🛡️ FISV $3M LEAP Put - Big Money Betting on Extended Downside After Historic Crash!

📅 February 17, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $3 MILLION on FISV puts with an 11-month expiration - this is a LEAP, not a quick trade! With FISV already down 74% from its March 2025 highs after that catastrophic 44% single-day crash in October, this trader is betting the pain isn't over. The Z-score of 66.42 means this is EXTREMELY UNUSUAL - roughly 66 standard deviations from normal activity. Translation: Institutional money sees more downside ahead even at these battered levels.

📊 Company Overview

Fiserv, Inc. (FISV) is a leading fintech powerhouse providing core banking technology and payment processing services:

- Market Cap: $31.9 Billion (down from ~$76B at 2025 peak)

- Industry: Business Services (Financial Technology)

- Current Price: $63.66 (near 52-week low of $57.79)

- Employees: 38,000

- Headquarters: Milwaukee, WI

- Primary Business: Core processing for banks/credit unions, Clover POS systems, merchant services, digital payments

💰 The Option Flow Breakdown

The Tape (February 17, 2026 @ 14:18:06):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 14:18:06 | FISV | ASK | BUY | PUT $70 | 2027-01-15 | $3M | $70 | 2K | 681 | 2,000 | $63.66 | $15.00 |

🤓 What This Actually Means

This is a long-term bearish bet with 11 months of runway. Here's what's happening:

- 💸 Massive premium paid: $3M ($15.00 per contract x 2,000 contracts)

- 📈 Already in-the-money: Strike at $70 vs current price $63.66 - these puts have $6.34 intrinsic value already!

- ⏰ LEAP structure: January 2027 expiration = 11 MONTHS to work. This isn't speculation - this is a thesis trade.

- 📊 Size dominates: Volume of 2,000 vs Open Interest of 681 = 2.9x the existing open interest. This trader just TRIPLED the market.

- 🏦 Classification: BTO (Buy to Open) Long Put - directional bearish bet, NOT hedging

What's really happening here:

This trader believes FISV has MORE downside even after crashing 74% from March 2025 highs. The LEAP structure (11 months) tells us this isn't about a quick earnings miss - they're betting on structural problems that will take quarters to play out. With the $70 strike already in-the-money, they're starting with a 10% cushion and betting the stock breaks below $55 (their breakeven = $70 strike - $15 premium).

Why a LEAP instead of short-dated puts?

LEAP puts give institutional traders time to be right. Instead of betting on THIS earnings report, they're betting the turnaround CEO Mike Lyons is promising won't materialize, or that the $3.5B securities lawsuit drags on, or that Clover keeps losing share to Toast and Square. When big money goes LONG-DATED bearish, they're saying "I have conviction this company is in trouble for QUARTERS, not days."

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-score: 66.42) - This means the trade is approximately 66 standard deviations above normal volume for this contract. For context, a Z-score above 3.0 is considered highly unusual. A Z-score of 66? That's the kind of conviction-driven institutional activity we see maybe a handful of times per quarter across all tickers.

