🐋 GEV $2.3M LEAP Bull Call Spread - Whale Bets Big on the AI Power King Through 2028!

📅 February 26, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $900K net premium on a massive GE Vernova bull call spread - buying $2.3M in January 2028 $900 calls while selling $1.4M in $1,200 calls - a 2-year LEAP bet that GEV rallies from $844 to at least $900 and potentially $1,200. Both legs are classified as EXTREMELY UNUSUAL with Z-scores of 61.47 and 27.68 respectively, meaning this kind of size shows up only a handful of times a year. With a record $150B backlog, gas turbines sold out through 2029+, and AI data center power demand exploding, this trader is positioning for the multi-year power infrastructure supercycle.

📊 Company Overview

GE Vernova Inc. (GEV) is the global leader in electric power - generating, transferring, converting, and storing electricity:

- ⚡ What they do: Gas turbines, grid equipment, wind turbines, nuclear SMRs, and electrification solutions - essentially the backbone of the global power grid

- 💰 Market Cap: ~$236B

- 🏢 Sector: Electronic & Other Electrical Equipment

- 📈 Exchange: NYSE

- 📊 Current Price: ~$860

- 🔥 Key Story: Record $150B backlog, 34% global gas turbine market share, gas turbines sold out through 2029+, and more than $2B in direct data center orders in 2025 alone - tripling the prior year

💰 The Option Flow Breakdown

📊 The Tape

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:09:52 | GEV | MID | BUY | CALL $900 | 2028-01-21 | $2.3M | $900 | 114 | 26 | 98 | $844 | $230.32 |

| 10:09:52 | GEV | MID | SELL | CALL $1,200 | 2028-01-21 | $1.4M | $1,200 | 114 | 14 | 98 | $844 | $140.32 |

🤓 What This Actually Means

Let me break this down:

- 💸 Net premium paid: ~$900K ($2.3M on the long $900 calls minus $1.4M collected on the short $1,200 calls)

- 📐 Structure: Bull Call Spread (LEAP) - buying 98 contracts of the $900 call while simultaneously selling 98 contracts of the $1,200 call, same January 2028 expiration

- ⏰ Nearly 2 years to expiration (January 21, 2028) - this is a true LEAP strategy, giving massive runway for the thesis to play out

- 📊 Vol/OI ratios of 4.4x and 8.1x - volume dwarfing open interest on both legs, confirming these are brand new positions opening

- 🤝 Both legs filled at MID and at the same timestamp (10:09:52) - this is one institutional trade, not two random fills

- 🎯 Breakeven at expiration: ~$992 ($900 strike + $90/share net debit per spread) - needs a +17.5% rally from $844

- 💰 Max profit: ~$2.04M if GEV reaches $1,200+ by January 2028 ($300 spread width x 98 contracts x 100 shares - $900K premium = ~$2.04M)

- 📈 Risk/reward: ~2.3:1 - risk $900K to make up to $2.04M

What's the thesis here?

This trader is betting GEV climbs from $844 to at least $900 - and ideally well past $1,200 - over the next two years. The LEAP timeframe is smart because it captures the company's entire 2026-2028 growth roadmap: the turbine production ramp to 20 GW, Prolec GE integration, continued data center order growth, and the path to $56B revenue and 20% EBITDA margins by 2028. At 25x 2028 EV/EBITDA ($56B revenue x 20% = $11.2B EBITDA), that implies an enterprise value of $280B or roughly **$1,040/share** - right in the sweet spot of this spread.

Why a spread instead of naked calls? By selling the $1,200 call, the trader cut their cost from $2.3M to $900K - a 61% discount on the trade. They're capping their upside at $1,200 but dramatically improving the risk/reward ratio. This is disciplined institutional money at work.

