MRNA Massive $12M Call Bet - Institution Loads Up Ahead of Cancer Vaccine Catalyst!

January 15, 2026 | Unusual Activity Detected

The Quick Take

Someone just dropped $12 MILLION on MRNA June calls this morning at 10:56:12! This massive bullish bet bought 18,000 contracts of the $40 strike calls expiring June 18th - almost exactly at-the-money with MRNA trading at $39.79. With Moderna's pivotal V940 cancer vaccine Phase 3 readout expected in September 2026 and an FDA decision on their flu vaccine coming mid-2026, smart money is positioning for a major turnaround in this beaten-down mRNA pioneer. Translation: Big money sees the bottom and is betting on a comeback!

Company Overview

Moderna, Inc. (MRNA) is a Cambridge, Massachusetts-based biotechnology company that pioneered messenger RNA (mRNA) therapeutics:

- Market Cap: ~$15.5 Billion

- Industry: Biotechnology / mRNA Therapeutics

- Current Price: $39.79 (near 52-week lows)

- 52-Week Range: $22.28 - $45.40

- Primary Business: COVID-19 vaccines, RSV vaccines, and pipeline candidates in oncology, infectious diseases, and rare diseases

Moderna gained global prominence through Spikevax, its COVID-19 vaccine that generated peak annual sales of $18.4 billion in 2022. The company is now racing to diversify beyond COVID-19 with its mRNA platform, targeting a 2028 breakeven with approximately $6.6 billion in cash reserves.

The Option Flow Breakdown

The Tape (January 15, 2026 @ 10:56:12):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:56:12 | MRNA | MID | BUY | CALL $40 | 2026-06-18 | $12M | $40 | 18K | 16K | 17,999 | $39.79 | $6.90 |

What This Actually Means

This is a massive directional bullish bet on Moderna's turnaround! Here's what went down:

- Huge premium paid: $12M ($6.90 per contract x 18,000 contracts)

- Strike selection: $40 is nearly at-the-money (stock at $39.79) - this is a HIGH CONVICTION play

- Strategic timing: 154 days to expiration captures Q4 earnings (February), Arbutus patent trial (March), and flu vaccine FDA decision (mid-2026)

- Size matters: 18,000 contracts represents 1.8 million shares worth ~$71.6M in notional exposure

- Opening position: Volume of 18,000 vs OI of 16,000 with Z-score of 23.28 = EXTREMELY UNUSUAL new position

What's really happening here:

This trader is betting that MRNA breaks out of its beaten-down range before June. At $6.90 per contract with the stock at $39.79, they need MRNA above $46.90 at expiration to profit - roughly 18% upside from current levels. But here's the key: they're positioning 5 months AHEAD of the September 2026 cancer vaccine readout, likely expecting the stock to run up in anticipation of that catalyst.

Unusual Score: EXTREMELY UNUSUAL (Z-score 23.28) - This is the kind of size that shows up only a handful of times per year. When someone drops $12M on a single options position in a beaten-down biotech, they either know something or have extremely high conviction in the catalyst calendar.

