💼 FDS $1.3M Call Bet Ahead of December 18 Earnings - Smart Money Positioning Pre-Report! 🎯

📅 December 4, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $1.3 MILLION on FDS calls this morning at 11:00:42! This bullish bet bought 1,500 contracts of $290 strike calls expiring December 19th - positioning for a major move just ONE DAY after FDS reports critical Q1 fiscal 2026 earnings on December 18th. With FDS down -44% from its 52-week high at $279.15 following CEO transition uncertainty and conservative guidance, smart money is betting on an earnings rebound. Translation: Institutional investors see a setup for a significant bounce in this beaten-down financial data giant!

📊 Company Overview

FactSet Research Systems (FDS) is a leading provider of integrated financial data and analytical applications:

- Market Cap: $10.45 Billion

- Industry: Computer Programming & Data Processing Services

- Current Price: $279.15 (down 44% from $496.90 52-week high)

- Primary Business: Aggregates financial data from multiple sources into integrated workstations, delivering portfolio analytics primarily to buy-side clients (80%+ of revenue including wealth managers, asset managers, and corporate entities)

Recent major acquisitions: CUSIP Global Services (2022), BISAM for risk analytics (2017), Portware for trade execution (2015)

💰 The Option Flow Breakdown

The Tape (December 4, 2025 @ 11:00:42):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order_Type | Confidence | Z_Score | Strategy_Type |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2025-12-04 | 11:00:42 | FDS | BUY | CALL $290 | 2025-12-19 | $290 | 1,500 | $1.3M | BTO | MEDIUM | 34.28 | STANDALONE |

🤓 What This Actually Means

This is an aggressive bullish bet on FDS rebounding sharply post-earnings! Here's what went down:

- 💸 Substantial premium: $1.3M ($8.67 per contract × 1,500 contracts, assuming ~$867 per contract)

- 🎯 Strike selection: $290 provides 3.9% upside target from current $279.15 price

- ⏰ Strategic timing: 15 days to expiration, expiring ONE DAY AFTER December 18th earnings report

- 📊 Size significance: 1,500 contracts represents 150,000 shares worth ~$42M notional exposure

- 🎰 High conviction play: Buying calls right before a binary earnings catalyst shows strong conviction

What's really happening here: This trader is making a DEFINED-RISK bet that FDS earnings on December 18th will beat expectations, driving the stock from its current depressed levels ($279) back above $290. The December 19th expiration gives just ONE day post-earnings for the thesis to play out - this is about capturing an immediate gap-up move, not a slow grind higher.

Think of it like buying a lottery ticket for the earnings lottery - except this lottery has fundamental odds backing it:

- Stock trading near 52-week lows ($250.50 low vs current $279.15)

- 91% client retention rate showing business strength

- $400M buyback program at compelling valuations

- December 2025 Arcesium partnership addressing $210B+ private credit market

Unusual Score: 🔥 EXTREME (279x average size) - This is a highly unusual bet that happens only a few times a year! The Z-score of 34.28 places this in the 99.93rd percentile - only 4 larger trades in the past 30 days. While not "once in a lifetime," this is definitely smart money making a big, calculated bet ahead of a critical catalyst.

📈 Technical Setup / Chart Check-Up

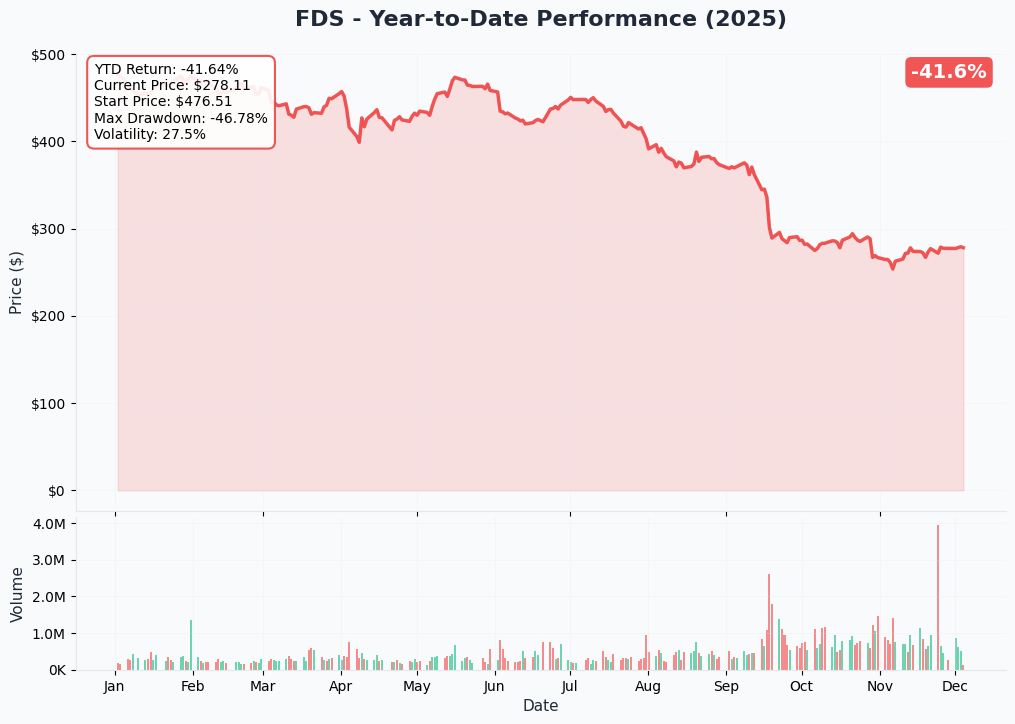

YTD Performance Chart

FDS has had a brutal year - the stock peaked at $496.90 in February 2025 but has since crashed -44% to current levels around $279.15. The chart tells a story of CEO transition uncertainty and conservative fiscal 2026 guidance weighing heavily on sentiment.

