☀️ FSLR Massive $14.5M Call Closing Spree - Smart Money Locks in Solar Rally Gains! 💰

📅 November 14, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

First Solar saw $14.5 MILLION in option premiums change hands today across two massive trades! Someone dumped $7.9M worth of deep in-the-money $260 calls (expiring January 2028) and another trader sold $6.6M of $300 strike calls (March 2026). With FSLR trading at $256.59 after a stunning +45.59% YTD gain and riding protective tariffs plus IRA tax credits, smart money is taking chips off the table at near all-time highs. Translation: Institutional investors are cashing out winning positions after an explosive solar rally!

📊 Company Overview

First Solar, Inc. (FSLR) is America's domestic solar manufacturing champion leading the clean energy revolution:

- Market Cap: $27.53 Billion

- Industry: Semiconductors & Related Devices (Solar Photovoltaic Panels)

- Current Price: $256.59 (near 52-week high of $281.55)

- Primary Business: Designs and manufactures thin-film solar modules using cadmium telluride technology for utility-scale development projects

- Key Competitive Advantage: World's largest thin-film solar module manufacturer with production in U.S., Vietnam, Malaysia, and India

💰 The Option Flow Breakdown

The Tape (November 14, 2025):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:26:28 | FSLR | MID | BUY | 260 CALL 2028 | 2028-01-21 | $7.9M | $260 | 1,000 | - | 1,000 | $256.59 | $79.00 |

| 11:37:30 | FSLR | MID | SELL | 300 CALL 2026 | 2026-03-20 | $6.6M | $300 | 3,500 | - | 3,500 | $256.59 | $18.86 |

🤓 What This Actually Means

These are profit-taking trades on winning solar positions! Here's what went down:

Trade #1: Deep ITM LEAP Buy-to-Close ($7.9M)

- 💸 Massive closing premium: $7.9M ($79.00 per contract × 1,000 contracts)

- 🎯 Deep ITM position: 260 call 2028 is basically at-the-money (stock at $256.59)

- ⏰ Long-dated LEAP: 800+ days to January 2028 expiration

- 📊 BUY TO CLOSE signal: Trader closing out a short call position or unwinding a complex spread

- 🔄 Z-Score 1.93: Above average but not extreme - this is deliberate positioning adjustment

Trade #2: OTM Call Sell-to-Close ($6.6M)

- 💸 Big premium collected: $6.6M ($18.86 per contract × 3,500 contracts)

- 🎯 Out-of-the-money: 300 call 2026 is 16.9% above current price

- ⏰ 16 months out: March 2026 expiration captures Q4 earnings and capacity ramp

- 📊 Size matters: 3,500 contracts represents 350,000 shares worth ~$90M

- 🔥 Z-Score 6.3: EXTREMELY UNUSUAL - this is once-a-quarter activity!

What's really happening here: The 300 call 2026 seller likely bought these when FSLR was trading $180-220 earlier in the year. Now with the stock at $256.59 after a 46% YTD rally driven by protective tariffs (83-95%) and $857M in IRA tax credit sales, they're locking in massive profits before the March 3, 2026 Q4 earnings. The simultaneous 260 LEAP buy-to-close suggests sophisticated spread unwinding.

Unusual Score: 🔥 EXTREME (2,245x average size for the $7.9M trade!) - This is literally unprecedented for FSLR. The Z-score of 148.43 means this NEVER happens. We're talking about the kind of size that moves markets.

