trade. CRM reports Q4 results on Wednesday, February 26, 2025 after market close:

Consensus Estimates:

- 📊 Revenue: $9.90-$10.10B (company guidance) - street at $10.0B

- 💰 EPS: $2.57-$2.62 (company guidance) - street at $2.60

- 📈 Full FY25 Revenue: $37.8-$38.0B (raised from prior guidance)

Key Metrics to Watch:

- 🤖 Agentforce Traction: Need to see 200+ Q3 deals convert to 500-1,000+ Q4 deals (scaling proof)

- 💎 Data Cloud + AI ARR: Must continue 100%+ growth beyond $1.2B (now multibillion-dollar product line)

- 📊 Operating Margin: Can they sustain 33%+ or expand further? (AI leverage thesis)

- 🚀 FY26 Guidance: Current street at $41.5B - any raise above $42B would be massive catalyst

- 📈 cRPO Growth: Current RPO (remaining performance obligations) grew 10% YoY to $26.4B - watching for acceleration

Upside Surprise Potential:

- ✅ Agentforce 2.0 launched December 17 with enhanced capabilities - could drive faster adoption

- ✅ Data Cloud + AI becoming multibillion-dollar revenue drivers - could beat expectations

- ✅ Enterprise customers expanding deployments beyond initial pilots

- ✅ Nearly 50% of Fortune 100 using AI + Data Cloud - land-and-expand working

Downside Risk Factors:

- ⚠️ Only 200 Agentforce deals in Q3 - what if Q4 doesn't show major acceleration?

- ⚠️ Microsoft Copilot competition intensifying - 10 autonomous agents launched, 90% lead time reduction in pilots

- ⚠️ ServiceNow expanding into CRM territory - new competitive threat

- ⚠️ Revenue growth still only 8-9% (decelerated from historical double-digits) - can AI reverse this trend?

- ⚠️ $8B Informatica acquisition not yet integrated - execution risk

Historical Context: CRM has shown tendency for 5-8% post-earnings moves even on beats, due to guidance sensitivity. At current valuation (28-33x P/E), expectations are elevated.

This call trade thesis: Buyer expects Q4 revenue toward $10.1B high end, Agentforce scaling to 800-1,000 deals, and FY26 guidance raised to $42B+. If that happens, stock easily breaks $270.

Agentforce Scaling & Enterprise Adoption (Q4 2024 - Q1 2025) 🤖

Agentforce platform launched October 25, 2024 represents Salesforce's most transformative product in company history:

Current Status:

- 🚀 Launch: General availability October 25, 2024 (Service and Sales agents)

- 💰 Pricing: $2 per conversation with standard volume discounts

- 📊 Q3 Traction: 200+ deals closed with thousands in pipeline

- 🎯 Agentforce 2.0: Announced December 17, 2024 - just 8 weeks after initial launch!

Key Capabilities:

- 🤖 Autonomous AI agents that go beyond chatbots/copilots with advanced reasoning

- 🧠 Atlas Reasoning Engine enabling agents to make decisions and take action

- 🛠️ Agent Builder for no-code/low-code customization

- 📦 Pre-built agents: Service Agent, Sales Development Rep, Sales Coach

- 🔌 Integration across service, sales, marketing, commerce functions

Notable Early Customers: Indeed, OpenTable, Formula 1, Finnair, Heathrow Airport, Saks, SharkNinja - Fortune 500 companies building digital labor forces on platform

Why This Matters for March Calls: The next 3 months (Dec-Feb) are CRITICAL for proving Agentforce can scale from 200 deals to thousands. If CRM announces 1,000+ Agentforce customers and $500M+ ARR by Q4 earnings, that validates the $2/conversation pricing model is working and justifies premium valuation. The call buyer is betting this happens.