Key observations:

- 📉 Severe drawdown: From Feb highs at $497 to September lows at $250.50 (-49.6% peak-to-trough)

- 🔄 Consolidating at lows: Trading in tight $260-$280 range for past 2+ months

- 📊 Heavy volume near lows: Institutional accumulation visible at $250-$260 levels

- 🎯 Support holding: Multiple tests of $250-$255 area have held firm

- ⚡ Coiled spring setup: Extended consolidation after -44% decline often precedes mean-reversion bounce

- 💪 Fundamental strength vs price action disconnect: Business fundamentals remain solid (91% retention, growing ASV) despite stock weakness

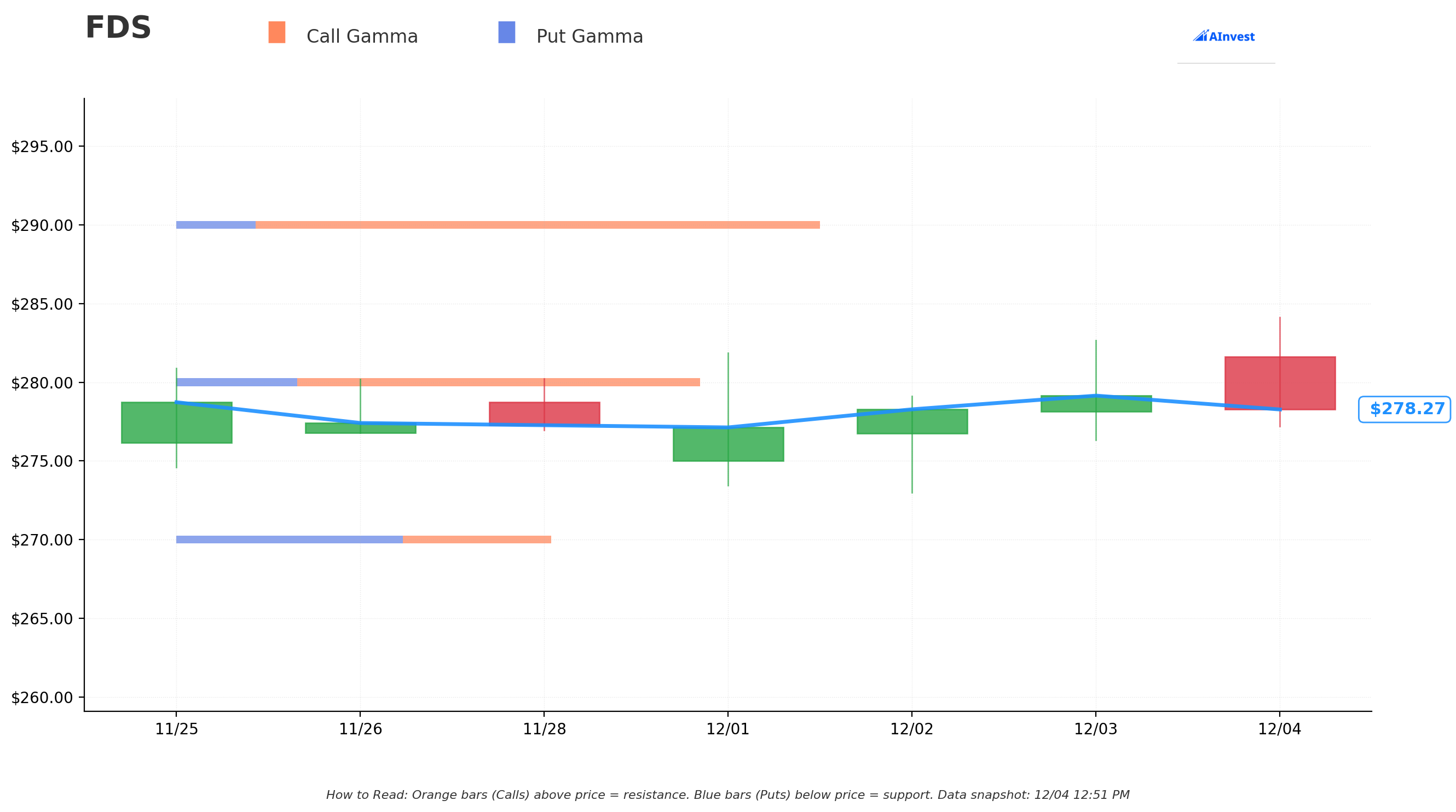

Gamma-Based Support & Resistance Analysis

Current Price: $278.44

The gamma exposure map reveals critical price magnets that will govern post-earnings price action:

🔵 Support Levels (Put Gamma Below Price):

- $270 - Immediate support with 0.171B total gamma (strongest nearby floor at -3.0% below price)

- $260 - Secondary support at 0.090B gamma (-6.6% below, major accumulation zone)

- $250 - Major structural floor with 0.092B gamma (-10.2% below, 52-week low area at $250.50)

- $230 - Extended disaster floor at 0.031B gamma (-17.4% below)

🟠 Resistance Levels (Call Gamma Above Price):

- $280 - Immediate ceiling with 0.239B gamma (STRONGEST RESISTANCE at just +0.56% above current price)

- $290 - Secondary resistance at 0.293B gamma (+4.2% above - THIS IS THE STRIKE! Highest call gamma)

- $300 - Major ceiling zone with 0.191B gamma (+7.7% above)

- $310 - Extended upside target at 0.138B gamma (+11.3% rally required)

- $320 - Aggressive target at 0.054B gamma (+14.9% above)

- $330 - Maximum upside at 0.032B gamma (+18.5% above)

What this means for traders: FDS is trading RIGHT AT massive resistance levels. The $280 level has 0.239B gamma creating natural selling pressure, but the real battle is at $290 where there's 0.293B call gamma - the single largest gamma concentration on the entire board!

This is NOT a coincidence - the call buyer struck EXACTLY at $290 where maximum dealer hedging activity will occur. If FDS breaks above $280-$285 on earnings, dealers will be FORCED to buy shares to hedge their short call positions, potentially triggering a gamma squeeze toward $290-$300. This is sophisticated positioning that understands options market mechanics.

The $270 support level (0.171B gamma) is critical - if earnings disappoint and FDS breaks below $270, momentum could accelerate toward $260 (-6.6% downside) where the next major support sits.

Net GEX Bias: Bullish (1.088B call gamma vs 0.554B put gamma) - Overall positioning skews bullish with nearly 2:1 call-to-put ratio. Market makers are positioned for upside, which creates mechanical buying pressure above key levels.