Technical Setup / Chart Check-Up

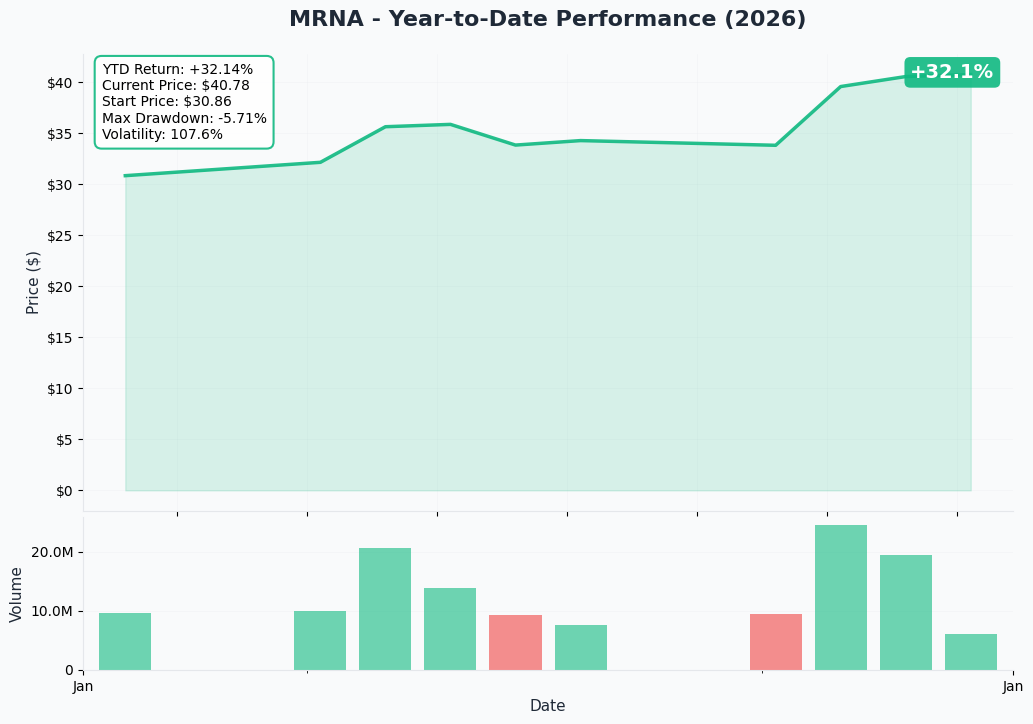

YTD Performance Chart

MRNA has been through the wringer - currently trading near the lower end of its 52-week range ($22.28 - $45.40). The stock peaked at over $450 during the pandemic and has declined roughly 85% from those highs as COVID-19 vaccine demand normalized. However, the recent price action shows potential bottoming behavior around the $33-40 range.

Key observations:

- Stock stabilizing after brutal multi-year decline from pandemic highs

- Current price of $39.79 represents potential support zone

- Volume picking up as value hunters and catalyst players enter

- 52-week range tightening suggests inflection point approaching

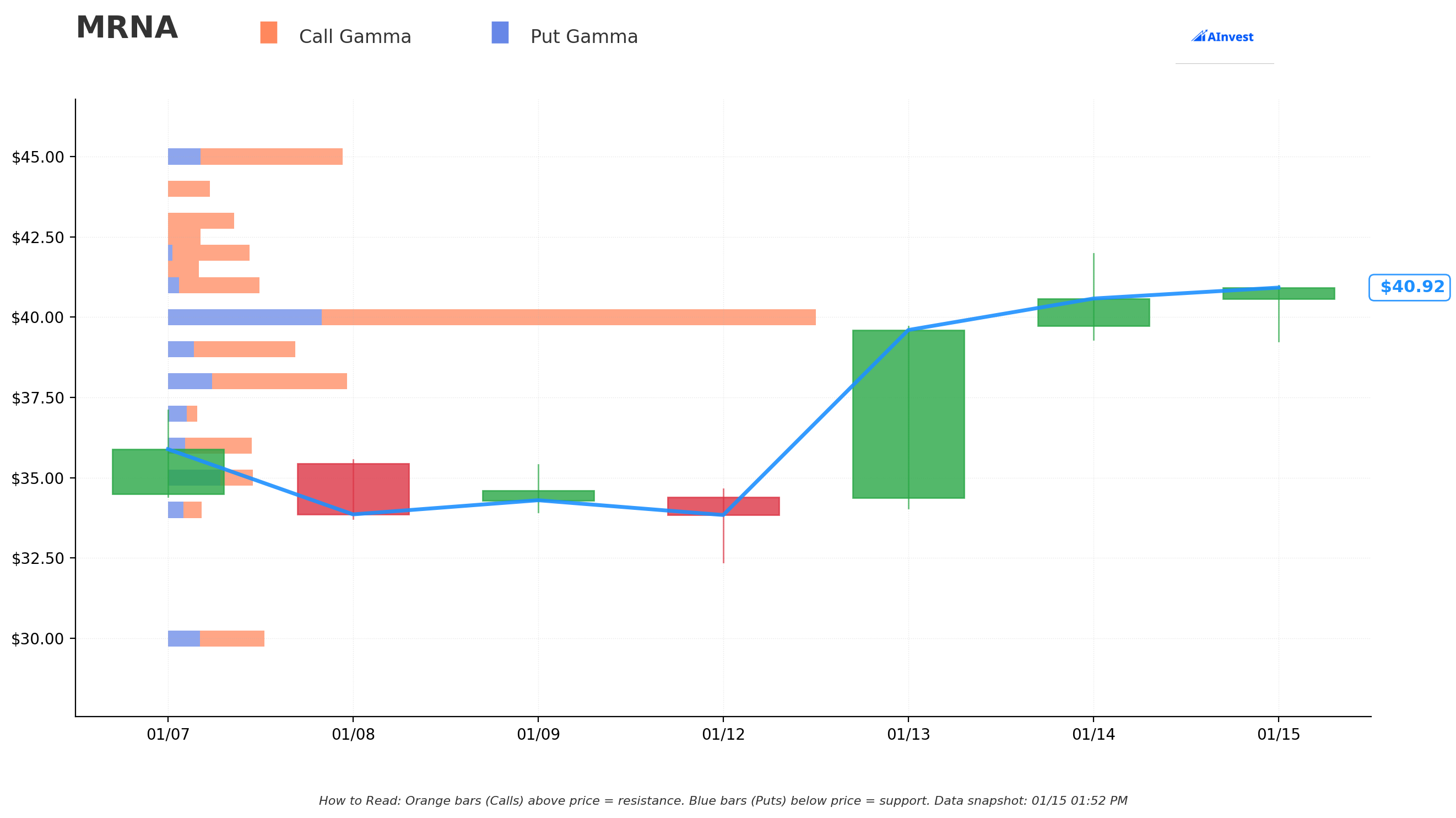

Gamma-Based Support & Resistance Analysis

Current Price: $40.87 (as of gamma calculation)

The gamma exposure map reveals critical price levels that will govern near-term price action:

Support Levels (Put Gamma Below Price):

- $40 - STRONGEST support with 26.4 total gamma exposure (this is where the call trade struck!)

- $39 - Secondary support at 5.2 total gamma

- $38 - Additional support at 7.7 total gamma

- $36 - Deeper support floor at 3.8 total gamma

- $35 - Extended support at 3.5 total gamma

Resistance Levels (Call Gamma Above Price):

- $41 - Immediate resistance at 3.7 total gamma (only 0.3% overhead)

- $42 - Secondary resistance at 3.3 total gamma

- $43 - Third level at 2.7 total gamma

- $44 - Light resistance at 1.7 total gamma

- $45 - Key psychological level and MAJOR resistance at 7.0 total gamma (10% above current)

What this means for traders:

The $40 strike has the HIGHEST gamma concentration - this is exactly where the $12M call buyer positioned! This level acts as a strong magnet for price action. The relatively light resistance above suggests that IF MRNA can break through $41-42, the path to $45 could open up quickly.

Net GEX Bias: Bullish (66.95 call gamma vs 25.23 put gamma) - Overall dealer positioning supports upward price movement.

