🐻 EXE: $6.2M Bearish Put Spread - Smart Money Hedges Natural Gas Giant!

📅 December 19, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just deployed $6.2 MILLION into a sophisticated two-legged put spread on Expand Energy (EXE), America's largest independent natural gas producer. This isn't a simple directional bet - it's a carefully structured bearish position using different strikes and expirations that screams "professional hedging strategy." With natural gas prices tanking 25% from December highs and EXE down 16% from its all-time high just two weeks ago, institutions are clearly preparing for more downside ahead.

💰 The Option Flow Breakdown

📊 What Just Happened

🕐 9:51:43 AM - Two simultaneous put purchases worth $6.2M:

Leg 1: March 2025 Protection

- 🐻 BUY PUT March 20, 2025 $95 strike

- 📦 Volume: 13,000 contracts

- 💵 Premium: $3.1M

- 🎯 Type: BTO (Buy-to-Open)

- ⚡ Z-Score: 919.44 (this is INSANE volume - roughly 919x more than average!)

Leg 2: January 2025 Near-Term Coverage

- 🐻 BUY PUT January 16, 2025 $105 strike

- 📦 Volume: 13,000 contracts

- 💵 Premium: $3.1M

- 🎯 Type: BTO (Buy-to-Open)

- ⚡ Z-Score: 10.14 (10x typical volume)

Total Bet: $6.2 MILLION on downside protection

🤓 What This Actually Means

Real talk: This is NOT your typical directional bet. Let's decode what this sophisticated structure tells us:

The Strategy: Calendar Put Spread or Staggered Protection

This trader bought puts at two different strikes ($95 and $105) with two different expirations (Jan 16 and Mar 20). Here's why that matters:

✅ Near-term protection ($105 Jan): Breaks even at ~$105 by monthly OPEX in 28 days - this covers immediate downside risk through earnings season and winter demand uncertainty

✅ Longer-term floor ($95 Mar): Protects against deeper correction into Q1 2025 - this is 13% below current price and aligns with technical support levels

✅ Staggered approach: Rather than going all-in on one strike/date, they're hedging multiple time horizons - classic institutional risk management

Translation for us regular folks: Someone controlling a MASSIVE position in EXE stock (likely millions of shares) is paying $6.2M for insurance against a selloff. The staggered expirations suggest they're worried about both:

- Short-term catalyst risk (earnings, winter weather, gas price volatility)

- Longer-term structural headwinds (oversupply, competition from EQT)

The 919x average volume on the March $95 puts is absolutely extraordinary - this represents roughly one or two times per year type of unusual activity, signaling this is a significant institutional positioning event.

🏢 Company Overview: Expand Energy (EXE)

Who They Are: Expand Energy is America's largest independent natural gas producer, formed in October 2024 through the $7.4 billion merger of Chesapeake Energy and Southwestern Energy. The combined entity controls 1.9 million acres across the Haynesville (Louisiana) and Marcellus/Utica (Appalachia) basins.

By The Numbers:

- 💰 Market Cap: $10.7 billion

- 📊 Production: 7.1-7.2 Bcfe/d (approximately 6.7% of total U.S. natural gas output)

- 🎯 Industry: Natural Gas Exploration & Production

- 💵 Dividend: $2.30/year (1.9% yield)

- ⭐ Credit Rating: BBB- (Investment Grade from S&P and Fitch)

Current Price Action:

- Current: $108.61

- All-Time High: $126.62 (December 5, 2025 - just 2 weeks ago!)

