🛡️ EFX $7.2M Risk Reversal Unwind - Smart Money Exits Bullish Position!

📅 December 5, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just closed $7.2 MILLION in Risk Reversal positions on Equifax this morning at 11:31:40! This massive unwind sold 18,000 contracts of $220 strike calls while buying back 18,000 contracts of $200 puts (both expiring December 19th) - dismantling a sophisticated bullish position just 14 days before expiration. With EFX trading at $212.45, this institutional player is taking profits or de-risking ahead of critical Q4 2024 earnings on February 6, 2025. Translation: Smart money is closing out their upside bets and removing downside protection - looks like they're going neutral or fully exiting before the next catalyst.

📊 Company Overview

Equifax (EFX) is one of the "Big Three" credit bureaus alongside Experian and TransUnion, dominating the U.S. consumer credit reporting industry:

- Market Cap: $25.86 Billion

- Industry: Consumer Credit Reporting, Collection Agencies

- Current Price: $212.45 (as of December 5, 2025)

- Primary Business: Credit reports and credit histories (60% revenue), workforce solutions including income verification and HR services (40% revenue), with 20-25% from international operations

💰 The Option Flow Breakdown

The Tape (December 5, 2025 @ 11:31:40):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Strategy |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:31:40 | EFX | MID | SELL | CALL $220 | 2025-12-19 | $4.4M | $220 | 18K | 18K | 17,650 | $212.45 | $2.49 | Risk Reversal |

| 11:31:40 | EFX | MID | BUY | PUT $200 | 2025-12-19 | $2.8M | $200 | 18K | 20K | 17,590 | $212.45 | $1.62 | Risk Reversal |

Net Premium: $4.4M (calls sold) - $2.8M (puts bought) = $1.6M credit received to close position

🤓 What This Actually Means

This is a Risk Reversal unwind - closing out a sophisticated bullish position! Here's the breakdown:

What is a Risk Reversal? A classic Risk Reversal (also called a "collar" or "synthetic long") is when you:

- SELL PUTS (collect premium, take on downside risk) at lower strike ($200)

- BUY CALLS (pay premium, get upside exposure) at higher strike ($220)

- Net effect: Bullish directional bet with defined risk

Today's Trade = CLOSING this position:

- ✅ Sell to Close (STC) the $220 calls - closing out the upside exposure they previously owned

- ✅ Buy to Close (BTC) the $200 puts - closing out the downside risk they previously sold

- 💸 Net credit of $1.6M - they're getting paid to exit (calls worth more than puts)

What's really happening here: This trader OPENED this Risk Reversal weeks or months ago when they were bullish on EFX. Back then, they likely:

- Sold $200 puts (betting EFX stays above $200) and collected premium

- Bought $220 calls (betting EFX rallies above $220) and paid premium

- Created synthetic long exposure between $200-$220 at low/no cost

Now they're unwinding because:

- 📊 With stock at $212.45 (between the strikes), the position is slightly profitable but not spectacular

- ⏰ Only 14 days to expiration - time to take profits before theta decay accelerates

- 🎯 Q4 earnings on February 6, 2025 are 2 months away - going neutral ahead of catalyst

- ⚠️ $15M CFPB fine in January 2025 created regulatory overhang

- 💰 Stock near 52-week lows ($199.98) with limited upside to $220 in next 2 weeks

Unusual Score: 🔥🔥 EXTREMELY UNUSUAL (Z-score 5.2 for calls, 4.6 for puts) - This is massive size representing over $42M notional exposure (18,000 contracts × $212.45 × 100 = $38.2M of stock equivalent). We're talking about closing out positions larger than most retail traders' entire accounts!

Volume vs Open Interest Analysis:

- Calls: 18K volume = 100% of 18K open interest (entire position created/closed today!)

- Puts: 18K volume = 90% of 20K open interest (closing most of position)

- Vol/OI Ratio: 1.0 and 0.9 = HIGH_ACTIVITY signal (definitively closing, not rolling)

The volume MATCHING the open interest is the smoking gun - this entire position was likely established recently and is now being fully unwound. This isn't a hedge adjustment or roll - this is an EXIT.

