💊 MRK Deep ITM $40 Strike Call - This is a $4.7M Covered Call on Merck Stock!

📅 December 15, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just sold $4.7 MILLION worth of deep in-the-money calls on Merck this morning! This massive trade sold 772 contracts at the $40 strike expiring December 19 - that's a DEEP ITM call with intrinsic value of $60.30 per contract. With MRK trading at $100.16, this is almost certainly a covered call position or assignment acceptance scenario, not a speculative bet. Translation: An institutional holder of 77,200 shares is either generating massive income or preparing for assignment at $100 (essentially capping upside for the week).

📊 Company Overview

Merck & Co., Inc. (NYSE: MRK) is a global pharmaceutical powerhouse delivering innovative health solutions across multiple therapeutic areas:

- Market Cap: $248.9 Billion (6th largest pharma globally)

- Industry: Pharmaceutical Preparations

- Current Price: $100.16 (near 52-week high of $105.84)

- Primary Business: Prescription medicines for cancer (Keytruda), vaccines (Gardasil), animal health products, cardiometabolic treatments

- Dividend: 3.3% yield ($0.85/quarter, ex-date December 15, 2025)

What they do: Merck develops and markets pharmaceutical products to treat cardiometabolic disease, cancer, and infections. Their flagship drug Keytruda generated $29.5B in 2024 - making it the world's best-selling medication.

💰 The Option Flow Breakdown

The Tape (December 15, 2025 @ 10:46:20):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:46:20 | MRK | BID | SELL | CALL $40 | 2025-12-19 | $4.7M | $40 | 772 | 0 | 772 | $100.16 | $60.30 |

🤓 What This Actually Means

This is a covered call income generation strategy or assignment acceptance - NOT a bearish bet! Here's what's really happening:

- 💸 Premium collected: $4.7M ($60.30 per contract × 772 contracts)

- 🎯 Deep ITM strike: $40 is $60.16 BELOW current stock price (60% in-the-money!)

- 📊 Position structure: Represents 77,200 shares of MRK stock (worth ~$7.7M at current price)

- ⏰ 4 days to expiration: December 19 weekly OPEX - assignment is virtually guaranteed

- 🏦 Institutional income: This trader holds the underlying stock and is capping upside at $100 to collect premium

Why sell a $40 strike call when stock is at $100?

This seems bizarre at first, but makes perfect sense for institutional positioning:

-

Covered Call Structure: The seller owns 77,200 shares of MRK purchased around $40-45 (likely years ago). They're writing covered calls to generate income while willing to let stock get called away at $100.

-

Assignment Expected: With MRK at $100.16 and the $40 call worth $60.30, there's literally ZERO extrinsic value. The option will be exercised early or at expiration with 100% certainty.

-

Effective Exit Price: If assigned, the seller gets $40 (strike) + $60.30 (premium collected) = $100.30 effective sale price on stock likely bought years ago around $40-50. That's a 100-150% gain plus dividend income over the holding period!

-

Tax/Portfolio Reasons: Large institutions often use deep ITM covered calls to:

- Lock in exit price at specific levels

- Generate income while accepting assignment

- Manage tax timing (assignment in 2025 vs 2026)

- Rebalance portfolio at predetermined price points

What makes this unusual:

- 🔥 Z-Score of 1,779.97 means this is EXTREMELY unusual - this specific structure (deep ITM, large size, short DTE) rarely happens

- 📊 Zero open interest before this trade - fresh positioning, not closing existing

- 💰 $4.7M premium is massive for a 4-day covered call - trader values certainty over additional upside

- 🎯 Classification: STANDALONE Short Call - appears to be isolated covered call, not part of spread

This is NOT bearish on MRK's prospects. It's a sophisticated exit/income strategy by a holder who bought years ago and is content to sell at $100.

