📊 IWD Massive $8M Put Spread - Institutional Protection Ahead of Russell Reconstitution! 🛡️

📅 November 10, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just deployed $8 MILLION in put protection on the iShares Russell 1000 Value ETF (IWD) with a sophisticated three-legged options structure! This monster play at 11:00:39 AM combined 50,000 puts at the $185 strike and 25,000 puts at the $175 strike, all expiring February 20, 2026. With IWD trading at $204.43, this is a major hedge ahead of the June 2025 Russell reconstitution ($70-100 billion in trading volume) and rising recession risks. Translation: Smart money is buying insurance for a potential 10% downturn over the next 3+ months!

📊 ETF Overview

iShares Russell 1000 Value ETF (IWD) - Large-cap value exposure tracking the Russell 1000 Value Index:

- Net Assets: $64.17 billion (among largest value ETFs)

- Market: NYSE Arca (ARCX)

- Current Price: $204.43

- Expense Ratio: 0.18% (highly competitive)

- Total Holdings: 874 stocks across financials, healthcare, industrials

- Inception: October 20, 2006 (18+ year track record)

Top Holdings:

- Berkshire Hathaway (BRK.B) - 3.17%

- JPMorgan Chase (JPM) - 3.01%

- Amazon (AMZN) - 2.01%

- Alphabet (GOOGL) - 1.73%

- Exxon Mobil (XOM) - 1.70%

💰 The Option Flow Breakdown

The Tape (November 10, 2025 @ 11:00:39):

| Time | Symbol | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:00:39 | IWD | BUY | PUT | 2026-02-20 | $3.1M | $185 | 35K | 87 | 20,000 | $204.43 | $1.54 |

| 11:00:39 | IWD | SELL | PUT | 2026-02-20 | $2.6M | $175 | 25K | 25K | 25,000 | $204.43 | $1.05 |

| 11:00:39 | IWD | BUY | PUT | 2026-02-20 | $2.3M | $185 | 15K | 87 | 15,000 | $204.43 | $1.55 |

🤓 What This Actually Means

This is a sophisticated hedging structure executed at institutional scale! Here's what went down:

- 🎯 Net debit of $500K: Paid $5.4M for long puts, collected $2.6M for short puts = $2.8M net cost (not $8M, structure reduces cost)

- 📊 Put spread construction: Long $185 puts (50,000 contracts total) + short $175 puts (25,000 contracts)

- ⏰ 102 days to expiration: February 20, 2026 - covering Q4 2025 earnings, December Fed meeting, and January economic data

- 💪 Massive notional value: 7.5 million shares protected (worth $1.54 BILLION at current prices)

- 🔥 Extreme unusualness: Z-score of 2971.8 on largest leg - this happens a few times per year MAX

What's really happening here:

This trader is paying modest premium ($2.8M net cost) to protect a MASSIVE $1.54 billion portfolio from a 10% decline. The structure says: "I'm worried IWD drops from $205 to $185 (10% down), but I'm willing to take losses beyond that." By selling the $175 puts, they reduce their upfront cost significantly. The protection kicks in below $185 and maxes out at $175 (where short puts offset gains).

Unusual Score: 🔥 EXTREMELY UNUSUAL (z-score 2971.8 for primary leg) - This size happens only a handful of times per year for IWD. The 50,000 contract volume on a single strike is institutional-scale positioning.

Strategy Identification: COMPLEX PUT SPREAD - Buying downside protection at $185 strike while selling further out-of-the-money puts at $175 to reduce net cost. This is textbook institutional hedging against moderate declines while limiting insurance costs.