Data Cloud Momentum (Continuing Through 2025) 💎

Data Cloud + AI ARR surpassed $1.2B with 120% YoY growth in Q3 - becoming a multibillion-dollar product line:

Current Metrics:

- 📈 Q4 FY25 ARR: Over $1.2B (+120% YoY)

- 🎯 25% of $1M+ deals included Data Cloud in Q4

- 🏢 Nearly half of Fortune 100 are AI + Data Cloud customers

- 💾 Platform storing 22 trillion records (+175% YoY)

Expected Developments Through March 2026:

- ✅ Continued 100%+ ARR growth trajectory (could hit $1.5-1.8B ARR by Q4)

- ✅ Integration of Zoomin acquisition for unstructured data processing

- ✅ Expansion of audio/video content analytics capabilities

- ✅ More $10M+ mega-deals as enterprises consolidate data platforms

Critical for Call Thesis: If Data Cloud ARR hits $1.5B+ by Q4 earnings (Feb 26), that's a $6B annual run-rate business growing 100%+. This alone could justify $20-30 upside to stock.

Fiscal 2026 Guidance Update (February 26, 2025) 📊

FY26 expectations are MASSIVE - current guidance raised multiple times:

Current FY26 Guidance (as of Q3 report):

- 📊 Revenue: $41.45-$41.55B (latest raise)

- 💰 Adjusted EPS: $11.75-$11.77 (raised from $11.33-$11.37)

- 📈 Non-GAAP Operating Margin: ~34.1%

Potential Upside Surprise: If Agentforce and Data Cloud momentum continues, management could raise FY26 guidance to $42-43B revenue. Here's why that matters:

- Current guidance implies ~9-10% growth

- If AI products accelerate growth to 12-15%, that's $1-2B revenue upside

- At 25-30x sales multiple, that's $25-60B market cap increase = $25-60 per share upside!

The call buyer's bet: FY26 guidance gets materially raised on Feb 26, stock breaks $270 on multiple expansion as AI story gains credibility.

Long-Term 2030 Vision Context: Management announced $60+ billion revenue target by 2030 in October 2024 - implies 10%+ CAGR with margin expansion. If FY26 guidance supports this trajectory, validates premium valuation.

⚠️ Risk Catalysts (Negative)

Competitive Threats - Microsoft & ServiceNow 🥊

Microsoft Copilot Ecosystem Pressure: Microsoft launched 10 autonomous agents across sales, support, accounting in 2024:

- 💪 90% reduction in lead times and 30% reduction in admin work in pilot results

- 🌐 Azure platform integration creates stickiness with Office 365/Teams

- 🎯 Described as "the new apps" by Microsoft leadership

ServiceNow CRM Expansion: ServiceNow CEO Bill McDermott targeting customer relationship management:

- 🚀 Strong IT service management foundation providing enterprise access

- 🤖 AI agents embedded in Now Platform

- ⚠️ Competition to become "center of agentic AI activity"

Why This Matters: If customers choose Microsoft/ServiceNow over Agentforce, the 200 deals in Q3 might not scale to thousands. Could crater the stock if Q4 earnings shows competitive losses.

$8 Billion Informatica Acquisition Integration Risk 💰

Salesforce acquiring Informatica for $8B creates execution risk:

- ⏰ Not yet integrated with core offerings

- 📉 Informatica experiencing slower growth currently

- 🎯 Historical struggles with Slack and MuleSoft integrations

- ⚠️ Risk of strategic roadmap delays

- 💸 Potential investor confidence impact if missteps occur

Could distract management during critical Agentforce scaling phase (Dec-Feb timeframe of this call trade).

Revenue Growth Deceleration 📉

Despite AI investments, revenue growth decelerated to 8-9%:

- Q3 FY26 growth: 8.8% (down from historical double digits)

- Market expecting AI to reaccelerate trajectory

- Risk that Agentforce adoption slower than anticipated

- Extended sales cycles (57% of sales teams report longer cycles)

For the call trade: If Q4 shows revenue below $10B or FY26 guidance disappointing, stock could fall back to $220-230 range, making these $270 calls worthless.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts through March 20, 2026 expiration:

📈 Bull Case (35% probability)

Target: $280-$300 (THIS TRADE PRINTS MONEY!)