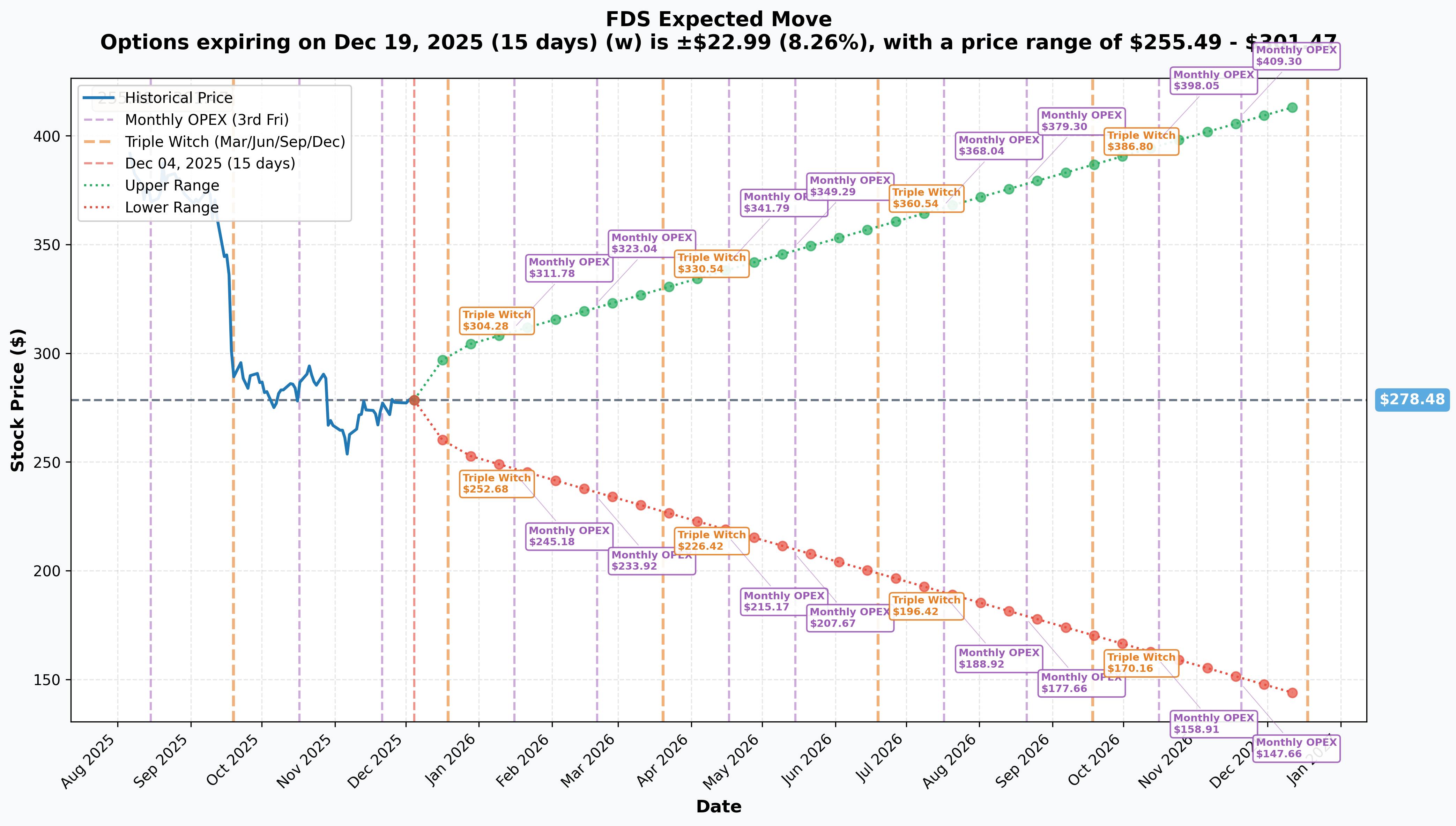

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 December 19 (Triple Witch - 15 days - THIS TRADE!): ±$22.99 (±8.26%) → Range: $255.49 - $301.47

- 📅 January 16 (Monthly OPEX - 43 days): ±$33.30 (±11.96%) → Range: $245.18 - $311.78

- 📅 December 18, 2026 (Yearly LEAPS - 379 days): ±$136.76 (±49.11%) → Range: $141.72 - $415.24

Translation for regular folks: Options traders are pricing in an 8.26% move ($23) through December 19th expiration which includes the December 18th earnings catalyst. The market expects SIGNIFICANT volatility around earnings - that's a substantial implied move for a $10.45B financial data company!

The December 19th implied range of $255.49-$301.47 is particularly relevant for this trade:

- Upper range: $301.47 - The call buyer's $290 strike sits WITHIN the expected range (needs +7.7% move vs 8.26% implied)

- Breakeven estimate: ~$298-299 - Assuming $8.67 paid per contract, needs stock at ~$298.67 to breakeven

- Probability of profit: ~35-40% - Strike is slightly in-the-money relative to implied volatility expectations

Key insight: The call buyer is betting that FDS moves LARGER than the 8.26% implied move, or that the move is specifically directional (up) rather than symmetrical. Historical FDS earnings moves average 5-8%, so an 11% move to $310 would be above-average but not unprecedented.

🎪 Catalysts

🔥 Immediate Catalysts (Next 14 Days)

Q1 Fiscal 2026 Earnings - December 18, 2025 (14 DAYS!) 📊

FDS reports fiscal Q1 results on Wednesday, December 18, 2025 before market open with conference call at 9:00 AM ET. This is THE catalyst that will make or break this $1.3M call trade!