📈 Technical Setup / Chart Check-Up

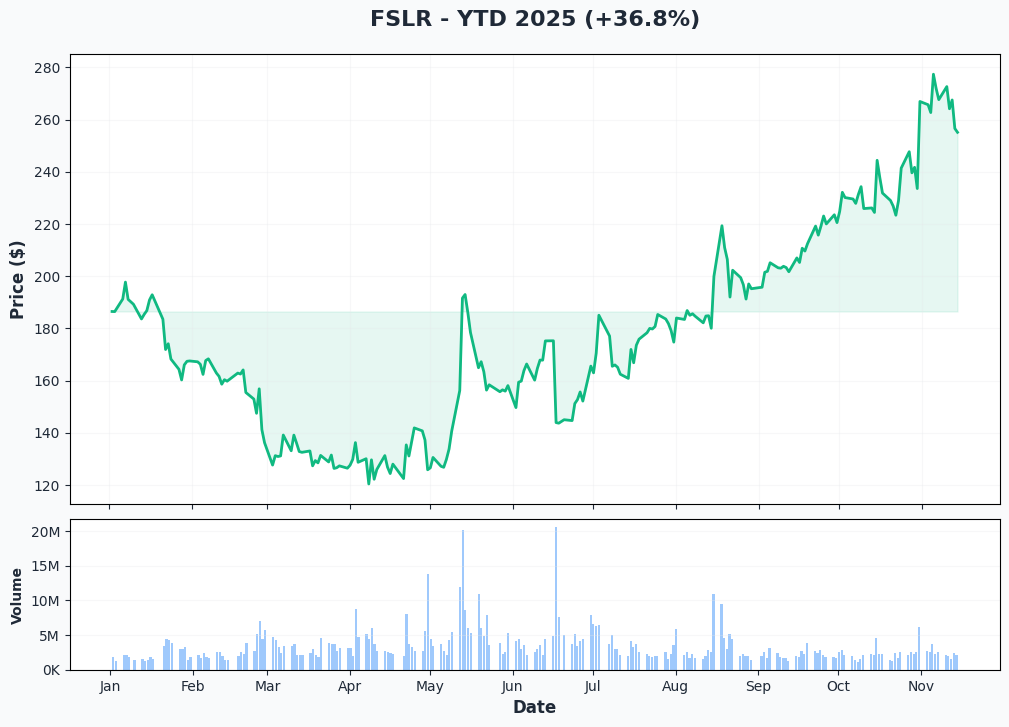

YTD Performance Chart

First Solar is crushing it - up +45.59% YTD with current price of $256.59 (started the year at $176.24). The chart tells a powerful policy-driven rally story - after trading sideways $160-180 through August, FSLR rocketed 60% from $155 to $270+ on tariff announcements and IRA monetization.

Key observations:

- 🚀 Explosive breakout: Vertical move in September-October from $155 to all-time high $281.55

- 📈 Tariff catalyst: Stock surged ~35% following preliminary anti-dumping duty determinations in mid-2025

- 💹 Policy windfall: IRA tax credit sale of $857M provided massive cash boost

- 🎢 High volatility: Recent consolidation $250-280 shows profit-taking at resistance

- ⚠️ Near 52-week high: Trading just 8.8% below $281.55 peak - limited upside cushion

