🔔 INTC Unusual Options Activity - $6.4M Three-Way Call Adjustment Before Earnings!

📅 January 21, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just executed a $6.4 MILLION three-way call position adjustment in Intel options, happening just ONE DAY before Q4 2025 earnings (January 22, 2026). We're seeing 3,100 contracts sold at the $53 strike, 3,100 bought at the $43 strike, and 3,000 sold at the $46 strike - all expiring February 20, 2026. This coordinated institutional activity totals $6.4M in premium and signals smart money is actively repositioning ahead of Intel's most important earnings report in years.

📊 Company Overview

Intel Corporation (INTC) is the pioneering digital chipmaker that invented x86 architecture:

- Market Cap: $231.6 Billion

- Industry: Semiconductors & Related Devices

- Current Price: ~$53.06-$53.76 (near 52-week high of $50.39, now broken)

- 52-Week Range: $17.67 - $50.39 (now trading above!)

- Employees: 108,900

- Primary Business: Microprocessor design and manufacturing for PCs, data centers, AI accelerators, and foundry services

Intel has staged a remarkable turnaround under CEO Lip-Bu Tan, with the stock surging over 100% in the past six months. The successful launch of 18A-based Panther Lake chips at CES 2026, a landmark foundry deal with Apple, and strategic investments from both the U.S. government ($8.9B) and Nvidia ($5B) have transformed market sentiment.

💰 The Option Flow Breakdown

📊 The Tape (January 21, 2026)

| Time | Symbol | Side | Type | Expiration | Strike | Volume | Premium | Order Type | Strategy | Z-Score | Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:50:11 | INTC20260220C53 | SELL | CALL | 2026-02-20 | $53 | 3,100 | $1.1M | STO | Short Call | 0.0 | NEW |

| 09:50:11 | INTC20260220C43 | BUY | CALL | 2026-02-20 | $43 | 3,100 | $3.0M | BTC | Close Long Call | 0.87 | TYPICAL |

| 09:50:11 | INTC20260220C46 | SELL | CALL | 2026-02-20 | $46 | 3,000 | $2.3M | STC | Close Short Call | 2.31 | HIGHLY_UNUSUAL |

Total Premium Flow: $6.4 MILLION

🤓 What This Actually Means

This is a complex position adjustment executed simultaneously across three strikes. Let me break down what's happening:

Trade 1 - INTC20260220C53 (Sell $1.1M):

- 🔴 Opening a NEW short call position at $53 strike (near current price)

- 📊 Volume/OI ratio of 6.4x signals HIGH ACTIVITY

- 💸 Collecting premium by selling calls at-the-money

- 🎯 Trader is capping upside above $53

Trade 2 - INTC20260220C43 (Buy $3.0M):

- 🟢 Closing an existing long call position at $43 strike (deep in-the-money)

- 📊 This was a profitable position being closed (stock rallied from $43 to $53+)

- 💰 Paying $3M to buy back/close these calls

- 🏦 Booking profits on deep ITM calls before earnings

Trade 3 - INTC20260220C46 (Sell $2.3M):

- 🔴 Closing an existing short call position at $46 strike

- 📊 Z-score of 2.31 = HIGHLY UNUSUAL activity level

- 💸 Collecting $2.3M to close out this short position

- ⚠️ Trader was previously short $46 calls and is buying them back

The Big Picture: This appears to be a trader rolling up their call spread or adjusting a covered position. They're:

- Taking profits on deep ITM $43 calls ($3M)

- Covering their existing short $46 calls ($2.3M)

- Re-establishing a new short call position at $53 ($1.1M)

Net Premium Flow: Roughly $400K collected (sells exceed buys), suggesting this is a premium collection strategy going into earnings.

Translation for regular folks: A large institution is locking in profits on Intel calls that went deep in-the-money during the rally, then resetting their position with a new short call at $53 to cap potential upside. They're getting DEFENSIVE before tomorrow's earnings - happy to collect premium but not willing to bet on continued upside above $53.