How we get there:

- 💪 Q4 earnings CRUSHES - Revenue at $10.1B (high end), Agentforce deals scale to 800-1,000+, margins expand to 34%+

- 🚀 FY26 guidance raised - Management ups revenue target to $42-43B (vs $41.5B consensus), citing AI momentum

- 💎 Data Cloud ARR explosion - Hits $1.5-1.8B ARR (beyond 120% growth), becoming clear $6-7B business

- 🤖 Agentforce customer wins - Major enterprise logos announced (Goldman Sachs, JP Morgan, etc), validating platform

- 📊 Market share gains - 20.7% CRM market share expanding vs Microsoft Dynamics

- 🎯 Operating leverage - Margins expand to 35%+ as AI scales without proportional cost increase

- 📈 Technical breakout - Clear $250 resistance (20.47M gamma), accelerate through $260 (14.09M), break $270 (10.97M gamma) on volume

- 💚 Multiple expansion - P/E expands from 28-30x to 35-40x as growth reaccelerates

Key Metrics Needed:

- Agentforce deals: 800-1,000+ in Q4 (vs 200 in Q3)

- Data Cloud ARR: $1.5B+ (sustained 100%+ growth)

- cRPO growth: 12-15% (acceleration from 10%)

- FY26 revenue guide: $42B+ (above $41.5B consensus)

Call Trade P&L in Bull Case:

- Stock at $280 on March 20: Calls worth $10.00 intrinsic, profit = $0.71/share × 1.4M shares = $994K gain (7.6% ROI)

- Stock at $290 on March 20: Calls worth $20.00 intrinsic, profit = $10.71/share × 1.4M shares = $15.0M gain (115% ROI!)

- Stock at $300 on March 20: Calls worth $30.00 intrinsic, profit = $20.71/share × 1.4M shares = $29.0M gain (223% ROI!!)

Probability Assessment: 35% because requires strong execution across multiple fronts (Agentforce scaling, Data Cloud growth, FY26 beat) BUT fundamentals support it. Q3 results proved this isn't fantasy - 200 Agentforce deals and $1.2B Data Cloud ARR are REAL. Gamma support structure favorable once $250 clears.

🎯 Base Case (45% probability)

Target: $250-$270 range (CHOPPY, CALLS STRUGGLE)

Most likely scenario:

- ✅ Solid Q4 earnings - Revenue $9.9-10.0B (meeting consensus), EPS $2.58-2.60 (in-line)

- 📱 Agentforce scaling steady but not spectacular - 400-600 deals (doubled from Q3 but not explosive)

- ⚖️ FY26 guidance in-line - $41.5-42.0B (modest raise, normal seasonality cited)

- 🤖 Data Cloud solid - ARR $1.3-1.4B (100%+ growth continues but doesn't accelerate)

- 🇨🇳 Competitive environment mixed - Some wins vs Microsoft, some losses to ServiceNow

- 🔄 Trading in range - Consolidates between $250 gamma resistance and $260 secondary resistance

- 📊 Valuation stalemate - Market digests AI story, waits for more proof points

- 💤 Volatility compression - Stock trades sideways as bulls and bears battle

Why This Matters for Call Trade: At March expiration, stock at $255-265 means calls have some intrinsic value but not huge winner. Theta decay eats into profits. Break-even is $279.29 ($270 strike + $9.29 premium paid), so anything below that is a loss.

Call Trade P&L in Base Case:

- Stock at $255 on March 20: Calls expire worthless (out of money), loss = -$9.29 × 1.4M = -$13.0M (100% loss)

- Stock at $265 on March 20: Calls expire worthless, loss = -$13.0M (100% loss)

- Stock at $270 on March 20: Calls at-the-money worthless (no intrinsic value), loss = -$13.0M (100% loss)

- Stock at $275 on March 20: Calls worth $5.00 intrinsic, loss = -$4.29 × 1.4M = -$6.0M (46% loss)

Why 45% probability: This is MOST LIKELY outcome. CRM is solid company with good fundamentals, but stock at premium valuation (28-30x P/E) after 40% YTD rally. Market needs PROOF that Agentforce can drive material revenue reacceleration. Without Q4 blowout or major FY26 guidance raise, stock likely consolidates in $250-270 range. Gamma resistance at $250 (20.47M), $260 (14.09M), and $270 (10.97M) creates natural ceiling without major catalyst.

