💎 ESTC Massive $1.3M Call Bet - Institutional Long Building Into March! 🚀

📅 December 10, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $1.3 MILLION on ESTC calls at 11:46:01 this morning! This aggressive bet bought 2,500 contracts of $85 strike calls expiring March 20th - positioning for a massive 12%+ rally from the current $75.85 price over the next 100 days. With ESTC down 28% since December 2024 despite delivering four consecutive earnings beats and signing a five-year AWS partnership, smart money appears to be loading the boat ahead of Q3 FY2026 earnings on February 26th. Translation: Institutional investors are betting on a major reversal in this beaten-down AI/search infrastructure play!

📊 Company Overview

Elastic N.V. (ESTC) is a global leader in search, observability, and security solutions powering enterprise AI and data analytics:

- Market Cap: $7.87 Billion

- Industry: Prepackaged Software Services / Enterprise Search & Observability

- Current Price: $75.85

- 52-Week Range: $68.10 - $118.84

- Primary Business: AI-powered search (vector + keyword), observability platforms, cloud security/SIEM, elastic stack infrastructure

- Key Products: Elasticsearch, Elastic Cloud, Elastic AI Assistant, Elastic Inference Service

💰 The Option Flow Breakdown

The Tape (December 10, 2025 @ 11:46:01):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:46:01 | ESTC | ASK | BUY | CALL $85 | 2026-03-20 | $1.3M | $85 | 2,500 | 152 | 2,500 | $75.85 | $5.00 |

🤓 What This Actually Means

This is an aggressive bullish directional bet with serious conviction! Here's what went down:

- 💸 Hefty premium paid: $1.3M ($5.00 per contract × 2,500 contracts)

- 🎯 Out-of-the-money strike: $85 represents 12.1% upside from current $75.85 price

- ⏰ Strategic timing: 100 days to expiration perfectly captures Q3 FY2026 earnings (Feb 26), continued GenAI adoption traction, and MI350-series product launches

- 📊 Meaningful size: 2,500 contracts represents 250,000 shares worth ~$19M notional exposure

- 🏦 Opening position: Only 152 existing OI means this trade represents 94% of ALL open interest at this strike - someone just CREATED this entire position

What's really happening here: This trader is making a PURE directional bet that ESTC rebounds sharply to $85+ by March 20th. They paid $5.00 per share for the March 20 $85 calls, which only profit if ESTC rallies above $90 (breakeven). This is NOT a hedge - this is a leveraged bet that the 28% YTD decline has created a massive opportunity. With ESTC trading at $75.85 after falling from $103.81 in December 2024, they're betting the Q3 earnings catalyst on February 26th will reverse the trend and drive the stock back toward $90-100 levels.

Unusual Score: 🔥 SIGNIFICANT (2,500 contracts vs 152 existing OI) - This is position-building by an institution with strong conviction. The fact they're buying OUT-OF-THE-MONEY calls (not protective puts) shows they expect a material rally, not just modest stabilization.

📈 Technical Setup / Chart Check-Up

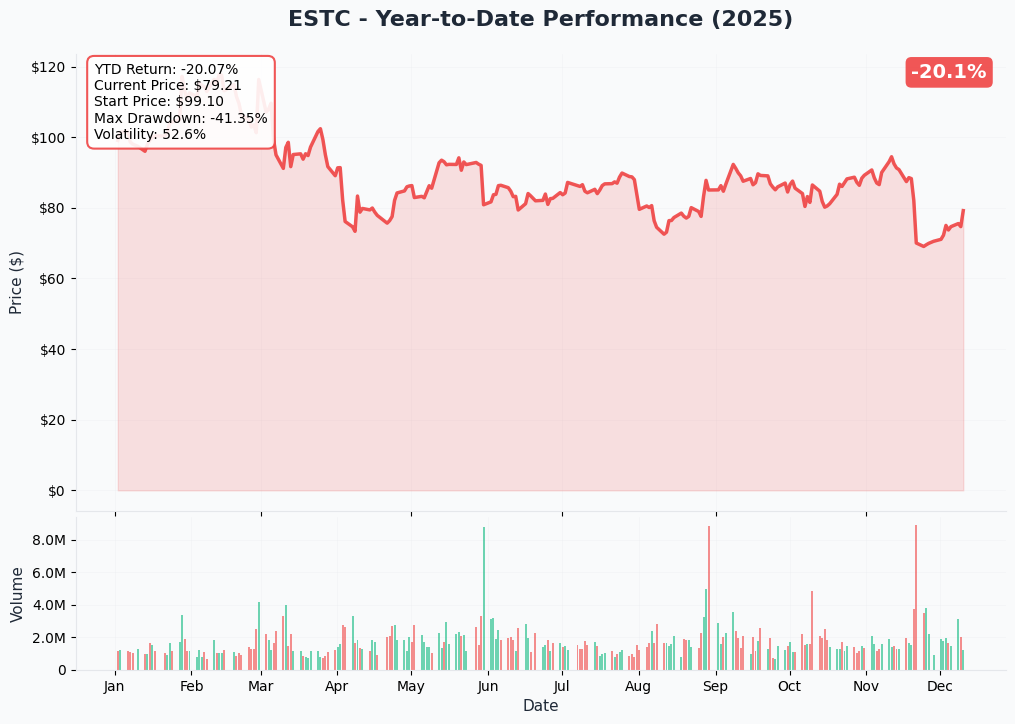

YTD Performance Chart

ESTC is down -28.05% from December 2024 levels with current price of $75.85 (started December 2024 at $103.81). The chart tells a brutal correction story - despite strong fundamental execution (four consecutive earnings beats, raised guidance), the stock has been demolished along with other enterprise software names.