📈 Technical Setup / Chart Check-Up

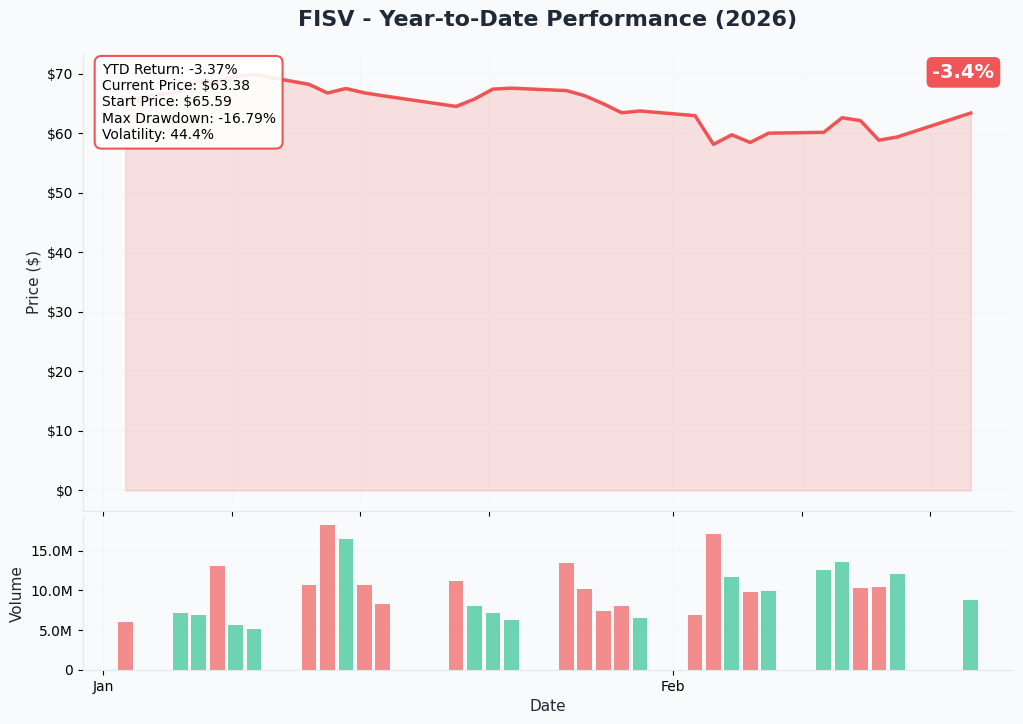

YTD Performance Chart

FISV has been absolutely crushed - down approximately 74% from its March 2025 high of $238.59 to current levels around $63.66. The chart tells a brutal story:

Key observations:

- 💥 Catastrophic October 29, 2025 crash: Single-day 44% drop erased $45B market cap on Q3 earnings disaster

- 📉 No recovery bounce: Unlike typical oversold situations, FISV has continued drifting lower since October

- 🔻 Near 52-week lows: Current price of $63.66 sits just above February 3rd low of $57.79

- 📊 Jana Partners pop (today): Stock jumped 6.5% on activist investor news, but LEAP buyer still betting bearish

- ⚠️ Death spiral pattern: Lower highs since October suggest sellers in control at every rally attempt