📈 Technical Setup / Chart Check-Up

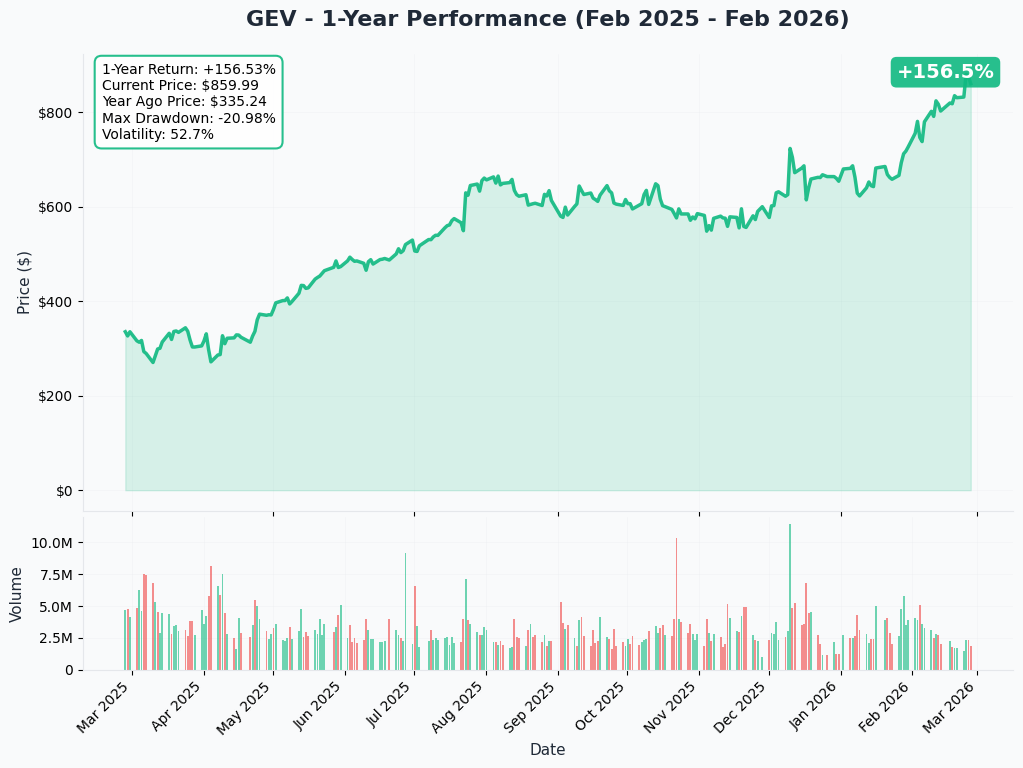

YTD Performance

GEV has been on a monster run. The stock is trading near its 52-week high of $879.73 set just two days ago on February 24. Key highlights:

- 🚀 1-year return: +117% - more than doubling in 12 months on the AI power demand story

- 📈 3-month performance: +26.5% rallying from $637 to $846+ since mid-January

- 💪 Near all-time highs: Currently trading at ~$860, just 2% off the $879.73 high

- 📊 Strong momentum: The stock has barely pulled back, riding the Q4 earnings beat and Prolec GE acquisition completion

- ⚡ Recent catalyst surge: February 24 nuclear SMR news in Poland added fresh fuel to the rally

Key takeaway: GEV is in a powerful uptrend with minimal pullbacks. The stock is consolidating near highs rather than pulling back - typically a sign of strong institutional demand absorbing any selling pressure.

