🔥 INTC Monster $29M Options Tsunami - Institutions Repositioning Ahead of CEO Transition! 🎢

📅 December 2, 2025 | 🔥 Extreme Unusual Activity Detected

🎯 The Quick Take

Holy moly! Someone just executed a $29.2 MILLION call spread on Intel at 11:01:10 this morning - and this isn't your typical bullish bet. This massive trade shows institutions ROLLING OUT of their March 2026 $40 calls ($14M closed), LOADING UP on March 2026 $50 calls ($9.4M opened), while simultaneously CLOSING March 2026 $60 calls ($2.2M) and SELLING new $40 calls ($3.6M). With Intel trading at $42.93 and new CEO Lip-Bu Tan taking over March 18, 2025, smart money is repositioning for a strategic reset. Translation: Institutions are adjusting their bets for Intel's turnaround, protecting gains while staying exposed to the 18A node breakthrough expected in 2025!

📊 Company Overview

Intel Corporation (INTC) is a legendary semiconductor pioneer fighting to reclaim its technological leadership:

- Market Cap: $190.8 Billion (86th most valuable company globally)

- Industry: Semiconductors & Related Devices

- Current Price: $42.93 (up from 52-week low of $17.67)

- Primary Business: Leading digital chipmaker focused on design and manufacturing of microprocessors for PC and data center markets, pioneered x86 architecture

- Employees: 108,900 (down from 124,800 after 23,000 job cuts)

- Current Status: Critical turnaround phase with $7.86B CHIPS Act funding, new CEO transition, and 18A process node validation expected 2025

💰 The Option Flow Breakdown

The Tape (December 2, 2025 @ 11:01:10):

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:01:10 | INTC | SELL | CALL $40 | 2026-03-20 | $14M | $40 | 22K | 36K | 20,000 | $42.93 | $7.11 | INTC 40C 03/20 |

| 11:01:10 | INTC | BUY | CALL $50 | 2026-03-20 | $9.4M | $50 | 27K | 19K | 26,000 | $42.93 | $3.60 | INTC 50C 03/20 |

| 11:01:10 | INTC | SELL | CALL $40 | 2026-03-20 | $3.6M | $40 | 27K | 36K | 5,000 | $42.93 | $7.12 | INTC 40C 03/20 |

| 11:01:10 | INTC | SELL | CALL $60 | 2026-03-20 | $2.2M | $60 | 13K | 25K | 12,000 | $42.93 | $1.85 | INTC 60C 03/20 |

🤓 What This Actually Means

This is a sophisticated repositioning trade executed as a multi-leg spread! Here's what went down:

- 💸 Net capital flow: $29.2M total premium exchanged across all legs in synchronized execution

- 🔄 Complex structure: Closing profitable $40 calls ($17.6M collected), buying higher $50 calls ($9.4M paid), closing $60 calls ($2.2M collected)

- 🎯 Strategic timing: March 20, 2026 expiration (107 days out) captures new CEO Lip-Bu Tan's first month in office (starts March 18), Q4 2024 earnings (Jan 30), 18A node volume production milestones, potential Apple foundry deal announcements

- 📊 Massive size: 63,000 total contracts across all legs representing ~6.3 million shares worth $270M+ of underlying exposure

- 🏦 Institutional complexity: This is professional portfolio management adjusting risk profile for new catalysts

What's really happening here: This trader is ROLLING their position structure to reflect changing Intel thesis. They're taking profits on deep in-the-money $40 calls (now worth $7.11 with stock at $42.93), using that capital to fund new $50 strike calls at $3.60, while closing out-of-the-money $60 calls that have limited upside in near term.

The new position structure:

- ✅ Long 26,000 calls at $50 strike = bullish on Intel reaching $50+ by March expiration (16.5% upside needed)

- ❌ Closed 25,000 calls at $40 strike = locked in profits from stock rally from low-$30s to $43

- ❌ Closed 12,000 calls at $60 strike = removed excessive upside bet (40% rally unlikely in 107 days)

Translation: This institution believes Intel can rally to $50 (reasonable 16% gain) driven by new CEO momentum and 18A validation, but doesn't expect explosive $60+ moonshot. They're optimizing for the "successful turnaround starts showing progress" scenario rather than "everything goes perfectly" scenario.

Unusual Score: 🔥🔥 EXTREMELY UNUSUAL across all legs

- $40 call close (20K): Z-score 5.3 = 5.3x more unusual than recent activity (happens few times a month)

- $50 call open (26K): Z-score 14.66 = EXTREMELY unusual (14.66x average, happens few times a year!)

- $40 call short (5K): Z-score 6.61 = extremely unusual

- $60 call close (12K): Z-score 2.27 = highly unusual

The $50 call purchase with Z-score 14.66 is the real story - this level of buying happens maybe 3-4 times per year. When combined with simultaneous closing of $40 and $60 positions, it screams "major portfolio adjustment by large institution."

