🐋 MAR $26M Covered Call Overwrite - Institutional Money Monetizes a Massive Marriott Position!

📅 February 25, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just SOLD $26 MILLION worth of MAR June $340 calls - 10,000 contracts representing 1,000,000 shares (~$346M worth of stock) in a single block at 10:59 AM. This is a classic institutional covered call overwrite on a position worth more than a third of a billion dollars. The seller is willing to cap their upside at an effective exit price of $366 (+5.7% from here) in exchange for collecting massive premium income, betting that MAR won't run away from them before the June Triple Witch expiration.

📊 Company Overview

Marriott International (MAR) is the world's largest hotel company and an absolute titan of the hospitality industry:

- 🏨 What they do: Operates and franchises 9,300+ hotels with 1.77 million rooms across 30+ brands worldwide, from ultra-luxury (Ritz-Carlton, St. Regis) to midscale (Series by Marriott)

- 💰 Market Cap: $90.9B

- 🏢 Sector: Hotels, Rooming Houses, Camps & Other Lodging Places

- 📈 Exchange: NASDAQ

- 📊 Current Price: ~$346.23

- 🌎 Key Story: Riding a wave of 35% projected surge in co-branded credit card fees, FIFA World Cup 2026 tailwinds, and international RevPAR outperformance, with 271 million Bonvoy loyalty members

💰 The Option Flow Breakdown

📊 The Tape

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:59:04 | MAR | MID | SELL | CALL $340 | 2026-06-18 | $26M | $340 | 10,000 | -- | 10,000 | $346.23 | $26.00 | MAR20260618C340 |

🤓 What This Actually Means

Let me break this down in plain English -- because this trade is NOT what most people think when they see "SELL CALL":

- 💸 $26 million COLLECTED: The seller received $26 per contract x 100 shares x 10,000 contracts = $26M in premium income

- 📊 STO (Sell-to-Open) = Opening a BRAND NEW short call position. This is fresh income generation, not closing a prior trade

- 🎯 $340 strike is IN-THE-MONEY -- it's 1.8% BELOW the current price of $346.23. That's the key to understanding this trade

- 💰 Premium decomposition: The $26 per contract breaks down as $6.23 intrinsic value ($346.23 - $340) + $19.77 in time value. The seller is getting paid almost $20/share in PURE TIME VALUE for agreeing to part with the stock

- ⏰ June 18 expiration = Triple Witch OPEX -- 113 days out (~4 months), one of the highest-liquidity options expirations of the year

- 📈 Effective exit price: $366 ($340 strike + $26 premium = $366). If the stock is above $340 at expiration, the shares get called away at an effective $366 per share -- that's +5.7% above current price

- 🏦 Position size: 1,000,000 shares (10,000 contracts x 100 shares) = approximately $346M in underlying stock being monetized. This is 0.38% of Marriott's entire market cap in a single trade

What's the thesis here?

This is textbook institutional income generation through a covered call overwrite. The trader almost certainly owns 1,000,000+ shares of MAR and is writing calls against the position to collect yield. Here's the math:

- 🧮 Annualized yield from premium: $26M collected on a $346M position over ~4 months = ~7.5% income for the period, or ~24% annualized yield on top of the 0.78% dividend yield

- 🛡️ Downside buffer: The $26 premium provides protection down to $320.23 ($346.23 - $26), creating a 7.5% cushion before the position starts losing money

- 📉 The catch: If MAR rallies above $366, the seller misses the upside beyond that level. They've essentially pre-sold their shares at $366

Why $340? This is an IN-THE-MONEY covered call, which means the seller is signaling they're comfortable having the stock called away at this level. Choosing an ITM strike (rather than OTM) maximizes premium collected and increases the probability of assignment. This is someone who has already made their money on MAR and is now squeezing out every last dollar of return through income generation. They're saying: "I'll take my $366 effective exit and collect fat premium while I wait."

Why June 18 (Triple Witch)? Maximum liquidity, maximum time value premium, and the expiration falls AFTER Q1 earnings (May 5-6) and right at the start of FIFA World Cup (June 11). The seller is deliberately capturing the elevated IV around these events and converting it into income.