📈 Technical Setup / Chart Check-Up

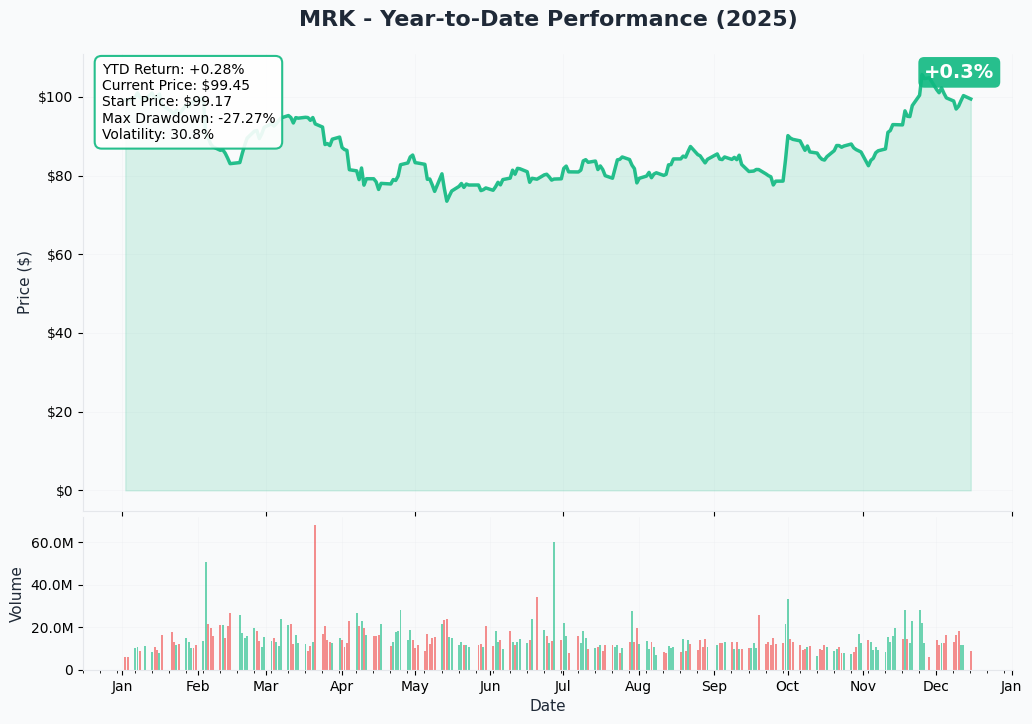

YTD Performance Chart

Merck has delivered solid performance this year - currently trading at $100.16 with a 52-week range of $73.31 - $105.84. The chart shows a strong uptrend from the July lows around $90, rallying to test the $105 all-time highs in November before consolidating in the $98-102 range.

Key observations:

- 📈 Strong recovery: Up from $90 support in July to current levels near $100

- 🎯 Consolidation pattern: Trading in tight $98-102 range post-November highs

- 💊 Dividend support: Ex-date December 15 (today!) provides natural support

- 📊 Relative stability: Low volatility stock (13.10x P/E) compared to growth names

- ✅ Near resistance: $105 represents key overhead resistance from November highs

The covered call seller is essentially saying "I'm happy to exit at $100 and capture my gains from earlier entry prices around $40-50."

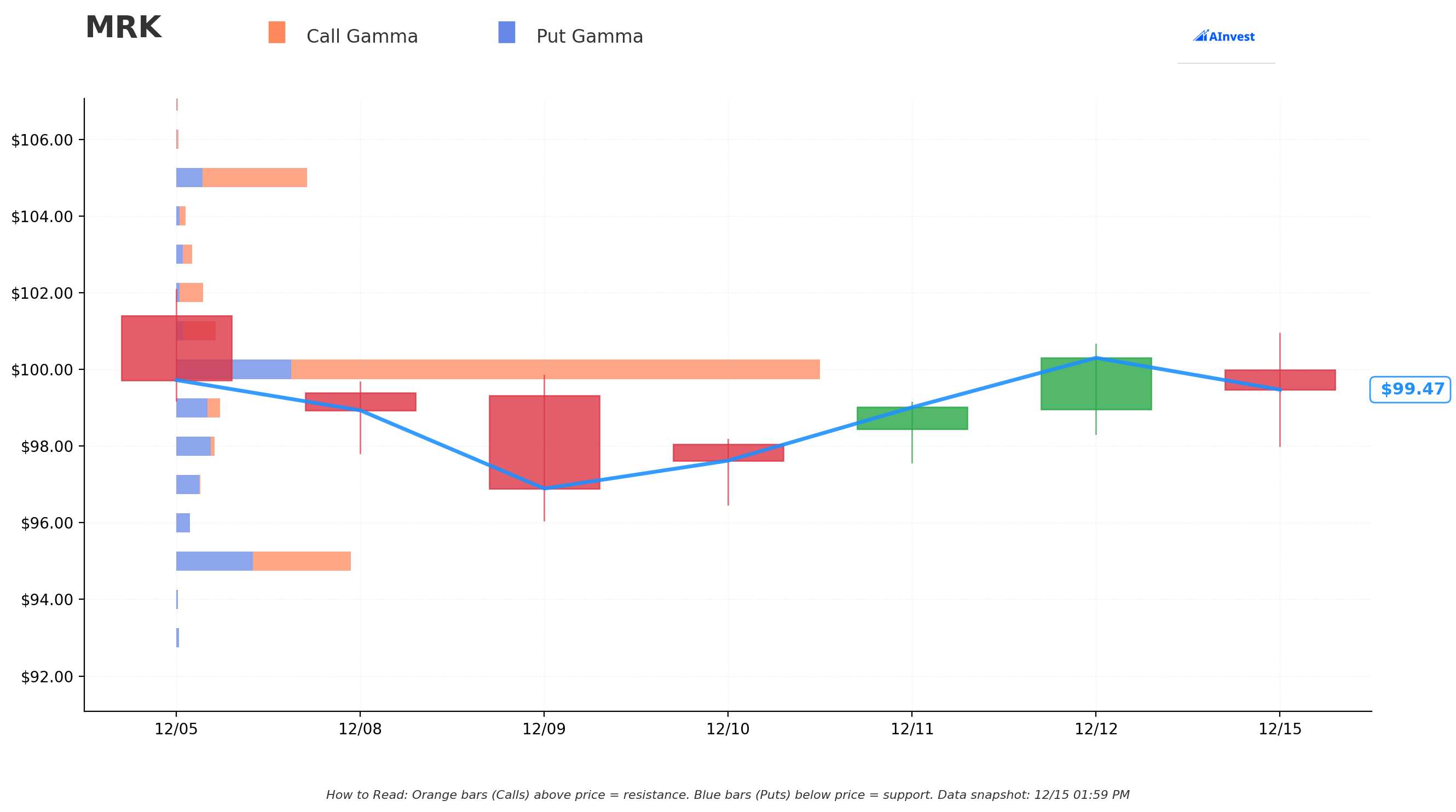

Gamma-Based Support & Resistance Analysis

Current Price: $99.49

The gamma exposure map shows critical price levels where options activity creates natural support and resistance:

🔵 Support Levels (Put Gamma Below Price):

- $99 - Immediate support with 4.8B total gamma (just 0.5% below current price)

- $98 - Secondary support at 4.2B gamma (1.5% cushion)

- $95 - Major structural floor with 19.4B gamma (HIGHEST PUT GAMMA - dealers defend this level!)