📈 Technical Setup / Chart Check-Up

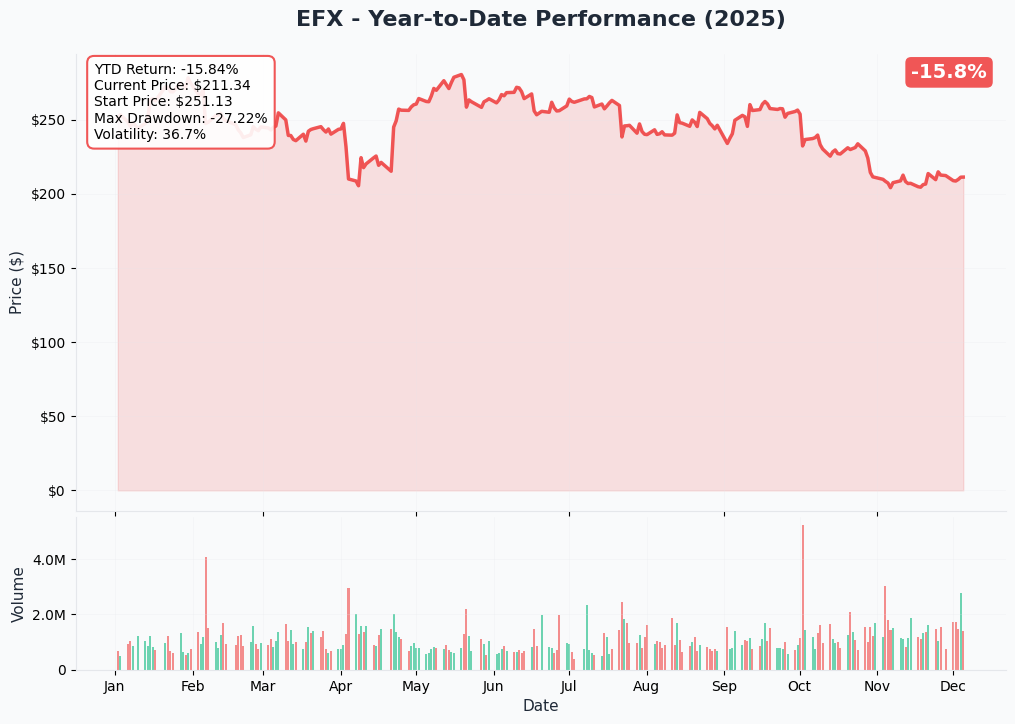

YTD Performance Chart

Equifax is having a rough year - down -12.8% since January with current price of $212.45 (started the year around $244). The chart shows a clear downtrend from the February 2025 peak of $281.07, reflecting mortgage market concerns and regulatory headwinds.

Key observations:

- 📉 Brutal selloff: Stock dropped from $281 high in February to $200 low in November (29% decline)

- 🛡️ Finding support: Currently bouncing off $200 psychological floor ($199.98 52-week low tested)

- 📊 Consolidation range: Trading $200-$215 for past 2 months with no clear direction

- ⚠️ Below key moving averages: Price underwater vs 50-day, 100-day, and 200-day MAs

- 🎢 Moderate volatility: Not as wild as tech stocks, but credit bureaus showing sector weakness

- 📈 Recovery attempt: Small bounce from November lows, but $220 resistance (exactly where calls are struck!) proving difficult

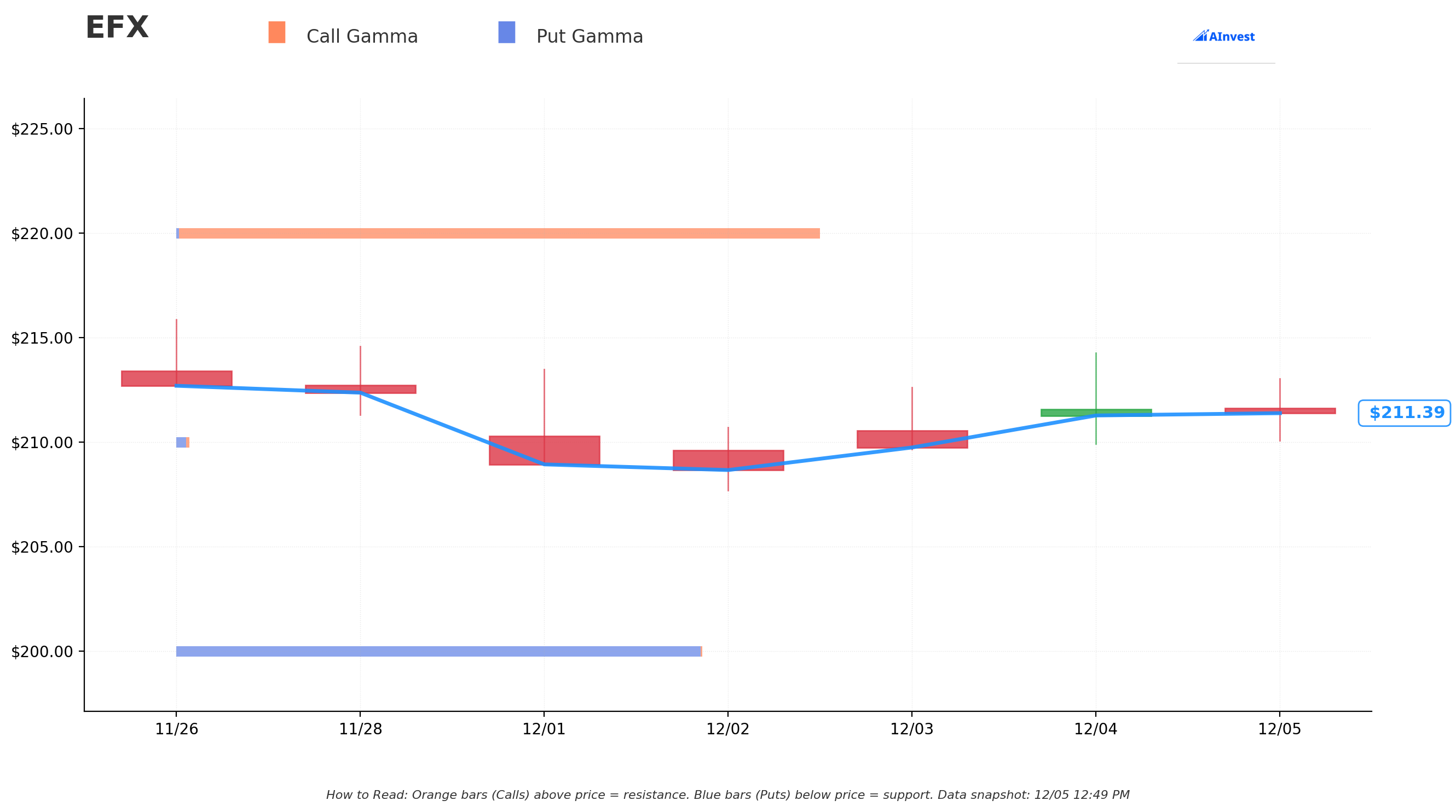

Gamma-Based Support & Resistance Analysis

Current Price: $211.50 (as of gamma calculation)

The gamma exposure map reveals critical price magnets that will govern near-term action through December 19th expiration:

🔵 Support Levels (Put Gamma Below Price):

- $210 - Immediate support with 0.195 total gamma exposure (strongest nearby floor!)