📈 Technical Setup / Chart Check-Up

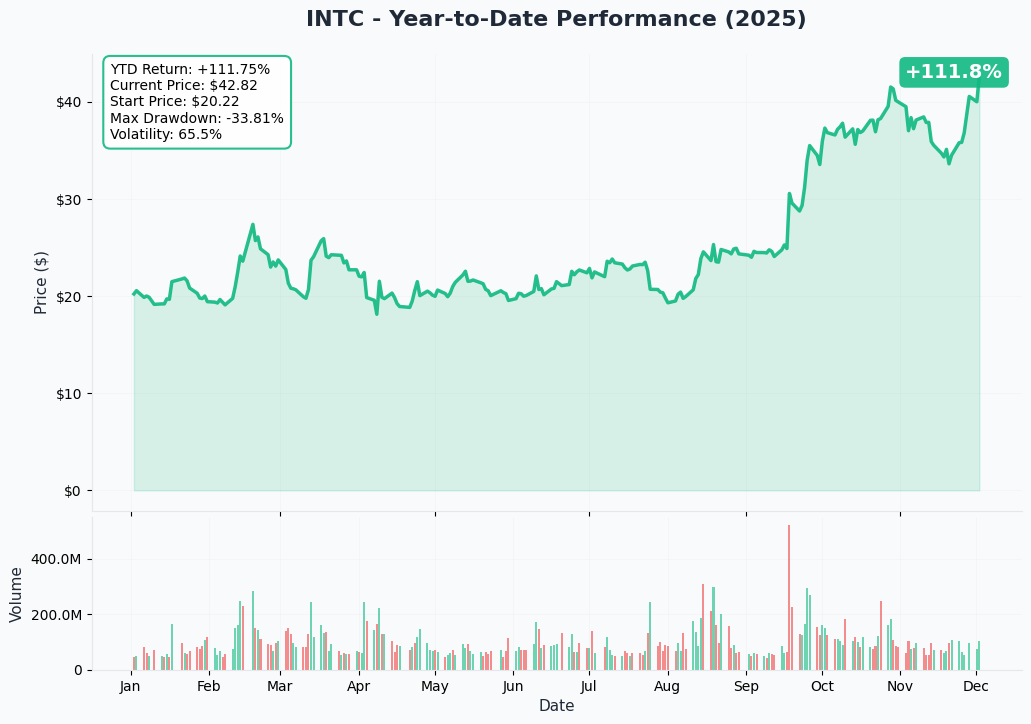

YTD Performance Chart

Intel is staging an impressive comeback - up +126.5% from 52-week low of $17.67 to current price of $42.93. The chart tells a redemption story after years of execution failures under former CEO Pat Gelsinger.

Key observations:

- 📈 Epic recovery: Massive rally from $17.67 low in August 2024 to $42.48 high - more than doubling on CHIPS Act funding and Apple foundry deal rumors

- 🎢 High volatility period: Stock surged 10% in late November on Apple partnership speculation

- 💥 Leadership catalyst: Pat Gelsinger forced out December 1, 2024 after stock fell 61% during his tenure

- 🚀 New CEO bounce: Lip-Bu Tan appointment effective March 18, 2025 bringing foundry expertise and shareholder confidence

- ⚠️ Still below all-time highs: Trading around $43 vs historical highs in $60-70 range - plenty of room to recover IF turnaround executes

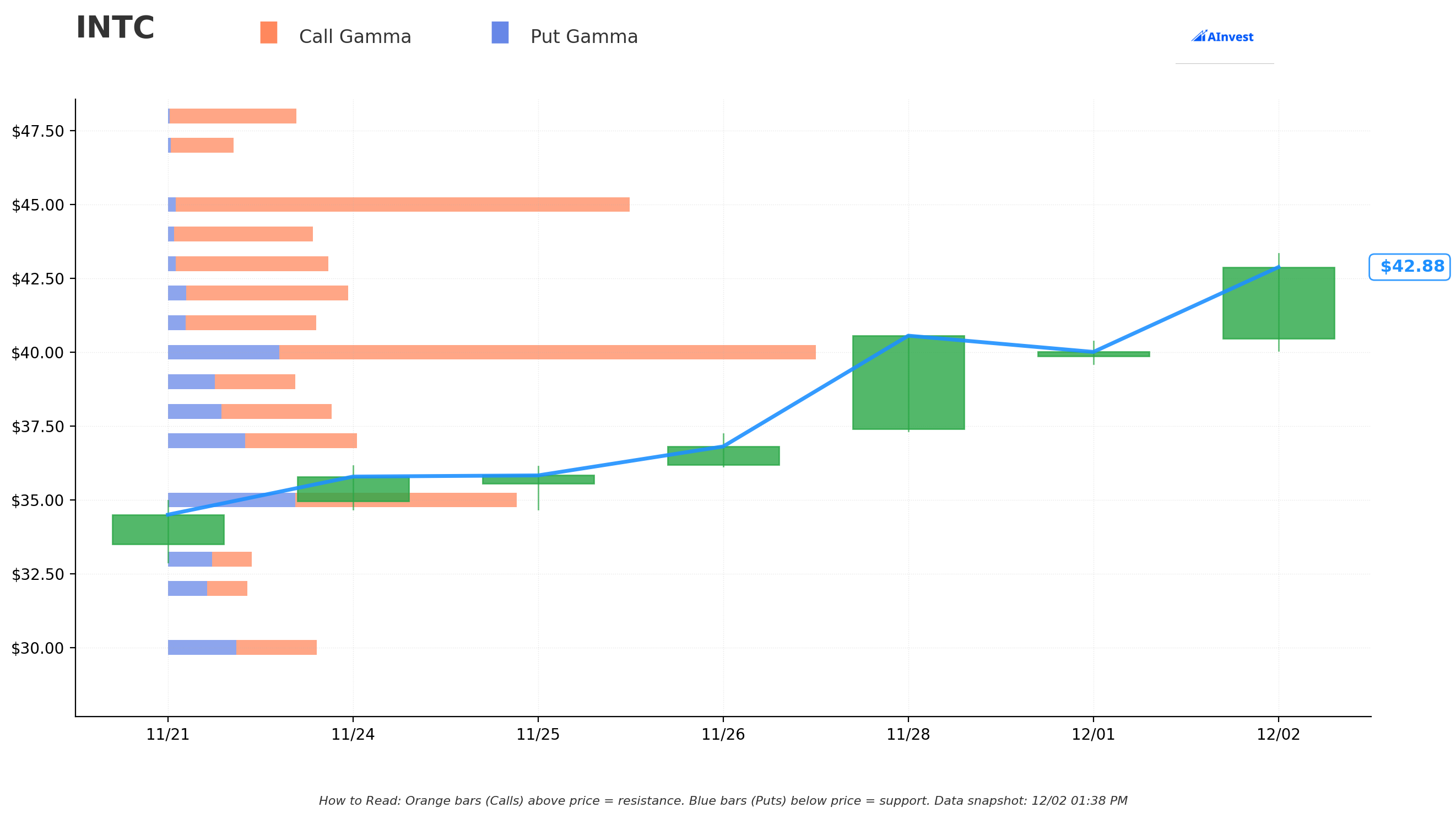

Gamma-Based Support & Resistance Analysis

Current Price: $42.86

The gamma exposure map reveals critical price magnets where Intel's stock will likely gravitate based on massive options positioning:

🔵 Support Levels (Put Gamma Below Price):

- $42 - Immediate support with 17.9B total gamma exposure (14.3B call + 1.8B put = strongest nearby floor!)