Key observations:

- 📉 Severe correction: Down from near-$119 highs to $68 lows - a 43% peak-to-trough drawdown

- 🎯 Critical support holding: Stock bounced off $68.10 52-week lows, now trading +11.4% off bottom

- 📊 Volume capitulation: Heavy selling volume in October-November suggests potential washout

- 💪 Relative strength emerging: Outperforming broader software sector in recent weeks

- ⚠️ Key resistance overhead: $85 (this call strike!) represents major technical hurdle - former support turned resistance

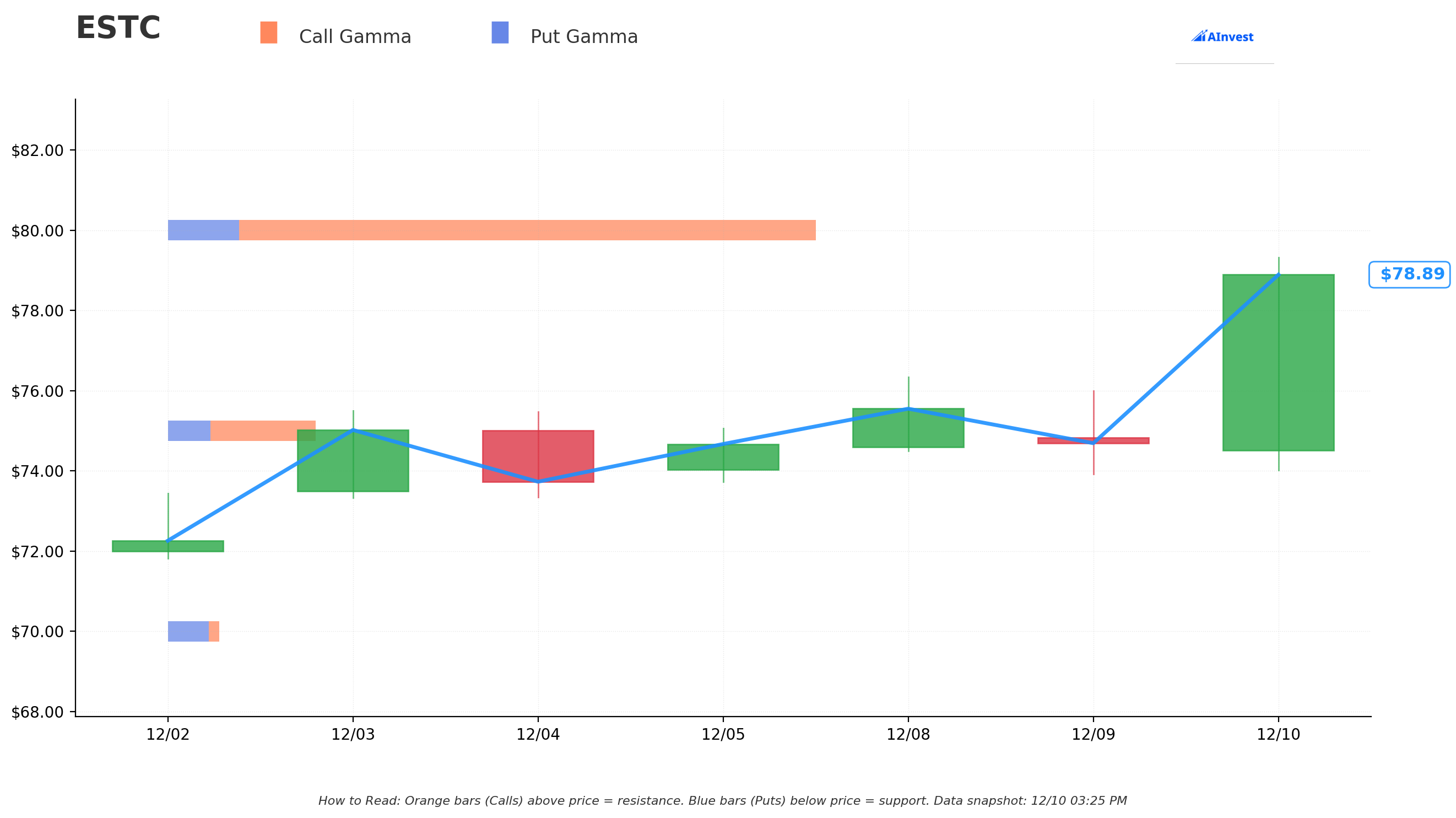

Gamma-Based Support & Resistance Analysis

Current Price: $78.88 (gamma data snapshot)

The gamma exposure map reveals critical price magnets that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $75 - STRONGEST SUPPORT with 0.63B total gamma exposure (call 0.45B, put 0.18B, net +0.26B bullish)

- Distance: 4.9% below current price

- This is the LINE IN THE SAND - break below $75 opens door to $70

- $70 - Secondary support at 0.22B total gamma (put-heavy: 0.17B puts vs 0.04B calls)

- Distance: 11.3% below current

- Deep value zone if reached

- $65 - Disaster floor with 0.50B gamma (heavily put-dominated: 0.50B puts vs 0.003B calls)

- Distance: 17.6% below current

- Would represent 45% decline from December 2024 highs

🟠 Resistance Levels (Call Gamma Above Price):

- $80 - IMMEDIATE CEILING with 2.81B gamma (STRONGEST LEVEL - call-heavy: 2.51B calls vs 0.30B puts)

- Distance: 1.4% overhead

- THIS IS THE KEY BREAKOUT LEVEL - dealers will resist moves above aggressively

- $85 - MAJOR RESISTANCE with 0.69B total gamma (call 0.37B, put 0.32B) - EXACTLY WHERE THIS TRADE IS STRUCK!

- Distance: 7.8% above current

- Former support from October now turned resistance

- Breaking above $85 opens path to $90+

- $90 - Extended resistance at 0.25B gamma (call-heavy: 0.21B calls)

- Distance: 14.1% rally required

- Represents mid-range of recent trading

What this means for traders: ESTC is in a critical battle zone. The massive $80 resistance (2.81B gamma - largest single level) creates a HUGE barrier just 1.4% overhead. Market makers holding enormous positions here will systematically sell into rallies. The call buyer needs ESTC to not only break $80 but also clear $85 (the strike they chose) for the trade to work.

