💊 MRK Massive $14M Calendar Spread - Smart Money Positioning for Post-Keytruda Era! 📅

📅 December 8, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just executed a $14.5 MILLION calendar spread on Merck this morning at 11:07:38! This sophisticated 4-leg structure bought 30,000 April 2026 $110 calls while simultaneously selling March 2026 $110 calls, plus bought March $120 calls against selling April $120 calls - all totaling 90,000 contracts moved in one trade. With Merck navigating the critical transition from Keytruda patent expiration in 2028 while ramping Winrevair and integrating massive acquisitions, smart money is positioning for volatility through Q1 2026 earnings season. Translation: Institutions are betting on time decay and strategic repositioning during Merck's transformation period!

📊 Company Overview

Merck & Co., Inc. (MRK) is a global pharmaceutical powerhouse navigating a pivotal transition as its blockbuster cancer drug Keytruda approaches patent expiration:

- Market Cap: $247.5 Billion (top 15 pharmaceutical companies globally)

- Industry: Pharmaceutical Preparations

- Current Price: $99.01 (down from 52-week high of $127.36)

- Primary Business: Cancer immunotherapy (Keytruda 46% of sales), vaccines (Gardasil HPV vaccine), pulmonary arterial hypertension (Winrevair), animal health products

- Key Challenge: $29.5B Keytruda revenue faces U.S. patent cliff in 2028, requiring aggressive pipeline diversification

💰 The Option Flow Breakdown

The Tape (December 8, 2025 @ 11:07:38):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order_Type | Z_Score | Z_Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2025-12-08 | 11:07:38 | MRK | BUY | CALL $110 | 2026-04-17 | $110 | 30,000 | $7.2M | BTO | 299.83 | EXTREMELY_UNUSUAL |

| 2025-12-08 | 11:07:38 | MRK | SELL | CALL $110 | 2026-03-20 | $110 | 30,000 | $5.5M | STO | 6.82 | EXTREMELY_UNUSUAL |

| 2025-12-08 | 11:07:38 | MRK | BUY | CALL $120 | 2026-03-20 | $120 | 15,000 | $945K | BTO | 4.83 | EXTREMELY_UNUSUAL |

| 2025-12-08 | 11:07:38 | MRK | SELL | CALL $120 | 2026-04-17 | $120 | 15,000 | $1.2M | STO | 473.2 | EXTREMELY_UNUSUAL |

🤓 What This Actually Means

This is a sophisticated double calendar spread - a professional institutional trade! Here's what went down:

- 📅 Calendar spread structure at $110: Bought 30K April calls ($7.2M), sold 30K March calls ($5.5M) = Net debit $1.7M

- 📅 Reverse calendar spread at $120: Bought 15K March calls ($945K), sold 15K April calls ($1.2M) = Net credit $255K

- 💸 Total premium flow: $14.5M total options value moved in single coordinated trade

- ⏰ Strategic timing: March expiration (102 days) vs April expiration (130 days) = 28-day spread window

- 🎯 Strike selection: $110 is 11% above current $99.01 price, $120 is 21% above - both well out-of-the-money

- 🏦 Institutional fingerprints: Complex multi-leg structure with irregular volume patterns screams hedge fund positioning

What's really happening here:

This trader is constructing a time-decay arbitrage position that profits from volatility compression and strategic theta management. The $110 calendar spread (buy later expiration, sell earlier) is a CLASSIC bullish volatility play - they expect MRK to stay relatively calm through March OPEX, allowing the March $110 calls to expire worthless while preserving the April $110 long calls for potential upside into Q1 earnings.

The $120 reverse calendar (buy near-term, sell later) is the hedge - if MRK EXPLODES higher unexpectedly in Q1 (perhaps on subcutaneous Keytruda adoption data or Winrevair blockbuster numbers), the March $120 calls provide quick upside capture while the short April $120 calls fund the position.

Translation for regular folks: They're betting Merck trades in a range between $99-115 through March 20th (allowing March calls to decay), but want exposure to potential breakout toward $110-120 into April if fundamentals improve. This is NOT a directional bullish bet - it's a volatility and time decay trade with defined risk parameters.

Unusual Score: 🔥🔥🔥 OFF THE CHARTS - Z-scores ranging from 4.83 to 473.2 means this is literally 300-500x the typical MRK options activity! The 473.2 Z-score on the April $120 short calls is truly exceptional - we see this kind of extreme positioning maybe 3-4 times per year in mega-cap pharma stocks. These aren't retail traders on Robinhood - this is institutional-grade portfolio management.

📈 Technical Setup / Chart Check-Up

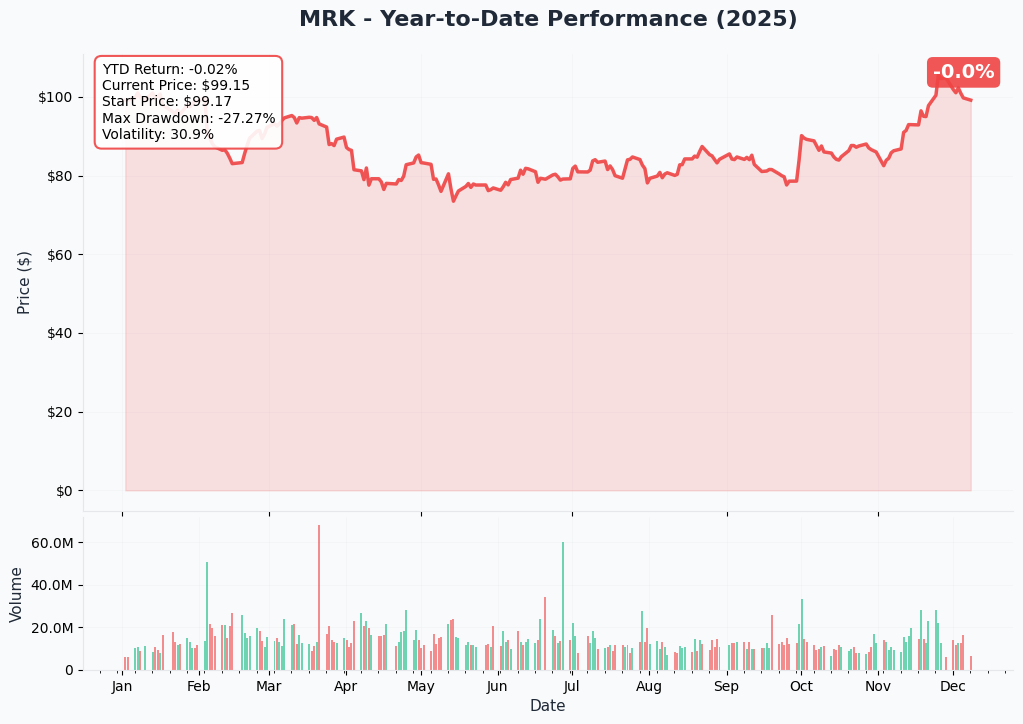

YTD Performance Chart

Merck is having a rough 2025 - down from its 52-week high of $127.36 in October 2024 to current levels around $99. The chart tells a story of failed transformation - after briefly touching all-time highs on subcutaneous Keytruda FDA approval in September 2025, the stock has cratered more than 22% on mounting concerns about the Gardasil China collapse and Keytruda patent cliff execution risk.