📈 Technical Setup / Chart Check-Up

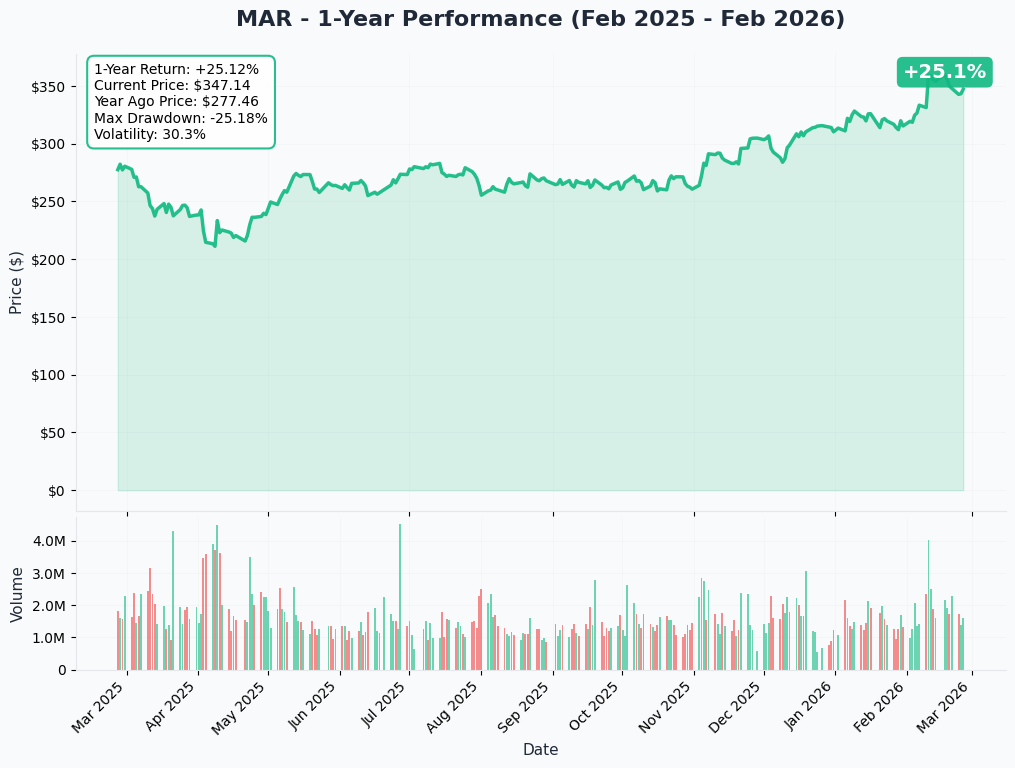

YTD Performance

MAR has had a strong start to 2026, trading at ~$346 after a significant post-earnings rally:

- 🚀 Post-earnings pop: Shares jumped ~9.1% on February 10 after Q4 2025 earnings beat revenue estimates ($6.69B vs $6.67B) and management projected a 35% surge in credit card fees for 2026

- 📈 Strong recovery from lows: Stock bounced from the ~$290 range three months ago to the mid-$340s, a gain of roughly +18%

- 📊 52-week range: $205.40 - $370.00 -- currently sitting in the upper third of that range

- 📉 Pullback from highs: Shares peaked near $361 on earnings day and have consolidated around $343-$347, digesting the rally

- 🎢 Insider selling cluster: CEO Capuano sold 63,000 shares and multiple EVPs sold at $356-$360 in mid-February -- insiders are taking profits near the highs

Key takeaway: MAR is consolidating after a powerful earnings-driven rally. The stock is trading near the top of its range but below the post-earnings spike high of $361. The overwrite trade at $340 suggests this institutional investor believes the stock will stay range-bound or grind modestly higher through June -- not blast through $370+.