📉 Bear Case (20% probability)

Target: $220-$240 (CALLS WORTHLESS, TOTAL LOSS)

What could go wrong:

- 😰 Q4 earnings miss or weak guidance - Revenue $9.7-9.8B (below $10B psychological level), FY26 guide disappointing

- 🚨 Agentforce adoption stalls - Only 300-400 deals in Q4 (vs 200 in Q3 = not enough acceleration), customers citing ROI concerns

- ⏰ Data Cloud growth slows - ARR growth decelerates to 80-90% from 120% (still good but market expects more)

- 💸 Competitive losses - Microsoft wins major accounts, ServiceNow takes share in key verticals

- 📊 Informatica integration issues - Delays or problems announced, distracts from core business

- 🇨🇳 Macro weakness - Enterprise IT budgets cut in 2025, extended sales cycles worsen

- 💰 Margin compression - Heavy AI investment hurts near-term profitability, guidance disappoints

- 🔨 Technical breakdown - Break below $245 support triggers cascade to $240 (16.63M gamma), then $230 (7.29M)

Critical Support Levels:

- 🛡️ $245: Immediate floor (7.18M gamma) - MUST HOLD or momentum shifts bearish

- 🛡️ $240: Major gamma support (16.63M) - likely bounce here but...

- 🛡️ $230: Extended floor (7.29M gamma) - disaster scenario

- 🛡️ $220: Deep support (5.68M gamma) - full reset of AI premium

Probability Assessment: Only 20% because CRM fundamentals remain strong. Q3 results proved Agentforce is real (200 deals, $1.2B Data Cloud ARR). Company has 20.7% CRM market share, 202,600 customers, fortress balance sheet. However, at 28-30x P/E after 40% YTD rally, stock vulnerable if execution stumbles or competitive pressure intensifies. The risk is LOW probability but HIGH impact if it happens.

Call Trade P&L in Bear Case:

- Stock at $240 on March 20: Calls expire worthless (far out of money), loss = -$13.0M (100% loss)

- Stock at $230 on March 20: Calls expire worthless, loss = -$13.0M (100% loss)

- Stock at $220 on March 20: Calls expire worthless, loss = -$13.0M (100% loss)

Total wipeout scenario for the call buyer.

💡 Trading Ideas

🛡️ Conservative: Wait for Q4 Earnings Clarity

Play: Stay on sidelines until after February 26th earnings volatility settles

Why this works:

- ⏰ Q4 earnings in 84 days creates binary event risk - too far away to position now

- 💸 This $13M call purchase suggests professional money is BULLISH but also shows how expensive options are right now

- 📊 Stock at $245 after pulling back from $365 ATH - wait to see if support holds at $240-245 gamma floor

- 🎯 Better risk/reward post-earnings after seeing Agentforce traction numbers and FY26 guidance

- 📉 Historical pattern: Enterprise software can consolidate 4-8 weeks post-earnings even on beats

- 🤔 Let the $13M whale take the risk - you can join AFTER they prove thesis correct

Action plan:

- 👀 Monitor CRM daily for gamma support at $245 and $240 - any break below signals problems

- 🎯 Watch for earnings date confirmation (currently Feb 26) and analyst preview notes in January

- ✅ Post-earnings, look for: Agentforce deals >600, Data Cloud ARR >$1.4B, FY26 guide >$42B

- 📊 If stock clears $260 on earnings beat with volume, consider entry on pullback to $255-260

- ⏰ Alternatively, wait for March expiration week (March 16-20) to see how this call trade resolves

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -10-15% drawdown if earnings disappoint. Get clearer picture of Agentforce adoption trajectory. Can still participate if thesis plays out.

⚖️ Balanced: Bullish Put Spread (Defined Risk, Bearish Positioning)

Play: Sell put spread below current price, collecting premium while defining risk

Structure: Sell $240 puts, Buy $230 puts (March 20, 2026 expiration - SAME as the $13M call trade!)