📈 Technical Setup / Chart Check-Up

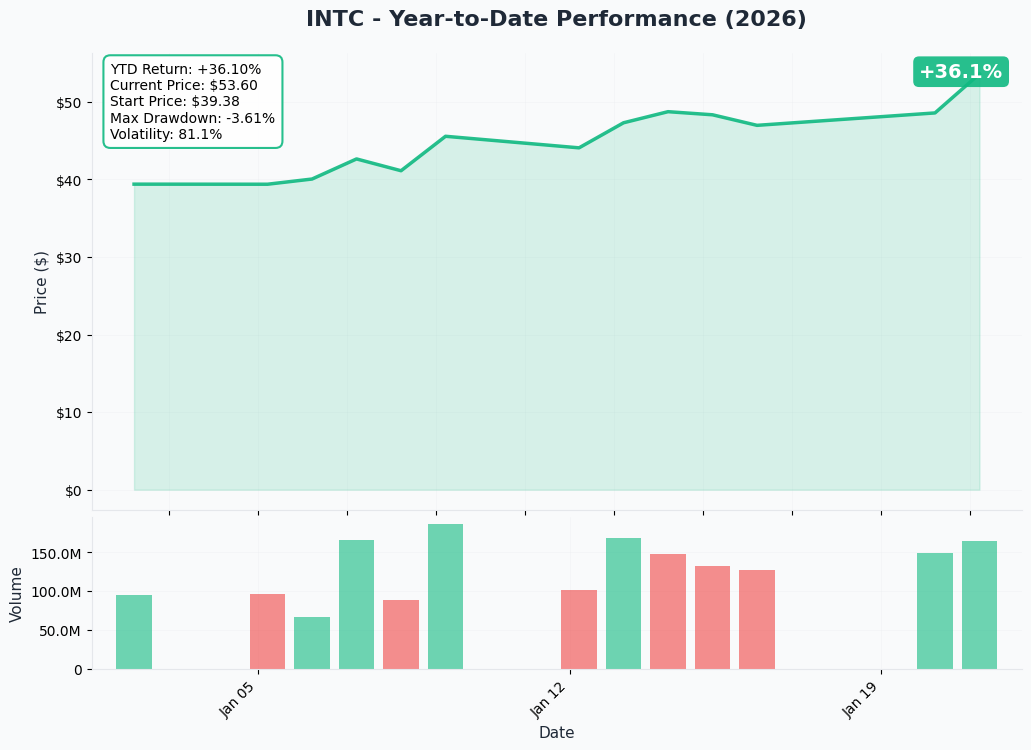

YTD Performance Chart

Intel has been one of the most remarkable turnaround stories in the semiconductor space. The stock has rallied over 100% in the past six months, breaking through its 52-week high of $50.39 and now trading above $53. Key observations:

- 🚀 Parabolic rally: From $17.67 lows to $53+ represents a stunning recovery

- 📈 Momentum acceleration: January surge of 35.7% alone driven by CES Panther Lake launch and Apple foundry deal

- 🎢 High volatility: Major swings as market digests turnaround narrative

- 📊 Volume confirmation: Institutional accumulation visible throughout Q4 2025

- ⚠️ Extended territory: Trading well above 52-week high suggests potential for consolidation