- Recent Performance: Down 16% from ATH, down 10.5% from prior week

- 52-Week Range: $91.02 - $126.62

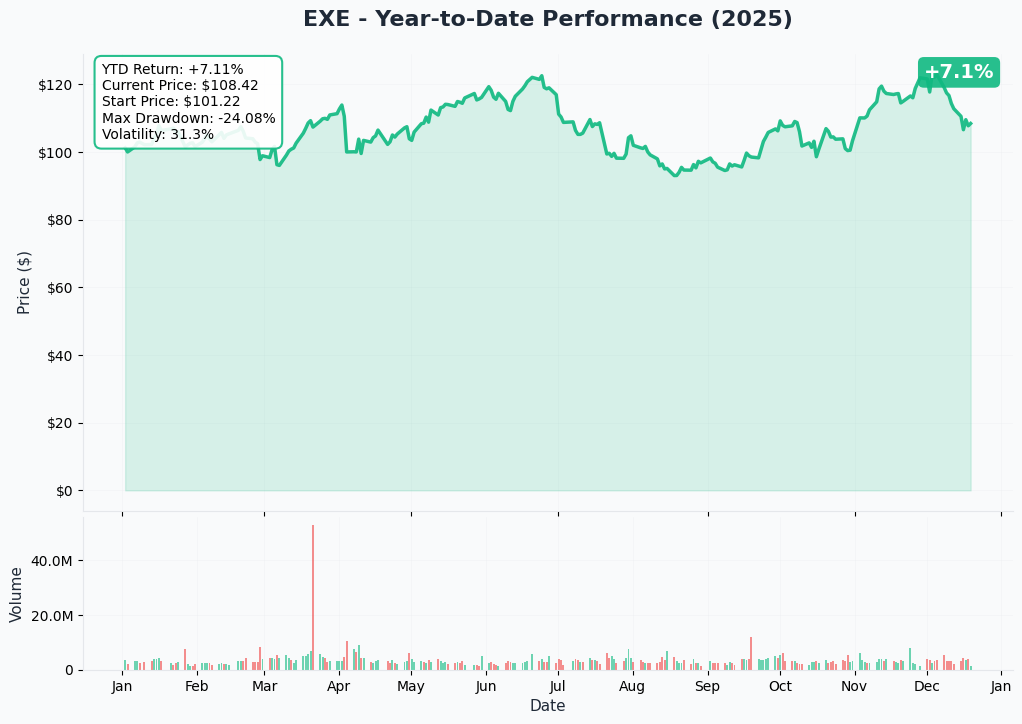

📈 Chart Check-Up

YTD Performance

The year-to-date chart tells a story of exceptional growth followed by sharp reversal. EXE rocketed from $91 lows in August to an all-time high of $126.62 on December 5 - a stunning 39% rally in just three months. This surge was driven by the successful Chesapeake-Southwestern merger completion, multiple analyst upgrades (UBS to $154 target), and cold weather forecasts boosting natural gas prices above $5.20/MMBtu.

However, the party ended abruptly in mid-December. The stock has shed 16% in just two weeks as natural gas prices crashed from $5.20 to $3.90 on forecasts for above-average temperatures heading into Christmas. This violent reversal has left EXE at a critical technical juncture - currently trading at $108.61, it's testing key support levels while sitting well below recent highs.

The massive $6.2M put spread trade we're analyzing was executed precisely as this breakdown accelerated, suggesting smart money is positioning for continued weakness.

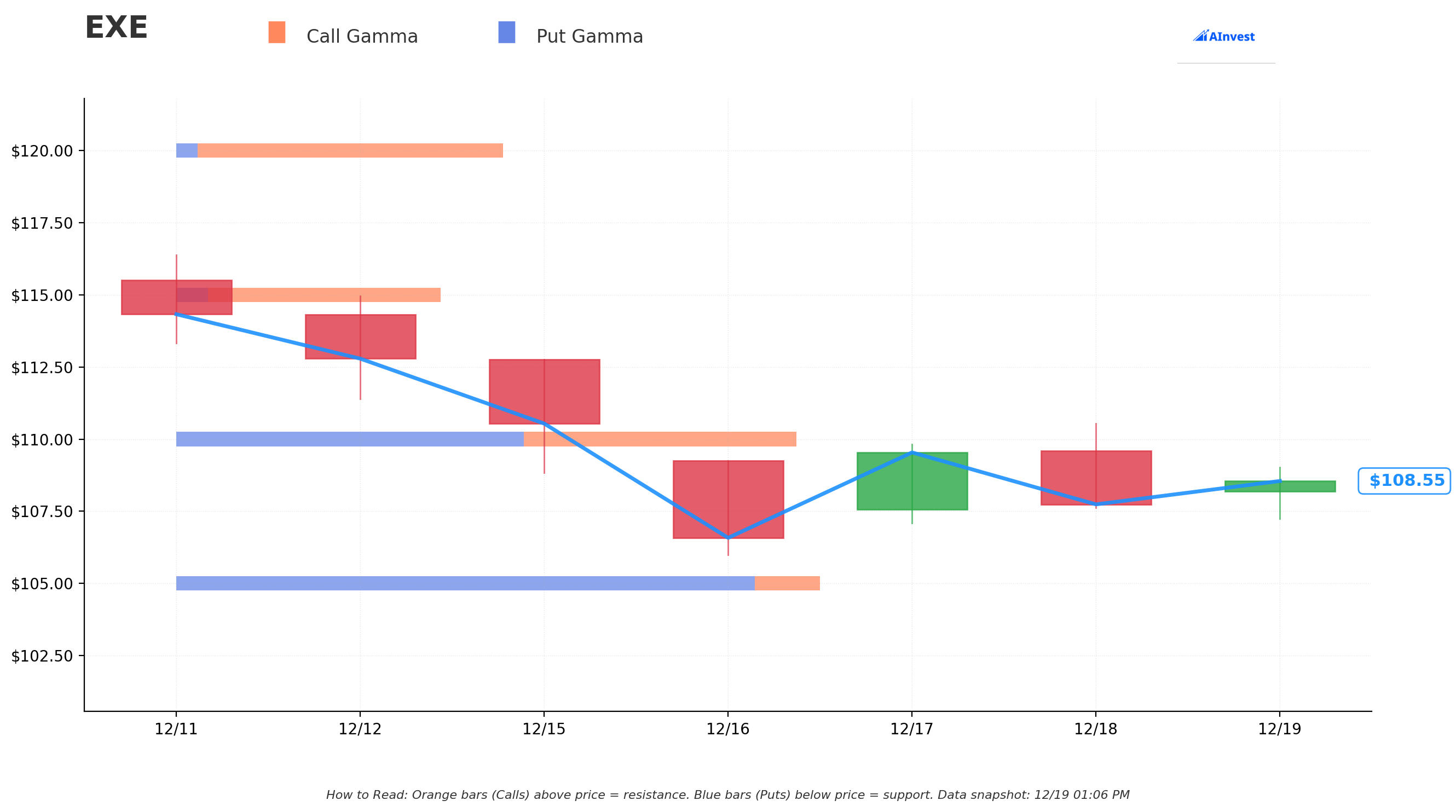

🎯 Gamma-Based Support & Resistance Analysis

Understanding Gamma Walls: Think of gamma levels as massive speed bumps on the price chart. These are strike prices where market makers have concentrated positions - they act like magnets, pulling the stock toward these levels. The bigger the gamma, the stronger the gravitational pull.