Notice the strategic strike selection? The call buyer chose $85 where there's 0.69B gamma - this was former support in October before the selloff. They're betting that earnings will propel the stock back through this technical level, triggering a cascade of short covering and momentum buying toward $90-95.

Net GEX Bias: Bullish overall (4.23B call gamma vs 1.69B put gamma) - Positioning suggests market expects upside resolution, supporting the bull thesis.

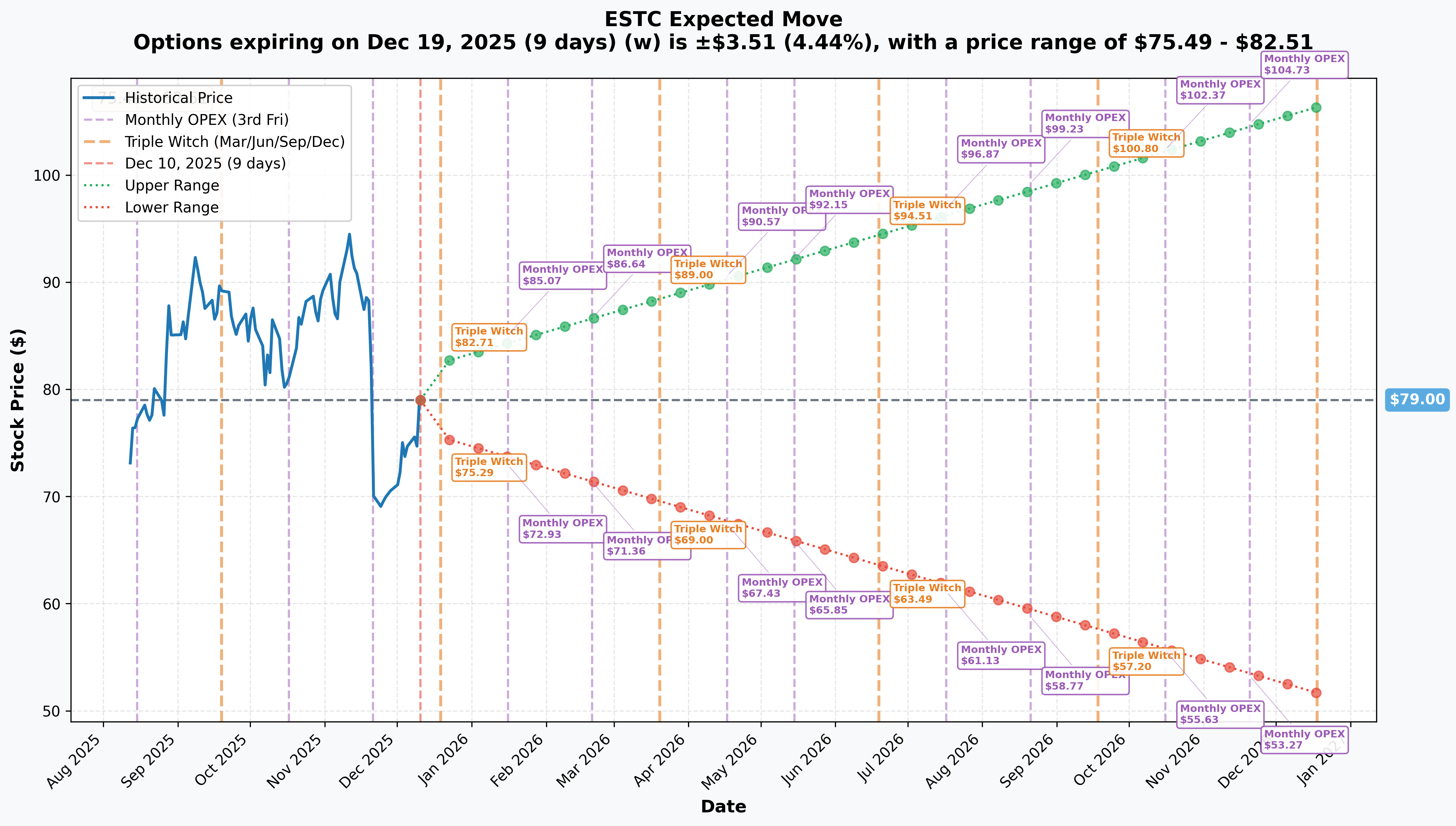

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 December Triple Witch (Dec 19 - 9 days): ±$3.51 (±4.44%) → Range: $75.49 - $82.51

- 📅 January OPEX (Jan 16 - 37 days): ±$7.70 (±9.73%) → Range: $71.30 - $86.70

- 📅 February OPEX (Feb 20 - 71 days): ±$10.53 (±13.28%) → Range: $68.47 - $89.53

- 📅 March Triple Witch (Mar 20 - 100 days - THIS TRADE!): ±$13.50 (±17.04%) → Range: $65.50 - $92.50

- 📅 Yearly LEAPS (Dec 18, 2026 - 373 days): ±$27.37 (±34.65%) → Range: $51.63 - $106.37

Translation for regular folks: Options traders are pricing in a 4.4% move ($3.51) through December OPEX, but a larger 17% move ($13.50) through March which includes the critical Q3 earnings on February 26th. The March upper range of $92.50 shows the market thinks there's a real possibility ESTC could rally to $90+ over the next 100 days.

Key insight: The call buyer's $85 strike falls comfortably within the implied range ($65.50-$92.50), suggesting the market is assigning reasonable probability to this outcome. However, with breakeven at $90, they need the stock to hit the UPPER END of the range to profit.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Barclays 23rd Annual Global Technology Conference - TODAY! (December 10, 2025) 📊

ESTC presents at the Barclays conference at 8:05 AM PT / 11:05 AM ET. This is the FIRST major public appearance since the stock's brutal selloff. Key items to watch:

- 🎯 GenAI customer growth update: Current 1,750+ Elastic Cloud customers using GenAI - looking for acceleration

- 💰 Q3 earnings preview: Any commentary on pipeline, deal activity, or quarterly trends ahead of Feb 26 earnings

- 🤝 AWS partnership progress: Five-year strategic collaboration signed in May - first real update on traction

- 📊 Competitive positioning: Management's response to valuation compression vs peers

- 🚀 Product roadmap: Updates on Elastic Inference Service adoption, Agent Builder traction, Jina AI integration

Why this matters for the call trade: If management sounds confident about Q3 trajectory and GenAI momentum, it could spark a near-term rally and validate the bullish positioning.