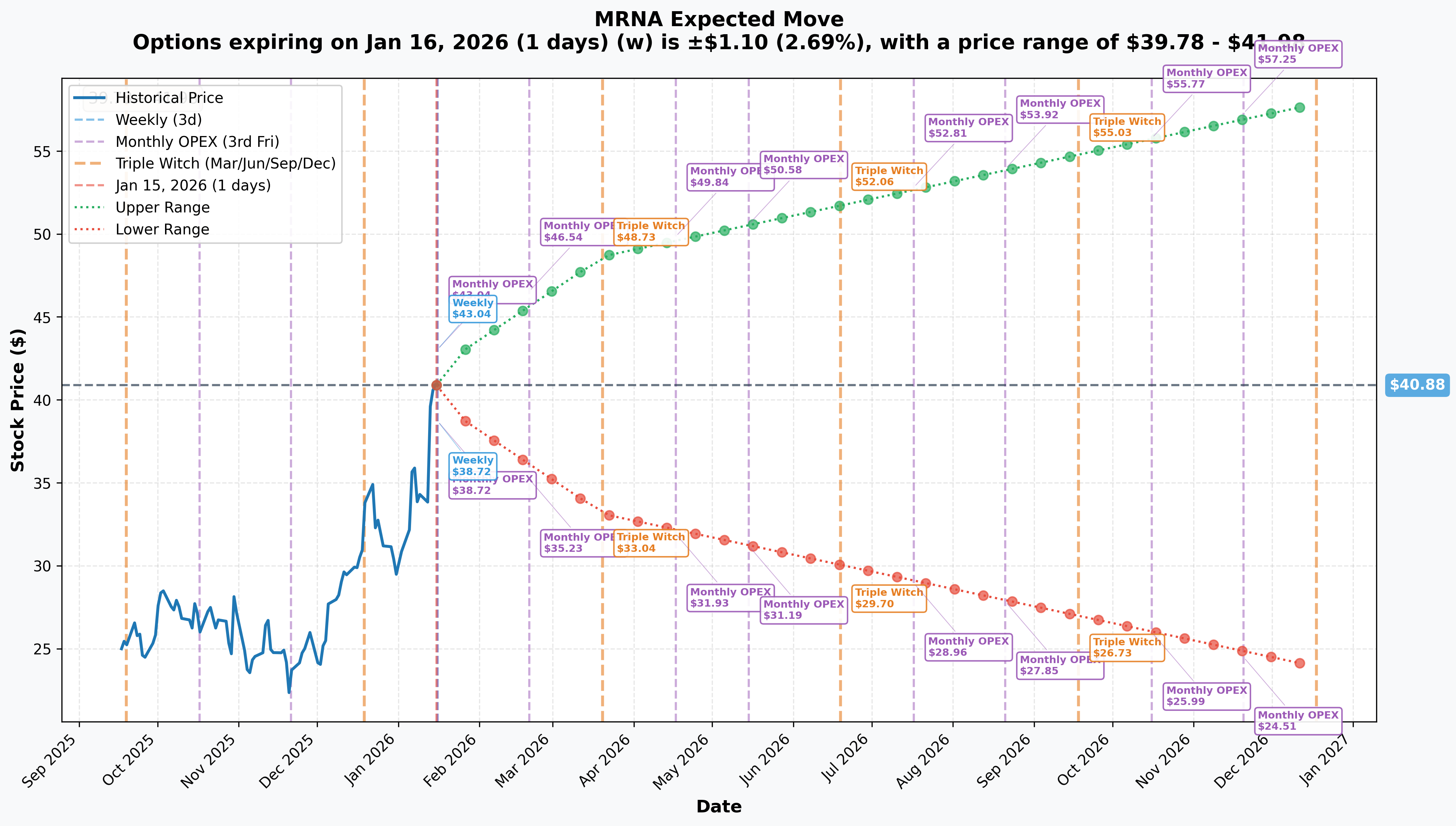

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 16 - 1 day): +/-2.69% (+/-$1.10) -> Range: $39.78 - $41.98

- Monthly OPEX (Feb 20): Range: $35.23 - $46.54 (captures Q4 earnings!)

- Quarterly Triple Witch (Mar 20): +/-19.02% (+/-$7.78) -> Range: $33.11 - $48.66 (captures patent trial!)

- June Triple Witch (Jun 19 - THIS TRADE!): Range: $29.70 - $52.06

Translation for regular folks:

Options traders are pricing in significant volatility through June - the market expects MRNA could move anywhere from $29.70 to $52.06 by this trade's expiration. That's a massive 55% potential range! The $40 call buyer needs the stock above $46.90 to profit, which sits well within the upper implied range of $52.06.