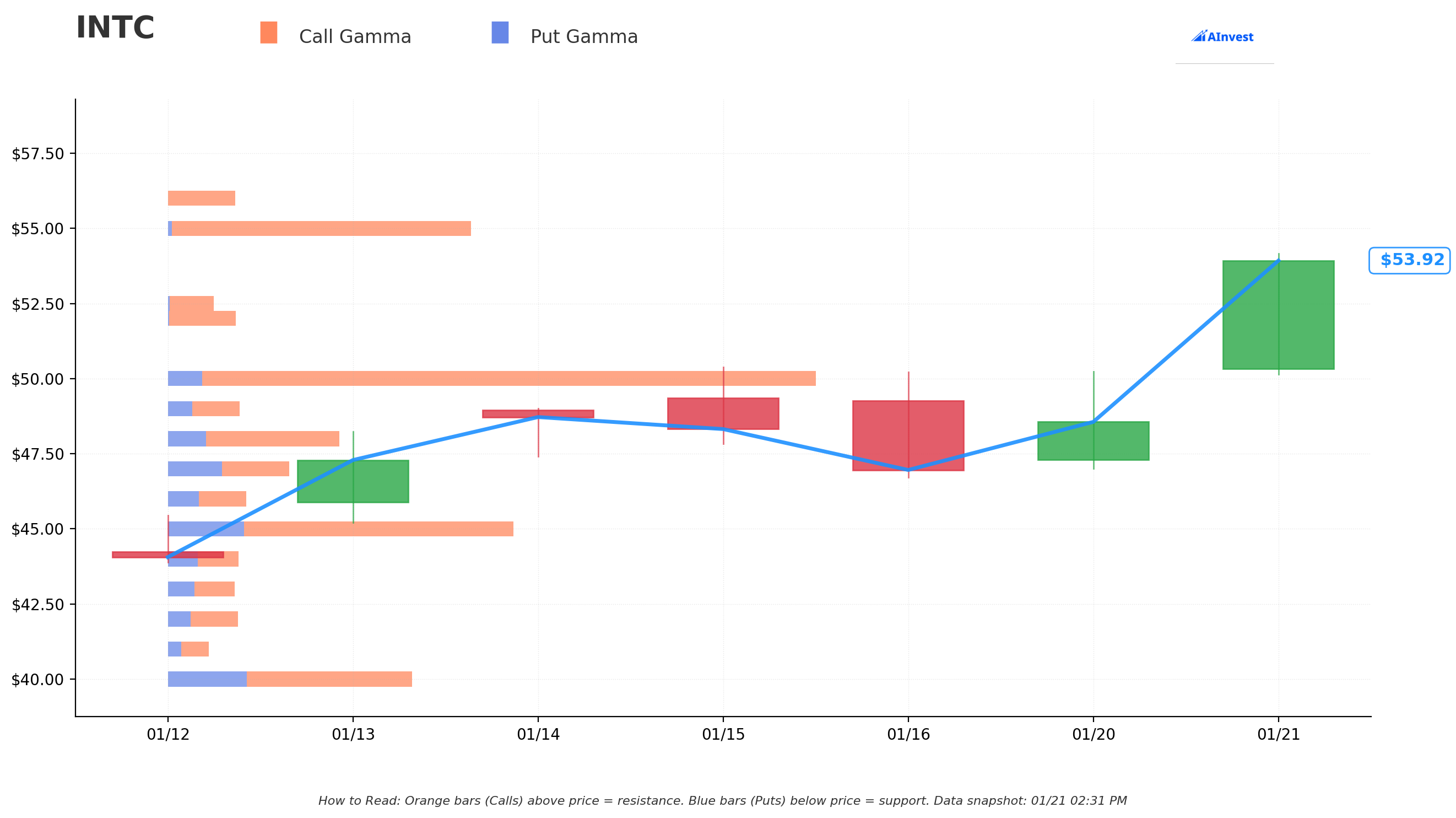

Gamma-Based Support & Resistance Analysis

Current Price: $53.76

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $52 - Immediate support with 4.87B total gamma (3.3% below current)

- $50 - MASSIVE support zone with 45.8B total gamma (strongest nearby floor!)

- $49 - Secondary support at 5.06B gamma (8.9% below)

- $48 - Support at 12.1B gamma (10.7% below)

- $47 - Support at 8.5B gamma (12.6% below)

- $46 - Support at 5.5B gamma (exactly where one trade was struck!)