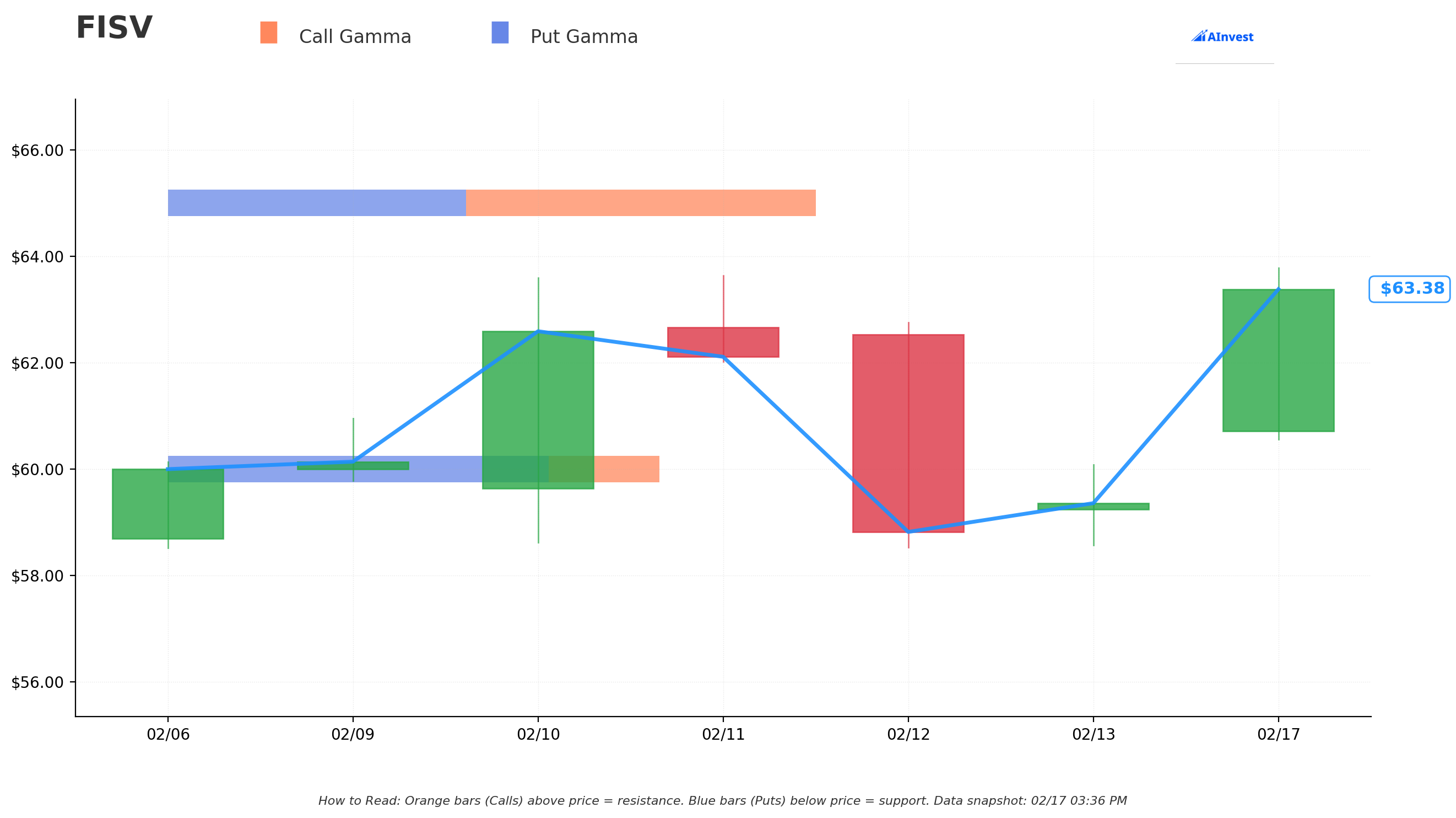

Gamma-Based Support & Resistance Analysis

Current Price: $63.66

The gamma exposure map reveals where options market makers will create natural buying/selling pressure:

🔵 Support Levels (Put Gamma Below Price):

- $62 - Immediate support with 0.03 total gamma exposure (very weak floor!)

- $61 - Secondary support at 0.07 gamma

- $60 - MAJOR structural floor with 8.83 total gamma (STRONGEST PUT GAMMA - this is key!)

- $59 - Additional support at 0.08 gamma

- $57.50 - Deep support at 0.03 gamma

- $55 - Extended floor with 2.05 gamma (the LEAP buyer's probable target zone)

🟠 Resistance Levels (Call Gamma Above Price):

- $64 - Immediate ceiling with 0.09 gamma (very weak)

- $65 - Secondary resistance at 11.52 gamma (STRONGEST LEVEL - major ceiling!)

- $70 - Heavy resistance at 6.77 gamma (exactly where this put is struck!)

- $75 - Extended ceiling at 1.61 gamma (unlikely without major catalyst)

What this means for traders:

FISV is trapped in a tight range with massive $65 resistance overhead (11.52 gamma - the strongest level on the chart) and $60 support below (8.83 gamma). The $70 strike where this put is positioned coincides with 6.77 gamma resistance - meaning market makers are positioned heavily there. Breaking above $65 will be DIFFICULT; breaking below $60 opens the floodgates toward $55.

Notice anything? The LEAP put buyer struck at $70 - exactly at a major gamma resistance level. They're betting that NOT ONLY will FISV fail to reclaim $70 (10% above current), but that it will break down through $60 support and head toward $55 or lower. The 11-month timeframe gives them plenty of runway to wait for the breakdown.

Net GEX Bias: Slightly Bullish (21.1B call gamma vs 19.9B put gamma) - but don't be fooled. The positioning is concentrated at key levels ($65 resistance, $60 support), creating a compression zone that will eventually break one direction or the other.