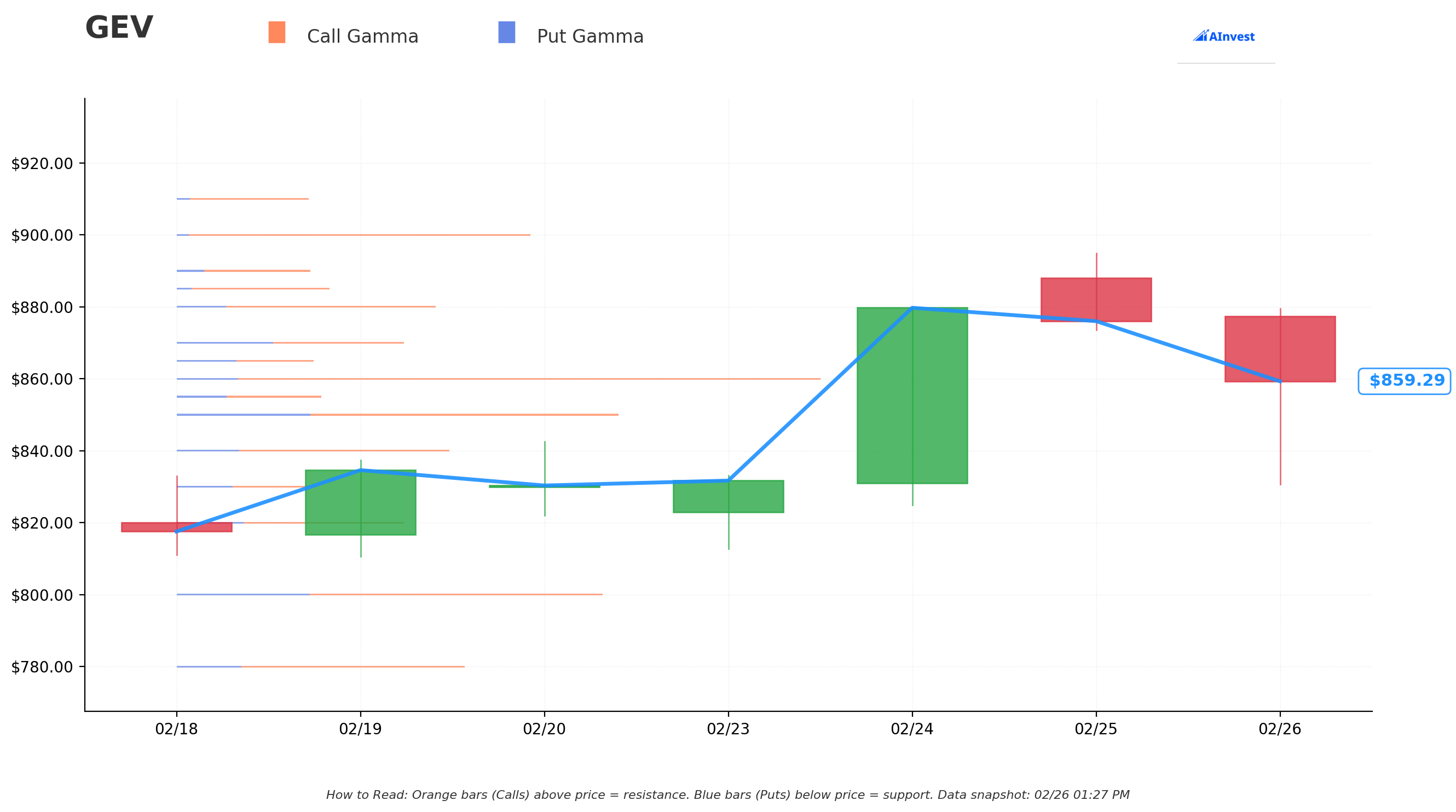

Gamma-Based Support & Resistance Analysis

Current Price: ~$860

The gamma exposure map shows where market makers have heavy options positioning, creating natural price floors and ceilings:

🔵 Support Levels (Below Price):

- $850 - Strongest immediate support with 1.29B total gamma exposure (just 1.2% below - very tight floor!)

- $840 - Secondary support at 0.80B gamma (2.3% below)

- $820 - Medium support at 0.66B gamma (4.7% below)

- $800 - Major structural support at 1.26B gamma (7.0% below - this is the LINE IN THE SAND)

- $780 - Extended floor at 0.84B gamma (9.3% below)

🟠 Resistance Levels (Above Price):

- $860 - Strongest resistance at 1.88B total gamma (right at the current price - this is THE level to break)

- $870 - Light resistance at 0.67B gamma (1.2% above)

- $880 - Moderate resistance at 0.75B gamma (2.3% above)

- $900 - Strong resistance at 1.03B gamma (4.7% above - this is the LONG CALL STRIKE on the whale trade!)

- $1,000 - Extended resistance at 0.57B gamma (16.3% above)

What this means for traders: GEV is battling the $860 resistance right now - the biggest gamma wall on the board. A clean break above $860 opens a relatively smooth path to $870-$880, and then the $900 level becomes the next major target. Notice how the $900 strike on the whale trade aligns perfectly with a key gamma resistance level. That's not a coincidence - institutional traders use these levels as reference points.