- $200 - MASSIVE structural floor with 7.938 total gamma (HUGE put gamma wall - this is THE LINE IN THE SAND)

- $195 - Secondary support at 0.034 gamma

- $190 - Extended support zone with 0.090 gamma

- $185-$180 - Deep disaster floors with minimal gamma

🟠 Resistance Levels (Call Gamma Above Price):

- $220 - CRUSHING resistance with 9.807 total gamma (STRONGEST LEVEL - exactly where calls were struck!)

- $230 - Secondary resistance at 0.111 gamma (4.7% overhead)

- $240-$250 - Extended upside targets with minimal gamma

What this means for traders: The gamma map tells the ENTIRE story of this trade! The $220 strike has absolutely MASSIVE call gamma (9.807 total) - by far the strongest resistance level. This is where dealers and market makers have huge positions that create natural selling pressure. The trader who closed this Risk Reversal KNEW they weren't getting to $220 in 14 days with that wall overhead.

On the flip side, $200 has enormous put gamma (7.938) creating a rock-solid floor. The stock tested $199.98 (52-week low) and bounced hard - that put wall held. The trader's original short puts at $200 were safe, so they're buying them back to close the position.

Notice the positioning? Stock at $211.50 is trapped in a tight $200-$220 range defined by these massive gamma walls. The Risk Reversal unwind makes PERFECT sense - with stock stuck in the middle and only 14 days left, neither the upside calls nor downside puts will hit their targets. Better to close for small profit now than risk theta decay eating the remaining value.

Net GEX Bias: Bullish (10.06 call gamma vs 8.31 put gamma) - Overall market positioning remains slightly bullish, but the stock is range-bound between powerful support ($200) and resistance ($220).

Distance Analysis:

- Current price to $220 resistance = +4.0% move needed (unlikely in 14 days given current momentum)

- Current price to $210 support = -0.7% (immediate floor nearby)

- Current price to $200 floor = -5.4% (would take major catalyst to break)

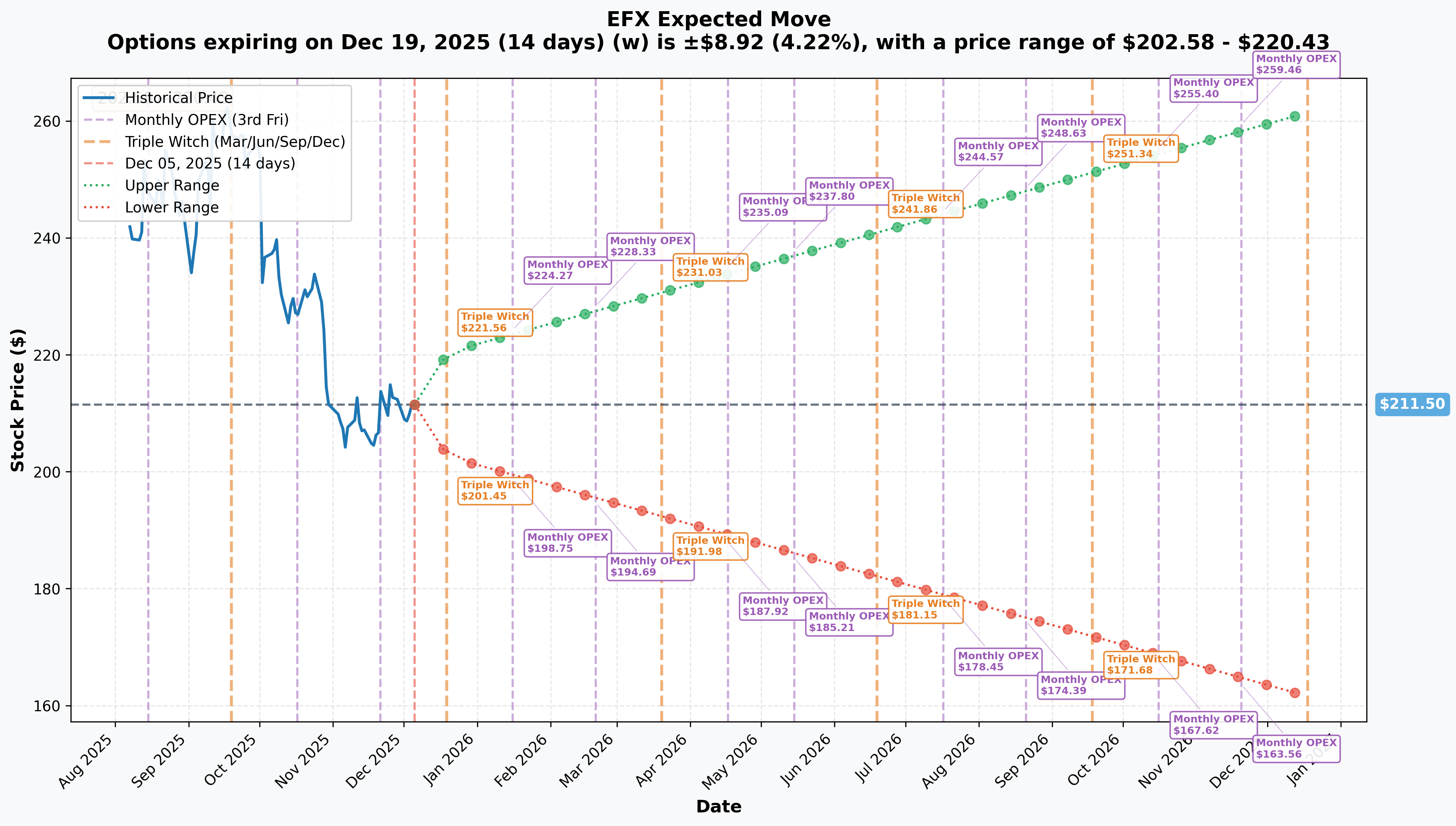

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 December 19 Triple Witch (14 days - THIS TRADE!): ±$8.92 (±4.22%) → Range: $202.58 - $220.43

- 📅 January 16 OPEX (42 days): ±$12.78 (±6.04%) → Range: $198.75 - $224.27

- 📅 February 20 OPEX (77 days): ±$16.34 (±7.73%) → Range: $194.69 - $228.33

- 📅 LEAPS (378 days - 1 year): ±$49.98 (±23.63%) → Range: $161.53 - $261.49

Translation for regular folks: The market expects EFX to move ±4.2% ($8.92) over the next 14 days through December 19th expiration. That puts the expected range at $202.58-$220.43 - notice how this PERFECTLY brackets the $200-$220 Risk Reversal strikes!