Wall Street consensus and key expectations:

- 📊 Revenue: ~$572-577M (implied from annual guidance, +5-6% YoY growth)

- 💰 EPS: $4.39 consensus (+0.5% YoY vs $4.37 prior year)

- 🤖 Organic ASV Growth: Looking for trajectory toward $100-150M annual target (4-6% growth rate)

- 👥 Client Retention: Must maintain 91% retention rate or higher

- 💵 Free Cash Flow: Critical metric after Q1 FY2026 showed 56.4% YoY decline to $60.5M

- 🚀 Arcesium Partnership: Commentary on December 2025 partnership pipeline and traction

Why this could be a positive surprise:

-

Lowered expectations: Stock down 44% from highs with conservative fiscal 2026 guidance ($16.90-$17.60 adjusted EPS) creating low bar to beat

-

Arcesium partnership announced December 3: Transformative deal addressing $210B+ private credit market - management could provide bullish commentary

-

Insider buying signal: EVP Goran Skoko purchased 500 shares at $252.93 on November 6 near 52-week lows - management confidence indicator

-

$400M buyback at compelling prices: With stock at $279 vs prior average buyback price of $419, this program could retire ~4% of shares and add ~$0.70 to EPS

-

AI product launches momentum: Mercury chatbot, Pitch Creator for bankers, and Hebbia partnership could drive ARPU expansion commentary

Downside risk factors:

- Any disappointment in organic ASV growth (target is 4-6%, below historical 6-8%)

- Free cash flow concerns if working capital headwinds persist

- Conservative Q2 guidance would reinforce "reset year" narrative

- China revenue exposure (~15-20% of sales) with geopolitical uncertainty

- CEO transition execution questions (Sanoke Viswanathan took over September 2025)

Historical precedent: FDS has shown mixed recent track record, beating estimates twice and missing twice in last four quarters. Typical post-earnings moves range 3-7%, but this setup could produce larger move given -44% YTD decline and positioning.

Quarterly Dividend Payment - December 18, 2025 💰

FDS pays $1.10 per share dividend on December 18th (same day as earnings):

- Annualized: $4.40 per share (1.6% yield at current price)

- Ex-Dividend Date: November 28, 2025 (already passed)

- Recent Increase: 6% dividend increase announced in fiscal 2025

- 43-year track record: 43rd consecutive year of revenue growth

This dividend payment removes downside support but also signals management confidence in cash generation.

🚀 Near-Term Catalysts (Q1-Q2 2026)

Arcesium Strategic Partnership - December 2025 Launch 🤝

FDS announced transformative partnership with Arcesium on December 3, 2025 (just yesterday!) to unify front, middle, and back-office workflows:

Why this matters (HUGE TAM opportunity):

- 🎯 Target Market: Asset owners/managers managing $5.3T in gross AUM through Arcesium

- 💰 Private Credit TAM: Private credit fundraising hit $210B in 2024 + $124B in H1 2025 - massive growth market

- 🏆 Competitive Advantage: First "single source of truth" solution addressing traditionally siloed middle/back-office functions

- 📊 Technology Integration: Combines FDS analytics with Arcesium's IBOR, ABOR, and Reference Data in cloud-native platform

- 💸 Revenue Potential: Could address market where data fragmentation has doubled regulatory compliance costs over past decade

Timeline and expectations:

- Q1 FY2026 earnings (Dec 18): Early commentary on partnership structure and go-to-market strategy

- Q2-Q3 FY2026: Initial customer pilots and proof-of-concept deployments

- FY2027+: Material revenue contribution expected as solution scales

This partnership could be the catalyst that shifts sentiment from "FDS is declining" to "FDS is innovating" - exactly what the stock needs after -44% drawdown.

Share Repurchase Program Execution (September 2025 - August 2026) 💵

FDS authorized $400M buyback program on June 17, 2025, available from September 1, 2025:

Buyback effectiveness at current prices:

- 💰 Prior Program: Repurchased 443,771 shares for $186.3M at $419.53 average price in fiscal 2025

- 🎯 Current Opportunity: Stock at $279 vs prior $419 average = 33% cheaper per share

- 📊 Impact Estimate: $400M could retire ~1.43M shares (~4% of 37.2M float) at current prices

- 💵 EPS Accretion: Could add ~$0.70 to annual EPS through share count reduction

- ⏰ Timing: Management likely accelerating buybacks at $250-$280 range (insider buying confirms this)

Why this matters for the call trade: Aggressive buyback execution in Q1-Q2 FY2026 would provide sustained buying pressure and signal management confidence, supporting upside momentum post-earnings.

AI Product Rollout - Mercury & Pitch Creator (Early 2025) 🤖

FDS unveiling AI-powered intelligent platform with multiple products launching Q1-Q2 2026:

Key Products:

- Mercury Chatbot: LLM-powered knowledge agent for junior banker workflows, fact-based decision-making

- Conversational API: Mercury-powered chatbot for client tech stack integration

- Pitch Creator for Bankers: AI-automated tombstone generation, chart creation, slide development (launching early 2025)

- GenAI Data Packages: Consolidated data feeds for AI workflows

Revenue implications:

- Expected to drive workflow productivity gains (reduces time spent on manual tasks)

- Premium pricing tier potential - AI features could justify 10-20% price increases for power users

- Client retention tool - AI capabilities reduce switching costs and increase stickiness

- Competitive differentiation vs Bloomberg's aging terminal interface

Potential earnings commentary: FDS could provide AI product adoption metrics or early customer feedback that exceeds expectations, driving multiple expansion.

Hebbia Partnership for AI-Driven Research (September 2025 Launch)

Partnership announced September 2025 to combine FDS structured data with Hebbia's unstructured intelligence:

- Uses Hebbia's Iterative Source Decomposition (ISD) technology

- Combines financials, market prices, estimates with unstructured research

- Gradual rollout through Q1-Q2 FY2026

⚠️ Risk Catalysts (Downside Scenarios)

CEO Transition Execution Uncertainty 👔

Sanoke Viswanathan became CEO in September 2025 with limited financial data/SaaS experience:

- Background: Former CEO JPMorgan International Consumer and Wealth; McKinsey Partner

- Conservative fiscal 2026 guidance fell significantly below analyst expectations

- Phil Snow (prior CEO) advisory role ends December 2025 - losing institutional knowledge support

- ⚠️ December 18 earnings will be first full quarter under new leadership

ASV Growth Deceleration Concerns 📉

Organic ASV growth decelerated to 4.1% in Q2 FY2025 (vs 5.1% consensus):

- Fiscal 2026 guidance targets 4-6% growth ($100-150M addition) vs historical 6-8% range

- Influenced by weaker seasonal hiring, lower CPI-price increases, erosion in buy-side/sell-side ASV

- Any further deceleration below 4% would confirm secular growth concerns

Competitive Threats from Google Finance AI 🤖

Google rolled out AI-driven "Deep Search" in November 2025 powered by Gemini models:

- Democratizes sophisticated financial research at lower/free cost

- Could pressure FDS client acquisition in mid-market segment

- Forces incumbents to innovate and adjust pricing strategies

Market Share vs Bloomberg Terminal 📊

FDS operates in highly concentrated $20B+ market:

- Bloomberg: 33-35% market share, dominant player at $27,660/year pricing

- FactSet: 4.5-22.5% market share at $12,000/year (estimates vary)

- Bloomberg maintains massive moat via network effects and workflow lock-in

- FDS struggles to displace Bloomberg on sell-side trading desks and in fixed income

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming December 18th earnings catalyst, here are the scenarios through December 19th expiration:

📈 Bull Case (35% probability)

Target: $295-$310

How we get there:

- 💪 Earnings beat expectations: Revenue toward $580M+ (high-end), EPS $4.50+ (beat by $0.10+)

- 🚀 Organic ASV growth surprises: 5-6% growth rate vs feared deceleration, driven by AI product adoption

- 💵 Free cash flow recovery: Working capital headwinds resolved, FCF back above $100M for quarter

- 🤝 Arcesium partnership traction: Management provides bullish commentary on pipeline, early customer interest exceeding expectations

- 📈 Q2 guidance raises full-year outlook: Adjusted EPS guidance raised from $16.90-$17.60 to $17.20-$17.80 range

- 👥 Client retention remains stellar: 91%+ retention maintained, user seat expansion accelerating

- 💰 Buyback execution confirmed: Management discloses aggressive share repurchases at $250-$280 range

Key metrics needed for bull case:

- Organic ASV: +5-6% YoY (vs feared 4% floor)

- Client count: +50-75 net new clients in quarter

- Adjusted operating margin: 35.5%+ (showing operating leverage)

- Data center segment growth: 6-8% YoY

Technical path to $295-$310:

- ✅ Gap up through $280 resistance on earnings beat

- ✅ Break above $290 gamma resistance triggers dealer buying (gamma squeeze potential)

- ✅ $300 becomes next target as momentum builds

- ✅ Implied move upper range at $301.47 provides psychological ceiling to break

Probability assessment: 35% because requires solid earnings beat PLUS positive forward guidance in environment where expectations are low. The $290 call strike becomes profitable above ~$298-299, requiring 7-8% earnings day move. Historical FDS moves average 5-7%, but the -44% YTD decline and low positioning create setup for above-average move.

Call buyer's P&L in bull case:

- Stock at $300: Calls worth $10.00, profit = ~$1.33/share × 1,500 = ~$200K gain (15% ROI)

- Stock at $310: Calls worth $20.00, profit = ~$11.33/share × 1,500 = ~$1.7M gain (131% ROI!)

- Stock at $295: Calls worth $5.00, profit = -$3.67/share × 1,500 = -$550K loss (42% loss)

🎯 Base Case (45% probability)

Target: $270-$290 range (MEET EXPECTATIONS, LIMITED MOVE)

Most likely scenario:

- ✅ Solid but unspectacular earnings: Revenue ~$574-576M, EPS $4.35-4.42 (in-line to slight beat)

- ⚖️ ASV growth in-line: Organic ASV +4.5-5.0% (meets low-end guidance, doesn't excite)

- 📊 Guidance maintained: Fiscal 2026 adjusted EPS $16.90-$17.60 reiterated (no raise, no cut)

- 💵 Free cash flow modestly improved: $70-80M for quarter (better than Q1 but not great)

- 🤝 Arcesium commentary positive but vague: "Early innings, seeing strong interest" without specifics

- 📉 Post-earnings profit-taking: Initial gap toward $285-290 followed by fade back to $275-280

- ⏰ Implied volatility crush: Options premiums collapse 40-50% post-earnings regardless of direction

- 🔄 Consolidation continues: Stock trades in $270-$290 range through year-end, waiting for next catalyst

Why 45% probability: This is the "nothing changes" scenario - FDS delivers what's expected but doesn't provide catalyst for major re-rating. Stock has been consolidating $260-$280 for months; one in-line quarter won't change that pattern. The challenge for the call buyer is that even a modest move to $285-288 may not overcome the implied volatility crush and time decay.

Call buyer's P&L in base case:

- Stock at $285: Calls worth $0-2.00, loss = -$6.67 to -$8.67/share × 1,500 = -$1M to -$1.3M (77-100% loss)

- Stock at $288: Calls worth $0-3.00, loss = -$5.67 to -$8.67/share × 1,500 = -$850K to -$1.3M (65-100% loss)

- Stock at $290: Calls worth $0-5.00, loss = -$3.67 to -$8.67/share × 1,500 = -$550K to -$1.3M (42-100% loss)

Reality: This scenario is BRUTAL for the call buyer. Even if stock ends right at the $290 strike, time decay and IV crush mean the calls could expire nearly worthless. Need stock ABOVE $298-299 to breakeven.

📉 Bear Case (20% probability)

Target: $250-$270 (EARNINGS DISAPPOINT)

What could go wrong:

- 😰 Earnings miss or weak guidance: Revenue below $570M, EPS miss by $0.05+, or guidance cut

- 🚨 ASV growth disappoints: Organic ASV growth decelerates to 3-4% range, confirming secular headwinds

- 💸 Free cash flow concerns persist: FCF remains weak at $50-60M, raising dividend/buyback sustainability questions

- 🤔 Arcesium partnership overhyped: Management provides minimal detail, market realizes revenue contribution is years away

- 🇨🇳 China exposure mentioned as headwind: 15-20% revenue exposure cited as drag on growth

- 📊 Client metrics deteriorate: Retention slips to 89-90% or client count growth stalls

- 💰 Conservative Q2 outlook: "Cautious" commentary on macro environment and enterprise IT spending

- 🔨 Break below $270 support triggers cascade: Gamma support at $270 fails, momentum accelerates to $260 then $250

Critical support levels:

- 🛡️ $270: Immediate gamma floor (0.171B) - MUST HOLD or sentiment shifts very bearish

- 🛡️ $260: Major support (0.090B gamma) + institutional accumulation zone - likely buying here

- 🛡️ $250: 52-week low area (0.092B gamma) - disaster scenario, near October 2025 low of $250.50

Probability assessment: Only 20% because FDS fundamentals remain solid (91% retention, growing ASV, $400M buyback, Arcesium partnership) despite sentiment challenges. The bar for earnings is LOW after -44% decline - management would need to materially disappoint to trigger further selloff. However, any signs of secular deceleration (ASV growth <4%, retention slipping, weak guidance) could extend the bear market.