- $90 - Deep support at 7.9B gamma (9.5% below)

- $85 - Extended floor at 3.0B gamma

- $80 - Disaster scenario support at 3.1B gamma (19.6% drawdown)

🟠 Resistance Levels (Call Gamma Above Price):

- $100 - MASSIVE WALL with 72.0B gamma (STRONGEST SINGLE LEVEL - exactly where this trade is struck!)

- $101 - Secondary resistance at 4.4B gamma (1.5% overhead)

- $105 - Major ceiling at 14.7B gamma (5.5% rally needed)

- $110 - Extended upside target at 14.9B gamma (10.6% move required)

What this means for traders:

The gamma data tells a CRYSTAL CLEAR story: MRK is pinned just below the absolutely MASSIVE $100 resistance level with 72.0B gamma (by far the largest level on the entire chain!). This creates enormous mechanical resistance as market makers hedge their positions.

Notice anything? The covered call seller struck EXACTLY at $100 where there's 72.0B gamma - the single most important price level. This isn't coincidental. They know that:

- MRK faces massive resistance at $100 from options positioning

- Stock unlikely to break through and stay above $100 in next 4 days

- Perfect strike to ensure assignment while maximizing their exit price

The $95 level with 19.4B put gamma is THE critical support - this is where institutions have placed their downside bets. The stock has natural buying pressure at that level.

Net GEX Bias: Bullish (121.9B call gamma vs 51.6B put gamma) - Overall positioning leans bullish, but immediate price action constrained by the $100 gamma wall.

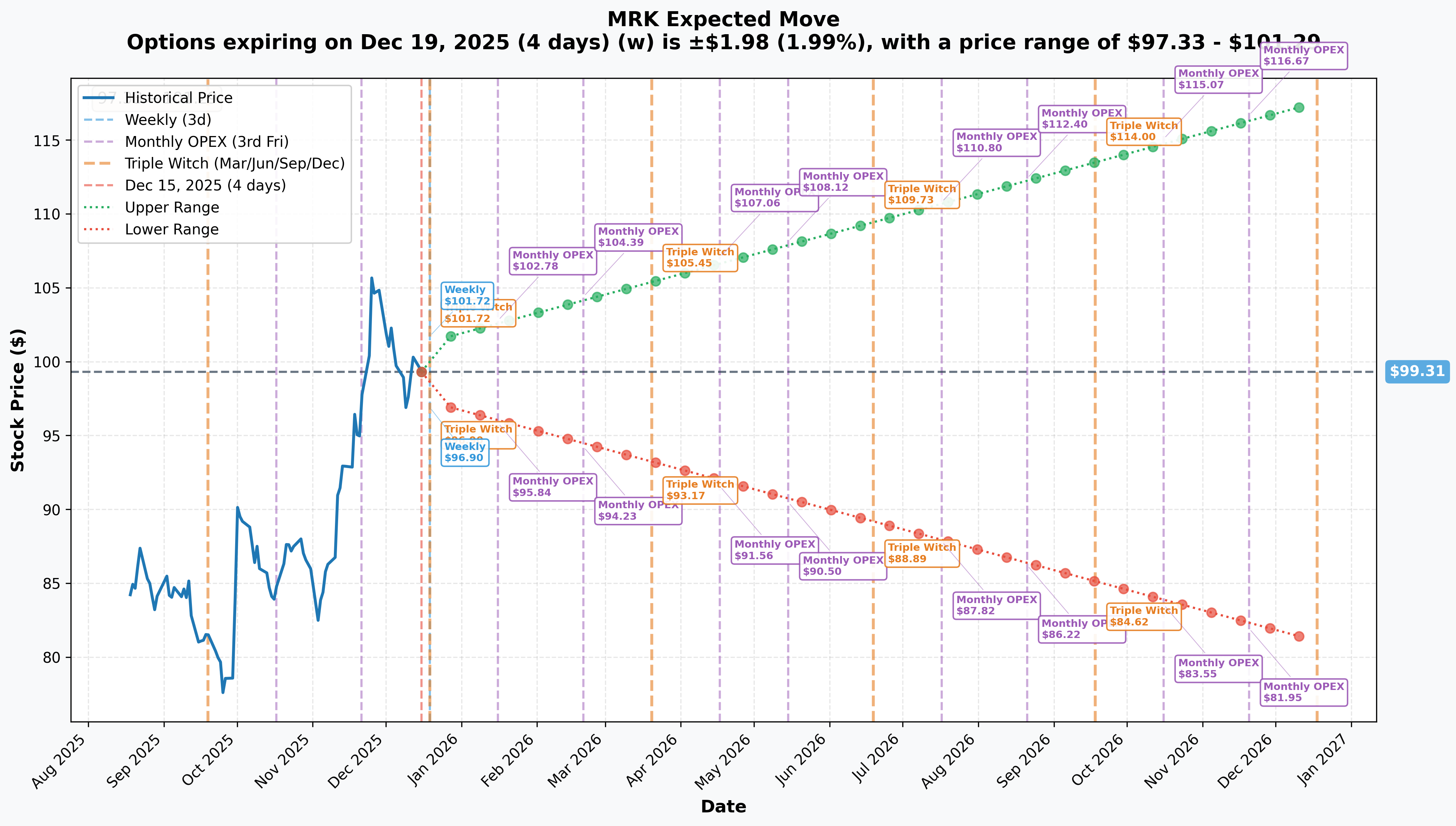

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 4 days): ±$1.98 (±1.99%) → Range: $97.33 - $101.29