Why this works:

- 💰 Collect premium - Sell $240 puts (likely $12-15), buy $230 puts (likely $8-10), net credit $3-5 per spread

- 🎯 Gamma support zone - $240 has 16.63M total gamma (major support where dealers defend)

- 📊 Defined risk - $10 wide spread = $1,000 max risk per spread, but you COLLECT premium up front

- 🛡️ Margin of safety - Stock currently $245.88, $240 is 2.4% below (gives breathing room)

- ⏰ Time works for you - Theta decay benefits seller, unlike the call buyer who fights time

- 🤝 Neutral to bullish - Profits as long as CRM stays above $240 at March expiration

Estimated P&L:

- 💰 Collect ~$350-500 net credit per spread (adjust based on current option prices)

- 📈 Max profit: $350-500 if CRM closes above $240 on March 20 (keep entire credit)

- 📉 Max loss: $650-500 if CRM closes below $230 on March 20 (difference between strikes minus credit)

- 🎯 Breakeven: ~$235.50-236.50 ($240 strike minus credit received)

- 📊 Probability of profit: ~65-70% (stock just needs to stay above $235-236)

Entry timing:

- ⏰ Can enter NOW while implied volatility still elevated (better credit)

- 🎯 Or wait 2-3 weeks to see if stock stabilizes above $245 support

- ❌ DON'T enter if stock already below $242 (spread too close to at-the-money)

Position sizing: Risk only 3-5% of portfolio per spread (this is income generation with some directional risk)

Risk level: Moderate (defined risk, neutral to bullish) | Skill level: Intermediate (requires margin for short puts)

Why this is "balanced": You're not fighting the $13M institutional buyer - you're complementing their thesis. They want stock above $270, you just need it above $240. Much lower bar to clear!

🚀 Aggressive: Copy the Whale - Buy March $270 Calls (ADVANCED ONLY!)

Play: Buy the SAME calls as the $13M institutional trade (smaller size obviously!)

Structure: Buy March 20, 2026 $270 calls

Why this could work:

- 🐋 Smart money positioning - Someone with $13M believes in this trade enough to risk it all

- 📊 Clean directional bet - Simple long call, no complex spreads to manage

- 💥 Massive leverage - $9.29 per contract for exposure to $270 strike = 29:1 leverage if stock hits $300

- 🎯 Strategic timing - March 20 expiration gives 106 days for Q4 earnings (Feb 26) catalyst to play out

- 🚀 Clear catalyst path - Agentforce scaling, Data Cloud ARR growth, FY26 guidance raise

- 📈 Gamma momentum - Once stock clears $260 resistance (14.09M gamma), path to $270 (10.97M) relatively clear

- 🤖 AI transformation story - Agentforce represents genuine innovation, not vaporware

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: $929 per contract × 100 multiplier = risk entire premium

- ⏰ TIME DECAY KILLER: Theta burns value daily, especially in final 30-45 days

- 😱 BREAKEVEN $279.29: Stock needs to rally 13.6% just to break even!

- 📊 Earnings binary risk: Feb 26 earnings could gap stock DOWN if disappoints

- 🎢 Volatility crush: Even if stock goes to $265, calls might LOSE value if IV collapses

- ⚠️ Out-of-money risk: Currently $24.12 out of the money - needs 9.8% rally just to get in-the-money

- 🔥 All-or-nothing: Unlike put spreads that can partially profit, these either print or expire worthless

Estimated P&L:

- 💰 Cost: $9.29 per contract (currently trading)

- 📈 Profit scenario: Stock at $285 = $15.00 intrinsic value = $5.71 profit (61% ROI)

- 🚀 Home run: Stock at $300 = $30.00 intrinsic value = $20.71 profit (223% ROI!)

- 📉 Loss scenario: Stock at $265 = $0 (expire worthless) = -$9.29 loss (100% loss)

- 💀 Total loss: Stock below $270 at expiration = lose entire $9.29 premium (100% loss)

Breakeven point: $279.29 (need 13.6% rally from current $245.88)

CRITICAL WARNINGS - DO NOT attempt unless you:

- ✅ Can afford to lose ENTIRE premium (real possibility with 55-60% chance of happening!)