Net GEX Bias: Bullish (14.9B total call gamma vs 7.4B total put gamma). Call gamma is running nearly 2x put gamma, meaning dealers are heavily positioned on the call side. This creates a "gamma magnet" effect where the stock tends to gravitate upward toward high-gamma call strikes.

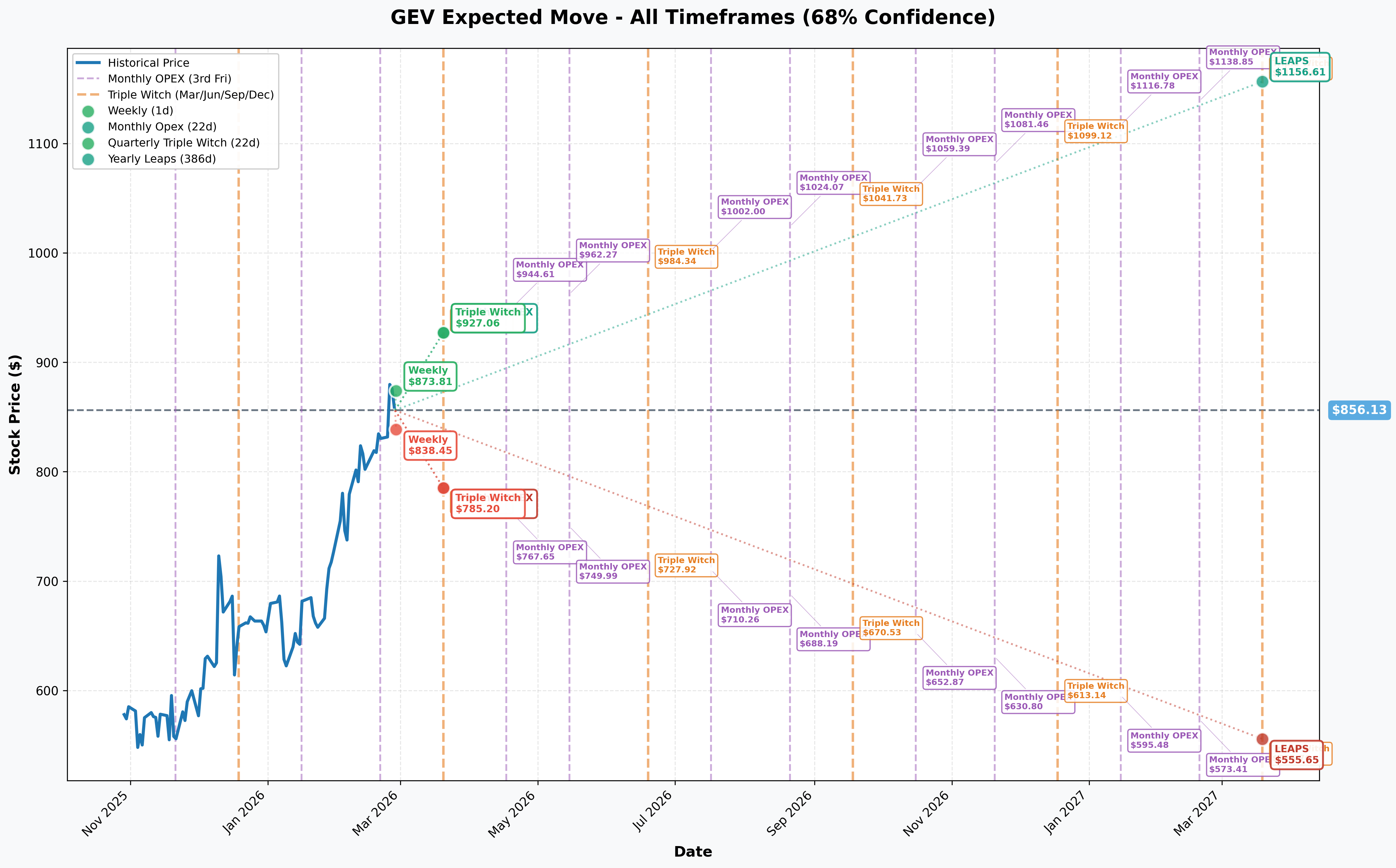

Implied Move Analysis

Options market pricing for upcoming expirations (68% confidence):