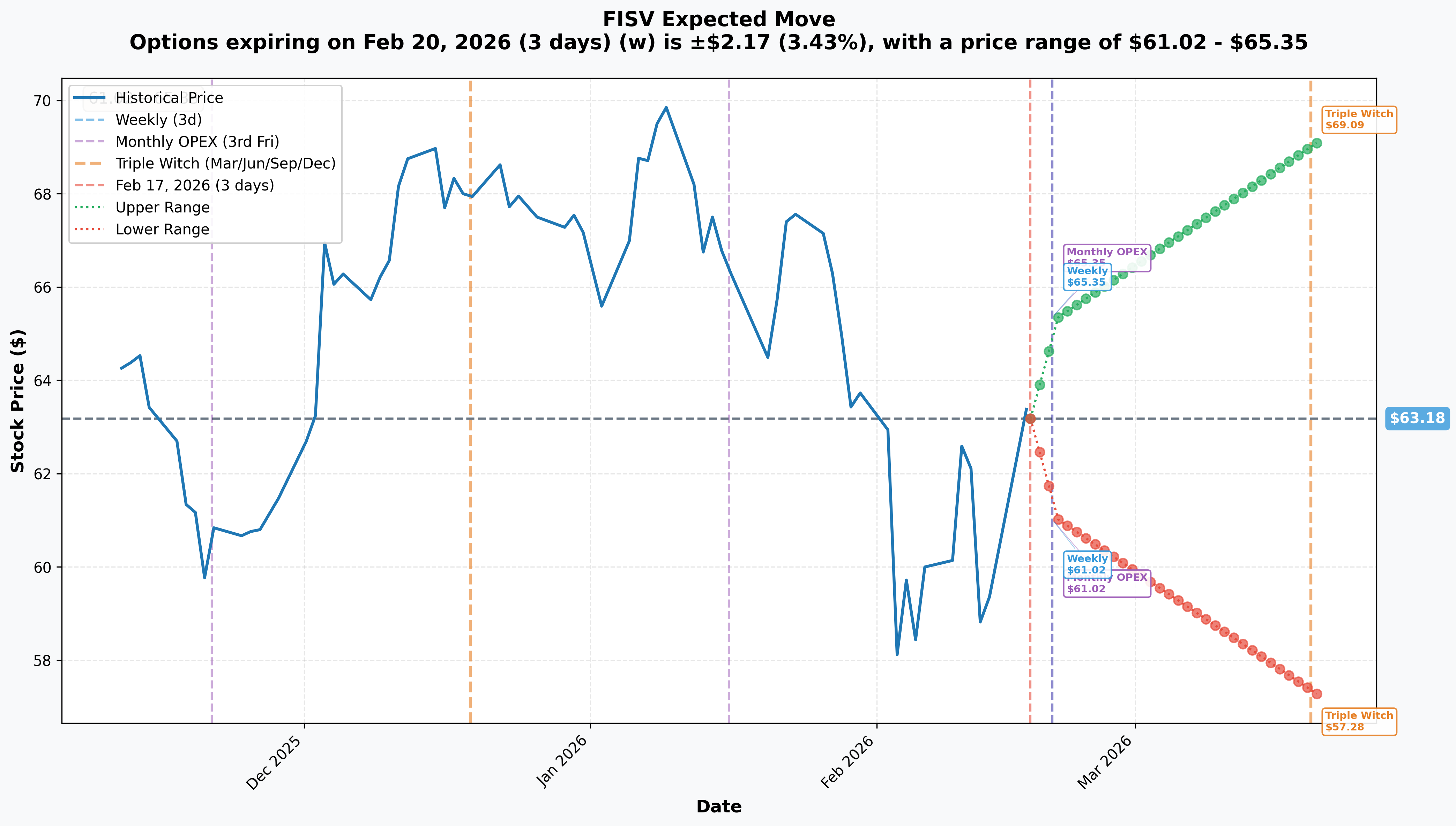

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Feb 20 - 3 days): ±$2.17 (±3.43%) → Range: $61.02 - $65.35

- 📅 Monthly OPEX (Feb 20 - 3 days): ±$2.17 (±3.43%) → Range: $61.02 - $65.35

- 📅 Triple Witch (Mar 20 - 31 days): ±$5.91 (±9.35%) → Range: $57.28 - $69.09

Translation for regular folks:

Options traders expect FISV to stay in a relatively tight 3.4% range through this week's expiration, but the March quarterly expiration implies a potential 9.4% move. That's a much wider expected range ($57.28 to $69.09) as the market prices in uncertainty around Q1 earnings (late April) and the May 14 Investor Day.