Key Resistance Zones (Orange Bars - Call Gamma Above Price):

🔴 $110 Strike - STRONG Resistance (5.12M gamma)

- This is the big one! Massive call gamma wall just $1.40 above current price

- Market makers sold tons of $110 calls, creating natural selling pressure as price approaches

- Breaking above $110 would require serious conviction and likely trigger a gamma squeeze

- Probability of reaching by Jan OPEX: Low (~25%) given current momentum

🔴 $115 Strike - MODERATE Resistance (3.27M gamma)

- Secondary resistance zone 6% above current price

- Would require significant catalyst (major cold snap, LNG export surge) to reach

- Aligns with analyst price targets but feels distant in current environment

Key Support Zones (Blue Bars - Put Gamma Below Price):

🔵 $105 Strike - STRONG Support (4.89M gamma)

- Critical floor just 3.3% below current price - this is THE level to watch

- Exactly matches the near-term put strike from our $6.2M trade!

- Market makers bought puts here, creating buying pressure if we drop

- Notice: This is where the January $105 puts were purchased - not a coincidence!

🔵 $100 Strike - MODERATE Support (2.14M gamma)

- Psychological round number with decent gamma support

- Would represent 8% pullback from current levels - not out of the question

- Aligns with technical retracement levels from August-December rally

The Gamma Story: Current price ($108.61) sits in a tight range between $105 support and $110 resistance. This 5-point zone acts like a cage - the stock wants to break one way or the other. The $6.2M put spread suggests institutions expect a break LOWER toward $105, then potentially toward $100 and $95.

Notice how the trader strategically chose $105 and $95 - these align perfectly with gamma support levels where market maker activity creates natural buying, limiting downside. Smart hedging picks strikes where support exists!

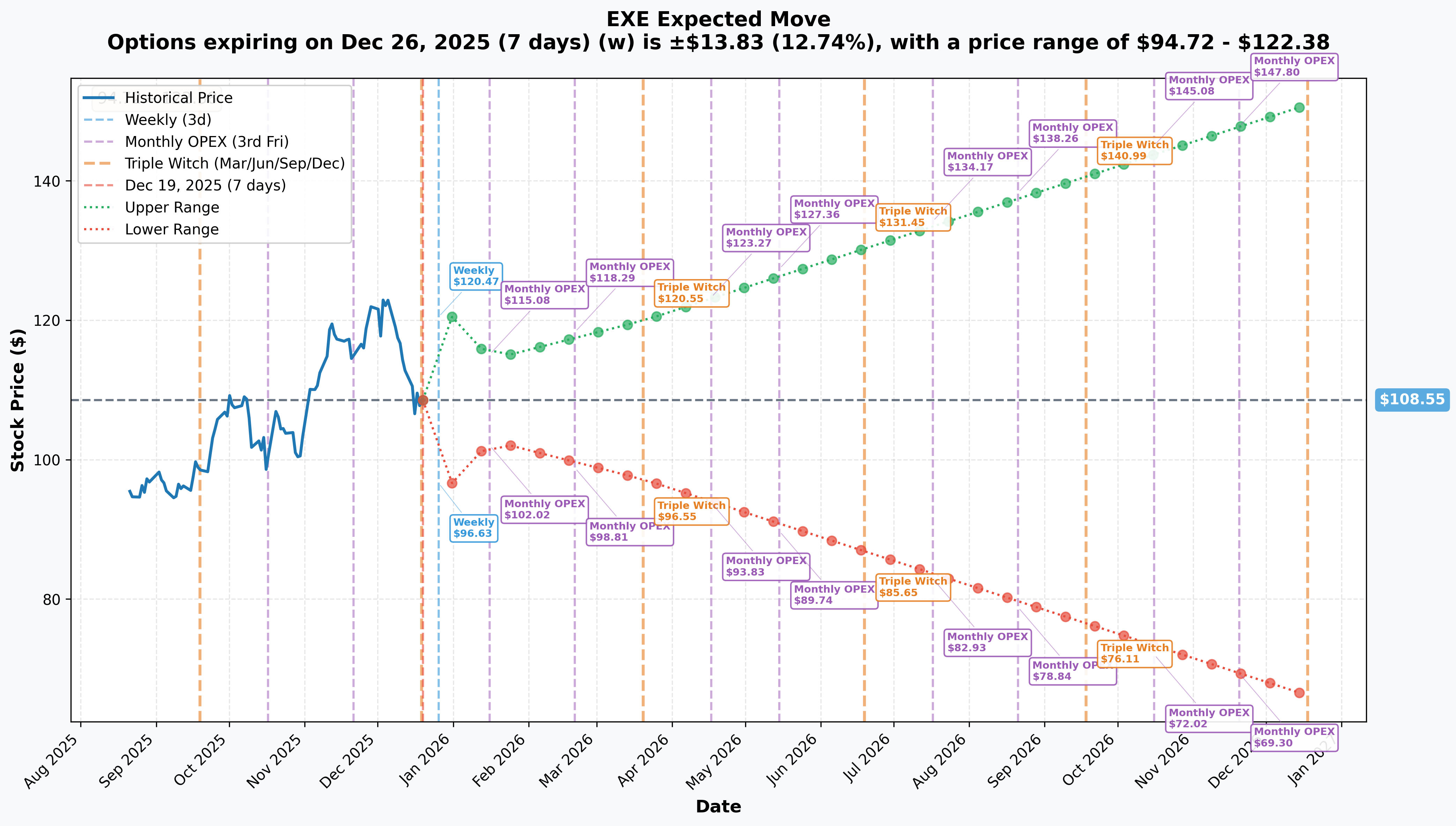

📊 Implied Move Analysis

What Is Implied Move? Think of implied move as the market's "expected range" based on options prices. It's like looking at betting odds - higher implied moves mean the market expects bigger swings.