Call buyer's P&L in bear case:

- Stock at $270: Calls expire worthless, loss = -$8.67/share × 1,500 = -$1.3M (100% loss)

- Stock at $260: Calls expire worthless, loss = -$8.67/share × 1,500 = -$1.3M (100% loss)

- Stock at $250: Calls expire worthless, loss = -$8.67/share × 1,500 = -$1.3M (100% loss)

💡 Trading Ideas

🛡️ Conservative: Wait for Post-Earnings Clarity

Play: Stay on sidelines until after December 18th earnings volatility settles

Why this works:

- ⏰ Binary catalyst in 14 days: Earnings create unpredictable gap-up or gap-down risk

- 💸 Options extremely expensive: Implied volatility elevated at 8.26% expected move - premiums rich pre-earnings

- 📊 Better entry likely post-earnings: Historical pattern shows stocks often consolidate or pullback even after beats

- 🎯 IV crush reduces costs: Option premiums typically drop 40-50% after earnings as uncertainty resolves

- 🤔 The $1.3M call buyer could be wrong: Even smart money loses on binary events - don't blindly follow

Action plan:

- 👀 Watch December 18 earnings closely: Focus on organic ASV growth, client retention, free cash flow, and guidance quality

- 🎯 Look for pullback entry: If stock gaps to $290-295 on earnings beat then pulls back to $280-285, that's a lower-risk entry for stock position

- ✅ Need confirmation: See positive Arcesium commentary, AI product traction, and buyback execution before committing capital

- 📊 Monitor analyst reactions: Upgrades and price target raises post-earnings would signal sentiment inflection

- ⏰ Revisit in January 2026: Q2 earnings in March will provide next major catalyst with more AI product data

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 5-10% drawdown if earnings disappoint. If earnings beat, can enter at better levels post-IV crush. Maintain optionality and protect capital.

⚖️ Balanced: Post-Earnings Bull Put Spread (Income Play)

Play: After earnings, sell bull put spread to collect premium with defined risk

Structure: Sell $270 puts, Buy $260 puts (January 16 expiration)

Why this works:

- 🎢 IV crush makes premium collection attractive: Post-earnings, put premiums elevated but declining - optimal time to sell

- 📊 Defined risk: $10 wide spread = $1,000 max risk per spread

- 🎯 Targets gamma support zone: $270 gamma support (0.171B) provides technical floor

- 💰 Income generation: Collect $2-3 net credit per spread (~$200-300 profit if FDS stays above $270)

- ⏰ 33 days to expiration: Sufficient time for thesis to work, theta decay in your favor

- 🛡️ Bullish but not aggressive: Benefits from stock staying flat-to-up, don't need explosive rally

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Collect: ~$2-3 credit per spread ($200-300 collected)

- 📈 Max profit: $200-300 if FDS above $270 at January expiration (keep entire credit)

- 📉 Max loss: $700-800 if FDS below $260 (defined and limited to spread width minus credit)

- 🎯 Breakeven: ~$267-268

- 📊 Probability of profit: ~60-65% based on $270 support and current price levels

Entry timing:

- ⏰ Wait 2-3 days post-earnings: Let IV fully collapse by December 19-20

- 🎯 Only enter if stock above $275: Need cushion between current price and short strike

- ❌ Skip if stock gaps below $265: Spread too close to at-the-money, risk/reward unfavorable

Position sizing: Risk only 3-5% of portfolio (defined risk but still directional bet on support holding)

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

Why this is better than buying calls: Theta decay works FOR you instead of against you. Don't need explosive rally - just need stock to not collapse. Much higher probability of profit than long calls.

🚀 Aggressive: Earnings Straddle - Bet on BIG MOVEMENT (EXPERT ONLY!)

Play: Buy straddle betting on post-earnings volatility EXCEEDING 8.26% implied move

Structure: Buy $280 calls + Buy $280 puts (December 19 expiration)

Why this could work:

- 💥 Implied move may underestimate: 8.26% implied move seems conservative given -44% YTD decline and major catalysts

- 🎰 Betting market is UNDERPRICING volatility: Historical FDS moves 5-7%, but this setup has potential for 10-12% move either direction

- 📊 Stock at major inflection point: Either sentiment shifts positive (Arcesium, AI products, buybacks) OR secular decline confirmed

- 🚀 Arcesium partnership expectations: Market may be underestimating significance of December 3rd announcement - guidance could surprise

- ⚡ Only need 9-10% move to profit: Breakeven ~$255-$260 downside or ~$300-$305 upside

- 📈 Gamma positioning creates explosive potential: Heavy $280-$290 gamma could trigger acceleration on breakout

Why this could blow up (SERIOUS RISKS - READ THIS!):

- 💸 EXPENSIVE: Straddle costs ~$22-25 ($2,200-2,500 per straddle) - that's 8-9% of stock price!

- ⏰ TIME DECAY DEVASTATION: Theta burns -$80-100/day as earnings approaches - paying for volatility is VERY expensive

- 😱 IV CRUSH MASSACRE: Even if stock moves 6-7%, IV collapse from 40% to 20% could still result in LOSS on both legs

- 📊 Two-way risk: Stock could stay in $270-$285 range and you lose ENTIRE premium ($2,200-2,500)

- 🎢 Need 10%+ move to breakeven: After IV crush factored in, need move LARGER than implied move just to breakeven

- ⚠️ In-line earnings = total loss: "Good but not great" scenario where stock goes to $285 = lose 60-80% of premium

- 💀 Historical precedent against you: FDS typically moves 5-7% on earnings, NOT 10-12%

Estimated P&L:

- 💰 Cost: ~$22-25 per straddle (using Dec 19 expiration for 1-day post-earnings window)

- 📈 Profit scenario: Stock moves to $305+ or $255- (10%+ move) = $20-30 gain (80-120% ROI)