The LEAP put buyer is looking way beyond these near-term timeframes. Their January 2027 expiration gives them runway through:

- Q1 2026 earnings (April)

- Investor Day (May 14, 2026) - critical catalyst for turnaround thesis

- Q2 earnings (late July)

- Mid-2026 margin improvement expectations

- Q3 earnings (October)

- Full year 2026 outlook

Key insight: The LEAP buyer is betting that the "One Fiserv" turnaround simply won't work, and that 11 months from now the stock will be materially lower despite management's promises. At $55 breakeven, they need another 13.5% downside to profit.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened)

Q3 2025 Earnings Disaster - October 29, 2025 💥

This was the day everything changed. FISV crashed 44% in a single session - its worst day EVER:

- 😱 EPS: $2.04 vs $2.64 consensus (22.7% miss!)

- 💸 Revenue: $4.9B vs ~$5.3B expected (8% miss)

- 📉 Organic growth: Just 1% vs 10%+ previously guided

- ⚠️ Guidance slashed: Full year EPS cut to $8.50-$8.60 from $10.15-$10.30

- 💔 Root cause: Argentina business that drove 10 percentage points of 2024's growth completely evaporated

Q4 2025 Earnings - February 10, 2026 📊

Mixed results that beat low expectations but showed continued margin pressure:

- ✅ EPS beat: $1.99 vs $1.90 consensus (+4.7%)

- ❌ Revenue flat: Organic revenue unchanged in Q4

- 📉 Margin compression: Adjusted operating margin fell to 34.9% from 42.9% (800 basis points!)

- 💸 Free cash flow decline: $4.44B vs $5.23B prior year (-15%)

Jana Partners Activist Stake - February 17, 2026 (TODAY!) 📰

Breaking news that sparked today's 6.5% rally:

- 🦈 Activist hedge fund Jana Partners disclosed a stake in Fiserv

- 🎯 Pushing for strategic review and focus on core banking franchise

- 🤝 Supporting CEO Mike Lyons' turnaround efforts

- 📈 Stock popped on the news - but the LEAP put buyer STILL bought bearish at these higher prices

Strategic Partnerships (Recent)

- 🤝 Mastercard partnership expansion for "agentic commerce" (January 2026)

- 🤖 Microsoft AI collaboration deploying Copilot (January 2026)

- 🇯🇵 Sumitomo Mitsui partnership bringing Clover to Japan (late 2026)

🚀 Upcoming Catalysts

Q1 2026 Earnings - Expected April 23-28, 2026 📅

This will be critical for the turnaround narrative:

- 📊 Consensus Revenue: ~$4.76 billion

- 💰 Consensus EPS: $1.67

- ⚠️ Management warning: Guided to "low single digit" adjusted revenue DECLINE in H1 2026

- 🎯 Key watch: Organic revenue trends, client retention, margin trajectory

Investor Day - May 14, 2026 (NEW YORK CITY) 🎯

This is THE catalyst that will make or break the turnaround story:

- 📈 Expected to detail "One Fiserv" turnaround progress

- 🎯 Updated long-term financial targets

- 🚀 Clover growth roadmap and international expansion

- 🤖 AI strategy presentation

- ⚠️ If they disappoint here, the stock could retest October lows

Multi-Site Resiliency Completion - Mid-2026 🔧

- Adding redundancy across payment platforms

- On track per CEO Lyons

- Addresses cybersecurity lawsuit concerns

Clover Japan Launch - Late 2026 🇯🇵

- Partnership with Sumitomo Mitsui

- Supports Japan's 65% cashless payments goal by 2030

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, catalysts, and the LEAP put positioning, here are the scenarios through January 2027:

📈 Bull Case (20% probability)

Target: $80-$90

How we get there:

- ✅ Jana Partners activism succeeds in unlocking value through strategic actions

- 📈 "One Fiserv" turnaround delivers better-than-expected results by Q3 2026

- 💪 Clover international expansion (Japan, Canada) gains traction

- 📊 Margins recover toward 38-40% by H2 2026 as promised

- 🎯 May 14 Investor Day provides compelling long-term targets

- ⚖️ $3.5B securities lawsuit settles for manageable amount

- 🚀 Breakout above $65 gamma resistance triggers technical rally toward $70, then $75-80

- 📈 Multiple expansion from 10x P/E to 12-14x on improved outlook

Probability assessment: Only 20% because it requires multiple things to go RIGHT after a year of everything going WRONG. The LEAP put buyer clearly doesn't believe this scenario - they're betting $3M against it.