Key insight: The upper end of the implied move range ($220.43) is almost EXACTLY at the call strike ($220). This tells us the market is pricing in LOW probability of EFX breaking above $220 by December 19th. The trader who closed their calls is simply aligning with market probabilities - why hold calls with a strike at the very top of the expected range?

Similarly, the lower end ($202.58) is well ABOVE the $200 put strike, meaning the market sees very low risk of breaking that floor. The trader's short puts were never in danger, so closing them removes exposure and frees up capital.

Quarterly outlook: The February 20 OPEX implied move (±7.73%) spans $194.69-$228.33, which DOES include potential for bigger moves around Q4 earnings on February 6. This explains why the trader is exiting NOW - they don't want to hold through earnings volatility.

🎪 Catalysts

🔥 Immediate Catalysts (Already Happened)

Mastercard Fraud Prevention Partnership - December 5, 2024 (TODAY!) 🤝

Equifax and Mastercard announced a strategic partnership to combat payment fraud in Latin America:

- 💳 Integrates Kount Payment Fraud solution with Mastercard Identity and Ethoca services

- 🌎 Addresses 4.6% e-commerce fraud rates in Latin American financial institutions

- 📊 Expands Equifax's international footprint (currently 20-25% of revenue)

- ⚠️ Market reaction: Minimal - stock barely moved on announcement (suggests limited near-term revenue impact)

Cloud Migration Completion - Q4 2024 ☁️

Equifax completed its massive $3 billion cloud transformation in Q4 2024:

- 🏭 North American mainframe and data center decommissioning finished after 6-year project

- 💾 90% of revenue now runs through Equifax Cloud with enhanced AI capabilities

- 💰 Achieved $90 million in annual cost savings

- 🤖 100% of new models in Q3-Q4 2024 built using AI/ML (up from 70% in 2023)

- Impact: Long-term positive for margins, but market already digested this news

CFPB Regulatory Fine - January 17, 2025 ⚠️

CFPB fined Equifax $15 million for credit reporting errors and flawed dispute processes:

- 💸 $15M penalty for errors since October 2017

- 📋 Required to update dispute resolution processes per Fair Credit Reporting Act

- 🎯 Company claims 99.83% accuracy as of December 2024

- 🏛️ Regulatory overhang: Creates uncertainty ahead of Q4 earnings

- Stock reaction: Down 3-5% on announcement, contributing to weakness

Analyst Downgrades - Recent Weeks 📉

Several analysts cut targets due to mortgage market concerns:

- 🔻 Wolfe Research: Downgraded from Outperform to Peerperform (revised 2025 mortgage outlook)

- 🔻 Oppenheimer: Cut price target from $315 to $286 (maintained Outperform)

- 🔻 Jefferies: Reduced target from $340 to $300 (kept Buy rating)

- Consensus: Still bullish long-term, but near-term headwinds acknowledged

🚀 Upcoming Catalysts (Next 6 Months)

Q4 2024 Earnings Release - February 6, 2025 (63 DAYS AWAY!) 📊

Equifax reports Q4 2024 results on Thursday, February 6, 2025 at 6:30 AM ET:

Consensus Expectations:

- 📊 Revenue: $1.4 billion (up 8.6% YoY) vs $1.29B last year

- 💰 EPS: $2.10 (up 16% YoY) vs $1.81 last year

- 🏢 USIS Operating Revenue: $472.65M (up 10.5% YoY) - mortgage recovery signals critical

- 👔 Workforce Solutions: $611.84M (up 9.4% YoY) - verification services growth

- 📈 Verification Services: $515.01M (up 12.7% YoY) - non-mortgage growth driver

Key Metrics to Watch:

- 🏡 Mortgage Market Commentary: Management expects bottom in H2 2025, but 2025 guidance assumes ~12% decline in mortgage inquiries

- 💻 Cloud Migration ROI: First full quarter with completed North American migration - cost savings realization

- 🤖 AI Product Revenue: Contribution from 100+ new products launched in 2024

- 💵 Free Cash Flow: Target $900M+ for full year 2024 (up from $813M)

- 📊 2025 Guidance: Critical for stock direction - conservative guidance could pressure shares

Analyst Sentiment: Zacks Earnings ESP of -1.00% with Rank 4 (Sell) suggests potential for modest miss versus consensus. However, overall Street remains constructive with 14 Buy ratings and average $282 price target (32% upside from current levels).

Why This Matters for the Trade: The Risk Reversal unwind happens 63 days BEFORE earnings, suggesting the trader doesn't want to hold through the binary event. Smart move - earnings can create 8-12% moves either way, and they're already sitting on modest profits. Lock in gains, avoid volatility.