📈 Technical Setup / Chart Check-Up

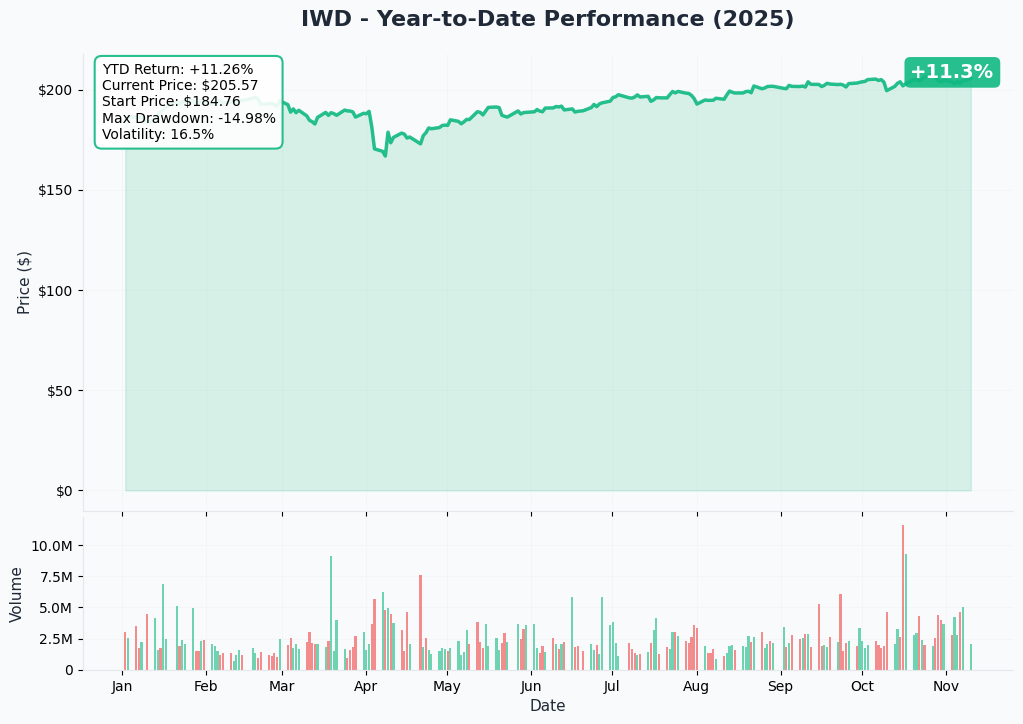

YTD Performance Chart

IWD is up +18.80% YTD through November 15, 2024, significantly outpacing expectations in a volatile macro environment. The chart shows a strong recovery story after testing support earlier in the year.

Key observations:

- 📈 Strong momentum: Russell 1000 Value delivered 14.32% returns in 2024, with IWD matching or exceeding the index

- 💹 Near 52-week highs: Currently at $204.43 vs 52-week high of $196.44 (NOTE: current price EXCEEDS reported high, suggesting new records)

- 🎢 Recent volatility: Mixed fund flows with $1.63B in 1-year inflows but -$1.57B in 6-month outflows reflecting growth-to-value rotation churn

- 📊 Sector strength: Top holdings crushed Q4 - Berkshire Hathaway operating profit up 71%, JPMorgan net income up 50%