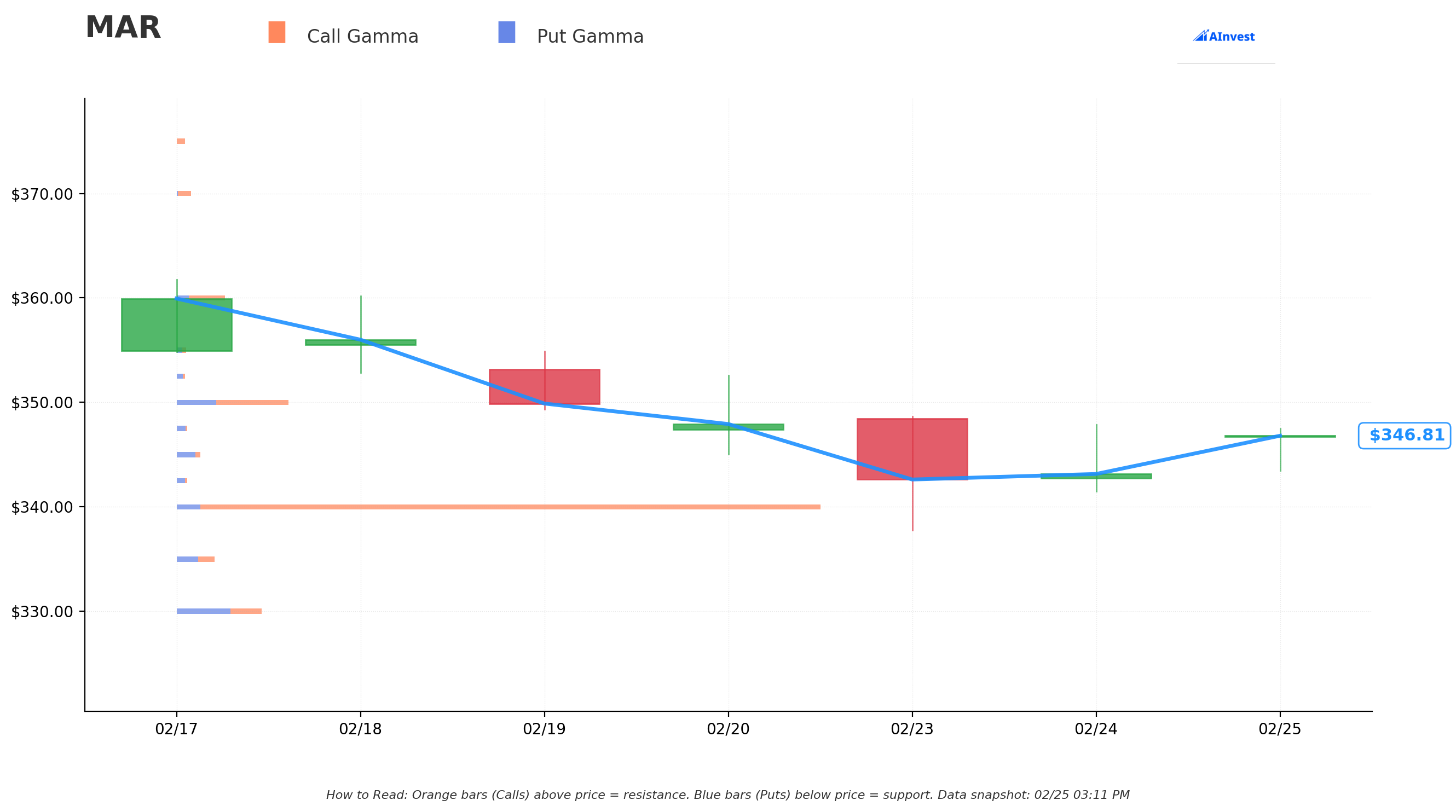

Gamma-Based Support & Resistance Analysis

Current Price: $346.70

The gamma exposure map reveals where options market makers have concentrated positions, creating natural price magnets and barriers:

🔵 Support Levels (Below Price):

- $345 -- Immediate support with 0.31B total gamma (just 0.5% below -- tight floor right underneath us)

- $340 -- MASSIVE structural support with 8.43B total gamma (1.9% below). This is THE strike from the overwrite trade! Enormous call gamma concentration here creates a powerful gravitational pull

- $335 -- Secondary support at 0.49B gamma (3.4% below)

- $330 -- Extended support at 1.11B gamma (4.8% below -- put gamma concentration picks up)

- $320 -- Deep support at 0.37B gamma (7.7% below)

- $310 -- Distant floor at 0.28B gamma (10.6% below)

- $300 -- Disaster scenario support at 0.37B gamma (13.5% below)

🟠 Resistance Levels (Above Price):

- $350 -- First resistance at 1.47B gamma (just 1.0% overhead -- reachable this week)

- $360 -- Significant resistance at 0.63B gamma (3.8% above -- approaching the post-earnings high)

- $370 -- Extended resistance at 0.19B gamma (6.7% above -- 52-week high territory)

What this means for traders: The gamma landscape is DOMINATED by the $340 strike with 8.43B in total gamma -- by far the highest concentration on the board. This creates a powerful gravitational pull toward $340 that works in the overwrite seller's favor. The $345-$350 corridor has moderate gamma, suggesting the stock can oscillate in this zone, but breaking above $360 becomes harder with fading gamma support. The trade's effective exit at $366 sits above all significant gamma resistance levels.

Net GEX Bias: Bullish (11.6B total call gamma vs 3.9B total put gamma) -- dealer positioning leans bullish overall, but the massive call gamma at $340 means dealers are short calls and will buy stock on dips to $340 (providing support) and sell into rallies (providing resistance above). This creates the range-bound environment that is ideal for covered call sellers.