🚀 Near-Term Catalysts (Q1 2026)

Q3 Fiscal 2026 Earnings - February 26, 2026 (78 DAYS AWAY!) 📊

ESTC reports fiscal Q3 results on Wednesday, February 26, 2026 after market close. This is THE primary catalyst driving this call bet. Management guidance and consensus expectations:

- 📊 Revenue: $396-398M (company guidance) representing 14% YoY growth

- 💰 Non-GAAP EPS: $0.41-0.43 (company guidance)

- 🤖 GenAI Metrics to Watch:

- Customer count using GenAI solutions (baseline: 1,750+ as of Q3 FY2025)

- GenAI ACV commitments (240+ customers spending $100K+ annually on GenAI)

- Sequential acceleration in GenAI revenue contribution

- 💻 Elastic Cloud Revenue: Continued growth trajectory (was $180M in Q3 FY2025, up 26% YoY)

- 📈 Key Metrics:

- Total subscription customers (~21,350 baseline)

- $100K+ ACV customers (1,420+ baseline)

- Net expansion rate (112% baseline - looking for improvement)

- Operating margin expansion (17% non-GAAP baseline)

- Free cash flow margin (26% baseline)

Beat potential: ESTC has beaten both revenue and EPS consensus for FOUR consecutive quarters. Last quarter delivered $423M revenue vs $397M consensus (+6.5% beat) and $0.64 EPS vs $0.42 consensus (+52% beat). The company has a track record of conservative guidance and strong execution.

Upside surprise scenario: GenAI customer count accelerates to 2,000+, cloud revenue growth reaccelerates to 30%+, operating margins expand to 18-19%, and FY2026 guidance raised meaningfully. This could drive the stock to $85-90 quickly.

Downside risk: Any deceleration in GenAI momentum, weaker cloud growth, conservative Q4 guidance, or macro headwinds impacting enterprise software spending. Given the 28% YTD decline, much negativity already priced in, but another disappointment could test $70 support.

AWS Strategic Partnership Traction (Ongoing through Q1 2026) 🤝

Elastic's five-year AWS Strategic Collaboration Agreement announced May 28, 2025 represents a transformative catalyst:

- 🏭 Comprehensive partnership: Joint product integrations including Elastic AI Assistant, Attack Discovery, and Automatic Migration with Amazon Bedrock

- 🎯 Focus on regulated industries: Financial services, healthcare, government requiring robust data protection

- 💰 Revenue opportunity: Multi-year agreement could drive material revenue contribution

- 🏆 Validation: Builds on Elastic being named AWS Global Generative AI Infrastructure and Data Partner of the Year (December 2024)

- 🚀 Agentic AI Specialization: Elastic achieved AWS Agentic AI Specialization in December 2025 - joint go-to-market launching early 2026

Why this matters: The AWS partnership de-risks ESTC's competitive position against cloud giants. If joint wins materialize in Q3/Q4, it validates the thesis that ESTC is a strategic partner (not competitor) to hyperscalers.

Jina AI Acquisition Integration (Completed October 9, 2025) 🧠

Elastic completed acquisition of Jina AI to enhance vector search, RAG, and context engineering:

- 🔬 Technology: Multimodal and multilingual dense embeddings, advanced rerankers, specialized small language models

- 💻 Integration: Jina AI models available via Elastic Inference Service and Hugging Face

- 🎯 Use case expansion: Better support for GenAI applications requiring sophisticated embedding models

- 📈 Cross-sell opportunity: Existing ESTC customers can enhance applications with Jina AI capabilities

Early revenue impact expected in Q3/Q4 FY2026 - looking for management commentary on adoption.

📊 Product Momentum (Q4 2025 - Q1 2026)

Elastic Inference Service (EIS) Traction 🚀

Launched October 9, 2025, EIS provides GPU-accelerated inference-as-a-service:

- 💪 Infrastructure: NVIDIA GPUs with native Elasticsearch integration

- 🎯 Target market: Semantic search, vector search, and GenAI workflows

- 💰 Revenue model: Consumption-based pricing creates recurring revenue stream

- 📊 Competitive positioning: Competes with Pinecone, MongoDB Atlas Vector Search, and cloud-native vector DBs

Key metric: Looking for disclosure on EIS adoption rate and revenue contribution in Q3 earnings.

Agent Builder Adoption (Launched October 21, 2025) 🤖

Agent Builder provides native conversational interface:

- 💬 Functionality: Query data using natural language via ES|QL

- 🛠️ Customization: Create custom tools and agents

- 🔗 Integration: Model Context Protocol (MCP) and agent-to-agent (A2A) communication

- 🎯 Market: Democratizes data access for non-technical users - expands TAM

Early enterprise feedback critical - this could be major differentiator vs competitors.

ES|QL Platform Momentum 📊

ES|QL (Elasticsearch Query Language) achieving strong adoption:

- 📈 Current usage: Over 10,000 clusters using ES|QL weekly

- 🚀 New features: LOOKUP JOIN and Cross-Cluster Search (CCS) for petabyte-scale environments

- 💪 Performance: Significant query optimization for large datasets

- 🎯 Stickiness: Advanced query capabilities create switching costs

This is a "silent killer" feature - existing customers deepening usage increases NRR and reduces churn.