- $41 - Secondary support at 14.8B gamma (11.3B call + 1.7B put)

- $40 - MAJOR structural floor with 64.4B gamma (53.3B call + 11.1B put = MASSIVE PUT GAMMA WALL - this is the LINE IN THE SAND!)

- $38 - Deep support at 16.3B gamma (11.0B call + 5.3B put)

- $37 - Extended support zone with 18.8B gamma (11.1B call + 7.7B put)

- $35 - Disaster floor at 34.7B gamma (22.0B call + 12.7B put)

🟠 Resistance Levels (Call Gamma Above Price):

- $43 - Immediate ceiling with 16.0B gamma (15.2B call + 0.8B put = dealers will sell rallies here!)

- $44 - Secondary resistance at 14.4B gamma (13.8B call + 0.6B put)

- $45 - Major ceiling zone with 45.8B gamma (45.1B call + 0.8B put = STRONGEST OVERHEAD RESISTANCE!)

- $50 - Extended upside target at 42.0B gamma (41.7B call + 0.3B put = EXACTLY WHERE THE CALL BUYER STRUCK!)

What this means for traders: Intel is trading in a tight range between massive $42 support and crushing $43-$45 resistance zone. The gamma data shows $40 is THE critical support with 64.4B gamma (largest single level) - this is where the original $40 calls were struck that this trader just closed. If Intel breaks below $40, it could accelerate toward $38-$35.

On the upside, $45 represents a HUGE resistance wall at 45.8B gamma. Breaking through $45 opens the path to the $50 target where this institutional trader positioned their 26,000 new calls. The $50 level has 42.0B gamma sitting there like a price magnet.

Notice the trade structure? The trader:

- ✅ Sold $40 calls = at massive 64.4B gamma support (smart profit-taking!)

- ✅ Bought $50 calls = at 42.0B gamma level (betting on breakthrough to this magnet)

- ✅ Closed $60 calls = too far from significant gamma zones (removing lottery ticket)

Net GEX Bias: BULLISH (375.7B call gamma vs 96.1B put gamma = 3.9:1 ratio) - Overall positioning heavily bullish, but immediate price action constrained by $43-45 resistance band.

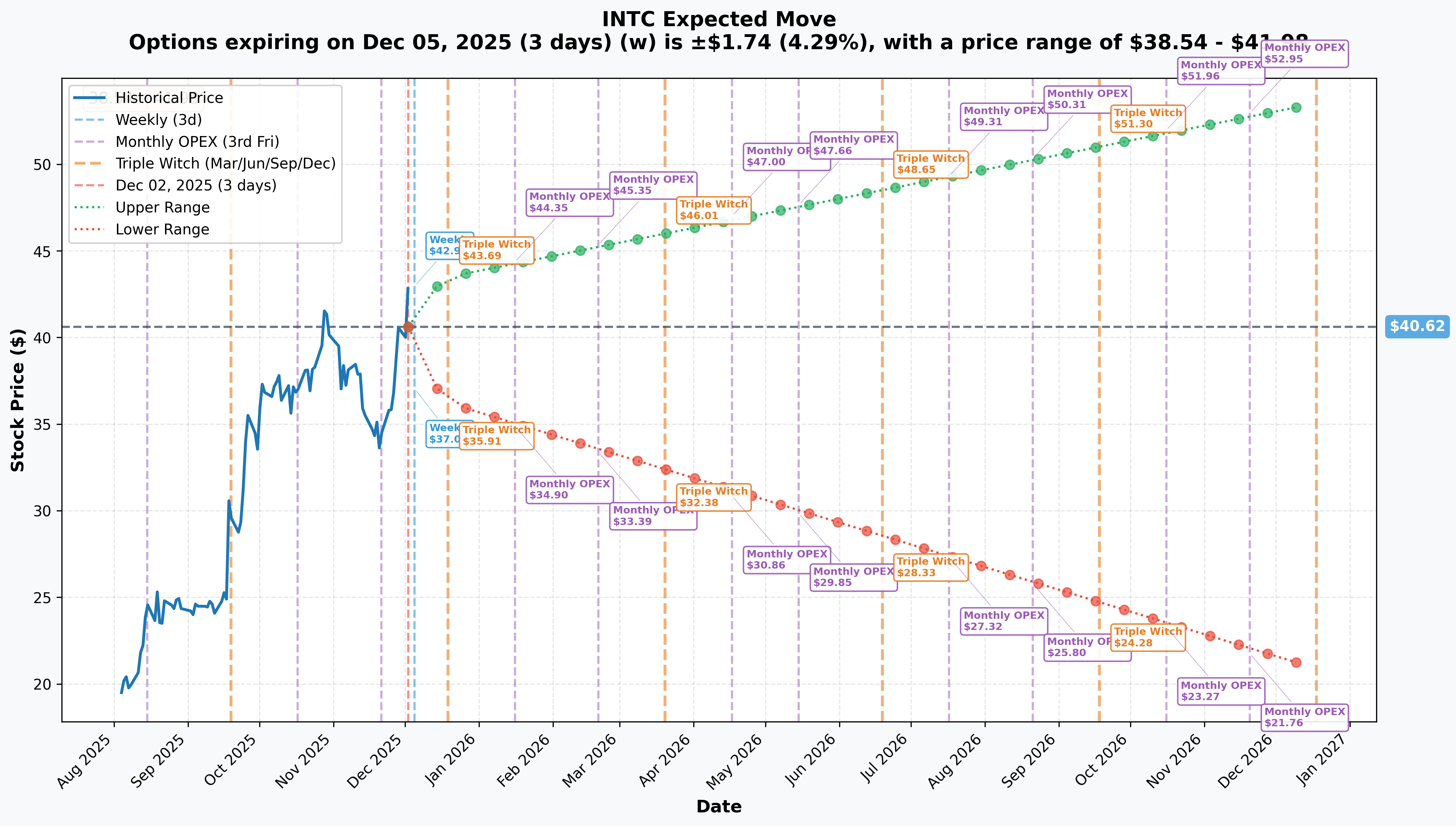

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 5 - 3 days): ±$1.74 (±4.29%) → Range: $38.54 - $41.98