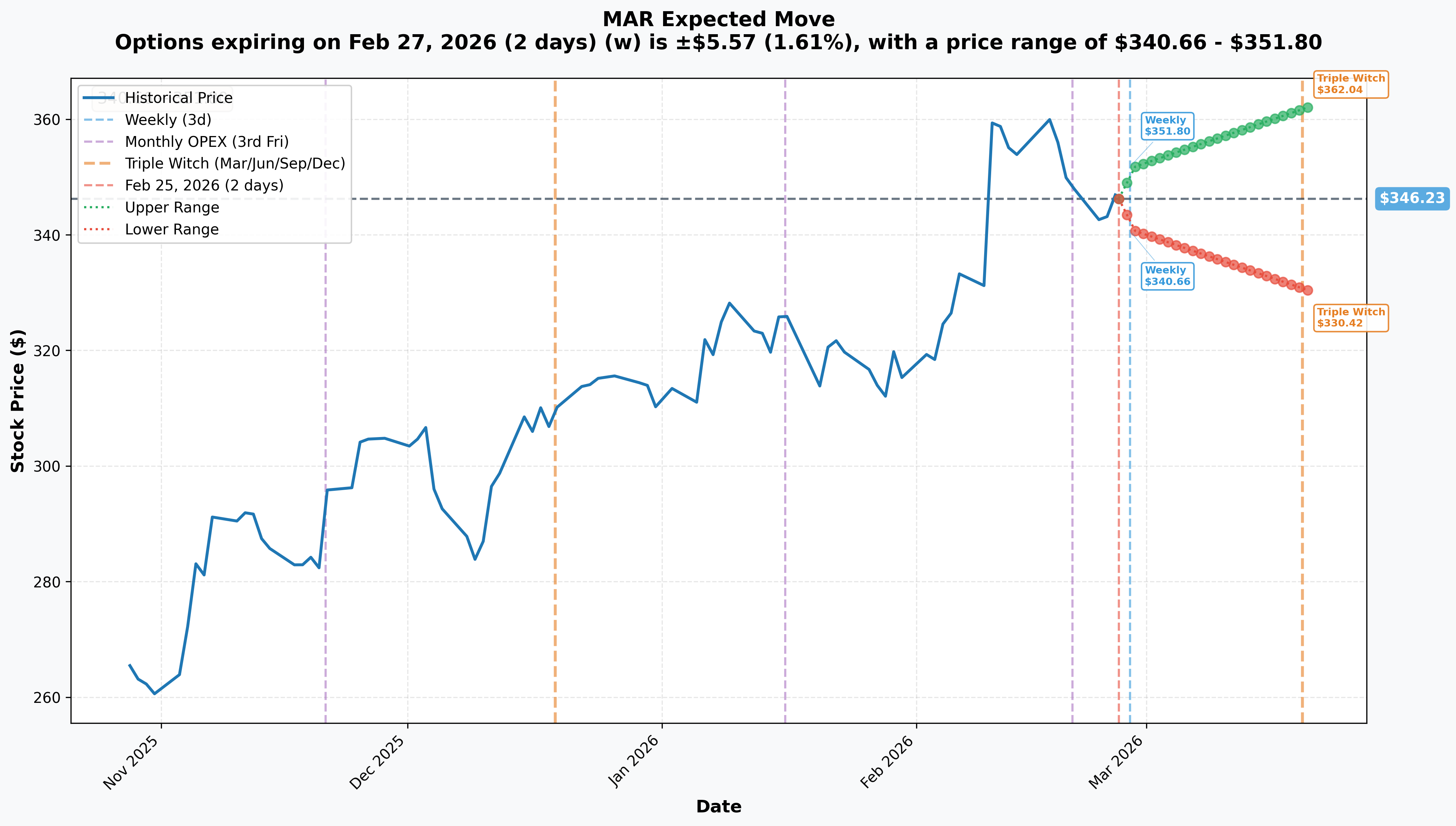

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Feb 27 -- 2 days): ±$5.57 (±1.61%) --> Range: $340.66 - $351.80

- 📅 Monthly OPEX / Triple Witch (Mar 20 -- 23 days): ±$15.81 (±4.57%) --> Range: $330.42 - $362.04

- 📅 June 18 OPEX (THIS TRADE!): The effective exit of $366 sits ABOVE the monthly Triple Witch implied upper range of $362.04

Translation: The options market currently prices MAR for a move of about ±4.6% through March Triple Witch. The overwrite seller's effective exit of $366 is ABOVE even the upper end of the monthly implied move ($362). In other words, this seller is getting paid a premium that exceeds what the market expects the stock to do. The implied move data supports the thesis that $366 is a generous exit price -- the market says MAR is more likely to stay BELOW that level than above it.

Key insight: The weekly implied move puts the lower bound at $340.66 -- almost exactly at the sold $340 strike. This means the market thinks $340 is close to the maximum downside for just this week alone. The strike wasn't chosen randomly; it aligns with the maximum probability zone for support.

🎪 Catalysts

🔥 Upcoming Catalysts

Q1 2026 Earnings -- Expected May 5-6, 2026 📊

This is the next major checkpoint for MAR, and the overwrite trade SPANS this event. Guidance calls for $2.50-$2.55 adjusted EPS (consensus $2.52). Key things to watch:

- 📊 U.S. & Canada RevPAR recovery after the 43-day government shutdown dragged Q4 RevPAR down 30%+

- 💳 Credit card fee momentum -- is the 35% growth target tracking on schedule?