🏆 Market Position Catalysts

Platform Consolidation Wins (Ongoing) 💼

Elastic positioned as Visionary in 2025 Gartner Magic Quadrant for SIEM:

- 🎯 Displacement opportunity: Legacy SIEM tools (Splunk, legacy APM solutions) ripe for replacement

- 💰 Deal sizes: Recent seven-figure deals signal enterprise traction (automotive industry GenAI deal)

- 📊 Unified platform value: Single platform for search, security, and observability vs point solutions

- 🏢 Target customers: 1,420+ customers already spending $100K+ ACV - upsell opportunity

Forrester Wave Leader Recognition Impact (Q4 2025-Q1 2026) 🏆

Named Leader in Forrester Wave: Cognitive Search Platforms, Q4 2025:

- 🎖️ Third-party validation: Analysts recognize ESTC's leadership position

- 🔓 Open source renaissance: Return to open source model expected to accelerate innovation and developer adoption

- 📈 Market visibility: Potential new customer acquisitions from increased awareness

- 🎯 Enterprise credibility: Helps win competitive evaluations against MongoDB, Pinecone

⚠️ Risk Catalysts (Headwinds)

Competitive Pressure Intensifying 🥊

- Cloud Giants: AWS, Azure, Google Cloud native services eroding market share potential

- SIEM Competition: CrowdStrike gaining significant SIEM traction; Splunk (Cisco-owned) defending turf

- Vector DB Specialists: Pinecone, Weaviate offering purpose-built solutions

- Performance challenges: Redis demonstrating 18x faster vector search in some benchmarks vs OpenSearch/Elasticsearch

Macro Software Spending Headwinds 📉

- Enterprise budget constraints: IT spending growth decelerating in 2026

- Deal cycle elongation: Enterprises taking longer to close new contracts

- Federal government uncertainty: Potential budget cuts impacting public sector deals

- Cloud optimization: Customers reducing cloud spend impacting consumption revenue

Valuation Re-Rating Risk 📊

- Trading at 22% discount to infrastructure software peers (forward P/S ~5.5x)

- Revenue growth decelerating from 20%+ in FY2024 to 16% currently

- GAAP profitability still elusive despite strong non-GAAP margins

- If market continues to de-rate high-growth software, ESTC could compress further to 4.5-5.0x P/S (implies $65-70 price)

Leadership Transition Uncertainty 👔

- CFO/COO Janesh Moorjani departure (December 13, 2024): Interim CFO Eric Prengel appointed

- Near-term execution risk during transition period

- Investor confidence dependent on smooth handoff

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through March 20th expiration:

📈 Bull Case (35% probability)

Target: $90-$100

How we get there:

- 💪 Q3 earnings CRUSH: Revenue $400M+ (vs $396-398M guidance), EPS $0.50+ (vs $0.41-0.43 guidance)

- 🚀 GenAI acceleration: Customer count hits 2,000+, GenAI revenue contributing 25%+ of total

- 🤝 AWS partnership wins: Multiple seven-figure joint deals announced, validates strategic value

- 📊 Operating leverage emerges: Non-GAAP margins expand to 18-19%, FCF margin hits 28-30%

- 🎯 Competitive wins disclosed: Major Splunk/Datadog displacements, market share gains in SIEM/observability

- 🏆 Product traction: EIS and Agent Builder showing strong adoption, expanding TAM

- 💰 FY2026 guidance raised: Full-year revenue guidance increased to $1.73-1.74B (vs $1.715-1.721B)

- 📈 Technical breakout: Clear $80 resistance, then $85, momentum carries to $90-95 as shorts cover

Key metrics needed:

- Elastic Cloud revenue growth reaccelerating to 28-30% YoY

- Net expansion rate improving to 115%+

- GenAI ACV commitments doubling QoQ

- New customer acquisition accelerating (not just expansion)

Call P&L in Bull Case:

- Stock at $95 on March 20: Calls worth $10.00, profit = $5.00/share × 2,500 = $1.25M gain (96% ROI!)

- Stock at $100 on March 20: Calls worth $15.00, profit = $10.00/share × 2,500 = $2.5M gain (192% ROI!!)

Probability assessment: 35% because it requires strong execution AND market re-rating. The pieces are in place (AWS partnership, GenAI momentum, product launches), but needs Q3 earnings to validate. Gamma resistance at $80-85 creates technical hurdles.

🎯 Base Case (45% probability)

Target: $78-$88 range (MODEST RECOVERY)

Most likely scenario:

- ✅ Solid Q3 earnings: Meets/slightly beats guidance ($398-400M revenue, $0.43-0.45 EPS)

- 📊 GenAI steady progress: Customer count grows to 1,850-1,900, no fireworks but healthy

- 💼 AWS partnership progressing: Early wins disclosed, pipeline building, but revenue impact still 6+ months out

- ⚖️ Guidance conservative: FY2026 reiterated or modest raise, Q4 guided in-line with seasonality

- 🤖 Product adoption solid: EIS/Agent Builder gaining traction but not explosive

- 📈 Stock consolidates higher: Breaks through $80 resistance post-earnings, trades $82-88 range

- 💤 Volatility normalizes: Trading settles in new range, waiting for Q4 earnings and FY2027 outlook

This is the "call buyer breaks even" scenario: Stock rallies to $85-88, calls worth $3-8 at expiration, minimal profit but thesis validated. The strategic positioning was correct even if magnitude falls short.

Call P&L in Base Case:

- Stock at $88 on March 20: Calls worth $3.00, loss = -$2.00/share × 2,500 = -$500K (38% loss)

- Stock at $90 on March 20: Calls worth $5.00, breakeven = $0/share × 2,500 = $0

- Stock at $85 on March 20: Calls worth $0 (at-the-money), loss = -$5.00/share × 2,500 = -$1.25M (96% loss)

Why 45% probability: Stock technically oversold after 28% decline, fundamentals solid (four consecutive beats, raised guidance, AWS partnership), and valuation compressed vs peers. Recovery likely but magnitude uncertain. Most institutions will wait for Q3 confirmation before aggressive repositioning.