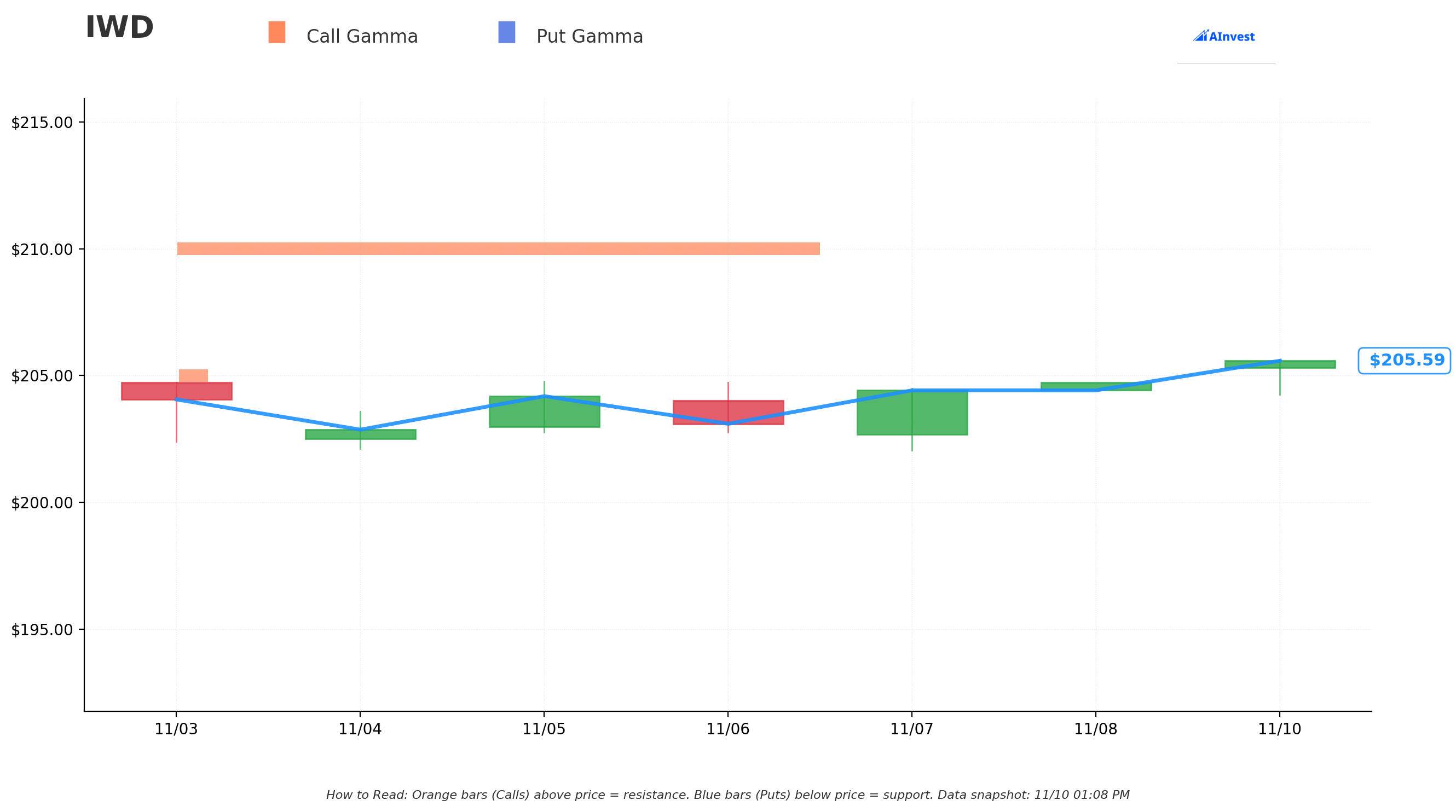

Gamma-Based Support & Resistance Analysis

Current Price: $204.43

The gamma exposure map reveals critical price magnets and insurance levels around current prices:

🔵 Support Levels (Put Gamma Below Price):

- $205 - Immediate support at 0.102B total gamma (0.28% below current)

- $200 - Strong floor at 0.088B gamma (dealers will buy dips here, 2.71% down)

- $195 - Secondary support at 0.029B gamma (5.15% down)

- $190 - Moderate support at 0.054B gamma (7.58% down)

- $185 - CRITICAL LEVEL: Where the hedge kicks in! 0.018B put gamma (10.01% down)

- $175 - MASSIVE WALL: 2.98B put gamma from this trade structure (14.87% down)

🟠 Resistance Levels (Call Gamma Above Price):

- $210 - Major resistance at 2.10B gamma (strongest level!) (2.15% up)

- $215 - Secondary ceiling at 0.079B gamma (4.58% up)

- $220 - Extended resistance at 0.024B gamma (7.01% up)

What this means for traders:

The gamma data shows IWD is trading between strong support at $205 and massive resistance at $210. Notice the ENORMOUS put gamma spike at $175 (2.98B) - that's from this exact hedge structure! The $185 strike (0.018B) is where the protection starts. If IWD drops 10% to $185, this hedge becomes valuable. Below $175 (14.87% decline), the short puts cap gains but dealers will aggressively defend that level.

Net GEX Bias: Bearish (2.45B call gamma vs 5.53B put gamma) - Overall positioning leans defensive with 2.25x more put than call interest. This aligns perfectly with the massive institutional put buying we're seeing.