Near-Term Range (Dec 26 Weekly OPEX):

- Expected Move: ±12.74%

- Price Range: $94.72 - $122.38

- Current Price: $108.61

Whoa! 🎢 A 12.74% weekly expected move is MASSIVE volatility - this suggests the market anticipates explosive price action in the next 7 days. This could be driven by:

- Year-end natural gas inventory reports

- Winter weather forecasts updates

- LNG export demand data

- General holiday volatility and thin trading

The bearish case ($94.72 downside target) would represent a 13% crash in one week - extreme but not impossible given recent gas price action. The January $105 puts would be deep in-the-money at this level.

Monthly OPEX (Jan 16) - 28 Days Out:

- Expected Move: ±5.36%

- Price Range: $102.73 - $114.37

- Z-Score Alert: The $105 Jan puts align perfectly with the lower end of this range!

This is where the strategy gets smart. The January $105 puts break even around $102-103, which is EXACTLY the lower boundary of the monthly expected move. The trader isn't betting on a crash - they're positioning for a normal-sized pullback that options pricing already anticipates.

Quarterly OPEX (Mar 20) - 91 Days Out:

- Expected Move: ±10.53%

- Price Range: $97.12 - $119.98

- Z-Score Alert: The $95 Mar puts sit just below this range's lower boundary

The March $95 puts provide catastrophic insurance - they only pay off if EXE falls more than the market expects. Given the 919x average volume, this suggests the trader is willing to pay up for tail-risk protection.

Probability Analysis:

Based on implied moves and current momentum:

📊 Reach $105 by Jan 16: ~45% probability (near-term put breakeven) 📊 Reach $100 by Mar 20: ~30% probability (psychological support) 📊 Reach $95 by Mar 20: ~15-20% probability (long-term put strike)

The staggered strikes reflect decreasing probabilities - higher premium for near-term $105 puts (higher chance), lower premium for out-of-the-money $95 puts (lower chance but bigger payoff).

🎪 Catalysts: What's Driving This Trade?

🔮 Upcoming Catalysts (Next 3 Months)

Q4 2025 Earnings - Late February 2026 📅

- Expected timing based on historical pattern (Q4 2024 reported Feb 26, 2025)

- Analyst expectations: Full-year 2025 EPS of $8.12 (up 476% YoY!)

- Key metrics to watch:

- Merger synergy realization vs. $400M target

- Free cash flow and debt reduction progress

- 2026 guidance (targeting 7.5 Bcfe/d on flat capex)

- Risk: Natural gas prices averaged $3.90-4.30 in Q4 vs. $5.20+ earlier assumptions - could pressure results

- Why it matters for puts: If earnings disappoint due to weak gas prices, the January $105 puts expire just BEFORE the report, limiting their value. But the March $95 puts capture post-earnings volatility!

Winter Heating Season Demand - Through March 2026 ❄️

- Peak demand period for natural gas (residential/commercial heating)

- EIA raised winter forecast to $4.30/MMBtu average (up 22% vs. prior winter)

- December 2025: 8% more heating degree days than 10-year average

- The Plot Twist: Despite cold early December, recent forecasts show above-average temperatures through Christmas, crushing gas prices

- Why it matters for puts: If winter stays mild, gas prices stay weak, and EXE stock follows - exactly what this bearish spread is betting on

LNG Export Capacity Coming Online - Q1 2026 🚢

- U.S. LNG exports forecast: 14.9 Bcfd in 2025 (up 25%), 16.3 Bcfd in 2026 (up 37%)

- Key projects commissioning:

- Venture Global Plaquemines LNG Phase 1 (already commissioning)

- NG3 Pipeline to Gillis, Louisiana (2.5 Bcfe/day) - directly benefits EXE's Haynesville assets

- EXE's advantage: 60% of production weighted toward Haynesville = direct access to Gulf Coast LNG terminals

- Why it matters for puts: LNG is the BULL case for natural gas. If export growth disappoints or gets delayed, EXE loses its structural tailwind

2026 Production Growth Outlook - Expected with Q4 Earnings 📈

- Management previously indicated potential 7.5 Bcfe/d in 2026 (5% growth on flat $2.85B capex)

- Driven by recent acreage acquisitions (75,000+ acres in Western Haynesville, 7,500 acres in Marcellus)

- Why it matters for puts: If they guide conservatively due to weak pricing environment, stock could gap down

Merger Synergy Milestones - Throughout 2026 💼

- Target: $500M annual run-rate synergies by year-end 2026 (one year ahead of schedule!)