Mortgage Market Recovery Timeline - 2025-2026 🏡

Management expects mortgage market to bottom in H2 2025 with potential recovery in 2026:

- 📉 Current state: Mortgage volumes 50% below "normal" 2015-2019 pre-COVID levels

- 💰 Revenue opportunity: $1.2 billion incremental revenue when market normalizes

- 🎯 2025 outlook: Guidance assumes ~12% decline in U.S. mortgage hard credit inquiries

- 📈 2026-2027 projections: ~50% mortgage volume growth from current levels possible if Fed maintains stable/lower rates

- ⚠️ Risk: Recovery timing highly uncertain - could extend into 2027 if rates stay elevated

- Probability: 60-70% for 2026 recovery start (Fed-dependent)

Share Repurchase Program Execution - 2025-2028 💰

Equifax authorized $3 billion four-year buyback program in April 2025:

- 💵 Q2 2025: Repurchased 480,000 shares for $127M

- 🎯 Strategy: Consistently offset employee dilution with opportunistic additional buybacks

- 📊 Dividend: 28% increase announced alongside buyback (now $2.00 annually, 0.96% yield)

- 💪 Cash generation: $813M free cash flow in 2024, targeting 95%+ conversion long-term

- Impact: Supports stock price floor, demonstrates confidence in business outlook

AI Product Revenue Scaling - 2025 🤖

Equifax targeting ~150 new product launches in 2025 vs 100+ in 2024:

- 🧠 99% of global models using AI/ML as of H2 2024

- 💻 Equifax Ignite and InterConnect platforms enable deployment in days vs months

- 💰 Revenue impact: Each new product cohort showing 50% higher average revenue than 2021 baseline

- 📈 Competitive advantage: 300+ issued/pending AI patents, industry-first explainable AI

- ⏰ Timeline: Revenue realization extends through 2025-2026 (long sales cycles for enterprise)

Regulatory Timeline - Q1 2025 🏛️

CFPB Data Broker Rule comment period closes March 3, 2025:

- 📋 Proposed expansion of Fair Credit Reporting Act to cover all data brokers

- 💸 Could require significant compliance restructuring if implemented as proposed

- 🇺🇸 Trump administration shift: Expected to reduce regulatory intensity vs current CFPB stance

- ⚖️ Potential reversal: Industry expects softer approach from incoming administration

- Timeline: Final rule implementation uncertain due to political transition

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, catalysts, and the Risk Reversal unwind signal, here are scenarios through February earnings:

📈 Bull Case (30% probability)

Target: $235-$250

How we get there:

- 💪 Mortgage market shows early stabilization signs (Fed rate cuts accelerate refinancing)

- 📊 Q4 earnings BEAT expectations with revenue toward $1.45B high-end and margins expanding

- 🤖 AI product revenue contribution exceeds expectations ($150M+ in Q4)

- 💵 Strong free cash flow ($900M+) and aggressive buyback execution supports stock

- 🎯 2025 guidance surprises positively - less mortgage decline than feared (-8% vs -12% expected)

- 🏛️ Trump administration signals CFPB regulatory relief

- ✅ Verification Services non-mortgage growth accelerates to 20%+ (Government/Talent Solutions strength)

- 📈 Breakout above $220 gamma resistance triggers short squeeze to $240

Key metrics needed:

- Workforce Solutions revenue growth >12% YoY

- Gross margins expanding above 33% (proving cloud cost savings)

- Positive mortgage commentary for 2025-2026 recovery path

- No new regulatory enforcement actions

Why only 30%: Requires multiple positive catalysts aligning simultaneously. Stock already down 13% YTD with heavy overhead resistance at $220 (9.8 gamma). Analyst downgrades and mortgage headwinds create skepticism. The Risk Reversal unwind suggests even sophisticated bulls are taking profits, not adding - bearish sentiment signal.

🎯 Base Case (50% probability)

Target: $200-$220 range (CONSOLIDATION CONTINUES)

Most likely scenario:

- ✅ Solid Q4 earnings meeting consensus (~$1.4B revenue, $2.08-2.12 EPS)

- 📊 Cloud migration savings materializing ($90M run-rate) but not exceeding expectations

- 🏡 Mortgage market commentary remains cautious - bottom pushed to late 2025/early 2026

- 📈 Non-mortgage verification services growing 15-18% (good but not spectacular)

- 💰 Free cash flow solid ($850-900M range) supporting buyback and dividend

- ⚖️ Guidance in-line to slightly conservative reflecting macro uncertainty

- 🔄 Trading within $200 support (massive put gamma) and $220 resistance (huge call gamma) for months

- 😴 Volatility range-bound as market waits for mortgage recovery proof points

- 🇨🇳 International growth (20-25% of revenue) continues steady but unspectacular

This is what the Risk Reversal unwind signals: Trader expects stock to stay trapped in $200-220 range through December 19th expiration and likely beyond. With only 14 days left, neither strike ($200 puts or $220 calls) will be in-the-money, so better to close now for small profit than let theta decay eat remaining value. The $1.6M net credit received to close position suggests they made modest gains overall.

Why 50% probability: Stock showing clear technical range with defined support ($200 put wall) and resistance ($220 call wall). Fundamentals solid but not exciting enough to break out. Mortgage recovery timing uncertain. Valuation reasonable (39.75x P/E) but not cheap enough to attract aggressive buyers. Most likely outcome is consolidation until mortgage catalysts materialize in late 2025/2026.

📉 Bear Case (20% probability)

Target: $180-$200

What could go wrong:

- 😰 Q4 earnings miss or weak 2025 guidance disappoints market

- 🏡 Mortgage market deteriorates further - Fed keeps rates higher for longer, pushing recovery to 2027+

- 💸 Additional CFPB enforcement actions or expanded data broker regulations announced

- 📉 Broader credit bureau sector weakness (Experian/TransUnion competition intensifies)

- 🇨🇳 International revenue disappoints (China economic slowdown, regulatory issues)

- 💰 Free cash flow misses targets, raising questions about cloud ROI

- 🔨 Break below $200 massive gamma support triggers cascade to $190, then $180

- 📊 Workforce Solutions growth slows due to weak U.S. hiring market

Critical support levels:

- 🛡️ $210: Immediate floor with 0.195 gamma - recent consolidation low

- 🛡️ $200: MASSIVE put wall (7.938 gamma) - this is THE LINE (52-week low $199.98)

- 🛡️ $195: Secondary floor at 0.034 gamma

- 🛡️ $190: Extended support (0.090 gamma) - disaster scenario

Probability assessment: Only 20% because Equifax fundamentals remain solid (completed cloud migration, strong cash flow, oligopoly market position). The $200 level has proven rock-solid (tested in November, bounced hard). Management executing well despite mortgage headwinds. However, execution risk exists and mortgage timing uncertainty creates overhang.