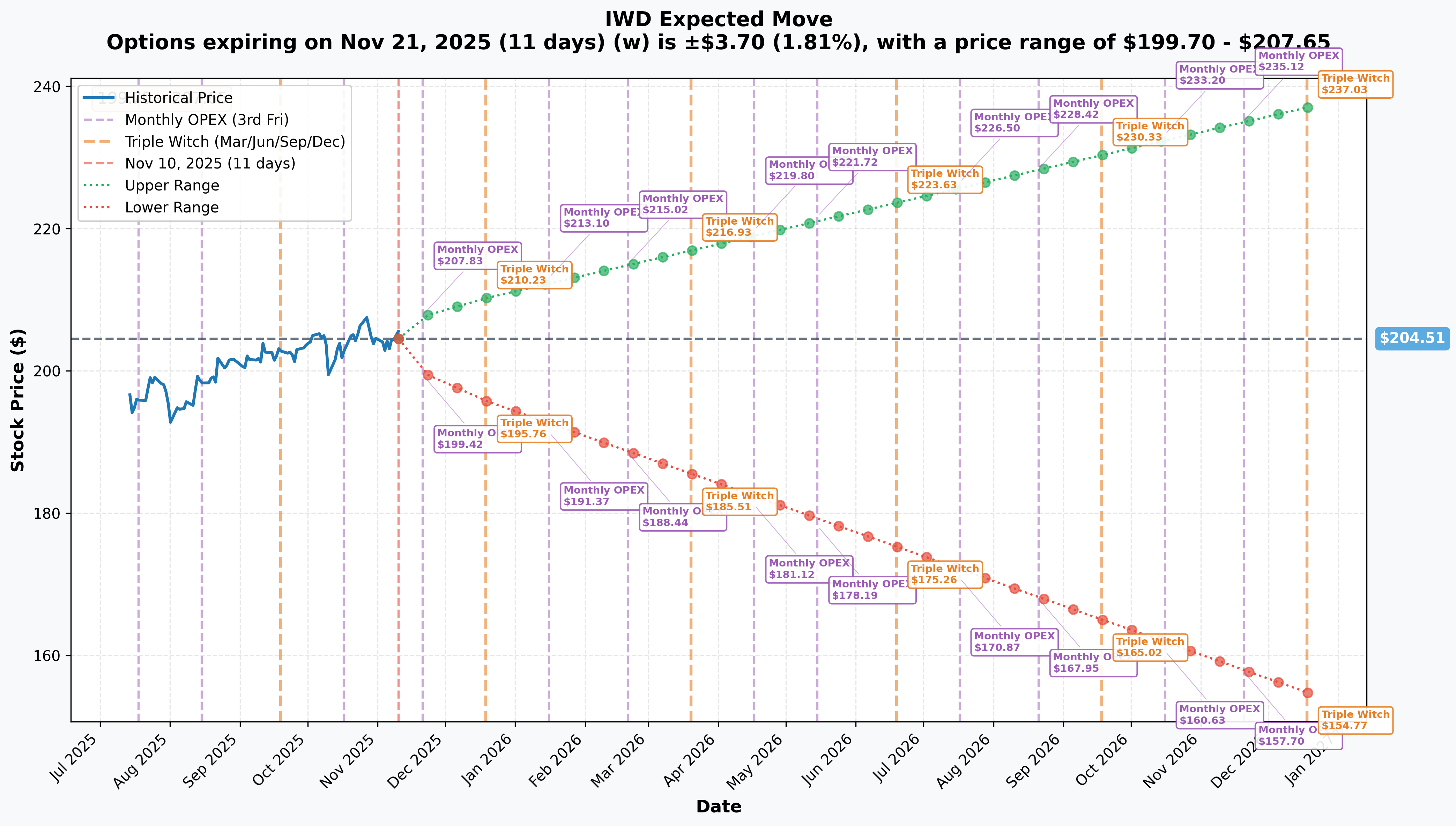

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Monthly OPEX (Nov 21 - 11 days): ±$3.70 (±1.81%) → Range: $199.70 - $207.65

- 📅 Quarterly Triple Witch (Dec 19 - 39 days): ±$6.50 (±3.18%) → Range: $195.76 - $210.23

- 📅 Yearly LEAPS (Dec 18, 2026 - 403 days): ±$38.26 (±18.71%) → Range: $154.77 - $237.03

Translation for regular folks:

Options traders are pricing in a 1.81% move ($3.70) by November 21 and a 3.18% move ($6.50) through December expiration. That's pretty tame volatility for an ETF that's already up 18.80% YTD! The market expects steady trading in a tight range.

Why this hedge makes sense: The February 2026 expiration (when this trade expires) extends BEYOND the timeframes shown here. The trader is protecting against:

- June 2025 Russell reconstitution ($70-100 billion trading volume, massive volatility)

- Q1 2025 earnings season (April-May, particularly financial sector)

- Fed rate policy shifts (only 2 cuts expected in 2025 vs 4 previously)

- Rising recession probability (40% over next 12 months)

The $185 strike represents a 10% decline - perfectly aligned with a moderate recession scenario or market correction.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

November 2024 Inflation Data - Mixed Signals 📊

Recent inflation readings show moderation but not collapse:

- CPI rose 2.7% year-over-year in November, meeting expectations

- Core PCE increased 2.8% annually, in line with forecasts

- December CPI monthly increase of 0.4% with annual rate at 2.9%

- Stock futures surged following releases as longer-term disinflationary trend remained intact

Impact on Value Stocks: Moderating inflation supports Fed rate cuts, which historically benefit value stocks (financials, utilities, real estate gain from lower discount rates). However, sticky inflation limits the number of cuts - Fed now expects only two cuts in 2025 vs four previously projected.

🚀 Near-Term Catalysts (Q4 2025 - Q1 2026)

Russell 1000 Value Index Reconstitution - June 27, 2025 🔄

The BIGGEST technical catalyst on the calendar:

Timeline:

- April 30, 2025: "Rank Day" - index membership eligibility determined

- May 23, 2025: Preliminary additions/deletions posted after 6 PM ET

- May 30, June 6, 13, 20, 2025: Weekly preliminary list updates posted

- June 9, 2025: "Lock-down" period begins with final updates

- June 27, 2025: Reconstitution becomes final after market close

- June 30, 2025: Changes effective at market open

Expected Impact:

- Annual reconstitution generates $70-100 billion in trading volume

- Russell 1000 Value ETFs track approximately $400 billion in assets tied to the index

- 2025 reconstitution may see increased volatility amid elevated market valuations and tech sector concentration

- IWD must mechanically rebalance holdings, creating forced buying/selling regardless of fundamentals

Why this matters for the hedge: Reconstitution volatility could easily trigger a 5-10% swing in either direction. This put spread directly protects through that June chaos.