🎯 Base Case (45% probability)

Target: $55-$68 (RANGE-BOUND GRIND)

Most likely scenario:

- ⚖️ Mixed quarterly results - some beats, some misses

- 📊 Slow turnaround progress - "transition year" as management calls it

- 🔄 Trading between $60 support and $65 resistance for months

- 🤔 Jana Partners activism creates some value but no dramatic changes

- ⏰ Market waits for proof that turnaround is working

- 💤 Volatility settles as "show me" mode takes over

- 📉 Stock drifts toward $60 support, bounces, fails at $65, repeat

LEAP put P&L in base case: At $60 by January 2027, puts worth $10.00, loss = -$5.00/share x 2,000 = -$1M (33% loss). The put buyer needs MORE than base case to profit.

📉 Bear Case (35% probability)

Target: $45-$55 (BREAKDOWN BELOW SUPPORT)

What could go wrong:

- 😰 Q1 2026 earnings show organic revenue declining faster than expected

- 🔻 May Investor Day fails to inspire confidence - turnaround questioned

- ⚖️ $3.5B securities lawsuit progresses toward trial, creating uncertainty

- 🔓 Additional cybersecurity incidents emerge (lawsuits ongoing)

- 📉 Clover loses share to Toast (26% TPV growth vs Clover's 14%) and Square

- 💸 Margin recovery fails to materialize - stuck at 34% operating margin

- 🏦 Financial Solutions segment continues declining

- 💥 Break below $60 gamma support triggers cascade to $55, then $50

- 📊 P/E compresses to 6-7x on no-growth outlook

Critical support levels:

- 🛡️ $60: Major gamma floor (8.83 gamma) - MUST HOLD or momentum shifts very bearish

- 🛡️ $57.50: Intermediate support - near 52-week low

- 🛡️ $55: LEAP put buyer's breakeven zone - if stock gets here, they're profitable

- 🛡️ $50: Disaster scenario - would represent 79% decline from 2025 highs

LEAP put P&L in bear case:

- Stock at $55 on Jan 15, 2027: Puts worth $15.00, breakeven (no profit, no loss)

- Stock at $50 on Jan 15, 2027: Puts worth $20.00, profit = $5.00/share x 2,000 = $1M gain (33% ROI)

- Stock at $45 on Jan 15, 2027: Puts worth $25.00, profit = $10.00/share x 2,000 = $2M gain (67% ROI)

Why 35% probability? The stock is already down 74% from highs, but the problems that caused the crash (Argentina revenue loss, margin compression, competitive pressure) haven't been fixed. The turnaround is promised but unproven. The LEAP put buyer clearly assigns meaningful probability to continued deterioration - and they're backing it with $3M.

💡 Trading Ideas

🛡️ Conservative: Wait-and-Watch with Defined Entry

Play: Stay on sidelines until Q1 earnings (late April) provides clarity on turnaround

Why this works:

- ⏰ Too much uncertainty around turnaround execution - let the company prove it

- 📊 May 14 Investor Day is THE critical event - why guess before then?