Why the Risk Reversal close ISN'T bearish: The trader closed BOTH sides (calls AND puts), receiving net $1.6M credit. This signals neutrality/profit-taking, NOT bearish conviction. If they were truly bearish, they'd keep the $200 short puts (collecting premium) and only close the $220 calls. Instead, they're going flat - removing all exposure.

💡 Trading Ideas

🛡️ Conservative: Wait for Q4 Earnings Clarity

Play: Stay on sidelines until February 6th earnings provide direction

Why this works:

- ⏰ Earnings 63 days away creates major uncertainty - no catalyst to drive breakout before then

- 📊 Stock trapped in $200-$220 range with powerful gamma walls at both ends

- 💸 Institutional Risk Reversal unwind signals smart money going neutral (they know more than us!)

- 🏡 Mortgage recovery timing remains unclear - could be 2026 or 2027

- 🏛️ Regulatory overhang from CFPB fine and proposed data broker rules

- 📉 Stock down 13% YTD with multiple analyst downgrades - negative momentum

- 🎯 Better entry likely post-earnings at $200-210 if results disappoint OR $215-220 if they beat

Action plan:

- 👀 Monitor Q4 earnings on February 6, 2025 (6:30 AM ET) for revenue ($1.4B+ needed), margins, and mortgage commentary

- 📊 Watch for 2025 guidance quality - mortgage decline -8% to -10% would be positive vs -12% feared

- ✅ Need to see free cash flow $900M+ and confirmation of cloud cost savings ($90M run-rate)

- 🏡 Look for mortgage market bottom timing update (H2 2025 vs 2026 makes big difference)

- 💰 Post-earnings pullback to $205-210 would offer 8-10% margin of safety for stock entry

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid theta decay on options in range-bound stock. Get clearer picture post-earnings. Potentially enter at better prices if stock dips or wait for mortgage recovery proof.

⚖️ Balanced: Short Iron Condor - Profit from Range-Bound Action

Play: Sell iron condor capturing $200-$220 expected range through January OPEX

Structure:

- Sell $215 calls / Buy $220 calls (January 16 expiration)

- Sell $205 puts / Buy $200 puts (January 16 expiration)

Why this works:

- 📊 Stock consolidating $200-$220 for 2 months with no breakout catalyst before earnings

- 🎯 Gamma walls at $200 (support) and $220 (resistance) reinforce range

- 💰 Collect premium from selling options at edges of expected range

- ✅ Risk Reversal unwind confirms institutional expectation of continued consolidation

- 📈 Implied move for January OPEX (±6.04%) suggests $198-225 range - our strikes inside that

- ⏰ 42 days to January 16 expiration provides theta decay edge

- 🛡️ Defined risk structure ($5 wide on each side = $500 max risk per condor)

Estimated P&L (check current prices):

- 💰 Collect ~$1.00-1.50 net credit per iron condor ($100-150 premium)

- 📈 Max profit: $100-150 if EFX stays between $205-$215 at January 16

- 📉 Max loss: $400-350 if EFX breaks above $220 or below $200 (defined)

- 🎯 Breakeven: ~$203.50 and ~$216.50

- 📊 Profit zone: Stock anywhere between $205-$215 (current price $212.45 is perfect!)

- 🔥 Win probability: ~60-65% (market pricing 6% move, we're giving 2.5% cushion each side)

Entry timing:

- ✅ Enter NOW or next few days (maximize theta decay collection)

- 📊 Only if stock between $210-$215 (middle of range)

- ❌ Skip if stock near $200 or $220 (too close to short strikes)

Exit strategy:

- 💰 Close at 50-70% max profit ($50-100 gain) - don't be greedy

- ⚠️ Set alerts at $218 (upside) and $202 (downside) to manage early

- 🎯 If stock approaches $220 or $200, consider rolling strikes out in time

- ❌ Exit immediately if unusual news hits (CFPB action, major analyst downgrade, etc.)

Position sizing: Risk only 3-5% of portfolio (1-2 iron condors max for $10K account)

Risk level: Moderate (defined risk, neutral strategy) | Skill level: Intermediate

This mirrors the institutional thinking: The Risk Reversal unwind shows smart money expects range-bound action. We're doing the same thing but profiting from selling premium at the range edges rather than closing long positions.

🚀 Aggressive: Earnings Call Spread - Bet on Recovery Beat (ADVANCED!)

Play: Bull call spread betting Q4 earnings surprise drives breakout above $220

Structure:

- Buy $210 calls / Sell $230 calls (February 20 expiration - 2 weeks AFTER earnings)

Why this could work:

- 💪 Expectations LOW after analyst downgrades and YTD weakness - setup for positive surprise

- 🏡 If mortgage market shows ANY stabilization signs, stock could rip 15-20%

- 💰 $3B buyback program and strong free cash flow support upside

- 🤖 AI product revenue contribution underappreciated by Street

- ✅ Cloud migration ROI ($90M savings) dropping to bottom line in Q4

- 🎯 Average analyst target $282 (32% upside) - room to run if fundamentals deliver

- 📈 Breakout above $220 massive gamma resistance could trigger squeeze to $235-240

- ⚖️ Potential regulatory relief from Trump administration reduces downside risk

Why this could blow up (SERIOUS RISKS):

- ⏰ EARNINGS BINARY RISK: Results February 6th create massive volatility - could gap down 10% on miss

- 🏡 Mortgage recovery delayed: If management pushes bottom to 2026/2027, stock tanks

- 💸 Guidance disappointment: Conservative 2025 outlook (-12% mortgage decline) already expected - worse would crush

- 📊 $220 resistance: HUGE gamma wall (9.8 total) - sellers waiting at that level

- 😱 IV Crush: Even if stock moves to $220 post-earnings, volatility collapse could limit gains

- 🔨 Regulatory: New CFPB enforcement or bad data broker rule would create selloff

- ❌ Execution risk: Cloud savings, AI revenue, or cash flow missing targets

Estimated P&L (check prices closer to entry):

- 💰 Cost: ~$4-6 per call spread ($400-600 total cost)

- 📈 Max profit: $14-16 if EFX above $230 at Feb 20 ($1,400-1,600 gain = 200-250% ROI!)