- 📅 Monthly OPEX (Dec 19 - 17 days): ±$3.39 (±8.35%) → Range: $36.21 - $43.50

- 📅 Quarterly Triple Witch (Dec 19 - 17 days): ±$3.39 (±8.35%) → Range: $36.21 - $43.50

- 📅 January OPEX (Jan 16 - 45 days): ±$4.71 (±11.60%) → Range: $34.90 - $44.35

- 📅 March OPEX (Mar 20 - 107 days - THIS TRADE!): ±$8.62 (±21.23%) → Range: $32.38 - $46.01

Translation for regular folks: Options traders are pricing in a 4.3% move ($1.74) by this Friday for weekly expiration, and an 8.4% move ($3.39) through December monthly OPEX. But look at the March 20th expiration (when this massive trade expires) - the market is pricing a 21.2% move ($8.62) which gives a range of $32.38 to $46.01.

This aligns PERFECTLY with the institutional trader's positioning! The upper range of $46.01 is just below their $50 call strike, suggesting they believe Intel has a realistic shot at reaching that level if execution improves under new CEO Lip-Bu Tan and 18A node delivers.

Key insight: The sharp increase in implied volatility from 4.3% (weekly) to 21.2% (March expiration) reflects massive uncertainty around:

- Q4 2024 earnings on January 30, 2025 - critical first results under new leadership

- New CEO Lip-Bu Tan taking over March 18, 2025 - just 2 days before this option expires!

- 18A node volume production milestones in 2025

- Potential Apple foundry deal announcements

Smart money is paying up for this March expiration because THE critical turnaround validation events all happen in this window!

🎪 Catalysts

🔥 Past Catalysts (What Already Happened)

Leadership Transition Complete - New CEO Announced (December 2024) 👔

Intel's most dramatic leadership shake-up just concluded:

- 😰 Pat Gelsinger forced out December 1, 2024 after contentious board meeting over lack of turnaround progress

- 📉 Stock declined 61% during Gelsinger's tenure (Feb 2021 - Dec 2024), company posted $16.6B loss in Q3 2024 (largest quarterly loss ever!)

- ✅ MAJOR CATALYST: Lip-Bu Tan appointed CEO effective March 18, 2025 - former Cadence CEO and ex-Intel board member who resigned in August 2024 over foundry strategy disagreements

- 🚀 Considered top candidate by shareholders and analysts, bringing semiconductor industry expertise and credibility

CHIPS Act Funding Finalized (November 26, 2024) 💰

Intel secured confirmed $7.86B in direct CHIPS Act funding:

- 💵 Final award: $7.86B (reduced from preliminary $8.5B due to separate $3B DoD contract)

- 🏗️ Additional benefits: up to $11B in low-interest loans + 25% investment tax credit on up to $100B capex

- 🇺🇸 Investment commitments: $100B+ across Arizona ($32B+), Ohio ($28B), Oregon ($36B), New Mexico ($4B)

- 👷 Expected to support 10,000+ Intel jobs, 20,000 construction jobs, 50,000+ indirect jobs

- ✅ This removes major funding uncertainty - Intel now has confirmed government backing for foundry buildout

Q3 2024 Earnings Beat (October 31, 2024) 📊

Most recent quarterly results showed mixed picture:

- 📈 Revenue: $13.3B (beat estimate of $12.944B), up 4% sequentially but down 6% YoY

- 😱 GAAP Net Loss: $16.6B (largest ever) vs $0.3B profit in Q3 2023

- 💸 Non-GAAP EPS: -$0.46 vs consensus -$0.02 (massive miss)

- ⚠️ Non-GAAP gross margin: 18% impacted by $3B impairment of Intel 7 assets

- 📉 Annual performance: 2024 revenue $53.1B down 2% YoY from $54B in 2023

18A Node Major Milestones Achieved (Q4 2024) 🏭

Critical technical validation completed:

- ✅ Panther Lake (AI PC) and Clearwater Forest (server) successfully booted OS - HUGE proof point!

- ⚡ Power-on achieved less than 2 quarters after tape-out - ahead of schedule

- 🔬 First successful implementation of RibbonFET gate-all-around transistors and PowerVia backside power

- 🏢 Fab 52 in Arizona successfully processed first wafer through facility

- 📈 Volume production scheduled for 2025 in Oregon fabs with Arizona ramping later

🚀 Upcoming Catalysts (Next 6 Months - Through March Expiration!)

Q4 2024 Earnings Report - January 30, 2025 (58 DAYS!) 📊

This is THE FIRST major test of the turnaround under interim leadership:

- 📅 Date: January 30, 2025 after market close

- 🎯 Expected revenue: $13.8B (midpoint of guidance range $13.3-14.3B)

- 💰 Expected non-GAAP EPS: $0.12

- ⚖️ Key metrics to watch:

- Revenue vs guidance

- 2025 full-year guidance (CRITICAL for validating turnaround timeline)

- Capital allocation and foundry spin-off updates

- Progress on $10B cost reduction plan

- 18A production ramp commentary

- Customer win announcements

Why this matters for the option trade: This earnings happens 49 days before the March 20 expiration. If Intel delivers strong results with optimistic 2025 guidance, it could spark rally toward $50 target. Disappointing results could send stock back toward $35-38 range.

New CEO Lip-Bu Tan Assumes Role - March 18, 2025 (106 DAYS!) 🎯

The institutional trader positioned for this EXACT catalyst:

- 👔 Lip-Bu Tan becomes permanent CEO March 18, 2025 - just 2 DAYS BEFORE the March 20 option expiration!

- 🔄 Potential strategic review and foundry strategy changes given Tan's prior board disagreements

- 📈 Street expects "honeymoon period" rally when new CEO officially starts

- 🎤 First earnings call as permanent CEO expected late April/early May 2025 (Q1 2025 results)

- 💡 Brings credibility with investors - considered top choice by analysts and shareholders

This is NOT a coincidence! The option buyer structured March 20 expiration to capture the CEO transition announcement impact. If market reacts positively to Tan officially taking helm, stock could rally in those final 2 days before expiration.