- 📅 Quarterly Triple Witch (Dec 19 - 4 days): ±$2.05 (±2.07%) → Range: $97.26 - $101.36

- 📅 Monthly OPEX (Jan 16 - 32 days): ±$4.34 (±4.37%) → Range: $94.97 - $103.65

- 📅 Yearly LEAPS (Dec 18, 2026 - 368 days): ±$18.25 (±18.38%) → Range: $81.06 - $117.56

Translation for regular folks:

Options traders are pricing in a TINY 2% move ($2) through Friday's weekly expiration - this is extremely low volatility for a $249B mega-cap pharma stock. The market expects MRK to trade in a tight $97-$101 range through December 19th OPEX.

This aligns PERFECTLY with the covered call trade: The $40 strike call seller knows MRK has only 2% implied volatility through Friday. Even if stock dips to $97.33 (lower implied range), the $40 calls are still massively ITM and will be assigned. The trade is essentially a LOCK to execute.

The one-year LEAPS implied range of $81-$117 (±18%) shows long-term uncertainty around Keytruda's 2028 patent cliff and pipeline execution, but near-term action should remain range-bound.

Key insight: Low implied volatility (2% weekly) combined with massive $100 gamma resistance creates perfect conditions for covered call strategies at this strike. The seller has extremely high confidence of assignment.

🎪 Catalysts

🔔 Already Happened (Past Catalysts)

Dividend Ex-Date - December 15, 2025 (TODAY!) 💰

Merck announced a cash dividend of $0.85 with ex-date of December 15, 2025 (today). This provides natural support around current levels as dividend-focused investors accumulate before the ex-date. The 3.3% dividend yield remains attractive for income investors.

Q4 2024 & Full Year Results - February 4, 2025 📊

Merck reported strong Q4 2024 results that exceeded analyst expectations:

- Q4 Revenue: $15.62B (+7% YoY vs. $15.49B expected)

- Q4 Adjusted EPS: $1.72 (vs. $1.62 expected)

- Full Year 2024 Revenue: $64.2B (+7% YoY)

- Keytruda Sales: $29.5B (world's best-selling drug, ~46% of total revenue)

- Winrevair: $419M in first full year (strong launch)

- Gross Margin: ~82%

The strong Q4 performance validated Merck's diversification strategy beyond Keytruda, with successful launches of Winrevair and Capvaxive offsetting Gardasil China headwinds.

Subcutaneous Keytruda Phase 3 Success - November 19, 2024 ✅

Merck announced positive topline results from the pivotal Phase 3 trial evaluating subcutaneous pembrolizumab:

- ✅ Primary Endpoints Met: Demonstrated noninferior pharmacokinetics vs. IV Keytruda

- ⏰ Administration Time: 2-3 minutes vs. 30-minute IV infusion

- 💉 Patient Experience: Major improvement in convenience and access

- 📋 FDA Status: Accepted filing with decision expected September 23, 2025

This could extend Keytruda's commercial life by improving patient experience and creating differentiation from biosimilars post-2028 patent expiration.

Cidara Therapeutics Acquisition - November 14, 2024 🏢

Merck announced a definitive agreement to acquire Cidara for $221.50 per share, total value approximately $9.2 billion:

- 🎯 Target Asset: CD388, Phase 3 long-acting influenza prevention antiviral

- 💊 Mechanism: Small molecule neuraminidase inhibitor - potential first-in-class

- 📊 Phase 2b Results: 76% protection against seasonal influenza

- 🗓️ Expected Close: Q1 2026

- 💰 Strategic Rationale: Diversifies portfolio beyond oncology into infectious disease

This represents Merck's largest recent acquisition focused on portfolio diversification ahead of the Keytruda 2028 patent cliff.

HIV Treatment Phase 3 Success - December 19, 2024 🧬

Merck announced topline results from two pivotal Phase 3 trials of doravirine/islatravir (DOR/ISL):

- 📋 Trial 051: 551 participants through Week 48

- 📋 Trial 052: 513 participants through Week 144

- ✅ Results: Both trials met efficacy success criteria for non-inferiority

- 💊 Advantage: Simplified two-drug regimen vs. standard three-drug therapies

Represents potential next-generation HIV treatment with improved convenience.

🚀 Upcoming Catalysts (Next 6 Months)

Subcutaneous Keytruda FDA Decision - September 23, 2025 📋

PDUFA Date: September 23, 2025 (9 months away)

FDA accepted filing for subcutaneous Keytruda with decision expected September 2025. High probability of approval based on successful Phase 3 data meeting all primary endpoints.

Revenue Impact:

- 💰 Potential to extend Keytruda franchise life beyond 2028 patent expiration

- 🎯 Could differentiate from biosimilars through superior patient experience

- 📈 Estimated incremental peak sales: $2-3B annually if successfully positions vs. IV biosimilars

This is a CRITICAL catalyst for extending Keytruda's dominance and could add years of commercial exclusivity through formulation differentiation.