- 📅 Weekly (Feb 27 - 1 day): ±$17.68 (±2.1%) --> Range: $838 - $874

- 📅 Monthly OPEX (Mar 20 - 22 days): ±$70.93 (±8.3%) --> Range: $785 - $927

- 📅 Quarterly Triple Witch (Jun 19): Upper $984 / Lower $728

- 📅 Yearly LEAPs (Mar 2027): ±$300.47 (±35.1%) --> Range: $556 - $1,157

Translation: The options market expects GEV could realistically trade anywhere from $556 to $1,157 by March 2027. The LEAP implied range stretching above $1,150 tells you the market sees a path to $1,000+ within the next year - and this whale trade's $900-$1,200 range sits squarely in the upper half of that distribution. By January 2028 (this trade's expiration), the implied range would be even wider, making $1,200 clearly within the realm of possibility.

Key insight: The monthly implied move already puts $927 as the upper end by March 20. That means just one month of upside volatility could push GEV above the $900 long strike on this trade. The weekly 2.1% implied move reflects moderate near-term volatility - not cheap, but not panic-level either.

🎪 Catalysts

🔥 Upcoming Catalysts

Q1 2026 Earnings - April 22, 2026 (Before Market Open) 📊

This is the next major inflection point. MarketBeat confirms the date with consensus EPS at $1.68. Key things to watch:

- 📊 First full quarter of Prolec GE consolidated results (Electrification margin target 16-17%)

- ⚡ Power segment organic revenue growth (guided high-single digits)

- 💨 Wind segment losses ($300-400M guided - how bad is it?)

- 🤖 Data center order cadence (following >$2B in 2025 direct orders)

- 🏭 Gas turbine production ramp progress toward 20 GW target

Gas Turbine 20 GW Production Ramp - Mid-2026 🏭

The company is targeting 20 GW annualized production by mid-2026, up from ~13 GW currently. CEO expects turbine reservations sold out through 2030 by year-end 2026. Hitting this milestone would be a powerful confirmation that GEV can convert its massive backlog into actual revenue.

$10B Buyback Execution 💰

With ~$6.7B remaining authorization and $5.0-5.5B annual free cash flow, GEV has significant ongoing support for the share price. That's meaningful buying power soaking up any dips.

Nuclear SMR Regulatory Milestones ☢️

NRC review of TVA Clinch River BWRX-300 application is ongoing. Any approval milestone would be a major positive catalyst for the nuclear narrative. The Poland design agreement for ~24 BWRX-300 units backed by up to $4B in US financing adds further optionality.

Offshore Wind Resolution - End of March 2026 ⚠️

This is the wild card. Federal stop-work orders on five offshore wind projects continue since December 22, 2025. Critical deadline at end of March when developers lose access to the Sea Installer vessel. Resolution could remove an overhang; deterioration adds ~$250M revenue drag.

2028 Revenue & EBITDA Targets 🎯

The company's 2028 outlook of $56B revenue, 20% EBITDA margin, and $24B+ cumulative FCF is the fundamental anchor for this trade. Every quarterly update either validates or challenges this roadmap.

✅ Recent Catalysts (Already Happened)

Q4 2025 Earnings Blowout - January 28, 2026 📊

Revenue $11.0B (beat by 7.53%), EPS $13.39 vs. $3.22 consensus (a 316% beat). Q4 orders surged 65% YoY to $22.2B. Full-year 2025 revenue hit $38B with free cash flow doubling to $3.7B. This was a monster quarter.

Prolec GE Acquisition Completed - February 2, 2026 🏭

Acquired remaining 50% stake for $5.275B, adding ~$3B revenue to the Electrification segment, 10,000 employees, and seven manufacturing sites. Immediately accretive and strengthens the transformer/grid equipment position during a critical North American grid bottleneck.