Apple Foundry Deal Potential Announcement (Q1 2026 Timeline) 🍎

Rumors intensified in late November 2025:

- 🤝 Intel would manufacture Apple M-series chips (15-20M chips annually starting 2027)

- 📋 Apple signed NDA for Intel 18AP process design kit access (0.9.1 GA revision)

- 🎯 Next milestone: Intel 18AP PDK 1.0/1.1 delivery expected Q1 2026

- 💰 Estimated revenue potential: $1.5-$2B annually (assuming $80-100/chip ASP)

- ⚠️ Important: Pre-contract stage; no confirmed manufacturing agreement yet

- 🚨 Stock surged 10% on these rumors alone!

Potential catalyst: Any formal announcement or leaked progress on Apple deal validation would be MASSIVE for Intel shares, potentially driving toward $50-55 range instantly.

18A Node Volume Production Ramp (Throughout 2025) 🏭

Currently in risk production, volume manufacturing expected in 2025:

- 📅 Volume production begins in Oregon fabs with Arizona ramping later in 2025

- 💻 Panther Lake (Client): High-volume production ramp in 2025, first SKUs ship by end of 2025

- 🖥️ Clearwater Forest (Server): Launch timing H1 2026 but production news expected Q1 2025

- 🏢 Microsoft chip design confirmed to be produced on Intel 18A

- 📊 Total of 3 Intel 18A customers signed (one major unnamed with large prepayment)

Why this is CRITICAL: 18A is Intel's "prove it or lose it" moment. Successful volume production with good yields validates the entire foundry strategy and justifies the massive CHIPS Act investment. Any delays or yield issues would be catastrophic.

Potential Foundry Spin-Off or Restructuring Announcements (Q1 2025) 🔄

Management considering foundry spin-off or restructuring:

- 💸 Intel Foundry posted $2.8B operating loss in Q2 2024, billions in cumulative losses

- 🔀 New CEO Lip-Bu Tan may accelerate restructuring given his foundry expertise

- 📊 Potential scenarios: Full spin-off, partial IPO, or strategic partnership

- 🎯 Could unlock shareholder value if foundry separated from products business

- ⚠️ Also carries execution risk - complex separation could distract from core operations

⚠️ Risk Catalysts (Negative - Could Hurt the Trade)

Export Restrictions & China Headwinds 🇨🇳

- 🚨 Ongoing geopolitical tensions create uncertainty for China revenue (historically 25-30% of sales)

- ⚖️ Future export controls could impact new products without warning

- 💸 Lost China revenue would offset gains from U.S. sovereign AI projects

Continued Market Share Losses to AMD/Arm ⚔️

- 📉 AMD gaining market share in both client and server CPUs

- 🔀 Arm-based alternatives (AWS Graviton, Ampere) growing in data centers

- 💰 Pricing pressure to remain competitive could hurt margins

Macroeconomic Headwinds 📉

- 💻 PC market structural decline affects Intel's core business

- 🏢 Data center spending slowdown would impact server CPU demand

- 💸 Higher interest rates increase cost of $11B CHIPS Act loans

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through March 20th expiration:

📈 Bull Case (35% probability)

Target: $48-$52 ($50 CALL STRIKE!)

How we get there:

- 💪 Q4 earnings on Jan 30 BEAT with revenue toward $14B+ high-end and positive 2025 guidance

- 🚀 18A volume production ramp proceeds ahead of schedule with strong yields reported

- 🍎 Apple foundry deal progress announced or leaked - validation testing going well

- 👔 New CEO Lip-Bu Tan (March 18) receives positive market reception and announces strategic initiatives

- 🏢 Additional 18A customer wins beyond the existing 3 customers

- 💰 Foundry restructuring plan announced that unlocks shareholder value

- 📈 Breakout above $45 gamma resistance (45.8B) triggers technical rally to $50 (42.0B gamma magnet)

- 🎯 Market begins pricing in 2026 turnaround success (Panther Lake launch, Clearwater Forest, improved margins)

Key metrics needed:

- 2025 revenue guidance showing return to growth

- 18A production milestones met on schedule

- Gross margins expanding trajectory toward 50%+

- Client and server market share stabilizing

Probability assessment: 35% because it requires solid execution across multiple fronts BUT new CEO brings credibility reset and 18A technical milestones already achieved. The $50 target is realistic (16.5% upside) if turnaround story gains traction. Notice the institution bought $50 calls at $3.60 - they clearly think odds are better than 35%.

Call P&L in Bull Case:

- Stock at $50 on March 20: $50 calls worth ~$0 (at-the-money), small loss of ~$3.60/share × 26,000 = -$9.4M

- Stock at $52 on March 20: Calls worth $2.00, reduced loss = -$1.60/share × 26,000 = -$4.2M

- Stock at $55 on March 20: Calls worth $5.00, profit = $1.40/share × 26,000 = $3.6M gain (38% ROI)

- Stock at $60 on March 20: Calls worth $10.00, profit = $6.40/share × 26,000 = $16.6M gain (177% ROI!)

🎯 Base Case (45% probability)

Target: $40-$46 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ Solid Q4 earnings meeting consensus ($13.7-13.9B revenue, $0.10-0.12 EPS)

- 📱 18A ramp progressing on track but not spectacular - steady production without major customer win announcements

- ⚖️ 2025 guidance cautiously optimistic but conservative given macro uncertainty

- 🍎 Apple foundry deal remains in validation phase - no formal announcement yet but progress continues

- 👔 CEO transition smooth, Tan receives positive initial reception but wait-and-see approach from investors

- 🔄 Trading within gamma support ($40-$42) and resistance ($43-$45) bands for weeks

- 📊 Market digests massive 2024 recovery (+126% from lows), waits for Panther Lake launch proof points

- 💤 Volatility moderates after January earnings (IV from current levels to 35-40% range)

This is likely the option trader's target scenario: Stock consolidates in low-to-mid $40s, the $50 calls expire worthless or slightly out of money, but overall trade was profitable because they:

- Locked in profits on $40 calls bought when stock was in $30s ($17.6M collected!)