Q1 2025 Earnings Report - Late April/Early May 2025 📊

Expected Timing: Late April or early May 2025

Key Metrics to Watch:

- 📈 Keytruda quarterly growth trajectory (need to sustain 15-20% growth)

- 💊 Gardasil recovery signs post-China shipment pause

- 🚀 Winrevair and Capvaxive uptake acceleration (critical for diversification thesis)

- 🎯 2025 guidance confirmation or revision

- 🔬 Pipeline updates from ongoing trials

Guidance Context: Full-year 2025 revenue guidance of $64.5-65.0B (+1-2% growth) and EPS of $8.93-$8.98 sets conservative baseline. Any upside surprise could drive stock to $105-110.

Keytruda Label Expansion Decisions - H1 2025 🎯

Head and Neck Cancer Perioperative Treatment:

- 📋 Status: FDA granted Priority Review

- 🗓️ Expected Decision: H1 2025 (next 6 months)

- 💰 Market Impact: Expands addressable patient population; estimated $500M+ incremental peak sales

Multiple ongoing Phase 3 trials across 10+ tumor types provide continuous label expansion opportunities to maximize Keytruda's pre-patent expiration revenue.

Cidara Acquisition Close - Q1 2026 🏢

Expected Timeline: First quarter 2026 (12-15 months away)

- 🎯 Integration Focus: CD388 Phase 3 trial completion and potential FDA filing

- 💊 Commercial Launch: Potentially 2026-2027 if Phase 3 successful

- 💰 Revenue Contribution: Could add $2-5B in peak annual sales if CD388 achieves blockbuster status in influenza prevention market

⚠️ Risk Catalysts (Negative)

Keytruda Patent Cliff - 2028 ⏰

The elephant in the room: Keytruda's patent expiration in 2028 represents Merck's biggest long-term risk:

- 💰 Revenue Concentration: 45-46% of total revenue from single drug

- 📉 Projected Decline: Analyst consensus ~$7B by 2032 (77% decline from $32.7B 2026 peak)

- 🧪 Biosimilar Competition: Multiple developers preparing for 2028 launch

- ⚖️ Price Erosion: Typical 30-50% within 3 years of biosimilar entry

Mitigation strategies:

- 💉 Subcutaneous formulation provides differentiation

- 📈 Label expansion maximizes pre-expiration revenue

- 💰 $3B cost-cutting initiative protects margins

- 🔬 Pipeline diversification ($12.5B+ in acquisitions)

Gardasil China Collapse 🇨🇳

Merck announced a temporary halt of Gardasil shipments to China from February through at least mid-2025:

- 📉 Q4 2024: $1.6B (down 18% YoY)

- 💸 Full Year 2024: $8.6B (down 3% from $8.9B peak)

- 🇨🇳 China Exposure: 60-70% of international sales (~$4-4.5B annually)

- 💰 Competitive Pressure: Domestic 9-valent HPV vaccine priced 60% cheaper

Root causes: Inventory buildup, weak consumer demand from anti-corruption probe, out-of-pocket payment barrier. Recovery timeline uncertain.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timeline through January 16th (next monthly OPEX):

📈 Bull Case (30% probability)

Target: $105-$110

How we get there:

- 💪 Strong Q1 2025 earnings in late April (revenue toward $16.5B+, beat expectations)

- 🚀 Winrevair and Capvaxive adoption accelerates beyond current trajectory

- 💊 Gardasil China shipment resumption announced earlier than expected

- 📊 Positive pipeline news (additional Keytruda label expansions approved)

- ✅ Subcutaneous Keytruda approval track looks solid (positive FDA commentary)

- 🤝 M&A speculation (additional acquisitions to diversify portfolio)

- 📈 Breakout above $100 gamma resistance triggers technical rally to $105-110

Key metrics needed:

- Keytruda growth sustaining 15%+ YoY

- 2025 guidance raised from conservative $64.5-65B baseline

- Gross margins expanding (proving pricing power despite competition)

- Pipeline assets advancing (Phase 3 successes in cardiometabolic)

Why only 30%: Requires breaking through massive $100 gamma wall (72.0B) and multiple positive catalysts aligning. Stock already near 52-week highs at $105.84. Conservative valuation (13.10x P/E) limits explosive upside. Gardasil headwinds and Keytruda patent cliff create structural headwinds.

🎯 Base Case (50% probability)

Target: $95-$102 range (CONSOLIDATION)

Most likely scenario:

- 📊 Solid Q1 earnings meeting consensus (in-line performance)

- ⚖️ Guidance reaffirmed at $64.5-65B revenue, $8.93-8.98 EPS

- 💊 Gardasil China remains question mark - neither major positive nor negative

- 🚀 New product launches progressing steadily (Winrevair, Capvaxive on track)

- 📈 Keytruda continues 15-17% growth (meeting expectations, not exceeding)

- 🔄 Trading within gamma support ($95-$99) and resistance ($100-$101) bands

- 💤 Low volatility consolidation as market awaits September subcutaneous decision

- 🎯 Dividend support at 3.3% yield attracts income investors around $95-98

This is where the covered call makes perfect sense: Stock consolidates in tight range, pinned by $100 resistance. The seller gets assigned at their target exit price of ~$100, capturing gains from much lower entry. Everybody wins.