- 2025 target: $400M (up from original $225M)

- Free cash flow impact: Additional $500M in 2026

- Why it matters for puts: Synergies are the good news story offsetting weak gas prices. Any execution stumbles = stock drops

✅ Past Catalysts (Already Happened - Context for Current Setup)

December Analyst Upgrades - Multiple Firms Raised Targets 📊

- UBS raised target to $154 (Dec 12) - 45% upside!

- Mizuho raised to $142 (Dec 12)

- JPMorgan raised to $132 (Dec 8)

- The irony: Stock peaked at $126.62 on Dec 5, THEN analysts upgraded, THEN it crashed 16%

- Why it matters: These upgrades assumed strong winter demand and high gas prices - that narrative is now broken

All-Time High of $126.62 (December 5, 2025) 🚀

- Represented 39% rally from August lows

- Driven by merger completion, winter optimism, LNG tailwinds

- Current price ($108.61) is 16% below this level - momentum has completely reversed

- Why it matters for puts: Many investors who bought the breakout are now underwater and may panic sell

Q3 2025 Earnings Beat (October 28, 2025) ✅

- Daily production: 7.33 Bcfd (92% natural gas)

- Raised full-year guidance to 7.15 Bcfe/d

- Reduced capex guidance by $75M to $2.85B

- Announced major acreage acquisitions (75,000+ acres Western Haynesville)

- Why it matters: Last earnings were great, but that was with higher gas prices - Q4 will be the test

Investment-Grade Credit Rating (October 2024) 🏆

- S&P and Fitch upgraded to BBB-

- Unlocks institutional investor base

- Lower borrowing costs

- Why it matters: Strong balance sheet limits bankruptcy risk, but doesn't protect against stock price volatility

🎲 Price Targets & Probabilities

Using Gamma Levels and Implied Move for Targets:

Let me break down three scenarios using our gamma analysis, implied move data, and catalyst timeline:

🐻 Bear Case: $95-100 Target by March 2025 (35% probability)

The Setup:

- Natural gas stays weak through winter (mild weather persists)

- Henry Hub settles around $3.50-3.80/MMBtu vs. $4.30+ expectations

- Q4 earnings disappoint on lower realizations

- LNG export growth slower than expected

- EQT reclaims #1 producer title through acquisitions

Price Path:

- Near-term (Jan 16): Test $105 gamma support → break lower to $100-102

- Medium-term (Mar 20): Grind down to $95-100 range

- Support levels: $105 (strong), $100 (moderate), $95 (long-term floor)

Put Spread Payoff:

- January $105 puts: In-the-money by $3-5 → worth $300-500k profit

- March $95 puts: At-the-money → worth $1-2M profit

- Total return: 20-40% on $6.2M premium ($1.2M-2.5M profit)

Catalysts That Get Us Here:

- Continued mild winter weather through January-February

- Weak Q4 earnings in late February

- Natural gas inventory builds above seasonal norms

- Broader energy sector rotation away from nat gas

⚖️ Base Case: $105-110 Range-Bound (45% probability)

The Setup:

- Natural gas finds floor around $3.80-4.00/MMBtu

- Winter demand moderately supportive but not spectacular

- Q4 earnings meet lowered expectations

- Merger synergies continue tracking ahead of plan

- Stock consolidates in gamma "cage" between $105 and $110

Price Path:

- Near-term (Jan 16): Chop between $105-110, test both levels multiple times

- Medium-term (Mar 20): Remain range-bound as market awaits 2026 guidance

- Key levels: $105 floor (strong gamma support), $110 ceiling (strong gamma resistance)

Put Spread Payoff:

- January $105 puts: Expire worthless or minimal value if stock holds $105

- March $95 puts: Decay significantly as time passes and stock stays above $100

- Total return: -30% to -60% on $6.2M premium ($2M-4M loss)

- Why hedge still works: If trader holds millions in EXE stock, that stock holds value too - this is insurance, not speculation

Catalysts That Get Us Here:

- Stable natural gas prices without major weather surprises

- In-line Q4 earnings with cautious but not terrible 2026 guidance

- Continued LNG export momentum offsetting production growth

- Market digests recent selloff and finds equilibrium

🚀 Bull Case: $115-120+ Rebound (20% probability)

The Setup:

- Arctic blast hits in January-February, spiking heating demand

- Natural gas rallies back above $4.50-5.00/MMBtu

- Q4 earnings beat with strong free cash flow

- Major LNG export contracts announced

- Share buyback program starts aggressively ($1B authorization)

Price Path:

- Near-term (Jan 16): Break above $110 resistance → gamma squeeze to $115

- Medium-term (Mar 20): Retest all-time highs around $120-126

- Resistance levels: $110 (must break first), $115 (secondary), $120-126 (prior highs)

Put Spread Payoff:

- Both puts expire worthless

- Total return: -100% on $6.2M premium (complete loss)

- Why hedge still makes sense: If stock rallies to $120, the underlying stock position gains $11.40/share. On 1M shares, that's $11.4M gain vs. $6.2M insurance cost = net profit of $5.2M

Catalysts That Get Us Here:

- Major cold snap in January-February (Polar Vortex event)

- Surprise LNG export acceleration or new facility announcements

- Natural gas inventory draws exceed expectations

- Broader energy sector rally on geopolitical developments

📊 Probability-Weighted Target

By January 16, 2025 (28 days):

- Expected range: $102-114 (±5.36% implied move)

- Most likely: $105-110 consolidation

- High probability of testing $105 support (45%+)

By March 20, 2025 (91 days):

- Expected range: $97-120 (±10.53% implied move)

- Most likely: $100-110 zone

- Real risk of hitting $95 strike if bear case plays out (20% probability)

Bottom Line on Targets: The put spread is structured for a base case of $100-105 by March, with insurance against a worst case of $95. The trader isn't calling for a crash - they're paying $6.2M for protection against a rational pullback driven by weak natural gas fundamentals. Given the 16% drop already happened in 2 weeks, they might be late to the party... or early to the next leg down.