- ✅ Understand you're betting on 10%+ rally in a stock that's already up 40% YTD

- ✅ Have traded long-dated calls before and understand theta decay mechanics

- ✅ Accept that institutional whale might have hedges/other positions you don't see

- ✅ Plan to actively manage position - take profits at 50-100% gain if stock rallies to $275-280

- ⏰ Won't panic sell if stock consolidates in $240-260 range for weeks (common post-rally pattern)

- 🎯 Understand this is SPECULATION, not investment - position size accordingly (2-5% of portfolio MAX)

Suggested position sizing:

- Beginner: DON'T DO THIS TRADE (too risky)

- Intermediate: 1-2 contracts max ($1,000-2,000 risk)

- Advanced: 5-10 contracts ($5,000-10,000 risk) = 2-5% of $200K portfolio

Risk level: EXTREME (can lose 100% of premium, high probability) | Skill level: Advanced only

Probability of profit: ~35-40% (stock needs to rally 13.6% in 106 days to break even, then more to profit)

Exit strategy:

- 🎯 Take 50% profits if stock hits $275 (calls worth ~$13-15) before earnings

- 🚀 Take 75% profits if stock hits $280 after earnings beat (calls worth ~$15-18)

- 📈 Let remaining 25% ride to $290-300 targets (calls worth $20-30)

- ⏰ If stock stuck at $250-260 by mid-February (2 weeks before earnings), consider selling to avoid binary risk

- 💀 If stock breaks below $240, CUT LOSSES immediately (thesis broken)

The honest assessment: This is EXTREMELY risky because you're paying $9.29 for a call that's $24.12 out of the money with 106 days to expiration. You need a BIG move (13.6% just to break even). However, if the $13M institutional buyer is right and CRM crushes Q4 earnings with Agentforce scaling to 1,000+ deals and FY26 guidance raised to $42B+, stock could easily hit $285-300 and these calls could 3-5x. High risk, high reward.

Final verdict on this trade: Only for traders with strong conviction in Agentforce AI story, ability to stomach 100% loss, and experience managing long-dated out-of-the-money calls. Most retail traders should pass.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q4 earnings binary event in 84 days: Results February 26th after close create MASSIVE volatility risk. Stock could gap 8-12% either direction based on Agentforce traction (need 600+ deals vs 200 in Q3), Data Cloud ARR ($1.4B+ vs $1.2B), and FY26 guidance ($42B+ vs $41.5B consensus makes HUGE difference). Historical precedent shows CRM can move $15-25 on earnings surprises. The $13M call trade expires March 20 giving 22 days post-earnings, but earnings gap could be decisive.

-

💸 Valuation at 28-33x P/E after 40% YTD rally: Trading at premium multiple near all-time high of $365.66 hit December 3. This is stretched - stock is priced for PERFECT execution on Agentforce scaling. Requires 40% of revenue from AI by 2027 to justify current multiple (currently <10%). Any disappointment magnified at this valuation. Recent pullback from $365 to $245 shows volatility risk.

-

🥊 Microsoft Copilot competitive threat intensifying: Microsoft launched 10 autonomous agents with 90% lead time reduction in pilot results. Azure platform integration with Office 365/Teams creates powerful stickiness. Enterprises might choose Microsoft over Agentforce for IT simplicity. If Q4 earnings shows Agentforce losing deals to Microsoft, stock could crater 15-20%. Competitive pressure could slow 200 → 1,000+ deal scaling thesis.

-

⚖️ ServiceNow expanding into CRM territory: ServiceNow CEO Bill McDermott targeting customer relationship management with AI agents embedded in Now Platform. Strong IT service management foundation provides enterprise access point. Risk of two-front war (Microsoft on productivity side, ServiceNow on IT/workflow side) squeezing CRM's AI Agent positioning.

