💰 MMM: Whale Dumps $61M in Deep ITM Calls — Cashing Out of the Turnaround!

📅 February 6, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just sold a $61 MILLION block of deep in-the-money MMM calls — that's 26,500 contracts at the $150 strike, one of the largest single option trades in 3M's history. With MMM trading at $172.33, this looks like a massive profit-taking event after the stock's turnaround from 2024 lows. Are the smart money players heading for the exits? 👀

🏢 Company Overview

3M Company ($87B market cap) is a multinational conglomerate selling tens of thousands of products from sponges to respirators across three segments: Safety & Industrial, Transportation & Electronics, and Consumer. The company is in the middle of a major turnaround after spinning off its healthcare unit (Solventum) and resolving multi-billion dollar litigation for Combat Arms earplug settlements ($6B) and PFAS water contamination ($10.3B). Sector: Surgical & Medical Instruments | Employees: 60,500

💰 The Option Flow Breakdown

📊 What Just Happened

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:56 | MMM | MID | SELL | CALL | 2026-03-20 | $61.0M | $150 | 27,000 | 28,000 | 26,500 | $172.33 | $23.10 |

💵 Total Premium: $61.0M

🤓 What This Actually Means

This is a sell-to-close (STC) of deep in-the-money calls — classic institutional profit-taking:

🐋 The Trade Breakdown:

- Sold 26,500 contracts of the March 20 $150 calls at ~$23.10 each

- With MMM at $172.33, these calls have $22.33 of intrinsic value

- The Volume (27,000) roughly matches Open Interest (28,000) — nearly the entire position was liquidated

- At $61M in proceeds, this is someone cashing a monster winner

Translation: A big player rode MMM from much lower levels (likely bought when the stock was near $150 or below) and is now ringing the register after a 15%+ move. This isn't a new bearish bet — it's an old bullish bet being closed out. The question is: do they know something about the ceiling here, or are they simply disciplined about taking profits?

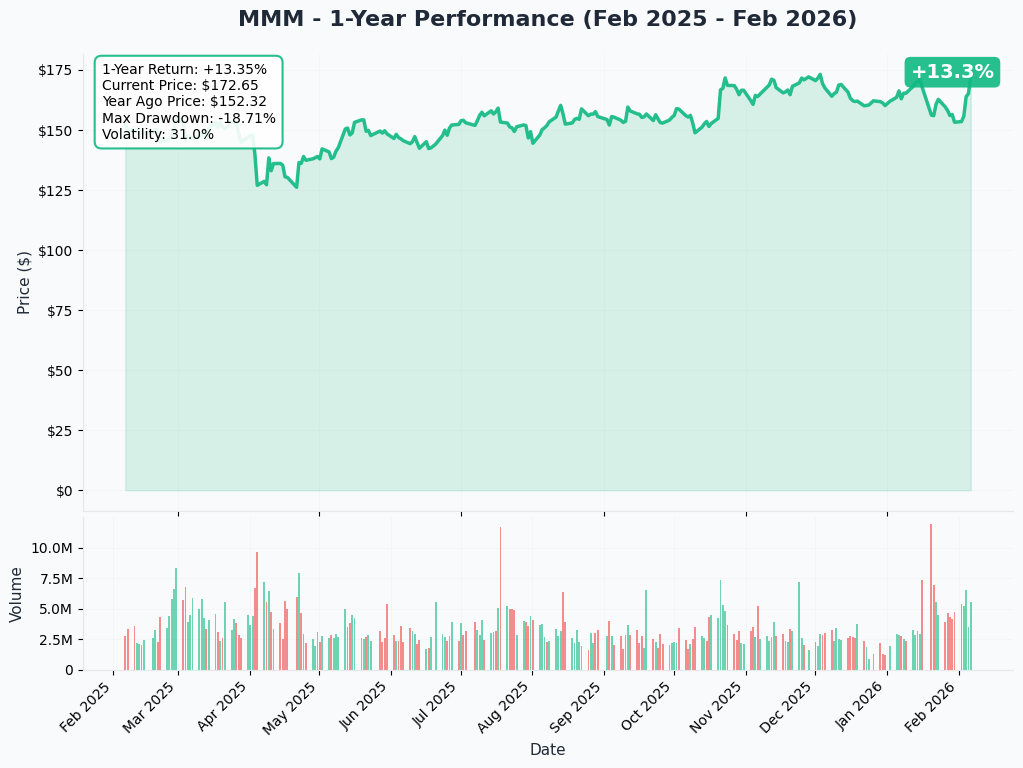

📈 Technical Setup / Chart Check-Up

YTD Performance

MMM is down about 4.4% YTD after a January selloff triggered by the Q4 earnings guidance miss. The stock dropped 8.8% after reporting.