- 🏨 Pipeline conversion pace (record 610,000 rooms in pipeline, 265,000 under construction)

- 🌏 International RevPAR trajectory (was +6.1% ex-China in Q4)

- 🇨🇳 Greater China demand (guided "roughly flat" for 2026)

Co-Branded Credit Card Fee Renegotiation -- H1/H2 2026 💳

This is potentially the single most impactful financial catalyst for MAR in 2026. Marriott is actively negotiating new credit card deals with JPMorgan Chase and American Express, expecting a 35% increase in credit card fee revenue -- from $716M in 2025 to an estimated ~$967M in 2026 (an incremental $251M in near-pure-margin revenue). This is the kind of catalyst that justifies holding the stock even while capping upside with a covered call.

FIFA World Cup 2026 -- June 11 to July 19, 2026 ⚽

Marriott Bonvoy is the Official Hotel Supporter in North America for the FIFA World Cup 2026. Management estimates the tournament will contribute approximately $55-65 million in hotel booking fees and add 30-35 basis points of global RevPAR growth for the year. The overwrite trade expires June 18 -- right at the START of the World Cup. The seller collects premium through the pre-tournament booking surge, then the stock potentially gets called away just as the event kicks off.

AI & Technology Deployment -- H1 2026 🤖

Marriott is deploying natural language search on marriott.com and its loyalty app, partnering with Google AI mode for travel planning and OpenAI Ad Pilot program. These aim to improve conversion rates and direct booking percentages across 271 million Bonvoy members.

International Growth Acceleration 🌍

Asia-Pacific (ex-China) delivered a third consecutive year of record development activity, with nearly 200 deals signed adding 28,000+ rooms. India alone saw a record 99 deals. This secular international expansion story provides structural growth beyond U.S. cycle dynamics.

✅ Recent Catalysts (Already Happened)

Q4 2025 Earnings -- February 10, 2026 📊

Record results that sparked a 9.1% rally: Revenue $6.69B (beat by $20M), Adjusted EPS $2.58 (slight miss vs $2.61 consensus but up from $2.45 YoY), and Adjusted EBITDA $1,402M (+9% YoY). The real catalyst was 2026 guidance: +13-15% adjusted EPS growth, +4.5-5.0% net rooms growth, and that blockbuster 35% credit card fee increase.

citizenM Acquisition Completed -- July 2025 🏨

Marriott completed its $355M acquisition of the citizenM brand, adding 37 hotels (8,789 rooms) across 20+ cities. The brand is now fully integrated into Marriott Bonvoy.

Record Development Pipeline -- January 2026 📈

4,056 properties with nearly 610,000 rooms in the pipeline -- a record, up 6% YoY with 265,000 rooms under construction (+15% YoY). Marriott signed 163,000 rooms organically in 2025, including a record 114 luxury deals.

Capital Returns -- $4B+ in 2025 💵

Over $4.0 billion returned to shareholders through dividends and buybacks, with 2026 guidance for more than $4.3B. The board expanded share repurchase authorization by 25 million shares.

Analyst Upgrades Wave -- January/February 2026 📊

Multiple price target raises post-earnings: Goldman Sachs to $398 (Buy), Evercore ISI to $350 (Outperform), JPMorgan to $356 (Neutral), Bernstein to $327 (Outperform). Consensus: Moderate Buy (8 Buy, 21 Hold, 0 Sell) with average target ~$343 (range $276-$398).

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, analyst targets, and the catalyst calendar, here are the scenarios through the June 18, 2026 expiration:

📈 Bull Case (25% probability)

Target: $370-$400

How we get there:

- 🚀 Q1 earnings crush expectations, U.S. RevPAR recovery stronger than the +1.5-2.5% guidance

- 💳 Credit card renegotiation finalizes early with terms better than the 35% projection -- approaching $1B in annual fees

- ⚽ FIFA World Cup booking data shows massive demand surge, driving ADR spikes in host cities

- 📊 Analyst upgrades accelerate, with more targets following Goldman's $398

- 📈 Stock breaks through $350 and $360 gamma resistance, clearing the path to new 52-week highs

- 🌍 International RevPAR continues to outperform at 5%+, APEC delivers another record year

What happens to the overwrite trade:

- At $370: Stock called away at $340, seller keeps $26 premium. Effective exit $366. Misses $4/share of upside above $366. Still profits $19.77/share in time value collected

- At $400: Stock called away at $340, seller keeps $26 premium. Misses $34/share of upside above $366. The "cost" of the covered call is real, but the seller still made $26 on a $346 stock (+7.5%)

This is the scenario where the overwrite seller leaves money on the table. But remember -- they collected $26M in premium. That's real cash, not paper gains. The opportunity cost hurts, but the income is banked.