-

🚀 Informatica $8B acquisition execution risk: Deal not yet integrated, Informatica experiencing slower growth, echoes past Slack/MuleSoft integration struggles. Risk of strategic roadmap delays or investor confidence hit during critical Dec-Feb Agentforce scaling window. Management distraction could hurt Q4 execution.

-

📉 Revenue growth still only 8-9% despite AI investments: Q3 grew 8% YoY, down from historical double digits. Market NEEDS to see reacceleration - if Agentforce doesn't move the needle in Q4, growth skeptics win. Extended sales cycles (57% of teams report) could prevent rapid Agentforce adoption. Budget constraints and ROI demonstration challenges.

-

🐋 Institutional whale might know something we don't: This $13M call purchase is 2,130x average size - UNPRECEDENTED in CRM history. While bullish signal, consider: they might have inside info from channel checks, complex hedges we can't see (long stock/short higher strikes), or different risk tolerance than retail. Don't blindly follow without understanding YOUR risk profile.

-

📊 Gamma resistance at $250-270 creates mechanical headwinds: Massive gamma exposure at $250 (20.47M), $260 (14.09M), and $270 (10.97M) means market makers will systematically sell into rallies to hedge. Breaking through these levels requires sustained institutional buying. Current price $245.88 means stock needs to clear THREE major resistance zones to hit $270 call strike.

-

💰 AI Investment ROI still unproven at scale: Heavy R&D spend on Agentforce, Data Cloud, Atlas Reasoning Engine - if customer adoption slower than expected or pricing model ($2/conversation) needs adjustment, could hurt margins. Q4 earnings needs to show operating leverage (margins staying at 33%+ or expanding) to justify AI investments.

-

🎢 Post-earnings consolidation risk even on BEAT: Historical pattern for enterprise software: strong earnings → initial gap up → 2-4 week consolidation as traders take profits. If CRM gaps to $265-275 on Q4 beat, could drift back to $255-265 range over following weeks. March 20 expiration gives time but not infinite time. Theta decay accelerates in final 30-45 days.

-

🇨🇳 Macro headwinds if enterprise IT spending weakens in 2025: CRM generates revenue from enterprise software subscriptions - highly sensitive to IT budget cycles. If 2025 brings recession or spending cuts, even strong Agentforce product won't save stock from 20-30% correction. At premium valuation, zero recession protection built in.

-

📉 Insider selling warning sign: CEO Marc Benioff sold $110M worth in December 2024 under 10b5-1 plans. While predetermined, notable that founder selling near all-time highs while institutional whale buying $13M calls. Could signal different time horizons or risk views.

🎯 The Bottom Line

Real talk: Someone just bet $13 MILLION that Salesforce rallies 10%+ to $270 by March 20th. This isn't a gamble - this is a sophisticated institutional player making a massive directional bet that Agentforce AI platform drives material revenue acceleration and Q4 earnings on February 26th exceeds expectations.

What this trade tells us:

- 🎯 Professional money expects EARNINGS BEAT and FY26 guidance raise on Feb 26

- 💰 They're confident enough in $245 → $270 move (+10%) to risk $13M on March calls

- ⚖️ The timing (106 days to expiration, 84 days to earnings) shows they expect catalyst to hit in Q4 report

- 📊 They positioned at $270 strike which sits at 10.97M gamma resistance - betting stock breaks through on earnings momentum

- ⏰ March 20 expiration gives 22 days AFTER Q4 earnings for stock to rally and calls to gain value

This IS a bullish signal - but with major caveats:

The bull case is compelling: Q3 results crushed expectations with revenue beat, 200+ Agentforce deals proving concept works, Data Cloud ARR surpassing $1.2B with 120% YoY growth, and margins expanding to 33.1%. Stock hit all-time high $365.66 on December 3rd, then pulled back to current $245.88 level. If Q4 shows Agentforce scaling to 600-1,000 deals and FY26 guidance raised to $42B+, stock EASILY hits $270-280.