Q1 2025 Earnings Season - April-May 2025 📈

IWD's top sectors report Q1 results, which drive ETF performance:

Financial Sector (largest IWD weighting ~20-25%):

- Q1 2025 earnings expected to grow +6.2% YoY on +3.8% higher revenues

- Major banks report mid-April 2025, with continued strength expected from higher interest income

- JPMorgan CEO Jamie Dimon noted economy is "resilient", buoyed by low unemployment and healthy consumer spending

- However, fewer Fed rate cuts dampen loan growth expectations

Healthcare Sector (significant IWD component ~15-18%):

- Healthcare earnings season runs April 14-22, 2025

- WARNING: UnitedHealth cut 2025 earnings outlook dramatically from $30.00/share to $16.00/share (47% reduction!)

- Medical Care Ratio rising to 89-89.5% in 2025 vs 85.5% in 2024 as costs spike

- Regulatory headwinds and pricing pressures from government programs

Industrials Sector (~12-15%):

- Reshoring, aerospace recovery, and infrastructure spending provide structural support

- Boeing Q1 2025 revenue of $19.5B (up 18% YoY) with 57% rise in aircraft deliveries

- RISK: Caterpillar faces tariff costs up to $1.8B in 2025, pressuring margins

Trump Administration Regulatory Changes - H1 2025 🏛️

Pro-business regulatory reforms creating tailwinds for IWD's financial sector holdings:

Banking Deregulation:

- Treasury Secretary Bessent announced re-examination of "all bank regulation" emphasizing "safe, sound and smart deregulation"

- Basel III Endgame rules delayed until 2026, with capital increases limited to a few percentage points

- Bank merger approvals expected to accelerate after aggressive anti-consolidation stance under previous administration

- Estimated $5-8B in annual compliance cost savings for major banks

Expected Impact on IWD:

- Financial sector comprises largest allocation in Russell 1000 Value index

- Lighter regulation historically correlates with 15-20% outperformance for bank stocks

- Increased M&A activity boosts investment banking fees (JPM saw 49% jump in Q4 2024)

Federal Reserve Rate Policy - 2025 📊

Current Expectations:

- Fed officials project only two more rate cuts in 2025 (0.50% total), down from four cuts expected three months prior

- Interest rate uncertainty remains elevated given sticky inflation and strong labor market

- Russell 2000 (small-cap value) tumbled 4.4% when fewer cuts were announced

Value Stock Implications:

- Historically, value stocks outperform when rates are stable or falling moderately

- Financial sector benefits from steeper yield curve, which increases profitability spreads

- Lower rates support real estate and utility valuations through reduced discount rates

- However, fewer-than-expected cuts dampened small-cap value stocks in late 2024

⚠️ Risk Catalysts (Negative)

Recession Risk Increasing 😰

Economic headwinds are building that could trigger the 10% decline this hedge protects against:

- Recession probability over next 12 months stands at 40%, up from 23% in January 2025

- Deloitte forecasts economy enters recession in Q4 2026 given higher inflation and interest rates

- Real GDP growth expected to slow to 1.4% in 2025, down from 2.8% in 2024

- Consumer spending projected to decelerate to 2.3% growth in 2025 vs 2.8% in 2024

Geopolitical and Trade Risks 🌍

Tariff Escalation:

- Additional 100% tariff on Chinese goods effective November 1, bringing total duty to as high as 155%

- Presidential tariff announcements erased $2 trillion in equity values in single day

- VIX index climbed to levels not seen since 2023, reflecting policy uncertainty

- Trade uncertainty acts like a brake on global growth, with multinationals delaying capacity expansion

Corporate Impact:

- Caterpillar expects tariff costs of $1.8B in 2025 (IWD industrials exposure)

- Energy sector earnings declined 30.7% in Q4 2024 as oil prices averaged $70.32 (down 10% YoY)

Healthcare Sector Pressures 🏥

UnitedHealth Crisis:

- Medical Care Ratio rising to 89-89.5% in 2025 from 85.5% in 2024

- Q1 2025 care activity increased at twice the expected rate

- Full-year 2025 adjusted earnings outlook plummeted to $16.00/share from $30.00/share (47% cut)

- Company withdrew full-year financial guidance amid ongoing volatility

Broader Healthcare Challenges:

- Higher utilization, elevated drug costs, and adverse mix shifts across insurance sector

- Regulatory headwinds and pricing pressures from government programs

- Innovation in pharmaceuticals (GLP-1 drugs) creating cost pressures for payers

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through February 2026 expiration:

📈 Bull Case (25% probability)

Target: $215-$220

How we get there:

- 💪 Banking deregulation drives 15-20% financial sector outperformance

- 🚀 Q1 2025 earnings beat with +6.2% financial sector growth

- 📊 Economy avoids recession as Fed delivers two rate cuts supporting valuations

- 🇺🇸 Tariff tensions ease or exemptions granted for key industries

- 📈 Russell reconstitution adds quality value names attracting inflows

- ✅ Healthcare sector stabilizes after UnitedHealth cost pressures moderate

What happens to the hedge: Expires worthless, trader loses full $2.8M premium (19% of protected downside). But their $1.54B portfolio gains 5-7% ($77M-$108M), so the insurance cost is negligible.