- $45 - Deep support at 24.4B gamma (16.3% below)

🟠 Resistance Levels (Call Gamma Above Price):

- $55 - Immediate ceiling with 21.3B gamma (2.3% overhead)

- $60 - Major resistance at 29.7B gamma (11.6% above)

What this means for traders: INTC is trading in an interesting zone with immediate resistance at $55 (2.3% away) and strong support forming at $52 and massive support at $50. The $50 strike has 45.8B in total gamma - this is THE LINE IN THE SAND. If earnings disappoint and the stock breaks $52, expect it to find strong buying interest at $50 where dealers will need to buy to hedge their gamma exposure.

Net GEX Bias: Bullish (220.3B call gamma vs 67.5B put gamma) - Overall dealer positioning remains bullish, supporting the uptrend.

Notice the trade structure? The trader closed their $46 short calls (where there's 5.5B gamma support) and moved up to $53 - essentially following the gamma levels as the stock rallied.

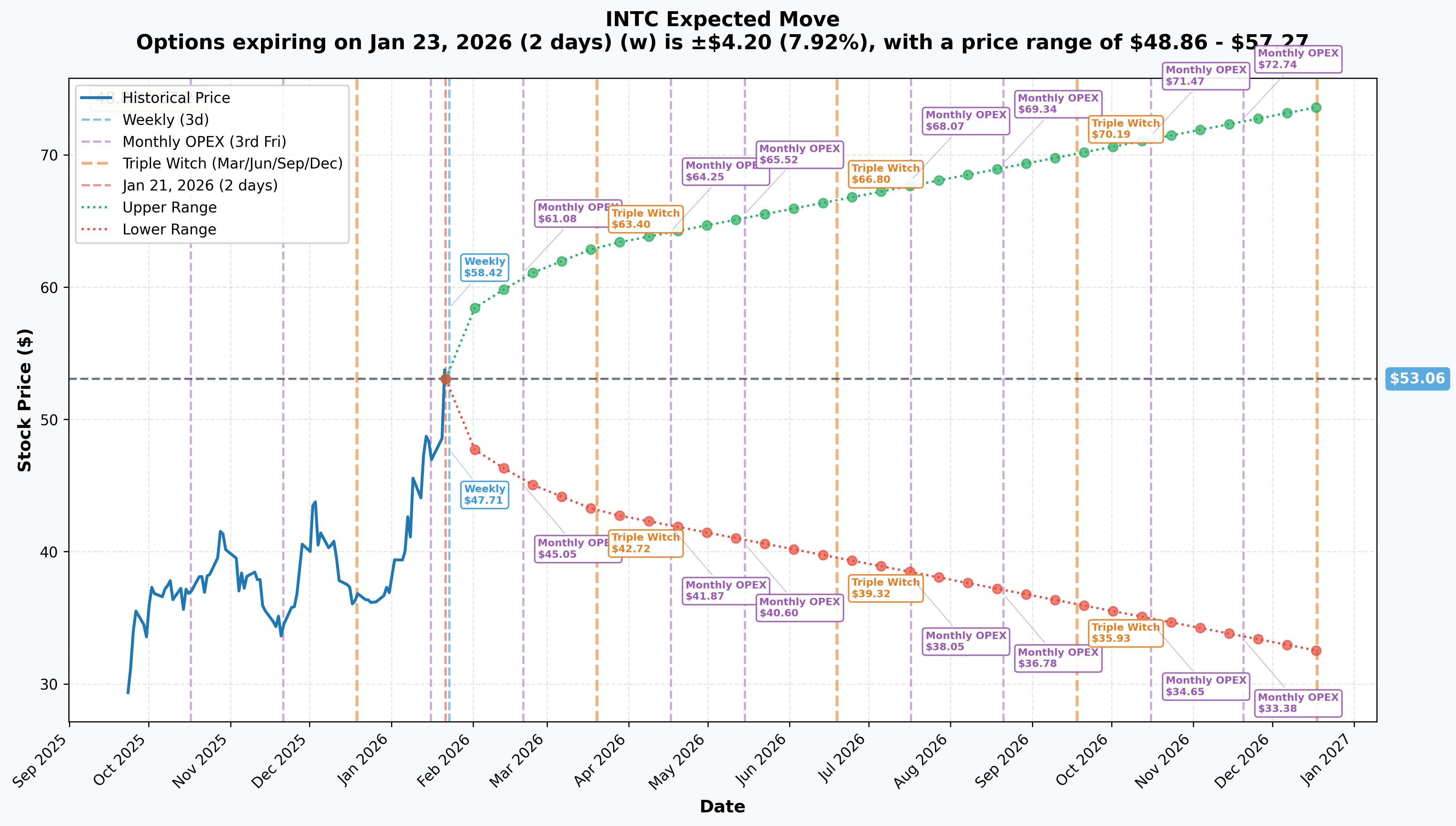

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 23 - 2 days - EARNINGS!): +/- $4.20 (+/- 7.92%) → Range: $48.86 - $57.27

- 📅 Monthly OPEX (Feb 20 - 30 days - THESE TRADES!): +/- $7.78 (+/- 14.66%) → Range: $45.29 - $60.84

- 📅 Quarterly Triple Witch (Mar 20 - 58 days): +/- $10.03 (+/- 18.9%) → Range: $43.03 - $63.09

- 📅 Yearly LEAPS (Dec 18 - 331 days): +/- $20.57 (+/- 38.76%) → Range: $32.49 - $73.63

Translation for regular folks: The options market is pricing in a MASSIVE 7.9% move ($4.20) by Friday's weekly expiration which captures tomorrow's earnings. That's significant for a $231B market cap company! The February 20 expiration (where all three trades are positioned) has an implied move of 14.66% - meaning the market expects INTC could trade anywhere from $45.29 to $60.84 by then.