Poland Nuclear SMR Agreement - February 24, 2026 ☢️

Signed the Poland Generic Design Agreement for BWRX-300 deployment with Orlen Synthos Green Energy. Plans for ~24 units across six locations, backed by up to $4B from US Ex-Im Bank and DFC.

2025 Investor Update - December 9, 2025 📈

Raised 2026 guidance to $44-45B revenue and $5.0-5.5B FCF. Doubled the dividend to $0.50/quarter and increased buyback authorization to $10B. 2028 outlook raised to $56B revenue (from $52B).

Goldman Sachs Price Target Raise 📊

Goldman raised their target to $925 from $840 (Buy rating). Evercore ISI to $905 from $860 (Outperform). The Street is chasing the stock higher.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, analyst targets, and the 2028 fundamental roadmap, here are the scenarios through the January 21, 2028 LEAP expiration:

📈 Bull Case (35% probability)

Target: $1,100-$1,200+

How we get there:

- 🚀 Gas turbine production hits 20 GW on schedule by mid-2026, slots sold out through 2030

- ⚡ Data center power orders accelerate beyond $2B/year run rate as AI demand compounds

- 🏭 Prolec GE integration delivers synergies, Electrification margin hits 19%+ by 2027

- ☢️ BWRX-300 nuclear SMR gets NRC milestone, adding optionality premium

- 📈 2028 revenue tracking to $56B+ with 20% EBITDA margins ($11.2B EBITDA)

- 💰 At 25x EV/EBITDA =

$280B enterprise value = **$1,040/share** fundamentally - 📊 Multiple expansion to 28-30x on scarcity premium (only 3 players globally) pushes toward $1,200

Bull call spread P&L at $1,200+: Max profit of ~$2.04M (spread worth $300/contract x 98 contracts x 100 = $2.94M - $900K cost)

This is the scenario where everything clicks - and it aligns closely with GEV's own 2028 targets. The implied move upper range already puts $1,157 as reachable by March 2027 - a full 10 months before this trade expires.

🎯 Base Case (40% probability)

Target: $950-$1,050 range

Most likely scenario:

- ✅ Turbine ramp proceeds but with some supply chain delays (yttrium constraints)

- 📊 Quarterly earnings generally meet guidance but no major upside surprises

- ⚖️ Wind segment losses stabilize but don't improve meaningfully

- 🔄 Stock grinds higher through gamma resistance at $860, $880, $900 over months

- 📈 2027 revenue of $48-50B keeps the stock on an upward trajectory

- 💰 Analyst consensus gradually moves toward $900-$1,000 range

Bull call spread P&L at $1,000: Spread worth ~$100/share, profit = ($100 x 98 x 100) - $900K = ~$80K gain (9% ROI) Bull call spread P&L at $1,050: Spread worth ~$150/share, profit = ($150 x 98 x 100) - $900K = ~$570K gain (63% ROI)

In this scenario, the trade is solidly profitable but doesn't hit max profit. The trader makes money as long as GEV stays above the ~$992 breakeven. Given the 2-year timeframe and strong fundamental trajectory, this is the most likely outcome.

📉 Bear Case (25% probability)

Target: $700-$850

What could go wrong:

- 😰 Yttrium supply chain disruption delays the 20 GW turbine ramp, missing 2026 targets

- 🌬️ Wind segment losses widen beyond $400M, offshore wind policy deteriorates further

- 💸 Tariff costs of $300-400M erode margins more than expected

- 📉 AI CapEx spending decelerates, reducing data center power demand growth

- ⚖️ Baird's overcapacity thesis plays out as Siemens Energy and Mitsubishi ramp competing capacity

- 📊 Stock breaks below $800 gamma support, triggering momentum selling

- 🤒 Broader market correction hits premium-valuation industrial names hardest

Bull call spread P&L: Both calls expire worthless, loss = -$900K (-100% of premium)

The $800 level with 1.26B total gamma is the critical structural support. A break below that changes the entire technical picture. However, even in this scenario, the loss is capped at $900K - that's the beauty of the spread structure.