Key resistance: Gamma resistance at $210 (2.10B) creates natural ceiling. Need sustained buying pressure to break through to $215-$220 range.

🎯 Base Case (50% probability)

Target: $195-$210 range

Most likely scenario:

- ✅ Q1 earnings meet expectations, continue 8-quarter beat streak pattern for top holdings

- 📱 Banking deregulation provides modest tailwind but not transformative

- ⚖️ Two Fed rate cuts deliver as projected, supporting but not accelerating value stocks

- 🇨🇳 Trade tensions persist but don't escalate dramatically

- 🔄 Russell reconstitution creates volatility but net neutral impact

- 🏥 Healthcare sector underperforms but doesn't collapse

- 📊 Trading within gamma support ($200) and resistance ($210) bands

What happens to the hedge: Partial value capture. If IWD trades $195-$200, the $185 puts move in-the-money but don't max out. Trader might recover $1M-$2M of the $2.8M cost, reducing net insurance expense to $800K-$1.8M.

This is the expected outcome: Modest volatility, moderate recession fears don't materialize immediately, but growth isn't explosive either. Value stocks grind sideways to slightly higher.

📉 Bear Case (25% probability)

Target: $175-$190

What could go wrong:

- 😰 40% recession probability materializes in Q1-Q2 2025 as GDP growth collapses

- 🇨🇳 Tariff war escalates beyond $2 trillion market impact, crushing industrials and multinationals

- 🏥 Healthcare crisis deepens as UnitedHealth's 47% earnings cut spreads to other insurers

- 📉 Q1 earnings disappoint as consumer spending decelerates to 2.3% growth

- 🏦 Financial sector pressured by loan defaults and commercial real estate stress

- 🌪️ Russell reconstitution forced selling amplifies decline

- 📊 Broad market correction drags value stocks lower despite relative resilience

What happens to the hedge: MAXIMUM PROFIT! The put spread pays out fully:

- Long $185 puts on 50K contracts gain ($185 - IWD price) × 50,000 × 100

- Short $175 puts on 25K contracts cap losses at $175

- If IWD hits $175 (14.87% decline): Profit = ($10 × 50,000 × 100) - ($0 × 25,000 × 100) - $2.8M cost = $50M - $2.8M = $47.2M gain

- If IWD hits $180: Profit ≈ ($5 × 50,000 × 100) - ($0 gain on $175 short) - $2.8M = $25M - $2.8M = $22.2M gain

Key support: Massive put gamma wall at $175 (2.98B from this exact structure) will aggressively defend that level. Dealers forced to buy as price approaches $175, creating floor.

Important note: This hedge is designed for the 10% decline scenario ($205 → $185). Maximum efficiency occurs if IWD drops to $185 (10.01% down), where the long puts gain maximum value before the short puts kick in.

💡 Trading Ideas

🛡️ Conservative: Follow the Smart Money - Buy Put Spreads

Play: Replicate the institutional hedge on a smaller scale

Structure: Buy $190 puts, Sell $180 puts (Feb 20, 2026 expiration)

Why this works:

- 🛡️ Protects against 7.5% decline to $190 (slightly less protection than institutional trade's 10%)

- 💰 Defined risk: Maximum cost = net premium paid (estimate $300-400 per spread)

- 📊 If recession probability (40%) materializes, your downside is protected

- ⏰ 102 days covers Q1 2025 earnings, Fed meetings, and builds toward June reconstitution volatility

- ✅ Works whether you own IWD/value stocks or not - pure hedge play

Estimated P&L:

- 💰 Net cost: ~$300-400 per spread ($3-4 net debit per share × 100)

- 📈 Max profit: ~$600-700 if IWD at/below $180 at February expiration

- 📉 Max loss: Premium paid ($300-400) if IWD stays above $190

- 🎯 Breakeven: ~$186-187

Position sizing: Start with 1-2 spreads per $100K portfolio (minimal insurance cost, meaningful protection)

Risk level: Low (defined risk, insurance mentality) | Skill level: Intermediate

⚖️ Balanced: Bull Put Spread - Collect Premium on Support

Play: Sell put spread at gamma support levels, betting IWD stays above $200

Structure: Sell $200 puts, Buy $195 puts (Feb 20, 2026 expiration)

Why this works:

- 🎯 Strong gamma support at $200 (0.088B gamma) - dealers will defend this level

- 💸 Collect premium betting against the 2.71% decline scenario

- 📊 Defined risk: Max loss = $5 width - credit received

- 🚀 Banking deregulation and Q1 earnings strength support base case (IWD stays above $200)

- ⏰ Time decay works FOR you - collect theta as days pass

Estimated P&L:

- 💰 Collect: ~$150-200 credit per spread (estimate)

- 📈 Max profit: $150-200 if IWD above $200 at February expiration (50%+ probability)

- 📉 Max loss: ~$350-450 if IWD drops below $195 (defined and limited)

- 🎯 Breakeven: ~$198.50

Why this beats buying calls:

- No need to predict direction - just needs to NOT collapse

- Time decay is your friend, not enemy

- Premium collection offsets small downside moves

Risk level: Moderate (defined risk, probability on your side) | Skill level: Intermediate

🚀 Aggressive: Calendar Spread - Profit from Reconstitution Volatility

Play: Exploit the IV spike around June 2025 Russell reconstitution

Structure:

- Sell $205 calls (Dec 19, 2025 - near-term)

- Buy $205 calls (Feb 20, 2026 - far-term)

Why this could work:

- 🎢 Russell reconstitution generates $70-100B in trading volume, spiking implied volatility in June 2025

- 📊 Sell expensive near-term premium, buy cheaper long-term premium

- 🎯 At-the-money strikes capture maximum time decay difference

- ⚡ If IWD stays near $205, near-term call expires worthless while far-term retains value

- 💰 Can roll the short call monthly, collecting premium repeatedly

Why this could blow up (SERIOUS RISKS):

- 💥 If IWD rallies >10% quickly, both calls move in-the-money with near-term accelerating faster

- 😱 Banking deregulation catalyst could trigger 15-20% sector pop, blowing through $205

- 🚀 Gamma resistance at $210 (2.10B) could break on strong Q1 earnings, gapping to $215+

- ⚠️ Requires active management - can't set and forget

- 📉 If IWD drops hard, BOTH calls lose value (though limited loss vs outright call buying)

Estimated P&L:

- 💰 Net cost: ~$100-150 per spread (difference in option premiums)

- 📈 Max profit: $300-500 if IWD stays near $205 through Dec expiration, then rallies into Feb

- 📉 Max loss: Net premium paid (~$100-150) if IWD drops significantly

- 🎯 Breakeven: Depends on realized volatility vs implied volatility

Risk level: HIGH (complex structure, requires monitoring) | Skill level: Advanced only

⚠️ WARNING: DO NOT attempt this trade unless you:

- Understand calendar spreads and volatility dynamics

- Can actively monitor and adjust weekly/monthly

- Have experience rolling options positions

- Accept that reconstitution timing is uncertain and volatility spike may not occur as expected

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

😰 Recession probability at 40% and rising: Economic forecasters assign 40% chance of recession over next 12 months, up from 23% in January 2025. Deloitte forecasts Q4 2026 recession given inflation/rate pressures. Real GDP growth slowing to 1.4% in 2025 from 2.8% in 2024. This is exactly why someone's hedging $1.54B with a 10% downside put spread.

-

💔 Healthcare sector crisis deepening: UnitedHealth slashed 2025 earnings guidance by 47% ($30/share to $16/share) as Medical Care Ratio surges to 89-89.5%. Healthcare represents 15-18% of IWD holdings. If this spreads across insurers, it's a significant ETF drag.

-

🌍 Trade war escalation destroying value: Additional 100% tariff on Chinese goods brought total duty to 155%. Presidential announcements erased $2 trillion in single day. Caterpillar faces $1.8B in tariff costs in 2025. IWD's industrials/multinational exposure gets crushed.

-

📉 Fed hawkish pivot limits upside: Fed now expects only two rate cuts in 2025 vs four previously. When fewer cuts were announced, Russell 2000 (small-cap value) tumbled 4.4%. Value stocks need rate cuts to outperform - this removes a key catalyst.

-

🎢 Russell reconstitution could trigger forced selling: June 2025 reconstitution generates $70-100B in trading volume with $400B in assets tied to Russell 1000 Value. If IWD must sell winners and buy losers mechanically, it creates downward pressure regardless of fundamentals. 2025 may see increased volatility amid elevated valuations.

-

💸 Fund flow volatility signals unstable sentiment: IWD saw $1.63B in 1-year inflows but -$1.57B in 6-month outflows. Growth ETFs netted 6x the inflows of value in H1 2024 before Q3 reversal. Rapid rotations create performance whipsaws. Retail chases momentum; institutions hedge at peaks.