- Closed $60 calls before time decay accelerates ($2.2M recovered)

- Maintains upside exposure via $50 calls in case turnaround accelerates

Why 45% probability: Intel at technical and fundamental inflection point. New CEO brings hope but needs time to execute. 18A technically validated but commercial success TBD. Most professional investors will hold current positions and wait for next major catalyst (actual Panther Lake shipments, Apple deal finalization).

📉 Bear Case (20% probability)

Target: $35-$40 (TEST CRITICAL SUPPORT!)

What could go wrong:

- 😰 Q4 earnings miss or disappointing 2025 guidance - even meeting lowered expectations might not satisfy at current valuation

- 🚨 18A production issues emerge - yield problems, delays in customer chip production, or technical setbacks

- ⏰ Apple foundry deal falls apart or significantly delayed - rumors cool, no formal announcement materializes

- 🇨🇳 New China export restrictions hit revenue opportunities

- 💸 Broader tech/semiconductor selloff drags Intel lower despite good fundamentals

- 📊 AMD continues aggressive market share gains in client and server, Intel loses pricing power

- 🤖 AI accelerator (Gaudi 3/4) adoption slower than expected vs Nvidia dominance

- 💰 Foundry losses continue mounting ($3B+/quarter) with no clear path to profitability

- 🔨 Break below $40 gamma support (64.4B - massive wall!) triggers cascade to $38, then $35

Critical support levels:

- 🛡️ $42: First gamma floor (17.9B) - current support holding

- 🛡️ $40: MAJOR gamma floor (64.4B - largest level!) - MUST HOLD or momentum shifts bearish

- 🛡️ $38: Deep support (16.3B gamma) - warning signal

- 🛡️ $35: Extended floor (34.7B gamma) - disaster scenario

Probability assessment: Only 20% because Intel has significant positive catalysts (CHIPS funding confirmed, new credible CEO, 18A milestones achieved, potential Apple deal). The bear case requires multiple failures simultaneously. However, execution risk remains very real given years of disappointments.

Why institution closed $40 calls and $60 calls:

- If stock drops to $35-38, they protected $17.6M+ in gains by closing $40 calls early

- The $50 calls would be worthless but only lost $9.4M vs keeping $40 calls which would give back all profits

💡 Trading Ideas

🛡️ Conservative: Cash Gang Until CEO Transition Clarity

Play: Stay on sidelines until after Lip-Bu Tan officially starts March 18 and market digests his initial direction

Why this works:

- ⏰ Q4 earnings on January 30 creates binary event risk - stock could gap $3-5 either direction

- 👔 CEO transition March 18 adds significant uncertainty - will he accelerate foundry spin-off? Change strategy?

- 📊 Intel still in "prove it" mode - 18A technical success doesn't guarantee commercial wins

- 💸 Multiple quarters needed to validate turnaround is real vs false start

- 🎯 Better entry likely post-March expiration after option-driven volatility settles

- 🤔 Even sophisticated institutions are repositioning (this $29M trade!) - signals uncertainty

Action plan:

- 👀 Watch January 30 earnings for revenue ($13.8B+ target), 2025 guidance quality, 18A production commentary

- 🎯 Monitor new CEO Lip-Bu Tan's first public statements and strategic announcements after March 18

- ✅ Need to see Panther Lake customer feedback and 18A yield data before committing capital

- 📊 Look for pullback to $38-40 range (10-15% below current) for stock entry with margin of safety

- ⏰ Revisit Q2 2025 when Panther Lake actual shipments and customer reviews provide validation

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -10-15% drawdown if earnings or CEO transition disappoints. Get better entry if stock consolidates or corrects. Maintain full optionality for when picture becomes clearer.

⚖️ Balanced: Bull Call Spread (Copy The Pros' Structure!)

Play: After January earnings, replicate institutional positioning with defined-risk bull call spread

Structure: Buy $45 calls, Sell $50 calls (March 20 expiration - SAME as the institutional trade!)

Why this works:

- 🎢 Post-earnings IV crush makes spreads cheaper - buy AFTER volatility drops 30-40%

- 📊 Defined risk spread ($5 wide = $500 max risk per spread)

- 🎯 Targets breakout above $45 gamma resistance (45.8B) toward $50 where institution positioned

- 🤝 Essentially "copying" smart money positioning at better post-earnings prices

- ⏰ Captures new CEO Lip-Bu Tan transition (March 18) and potential strategic announcements

- 🛡️ Limited downside risk if turnaround takes longer than expected

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Pay ~$2.00-2.50 net debit per spread post-earnings (vs $3.00+ now)

- 📈 Max profit: $250-300 per spread if Intel above $50 at March expiration (100-150% ROI!)

- 📉 Max loss: $200-250 per spread if Intel below $45 (defined and acceptable)

- 🎯 Breakeven: ~$47-47.50

- 📊 Risk/Reward: ~1:1 to 1.5:1 which is solid for defined-risk bullish play

Entry timing:

- ⏰ Wait 2-3 days after January 30 earnings (by Feb 2-3) for full IV collapse

- 🎯 Only enter if earnings showed positive signals (guidance up, 18A on track, optimistic 2025 outlook)

- ❌ Skip if stock already above $47 (spread too expensive) or below $40 (bearish breakdown)

- ✅ Ideal entry: Stock in $42-45 range after earnings with constructive forward guidance

Position sizing: Risk only 3-5% of portfolio (this is directional speculation on turnaround thesis)

Exit strategy:

- 🎯 Take profits if stock hits $48-49 before expiration (don't wait for $50 - capture 80% of max gain)

- 🛑 Exit if stock breaks below $40 support after entry (cut losses early)

- ⏰ Consider rolling to June expiration if stock at $47-48 with 2 weeks to go (extend timeline)

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

🚀 Aggressive: Straddle the CEO Transition - Bet on VOLATILITY (ADVANCED!)

Play: Buy straddle betting on explosive move around new CEO Lip-Bu Tan's first week in office

Structure: Buy $43 calls + Buy $43 puts (March 20 expiration)

Why this could work:

- 💥 March 20 expiration captures TWO massive catalysts: Q4 earnings (Jan 30) AND new CEO start (March 18 - 2 days before expiration!)