- 🚀 Home run: Stock moves to $320 or $240 (15%+ move) = $35-40 gain (140-160% ROI)

- 📉 Loss scenario: Stock ends $270-$290 range = lose $12-20 (50-80% loss)

- 💀 Total loss: Stock flat at $280 = lose entire $22-25 (100% loss)

Breakeven points:

- 📈 Upside breakeven: ~$302-305 (need 9-10% rally)

- 📉 Downside breakeven: ~$255-258 (need 8-9% drop)

CRITICAL WARNING - DO NOT ATTEMPT UNLESS YOU:

- ✅ Have traded straddles through earnings multiple times and understand IV crush mechanics intimately

- ✅ Can afford to lose ENTIRE premium (very real possibility - this is SPECULATION not investment)

- ✅ Understand you're betting AGAINST market's probability assessment (implied move suggests 8.26%, you need 10%+)

- ✅ Can monitor position Thursday morning post-earnings and take profits QUICKLY if it works

- ✅ Accept that even if RIGHT on direction, IV crush could cause loss (stock to $285 on "in-line" = lose money)

- ⏰ Plan to close position within 24 hours post-earnings (don't hold to December 19 expiration - theta will destroy you)

- 💰 Position size is <2% of portfolio (this is a LOTTERY TICKET trade)

Risk level: EXTREME (can lose 100% of premium easily) | Skill level: Expert only

Probability of profit: ~35-40% (lower than 50% due to IV crush dynamics and need for larger-than-expected move)

Why I'm even mentioning this: The setup IS interesting - FDS down 44%, major catalysts, low positioning. But straddles are BRUTAL on retail traders who don't understand IV crush. I'm including this to EDUCATE about the mechanics, not to recommend it. Unless you're an experienced options trader who's lost money on earnings straddles before and learned the lesson, SKIP THIS.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Binary earnings catalyst in 14 days: December 18th earnings before open create MASSIVE single-day volatility risk. Stock could gap 5-10% either direction based on organic ASV growth (4% vs 6% makes huge difference), free cash flow quality ($60M vs $90M changes narrative), and Arcesium partnership commentary. Historical FDS post-earnings moves range 3-7%, but this -44% YTD decline setup could produce 8-12% move. Options pricing 8.26% implied move but actual result could be larger or smaller.

-

💸 Implied volatility crush DESTROYS premium: Pre-earnings IV inflates option prices significantly. Even if you're RIGHT on direction, the post-earnings collapse in IV (typically 40-50% decline) can result in losses. For example, stock could rally from $279 to $288 (+3.2%) but your $290 calls still lose 50%+ value due to IV dropping from 40% to 20%. This is the OPTIONS TRAP that kills most retail traders on earnings plays.

-

👔 New CEO execution uncertainty: Sanoke Viswanathan became CEO September 2025 with background in banking operations, not financial data/SaaS. Conservative fiscal 2026 guidance ($16.90-$17.60 adjusted EPS) fell below expectations. December 18 earnings will be first full quarter under new leadership - ANY stumbles in communication, metrics, or guidance could trigger selloff. Prior CEO Phil Snow's advisory role ends December 2025, removing institutional knowledge safety net.

-

📉 ASV growth secular deceleration risk: Organic ASV growth decelerated to 4.1% in Q2 FY2025 vs 5.1% consensus. Fiscal 2026 guidance targets 4-6% growth vs historical 6-8% range. ANY further deceleration below 4% would confirm structural headwinds (pricing pressure, competition, market share loss) and invalidate "this is just a temporary pause" thesis. Market is giving FDS benefit of doubt - one bad quarter breaks that faith.

-

💵 Free cash flow volatility unresolved: Q1 FY2026 free cash flow collapsed 56.4% YoY to $60.5M from $138.7M due to working capital timing and AI platform investments. If Q2 shows similar weakness, raises SERIOUS questions about dividend sustainability ($4.40/year = $164M annually) and buyback program execution ($400M authorized). Cash generation is the FOUNDATION of FDS value proposition - cracks here would be devastating.

-

🤖 Google Finance AI competitive threat: Google rolled out AI-driven "Deep Search" in November 2025 powered by Gemini models, offering sophisticated financial research at low/free cost. This democratization of financial analysis threatens FDS's mid-market customer base (startups, smaller asset managers). FDS charges $12,000/year vs Bloomberg's $27,660 - but if Google offers comparable functionality free, FDS could face pricing pressure and churn acceleration. Bloomberg has brand/network effects moat; FDS in the "squeezed middle."

-

📊 Bloomberg Terminal competitive moat remains MASSIVE: Bloomberg controls 33-35% market share with $27,660/year pricing vs FDS at 4.5-22.5% share with $12,000/year pricing. Bloomberg's dominance in fixed income and sell-side trading desks creates powerful network effects - traders NEED Bloomberg to see where liquidity is. FDS favored by buy-side equity analysts but struggles to displace incumbent. The TAM FDS can realistically address may be smaller than bulls assume.

-

🤝 Arcesium partnership expectations potentially TOO HIGH: Market may be pricing in immediate revenue contribution from December 2025 announcement. Reality: enterprise software sales cycles are 12-18+ months, especially for mission-critical back-office systems. Meaningful revenue contribution likely not until FY2027. If management provides vague "early stages" commentary without specific customer wins or pipeline metrics, the "catalyst" could fizzle. The $210B private credit TAM is real, but FDS has to WIN deals against entrenched competitors.

-

🎢 December 19 expiration gives ZERO margin for error: This $1.3M call trade expires ONE DAY after earnings. There's no time for "stock to recover from initial selloff" or "market to digest and re-rate." It's purely a gap-up play. If FDS gaps to $285 on earnings (good but not great), these calls could still expire worthless due to time decay. The call buyer needs IMMEDIATE explosive move to $295-300+ to profit - that's a 6-8% gap which is above historical average.

-

💰 $400M buyback at current prices NOT YET CONFIRMED ACTIVE: While authorized September 2025, we don't know execution pace. Prior program bought at $419 average - management may be waiting for sub-$260 levels rather than $279. If Q1 FY2026 earnings show minimal buyback activity, signals lack of management conviction at these "cheap" levels. That would be VERY bearish signal.