📉 Bear Case (20% probability)

Target: $65-$75 (TEST 52-WEEK LOWS)

What could go wrong:

- 😰 Q3 earnings disappoint: Revenue misses guidance, GenAI growth decelerates, cloud revenue slows

- 🚨 Guidance cut: Management reduces FY2026 outlook citing macro headwinds, elongated sales cycles

- 💔 AWS partnership underwhelms: Limited near-term revenue impact disclosed, partnership progressing slower than expected

- 🥊 Competitive losses: MongoDB/Pinecone/Datadog winning key competitive deals, market share pressures

- 💸 Software sector selloff: Broader enterprise software multiple compression (Datadog, MongoDB, Snowflake weakness)

- 📉 Operating deleverage: Margins compress due to S&M investments, GenAI customer acquisition costs rising

- 🔨 Technical breakdown: Fails to break $80, consolidates $72-78, then breaks below $75 support triggering cascade to $68-70

- 🤔 Leadership uncertainty: CFO transition creates execution concerns, investor confidence shaken

Critical support levels:

- 🛡️ $75: Major gamma support (0.63B) - current battleground, MUST HOLD

- 🛡️ $70: Secondary floor (0.22B gamma) - deep value buyers likely emerge

- 🛡️ $68: 52-week low - psychological support

- 🛡️ $65: Disaster scenario (0.50B gamma) - would trigger major capitulation

Call P&L in Bear Case:

- Stock at $75 on March 20: Calls expire worthless, loss = -$5.00/share × 2,500 = -$1.3M (100% loss)

- Stock at $70 on March 20: Calls expire worthless, loss = -$5.00/share × 2,500 = -$1.3M (100% loss)

- Stock at $82 on March 20: Calls expire worthless (below breakeven), loss = -$5.00/share × 2,500 = -$1.3M (100% loss)

Probability assessment: Only 20% because fundamentals remain solid (consistent beats, strong FCF, product momentum), valuation already compressed 22% vs peers, and much negativity priced in after 28% decline. Would require multiple negative catalysts AND continued software sector weakness.

💡 Trading Ideas

🛡️ Conservative: Wait for Q3 Earnings Clarity

Play: Stay on sidelines until after February 26th earnings volatility

Why this works:

- ⏰ 78 days until catalyst: Q3 earnings on Feb 26 is THE make-or-break event - too early to position now

- 💸 Time decay risk: Paying $5.00 for $85 calls means losing $0.05/day to theta through expiration

- 📊 Uncertainty premium: Current IV elevated at ~35-40%, options expensive pre-earnings

- 🎯 Better entry post-earnings: If stock rallies to $85+ on strong Q3, can chase momentum with shorter-dated calls (April/May)

- 📉 Downside protection: If earnings disappoint, avoid catching falling knife from $75 to $65

- 🤔 Barclays conference today: Wait to hear management tone before committing capital

Action plan:

- 👀 Watch Barclays presentation (Dec 10): Listen for Q3 pipeline commentary, GenAI momentum, AWS traction

- 📊 Monitor technical levels: $75 support holding = bullish, break below = danger

- ⏰ Mark calendar for Feb 26: Review earnings results, guidance, and GenAI metrics

- 🎯 Post-earnings entry: If beats and guides up, buy April/May $85-90 calls with better risk/reward

- ✅ Stock entry alternative: If pulls back to $70-72 post-earnings, consider shares vs options

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential loss if thesis doesn't play out. Get better entry if earnings validate bull case.

⚖️ Balanced: Mini Call Spread (Copy The Trade With Defined Risk)

Play: Replicate the bullish positioning but with defined risk via call spread

Structure: Buy March 20 $80 calls, Sell March 20 $90 calls

Why this works:

- 📊 Defined risk spread: $10 wide = $1,000 max risk per spread, capped max loss

- 🎯 Better risk/reward than naked calls: Pay ~$2.50-3.00 net debit vs $5.00 for naked $85 calls

- 💰 Similar upside: Profit if ESTC rallies to $85-90 range (same thesis as institutional trade)

- 🛡️ Reduced theta burn: Selling $90 call offsets time decay from long $80 call

- ⏰ 100 days to work: Enough time for Q3 earnings catalyst (Feb 26) and follow-through

- 🤝 Aligned with gamma levels: $80 is major resistance, $90 is extended target - captures range

Estimated P&L:

- 💰 Pay ~$2.50-3.00 net debit per spread (vs $5.00 for naked $85 calls)

- 📈 Max profit: $7.00-7.50 if ESTC above $90 at March expiration

- 📉 Max loss: $2.50-3.00 if ESTC below $80 (defined and limited)

- 🎯 Breakeven: ~$82.50-83.00

- 📊 Risk/Reward: ~1:2.5 which is attractive for defined-risk bullish play

Entry timing:

- ⏰ After Barclays conference: Wait for management commentary today before entering

- 🎯 Ideal entry: Stock pullback to $74-75 provides better entry on spread

- ❌ Skip if: Stock already above $82 (reduces spread profitability)

Position sizing: Risk only 3-5% of portfolio (this is directional speculation)

Exit strategy:

- 🎯 Take profits: If ESTC hits $88-90 before earnings, close at 60-70% max profit

- 📊 Post-earnings adjustment: If rallies to $85+ on Feb 26, consider rolling up to $85/$95 spread

- ⚠️ Stop loss: If breaks below $72, consider exiting to preserve capital

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

🚀 Aggressive: Replicate The Institutional Trade (ADVANCED ONLY!)

Play: Buy March 20 $85 calls - EXACT same trade as the institution

Structure: Buy ESTC March 20, 2026 $85 calls

Why this could work:

- 🏦 Following smart money: Institution just deployed $1.3M in this EXACT trade - they have info edge

- 💥 Massive upside leverage: Stock to $100 = 200%+ ROI on calls vs 32% on shares

- 🎯 Strike makes sense: $85 was former support, now resistance - reclaiming signals trend reversal

- 📊 Earnings catalyst sized perfectly: 100 days captures Q3 (Feb 26), AWS traction, product momentum

- 🚀 Oversold setup: 28% YTD decline despite strong fundamentals creates asymmetric opportunity

- 💪 Gamma support: Strong $75 floor limits downside, while $80-85 breakout opens path to $95+

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE WITH HIGH BREAKEVEN: Costs $5.00, needs stock at $90+ to profit (18.8% rally required!)