- 📉 Max loss: $400-600 if EFX below $210 at Feb 20 (100% loss)

- 🎯 Breakeven: ~$214-216

- 📊 Stock needs to rally from $212.45 to $214+ just to breakeven (already small cushion)

- 🚀 Home run scenario: EFX rallies to $240+ on blowout earnings = near-max profit

Entry timing:

- ⏰ Enter 1-2 weeks BEFORE earnings (late January) to minimize IV crush impact

- 📊 Only if stock holding $210+ (our long strike)

- ❌ Skip if stock already above $218 (reduces risk/reward)

Exit strategy:

- 💰 Close at 100%+ gain if achieved quickly (don't get greedy!)

- 🎯 Immediately after earnings if stock gaps up 8-10% - take profits, don't wait

- ⚠️ Set stop loss at 50% loss ($200-300) if stock breaks below $205 pre-earnings

- ❌ Exit pre-earnings if major negative news hits

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can afford to lose ENTIRE premium ($400-600)

- ✅ Understand earnings create 8-12% moves either direction (coin flip!)

- ✅ Have experience trading through earnings volatility

- ✅ Accept that even correct directional bet could lose money if timing/magnitude wrong

- ✅ Monitor position actively around February 6 earnings release

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~35-40% (requires earnings beat AND breakout above resistance)

Why aggressive: You're betting AGAINST the institutional signal (Risk Reversal unwind shows smart money exiting bulls). You're fighting $220 gamma resistance. You're holding through binary earnings event. High risk, high reward - only for traders comfortable losing the entire $400-600 invested.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Mortgage market recovery timing wildly uncertain: Management expects bottom in H2 2025, but 2025 guidance assumes -12% decline in mortgage inquiries. Current volumes 50% below normal 2015-2019 levels represent $1.2 billion revenue opportunity when market normalizes. If Fed maintains higher rates through 2025-2026, recovery could push to 2027 or later. Stock has NO catalyst until mortgage inflection point visible. Each quarter of delay extends consolidation range.

-

🏛️ Regulatory overhang creates execution risk: $15M CFPB fine in January 2025 for credit reporting errors sets negative precedent. Proposed data broker rule expanding FCRA coverage could require significant compliance restructuring (comment period ends March 3, 2025). Even with Trump administration expected to soften approach, uncertainty remains. Future enforcement actions possible if 99.83% accuracy rate deteriorates. Ongoing compliance costs estimated $20-30M annually.

-

💸 Valuation offers limited margin of safety: At 39.75x forward P/E near 52-week lows, stock not "cheap" by historical standards (10-year average ~25-30x). Already down 13% YTD from $244 to $212. Street consensus $282 target (32% upside) assumes successful mortgage recovery and AI revenue scaling - both uncertain. Analyst downgrades from Wolfe, Oppenheimer, Jefferies reflect tempered expectations. Limited catalyst to drive re-rating before earnings.

-

📊 Institutional money EXITING bullish positions: The $7.2M Risk Reversal unwind (18,000 contracts!) shows sophisticated players taking profits and going neutral rather than adding to winners. When funds managing hundreds of millions choose to close $220 calls at current levels rather than hold 14 more days, it signals low conviction in near-term upside. The Z-scores (5.2 for calls, 4.6 for puts) mark this as EXTREMELY unusual activity - not normal portfolio rebalancing. Smart money is derisking.

-

🎯 Gamma ceiling at $220 prevents breakouts: Massive 9.807 total gamma at $220 strike creates mechanical selling pressure as dealers hedge exposure. This is THE strongest resistance level on the entire chain. Stock tested $220 multiple times in past 2 months and rejected each time. Would need sustained institutional buying or major positive catalyst to overcome. The Risk Reversal trader KNEW this level wouldn't break before December 19 expiration - hence the unwind.

-

💰 AI product revenue monetization timeline extends years: While 100% of new models using AI/ML sounds impressive, revenue contribution from 150 new products in 2025 won't materialize immediately. Enterprise sales cycles for credit solutions run 6-12 months. Each new product cohort showing 50% higher revenue than 2021 baseline, but off small base. Street won't reward AI investments until they show up in revenue growth (2026+ timeline).

-

🇨🇳 International growth (20-25% revenue) faces headwinds: China economic slowdown impacts Asia-Pacific operations. Latin American fraud partnership with Mastercard has minimal near-term impact. Boa Vista SCPC acquisition in Brazil (February 2023, $596M) needs to deliver ROI. International margins typically lower than U.S. business, diluting overall profitability.

-

🔨 Competition from Experian/TransUnion intensifies: Experian's $6.62B revenue ~16% larger than Equifax's $5.68B. Experian secured first major BNPL reporting arrangement with Apple Pay Later in February 2024. TransUnion acquired Monevo marketplace (April 2025) adding 150+ lender connections. Market share battles intensifying in oligopoly. Price competition could compress margins.