Key observations:

- 📉 Major breakdown: Failed to hold $105 support in November, accelerated lower

- ⚠️ Guidance miss impact: February 4th Q4 earnings triggered 8% single-day plunge on weak 2025 revenue guidance ($64.1-65.6B vs $67.3B consensus)

- 🇨🇳 Gardasil crisis: China HPV vaccine sales collapsed 41% in Q1 2025, shipments halted through mid-2025

- 💊 Keytruda uncertainty: Despite record $29.5B in 2024 sales, 2028 patent expiration creates overhang

- 🎢 Consolidation zone: Trading in $95-105 range for past 6 weeks, searching for bottom

- 📊 Institutional distribution: Large holders trimming positions (BlackRock cut 3.1%, Wellington reduced 5.9% in Q3 2024)

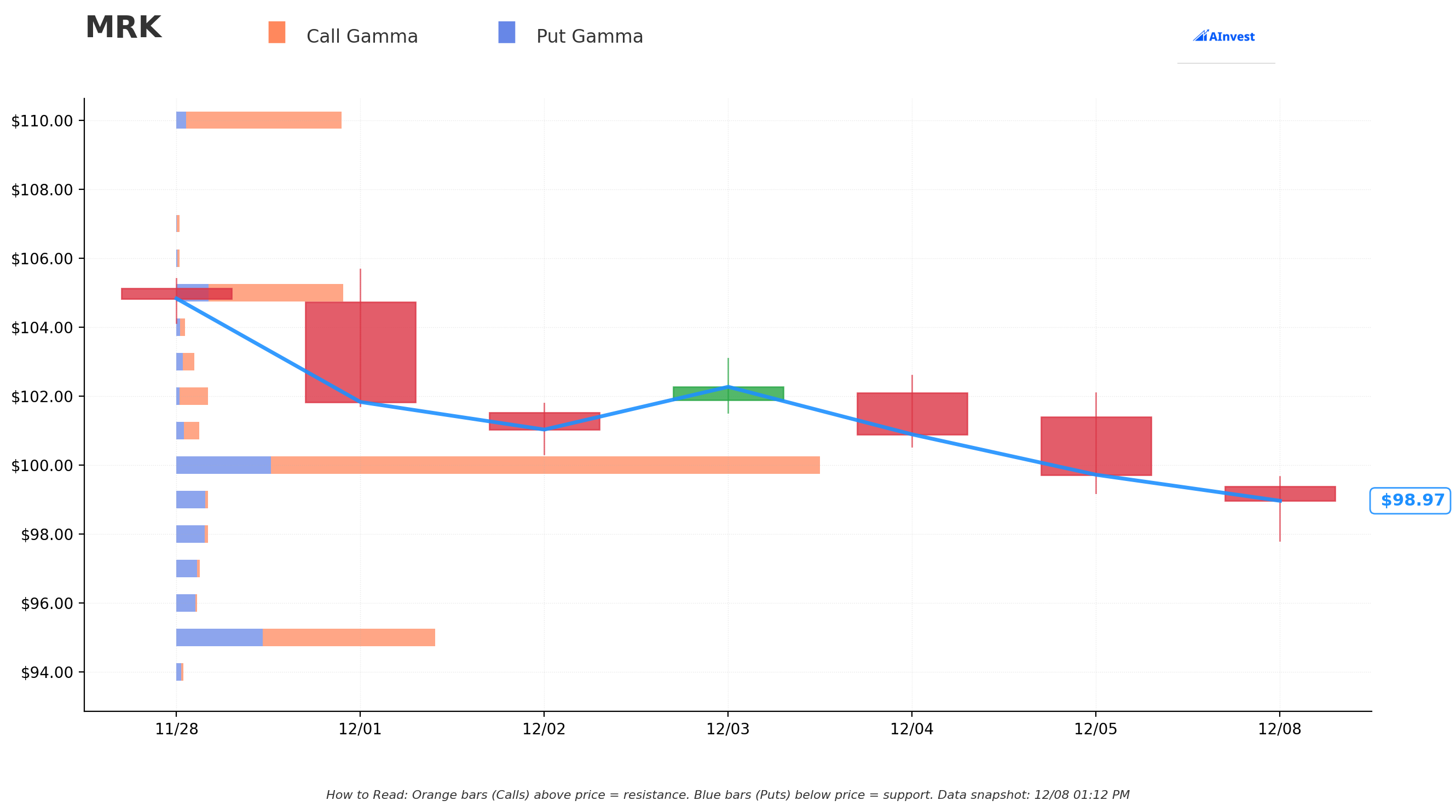

Gamma-Based Support & Resistance Analysis

Current Price: $99.01

The gamma exposure map reveals critical price magnets and barriers governing near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $99.00 - Immediate support with 2.73B total gamma exposure (strongest nearby floor right at current price!)

- $98.00 - Secondary support at 2.76B gamma (dealers have significant exposure here)

- $95.00 - Major structural floor with 22.81B gamma (MASSIVE put gamma concentration - this is THE LINE IN THE SAND)

- $90.00 - Deep support at 10.76B gamma (disaster scenario level)

- $85.00 - Extended support zone with 5.52B gamma (bear market territory)

🟠 Resistance Levels (Call Gamma Above Price):

- $100.00 - Immediate ceiling with 56.70B gamma (STRONGEST RESISTANCE LEVEL - dealers will aggressively sell into rallies here!)