- ⏰ MASSIVE TIME DECAY: Theta burns -$0.05-0.06/day, losing $150-180/day per 100 contracts

- 😱 BINARY EARNINGS RISK: If Q3 disappoints Feb 26, stock could gap to $65-70, calls worthless overnight

- 📊 Out-of-the-money risk: Stock at $82 at expiration = 100% loss despite 8% rally!

- 🎢 Need TWO things to go right: (1) Q3 earnings beat + strong guidance, AND (2) stock breaks $80-85 resistance

- ⚠️ Gamma resistance brutal: $80 level has 2.81B gamma - dealers will fight breakout attempts

Estimated P&L:

- 💰 Cost: $5.00 per contract ($500 per contract, $50,000 per 100 contracts)

- 📈 Profit scenario: Stock at $95 = calls worth $10, profit $5/share (100% ROI)

- 🚀 Home run: Stock at $105 = calls worth $20, profit $15/share (300% ROI!)

- 📉 Breakeven: Stock at $90 = calls worth $5 (0% return)

- 💀 Total loss: Stock below $85 = calls expire worthless (-100% loss)

Breakeven analysis:

- Need ESTC to rally from $75.85 to $90.00 = +18.8% gain required

- Time available: 100 days = need +0.19% per day compounded

- Earnings catalyst can provide 15-20% move in single day, but need follow-through

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have 6-figure account minimum and can afford to lose ENTIRE premium

- ✅ Understand you're betting on >18% rally in 100 days through major resistance

- ✅ Can monitor daily and willing to cut losses if thesis breaks (stop at -30-50%)

- ✅ Have traded ESTC before and understand its volatility patterns

- ✅ Accept binary risk: Earnings on Feb 26 could make or break entire position

- ⏰ Plan to take partial profits: If hits $88-90 pre-earnings, lock in 60-80% of position

Position sizing (if doing this):

- 💰 Risk ONLY 2-3% of total portfolio - this is pure speculation

- 🎯 Start with 10-25% of intended position - add after Barclays conference if bullish

- 📊 Consider scaling: Buy 1/3 now, 1/3 mid-January, 1/3 early February to average in

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~30-35% (needs everything to go right)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q3 earnings in 78 days creates binary risk: Results February 26th after close will determine trade outcome. Stock could gap 15-20% either direction based on revenue ($396-398M), GenAI metrics (2,000+ customers needed), and FY2026 guidance quality. Historical volatility suggests ESTC can move violently on earnings - last four quarters averaged 8-12% post-earnings moves. These $85 calls are 100% dependent on Q3 beat + guidance raise.

-

💸 Already down 28% YTD - more downside possible: Stock fell from $103.81 in December 2024 to $75.85 today despite BEATING earnings four straight quarters and RAISING guidance. This reflects broader software multiple compression, not ESTC-specific issues. However, if software sector continues to de-rate (Datadog, MongoDB, Snowflake weakness), ESTC could test $68-70 52-week lows again. The call buyer is betting the worst is over - but what if it's not?

-

🥊 Competitive threats intensifying across all fronts:

- Vector search: Pinecone, Weaviate purpose-built for GenAI; MongoDB Atlas Search gaining traction

- SIEM/Security: CrowdStrike aggressively expanding SIEM; Splunk (Cisco) defending turf

- Observability: Datadog dominant in cloud-native; New Relic, Dynatrace well-entrenched

- Performance: Redis benchmarks showing 18x faster vector search than Elasticsearch/OpenSearch

- Cloud giants: AWS, Azure, Google Cloud native services eating market share

- ESTC needs to PROVE differentiation through unified platform value prop - if customers choose best-of-breed point solutions, growth thesis breaks

-

📊 Valuation discount may reflect legitimate concerns: Trading at 22% discount to infrastructure software peers (forward P/S ~5.5x vs 7.0x peer average) despite solid fundamentals. Market may be pricing in: (1) GAAP profitability concerns (still negative operating income), (2) slowing growth (16% vs 20%+ historically), (3) execution risk in GenAI monetization, (4) CFO transition uncertainty. If concerns persist, multiple could compress FURTHER to 4.5-5.0x (implies $65-70 price).

-

🚧 Gamma resistance at $80-85 is BRUTAL: The $80 level has 2.81B gamma exposure (largest single level) creating mechanical selling pressure from dealers hedging. Breaking through requires sustained institutional buying volume - not just earnings beat, but SUSTAINED follow-through. Even if Q3 crushes, stock could rally to $82-85 then stall as dealers sell into strength. The $85 call strike sits RIGHT at this resistance - needs TWO breakouts ($80, then $85) to profit.

-

🤝 AWS partnership revenue impact 6-12 months away: While strategically important, the five-year AWS collaboration won't materially impact revenue until H2 FY2026 or FY2027. Joint go-to-market initiatives launching early 2026, but enterprise sales cycles 6-12 months mean revenue realization delayed. If Q3 earnings expected to show AWS traction and it's not there yet, disappointment could hit stock.

-

💰 Software spending macro headwinds building: Enterprise IT budgets under pressure in 2026 economic uncertainty. Deal cycles elongating, VC-backed startups (ESTC customers) reducing spend, federal government budget concerns. If management cites macro headwinds in Q3 earnings or guides conservatively for Q4, stock could re-test lows despite solid execution. Software sector correlation risk - if Datadog, MongoDB, Snowflake guide down, ESTC gets hit by association.

-

⏰ Time decay is BRUTAL on out-of-the-money calls: Paying $5.00 for $85 calls means losing $0.05-0.06 per day to theta. Over 100 days, that's $5-6 of decay. Stock needs to rally just to OFFSET time decay before generating profits. If ESTC consolidates $75-80 range for next 60 days, then rallies to $85 in late February, these calls still might be worth only $2-3 (40-60% loss!) due to theta burn.