Key insight: The trader positioning at the $53 strike for their short call is essentially betting the stock stays below $57-58 (upper implied move range) through February. Meanwhile, their $43 call close locked in profits from the rally, and the $46 close removed risk from their previous position.

The high implied volatility (14.66% for monthly) reflects massive earnings uncertainty tomorrow.

🎪 Catalysts

🔥 IMMEDIATE - Q4 2025 Earnings (TOMORROW - January 22, 2026!)

Intel reports Q4 2025 results TOMORROW after market close. This is THE catalyst driving all this options activity:

Key Metrics to Watch:

- 📊 Revenue: Guidance $12.8B - $13.8B, Consensus $13.37B

- 💰 Non-GAAP EPS: Guidance $0.08, Consensus ranges from -$0.02 to $0.08

- 📈 Gross Margin: Target ~36.5%

- 🤖 Data Center and AI: Estimates $4.36B (+28.8% YoY) per MarketBeat

- 💻 Client Computing Group: Estimates $8.33B (+4% YoY)

- 🏭 Intel Foundry Services: Estimates $4.39B (-2.4% YoY)

What analysts are watching:

- Foundry customer pipeline updates (any new wins beyond Apple?)

- 18A yield commentary (current estimates 55-65%)

- AI PC shipment volumes from Panther Lake launch

- Cost reduction progress toward $16B opex target

🚀 Recent Catalysts (Already Priced In)

CES 2026 - Panther Lake Launch (January 6-9, 2026): Intel unveiled Core Ultra Series 3 "Panther Lake" processors at CES, built on the 18A process. CEO Lip-Bu Tan stated they "over-delivered on 18A timeline." Key specs:

- 50 TOPS NPU performance (180 TOPS total platform)

- Up to 16 P+E cores

- Intel Arc with up to 12 Xe cores (+50% faster than Lunar Lake)

- First sub-2nm chip designed, built, and packaged in the U.S.