Why 50% probability: Stock at technical equilibrium between support and resistance. Fundamentals solid but not spectacular. No major near-term catalysts to drive breakout. Large-cap pharma tends to trade range-bound absent major news. The 2% implied weekly move reflects this stability.

📉 Bear Case (20% probability)

Target: $90-$95 (TEST SUPPORT)

What could go wrong:

- 😰 Q1 earnings disappoint (revenue/margin miss, conservative guidance)

- 🚨 Gardasil China situation worsens (shipment halt extended through 2025)

- 💸 Keytruda competition intensifies earlier than expected (biosimilar threats)

- ⏰ Pipeline disappointments (trial failures, FDA setbacks)

- 🇨🇳 China geopolitical tensions escalate (impacts broader pharma sector)

- 💰 Broader market selloff drags large-cap pharma lower

- 📉 Break below $95 gamma support triggers cascade to $90

Critical support levels:

- 🛡️ $99: Immediate floor (4.8B gamma) - first defense

- 🛡️ $95: MAJOR SUPPORT (19.4B gamma - highest put gamma level!) - MUST HOLD

- 🛡️ $90: Deep support (7.9B gamma) - disaster scenario

Why only 20%: Merck's fundamentals remain strong (Keytruda still growing 17%, successful new launches, pipeline advancing). Conservative valuation (13.10x P/E) provides downside protection. 3.3% dividend yield attracts buyers on dips. The $95 gamma floor with 19.4B exposure creates mechanical buying support. Would require multiple negative catalysts to break below this level.

Impact on covered call: Even in bear case with stock at $95, the $40 calls still worth $55 (massively ITM), assignment still occurs at expiration. The covered call seller's position is essentially bulletproof in ANY scenario given how deep ITM the strike is.

💡 Trading Ideas

🛡️ Conservative: Income Focus with Dividend Safety

Play: Buy MRK stock around $95-98 for 3.3% dividend yield and capital preservation

Why this works:

- 💰 3.3% dividend yield provides steady income (paid quarterly)

- 📊 Conservative valuation at 13.10x P/E vs. large-cap pharma average 15-20x

- 🛡️ Defensive pharma sector offers recession protection

- 📈 Strong gamma support at $95 (19.4B) creates natural floor

- 🎯 Keytruda growth still strong (17% in 2024) despite patent cliff concerns

- ✅ Successful new product launches (Winrevair $419M, Capvaxive ramping)

- 🔬 $12.5B in acquisitions/licensing deals diversifying pipeline

Action plan:

- 🎯 Enter on any pullback to $95-98 range (gamma support zone)

- 💰 Collect $0.85 quarterly dividend (next ex-date ~March 2026)

- ⏰ Hold 12-24 months for subcutaneous Keytruda approval catalyst (Sept 2025)

- 📊 Set mental stop at $90 (below major gamma support)

- 🚀 Upside target $110-115 if pipeline execution delivers (15-20% gain + dividends)

Position sizing: 30-40% of portfolio for income-focused investors

Risk level: Low (defensive sector, dividend support) | Skill level: Beginner-friendly

Expected outcome: Steady 3.3% dividend income + modest 5-15% capital appreciation if pipeline catalysts hit. Worst case, collect dividends while waiting for Keytruda replacement products to mature.

⚖️ Balanced: Sell Cash-Secured Puts at Support

Play: Sell cash-secured puts at $95 strike to get paid while waiting for entry

Structure: Sell $95 puts (January 16 expiration - 32 days out)

Why this works:

- 💰 Collect premium ($2-3 per contract = $200-300 income) for agreeing to buy at $95

- 🎯 $95 strike sits at MAJOR gamma support (19.4B - highest put gamma level!)

- 📊 If assigned, you own stock at $92-93 net cost (after premium) - excellent entry!

- ✅ If not assigned, keep premium and repeat monthly (12-15% annualized return on cash)

- 🛡️ Defined risk: Willing to own MRK at $95 anyway (conservative entry point)

- 📈 January expiration captures any Q1 earnings volatility pop

Estimated P&L:

- 💰 Collect $200-300 premium per contract

- 📈 Best case: Stock stays above $95, keep premium, repeat (annualizes to 12-15% return)

- 🎯 Assignment case: Own MRK at $92-93 net cost (5-8% below current price) - GREAT!

- 📉 Worst case: Stock drops to $85, you own at $92-93 net cost (underwater ~8-10%)

Entry timing:

- ⏰ Sell puts now through late December (capture time decay)

- 🎯 Target strikes at gamma support levels ($95 primary, $90 aggressive)

- 💰 Take profits at 50-60% of max gain if stock rallies (don't be greedy)

Position sizing: Risk 20-30% of cash on hand (leave room for assignment)

Risk level: Moderate (cash-secured, defined risk) | Skill level: Intermediate

Probability of profit: ~60-70% (stock has to drop 5%+ to break your net cost)

🚀 Aggressive: Bull Call Spread on Keytruda Catalysts (ADVANCED)

Play: Buy call spreads targeting subcutaneous Keytruda approval catalyst

Structure: Buy $105 calls, Sell $110 calls (January 16 expiration)

Why this could work:

- 🚀 Targeting breakout above $105 resistance (14.7B gamma) on positive pipeline news

- 📋 Subcutaneous Keytruda approval narrative builds into September 2025 decision

- 💰 Defined risk spread ($5 wide = $500 max risk per spread)

- 📈 Captures upside to $110 if multiple catalysts align (Q1 beat + pipeline wins)

- ⚖️ Much cheaper than buying stock outright (risk $500 vs. $10,000)

- 🎯 Potential 100-200% return if stock reaches $110 by January expiration

Why this could blow up (SERIOUS RISKS):

- 📊 Fighting massive resistance: $100 gamma wall (72.0B) then $105 (14.7B) - TWO layers to break!