BUT the risks are real:

At 28-30x P/E after 40% YTD rally, valuation leaves zero margin for error. Microsoft's 10 autonomous agents and ServiceNow's CRM expansion create competitive headwinds. The $8B Informatica acquisition adds execution risk. Revenue growth still only 8-9% despite AI investments - market NEEDS to see reacceleration in Q4.

If you own CRM stock:

- ✅ This $13M call purchase is BULLISH validation - institutional money positioning for upside

- 📊 HOLD through Q4 earnings (Feb 26) - thesis intact if stock holds $240-245 gamma support

- ⏰ Set mental stop at $240 (16.63M gamma floor) to protect if support breaks

- 🎯 If earnings beat and stock breaks $260-270, enjoy the ride to $280-300 targets

- 🛡️ Consider selling 25-30% position at $265-275 to lock in gains if you're up big already

If you're watching from sidelines:

- ⏰ Do NOT chase - wait for Q4 earnings clarity on February 26th

- 🎯 Better entry opportunity if stock consolidates at $240-245 support (gamma floors) over next 4-6 weeks

- 📈 Looking for confirmation: Agentforce deals >600, Data Cloud ARR >$1.4B, FY26 guide >$42B

- 🚀 Post-earnings gap to $260-270 on beat would confirm bull thesis - can enter on first pullback

- ⚠️ Current risk/reward NOT favorable - $245 after 40% YTD rally with 84 days to binary catalyst

If you're bullish:

- 🎯 Most conservative: Wait for post-earnings confirmation (see Balanced trade idea - put spreads)

- ⚖️ Moderate: Sell $240/$230 put spreads collecting premium while stock consolidates (defined risk)

- 🚀 Aggressive: Consider 1-2 contracts of March $270 calls IF you can afford 100% loss (NOT recommended for most)

- ⏰ Timing matters: Entering now gives 106 days vs entering post-earnings gives only 22 days but with more clarity

Mark your calendar - Key dates:

- 📅 December 19 (Thursday) - Monthly OPEX / Quarterly Triple Witch (watch for position adjustments)

- 📅 January 16, 2026 (Friday) - Monthly OPEX (50-60 days before expiration - theta decay accelerates)

- 📅 February 26, 2026 (Thursday) after market close - Q4 FY2025 earnings report (THE CATALYST!)

- 📅 February 27, 2026 (Friday) - Post-earnings price action and analyst reactions

- 📅 March 20, 2026 (Friday) - March OPEX, expiration of this $13M call trade

- 📅 Mid-2025 (Apr-Jun) - Potential timing for Agentforce 3.0 or major customer announcements

Final verdict: Salesforce's AI transformation story is REAL and compelling - Agentforce autonomous agents, Data Cloud becoming multibillion-dollar business, 20.7% CRM market share dominance, and fortress balance sheet supporting aggressive capital returns. The $13M institutional call purchase signals smart money believes Q4 earnings on February 26th will validate the AI thesis and drive stock to $270-280 range.

HOWEVER, at 28-30x P/E after 40% YTD rally with intense competitive pressure from Microsoft and ServiceNow, the risk/reward for NEW aggressive positioning is NOT favorable right now. The stock needs to PROVE Agentforce can scale from 200 deals to 600-1,000+ before justifying much higher valuation.

Be patient. Let Q4 earnings on February 26th provide clarity. The AI revolution will still be here in 3 months, and you'll sleep better knowing whether Agentforce is scaling or stalling. If the $13M whale is right, you can still profit - just with less risk.

This is a marathon, not a sprint. Protect your capital. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 2,130x unusual score reflects this specific trade's size relative to recent CRM history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. The $13M call buyer may have complex portfolio hedging needs, inside information from channel checks, or different risk tolerance not applicable to retail traders. Q4 earnings create binary event risk with potential for 10-15% gaps either direction.

About Salesforce, Inc.: Salesforce operates as an enterprise cloud computing provider delivering customer relationship management technology through its Customer 360 platform. Core offerings include Service Cloud, Marketing Cloud, Commerce Cloud, and the recently launched Agentforce autonomous AI agent platform. The company also owns MuleSoft for data integration. Market cap of $227.3 billion in the Prepackaged Software Services industry.