- 🎰 Implied move 21.2% ($8.62) but Intel historically moves 15-25% on major catalyst combinations

- 📊 New CEO taking over could announce MAJOR strategic shifts (foundry spin-off, cost cuts, M&A, partnerships)

- 🚀 Street underpricing CEO transition impact - this isn't just a new executive, it's someone who QUIT THE BOARD over strategy disagreements!

- ⚡ Either direction works: Bull case ($50+) or bear case ($35-38) both profitable

- 📈 Institutional repositioning (this $29M trade!) signals big money expects volatility

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Straddle costs ~$6-8 ($600-800 per straddle)

- ⏰ TIME DECAY KILLER: Theta burns -$30-50/day as expiration approaches (107 days of decay!)

- 😱 IV CRUSH: Post-earnings IV collapse could destroy value even if stock moves 8-10%

- 📊 Two-way risk: Stock could consolidate in $40-46 range for 3 months and you lose entire premium

- 🎢 Need 15%+ move ($6-7) just to breakeven after IV and time decay

- ⚠️ Earnings could be "fine" and CEO transition "smooth" - stock stays $41-44 (only 3% move) and straddle loses 60-80%

Estimated P&L:

- 💰 Cost: ~$6-8 per straddle (adjust based on current IV - check when entering!)

- 📈 Profit scenario: Stock moves to $50+ or $36- (15%+ either way) = $6-7+ gain (75-100% ROI)

- 🚀 Home run: Stock moves to $55 or $33 (25%+ move) = $10-12 gain (150-200% ROI!)

- 📉 Loss scenario: Stock ends $39-47 range = lose $3-6 (40-75% loss)

- 💀 Total loss: Stock flat at $43 = lose entire $6-8 (100% loss)

Breakeven points:

- 📈 Upside breakeven: ~$49-51 (need 15-19% rally)

- 📉 Downside breakeven: ~$35-37 (need 15-19% drop)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded straddles through MULTIPLE catalysts and understand dual IV crush risk

- ✅ Can afford to lose ENTIRE premium (very real possibility!)

- ✅ Understand you're betting Intel will have EXPLOSIVE move (not gradual drift)

- ✅ Can monitor closely and take profits quickly after catalysts (don't hold to expiration)

- ✅ Have experience with CEO transition volatility patterns

- ⏰ Plan to potentially close partial position after January earnings, hold remainder for CEO transition

Advanced tactic for experienced traders:

- 🎯 Enter 50% position size after January earnings if stock moved <5%

- 📊 This captures remaining CEO transition volatility at lower IV cost

- ⚠️ Still extremely risky - only for those who truly understand straddle mechanics

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced/Expert only

Probability of profit: ~35-40% (requires big move AND good timing on exit)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Double catalyst uncertainty: Q4 earnings January 30 PLUS new CEO March 18 creates MASSIVE volatility window. Either event could gap stock $3-5 overnight. Historical precedent shows CEO changes can move stock 10-20% as new leader announces strategic shifts. Combined with earnings binary risk, this is explosive setup.

-

💸 18A execution remains unproven commercially: While Panther Lake and Clearwater Forest successfully booted, actual volume production with competitive yields is different challenge. Intel has history of process node delays (10nm, 7nm credibility gap). Any yield issues or production delays in 2025 would be catastrophic for foundry thesis and stock would collapse toward $30-35.

-

🍎 Apple foundry deal is PURE SPECULATION: Reports show Apple signed NDA for design kit access but this is PRE-contract stage. Stock surged 10% on rumors alone - imagine the crash if deal falls apart or gets delayed beyond 2027. Apple could easily stay 100% with TSMC (their trusted partner for 15+ years) rather than risk Intel execution. Market may be pricing in deal that never happens.

-

💰 Foundry bleeding cash with no clear path to profitability: Intel Foundry posted $2.8B operating loss in Q2 2024, billions in cumulative losses over multiple quarters. Only 3 announced 18A customers - needs 20-30+ to justify investment. New CEO Lip-Bu Tan may decide foundry strategy is unfixable and recommend spin-off/shutdown, which would be strategic admission of failure.

-

📉 Massive losses continue: $16.6B Q3 2024 loss (largest ever!) reflects deep structural problems beyond just restructuring charges. Three consecutive years of revenue decline ($79B→$63B→$54B→$53B) shows core business deteriorating while competitors gain share. Even with CHIPS Act funding, Intel burning through cash at unsustainable rate.

-

🇨🇳 China geopolitical wildcard: Historically 25-30% of Intel revenue from China. Export restrictions could expand without warning, removing billions in revenue overnight. Competition from Chinese domestic chipmakers (SMIC, Huawei) reduces Intel's China growth potential even without export controls.

-

⚔️ AMD/Arm competitive pressure accelerating: AMD hit record 30.2% desktop CPU market share in Q2 2025, Arm-based alternatives growing in servers. Intel's decades-long CPU dominance being dismantled. Losing pricing power forces margin compression even if revenue stabilizes. Can't win back share without aggressive pricing which destroys profitability.

-

📊 Analyst sentiment tepid despite rally: Average 12-month target $22-37 range with average brokerage rating 3.21/5.0 (between Hold and Moderate Sell). Only 1 out of 38 analysts rates Strong Buy (2.63%). Street doesn't believe turnaround story yet - rally could reverse quickly if thesis cracks.

-

🎢 Stock up 126% from lows - vulnerable to profit-taking: Massive recovery from $17.67 to $42.93 over ~4 months means many holders sitting on triple-digit gains. Any disappointment triggers wave of selling as early buyers lock in profits. Technical pullback to $38-40 wouldn't be surprising even without fundamental catalyst.

-

💵 Dividend suspended, -$4.4B operating free cash flow deficit: Signals severe financial stress. Traditionally dividend-paying blue chip forced to cut payout reduces investor base (many funds require dividends). Won't be reinstated until cash flow improves significantly (2026+ at earliest).