The chart shows a sharp decline in late January when 2026 EPS guidance of $8.50-$8.70 missed consensus, followed by a partial recovery.

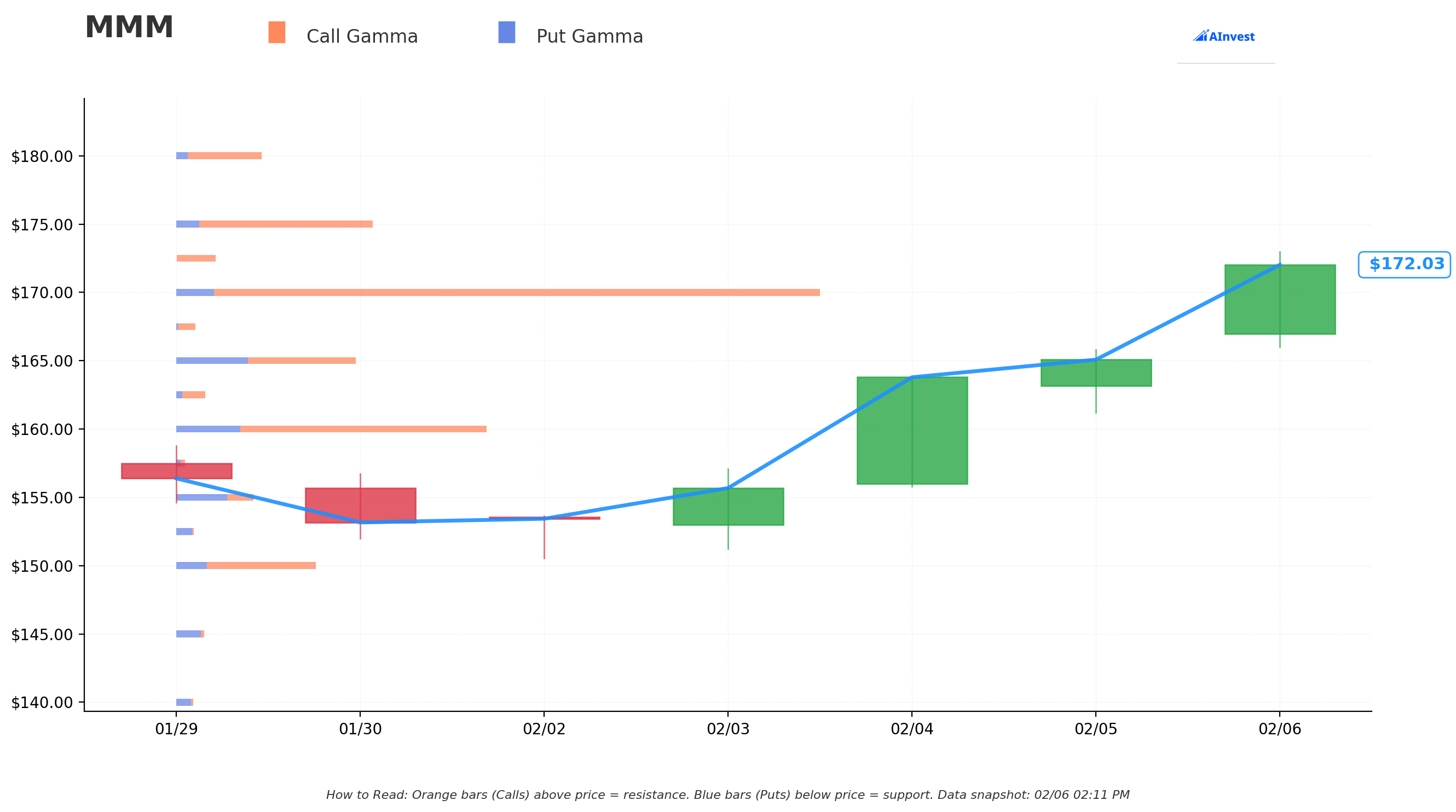

🔵🟠 Gamma-Based Support & Resistance Analysis

Gamma-Based Support & Resistance Analysis:

🛡️ Support Levels:

- $170 — Strongest gamma support level with heavy call GEX (7.75). This is the key floor to watch

- $165 — Secondary support with moderate activity

- $160 — Major support with significant call open interest

- $150 — The whale's strike price — huge gamma node here

🎯 Resistance Levels:

- $172.50 — Immediate resistance just above current price

- $175 — Strongest resistance with solid call GEX (2.23)

- $180 — Moderate resistance zone

- $185 — Upper resistance, near analyst targets

📊 GEX Bias: Bullish — Call GEX ($20.5) significantly exceeds Put GEX ($5.0), creating a positive gamma environment. Market makers are long gamma, which dampens volatility and creates a gravitational pull toward current levels.