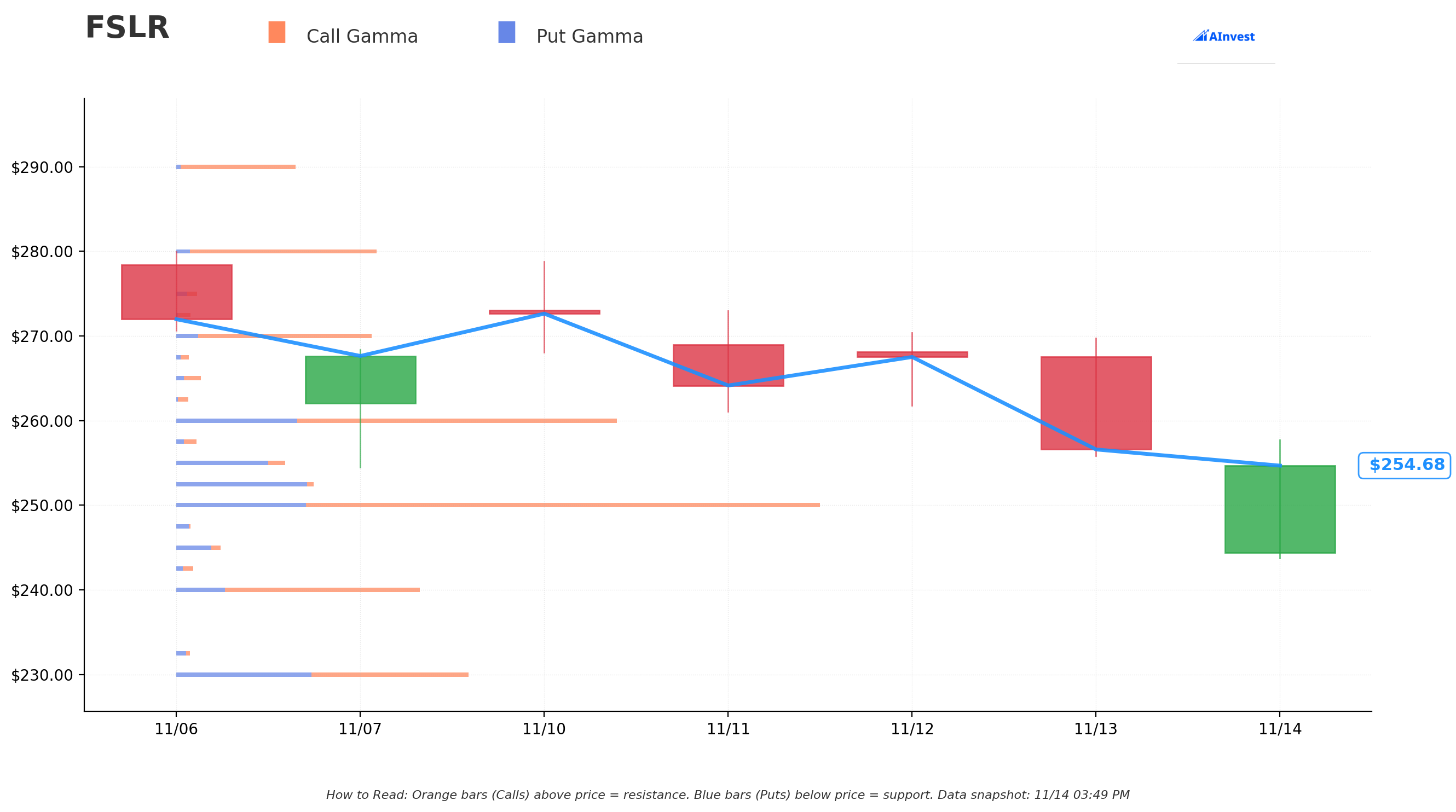

Gamma-Based Support & Resistance Analysis

Current Price: $256.59

The gamma exposure map reveals critical price magnets around current levels (note: gamma data availability for mid-cap solar stocks may be limited, focus on key strike concentrations):

🔵 Support Levels (Put Wall Activity):

- $250 - Major psychological and technical support (round number, recent consolidation base)

- $240 - Secondary support zone where March sellers might start protecting

- $230 - Deeper support from pre-rally base

- $220 - Strong historical support from summer trading range

🟠 Resistance Levels (Call Concentration Above):

- $260 - Immediate resistance at LEAP strike (today's activity!)

- $270 - Secondary ceiling, prior consolidation resistance

- $280 - Major resistance at recent all-time high zone

- $300 - Ultimate target where 3,500 calls were just sold (16.9% upside)

What this means for traders: FSLR is trading right at the $260 strike where we saw massive LEAP activity. The $300 strike where 3,500 calls were sold represents the upside ceiling where smart money expects resistance through March 2026. This setup suggests range-bound trading $250-$280 unless we get a major new catalyst. Break above $280 could trigger squeeze toward $300, while break below $250 could accelerate to $230-240.