💡 Trading Ideas

🛡️ Conservative: "Power Grid Dividend Collector" - Covered Call Strategy

Play: Buy 100 shares of GEV at ~$860, sell the June 2026 $950 call against it

Why this works:

- 📊 Collect the option premium PLUS the $0.50/quarter dividend while you wait

- 🛡️ The premium from selling the call provides a buffer if the stock pulls back 3-5%

- 💰 If GEV rallies to $950, you make ~$90/share in stock appreciation + premium collected

- 📈 The $950 strike aligns with the monthly implied move upper range of $927 for March - achievable but not a gimme

- ⏰ June expiration gives time for Q1 earnings catalyst on April 22

Position sizing: ~$86,000 for 100 shares. Premium collected reduces cost basis. Set a stop-loss at $800 (gamma support).

Risk level: Lower (stock ownership with income) | Skill level: Beginner-Intermediate

⚖️ Balanced: "Ride the Backlog" - LEAP Bull Call Spread

Play: Buy the GEV January 2028 $900 call, sell the January 2028 $1,100 call

Why this works:

- 🎯 Mirrors the whale trade's thesis at a narrower, more achievable spread width

- 💸 Lower net debit than the whale's $900-$1,200 spread (roughly $60-70 per spread)

- 📊 Max profit: $200 spread width minus cost = roughly $130-140 per spread

- ⏰ Same 2-year LEAP timeframe captures the entire 2026-2028 growth cycle

- 📈 The $1,100 target aligns with LEAP implied move upper range of $1,157

- 🤖 Risk/reward roughly 2:1, with clearly defined max loss

Position sizing: 5-10 spreads at ~$65 each = $32,500-$65,000 risk for $65,000-$135,000 max profit.

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

🚀 Aggressive: "Full Power" - LEAP Call Into Earnings

Play: Buy GEV June 2026 $900 calls outright

Why this works (and why it's risky):

- 💥 Captures the Q1 earnings catalyst on April 22 and the turbine ramp confirmation by mid-2026

- 📊 $900 strike is only ~4.7% above the current $860 price and aligns with the gamma resistance level - a clean breakout target

- ⏰ 4 months to expiration - enough time for a catalytic move without paying for 2 years of time value

- 🚀 If GEV rallies to $1,000 by June, these calls could be worth ~$100 each

- 📈 The monthly implied move already suggests $927 is reachable by March OPEX

Why it could blow up:

- 💸 Paying pure time premium on a near-the-money LEAP

- ⏰ Q1 earnings miss or turbine ramp delay would crush the position

- 📉 The 44x trailing P/E means any execution stumble gets punished hard

- 🌬️ Offshore wind headline risk around the end-of-March deadline

Position sizing: Risk only what you can afford to lose completely. 2-3 contracts max for most retail accounts.

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

⚠️ Risk Factors

Don't get blindsided by these potential headwinds:

-

📊 Premium valuation: GEV trades at 44x trailing earnings and 56x forward, well above the US Electrical industry average of 35x. A LOT of good news is already priced in. Any execution miss could trigger a sharp 15-20% correction.

-

🌬️ Wind segment is still bleeding: Projected $400M EBITDA loss in 2026 with low-double-digit revenue decline. The offshore wind stop-work order could add another $250M revenue drag, and potential 900 job cuts signal the segment isn't turning around anytime soon.

-

⛏️ Yttrium supply chain risk: Hitting the 20 GW gas turbine production target by mid-2026 depends on securing yttrium (a rare earth element) amid China export controls. If China tightens further, the entire production ramp timeline could slip.

-

💸 Tariff exposure: $300-400M annually. About 25% of GEV's total direct spend is affected by tariffs. While the company is mitigating via contract pass-throughs and a $600M US factory investment, margin compression remains a real concern.

-

🏢 Prolec GE integration risk: The $5.275B acquisition needs to deliver synergies. Any integration missteps could pressure Electrification margins in the near term, right when the market expects accretion.

-

📉 Insider selling pattern: Corporate insiders sold ~$2.0M in shares over the last 3 months with no notable insider buying. While these are likely routine scheduled dispositions, it's worth noting that insiders aren't loading up at these levels.

-

⚖️ Overcapacity concerns: Baird downgraded GEV to Neutral citing competition and power overcapacity fears. If Siemens Energy and Mitsubishi Power ramp production faster than demand grows, pricing power could erode.