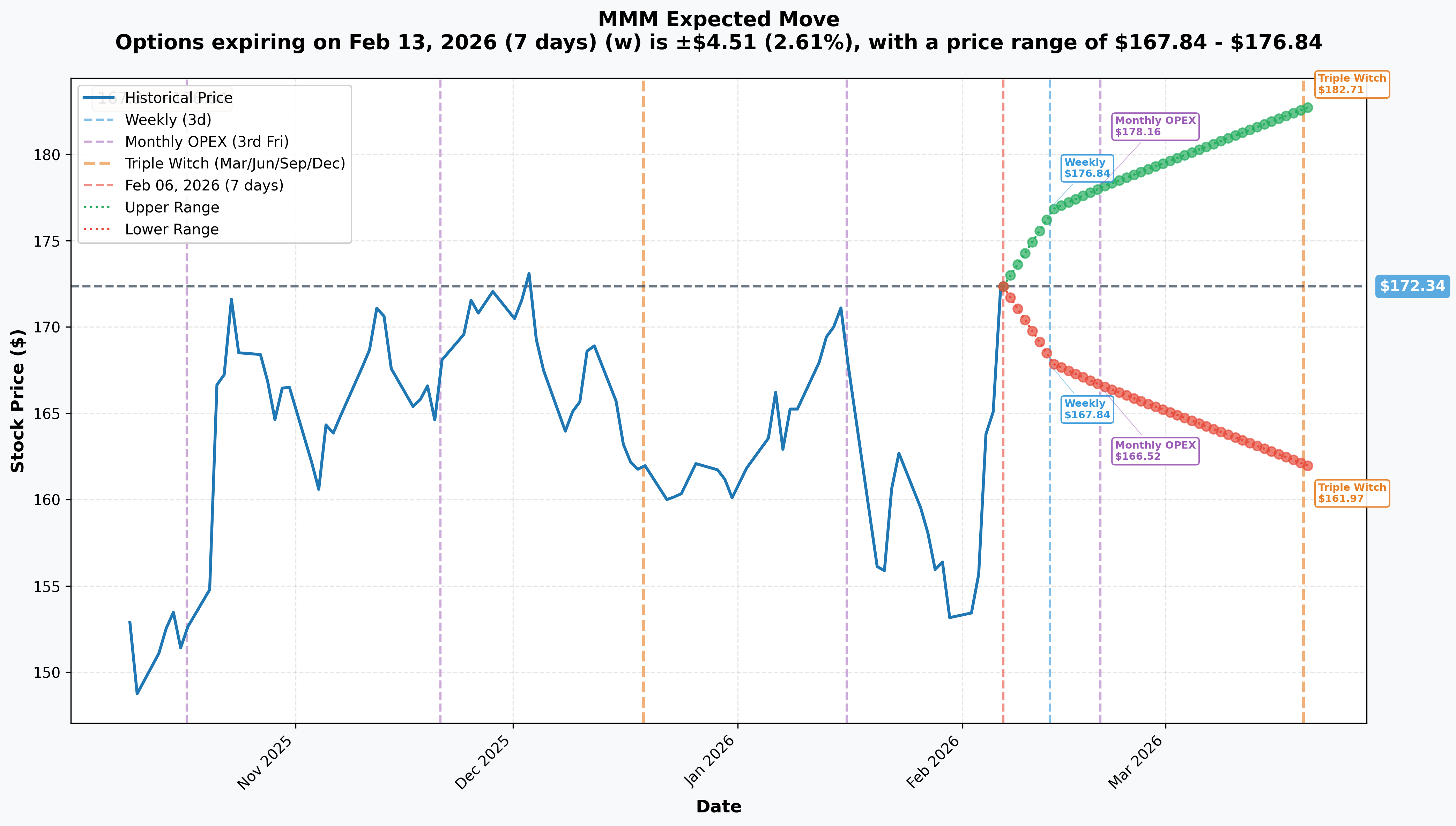

📊 Implied Move Analysis

Options-Implied Price Ranges:

The implied move data for MMM suggests a relatively contained trading range given the stock's lower volatility compared to tech names. The gamma support at $170 and resistance at $175 define a tight near-term range. The March 20 expiration (when the whale's calls expire) will be the key timeframe to watch.