🎯 Base Case (50% probability)

Target: $335-$365 range

Most likely scenario:

- ✅ Q1 earnings meet expectations ($2.50-$2.55 EPS), no major surprises

- 📊 RevPAR grows at the guided +1.5-2.5% globally, U.S. stays sluggish but stable

- 💳 Credit card fee trajectory on track but full details not disclosed until Q2

- ⚖️ Stock oscillates between $340 gamma magnet below and $350-$360 resistance above

- 📈 Analyst consensus (~$343 average) keeps the stock anchored near current levels

- 🏨 Pipeline conversions on schedule, no major positive or negative surprises

- 💤 Time decay erodes the call premium steadily, working in the seller's favor

What happens to the overwrite trade:

- At $350: Stock called away at $340, seller keeps $26 premium. Effective exit $366 vs $350 market price. Seller actually outperforms by $16/share -- the best possible outcome for a covered call

- At $340: Stock at the strike -- calls expire at-the-money. Seller keeps $26/share premium AND may keep the stock. Total return: $26 premium on $346 entry = +7.5% in 4 months

- At $335: Stock below strike, calls expire worthless. Seller keeps all $26M premium AND the shares. Stock is down $11.23 but premium of $26 more than offsets. Net position: +$14.77/share profit

This is the SWEET SPOT for the trade. In range-bound markets, the covered call overwriter wins big. They collect $26M and the stock barely moves. This is exactly why institutions love this strategy.

📉 Bear Case (25% probability)

Target: $300-$330

What could go wrong:

- 😰 U.S. recession materializes -- Marriott's own models show occupancy down 5-8 points, ADR down 5-10%, RevPAR down 10-15%

- 📉 Government travel cuts deepen further from DOGE-related federal spending reductions

- 🇨🇳 Greater China demand deteriorates beyond the "roughly flat" guidance

- 💳 Credit card deal negotiations hit snags or regulatory headwinds

- 📊 Premium valuation (36.6x P/E) compresses sharply on any earnings disappointment

- 🏷️ Multiple insider sales near $356-$360 prove to be prescient, not routine

- ⚔️ Hilton continues gaining competitive ground (6.7% room growth vs MAR's 4.3%)

- 📉 Stock breaks $340 gamma support and cascades toward $330, then $320

What happens to the overwrite trade:

- At $330: Calls expire worthless (seller keeps $26M), but stock is down $16.23. Net loss: $16.23 - $26 = still a +$9.77/share profit thanks to the premium cushion

- At $320: Calls expire worthless, stock down $26.23. Net position: essentially breakeven ($346.23 - $26 premium = $320.23 breakeven)

- At $300: Calls expire worthless, stock down $46.23. Net loss: $20.23/share after premium offset. This is where it hurts -- but the $26 cushion means the loss is $20/share instead of $46/share

Even in the bear case, the $26 premium provides meaningful downside protection. The overwrite seller breaks even at $320.23 -- that's 7.5% below current price. Only a full-blown selloff to $300 (-13.4%) starts generating real losses, and even then the loss is significantly less than holding the stock unhedged.

💡 Trading Ideas

🛡️ Conservative: "Copycat the Whale" - Covered Call Overwrite

Play: If you already own MAR shares, sell the June 18, 2026 $355 calls against your position

Why this works:

- 📊 Mirrors the institutional strategy but with a HIGHER strike ($355 vs $340), giving you more upside room before assignment

- 💰 Collect roughly $14-16/share in premium (~$1,400-$1,600 per 100 shares) -- that's income you keep no matter what

- 🛡️ Premium provides ~4-4.5% downside buffer on your shares

- 📈 Effective sale price of ~$369-$371 if called away -- that's above Goldman Sachs' average target and right at 52-week high territory

- ⏰ 113 days of time decay working in your favor -- theta is your friend

- 📊 Gamma structure shows $350-$360 is natural resistance -- stock likely struggles to blow past your strike anyway

- 🎯 If stock stays below $355, you keep shares AND premium -- roughly 4% income in 4 months (~13% annualized on top of dividends)

Position sizing: Only if you already own MAR shares and are willing to sell at ~$370. Write calls against 50-100% of your position depending on your willingness to part with shares.