💡 Trading Ideas: How To Play This Setup

🛡️ Conservative: "Sleep Well Strategy" - Cash Secured Puts

The Play: Sell cash-secured puts at strong support levels and collect premium while waiting to buy EXE cheaper.

Specific Trade:

- SELL PUT January 16, 2025 $100 strike

- Collect: ~$1.50-2.00 per share ($150-200 per contract)

- Cash Required: $10,000 per contract (must hold cash to buy 100 shares at $100)

- Breakeven: $98-98.50 (strike - premium collected)

Why This Works:

- $100 is psychological support + moderate gamma level

- If assigned, you buy EXE at $98-99 effective price (10% below current)

- If stock stays above $100, keep the premium as profit

- Even in bear case scenario, $98 is reasonable entry for long-term hold

Risk Management:

- Only do this if you WANT to own EXE at $98

- Don't over-leverage - max 20-30% of portfolio on any one trade

- Watch natural gas prices - if they crater below $3.50, $100 strike may not hold

Probability of Profit: ~60-65% (stock stays above $100) Max Profit: Premium collected ($150-200 per contract) Max Loss: Theoretically $9,800 if stock goes to zero (realistically limited to $10-15/share loss if $95 support holds)

⚖️ Balanced: "Calculated Hedge" - Put Debit Spread

The Play: Copy the institutional trade but size it appropriately for retail accounts. Use a put debit spread to limit cost while maintaining bearish exposure.

Specific Trade:

- BUY PUT February 20, 2025 $105 strike (pay ~$3.00-3.50)

- SELL PUT February 20, 2025 $100 strike (collect ~$1.50-2.00)

- Net Cost: ~$1.50-2.00 per share ($150-200 per spread)

- Max Profit: $3.50-4.00 per share ($350-400 per spread)

- Breakeven: ~$103-103.50

Why This Works:

- Mirrors the institutional bearish thesis with defined risk

- Targets the high-probability $100-105 range

- February expiration captures Q4 earnings reaction (late Feb)

- Max risk is $150-200 per spread vs. $6.2M institutional bet - appropriate sizing!

Position Sizing:

- Risk only 2-3% of portfolio on this trade

- Example: $50k account → risk $1,000-1,500 → buy 5-10 spreads

- Spreads cap both gain and loss - much safer than naked puts

Win Conditions:

- Stock breaks $105 support → both puts gain value

- Reaches $100 by expiration → max profit of $350-400 per spread

- Natural gas stays weak through winter → EXE follows

Loss Conditions:

- Stock rallies above $105 → spreads expire worthless

- Bullish catalyst (cold snap, LNG news) → lose full premium

Probability of Profit: ~40-45% (need stock below $103.50) Risk/Reward: 1:2 (risk $200 to make $400)

🚀 Aggressive: "YOLO with Training Wheels" - Leveraged Put Calendar Spread

The Play: For experienced options traders who understand calendars - sell near-term volatility, buy longer-term protection. This is ADVANCED.

Specific Trade (March expiration focus):

- BUY PUT March 20, 2025 $100 strike (pay ~$2.50-3.00)

- SELL PUT January 16, 2025 $105 strike (collect ~$1.50-2.00)

- Net Cost: ~$1.00-1.50 per share ($100-150 per spread)

The Strategy: This is a diagonal put calendar. You're selling expensive near-term premium (high IV in January) and buying cheaper longer-term protection (March). As January expiration approaches:

- If stock stays above $105 → Jan put expires worthless, you keep premium

- If stock drops toward $100 → March put gains value while Jan put losses are capped

- After Jan expiration, you own a naked March $100 put with reduced cost basis

Why This Is Aggressive:

- Requires understanding of time decay (theta) and volatility (vega)

- The short Jan $105 put creates undefined risk if stock crashes before Jan 16

- Calendar spreads profit from sideways/slight down movement, not crashes

- Need to actively manage - can't just set and forget

Advanced Variation - "The Institutional Copycat": For accounts with $25k+, copy the exact institutional trade at retail scale:

- BUY 10 contracts January $105 puts (~$3,000)

- BUY 10 contracts March $95 puts (~$1,500)

- Total Cost: ~$4,500

- Max Profit: Unlimited below $90 (but realistically $10k-15k if stock hits $90)

- Breakeven: Need stock below $104.70 by Jan, below $93.50 by March

Win Conditions:

- Bear case plays out → $100 by March → March put worth $10/share ($10k value on 10 contracts)

- Natural gas crashes → EXE follows to $95 or below → home run

Loss Conditions:

- Stock rallies or stays flat → lose 100% of premium ($4,500)

- Theta decay eats away value even if directionally correct but timing wrong

Who This Is For:

- Traders comfortable losing $4,500 completely

- Those who believe institutions know something about winter weakness

- Accounts that can allocate 5-10% to high-risk/high-reward plays

Probability of Profit: ~30-35% (need significant move down) Risk/Reward: 1:3 to 1:5 (risk $4,500 to make $15k-25k)

⚠️ Risk Factors: What Could Go Wrong

Let's be real about the risks here - this trade isn't a slam dunk, and there are plenty of ways it could blow up:

🌡️ Winter Weather Surprise - The Polar Vortex Scenario

The Risk: What if the "above-average temperatures through Christmas" forecast completely reverses in January-February? Arctic blasts can appear with just 7-10 days notice, and sudden cold snaps have historically sent natural gas prices soaring 50%+ in days.