- ⏰ 32 days to expiration: Limited time for thesis to play out

- 😰 Keytruda patent cliff overhang: Structural headwind limits upside enthusiasm

- 🇨🇳 Gardasil China risk: Any negative news tanks stock 5-10%

- 💸 Premium decay: Theta burns -$10-15/day as expiration approaches

- ⚠️ Stock needs to rally 5-10% just to reach breakeven after premium paid

Estimated P&L:

- 💰 Cost: ~$1.50-2.00 per spread (net debit)

- 📈 Max profit: $3.00-3.50 if MRK above $110 at expiration (150-200% return!)

- 🎯 Breakeven: ~$106.50-107.00 (need 6-7% rally from current $100)

- 📉 Max loss: $150-200 if MRK below $105 (100% loss of premium)

Entry timing:

- ⏰ Wait for pullback to $98-99 to improve risk/reward

- 🎯 Only enter if positive pipeline news emerges (trial success, FDA Priority Reviews)

- ❌ Skip if stock already above $103 (reduces profit potential)

Position sizing: Risk only 3-5% of portfolio (this is directional speculation)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand pharma approval timelines and FDA catalyst trading

- ✅ Can afford to lose ENTIRE premium (real possibility!)

- ✅ Have plan to take profits at 75-100% gain (don't get greedy)

- ✅ Recognize this is SPECULATION on multiple catalysts aligning perfectly

Risk level: HIGH (directional bet, fighting resistance) | Skill level: Advanced only

Probability of profit: ~35-40% (need significant rally to overcome resistance + premium cost)

⚠️ Risk Factors

Don't get blindsided by these potential headwinds:

-

💊 Keytruda Patent Cliff (2028): The 800-pound gorilla in the room - Keytruda represents 45-46% of total revenue with patent expiration in 2028. Analysts project sales dropping 77% from $32.7B peak to ~$7B by 2032 as biosimilars enter. This creates MASSIVE revenue replacement challenge requiring flawless pipeline execution. Even with subcutaneous differentiation, price erosion is inevitable. The entire MRK investment thesis hinges on successfully diversifying revenue before 2028.

-

🇨🇳 Gardasil China Collapse: Merck paused shipments to China from February through mid-2025 after Q4 2024 sales dropped 18% YoY. China represents 60-70% of Gardasil international sales (~$4-4.5B annually). Domestic competitor priced 60% cheaper while anti-corruption probe dampens demand. Full-year 2024 sales of $8.6B down from $8.9B peak. Recovery timeline completely uncertain - could be quarters or years. This removes a second major growth driver alongside Keytruda concerns.

-

🔬 Pipeline Execution Risk: Merck invested $12.5B+ in acquisitions (Cidara $9.2B, EyeBio $3B, Harpoon $680M) and licensing deals (LaNova $3.3B) to diversify beyond Keytruda. However, these assets face significant development risk:

- Cidara's CD388: Phase 3 trial ongoing - any failure wastes $9.2B investment

- Cardiometabolic pipeline: Claims $15B+ peak sales potential but none approved yet

- Historic precedent: June 2024 Complete Response Letter for patritumab deruxtecan shows FDA approval isn't guaranteed

- If multiple late-stage assets fail 2025-2027, there's NO backup plan for Keytruda cliff

-

💰 Conservative 2025 Guidance Signals Caution: Management guided to only 1-2% revenue growth for 2025 ($64.5-65B vs. $64.2B in 2024). This conservative outlook suggests:

- Limited confidence in Gardasil recovery

- Expectation of Keytruda growth deceleration

- New products (Winrevair/Capvaxive) not moving needle yet

- Potential macro headwinds in pharma spending

- This muted growth profile doesn't justify premium valuations or aggressive positioning

-

🌍 Geopolitical & Regulatory Risks: Pharma sector faces increasing headwinds:

- Drug pricing reforms: Medicare negotiation pressure on blockbusters

- China tensions: Export restrictions, reimbursement changes

- FX headwinds: ~0.5% currency drag in 2025 guidance

- Tariff impact: Estimated <$100M in 2025 but could escalate

- Patent challenges: Generic/biosimilar litigation ongoing

- Any combination of these macro factors could compress margins 2-3% and impact stock 10-15%

-

📊 Valuation Offers No Margin of Safety: While 13.10x P/E seems reasonable, this multiple assumes:

- Keytruda growth continues through 2027 (not guaranteed)

- New product launches succeed (Winrevair needs to hit $2-3B+ peak)

- Pipeline assets deliver on time (2026-2028 approvals critical)

- No major FDA setbacks or trial failures

- If ANY of these assumptions break, stock could quickly de-rate to 10-11x P/E = $80-85 price target

-

🧪 M&A Integration Execution: Three major acquisitions in 18 months create integration risk:

- Resource allocation across multiple programs

- Key employee retention at acquired companies

- Timeline delays from integration complexity

- Potential for "winners curse" - overpaying at peak of market

- Distraction from core business execution

- History shows pharma M&A has 50-60% failure rate

-

💸 Limited Near-Term Catalysts: Next major positive catalyst is Q1 earnings (April/May 2025) followed by subcutaneous Keytruda decision (September 2025). That's 4-9 months of potential drift with:

- No earnings for 3+ months

- Gardasil China situation unresolved

- Pipeline news likely incremental, not transformative

- Competitive landscape intensifying (Novo Nordisk, Eli Lilly pressuring cardiometabolic)

- Stock could trade sideways or lower for months awaiting catalysts

🎯 The Bottom Line

Real talk: This $4.7M covered call trade isn't a bearish signal on Merck's future - it's a sophisticated institutional exit strategy at a target price. The seller likely accumulated 77,200 shares years ago around $40-50 and is NOW content to exit at $100 (100-150% gain!) by accepting assignment on these deep ITM calls.

What this trade reveals:

- 🎯 $100 is a major psychological AND technical resistance - massive 72.0B gamma wall confirms this

- 📊 Stock unlikely to break through $100 in next 4 days - 2% implied weekly move keeps it range-bound

- 💰 Holder locking in triple-digit gains - smart profit-taking after multi-year hold from $40s to $100

- ⏰ Assignment virtually certain - with 4 days to expiration and $60.30 intrinsic value, these calls WILL be exercised

- 🏦 Tax/portfolio management timing - December assignment gets trade into 2025 tax year

This is NOT a "sell everything" signal - it's a "trim and take profits" signal if you've held for years.

If you own MRK:

- ✅ Long-term holders (bought <$80): Consider trimming 25-40% around $100 to lock in gains like this trader. Keep core position for dividend income (3.3% yield) and pipeline optionality.

- 📊 Recent buyers ($95-100): Hold for subcutaneous Keytruda approval catalyst (September 2025) and Q1 earnings. Set mental stop at $95 gamma support.

- 💰 Dividend investors: MRK remains solid income play - 3.3% yield, 13.10x P/E, defensive sector positioning. Collect dividends while waiting for pipeline to develop.

- 🎯 Consider covered calls yourself: If you own 100+ shares, selling OTM calls at $105 generates income while stock consolidates against resistance.

If you're watching from sidelines:

- 🎯 Best entry: $95-98 pullback - targets major gamma support (19.4B at $95) with 3.3% dividend yield cushion

- ⏰ Key timing: After any Q1 earnings weakness (late April/May) when IV drops and better risk/reward emerges

- 📈 Bullish catalyst chain: Q1 earnings beat → Gardasil China recovery → Subcutaneous approval (Sept) → Pipeline wins

- 📊 Fair value estimate: $100-105 - current price around fair value, not screaming bargain but not overvalued either

- ⚠️ Need margin of safety: Don't chase at $100-102. Wait for pullback to $95-97 for 5-8% cushion.

If you're bearish:

- 🚫 Don't fight the dividend support - 3.3% yield provides natural floor around $95 from income buyers

- 📉 Target break below $95 gamma support - that's the trigger for cascade to $90, then $85

- ⏰ Timing is key: Wait for actual negative catalyst (earnings miss, pipeline failure, Gardasil deterioration)

- 💰 Put spreads more effective than outright shorts - defined risk, lower capital requirement, better risk/reward

- 🎯 Watch for January $95 puts - if institutions start piling into these, it signals serious concern

Mark your calendar - Key dates:

- 📅 December 19 (Friday) - Weekly OPEX, this $4.7M covered call assignment occurs

- 📅 January 16, 2026 (Friday) - Monthly OPEX, next major options expiration

- 📅 Late April/Early May 2025 - Q1 2025 earnings report (next major fundamental catalyst)

- 📅 September 23, 2025 - Subcutaneous Keytruda FDA PDUFA decision (CRITICAL CATALYST!)

- 📅 Q1 2026 - Cidara acquisition expected to close ($9.2B deal)

- 📅 Mid-2025 - Keytruda label expansion decisions (head/neck cancer indication)

- 📅 2028 - Keytruda first patent expiration (THE existential event)

Final verdict: Merck is a SOLID large-cap pharma story with real catalysts (subcutaneous Keytruda, new launches, pipeline diversification) but faces SIGNIFICANT structural headwinds (Keytruda 2028 patent cliff, Gardasil China collapse). At $100 with 13.10x P/E and 3.3% dividend yield, it's fairly valued - neither a screaming buy nor an obvious sell.

The $4.7M covered call shows smart institutional money taking profits at technical resistance after multi-year gains. That's prudent risk management, not bearish thesis.

Best approach: Wait for $95-98 pullback to enter with margin of safety. Let this $100 resistance get tested and resolved. Be patient - Merck will still be here, and better entry points are likely in coming months. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The deep ITM covered call structure described reflects institutional portfolio management needs that may not apply to retail traders. Always do your own research and consider consulting a licensed financial advisor before trading. The $4.7M premium represents a unique covered call exit strategy, not a recommendation to short MRK or sell covered calls at this specific strike. Keytruda patent expiration in 2028 creates significant long-term uncertainty requiring careful monitoring of pipeline development progress.

About Merck & Co., Inc.: Merck makes pharmaceutical products to treat several conditions in a number of therapeutic areas, including cardiometabolic disease, cancer, and infections, with a market cap of $248.9 billion in the Pharmaceutical Preparations industry.