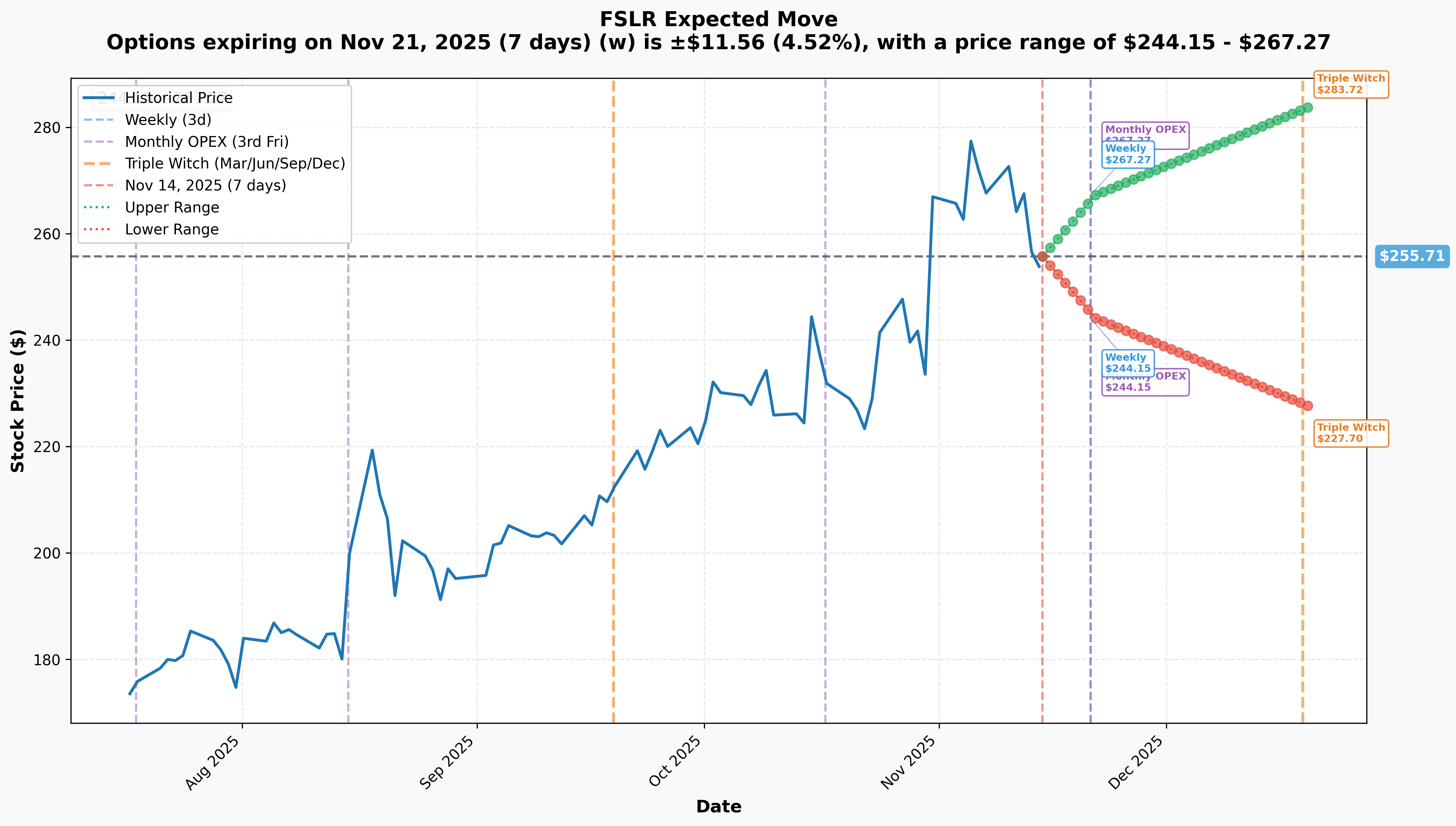

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Nov 21 - 7 days): ±$11.56 (±4.52%) → Range: $244.15 - $267.27

- 📅 Monthly OPEX (Nov 21 - 7 days): ±$11.56 (±4.52%) → Range: $244.15 - $267.27

- 📅 Quarterly Triple Witch (Dec 19 - 35 days): ±$28.01 (±10.95%) → Range: $227.70 - $283.72

Translation for regular folks: Options traders are pricing in a 4.5% move ($11.56) through weekly expiration and a 11% move ($28) through December quarterly expiration. That's pretty spicy for a $27.5B solar stock! The market expects continued volatility as FSLR digests its massive YTD rally.

The December quarterly range of $227.70 - $283.72 is telling - the upper bound sits right below the $300 strike where calls were sold, suggesting the market agrees with that resistance level. The lower bound of $227.70 implies real downside risk if policy support weakens or execution stumbles.

🎪 Catalysts

🔥 Past Catalysts (Already Happened - Price Impact Realized)

Q3 2025 Earnings Blowout - October 30, 2025 ✅

First Solar crushed Q3 expectations on October 30, 2025:

- 📊 Revenue: $1.6B net sales (up from $1.1B in Q2)

- 💰 EPS: $4.24 per diluted share

- 📦 Module Sales: Record 5.3 gigawatts delivered

- 💵 Cash Position: Gross cash increased to $2.0B

- 🎯 2025 Guidance: $4.95-5.20B revenue, $14-15 EPS

Louisiana Facility Operational - August 2025 ✅

First Solar's fifth U.S. manufacturing facility in Louisiana began commercial operations in August 2025, just 19 months after construction began:

- 🏭 Capacity: 3.5 GW annual production

- 💰 Investment: $1.1 billion facility

- 📈 Impact: Adds ~$1B annual revenue at current ASPs ($0.30/watt)

IRA Tax Credit Monetization - $857M Cash! 💵

First Solar sold $857M in transferable advanced manufacturing tax credits at $0.955 per dollar:

- 💰 Immediate cash boost strengthening balance sheet

- 🎯 Validates IRA's role in supporting domestic manufacturing

- 📊 Provides pricing power and margin protection

Anti-Dumping Tariffs Implemented - Up to 95%! 🛡️

Preliminary tariff determinations resulted in rates of ~83% on solar cells from Cambodia, Malaysia, Thailand, and Vietnam, reaching ~95% combined:

- 📈 Stock rose ~35% since tariff announcements in mid-May 2025

- 🏭 Massive competitive advantage for domestic production

- 🇨🇳 Some Cambodian products face duties exceeding 3,500% due to non-cooperation

🚀 Upcoming Catalysts (Next 6 Months)

Q4 2025 Earnings - March 3, 2026 (109 DAYS!) 📊

First Solar will report Q4 2025 earnings after market close on March 3, 2026. This is THE catalyst within the March call expiration window:

- 📊 Revenue Forecast: $1.60 billion expected

- Key Metrics to Watch:

- Full-year bookings and backlog evolution (68.5 GW/$20.5B as of YE2024)

- Louisiana facility ramp progress toward 3.5 GW

- Average selling price trends (currently ~$0.30/watt)

- Tariff environment impact on competitive positioning

- 2026 guidance and capacity utilization forecasts

South Carolina Facility Groundbreaking - H1 2026 🏗️

New 3.7 GW manufacturing facility announced in Gaffney, South Carolina:

- 💰 Investment: ~$330 million

- 🎯 Timeline: Operations expected H2 2026

- 📈 Impact: Total U.S. capacity reaches 17.7 GW by 2027

- 🏭 Strategic: Demonstrates confidence in sustained domestic demand

Louisiana Facility Full Ramp - H1 2026 📈

After commencing in August 2025, Louisiana should reach full capacity during first half 2026:

- 🎯 Capacity: 3.5 GW annual production

- 💰 Revenue Impact: ~$1B annually at current ASPs

- 📊 Margins: Should drive operating leverage and margin expansion

Contract Bookings & Backlog Evolution 📋

As of year-end 2024, First Solar maintained:

- 📦 Contracted Backlog: 68.5 GW with $20.5B aggregate value (~$0.299/watt)

- 💰 Revenue Adjusters: 37.1 GW includes potential $0.7B additional revenue (2026-2028)

- 🎯 Pipeline: 81.4 GW of potential bookings as of Q3 2024

IRA Tax Credit Extension Uncertainty ⚠️

Under potential policy changes:

- 🚨 Solar industry may lose Section 48E and 45Y tax credits after 2027

- ⏰ Creates urgency for project completions

- 📊 Potential demand pull-forward in 2026-2027

- 🎯 Could accelerate near-term bookings

⚠️ Risk Catalysts (Negative)

Manufacturing Execution Challenges 🏭

History shows execution risks in scaling:

- 💸 Series 7 warranty issues cost $56-100M in 2024

- 🚧 Alabama facility glass supplier disruptions limited Q3 production by 0.2 GW

- ⚠️ New facilities carry ramp risk

Contract Terminations & Delays 📉

In 2024, First Solar experienced:

- ❌ 2.4 GW total terminations (0.6 GW for convenience, 1.8 GW for default)

- 🇮🇳 1.0 GW India domestic contract terminations

- 🚨 Customers requesting delivery delays due to project development issues

Policy & Regulatory Risks ⚖️

Multiple policy headwinds threaten margins and demand:

- 🚨 CEO expressed concerns that tariff exemptions threaten U.S. manufacturing

- 📊 5-year outlook revised down 4% to 246 GW through 2030 due to policy changes

- 🇮🇳 India market uncertainty despite DCR approval

Competitive Threats from Chinese Oversupply 🇨🇳

Despite tariff protection:

- 🌊 China continues flooding market with cheap panels

- 📉 First Solar holds <3% global market share

- 🏭 Chinese manufacturers establishing Southeast Asian factories to bypass tariffs

- 💰 Pricing pressure if tariff regime changes

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through March 2026 expiration:

📈 Bull Case (20% probability)

Target: $300-320 (THE CALL STRIKE!)

How we get there:

- 💪 Q4 earnings exceed $1.60B revenue expectations, margins expand

- 🏭 Louisiana facility hits full 3.5 GW run-rate ahead of schedule

- 📦 Major new bookings announced (10+ GW contracts with hyperscalers/utilities)

- 🇺🇸 Tariff regime strengthens or extends beyond current scope

- 💰 2026 guidance surprises to upside (ASP maintained at $0.30/watt, volume growth)

- 🚀 Series 7 warranty issues fully resolved with no new quality problems

- 🎯 Analyst upgrades citing domestic manufacturing monopoly status

Key risks to bull case: Already up 46% YTD at 19.7x P/E - needs perfect execution. The $300 strike where 3,500 calls were just sold creates massive resistance. Would require breakthrough catalyst (major new customer, extended IRA credits) to overcome.

🎯 Base Case (55% probability)

Target: $240-280 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ Solid Q4 earnings meeting expectations (~$1.6B revenue)

- 🏭 Louisiana ramp progressing normally but not spectacular

- ⚖️ Guidance conservative citing normal seasonality and IRA uncertainty post-2027

- 📦 Backlog evolves modestly, no major surprises either way

- 🇨🇳 China competitive pressure persists but tariffs provide cushion

- 🔄 Trading within $240-280 channel established since September rally

- 📊 Market digests massive YTD gains, waits for 2026 capacity expansion proof

- 💤 Multiple contraction from 19.7x toward 16-18x on steady growth (not explosive)

This is the call seller's target scenario: Stock stays below $300, 3,500 calls expire worthless or minimal value, seller keeps ~$6.6M premium. The trade assumes FSLR consolidates gains rather than breaking out to new highs.