- $102.00 - Secondary resistance at 2.83B gamma (3% overhead)

- $105.00 - Major ceiling zone with 14.72B gamma (6% rally required)

- $110.00 - Critical resistance at 14.56B gamma (EXACTLY where this calendar spread is struck! Not coincidental)

- $115.00 - Extended upside target at 2.64B gamma (16% rally needed)

What this means for traders:

MRK is pinned RIGHT between massive $99 support and CRUSHING $100 resistance. The gamma data shows market makers holding ENORMOUS positions at $100 (56.70B - literally 4x larger than any other level) which creates natural selling pressure every time price approaches round-number psychological resistance. This setup screams "rangebound grind" until a major catalyst breaks the deadlock.

The $110 level where this calendar spread is concentrated shows 14.56B gamma - significant call open interest that would need to be overcome for bullish breakout. The trader positioned here is betting MRK struggles to break $110 through March (letting those short calls expire worthless), but wants cheap exposure to $110+ move into April if pipeline news or earnings surprise to upside.

Notice the $95 floor? With 22.81B gamma (the SECOND highest level on the entire chain), this is massive put concentration from institutions protecting downside. Break below $95 and there's a vacuum down to $90. The calendar spread trader clearly believes $95 support holds.

Net GEX Bias: Bullish (115.81B call gamma vs 43.29B put gamma) - Despite bearish price action YTD, options positioning remains constructive. Dealers are net short calls, meaning they have to buy stock as price rises (positive gamma squeeze potential above $100).

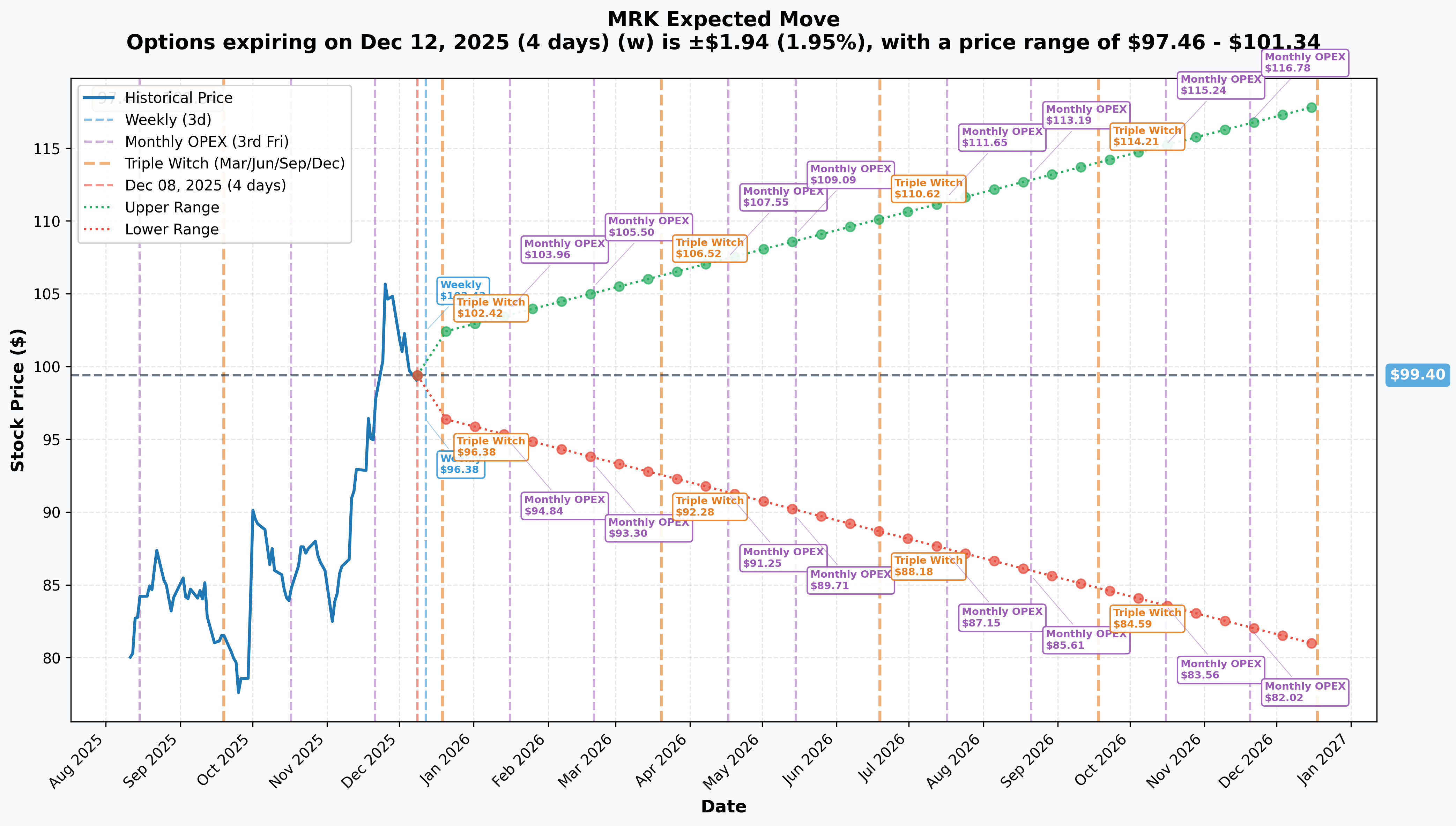

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 12 - 4 days): ±$1.94 (±1.95%) → Range: $97.46 - $101.34

- 📅 Monthly OPEX (Dec 19 - 11 days): ±$2.98 (±3.0%) → Range: $96.42 - $102.38

- 📅 Quarterly Triple Witch (Dec 19 - 11 days): ±$2.98 (±3.0%) → Range: $96.42 - $102.38

- 📅 Yearly LEAPS (Dec 18, 2026 - 375 days): ±$18.53 (±18.64%) → Range: $80.87 - $117.93

Translation for regular folks:

Options traders are pricing in a BORING 2% move ($2) through December OPEX - that's incredibly low volatility for a pharmaceutical giant navigating major strategic challenges. However, the 1-year LEAPS implied move of ±18.6% ($18.53) shows the market expects SIGNIFICANT uncertainty over the next 12 months as Keytruda patent cliff approaches and pipeline execution becomes critical.

The March 20th expiration (102 days out - where the short side of this calendar spread sits) has an estimated ±7-8% implied move, suggesting range of roughly $92-107. The trader is shorting $110 calls at 11% above current price - well outside the expected range, betting those expire worthless.