-

🏢 Morale risk from 23,000 job cuts: Workforce reduced from 124,800 to 108,900 over 2 years. Remaining employees demoralized, brain drain as top talent leaves for competitors. Hard to execute ambitious 18A roadmap with depleted, stressed engineering teams.

-

📉 Macro recession risk: If economy weakens in 2025-2026, enterprise IT budgets get cut first. PC market already in structural decline - recession accelerates that. Data center spending highly cyclical. Even perfect execution won't save Intel from 20-30% correction in recession scenario.

🎯 The Bottom Line

Real talk: A sophisticated institution just executed a $29.2 MILLION options repositioning that tells a very specific story about Intel's next 4 months. This wasn't a simple bull or bear bet - this was professional risk management adjusting exposure for changing probabilities.

What this complex trade reveals:

The trader is saying: "Intel's turnaround has potential (that's why we bought $50 calls for $9.4M), BUT we're taking chips off the table from our original bullish bet (closed $40 calls for $17.6M profit) and removing the moonshot scenario (closed $60 calls for $2.2M)."

Translation of position structure:

- ✅ Closed $40 calls: "We made bank on the rally from $30s to $43, locking in gains before January earnings and CEO transition risk"

- ✅ Bought $50 calls: "We believe new CEO Lip-Bu Tan + 18A success can push Intel to $50 (16% upside), but we're paying only $3.60 for that bet"

- ❌ Closed $60 calls: "Stock reaching $60 (40% rally) in next 4 months is unrealistic - Intel's not going to moon, this is gradual turnaround"

- ❌ Sold new $40 calls: "Funding part of the $50 call purchase by selling premium at current support level"

This is NOT a "sell everything" signal - it's a "adjust your expectations and manage risk" signal.

The institutional thesis appears to be:

-

🎯 Intel has legitimate path to $48-52 by March if:

-

⚠️ BUT significant risk remains that stock consolidates in $38-45 range if:

- Earnings are "fine but not exciting"

- CEO transition takes time to show results

- 18A production is "on track" but no major customer wins announced

- Apple deal remains in validation phase without commitment

-

💰 The right play is: Protect gains from the $30s→$43 rally, maintain upside exposure to $50 target, eliminate unlikely $60+ scenarios

If you own Intel:

- ✅ Consider trimming 20-30% at current $42-43 levels if you bought below $30 (lock in 40%+ gains!)

- 📊 If holding through catalysts, set MENTAL STOP at $40 (major 64.4B gamma support wall)

- ⏰ Don't get impatient - turnarounds take time. You've already won if you bought the bottom!

- 🎯 If stock breaks above $45 resistance on good earnings, could re-add trimmed shares for run to $48-50

- 🛡️ For large positions, consider buying 1-2 $43 or $45 protective puts per 100 shares as insurance

If you're watching from sidelines:

- ⏰ January 30 after close is first major test - DO NOT enter before Q4 earnings clarity!

- 🎯 Post-earnings pullback to $38-40 would be EXCELLENT entry (12-15% off current price at gamma support)

- ✅ Looking for confirmation: 2025 revenue guidance showing return to growth, 18A yield data, customer win announcements, positive CEO transition reception

- 📈 Longer-term (6-12 months), if 18A succeeds commercially and Apple deal materializes, Intel could genuinely reach $55-60

- ⚠️ Current valuation requires FLAWLESS execution - one stumble and it's back to $35-38

If you're bearish:

- 🎯 Wait for catalysts to play out - don't fight 126% momentum rally without clear breakdown signal

- 📊 Watch for break below $40 gamma support (64.4B wall!) - that's the trigger for cascade to $35-38

- ⚠️ Post-earnings put spreads or bear call spreads offer defined-risk ways to play downside

- 📉 Remember Intel has years of execution failures - new CEO doesn't guarantee success

- ⏰ Patience required - this is multi-year turnaround story, not quick flip

Mark your calendar - Key dates to watch:

- 📅 December 5 (Friday) - Weekly options expiration, near-term volatility window

- 📅 December 19 (Friday) - Monthly OPEX / Quarterly Triple Witch

- 📅 January 16, 2026 (Friday) - Monthly OPEX

- 📅 January 30, 2025 (Thursday after close) - Q4 2024 earnings report (58 DAYS!)

- 📅 March 18, 2025 (Wednesday) - Lip-Bu Tan officially becomes CEO (106 DAYS!)

- 📅 March 20, 2025 (Friday) - Monthly OPEX, expiration of this $29M institutional trade

- 📅 Late April/Early May 2025 - Q1 2025 earnings (first under new CEO Tan)

- 📅 Throughout 2025 - 18A volume production ramp milestones

- 📅 Q1 2026 - Intel 18AP PDK 1.0/1.1 delivery to Apple (if deal progressing)

Final verdict: Intel's turnaround story has REAL substance - confirmed $7.86B CHIPS Act funding, credible new CEO with foundry expertise, 18A technical milestones achieved, and potential transformative Apple partnership. BUT this is a MULTI-YEAR story that requires perfect execution across multiple fronts against formidable competition.

The $29M institutional repositioning signals smart money believes in the $48-50 upside case (that's why they bought 26,000 calls at $50!), but they're also PROTECTING gains and removing tail risk (that's why they closed $40 and $60 positions). This is sophisticated portfolio management, not blind optimism.

Be strategic. Take some profits if you've got them. Stay exposed to upside but manage downside. The Intel turnaround will take 2-3 years to fully play out - you don't need to bet everything on the next 4 months.

This is a marathon rebuilding one of America's most important technology companies. Trade accordingly. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual Z-scores reflect these specific trades' sizes relative to recent INTC history - they do not imply the trades will be profitable or that you should follow them. Always do your own research and consider consulting a licensed financial advisor before trading. Intel faces significant execution risks including 18A production challenges, leadership transition uncertainty, competitive pressures from AMD/Arm, and potential macroeconomic headwinds. The Apple foundry deal is speculative and not confirmed. Stock volatility can result in rapid losses.

About Intel Corporation: Intel Corporation is a leading digital chipmaker pioneering x86 microprocessor architecture, focused on the design and manufacturing of microprocessors for the global personal computer and data center markets, with a market cap of $190.8 billion in the Semiconductors & Related Devices industry.