🎪 Catalysts

✅ Already Happened (Recent)

- 📊 Q4 2025 Earnings (Jan 20) — Adjusted EPS $1.83 (+9% YoY), revenue $6.1B (+2.1%) per 3M Investor Relations

- 😰 2026 Guidance Miss — EPS guidance $8.50-$8.70 missed consensus, stock dropped 8.8% per Seeking Alpha

- ✅ Earplug Settlement Progress — Over $3.1B of $6B paid out, only 9 cases remain per DrugWatch

- ✅ PFAS Settlement Approved — $10.3B settlement received final court approval per 3M IR

- 📈 Margin Expansion — Full-year operating margin expanded 200bps to 23.4% per 24/7 Wall St

- 📉 JP Morgan Downgrade (Jan 16) — Cut from Overweight to Neutral, PT $182 per StockAnalysis

🔮 Upcoming

- 📊 Q1 2026 Earnings — April 28, 2026 (estimated) per MarketBeat

- 💰 Earplug Payment — $75M cash payment scheduled April 15, 2026 per Miller & Zois

- ⚠️ PFAS Claims Deadline — Phase 2 claims due by July 31, 2026 — could reveal additional liabilities per PFAS Settlement

- 🌍 Tariff Headwinds — $30-40M European tariff headwind NOT in guidance per Primary Ignition

🎲 Price Targets & Probabilities

Using gamma levels, implied moves, and catalyst timing:

🐻 Bear Case: $155-$165 (20% probability)

- Break below $170 gamma support triggers selling

- Tariff headwinds + guidance disappointment at Q1 earnings

- PFAS Phase 2 reveals higher-than-expected liabilities

- Analyst low target at $109.50 (extreme case)

⚖️ Base Case: $170-$180 (55% probability)

- Range-bound between $170 support and $175-$180 resistance

- Restructuring margin expansion continues at 70-80bps

- Forward P/E of ~19.9x still well below peer group (~33.5x)

- Analyst consensus target: $172.53 per MarketBeat

🚀 Bull Case: $180-$200 (25% probability)

- Strong Q1 earnings accelerate organic growth above 3%

- Consumer segment returns to growth

- Litigation discount fully unwinds as settlements complete

- Barclays target: $190 per StockAnalysis

💡 Trading Ideas

🛡️ Conservative: "The Dividend Collector"

- Buy MMM shares at $170-$172 (near gamma support)

- Collect the 1.77% dividend yield ($2.92/year) while you wait

- Set stop-loss at $160

- Target: $180-$185 over 3-6 months

- Risk: ~7% | Reward: ~5-8% + dividend | R:R = 1:1

- Why this works: Forward P/E at 19.9x is 40% below peers. Litigation overhang clearing

⚖️ Balanced: "The Range Player"

- Sell March 20 $165 puts (collect ~$1-2 premium)

- You're getting paid to potentially buy at $163-164 if it dips

- Gamma support at $165 makes this a solid floor

- Risk: Must buy 100 shares at $165 per contract | Reward: Premium income

- Why this works: The whale just closed their position — max selling pressure may be done

🚀 Aggressive: "The Turnaround Bet"

- Buy April 28 $175 calls (near Q1 earnings)

- Estimated cost: ~$3-4 per contract

- Break-even: ~$178-179 by expiration

- Target: $185+ on a strong Q1 earnings beat

- Risk: Full premium | Reward: 3-5x if bull case

- Why this works: If restructuring gains continue, the guidance miss gets corrected at Q1

⚠️ Risk Factors

- 📉 Whale Exit Signal — When $61M walks out the door, it's worth asking why

- 💸 Guidance Already Missed — EPS target of $8.50-$8.70 disappointed the market once. Can they deliver?

- 🌍 Tariff Uncertainty — $30-40M European tariff headwind excluded from guidance per GuruFocus

- ⚖️ PFAS Phase 2 Risk — July 31 deadline could surface additional liabilities

- 📊 Consumer Segment Weakness — Organic growth declined 2.2% in Q4 per Motley Fool

- 📉 Margin Deceleration — Guided +70-80bps in 2026 vs. +200bps achieved in 2025

🎯 The Bottom Line

Here's the deal: A whale just cashed out $61M from a deep ITM position in MMM — that's profit-taking on the turnaround trade, plain and simple. The good news? MMM's turnaround fundamentals are intact: litigation is clearing, margins are expanding, and the stock trades at a steep discount to peers (19.9x vs. 33.5x). The bad news? Growth is modest (~3% organic), guidance already disappointed, and tariffs are a wildcard.

The game plan:

- 🟢 If you own it: The turnaround story is still playing out. Hold for $180+ unless $170 breaks

- 🟡 If you're watching: Wait for the dust to settle from this $61M exit. The April Q1 earnings will be the next big test

- 🔴 If you're bearish: The whale agrees with you short-term. But the 19.9x forward P/E limits the downside

The turnaround isn't over. But the easy money has been made. 💪

⚠️ Disclaimer: This analysis is for educational purposes only and does not constitute financial advice. Options trading involves significant risk of loss. Always do your own research and consider your risk tolerance before trading.