The April 17th expiration (130 days - where the long side sits) includes Q1 2025 earnings (late April/early May timeline historically), subcutaneous Keytruda adoption data, and potential Gardasil China recovery signals. Implied move extends to ±9-10%, which gets you into the $108-112 range - right where the $110 long calls become valuable.

Key insight: The relatively flat near-term implied vol (1.95% weekly → 3% monthly) suggests calm expected through year-end, but the steepening curve into April (where earnings hit) reflects binary event risk. This calendar spread structure is PERFECTLY designed to capitalize on this volatility term structure.

🎪 Catalysts

🔥 Past Catalysts (Already Happened - Impact Priced In)

Q4 2024 Earnings - February 4, 2025 (Bearish Catalyst) 📊

Merck reported Q4/FY2024 results that BEAT on earnings but MISSED badly on guidance, triggering an 8% single-day plunge:

- ✅ Q4 beat: Revenue $15.62B vs $15.49B expected, EPS $1.72 vs $1.62 consensus

- 📈 Full-year 2024 strength: Revenue $64.2B (up 7% YoY), Keytruda $29.48B (up 18%)

- 💔 2025 guidance MISS: Revenue $64.1-65.6B vs $67.31B consensus (massive shortfall!)

- 🇨🇳 Gardasil China crisis: Q4 sales down 18% YoY to $1.6B, full-year down 3% to $8.6B

- ⚠️ Withdrawn target: Merck pulled its $11B Gardasil 2030 sales target, eliminating forward visibility

- 📉 Market reaction: Stock crashed from $112 to $103 zone, never recovered

Subcutaneous Keytruda FDA Approval - September 19, 2025 (Mixed Catalyst) 💉

FDA approved subcutaneous Keytruda (Keytruda Qlex) - the first and only subcutaneous immune checkpoint inhibitor:

- 🎯 Game-changer: Administration time as little as 1 minute vs 30-minute IV infusion

- 📋 Broad approval: Covers 38 solid tumor indications in U.S.

- 🌍 EU approved: European Commission approved for all 33 adult indications

- 🇺🇸 Availability: U.S. launch late September 2025

- 💰 Revenue potential: Analysts expect 30-40% of Keytruda uses switching within 18-24 months

- 📜 Patent extension: Critical for extending Keytruda franchise beyond 2028 IV patent expiration

- 📊 Market reaction: Brief rally to $127 all-time high, then faded on realization 2028 cliff still looms

Verona Pharma Acquisition Completed - October 2024 ($10B Deal) 🏭

Merck completed $10 billion acquisition of Verona Pharma for Ohtuvayre (ensifentrine):

- 💊 Product: First-in-class COPD maintenance treatment, FDA approved June 2024

- 🚀 Launch performance: $71M in Q1 2025 sales - strongest COPD launch in history

- 🏥 Market opportunity: First new inhaled COPD treatment in 20+ years

- 💰 Valuation: $10B upfront - represents concentrated bet on single asset

- ⚠️ Risk: Limited commercial proof at time of acquisition, long payback period

Q1 2025 Earnings - April 24, 2025 (Mixed Results) 📉

Q1 2025 results showed Gardasil collapse accelerating while core business held up:

- 📊 Revenue: $15.5B down 2% YoY (up 1% excluding FX) - slight miss

- 💰 EPS: $2.22 non-GAAP vs estimates - in-line

- 🚀 Keytruda: $7.2B up 4% - growth decelerating from 18-21% range in 2024

- 💊 Winrevair: $280M (continuing strong PAH ramp)

- 💔 Gardasil disaster: $1.3B down 41% YoY - shipment halt to China through mid-2025

- ⚠️ China crisis: Anti-bribery crackdown + consumer spending pressure = zero visibility on recovery

🚀 Upcoming Catalysts (Next 6 Months - Within Calendar Spread Window)

Gardasil China Recovery Timeline - Q1/Q2 2026 (CRITICAL UNKNOWN) 🇨🇳

The elephant in the room - Merck halted Gardasil shipments to China from February 2025 through at least mid-2025:

- 💔 Impact: China represents 60-70% of all Gardasil sales outside the U.S.

- 📉 Performance: Q1 2025 sales collapsed 41% YoY ($1.3B from $2.2B)

- 🚨 Withdrawn target: Merck pulled $11B Gardasil 2030 sales goal - massive credibility hit

- 🔍 Root causes: Anti-bribery crackdown in Chinese healthcare, discretionary consumer spending collapse, vaccine market weakness

- ⏰ Recovery timeline: Management monitoring Q2-Q3 2025 demand signals - zero concrete guidance

- 🎯 Calendar spread implication: March-April window is EXACTLY when we might get clarity on China restart

Catalyst probability: If Merck announces China shipment resumption or demand recovery in Q1 2026 earnings (late April), the stock could rally 10-15% overnight. The April $110 long calls would explode in value. This is the PRIMARY upside catalyst for this trade structure.

Subcutaneous Keytruda Adoption Data - Q4 2025/Q1 2026 📊

Launched late September 2025, first real-world adoption data coming in Q1 2026:

- 🎯 Target: 30-40% of Keytruda volume switching to SC within 18-24 months

- 💉 Advantages: 1-minute administration vs 30-minute IV, improved patient experience, reduced chair time

- 💰 Revenue impact: If successful, extends Keytruda franchise life beyond 2028 IV patent expiration

- ⚠️ Adoption hurdles: Physician inertia, reimbursement complexity, infrastructure changes required

- 📈 Bull case: Early adoption exceeds 40% target, validates lifecycle extension strategy, reduces 2028 cliff fears

- 📉 Bear case: Adoption stuck at 10-15%, physicians stick with IV, subcutaneous fails to move needle

First concrete data point: Q4 2024 earnings call (February 2025) will provide initial prescription data. Q1 2025 earnings (April 2025) will show first full quarter of adoption - this is EXACTLY when the April long calls expire!

Winrevair Blockbuster Trajectory - Q1 2026 Earnings 🚀

Winrevair (sotatercept) for pulmonary arterial hypertension executing strongest PAH launch ever:

- 💰 Performance: $419M in FY2024 (including $200M in Q4), $280M in Q1 2025

- 📈 Trajectory: Citi forecasts $1.5B in 2025, $6.1B peak sales by 2030

- 💊 Pricing: $238,000 annual cost ($14,000 per vial every 3 weeks)

- 🏆 Competitive position: First-in-class activin signaling inhibitor, differentiated mechanism vs J&J products

- 🎯 Market size: ~40,000 PAH patients in U.S., $7.3B total market (J&J holds 50% share)

- 📊 Q1 2026 catalyst: If Winrevair hits $400-500M in Q4 2025 (reported late April 2026), validates $1.5B+ 2025 trajectory

Why this matters for the calendar spread: Winrevair beating expectations could be THE catalyst that pushes MRK through $110 resistance into April. Strong Q4 numbers reported in late April earnings = potential $110 call jackpot.