-

👔 CFO transition creates near-term uncertainty: CFO/COO Janesh Moorjani departed December 13, 2024, interim CFO Eric Prengel appointed. Q3 earnings will be first full quarter under new leadership. Any execution stumbles, accounting surprises, or guidance conservatism could be blamed on transition and hit stock. Investors prefer stability in C-suite, especially pre-earnings.

-

🎢 High open interest ratio creates volatility risk: Only 152 existing OI at $85 strike before this trade. Adding 2,500 contracts means this ONE trade represents 94% of total OI at this strike. If trader decides to exit early (rolls down/out, takes profit, cuts loss), it could create significant price pressure in both stock and options. Additionally, low liquidity at this strike means wider bid-ask spreads and slippage on exit.

-

📉 GenAI monetization still unproven: While 1,750+ customers using GenAI solutions sounds impressive, ESTC hasn't disclosed what % of revenue GenAI represents or path to meaningful contribution (need 15-20% of revenue to move the needle). If Q3 shows GenAI customer count grew but revenue contribution remains <5%, market will question monetization ability. Proof-of-concept to production transition in GenAI taking 12-18 months industry-wide.

🎯 The Bottom Line

Real talk: Someone just bet $1.3 MILLION that ESTC rallies from $75.85 to $90+ over the next 100 days. This isn't a hedge - this is a DIRECTIONAL BET with serious conviction that the 28% YTD selloff has created a massive opportunity.

What this trade tells us:

- 🎯 Sophisticated buyer sees value after 28% decline - believes worst is over and Q3 earnings will reverse trend

- 💰 Willing to pay $5.00 for out-of-the-money calls ($85 strike vs $75.85 stock) shows high conviction

- ⚖️ Positioned for Q3 earnings catalyst (Feb 26) expecting BEAT + guidance raise to drive $85-95 rally

- 📊 Chose strategic strike at former support - $85 was support in October, now resistance; reclaiming signals trend change

- ⏰ 100-day timeframe perfect: Captures Q3 earnings, AWS traction updates, Jina AI integration, product momentum (EIS, Agent Builder)

- 🏦 Created entire open interest: 2,500 contracts vs 152 existing = 94% of OI at this strike - this IS the market

This is NOT a "buy blindly" signal - it's a "pay attention, thesis developing" signal.

If you own ESTC:

- ✅ Hold through Q3 earnings (Feb 26) - four consecutive beats suggests management conservative, likely beats again

- 📊 Watch Barclays conference TODAY (Dec 10, 11:05 AM ET) for management tone on Q3 pipeline and GenAI

- 🎯 Key support at $75 - if breaks below, consider trimming 25-30% to manage risk

- 🚀 If breaks above $80, momentum likely accelerates to $85-90 as shorts cover and institutions chase

- 💪 Consider adding on pullbacks to $72-74 range ahead of earnings - averaging down into strength

If you're watching from sidelines:

- ⏰ Barclays conference TODAY is first tell - listen for Q3 confidence, GenAI momentum, AWS wins

- 🎯 Wait for technical confirmation: Break above $80 with volume = chase momentum; break below $75 = wait for $70

- 📈 Post-earnings entry likely best: If Q3 beats and guides up (expected), pullback to $85-88 provides better entry than chasing

- 🛡️ Lower-risk alternative: Wait for Q3 results, then buy stock at $85-88 vs gambling on calls at $75

- 📊 Call spread more prudent: Buy March $80/$90 call spread for $2.50-3.00 vs $5.00 for naked $85 calls

If you're bearish or neutral:

- 🎯 Respect the support at $75 - gamma data shows 0.63B exposure here, strong institutional buying likely

- ⚠️ Don't fight the trend if breaks $80 - institutional call buying can create self-fulfilling momentum

- 📉 Put spreads risky given low IV - option premiums compressed after 28% decline, limited put premium to collect

- ⏰ Better to wait for earnings - if Q3 disappoints, PLENTY of time to get short at higher levels

Mark your calendar - Key dates:

- 📅 December 10, 2025 (TODAY!) - Barclays conference presentation, 8:05 AM PT / 11:05 AM ET

- 📅 December 19 - Monthly OPEX (±4.4% implied move through this date)

- 📅 January 16, 2026 - Monthly OPEX (±9.7% implied move)

- 📅 February 20, 2026 - Monthly OPEX (±13.3% implied move)

- 📅 February 26, 2026 (CRITICAL!) - Q3 FY2026 earnings report after market close

- 📅 March 20, 2026 - Quarterly Triple Witch, EXPIRATION of this $1.3M call trade

Final verdict: ESTC's fundamental story remains compelling - AWS five-year partnership, GenAI adoption acceleration (1,750+ customers), strong execution track record (four consecutive beats), and product innovation (Jina AI acquisition, EIS launch, Agent Builder). The 28% YTD decline appears overdone given fundamentals, creating asymmetric setup.

However, these $85 out-of-the-money calls require an 18.8% rally to breakeven ($90) in 100 days. That's aggressive positioning dependent on Q3 earnings beat + guidance raise + technical breakout through $80-85 resistance. The institutional trader clearly has conviction, but retail traders should consider LOWER-RISK alternatives (shares, call spreads, waiting for confirmation).

Be smart. Watch the Barclays conference today. Let the setup develop. Q3 earnings will tell the story. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The call buyer may have complex portfolio strategies, hedging needs, or information not available to retail traders - do not blindly follow institutional trades. Always conduct independent research and consider consulting a licensed financial advisor before trading. Out-of-the-money options can expire worthless, resulting in 100% loss of premium paid. The breakeven price of $90 requires an 18.8% rally from current levels.

About Elastic N.V.: Elastic specializes in AI-powered search, observability, and security solutions, offering both conventional keyword search and vector search capabilities to support contextually relevant queries. Operating with open-source foundations, Elastic generates revenue through premium features serving enterprise customers worldwide, with a market cap of $7.87 billion in the Prepackaged Software Services industry.