Risk level: Low (you already own the stock, this generates income) | Skill level: Beginner-Intermediate

⚖️ Balanced: "The Range Rider" - Iron Condor

Play: Sell the June 18 $370 call / buy the $380 call AND sell the $320 put / buy the $310 put

Why this works:

- 🎯 Profits from MAR staying inside the $320-$370 range through June -- the same range-bound thesis behind the $26M overwrite

- 💰 Collect premium on both sides (call spread + put spread), estimated ~$4-6 per iron condor

- 📊 Short strikes ($320 put, $370 call) are well beyond the monthly implied move range of $330-$362

- 🛡️ Defined risk: maximum loss is $10 per spread minus premium collected (~$4-6 max loss)

- ⏰ Benefits from time decay on ALL four legs as June approaches

- 📈 The massive $340 gamma wall with 8.43B total gamma acts as a natural anchor keeping the stock range-bound

- 🤝 Net GEX bullish bias (11.6B call vs 3.9B put) supports dampened volatility and stable trading

Position sizing: 10-20 iron condors at ~$5 credit each = $5,000-$10,000 income, risking ~$5,000-$10,000 max.

Risk level: Moderate (defined risk, needs range-bound market) | Skill level: Intermediate-Advanced

🚀 Aggressive: "World Cup Rally" - June Bull Call Spread

Play: Buy the MAR June 18 $350 call, sell the June 18 $370 call

Why this works (and why it disagrees with the whale):

- 💥 Bets AGAINST the overwrite seller's thesis -- you're saying MAR breaks out to the upside

- 📊 The $350-$370 spread targets the zone above gamma resistance through the 52-week high

- ⚽ FIFA World Cup starts June 11 -- just one week before expiration. Booking revenue could surge and lift the stock

- 💳 Credit card deal finalization could be the surprise catalyst that pushes the stock through $360

- 💰 Cost: roughly $7-9 per spread. Max profit: $20 per spread minus debit = ~$11-13 profit

- 📈 Risk/reward: roughly 1.5:1, and you only need MAR above $358-$359 to profit

Why it could blow up:

- 📉 The $26M overwrite trade is telling you a sophisticated institution doesn't expect MAR above $366

- 🎢 Insider selling cluster at $356-$360 creates natural supply pressure

- ⏰ Need MAR to break through gamma resistance at $350 AND $360 within 4 months

- 📊 Consensus average target is only $343 -- the Street says you're wrong

Position sizing: Risk no more than 2-3% of portfolio. 10 spreads at ~$8 each = $8,000 risk for up to $12,000 max profit.

Risk level: HIGH (directional bet against a $26M institutional trade) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

📉 Insider selling cluster at record highs: CEO Capuano sold 63,000 shares, and multiple EVPs sold at $356-$360 in mid-February. While likely pre-planned (10b5-1 plans), the volume and timing near 52-week highs create visible supply pressure. When the people running the company are taking chips off the table, pay attention.

-

🏨 U.S. demand softness is real: U.S. & Canada RevPAR was essentially flat (-0.1%) in Q4, dragged down by the government shutdown. Government travel remains depressed ~15% for the year, and DOGE-related federal spending cuts could make it worse. Business travel still hasn't fully recovered to 2019 levels.

-

💸 Premium valuation leaves no room for error: At ~36.6x P/E, MAR trades at a premium to Hilton (~35x) and Hyatt (~32x). Consensus average price target ($343) is essentially AT current price, suggesting the Street sees limited near-term upside. Any guidance miss could trigger meaningful multiple compression.

-

📉 Recession risk is real: Marriott's own modeling suggests that in a moderate recession (GDP -1% to -2%): occupancy down 5-8 points, ADR down 5-10%, RevPAR down 10-15%, and fee revenue down 10-15%. The 2026 guidance assumes a "relatively steady macro environment" -- one that is not guaranteed.

-

💳 Credit card deal uncertainty: The 35% credit card fee growth projection is based on negotiations with JPMorgan Chase and American Express that are NOT yet finalized. The 2026 guidance actually EXCLUDES potential additional upside from restructured deals. If negotiations stall or regulatory changes impact interchange fees, this catalyst could underwhelm.

-

🇨🇳 Greater China remains a headwind: Marriott guided Greater China RevPAR "roughly flat" for 2026, with weak macro conditions and soft consumer sentiment continuing to drag. This is a meaningful portion of the international portfolio showing no growth.

-

⚔️ Hilton is gaining ground: Hilton's net rooms growth (6.7%) materially outpaces Marriott's (4.3%), and Hilton Honors membership is projected to surpass Marriott Bonvoy's 271M members by mid-to-late 2026. Hilton's EPS growth estimate (14.2%) also slightly exceeds Marriott's (13.5%). The competitive moat is narrowing.

-

🏚️ Sonder fallout: The Sonder bankruptcy removed ~9,000 rooms from Marriott's planned additions and left guests stranded at former properties. While management called it a learning experience with limited financial impact, the pipeline hit and reputational risk are real.

-

⏰ Earnings volatility risk: Q1 earnings on May 5-6 falls within this option's lifespan. Even an in-line report could trigger a "sell the news" reaction after the 9% post-Q4 jump. The market has high expectations for credit card fee momentum and RevPAR recovery -- any shortfall gets punished at this valuation.