- 💸 Stock already cheap on paper (10x P/E) but could get cheaper if turnaround fails

- 🦈 Jana Partners involvement is positive but uncertain outcome

- 🎯 Better entry likely after Investor Day if story turns positive ($60-65) or negative ($50-55)

Action plan:

- 👀 Watch Q1 earnings (late April) for organic revenue trends and margin trajectory

- 📅 Mark May 14 Investor Day on your calendar - this is the decision point

- 🎯 If bullish after Investor Day: Buy stock at $60-65 with stop at $55

- 🎯 If bearish after Investor Day: Consider put spreads similar to the LEAP trade

- ❌ Avoid the temptation to "catch the falling knife" before proof of turnaround

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

⚖️ Balanced: Bear Put Spread (Defined Risk Bearish)

Play: Buy put spread to profit if stock drifts lower through H1 2026

Structure: Buy $65 puts, Sell $55 puts (July 2026 expiration)

Why this works:

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 🎯 Targets gamma support zone at $55-60 where breakdown could accelerate

- 🦈 Jana Partners catalyst uncertainty cuts both ways - stock could fade after initial pop

- ⏰ July expiration captures Q1 earnings AND Investor Day reactions

- 💸 Lower cost than outright puts while maintaining bearish exposure

- 📈 Profits if stock at $55 or below by July

Estimated P&L:

- 💰 Pay ~$3-4 net debit per spread (adjust based on current IV)

- 📈 Max profit: $600-700 if FISV below $55 at July expiration

- 📉 Max loss: $300-400 if FISV above $65 (defined and limited)

- 🎯 Breakeven: ~$61-62

Position sizing: Risk only 2-3% of portfolio - this is speculative, not a core holding

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

🚀 Aggressive: Copy the LEAP Structure (Long-Term Conviction Play)

Play: Buy LEAP puts similar to the $3M institutional trade

Structure: Buy January 2027 $65 puts (slightly lower strike for better risk/reward)

Why this could work:

- 🐋 You're following institutional money with high conviction

- ⏰ 11 months gives time for turnaround thesis to fail

- 📊 Captures multiple earnings reports, Investor Day, and full year results

- 🎯 $3.5B lawsuit could progress toward resolution

- 💥 Competitive pressures (Toast, Square) unlikely to ease

- 📉 At $65 strike, you start closer to at-the-money with better leverage

Why this could blow up:

- 💸 EXPENSIVE: LEAPs cost significant premium ($10-12 per contract)

- ⏰ TIME VALUE: Even if stock stays flat, theta decay erodes value

- 🦈 Jana Partners wildcard: Activist involvement could accelerate positive changes

- 📈 Beaten down already: Stock down 74% - much of the bad news may be priced in

- 🚀 Turnaround could work: CEO Lyons is executing, just slowly

Estimated P&L at $65 strike:

- 💰 Cost: ~$10-12 per contract ($1,000-1,200 per contract)

- 📈 Profit scenario: Stock at $50 = put worth $15.00, gain ~$3-5/contract (30-50% ROI)

- 📉 Loss scenario: Stock at $65+ = put expires worthless, 100% loss

- 🎯 Breakeven: ~$53-55

Position sizing: Risk only 1-2% of portfolio maximum - this is a high-conviction speculative bet

Risk level: HIGH (can lose entire premium) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🦈 Jana Partners activism is a wildcard: The activist stake disclosed today could push for changes that unlock value - strategic asset sales, aggressive cost cuts, or even a sale of the company. This is a BULLISH catalyst that the LEAP put buyer is betting against.

-

📈 Stock already down 74% - turnaround could be real: At 10x P/E (decade low), much of the bad news may be priced in. CEO Mike Lyons' "One Fiserv" plan could work if execution improves in H2 2026 as guided. The LEAP put needs the turnaround to FAIL.

-

⚖️ $3.5B securities lawsuit uncertainty: The City of Hollywood Police Officers' Retirement System lawsuit alleges inflated growth metrics. This could settle, go to trial, or drag on for years. A quick settlement could remove overhang; a large judgment could crush the stock further.

-

🔓 Cybersecurity litigation ongoing: Multiple lawsuits including Self-Help Credit Union allege inadequate security practices. Additional incidents could accelerate client losses.

-

📊 Clover competitive pressure: Toast growing 26% vs Clover's 14% in TPV growth. Analyst Ken Suchoski notes Clover's growth may be cannibalization of legacy Fiserv products, not market share gains.

-

💸 Margin compression may be structural: Operating margins fell from 43% to 35% - management guides to 35-36% in H2 2026. If margins don't recover, the stock has limited upside.

-

🎯 May 14 Investor Day is make-or-break: If the company fails to deliver compelling long-term targets and turnaround evidence, the stock could retest October lows near $60 or below.