Apple Foundry Partnership (January 2026): In a landmark development, Apple signed a foundry deal with Intel to manufacture entry-level M-series chips on 18A:

- Target: MacBook Air, iPad Pro entry-level SoCs

- Volume: 15-20 million units annually

- Timeline: Production silicon expected Q2-Q3 2027

- 18A yields reportedly over 60%

CEO Lip-Bu Tan White House Meeting (January 8-9, 2026): Tan met with President Trump, who called him "very successful." U.S. government stake (purchased at $20.47/share) now worth ~$19.74B vs. $8.9B cost.

Nvidia $5B Investment (December 26, 2025): Nvidia completed a $5B equity investment in Intel (214.7M shares at $23.28/share, 4.4% stake). Joint development of AI infrastructure and PC products.

📅 Upcoming Catalysts (Next 3-6 Months)

Panther Lake Volume Ramp - Q1 2026: Broad market availability of Core Ultra Series 3 processors begins January 2026. Watch for OEM adoption rates and ASP trends.

Xeon 6+ (Clearwater Forest) Launch - H1 2026: Intel's first 18A-based server processor targeting data center AI inference workloads. Per Intel Newsroom, this will be "the most efficient server processor Intel has ever created."

Crescent Island AI GPU Sampling - H2 2026: New data center GPU designed for AI inference begins customer sampling.

14A Process Updates - Throughout 2026: CEO Tan stated Intel is "going big time into 14A" with production-ready target in 2027.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timing:

📈 Bull Case (30% probability)

Target: $58-$65

How we get there:

- 💪 Q4 earnings beat with revenue toward $13.8B high-end and positive Q1 2026 guidance

- 🚀 Foundry customer pipeline announcements (additional wins beyond Apple)

- 🤖 Strong Panther Lake early adoption metrics and positive OEM feedback

- 📈 18A yields confirmed at 60%+ with commentary on improvement trajectory

- 🌐 Data center segment beats $4.36B estimates showing AI traction

- 📊 Breakout above $55 gamma resistance triggers momentum buying to $60 implied move upper range

Key metrics needed:

- Revenue above $13.5B

- Positive EPS surprise (above $0.08)

- Foundry customer win announcements

- 18A yield improvement confirmation

🎯 Base Case (45% probability)

Target: $48-$55 range (CONSOLIDATION)

Most likely scenario:

- ✅ Solid earnings meeting guidance (~$13.0-13.4B revenue)

- 📱 18A/Panther Lake progressing on schedule without major surprises

- ⚖️ Guidance in-line with Street (no major upside or downside)

- 🤖 Foundry revenue flat to slightly down as expected

- 🔄 Trading within gamma support ($50-$52) and resistance ($55) bands

- 📊 Market digests recent rally, waits for H1 2026 Clearwater Forest proof points

- 💤 Volatility crush post-earnings (IV from 14.66% toward 8-10% range)

This is likely what the option traders expect: Stock consolidates after the massive run, short call at $53 collects premium while stock ranges. The February 20 expiration gives time for post-earnings digestion.

📉 Bear Case (25% probability)

Target: $43-$48

What could go wrong:

- 😰 Earnings miss or weak Q1 guidance citing macro headwinds

- 🚨 18A yield issues surface (below 55%)

- ⏰ Foundry customer pipeline weaker than expected

- 🇨🇳 China exposure concerns resurface

- 💸 Gross margin compression below 36%

- 📊 Broader tech selloff drags semis lower

- 🔨 Break below $50 gamma support triggers cascade to $45-48

Critical support levels:

- 🛡️ $50: MASSIVE gamma floor (45.8B) - MUST HOLD

- 🛡️ $45: Deep support (24.4B gamma)

- 🛡️ $43: Extended floor (where the closed long call was struck)

💡 Trading Ideas

🛡️ Conservative: Cash Gang Until Earnings Clear

Play: Stay on sidelines until January 22nd earnings volatility settles

Why this works:

- ⏰ Earnings TOMORROW creates binary event risk with +/- 7.9% implied move

- 💸 Implied volatility elevated - options expensive pre-earnings

- 📊 Stock up 100%+ in 6 months at 52-week highs - limited margin of safety

- 🎯 Better entry likely post-earnings after IV crush reduces option premiums

- 🤔 The institutional position adjustment signals smart money is derisking, not adding