🎯 The Bottom Line

Here's the deal: Someone managing a ~$346M position in MAR just collected $26 million in premium by writing 10,000 in-the-money calls at $340 expiring June 18. This is not a bearish bet. This is not a hedge. This is a professional income generation strategy executed by someone who has made their money on Marriott and is now squeezing every last drop of return from the position while they wait for a graceful exit.

What this trade tells us:

- 🎯 An institution with 1,000,000 shares believes MAR will stay in a range through June -- NOT crash, but NOT rocket to $400 either

- 💰 They're willing to sell their shares at an effective $366 (+5.7% from here) -- that's a decent return but well below Goldman's $398 target

- ⏰ The June Triple Witch expiration is strategic: it captures Q1 earnings IV, early World Cup buzz, and maximum time premium

- 📊 The ITM $340 strike signals comfort with assignment -- this is someone planning an EXIT, not hoping to keep the shares

- 🛡️ The $26/share premium creates a 7.5% downside cushion, protecting the position down to $320.23

This IS a neutral-to-mildly-bullish signal, with important context: The overwrite seller is saying: "MAR has had a great run, the catalysts are largely priced in at 36.6x P/E, insiders are selling near the highs, and I'd be happy to exit at $366 while collecting a ~24% annualized yield." That's a sophisticated, risk-aware view -- not wildly bullish, not bearish, just pragmatically taking income from a position that may have limited upside from here.

If you already own MAR:

- ✅ Consider writing covered calls against your position -- the institutional playbook is right in front of you

- 📊 Use the $340 gamma wall (8.43B total gamma) as your key support level -- if the stock breaks below with conviction, reassess

- ⏰ Mark May 5-6 (Q1 earnings) as the next major data point. If earnings disappoint, the stock could test $330

- 💳 Watch for credit card deal headlines -- finalization could be the catalyst that pushes MAR through $360+

If you're watching from the sidelines:

- 🎯 A pullback to the $330-$340 area (strong gamma support) would offer a better entry point

- 📊 The analyst consensus average of $343 says you're buying at fair value right now -- not a bargain

- ⚽ The FIFA World Cup starting June 11 is a quantifiable catalyst ($55-65M in fees) -- position ahead of it if you believe

- 📈 Goldman's $398 target is the high-water mark on the Street -- that's your theoretical ceiling if everything goes right

If you're bearish:

- ⚠️ The insider selling cluster at $356-$360 validates your skepticism

- 📉 U.S. RevPAR stagnation and 36.6x P/E create a fragile setup for any economic downturn

- 🛡️ Put spreads in the $320-$330 area offer defined-risk downside plays below the gamma support

- 📊 A break below $340 would be technically significant given the massive gamma concentration there

Key dates to mark:

- 📅 February 27 -- Weekly OPEX (±1.6% implied move)

- 📅 March 20 -- Monthly OPEX / Triple Witch (±4.6% implied move)

- 📅 May 5-6, 2026 (estimated) -- Q1 2026 earnings (credit card fee trajectory, U.S. RevPAR recovery)

- 📅 June 11, 2026 -- FIFA World Cup 2026 kicks off (Marriott Bonvoy is Official Hotel Supporter)

- 📅 June 18, 2026 -- THIS TRADE EXPIRES (Triple Witch OPEX -- moment of truth for the $26M overwrite)

- 📅 H1/H2 2026 -- Credit card deal renegotiation with JPMorgan Chase and American Express (timing TBD but this is the biggest catalyst)

- 📅 Late July / Early August 2026 -- Q2 2026 earnings (World Cup booking impact, updated full-year guidance)

Final verdict: This $26M overwrite trade is one of the most instructive institutional trades you'll see all year. It tells you exactly how a professional money manager thinks about a stock at full valuation: "I've made my money, the catalysts are known, the insiders are selling, and I can collect $26M in income while waiting for an orderly exit at $366." For retail traders, the lesson is clear -- when a stock is priced for perfection at 36.6x earnings, there's more money to be made selling premium than chasing upside. The covered call overwrite is the grown-up play. Let the stock pay you while you wait.

Be smart. Collect premium. And remember: the institution with $346M in MAR shares is telling you the easy money has already been made. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Covered call strategies limit upside potential while providing only partial downside protection. Selling options carries assignment risk. Always do your own research and consider consulting a licensed financial advisor before trading.

About Marriott International: Marriott International is the world's largest hotel company, operating and franchising over 9,300 properties with approximately 1.77 million rooms across more than 30 brands in 140+ countries and territories. With 271 million Marriott Bonvoy loyalty members and a market cap of $90.9B, Marriott is the dominant player in the Hotels, Rooming Houses, Camps & Other Lodging Places industry, spanning ultra-luxury (Ritz-Carlton, St. Regis) through midscale (Series by Marriott) hospitality.