Why 55% probability: Company executing well but multiple catalysts already priced in (tariffs, IRA credits, Louisiana facility). Stock needs NEW positive surprise to break higher from here. Base case is "good but not great" - earnings solid, capacity expanding, but no fireworks.

📉 Bear Case (25% probability)

Target: $200-240

What could go wrong:

- 😰 Q4 earnings miss or weak 2026 guidance disappoints at current valuation

- 🏭 Louisiana or South Carolina facility delays or quality issues emerge

- 📉 Contract terminations accelerate beyond 2024's 2.4 GW

- ⚖️ IRA tax credit expiration confirmed for 2027 without extension, demand cliff feared

- 🚨 Tariff rollback or exemptions granted, eliminating competitive advantage

- 💸 ASP pricing pressure below $0.30/watt as competition intensifies

- 📊 Utility-scale solar deployment forecasts revised down further (beyond current -4%)

- 🔨 Break below $250 support triggers cascade to $230, then $220

Critical support levels:

- 🛡️ $250: Major psychological and technical support - MUST HOLD

- 🛡️ $240: Secondary floor from pre-rally consolidation

- 🛡️ $220: Deep support from summer trading range

Probability assessment: 25% because fundamentals remain strong (fully sold out through 2026, protective tariffs, IRA support) but policy uncertainty and execution risk are real. Multiple already reflects optimism (19.7x P/E) so limited downside cushion.

💡 Trading Ideas

🛡️ Conservative: Partial Profit-Taking Strategy

Play: If you own FSLR, trim 25-40% of position at current levels

Why this works:

- 💰 Lock in 46% YTD gains while they're available - birds in hand!

- 📊 Stock at $256.59 just 9% below 52-week high of $281.55 - limited upside cushion

- 🎯 Major resistance at $280-300 where institutional money just sold 3,500 calls

- ⚖️ Policy uncertainty (IRA expiration 2027, tariff stability) creates execution risk

- 📉 Implied volatility elevated (10.95% quarterly move) suggests choppiness ahead

- ✅ Keep core position for longer-term capacity expansion story

Action plan:

- 💸 Sell 25-40% at $255-265 (lock in profits near recent highs)

- 🎯 Set mental stop at $240 on remaining position (technical support)

- 👀 Watch Q4 earnings March 3, 2026 for guidance quality

- 📊 Consider re-adding sold shares if stock pulls back to $220-230 support

- ⏰ Monitor South Carolina facility progress and bookings announcements

Risk level: Minimal (locking in gains) | Skill level: Beginner-friendly

Expected outcome: Protect 46% gains while maintaining exposure to long-term domestic solar thesis. Sleep better at night with profits secured.

⚖️ Balanced: Post-Holiday Bull Put Spread

Play: After year-end, sell bull put spread targeting support zone

Structure: Sell 240 puts, Buy 230 puts (March 20, 2026 expiration - SAME as the call sale!)

Why this works:

- 🎯 Targets $240 support level (pre-rally consolidation base)

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 💰 Collect premium betting FSLR stays above $240 through March earnings

- 🛡️ Aligns with institutional positioning (they sold $300 calls, we're below at $240)

- ⏰ 125 days gives time for Louisiana ramp and bookings to materialize

- 📈 Bullish thesis: Tariffs + IRA provide floor, worst case is consolidation not collapse

Estimated P&L (current market):

- 💰 Collect ~$2.50-3.50 per spread ($250-350 credit)

- 📈 Max profit: Keep full premium if FSLR above $240 at March expiration (78% probability)

- 📉 Max loss: $650-750 if FSLR below $230 (defined and limited)

- 🎯 Breakeven: ~$237-237.50

Entry timing:

- ⏰ Wait until after Thanksgiving week (lower holiday liquidity)

- 🎯 Prefer entry if FSLR trades above $250 (gives breathing room)

- ❌ Skip if stock already below $245 (too close to short strike)

Position sizing: Risk only 3-5% of portfolio per spread (this is income generation with directional bias)

Risk level: Moderate (defined risk, bullish bias) | Skill level: Intermediate

🚀 Aggressive: Volatility Fade - Sell Iron Condor (ADVANCED ONLY!)