-

⏰ 11-month time horizon works both ways: The LEAP structure gives time to be right, but also time to be WRONG. A lot can change in 11 months. Early signs of turnaround success could make these puts worthless.

🎯 The Bottom Line

Real talk: An institutional trader just dropped $3 MILLION betting FISV goes LOWER from here - even after a 74% crash from 2025 highs. This isn't a hedge on a long position; it's a directional bearish bet with 11 months of conviction. The Z-score of 66.42 tells us this is extraordinarily unusual activity.

What this trade tells us:

- 🎯 Sophisticated money believes the turnaround will take LONGER than management promises (or fail entirely)

- 💰 They're paying $15/share for puts already in-the-money - they need stock below $55 to profit

- ⏰ The LEAP structure (January 2027) means they're not betting on one earnings miss - they're betting on structural problems

- 📊 Even with Jana Partners activist involvement announced TODAY, this trader still pulled the trigger bearish

- 🎯 The $70 strike at 6.77 gamma resistance suggests they believe FISV will NEVER reclaim that level

This IS a bearish signal - but understand the risks:

The LEAP put buyer has a specific thesis: Fiserv's turnaround will fail, competitive pressures will intensify, and the stock will drift toward $50-55 over the next year. They could be right - the problems that caused the October crash (Argentina revenue loss, margin compression, growth deceleration) haven't been fixed.

BUT - they could also be wrong. Jana Partners activism could accelerate positive changes. CEO Lyons could execute better than expected. The 10x P/E already prices in significant pessimism. And the stock has already given back 74% - betting on further downside from here requires conviction that things get WORSE.

If you own FISV:

- 📊 Consider trimming if you're uncomfortable with the turnaround timeline

- ⏰ Mark May 14 Investor Day as your decision point

- 🛡️ Set mental stop at $57.50 (near 52-week lows) to protect remaining capital

- 👀 Watch for progress on cybersecurity improvements and margin recovery

If you're watching from sidelines:

- ⏰ Wait for Q1 earnings (late April) and Investor Day (May 14) before committing

- 🎯 If turnaround shows signs of working: Buy at $60-65 for value play

- 📉 If turnaround clearly failing: Consider bear put spreads or LEAP puts

- ❌ Don't chase the Jana Partners pop - let the news settle

If you're bearish (like the LEAP buyer):

- 📊 Bear put spreads offer defined risk way to play the thesis

- ⏰ July or October expirations capture key catalyst events

- 💸 LEAPs require significant capital and conviction - size appropriately

- 🎯 Target the $55-60 zone as the breakdown trigger

Mark your calendar - Key dates:

- 📅 April 23-28, 2026 - Q1 2026 earnings (turnaround progress check)

- 📅 May 14, 2026 - INVESTOR DAY, NEW YORK (critical catalyst!)

- 📅 Mid-2026 - Expected margin improvement / Multi-site resiliency completion

- 📅 Late 2026 - Clover Japan launch

- 📅 January 15, 2027 - LEAP put expiration (this $3M trade settles)

Final verdict: FISV is a genuine turnaround story with real risks on both sides. The stock is cheap (10x P/E) after a brutal 74% decline, but the problems that caused the crash remain unresolved. The $3M LEAP put signals that sophisticated institutional money doesn't believe the turnaround will work in the next 11 months.

If you're considering following this trade, understand you need the stock below $55 to profit - another 13% downside from here. That's a big move for a stock already at decade-low valuations. But if the turnaround fails and competitive pressures intensify, $50 or lower is absolutely possible.

This is a "show me" stock. Wait for proof before betting either direction. 👀

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-score of 66.42 reflects this specific trade's unusual volume relative to recent FISV history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. LEAP options have significant time value decay and can expire worthless even if your directional thesis eventually proves correct.

About Fiserv, Inc.: Fiserv is a leading provider of core processing and complementary services for U.S. banks and credit unions, with a focus on small and midsize financial institutions. The company also operates Clover, a leading cloud-based point-of-sale platform for merchants. Market cap of approximately $32 billion in the Business Services (Financial Technology) industry.