-

🌍 AI demand could decelerate: The entire bull thesis rests on AI data center power demand continuing to compound. If hyperscaler CapEx spending moderates or AI efficiency improvements reduce power needs, the demand curve flattens.

🎯 The Bottom Line

Here's the deal: A deep-pocketed institutional player just built a $900K net bull call spread on GEV with a nearly 2-year horizon, targeting a move from $844 to $900-$1,200 by January 2028. Both legs hit EXTREMELY UNUSUAL Z-scores (61.47 and 27.68), meaning this kind of trade size shows up just a few times per year in GEV options. This isn't someone hedging or rolling - this is a fresh, directional conviction bet on the power infrastructure supercycle.

What this trade tells us:

- 🎯 Institutional money believes GEV has at least +6.6% to the $900 breakeven and potentially +42% to the $1,200 max profit over two years

- 💰 The spread structure shows sophistication - they're not paying $2.3M for naked calls, they're cutting cost to $900K for a defined risk/reward profile

- ⏰ The January 2028 expiration captures the company's entire roadmap: turbine ramp, Prolec integration, data center order acceleration, nuclear SMR milestones, and the $56B revenue target

- 📊 The math works fundamentally: at 25x 2028 EBITDA of $11.2B, GEV's enterprise value would support ~$1,040/share

If you're bullish on GEV:

- ✅ Consider defined-risk strategies like bull call spreads rather than naked calls - follow the whale's playbook

- 📊 The $860 gamma resistance is the near-term level to watch - a clean break opens the path to $880-$900

- ⏰ Mark April 22 (Q1 earnings) as your first major thesis checkpoint

- 💡 The $800 gamma support is your downside line in the sand - set alerts there

If you're watching from the sidelines:

- 🎯 A pullback to the $820-$840 area (gamma support zone) would offer better risk/reward entry

- 📊 Wait for Q1 earnings on April 22 to see Prolec GE integration progress and turbine ramp data

- 📈 The analyst consensus average of $788-$851 suggests the stock is slightly above fair value right now, but Goldman's $925 target shows meaningful upside if execution delivers

If you're cautious:

- ⚠️ At 44x trailing earnings, GEV needs to keep delivering blowout quarters to justify the premium

- 📉 The Wind segment remains a $400M annual drag with no clear fix

- 🛡️ Consider selling put spreads below the $800 support level to generate income while waiting for a better entry - you get paid for patience

Key dates to mark:

- 📅 End of March 2026 - Offshore wind Sea Installer vessel deadline (binary catalyst)

- 📅 April 14, 2026 - Quarterly dividend payment ($0.50/share)

- 📅 April 22, 2026 - Q1 2026 earnings (first full quarter with Prolec GE)

- 📅 Mid-2026 - 20 GW gas turbine production ramp target

- 📅 H2 2026 - 2027 - BWRX-300 nuclear SMR regulatory milestones

- 📅 January 21, 2028 - THIS TRADE EXPIRES - the moment of truth for the $900K bull call spread

Final verdict: GE Vernova is the undisputed king of the AI power infrastructure trade. A record $150B backlog, 34% global gas turbine market share, turbines sold out through 2029+, and a clear path to $56B revenue by 2028 make a compelling fundamental case. This whale's $900-$1,200 bull call spread reflects that conviction with a disciplined, defined-risk structure. But at $860 with a 44x P/E, you're paying a premium for what the whole market already sees. The smarter retail play is to use defined-risk strategies, stay patient for pullbacks, and let the catalysts come to you. This is a 2-year story - you don't need to chase it today. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. LEAP bull call spreads are sophisticated instruments that can lose 100% of net premium if the stock doesn't reach the long strike by expiration. Always do your own research and consider consulting a licensed financial advisor before trading.

About GE Vernova: GE Vernova Inc. is the global leader in electric power - generating, transferring, converting, and storing electricity across gas turbines, wind energy, nuclear (SMR), grid equipment, and electrification solutions. Market cap of ~$236B in the Electronic & Other Electrical Equipment industry.