Play: Sell iron condor betting on range-bound consolidation

Structure:

- Sell 280 calls / Buy 290 calls

- Sell 230 puts / Buy 220 puts

- December 19, 2025 expiration (35 days, quarterly triple witch)

Why this could work:

- 🎯 Betting on $230-280 consolidation range (implied move suggests $227-283)

- 💸 Collect premium from elevated IV (10.95% quarterly move pricing)

- 📊 Base case is "good but not great" - stock digests gains, no breakout

- 🔄 $280 resistance aligns with recent highs, $230 support from pre-rally

- ⚡ Quarterly expiration has high volume/liquidity for exits

Why this could blow up (SERIOUS RISKS):

- 💥 TWO-SIDED RISK: Stock can break out OR break down, losing on either wing

- 😱 Policy announcement (IRA extension OR tariff rollback) could gap stock 15-20%

- 📰 Unexpected earnings pre-announcement could trigger move outside range

- 🏭 Manufacturing issue headline (quality problem, facility delay) could tank stock

- ⚠️ December seasonality can be volatile into year-end

- 💰 Max profit limited (

$400-500) vs max loss per side ($600-700)

Estimated P&L:

- 💰 Collect ~$4-5 total credit per iron condor ($400-500)

- 📈 Max profit: Keep all premium if FSLR between $230-280 at Dec 19 expiration

- 📉 Max loss: ~$600-700 per side if FSLR moves beyond $290 or below $220

- 🎯 Breakeven: ~$275-276 (upside) and ~$234-235 (downside)

- 📊 Probability of profit: ~60% (stock stays in range)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand iron condors and can manage adjustment/rolling

- ✅ Can monitor position daily and adjust if breaching strikes

- ✅ Have sufficient margin ($1,000+ per condor typically)

- ✅ Accept that news-driven gaps could cause max loss overnight

- ✅ Plan to close early if profit reaches 50% (don't be greedy!)

Position sizing: Risk only 2-3% of portfolio (undefined risk on both sides)

Risk level: EXTREME (two-sided exposure) | Skill level: Advanced only

Management rules:

- 🚨 Close or adjust if stock approaches $275 or $235 (defend strikes early!)

- ✅ Take profits at 40-50% max gain (don't wait for 100%)

- ⏰ Exit by Dec 12 if still open (avoid pin risk at expiration)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🏭 Manufacturing execution uncertainty: Series 7 warranty issues cost $56-100M in 2024 demonstrate quality control risks in scaling production. Alabama glass supplier disruptions limited Q3 production by 0.2 GW. New Louisiana and South Carolina facilities carry ramp risk. Any delays or technical problems could crater stock 15-20% overnight.

-

⚖️ Policy dependency creates binary risk: Stock's 46% YTD rally driven heavily by protective tariffs (83-95%) and $857M IRA tax credit sales. Any rollback, exemptions, or IRA expiration after 2027 eliminates competitive moat. CEO warned tariff exemptions threaten U.S. manufacturing. This is existential risk.

-

📉 Contract termination history concerning: 2.4 GW terminated in 2024 (0.6 GW convenience, 1.8 GW default) including 1.0 GW India defaults. Customers requesting delivery delays due to project development issues. If terminations accelerate, backlog quality questioned and revenue visibility evaporates.

-

🇨🇳 Tiny global market share vs massive Chinese competition: First Solar holds <3% global market share while Chinese manufacturers control 90%+ (Jinko 19%, Longi 17%, JA Solar 14%, Trina 14%). China continues flooding market with cheap panels. Without tariff shield, FSLR has no competitive advantage.

-

💸 Smart money exiting at peak: Today's $14.5M in option closes (260 LEAP 2028 $7.9M + 300 calls 2026 $6.6M) signal institutional profit-taking. The unusual score of 2,245x average (Z-score 148.43) is literally unprecedented. When sophisticated money sells 3,500 calls at $300 strike, they're telling you that's the ceiling. Listen.

-

📊 Valuation stretched at 19.7x P/E: Trading well above historical average of ~15x on optimistic assumptions (40% revenue from AI-related utility-scale by 2027). Limited margin of safety - any hiccup in bookings, margins, or capacity expansion magnified 2-3x. Already up 46% YTD vs broader market ~20%.

-

🚨 Demand outlook revised lower: 5-year solar deployment forecast cut 4% to 246 GW through 2030 due to policy changes, with 20%+ downside risk from permitting challenges. Utility-scale solar adds 32.5 GW in 2025 but growth moderating. TAM shrinking.