Q1 2026 Earnings - Late April/Early May 2026 (BINARY EVENT) 📅

Historical pattern shows Merck reports Q1 approximately 4-5 weeks after quarter-end (late April timeline):

What the Street will focus on:

- 📊 Revenue: Looking for return to growth after flat Q1 2025 ($15.5B)

- 🤖 Keytruda sustainability: Can growth reaccelerate above 10% despite patent cliff approaching?

- 🇨🇳 Gardasil China: ANY positive signal on shipment restart would be massive

- 💊 Winrevair ramp: Q4 2025 sales need to show $400M+ to stay on blockbuster trajectory

- 💉 Subcutaneous Keytruda: First full-quarter adoption data (% of total Keytruda volume)

- 🏭 Ohtuvayre uptake: Post-acquisition integration and continued launch momentum

- 💸 Cost cutting: Progress on $3B annual savings program through 2027 (6,000 job cuts)

Timing vs calendar spread: Q1 earnings fall EXACTLY in the April 17 expiration window! The long $110 April calls are positioned to capture earnings volatility, while the March $110 short calls expire BEFORE earnings, avoiding binary event risk on the short side. This is TEXTBOOK calendar spread positioning.

⚠️ Risk Catalysts (Negative - Could Destroy This Trade)

Keytruda Patent Cliff Accelerating - 2028 Timeline 💊

The $29.5B elephant in the room - Keytruda U.S. patent expiration in 2028:

- 📉 Revenue at risk: $29.5B represents 46% of total 2024 sales

- 🏭 Biosimilar competition: Celltrion, Samsung Bioepis, Amgen developing biosimilars for 2028+ launch

- 💰 Analyst projections: 30-60% sales erosion post-2028 from biosimilar competition

- 💊 Subcutaneous extension: May delay but not prevent erosion - IV and SC could both face biosimilars

- 📊 IRA pressure: Keytruda expected to enter IRA price negotiation 2026-2028, compounding revenue pressure

Timing: While 2028 is still 2+ years away, any negative news on subcutaneous adoption or biosimilar timeline acceleration in Q1 2026 could crater the stock.

Pipeline Execution Risk - $50B Revenue Replacement Needed 🎯

Merck touts 20 potential blockbuster drugs targeting $50B+ future revenue - but execution is FAR from guaranteed:

- 🔬 Clinical risk: Most assets in mid-stage development, years from commercialization

- 💊 Competition: TROP2 ADC space intensely competitive (vs Daiichi Sankyo/AstraZeneca)

- 🤖 Software gap: Lacks precision medicine ecosystem vs competitors

- ⏰ Time pressure: Need multiple $5B+ launches by 2028-2030 to offset Keytruda cliff

- 💰 M&A risk: Recent acquisitions (Verona $10B, EyeBio $3B) are HUGE bets on unproven assets

If pipeline disappoints in Q1 2026 earnings: Updates on key assets (patritumab deruxtecan, enlicitide decanoate, MK-2214 Alzheimer's, MK-8527 HIV PrEP) could move stock significantly either way.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts through April 2026, here are the scenarios for this calendar spread:

📈 Bull Case (30% probability)

Target: $110-$120 by April 17, 2026

How we get there:

- 🇨🇳 Gardasil China shipments resume Q1 2026 with strong demand recovery signals

- 💉 Subcutaneous Keytruda adoption exceeds 40% target in first 6 months, validating lifecycle extension

- 🚀 Winrevair Q4 2025 sales hit $450-500M, tracking toward $2B+ 2026

- 🏭 Ohtuvayre commercial uptake accelerates beyond $71M Q1 run rate

- 📊 Q1 2026 earnings beat with revenue growth returning (mid-single digits YoY)

- 💰 Cost-cutting program delivers ahead of schedule ($1B+ annual savings realized)

- 📈 Pipeline updates positive - key Phase 3 readouts meet endpoints

- 🎯 Break above $105 gamma resistance triggers short covering rally to $110-115

Calendar spread P&L in Bull Case:

- ✅ March $110 short calls expire worthless (stock still below $110 by March 20) = capture $5.5M premium

- 🚀 April $110 long calls worth $5-10 if stock at $115-120 post-earnings = $7.5-15M value

- 💰 Total P&L: $5.5M kept from short calls + $7.5-15M long call value - $7.2M cost = $5.8M to $13.3M profit (30-70% ROI)

What kills this scenario:

- China recovery fails to materialize or government crackdown intensifies

- Subcutaneous Keytruda adoption disappoints (stuck at 15-20%)

- Negative pipeline news or clinical trial failures

🎯 Base Case (50% probability)

Target: $95-$105 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ⚖️ Gardasil China remains question mark - shipments resume but demand tepid

- 📊 Subcutaneous Keytruda adoption steady but unspectacular (25-30% by mid-2026)

- 💊 Winrevair continues solid trajectory ($350-400M Q4) but no major surprises

- 📉 Q1 2026 earnings in-line, guidance conservative citing macro uncertainty

- 🔄 Stock trades within $95-105 gamma support/resistance bands for months

- 💤 Market in "wait and see" mode for 2028 Keytruda cliff clarity

- 🎪 Pipeline updates neutral - no major wins or disasters

Calendar spread P&L in Base Case:

- ⚖️ March $110 short calls expire worthless (stock at $100-105) = keep $5.5M premium

- 📊 April $110 long calls worth minimal ($1-3) if stock still $100-105 post-earnings = $1.5-4.5M residual

- 💰 Total P&L: $5.5M kept + $1.5-4.5M long value - $7.2M cost = Small loss to small profit: -$200K to +$2.8M (-1% to +15% ROI)

This is the "theta decay" scenario - trader collects premium from short March calls, April longs don't work out but minimize loss. The $120 reverse calendar component provides some hedge value if stock spikes unexpectedly.

Why 50% probability: Stock at technical no-man's land - fundamentals mixed (Keytruda strong, Gardasil weak, pipeline uncertain). Most institutional players holding and waiting for catalysts to clarify direction.