Key insight: The June $40 call trade aligns perfectly with the June Triple Witch expected upper range. The buyer is betting MRNA hits the upper end of its implied distribution - and given the catalyst calendar, that's not unreasonable.

Catalysts

Upcoming Catalysts (Next 6 Months)

Q4 2025 / Full Year 2025 Earnings - February 2026

Moderna's next earnings report is scheduled for approximately February 12-19, 2026, per NASDAQ and Investing.com.

- Full Year 2025 Revenue: ~$1.9 billion (achieved)

- 2026 Revenue Guidance Expected: Up to 10% growth (~$2.15 billion projected), per GuruFocus

- Key Metrics to Watch: Updated cost reduction progress, cash burn rate, 2026 guidance specifics, cancer vaccine trial updates

Arbutus Patent Trial - March 2026

A critical legal catalyst is the scheduled U.S. patent trial between Moderna and Arbutus Biopharma/Genevant Sciences, per FinancialContent and GEN.

- Background: Arbutus alleges Moderna's COVID-19 vaccine infringes patents related to lipid nanoparticle (LNP) delivery technology

- Potential Upside: Favorable ruling would remove major overhang and validate Moderna's technology

- Potential Downside: Adverse ruling could result in significant royalty obligations

mRNA-1010 Flu Vaccine FDA Decision - Mid-2026

Following regulatory filings in January 2026, Moderna expects FDA review of its standalone seasonal flu vaccine, per BioPharma Dive.

- Phase 3 Results: 26.6% relative vaccine efficacy vs. standard-dose vaccines in adults 50+, per CIDRAP

- Market Opportunity: U.S. flu vaccine market is ~$5-6 billion annually

- Timeline: Decision expected mid-2026 - WITHIN THIS TRADE'S EXPIRATION WINDOW

H5N1 Bird Flu Vaccine Phase 3 - Q1 2026

The CEPI-funded Phase 3 trial for mRNA-1018 is slated to begin early 2026, per CEPI. This $54.3 million funding came after the Trump administration terminated Moderna's $590 million BARDA contract, per Fierce Biotech.

The Big One: V940 Cancer Vaccine Phase 3 Readout - September 2026

The most significant upcoming catalyst is the pivotal Phase 3 readout for Moderna's personalized cancer vaccine V940 (mRNA-4157) in combination with Merck's Keytruda for adjuvant melanoma treatment, per Merck.

Why this matters:

- Phase 2b Results: 44% reduction in risk of recurrence or death at two years vs. Keytruda alone; nearly 50% risk reduction at three years, per PMC

- Designations: FDA Breakthrough Therapy Designation and EMA PRIME designation

- Market Significance: Success could establish Moderna in oncology and validate mRNA technology beyond vaccines

- Analyst View: The September 2026 readout is "potentially determining Moderna's survival as an independent entity," per FinancialContent

Why this call buyer is positioned NOW: While the cancer vaccine readout is in September (beyond the June expiration), stocks typically run up 3-6 months AHEAD of major catalysts. The call buyer is positioning for that anticipatory move.

Recent Catalysts (Already Happened)

Q3 2025 Earnings Beat (November 2025)

- Revenue: $1.02B vs. $909.97M consensus (12% beat), per GuruFocus

- EPS: $(0.51) vs. $(2.05) consensus (75% beat on loss reduction)

- Stock rose 7.22% in premarket following results

CEPI Bird Flu Vaccine Funding (December 2025)

- $54.3 million funding for H5N1 pandemic influenza vaccine Phase 3

- Historic: First mRNA-based bird flu vaccine to enter pivotal Phase 3 study

CMV Vaccine Failure (October 2025)

- Phase 3 CMV vaccine study failed to meet primary endpoint (6-23% efficacy), per BioSpace