-

🇨🇳 China exposure remains wildcard: FDS derives 15-20% revenue from China region historically. Geopolitical tensions, economic slowdown, and competitive threats from domestic providers (Wind Information, Eastmoney) create revenue risk. Any negative commentary on China trends would pressure estimates.

-

📉 Macro environment deteriorating: Financial data spending is highly correlated with capital markets activity (IPOs, M&A, hedge fund launches). If macro conditions worsen in Q1 2026 (recession fears, market volatility), enterprise IT budgets get cut and seat expansion stalls. FDS at current valuation has ZERO recession protection priced in.

-

🎯 The $290 strike sits at MAXIMUM gamma resistance: With 0.293B call gamma at $290 (highest level on board), market makers will SELL shares into any rally approaching $290 to hedge their short call exposure. This creates mechanical resistance. Breaking through $290 requires sustained institutional buying to overcome dealer hedging - not easy.

-

🐋 Smart money could be wrong: Just because someone spent $1.3M on calls doesn't mean it's a good trade. Institutional traders make bad bets all the time, especially on binary events. The call buyer could have information we don't (positive insider knowledge), OR they could simply be wrong about earnings impact. Don't assume "follow the smart money" is a winning strategy on binary catalysts.

🎯 The Bottom Line

Real talk: Someone just spent $1.3 MILLION betting that FDS rebounds sharply after December 18th earnings, targeting $290+ within 24 hours of the report. This is an AGGRESSIVE, high-conviction bet on a beaten-down stock (-44% from highs) showing signs of fundamental inflection.

What this trade tells us:

- 🎯 Sophisticated player sees asymmetric opportunity: Risk $1.3M to make potentially $2-4M+ if thesis works (stock to $300-310)

- 💰 They believe earnings will BEAT and guidance will RAISE: Otherwise this trade makes no sense - need major positive catalyst

- ⚖️ December 19 expiration = pure earnings play: No time for slow recovery - betting on immediate gap-up reaction

- 📊 Strike at $290 = maximum gamma level: Positioned exactly where dealer hedging could trigger acceleration if broken

- ⏰ Timing right before Arcesium partnership commentary: Management could provide unexpectedly bullish update on December 3rd deal

This is NOT a "blindly follow" signal - it's a "pay attention, something interesting brewing" signal.

If you own FDS stock:

- ✅ Hold through earnings if long-term investor: Fundamentals remain solid (91% retention, $2.37B ASV, Arcesium partnership, $400M buyback)

- 📊 Consider selling covered calls: If you believe stock stays below $290, sell $290 calls against shares to collect premium

- 🎯 Set mental stop at $260-265: If earnings badly disappoint, protect remaining capital by exiting below major support

- 💰 Take partial profits if gap to $295+: Lock in gains on any explosive post-earnings rally; can always re-enter

- 🛡️ Don't panic sell pre-earnings: The setup is actually decent - low expectations, major catalysts, insider buying at $252

If you're watching from sidelines:

- ⏰ December 18th before market open is the moment: DO NOT enter new positions until after earnings volatility

- 🎯 Post-earnings entry opportunity: If stock gaps to $295-300 on beat then pulls back to $285-290, that's attractive entry

- 📈 Looking for confirmation: Need to see organic ASV +5%+, free cash flow recovery, Arcesium traction, positive guidance

- 🚀 Longer-term (6-12 months): AI product rollout, Hebbia partnership, and Arcesium integration are legitimate catalysts for $320-350+ if execution delivers

- ⚠️ Current setup requires PERFECT earnings: At 8.26% implied move, need significant beat to justify entry at current levels

If you're considering options trades:

- 🎯 DON'T buy pre-earnings calls: IV is inflated, time decay brutal, and IV crush will destroy premium even on wins

- 📊 DON'T attempt straddles unless expert: This is one of the most retail-trader-killer strategies on earnings

- ⚖️ CONSIDER post-earnings bull put spreads: Sell $270/$260 put spread AFTER earnings to collect premium with defined risk

- ⏰ Timing is EVERYTHING: Best options risk/reward comes 2-3 days POST-earnings when IV has collapsed

- 💰 Position sizing discipline: Never risk more than 3-5% of portfolio on single binary event

Mark your calendar - Key dates:

- 📅 December 18 (Wednesday) before market open - Q1 FY2026 earnings report (14 DAYS!)

- 📅 December 18 at 9:00 AM ET - Earnings conference call with Q&A

- 📅 December 18 - Quarterly dividend payment of $1.10 per share

- 📅 December 19 (Thursday) - Post-earnings price action, December monthly OPEX, this $1.3M call trade expires

- 📅 January 16, 2026 - Monthly OPEX (next major options expiration)

- 📅 March 2026 - Q2 FY2026 earnings (next quarterly catalyst)

- 📅 Q2-Q3 2026 - AI product rollout (Mercury, Pitch Creator) and Arcesium partnership initial traction

Final verdict: FDS's medium-term story remains COMPELLING - Arcesium partnership addressing $210B+ private credit market, AI product launches, $400M buyback at attractive prices, and 91% client retention demonstrate business resilience despite CEO transition. BUT, the December 18th earnings is a BINARY catalyst that could gap stock 5-10% either direction. The $1.3M call buyer is making an aggressive bet on positive surprise - that setup is INTERESTING but requires perfect execution.

For most investors: Wait for post-earnings clarity. If earnings beat and stock gaps to $285-295, THAT'S your entry point for a position. Let the call buyer take the binary risk; you take the lower-risk follow-through trade.

Be patient. Let the catalyst clear. The financial data analytics market will still be a $20B+ TAM next month, and you'll sleep better entering at $285 with confirmation than $279 with uncertainty. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 279x unusual score reflects this specific trade's size relative to recent FDS history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for 5-10% gaps either direction. The December 19th expiration gives ZERO room for error - this is pure speculation on immediate post-earnings reaction. IV crush can cause losses even if directionally correct.

About FactSet Research Systems: FactSet aggregates financial data from multiple sources including third-party suppliers, news outlets, and exchanges into integrated workstations, delivering portfolio analytics solutions primarily to buy-side clients including wealth and corporate entities, with a market cap of $10.45 billion in the Computer Programming & Data Processing industry.