📉 Bear Case (20% probability)

Target: $85-$95 (BREAK SUPPORT, TEST DISASTER FLOOR)

What could go wrong:

- 😰 Gardasil China permanently impaired - government bans commercial promotion or applies export restrictions

- 💔 Subcutaneous Keytruda adoption fails (only 10-15%) - physicians refuse to change, patent extension strategy collapses

- 📉 Winrevair uptake slows materially (competitive pressure from J&J, safety concerns)

- 🚨 Pipeline setback - major Phase 3 trial failure announced (MK-2214 Alzheimer's, enlicitide decanoate CV trial)

- 💰 Q1 2026 earnings miss badly on revenue and margins

- 🇨🇳 Broader China exposure reduced due to geopolitical tensions

- 📊 New biosimilar data shows earlier-than-expected Keytruda competition (2027 instead of 2028)

- 🔨 Break below $95 gamma support triggers cascade to $90, then $85

Calendar spread P&L in Bear Case:

- ✅ March $110 short calls expire worthless (stock crashed to $85-95) = keep $5.5M premium

- 💀 April $110 long calls also worthless if stock at $85-95 = $0 value

- 📉 March $120 long calls worthless = lose $945K

- 💰 April $120 short calls expire worthless = keep $1.2M premium

- 💰 Total P&L: $5.5M kept + $1.2M kept - $7.2M cost - $945K March longs = -$1.445M loss (-8% ROI on $14.5M notional)

Probability assessment: Only 20% because it requires multiple negative catalysts aligning. Merck's core business remains solid (Keytruda still growing, Winrevair launching successfully), and $247B market cap provides some downside cushion. The gamma floor at $95 (22.81B) should provide technical support. However, the trader clearly structured with defined risk in mind - maximum loss scenario is contained.

💡 Trading Ideas

🛡️ Conservative: Wait for $95 Support Test, Then Buy Stock

Play: Stay in cash until stock tests major gamma support at $95, then accumulate shares for long-term hold

Why this works:

- 📊 Gamma data shows MASSIVE 22.81B support at $95 - if we get there, high probability bounce

- 💰 At $95, you're buying Merck at 13.5% discount from current $99, 25% discount from 52-week high $127

- 🏥 Core business fundamentals solid - Keytruda still growing 4-10% annually through 2028

- 💊 Pipeline has legitimate $50B+ revenue potential through 20+ blockbuster candidates

- 🚀 Winrevair executing strongest PAH launch in history - $1.5B+ 2025, $6B peak

- 🎯 Dividend yield ~3.2% at $95 provides income cushion while waiting for catalysts

- ⏰ 2028 Keytruda cliff still 2+ years away - plenty of time for subcutaneous adoption and pipeline execution

Action plan:

- 👀 Set price alert at $96 - if we break below, prepare to buy $95-96 range

- 💰 Allocate 3-5% of portfolio to MRK at $95 as "value" position

- ⏰ Plan to hold 12-24 months through Q1 2026 earnings, subcutaneous Keytruda adoption data, Gardasil China recovery

- 🎯 Target price $115-120 (15-20% upside) over 18-24 months as transformation story clarifies

- 🛡️ Stop loss at $88 (below $90 disaster support) to limit downside to 7-8%

Risk level: Low-Moderate (stock position, not options) | Skill level: Beginner-friendly

Expected outcome: Capture mean reversion bounce from oversold levels, collect 3%+ dividend, participate in 2026 catalysts without options complexity.

⚖️ Balanced: Copy the Pro Trade (Scaled-Down Calendar Spread)

Play: Replicate the institutional calendar spread structure at retail-appropriate size

Structure:

- Buy 5 April 2026 $110 calls @ ~$2.40 = $1,200 debit

- Sell 5 March 2026 $110 calls @ ~$1.83 = $915 credit

- Net debit: ~$285 per spread × 5 = $1,425 total risk

Why this works:

- 🤝 Literally copying the $14.5M institutional trade structure - if smart money likes it, there's logic

- 📅 Time decay arbitrage - March short calls decay faster than April long calls

- 🎯 Positioned for potential Q1 2026 earnings surprise (late April) after March expiration

- 🇨🇳 Captures Gardasil China recovery catalyst window (Q1 2026 clarity expected)

- 💉 Gets subcutaneous Keytruda adoption data through Q4/Q1 reporting

- 📊 Defined risk - can't lose more than $1,425 no matter what happens

- 🚀 If MRK consolidates $95-105 through March then rallies to $110-115 post-earnings = home run

Estimated P&L:

- 🎯 Max profit: If stock at $110 at March expiration, short calls expire worthless ($915 kept), then stock rallies to $115-120 by April = April longs worth $5-10 = $3,000-6,000 profit (210-420% ROI)

- ⚖️ Breakeven: Stock at $100-105 at March expiration, stays there through April = lose most of spread cost = -$800 to -$1,200 loss (-56% to -84%)

- 💀 Max loss: Stock crashes below $95 or explodes above $115 before March = -$1,425 (100% loss)

Entry timing:

- ⏰ Enter this week (early December) to match institutional timing

- 🎯 Only enter if stock between $97-102 (needs room to work within gamma bands)

- ❌ Skip if stock already above $108 (too close to strikes) or below $93 (support broken)

Management plan:

- 📅 At March 20 expiration: If short calls worthless, hold April longs for earnings

- 🚀 If stock approaching $110 in March: Consider rolling short calls to April $115 to extend position

- 📉 If stock below $100 at March expiration and trending down: Cut position, accept loss

Position sizing: Risk only 1-3% of options portfolio (this is speculative, not core holding)

Risk level: Moderate (defined risk, requires timing precision) | Skill level: Intermediate

🚀 Aggressive: Earnings Volatility Straddle (ADVANCED ONLY!)

Play: Bet on massive Q1 2026 earnings volatility exceeding implied move

Structure: Buy straddle using May 2026 expiration (post-earnings)

- Buy May $100 calls @ ~$5.00

- Buy May $100 puts @ ~$6.00

- Total cost: ~$11.00 per straddle = $1,100 per straddle

Why this could work:

- 💥 Q1 2026 earnings (late April) is BINARY EVENT - Gardasil China, subcutaneous Keytruda, Winrevair trajectory all come together

- 🎰 Implied move only 3% monthly but MRK has history of 8-12% post-earnings moves on surprises

- 📊 Betting the Street is UNDERPRICING catalyst risk - China recovery OR pipeline failure could gap stock 15%+ overnight

- 🇨🇳 Gardasil wildcard - zero consensus on China timeline, surprise either way moves stock violently

- 💉 Subcutaneous adoption data - if 40%+ target hit or if only 15%, both extreme outcomes = big move

- ⚡ Need stock to move to $115+ or $85- to profit (15% either direction)

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Straddle costs $11 ($1,100) on $99 stock = 11% of stock price!