Impact on Trade:

- Natural gas spikes from $3.90 back to $5.00+

- EXE stock gaps up 10-15% on one weather report

- Both January and March puts become worthless overnight

- Probability: 15-20% (weather is inherently unpredictable)

What Contrarians Say: EIA's December update shows 8% more heating degree days than average and expects 580 Bcf inventory withdrawals in December (28% above five-year average). One polar vortex event = game over for puts.

🚢 LNG Export Acceleration - The Structural Bull Case

The Risk: The ENTIRE long-term thesis for natural gas is LNG exports. U.S. LNG exports are forecast to hit 16.3 Bcfd by 2026 (up 37% vs. 2024), and EXE is strategically positioned with 60% of production in Haynesville near Gulf Coast terminals.

What If:

- Venture Global Plaquemines Phase 1 ramps faster than expected

- New LNG contracts announced (happened with Energy Transfer Lake Charles in April 2025)

- European energy crisis resurfaces, spiking LNG demand

- China signs massive long-term LNG purchase agreements

Impact on Trade:

- LNG demand creates structural floor under natural gas prices

- EXE's Haynesville assets become premium assets

- Stock re-rates higher on scarcity value

- Analyst targets ($154 from UBS) suddenly look conservative

- Probability: 25-30% (LNG is the strongest tailwind)

💪 Merger Synergies Beat Expectations - The Execution Story

The Risk: Expand Energy has CRUSHED synergy targets. Originally projected $400M by 2027, they now expect $500M by year-end 2026 - one year early and 25% higher!

What If Synergies Offset Weak Gas Prices:

- Q4 earnings show free cash flow remains strong despite commodity weakness

- $1 billion share buyback program begins aggressively (9.3% of market cap!)

- Debt reduction exceeds $1 billion target (they doubled it from $500M)

- Cost savings buffer margin compression

Impact on Trade:

- Stock gets re-valued on execution story rather than commodity exposure

- "Show me" story becomes "proven" story

- Multiple expansion despite weak gas prices

- Probability: 30-35% (execution has been flawless so far)

📉 You're Late to the Party - The "Weak Hands" Risk

The Risk: EXE is already down 16% from all-time highs made just two weeks ago. Natural gas crashed from $5.20 to $3.90 (25% decline). Much of the bad news may already be priced in.

The Technical Setup:

- $105 is STRONG gamma support (4.89M) - institutions will defend this level

- Sentiment is extremely bearish (contrarian indicator)

- Put/call ratios likely elevated (would need real-time data to confirm)

- The $6.2M institutional put spread might be the "final capitulation" signal

What Happens:

- Stock finds a floor at $105-108 and chops sideways

- Time decay (theta) kills put values even if directionally neutral

- By January/March expiration, puts worth 30-50% less just from time passage

- Probability: 40-45% (this is the BASE case scenario!)

🏆 Competition from EQT - The Market Share Battle

The Risk: EQT Corporation is actively trying to reclaim the #1 U.S. producer title. Despite having similar production (within 1 Bcf/d), EQT trades at $34.6B market cap vs. EXE's $10.7B - a staggering 3.2x valuation gap!

Why This Matters:

- EQT's premium valuation gives them M&A currency

- Pure Marcellus exposure is favored by institutions (lower breakevens)

- If EQT announces major acquisition, EXE loses "largest producer" branding

- Market may be correctly pricing in EXE's Haynesville risk vs. EQT's Marcellus advantage

Impact on Trade:

- Valuation gap persists or widens

- EXE remains "cheap" for fundamental reasons, not temporary sentiment

- Stock trades sideways in perpetuity while puts decay

- Probability: 20-25% (EQT is formidable competition)

💣 Black Swan: Regulatory or Policy Shock

The Risk: The incoming Trump administration (2025+) is expected to be fossil fuel friendly, but what if:

- EPA methane regulations accelerate despite 2025 delays

- LNG export permits get challenged on environmental grounds

- Tax code changes hurt E&P economics

- State-level production restrictions (Louisiana, Pennsylvania)

Impact on Trade: Could trigger sector-wide selloff, making puts profitable but for wrong reasons (structural risk vs. cyclical bet). EXE's investment-grade balance sheet limits bankruptcy risk but not stock price volatility.

Probability: 5-10% (tail risk, but worth mentioning)

🎯 The "Wrong Structure" Risk

The Risk: What if the $6.2M trade ISN'T a bearish bet at all? Consider:

- Could be a collar (they own stock + sold calls, buying puts for protection)

- Could be tax loss harvesting / portfolio rebalancing

- Could be merger arb unwind (buying puts to hedge while selling stock)

- Could be two separate traders (13k Jan $105 buyer + 13k Mar $95 buyer)

Impact on Trade: If we're misreading the institutional intent, we could be fading smart money when they're actually neutral or bullish on the stock. The 919x Z-score on March $95 puts suggests this IS unusual, but unusual doesn't always mean directional.