Action plan:

- 👀 Watch Thursday earnings for revenue ($13.4B+ target), margins (36%+ needed), and foundry commentary

- 🎯 Look for pullback to $50 gamma support post-earnings for stock entry

- ✅ Need to see 18A yield confirmation and customer pipeline updates before committing

- 📊 Monitor post-earnings options activity for institutional sentiment

Risk level: Minimal | Skill level: Beginner-friendly

⚖️ Balanced: Post-Earnings Put Spread at Support

Play: After earnings settle, sell put spread at gamma support levels

Structure: Sell $50 puts, Buy $45 puts (February 20 expiration)

Why this works:

- 🎯 $50 strike is MASSIVE gamma support (45.8B) - dealers will buy heavily there

- 📊 Defined risk spread ($5 wide = $500 max risk per spread)

- 💸 Collect premium betting stock stays above major support

- ⏰ 30 days to expiration gives time for post-earnings recovery if needed

- 🤝 Aligns with bullish gamma bias (220.3B call vs 67.5B put)

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Collect ~$1.00-1.50 net credit per spread post-earnings

- 📈 Max profit: $100-150 if INTC above $50 at February expiration

- 📉 Max loss: $350-400 if INTC below $45 (defined and limited)

- 🎯 Breakeven: ~$48.50-49.00

Entry timing:

- ⏰ Wait 1-2 days post-earnings (by Jan 24) for IV collapse

- 🎯 Only enter if stock trades above $50 (confirms support holding)

- ❌ Skip if stock gaps below $48 (support broken)

Risk level: Moderate | Skill level: Intermediate

🚀 Aggressive: Earnings Straddle (ADVANCED ONLY!)

Play: Buy straddle betting on post-earnings volatility exceeding implied move

Structure: Buy $53 calls + Buy $53 puts (January 23 weekly expiration)

Why this could work:

- 💥 Implied move 7.9% but Intel has history of 10-15% earnings moves

- 🎰 Betting Street is UNDERPRICING earnings volatility risk given turnaround narrative

- 📊 With Apple deal, Panther Lake, and foundry updates, guidance could surprise big either way

- ⚡ Need stock to move >9-10% either way to profit

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Weekly straddles carry extreme theta decay

- ⏰ TIME DECAY KILLER: Only 2 days to expiration after earnings

- 😱 IV CRUSH: Even if stock moves 6-7%, IV collapse could result in LOSS

- 📊 Two-way risk: Stock could stay in $50-56 range and you lose entire premium

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded straddles through earnings before

- ✅ Can afford to lose ENTIRE premium

- ✅ Plan to close position within 24 hours post-earnings

- ✅ Understand IV crush mechanics

Risk level: EXTREME | Skill level: Advanced only

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Earnings binary event TOMORROW: Results Thursday January 22nd after close create MASSIVE volatility risk. Stock could gap 8-10% either direction based on revenue, margins, and foundry guidance. Options pricing +/- 7.9% implied move.

-

💸 Valuation no longer cheap after 100%+ rally: Stock has doubled from lows. P/E ratio of 4,430x (distorted by restructuring charges) makes it hard to value traditionally. Premium pricing requires continued execution.

-

🏭 Foundry profitability remains elusive: Intel Foundry posted ~$7B operating loss in 2023 with continued multi-billion losses through 2024-2025. Path to profitability needs "Mega-Whale" customer beyond Apple. Per Trefis analysis, external customer revenue lags far behind internal demand.

-

⚖️ 18A yield risks persist: Current yields estimated at 55-65% per Motley Fool. Any yield drop could crater gross margins in 2026. High-volume manufacturing ramp carries execution risk.

-

🇨🇳 Competition from AMD/Nvidia: In data center, Nvidia dominates with CUDA ecosystem while AMD continues gaining share. Intel lacks clear roadmap to displace Nvidia in AI training workloads per AI Daily.