- ⏰ TIME DECAY MONSTER: Theta burns -$30-40/day as earnings approaches

- 😱 IV CRUSH: Even if stock moves 10%, implied volatility collapse could still cause LOSS

- 📊 Range-bound risk: Stock stays $95-105 and you lose 60-80% of premium

- ⚠️ Earnings could be "in-line" - stock gaps to $103-105 (only 5% move) and straddle loses 40%

- 🎢 Need 12-15%+ move just to breakeven after IV crush factored in

Estimated P&L:

- 💰 Cost: ~$11 per straddle (using May 15, 2026 expiration to capture earnings + IV expansion)

- 📈 Profit scenario: Stock moves to $115 or $85 (15% move) = $15 gain (136% ROI)

- 🚀 Home run: Stock moves to $125 or $75 (25% move) = $25+ gain (227% ROI)

- 📉 Loss scenario: Stock ends $95-105 range = lose $7-9 (64-82% loss)

- 💀 Total loss: Stock flat at $100 = lose entire $11 (100% loss)

Breakeven points:

- 📈 Upside breakeven: ~$111-112 (12% rally needed)

- 📉 Downside breakeven: ~$88-89 (11% drop needed)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded straddles through pharma earnings before and understand IV crush

- ✅ Can afford to lose ENTIRE premium (real possibility!)

- ✅ Understand you're betting AGAINST the options market's pricing

- ✅ Can monitor position morning after earnings and take profits quickly

- ✅ Accept that even if you're RIGHT on direction, theta + IV crush could cause loss

- ⏰ Plan to close position within 24-48 hours post-earnings (don't hold to expiration)

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~35% (lower than implied 50% due to IV crush dynamics in low-vol pharma names)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💊 Keytruda patent cliff approaching fast: U.S. patent expiration in 2028 represents $29.5B revenue (46% of 2024 sales) at risk. Biosimilar competition from Celltrion, Samsung Bioepis, Amgen in late-stage development. Analysts project 30-60% sales erosion post-2028. Subcutaneous formulation may delay but not prevent - IV and SC could both face biosimilars simultaneously. IRA price negotiations starting 2026-2028 compound pressure. This is the EXISTENTIAL risk - execution on pipeline must be flawless.

-

🇨🇳 Gardasil China permanently impaired: Q1 2025 sales collapsed 41% YoY to $1.3B after shipment halt through mid-2025. China represents 60-70% of non-U.S. Gardasil revenue. Merck withdrew $11B 2030 sales target - massive credibility hit. Root causes (anti-bribery crackdown, consumer spending weakness) show zero recovery signs. If China market permanently damaged, that's $3-5B annual revenue opportunity gone forever. Calendar spread positioned EXACTLY in Q1 2026 window when clarity emerges - could go either way violently.

-

📉 Subcutaneous Keytruda adoption may disappoint: FDA approval September 2025 for 1-minute SC administration vs 30-minute IV. Analysts expect 30-40% switching within 18-24 months. BUT physician adoption requires infrastructure changes, reimbursement clarity, staff training. Historical precedent shows healthcare providers SLOW to change established protocols. If adoption stuck at 10-15% by mid-2026, entire patent extension thesis collapses. First real data at Q1 2026 earnings (April) = binary catalyst within calendar spread window.

-

💰 Pipeline execution risk - $50B replacement needed: Merck claims 20 potential blockbusters targeting $50B+ revenue to offset Keytruda cliff. Most assets in mid-stage development, years from commercialization. Competition intense in TROP2 ADC space (vs Daiichi Sankyo/AstraZeneca datopotamab deruxtecan). Software ecosystem gap vs competitors limits precision medicine capabilities. Need multiple $5B+ launches by 2028-2030 - historically pharma success rate is 10-20%. Recent M&A (Verona $10B, EyeBio $3B) are concentrated bets on unproven single assets. One major Phase 3 failure in Q1 2026 window (MK-2214 Alzheimer's, enlicitide decanoate CV, MK-8527 HIV PrEP) could crater stock.

-

🎢 Low implied volatility underprices binary risk: Current implied move only 3% monthly suggests market expects calm, but upcoming catalysts are HIGH MAGNITUDE. Gardasil China recovery vs permanent impairment = $3-5B revenue swing. Subcutaneous Keytruda 40% adoption vs 10% = entirely different 2028 outlook. Winrevair trajectory could validate $6B peak or stall at $2B. These are BINARY outcomes compressed into Q1 2026 reporting. Calendar spread positioned for volatility expansion into April earnings - but if volatility DOESN'T expand, time decay kills the trade.

-

💸 Valuation offers limited margin of safety: At 17.2x forward P/E (vs historical 12-15x), MRK trades at premium despite execution risks. Market pricing in successful Keytruda lifecycle extension + pipeline delivery + Gardasil recovery. Any disappointment on these fronts and multiple contracts back to 12-14x = $85-95 stock price. Already down 22% from $127 high - further downside to $85 gamma floor possible if Bear Case catalysts align.

-

📊 Institutional distribution continues: BlackRock cut 3.1%, Wellington reduced 5.9% in Q3 2024, State Street trimmed 1.7%. Insider trading weighted toward selling throughout 2024 - absence of meaningful buying suggests management not confident at current levels. Large holders reducing exposure during 2024 rally from $105 to $127, now continuing to trim in $95-105 range. If institutional selling accelerates, retail can't provide support.

-

🏥 Winrevair commercial risk despite strong launch: While executing strongest PAH launch in history ($419M FY2024), J&J controls 50% of $7.3B PAH market with entrenched relationships. Long-term efficacy and safety data still accumulating - any adverse events could halt momentum. Pricing at $238,000 annual cost creates reimbursement hurdles. If Q4 2025 sales (reported April 2026) disappoint vs $400M+ expectations, validates Bear Case on pipeline execution.