Probability: 10-15% (structure seems bearish, but context matters)

🎯 The Bottom Line

Real talk: This $6.2M bearish put spread on EXE is a sophisticated institutional hedge, not a speculative crash bet. Let me give you the honest breakdown:

If You Already Own EXE Stock: 📊

This flow is a warning signal, but not necessarily a sell signal. The trader is hedging a massive long position - they still WANT to own EXE, they just want insurance against winter weakness and natural gas volatility. Consider:

✅ Hold if: You bought below $100, believe in LNG export thesis, and can stomach volatility ⚠️ Trim if: You bought above $120 chasing momentum, or need the cash soon ❌ Sell if: You're overleveraged, down big from $126 highs, or can't handle more downside to $95-100

If You're Considering Buying EXE: 🤔

Wait for better entry! The $6.2M put spread suggests institutions expect lower prices ahead. Be patient:

✅ Great entry: $95-100 range (aligns with put strikes and gamma support) ⚖️ Decent entry: $105 if it holds on high volume (strong gamma support level) ❌ Poor entry: Current $108.61 (stuck between support and resistance, no catalyst)

If You Want To Trade Options on This: 🎰

My Honest Take: The risk/reward is TRICKY here. Natural gas is notoriously volatile and weather-dependent - you could be right on direction and still lose money on timing. That said, three ways to play:

1️⃣ Conservative (60% of options allocation): Sell cash-secured $100 puts for January, collect premium, willing to own at $98 effective price

2️⃣ Balanced (30% of options allocation): Buy February $105/$100 put debit spread for $150-200, targeting Q4 earnings weakness

3️⃣ Aggressive (10% of options allocation): Copy institutional trade at small scale - 10 contracts each of Jan $105 and Mar $95 puts ($4,500 total risk)

Expected Outcome by March 20, 2025:

Given current setup, here's my probability-weighted forecast:

📊 Most Likely (45%): Range-bound $105-110, puts expire with 30-60% loss 📉 Bear Case (35%): Test $95-100 support, puts profit 20-100% 📈 Bull Case (20%): Rally to $115-120, puts expire worthless (-100%)

Mark Your Calendar: 📅

- January 16: Monthly OPEX - watch if $105 support holds or breaks

- Late February: Q4 earnings - critical for 2026 guidance and synergy update

- March 20: Quarterly OPEX - final judgment on put spread success

The Unvarnished Truth:

This trade works if natural gas stays weak ($3.50-4.00 range) through winter and Q4 earnings disappoint. It FAILS if we get a polar vortex, LNG contracts accelerate, or synergies offset commodity weakness. The institutional trader is paying $6.2M for protection - they clearly see risk, but that doesn't make it a sure thing.

For retail traders: Don't bet the farm on puts here. EXE has a strong balance sheet (BBB- rated), accelerating synergies, and structural LNG tailwinds. The stock could easily chop sideways and kill put values through time decay.

My contrarian worry? The $6.2M put spread might be the final capitulation signal. When institutions hedge this aggressively after a 16% decline, it sometimes marks the bottom. The best time to buy insurance is before the crash, not after.

Final Verdict:

- For put buyers: Small position sizing only (2-5% of portfolio max), use spreads to limit risk

- For stock buyers: Wait for $95-105 before building core position

- For premium sellers: Juicy opportunity to sell puts at $100 if you want to own EXE cheaper

This is a RESPECT THE TRADE moment, not a COPY THE TRADE moment. Institutions have different risk profiles, time horizons, and capital bases than retail traders. Learn from their positioning, but size appropriately for your own situation!

📊 Option Flow Tape (Official Record)

| Time | Type | Expiry | Strike | Volume | Premium | Action | Z-Score |

|---|---|---|---|---|---|---|---|

| 09:51:43 | PUT | 2025-03-20 | $95 | 13,000 | $3.1M | BTO | 919.44 |

| 09:51:43 | PUT | 2025-01-16 | $105 | 13,000 | $3.1M | BTO | 10.14 |

Total Premium: $6.2M Strategy Classification: Custom Spread (2-leg bearish put spread, different strikes and expirations) Institutional Confidence Level: High (919x average volume indicates significant positioning event)

🔗 Key Resources & Further Reading

Company Links:

- Expand Energy Investor Relations

- EXE Stock Page - Ainvest

- January $105 Put Option Chain

- March $95 Put Option Chain

Recent News & Analysis:

- Chesapeake-Southwestern Merger Completion

- Q3 2025 Earnings Results

- Investment Grade Rating Announcement

Market Data & Forecasts:

⚠️ Disclaimer

This analysis is for educational and informational purposes only. Options trading involves substantial risk and is not suitable for all investors. The risk of loss in trading options can be substantial and may exceed the amount invested.

Past performance does not guarantee future results. The $6.2M institutional trade discussed herein represents the actions of professional traders with different risk tolerances, capital bases, and time horizons than retail investors.

Before trading options, carefully consider your investment objectives, risk tolerance, and level of experience. Consult with a qualified financial advisor before making investment decisions.

Always remember: You can lose 100% of your investment in options. Never invest money you cannot afford to lose completely.

Analysis Date: December 19, 2025 EXE Price at Analysis: $108.61 Natural Gas (Henry Hub): $3.92/MMBtu

Trade responsibly. Manage risk. Stay informed. 💪