-

📊 Most analyst price targets BELOW current price: Current stock at $53+ trades above average analyst target of $35.67-$46.08 per Stock Analysis. The 69% Hold rating suggests limited upside consensus.

-

🎢 Restructuring strain: 35,500 jobs cut in less than two years creates organizational risk per Tom's Hardware. Culture transformation under new CEO is still early.

🎯 The Bottom Line

Real talk: An institution just executed a $6.4M three-way call position adjustment ONE DAY before Intel's most important earnings in years. They're:

- Locking in profits on $43 calls that went deep in-the-money during the rally

- Covering risk on their $46 short calls

- Re-establishing a new short call at $53 to cap upside and collect premium

What this trade tells us:

- 🎯 Sophisticated player expects CONSOLIDATION through February - not betting on continued rally above $53

- 💰 They're taking chips off the table after the 100%+ move, not adding to positions

- ⚖️ The timing (1 day pre-earnings) shows they're derisking, not speculating

- 📊 The $53 short call caps upside near current price - they're happy to collect premium here

This is NOT a crash warning - it's a "the easy money has been made, time to get defensive" signal.

If you own INTC:

- ✅ Consider trimming 20-30% at $53-55 levels (lock in gains after 100%+ rally)

- 📊 If holding through earnings, watch $50 gamma support as your line in the sand

- ⏰ Don't get greedy - stock has doubled. Protecting profits is smart.

- 🎯 If earnings beat AND stock breaks $55, could add back on momentum

If you're watching from sidelines:

- ⏰ Thursday January 22nd after close is the moment of truth - DO NOT enter before earnings!

- 🎯 Post-earnings pullback to $48-50 would be SOLID entry with gamma support

- 📈 Looking for: Strong Q4 revenue ($13.4B+), 18A yield confirmation (60%+), foundry customer pipeline updates

- 🚀 Longer-term catalysts remain compelling: Apple deal, Clearwater Forest launch H1, Nvidia partnership

If you're bearish:

- 🎯 Wait for earnings before initiating shorts - fighting 100% momentum into highs is dangerous

- 📊 First major support at $50 (45.8B gamma wall), deeper support at $45

- ⚠️ Post-earnings put spreads offer defined-risk way to play downside after IV crush

- 📉 Watch for break below $50 - that's the trigger for cascade to $45

Mark your calendar - Key dates:

- 📅 January 22, 2026 (TOMORROW) after market close - Q4 2025 earnings report

- 📅 January 23 - Post-earnings price action and analyst reactions

- 📅 February 20 - Monthly OPEX (expiration of these trades)

- 📅 H1 2026 - Xeon 6+ (Clearwater Forest) launch

- 📅 H2 2026 - Crescent Island AI GPU customer sampling

- 📅 Q2-Q3 2027 - Apple 18A production silicon

Final verdict: Intel's turnaround story is REAL - Panther Lake, Apple foundry deal, Nvidia investment, and government support have transformed the narrative. BUT, at $53+ after a 100%+ rally with earnings TOMORROW, the risk/reward is NO LONGER favorable for aggressive new positioning. The $6.4M institutional adjustment is a CLEAR signal: smart money is locking in gains and capping upside, not betting on continued moonshot.

Be patient. Let earnings clear. Look for better entry points at $48-50 if it pulls back. The turnaround will still be there in a few weeks, and you'll sleep better buying the dip instead of the rip.

This is about risk management, not missing out. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The position adjustment analyzed here may reflect complex hedging strategies not applicable to retail traders. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for 8-10% gaps either direction.

About Intel Corporation: Intel is a leading digital chipmaker focused on the design and manufacturing of microprocessors for personal computers and data centers. The firm pioneered x86 architecture and is expanding through Intel Foundry while maintaining market leadership in CPUs across PC and server segments. Market cap of $231.6 billion in the Semiconductors & Related Devices industry.