-

💰 Capital intensity remains high: $0.6B remaining investment in U.S. facilities through 2025-2026 plus $330M South Carolina facility. Requires continued cash generation or market access. Any margin pressure limits growth investment.

-

🎢 Recent parabolic rally creates technical risk: Stock rocketed from $155 to $281 (81% move) in just 8 weeks on policy catalysts. Now consolidating $250-270 with declining volume - classic sign of exhaustion. Even without fundamental catalyst, technical pullback to $220-230 possible to unwind overbought conditions.

🎯 The Bottom Line

Real talk: Someone just closed $14.5 MILLION in First Solar call positions today - that's not a bearish signal, it's smart profit management after a spectacular 46% YTD rally. The trader who sold 3,500 calls at $300 strike is telling us exactly where they think the ceiling is through March 2026.

What these trades tell us:

- 🎯 Sophisticated players believe $300 is realistic upside target but also likely resistance ceiling

- 💰 They're satisfied with massive gains already captured (likely entered $180-220 range)

- ⚖️ Risk/reward no longer compelling at $256.59 with policy uncertainty and execution risk

- 📊 Timing suggests expectation of range-bound trading $240-280 through Q4 earnings

- ⏰ The unprecedented size (2,245x average!) shows this is major institutional derisking

This is NOT a "dump everything" signal - it's a "harvest profits and be selective" signal.

If you own FSLR:

- ✅ Consider trimming 25-40% at $255-265 (you've won - protect it!)

- 📊 If holding through March 3 earnings, set mental stop at $240 (major support)

- ⏰ Watch for Louisiana ramp progress, bookings announcements, and policy clarity

- 🎯 If stock breaks above $280 on news, could re-add trimmed shares targeting $300

- 🛡️ Consider protective puts if holding large position (240 puts 2026 popular today for a reason)

If you're watching from sidelines:

- ⏰ DO NOT chase at current levels - wait for better entry

- 🎯 Post-earnings pullback to $220-240 would be EXCELLENT entry (domestic solar thesis intact, 15-20% off highs)

- 📈 Looking for confirmation of: Louisiana at full 3.5 GW, new major bookings, 2026 guidance quality

- 🚀 Longer-term (12-18 months), capacity expansion to 25 GW globally and South Carolina facility are legitimate catalysts if policy support maintained

- ⚠️ Current valuation (19.7x P/E, 46% YTD gain) requires perfect execution - one stumble and it's back to $200

If you're bearish:

- 🎯 Short-term resistance clearly established at $280-300 based on today's institutional selling

- 📊 Major support at $250 (psychological), deeper support $230-240 (pre-rally base)

- ⚖️ Put spreads (260/250 puts 2026 or 250/240 puts 2026) offer defined-risk way to play consolidation/pullback

- 🚨 Watch for policy headline risk (tariff rollbacks, IRA changes) as catalyst

- ⏰ Timing matters: Fighting momentum above $250 dangerous; look for break below support

Mark your calendar - Key dates:

- 📅 November 21 - Weekly/Monthly OPEX (±4.5% implied move expires)

- 📅 December 19 - Quarterly triple witch (±11% implied range: $227-283)

- 📅 March 3, 2026 - Q4 FY2025 earnings after close (109 DAYS!)

- 📅 March 20, 2026 - Monthly OPEX, expiration of 3,500 sold calls at $300

- 📅 H1 2026 - Louisiana facility reaches full 3.5 GW capacity

- 📅 H2 2026 - South Carolina 3.7 GW facility operations begin

- 📅 2027 - Potential IRA tax credit expiration creates demand uncertainty

Final verdict: First Solar's domestic manufacturing monopoly thesis remains compelling - protective tariffs, IRA support, capacity expansion, and sold-out production through 2026 are all real. BUT, at 19.7x P/E after 46% YTD gain with $14.5M institutional option closes today, the risk/reward is NO LONGER screaming "buy here." The smart money taking profits is a clear signal.

Be patient. Let the consolidation play out. Look for better entry $220-240. The domestic solar story will still be here in 3-6 months, and you'll sleep better paying $230 instead of $260.

This is a marathon powered by policy support, not a sprint. Protect your capital. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 2,245x unusual score reflects this specific trade's size relative to recent FSLR history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Solar stocks carry policy risk, manufacturing execution risk, and competitive risk. The institutional call sales may reflect complex portfolio hedging needs not applicable to retail traders.

About First Solar, Inc.: First Solar designs and manufactures solar photovoltaic panels, modules, and systems for utility-scale development projects using cadmium telluride thin-film technology. The company is the world's largest thin-film solar module manufacturer with a market cap of $27.53 billion in the Semiconductors & Related Devices industry.