-

📉 Cloud migration ROI must deliver: $3 billion invested over 6 years with $90M annual savings expected. Payback period ~33 years at current run-rate - needs to accelerate significantly. If cloud doesn't enable faster product launches, better margins, or revenue growth, investment was wasted. First full quarter post-migration (Q4 2024) will be critical proof point. Execution risk remains.

-

🎢 Earnings binary event February 6th: Results could create 8-12% move either direction based on revenue ($1.4B vs $1.45B makes huge difference), margins, mortgage commentary, and 2025 guidance. Zacks ESP -1.00% suggests potential miss vs consensus. Options pricing ±7.7% implied move for February OPEX. Historical precedent shows credit bureaus can gap on guidance changes even with in-line results.

-

💔 Macro recession risk: If economy weakens in 2025, consumer credit deteriorates (pressures USIS segment), corporate hiring freezes (hurts Workforce Solutions), and mortgage market worsens further. Equifax has cyclical exposure despite oligopoly moat. Recession could extend consolidation range to $180-$220 for quarters.

🎯 The Bottom Line

Real talk: When institutions unwind $7.2 MILLION in Risk Reversals just 14 days before expiration while stock sits in the middle of the strikes, that's a LOUD signal: smart money sees no catalyst to drive movement in the near term. This wasn't a bearish exit (they closed BOTH the calls AND puts) - it was a neutral profit-taking move by traders who made their money and don't want to watch theta decay eat the remaining value.

What this trade tells us:

- 🎯 Stock expected to stay RANGE-BOUND $200-$220 through December and likely into January

- 💰 No conviction in breakout above $220 (massive gamma resistance) before earnings

- 🛡️ $200 support rock-solid (huge put gamma wall) - floor is secure

- ⏰ No major catalysts until Q4 earnings February 6th (63 days away)

- 📊 Institutional players taking chips off table rather than adding - neutral/cautious sentiment

- 💸 The $1.6M net credit they received to close suggests they made modest gains overall

This is NOT a "sell everything" signal - it's a "consolidation continues, be patient" signal.

If you own EFX:

- ✅ Hold if you're long-term investor believing in mortgage recovery (2026-2027 timeline)

- 📊 Consider trimming 20-30% if you need liquidity - stock going nowhere fast

- ⏰ Don't expect fireworks before Q4 earnings February 6th

- 🎯 If stock breaks above $220, that's NEW information - resistance turned support would be bullish

- 🛡️ Set mental stop at $198-200 (52-week low support) to protect capital if fundamentals deteriorate

- 💰 $3B buyback program and 0.96% dividend ($2.00/year) provide some downside support

If you're watching from sidelines:

- ⏰ February 6th Q4 earnings is the moment of truth - wait for that catalyst

- 🎯 Looking for confirmation of: mortgage market stabilization signals, cloud cost savings ($90M+), AI revenue contribution growing, 2025 guidance not worse than feared

- 📈 Post-earnings dip to $205-210 would be attractive entry (10% margin of safety from current)

- 🚀 Alternatively, breakout above $220 on strong results could trigger rally to $235-240 (gamma squeeze)

- 💰 Consensus target $282 (32% upside) achievable IF mortgage recovery materializes in 2026

- ⚠️ Current valuation (39.75x P/E) reasonable but not compelling - need growth inflection

If you're a premium seller (theta gang):

- 🎯 This is YOUR environment! Range-bound stocks are premium-selling paradise

- 📊 Iron condors, strangles, or credit spreads at $200-$220 range edges offer attractive risk/reward

- ✅ Gamma walls at both ends create defined battleground - dealers will defend these levels

- 💰 Collect theta decay while institutions sit on hands waiting for earnings

- ⏰ January 16 or February 20 expirations optimal (capture time decay without holding through earnings)

- 🛡️ Position size conservatively - defined risk structures only (no naked options!)

Mark your calendar - Key dates:

- 📅 December 19, 2025 - Monthly OPEX, expiration of this Risk Reversal trade

- 📅 January 16, 2026 - Monthly OPEX

- 📅 February 6, 2026 (6:30 AM ET) - Q4 2024 earnings release + conference call

- 📅 February 20, 2026 - Monthly OPEX (post-earnings)

- 📅 March 3, 2026 - CFPB data broker rule comment period closes

- 📅 Q1 2026 Earnings (Late April) - First full quarter with completed cloud migration

- 📅 Mid-2025 forward - Mortgage market expected to bottom per management

Final verdict: Equifax is a QUALITY business with oligopoly moat, completed cloud transformation, strong cash flow generation, and massive mortgage recovery optionality. But TIMING is everything - mortgage market won't bottom until late 2025 at earliest (possibly 2026-2027), and near-term catalysts are sparse. The $7.2M Risk Reversal unwind by institutions shows smart money is NEUTRAL, not bullish OR bearish. Stock likely consolidates $200-$220 for months until earnings or mortgage data provides direction.

Be patient. Let the trade come to you. This isn't a "rush in" setup - it's a "wait for clarity" situation. The credit bureau business will still be a duopoly/oligopoly in 6 months, and you'll have much better information post-Q4 earnings about mortgage recovery timing, cloud ROI, and AI revenue contribution.

Sometimes the best trade is NO trade. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. The Risk Reversal unwind represents one institutional trader's positioning which may be part of complex portfolio hedging strategies not applicable to retail traders. Past performance doesn't guarantee future results. Always do your own research and consider consulting a licensed financial advisor before trading. The Z-scores (5.2 and 4.6) reflect this specific trade's size relative to recent EFX history - they do not imply the trade will be profitable or predictive of future price movement.

About Equifax Inc.: Equifax is one of the leading credit bureaus in the United States (alongside Experian and TransUnion), providing credit reports and histories while offering workforce solutions including income verification and HR services. With a market cap of $25.86 billion in the Consumer Credit Reporting industry, approximately 40% of revenue stems from workforce solutions with 20-25% from international operations.