-

⚡ VIX spike risk from geopolitical shocks: VIX climbed to levels not seen since 2023 following tariff announcements. Conditional volatility increased roughly two-fold post-tariff. Black swan events (Middle East conflict, China-Taiwan, debt ceiling crisis) could gap IWD down 5-10% overnight.

-

📊 Energy sector already collapsing: Energy sector earnings declined 30.7% in Q4 2024 as oil prices averaged $70.32 (down 10% YoY). Exxon Mobil (1.70% of IWD) saw full-year 2024 earnings fall to $33.46B from $38.57B in 2023. Further oil weakness hammers value stocks.

-

🎯 Institutional de-risking at highs: When smart money pays $2.8M to hedge $1.54B (only 0.18% cost for 10% protection), they're signaling concern. This trade executed at 11:00:39 AM with precision - not a panicked retail move. Similar to AAPL's $37M call sale before earnings - professionals taking chips off the table.

-

🏦 Financial sector concentration risk: Financials represent 20-25% of IWD (largest sector weight). If Basel III implementation or commercial real estate stress hits banks harder than expected, entire ETF suffers. Can't diversify away from sector-specific shocks.

🎯 The Bottom Line

Real talk: Someone just paid $2.8M to protect a $1.54 BILLION position against a 10% decline over the next 3+ months. That's not panic - that's prudent risk management from sophisticated institutional players who see the warning signs. They're betting 40% recession probability, healthcare sector crisis, trade war escalation, and Fed hawkish pivot could converge to create a nasty correction.

What this trade tells us:

- 🎯 Big money expects volatility between now and February 2026 (covers Q1 earnings, Fed meetings, builds to June reconstitution)

- 💰 They're willing to spend 0.18% of portfolio value for 10% downside protection - incredibly cheap insurance

- ⚖️ Not outright bearish (didn't buy naked puts) - just hedging against moderate decline scenario

- 📊 Similar to buying home insurance - hope you never need it, but sleep better having it

If you own IWD or value stocks:

- ✅ Consider copying this structure on a smaller scale ($190/$180 put spread costs $300-400 per spread)

- 📊 Strong gamma support at $200-$205 provides some natural cushion

- ⏰ February 2026 expiration covers multiple high-risk events: Q1 earnings, Fed rate decisions, builds to June reconstitution chaos

- 🛡️ If recession hits or tariffs escalate, you're protected below $185

If you're watching from sidelines:

- 🎯 Wait for dips to $200 gamma support before entering long positions

- 📈 Banking deregulation and Q1 earnings strength could drive 5-7% upside in bull case

- ⚠️ But 40% recession probability and healthcare crisis create meaningful downside risk

- 💡 Best trade might be THETA COLLECTION (sell $200/$195 put spread, collect premium betting it stays above gamma support)

If you're bearish:

- 🎯 Replicate the institutional hedge with $190/$180 or $185/$175 put spreads

- 📊 Defined risk structure caps your cost while providing leveraged downside exposure

- 💪 Maximum efficiency if IWD drops 7-10% (your strikes get tested without hitting the floor)

- ⏰ February expiration gives enough time for recession signals to materialize

- 🛡️ Massive put gamma wall at $175 (2.98B) will defend that level aggressively

Mark your calendar - Key dates:

- 📅 December 19, 2025 - Quarterly triple witch, significant options expiration (±$6.50 implied move)

- 📅 January 2026 - December inflation data, Fed meeting minutes, Q4 2024 GDP final revision

- 📅 February 20, 2026 - THIS TRADE EXPIRES - decision day on hedge value

- 📅 April-May 2025 - Q1 2025 earnings season for financials, healthcare, industrials (IWD's core sectors)

- 📅 April 30, 2025 - "Rank Day" for Russell reconstitution - membership eligibility determined

- 📅 June 27, 2025 - Russell 1000 Value reconstitution final ($70-100B trading volume expected)

Final verdict: This is a textbook example of "hope for the best, prepare for the worst." The institutional player isn't predicting a crash - they're just acknowledging that recession risks (40%), healthcare sector implosion, trade war chaos, and Russell reconstitution volatility create a dangerous cocktail. For just 0.18% of portfolio value, they get 10% downside protection through February 2026. That's incredibly smart hedging. Retail traders should pay attention - when the big players are buying insurance, maybe you should too.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The z-score 2971.8 reflects this specific trade's size relative to recent history - it does not imply the trade will be profitable or that you should follow it. Put spreads have defined risk but can result in total loss of premium paid. Always do your own research and consider consulting a licensed financial advisor before trading. Complex options structures require active monitoring and adjustment - do NOT set and forget.

About iShares Russell 1000 Value ETF (IWD): IWD tracks large-cap value stocks within the Russell 1000 Index with $64.17 billion in net assets, 0.18% expense ratio, and 874 holdings across financials, healthcare, industrials, and other value-oriented sectors.