-

📅 Calendar spread timing precision required: This is NOT a "set and forget" trade. Need to actively manage March 20 expiration - if stock approaching $110, may need to roll short calls to avoid assignment. If stock crashes below $95, April longs become worthless and you're just bleeding time decay. Requires monitoring gamma levels, IV changes, upcoming catalyst timing. Miss the management window and the trade structure breaks down.

-

🌍 Geopolitical tail risks: China exposure extends beyond Gardasil - any Taiwan conflict affects TSMC manufacturing, U.S. export restrictions could hit additional products, broader healthcare sector tensions. Merck already took $800M hit from MI308 export restrictions to China in Q2 2025 (later lifted). Future controls unpredictable.

-

💊 IRA price negotiations create overhang: Keytruda expected to enter Medicare price negotiation process 2026-2028, overlapping with patent expiration. Potential significant Medicare price reductions compound biosimilar erosion. Creates uncertainty for financial modeling through 2028-2030 period.

🎯 The Bottom Line

Real talk: Someone just deployed $14.5 MILLION in a sophisticated calendar spread structure on Merck - this isn't a directional bet on the stock exploding higher. This is a PROFESSIONAL time-decay and volatility arbitrage trade positioned EXACTLY for the Q1 2026 catalyst window when multiple binary events converge: Gardasil China recovery timeline, subcutaneous Keytruda adoption data, Winrevair blockbuster trajectory, and pipeline updates all hit in late April earnings.

What this trade tells us:

- 📅 Smart money expects MRK to trade RANGEBOUND ($95-$105) through March, allowing short $110 calls to expire worthless

- 🎯 But they want EXPOSURE to potential breakout toward $110-$120 into April if Q1 earnings surprise positively

- 🇨🇳 The March-to-April timing captures the EXACT window when Gardasil China clarity should emerge (Q2 2026 guidance in late April earnings)

- 💉 First full-quarter subcutaneous Keytruda adoption data (Q4 2025 reported in Feb, Q1 2026 in April) falls perfectly within structure

- 🚀 Winrevair Q4 trajectory ($400M+ validates $1.5B 2025, $6B peak thesis) reported late April

- ⚖️ The $120 reverse calendar component provides upside hedge if stock unexpectedly explodes before March

This is NOT a "Merck is going to the moon" signal - it's a "we're going to systematically harvest time decay while maintaining optionality for April catalysts" signal.

If you own MRK:

- ✅ Core pharma holding for dividend income (3.2% yield) and long-term transformation story remains valid

- 📊 $95 gamma support (22.81B) is YOUR line in the sand - if breaks, consider trimming 25-40% of position

- 🎯 Set ALERTS at $110 resistance and $95 support - these are the gamma battlegrounds

- ⏰ Key dates to watch: Q4 2024 earnings (Feb 2025 - already reported poorly), Q1 2026 earnings (late April - THE CATALYST)

- 🛡️ If holding large position, consider buying 1-2 protective $95 puts per 100 shares (copy institutional hedging mentality)

If you're watching from sidelines:

- ⏰ Best entry: Wait for test of $95 support (22.81B gamma floor) - that's 4% downside from current $99

- 🎯 At $95, you get 3.4% dividend yield + 25% discount from 52-week high + gamma support

- 📈 Long-term thesis intact: Keytruda growth through 2028, Winrevair ramping to $6B, pipeline delivering $50B revenue replacement

- 🚀 6-12 month catalysts legitimate: Subcutaneous Keytruda adoption, Gardasil China recovery, Ohtuvayre traction, pipeline readouts

- ⚠️ Current $99 level offers NO margin of safety - wait for pullback or jump in post-positive catalyst

If you're considering the calendar spread:

- 🎯 This is an INTERMEDIATE to ADVANCED trade requiring precise timing and active management

- 📅 Entry timing critical: Need stock between $97-102 to have room for structure to work

- ⏰ March 20 expiration requires decision point - roll, close, or hold through to April

- 💰 Position sizing: Risk only 1-3% of options portfolio - this is speculative income generation, not core holding

- ⚠️ If you don't understand calendar spreads, skip this - stick with stock accumulation at $95 support instead

Mark your calendar - Key dates:

- 📅 February 2025 (already passed) - Q4 2024 earnings (disappointed badly, triggered 8% drop)

- 📅 March 20, 2026 - Monthly OPEX, expiration of short calendar spread legs

- 📅 April 17, 2026 - Monthly OPEX, expiration of long calendar spread legs

- 📅 Late April/Early May 2026 - Q1 2026 earnings (BINARY CATALYST - Gardasil China, SC Keytruda adoption, Winrevair trajectory, pipeline updates)

- 📅 Mid-2026 - Gardasil China shipment resumption expected (if recovery materializes)

- 📅 2028 - Keytruda U.S. patent expiration (the cliff everyone's watching)

Final verdict: Merck's transformation story remains INCREDIBLY compelling - subcutaneous Keytruda lifecycle extension, Winrevair blockbuster launch, $10B Ohtuvayre acquisition, $50B pipeline potential, and potential Gardasil China recovery are all real. BUT at $99 after 22% decline from highs with binary catalysts 4-5 months away, the risk/reward favors PATIENCE.

The $14.5M calendar spread is a CLEAR signal: smart money expects consolidation near-term, wants optionality for April catalysts, and is harvesting time decay while waiting. Copy the structure at retail scale if you understand the mechanics, or simply wait for $95 support test to accumulate stock for the long-term transformation thesis.

Be patient. Let March expiration pass. Look for April earnings clarity. The pharmaceutical innovation cycle moves in years, not weeks - you won't miss the boat by waiting for better entry points. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The extreme Z-scores (299.83, 473.2) reflect this specific trade's size relative to recent MRK history - it does not imply the trade will be profitable or that you should follow it. Calendar spreads require active management and precise timing - inappropriate for beginners. Always do your own research and consider consulting a licensed financial advisor before trading. The pharmaceutical industry faces regulatory, clinical trial, and competitive risks that can cause sudden large price movements. Merck's Keytruda patent cliff in 2028 represents existential business model risk.

About Merck & Co., Inc.: Merck operates across multiple therapeutic areas including cardiometabolic disease, cancer, and infectious diseases. The company's immuno-oncology division, anchored by its Keytruda product, represents a significant revenue driver. Additionally, Merck maintains substantial vaccine operations, including Gardasil for human papillomavirus prevention. With a market cap of $247.5 billion in the Pharmaceutical Preparations industry, Merck employs 75,000 people globally and is headquartered in Rahway, NJ.