- Program discontinued - a setback, but CMV has historically been one of the hardest vaccine targets

$1.5 Billion Debt Financing

- Secured five-year loan from Ares Management to extend cash runway toward 2028 breakeven goal, per Investing.com

Price Targets & Probabilities

Using gamma levels, implied move data, and the catalyst calendar, here are the scenarios through June 18th expiration:

Bull Case (30% probability)

Target: $50-$58

How we get there:

- Flu vaccine FDA approval mid-2026 opens $5-6B market opportunity

- Arbutus patent trial favorable outcome removes legal overhang

- Market begins pricing in September cancer vaccine catalyst with positive anticipation

- RSV vaccine mRESVIA gains commercial traction vs. GSK/Pfizer

- Cost cuts exceed expectations, 2028 breakeven timeline accelerates

- Break above $45 gamma resistance triggers momentum buying to implied move upper range ($52.06)

Key metrics needed:

- Flu vaccine FDA approval or positive PDUFA signals

- Patent trial resolution in Moderna's favor

- Positive interim data or commentary on cancer vaccine trial

- Continued cost discipline and cash preservation

Probability assessment: 30% because multiple catalysts need to align favorably. However, the beaten-down valuation and dense catalyst calendar provide real optionality.

Call P&L in Bull Case:

- Stock at $50 on June 18: Calls worth $10.00, profit = $3.10/contract x 18,000 = $5.58M gain (46% ROI)

- Stock at $55 on June 18: Calls worth $15.00, profit = $8.10/contract x 18,000 = $14.58M gain (121% ROI)

- Stock at $58 on June 18: Calls worth $18.00, profit = $11.10/contract x 18,000 = $19.98M gain (166% ROI)

Base Case (45% probability)

Target: $38-$48 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- Stock trades in range as market awaits September cancer vaccine readout

- Flu vaccine FDA review progresses without major headlines

- Patent trial creates short-term volatility but no definitive resolution

- Q4 earnings in-line with expectations

- Gradual accumulation by value investors ahead of catalysts

- Stock gravitates toward $40-45 range per gamma levels

This is the breakeven scenario for the call buyer: Stock needs to be above $46.90 for the trade to profit. In the base case of $38-48, the outcome depends on where exactly the stock lands.

Why 45% probability: Moderna is in transition mode - too early to definitively call the cancer vaccine, too late to ride COVID-19 momentum. Market likely to wait and see.

Bear Case (25% probability)

Target: $28-$35

What could go wrong:

- Patent trial adverse ruling creates royalty overhang on all products

- Flu vaccine FDA delays or requires additional data

- RFK Jr.-led HHS creates new regulatory headwinds for mRNA vaccines

- Cash burn accelerates, 2028 breakeven timeline pushed back

- Broader biotech selloff drags MRNA lower

- Market loses confidence ahead of cancer vaccine readout

- Break below $35 gamma support triggers cascade to $30 implied move lower range

Critical support levels:

- $40: Major gamma floor - MUST HOLD for bullish thesis

- $38: Secondary support level

- $35: Break below opens path to $30

Probability assessment: 25% because Moderna has cash runway and multiple catalysts. However, pipeline execution risk is real after CMV failure.

Call P&L in Bear Case:

- Stock at $35 on June 18: Calls worth $0, loss = -$6.90/contract x 18,000 = -$12.42M (100% loss)

- Stock at $30 on June 18: Calls worth $0, loss = -$6.90/contract x 18,000 = -$12.42M (100% loss)

Trading Ideas

Conservative: Wait for Confirmation

Play: Stay on sidelines until Arbutus patent trial clarity (March) or flu vaccine FDA signals

Why this works:

- Patent trial in March creates binary event risk - outcome could swing stock 15-20%

- Flu vaccine FDA timeline uncertain - waiting for PDUFA date provides clarity

- September cancer vaccine readout is the REAL catalyst - plenty of time to position

- Beaten-down stocks can stay beaten down longer than you expect

- Better entry likely on pullback to $35-38 range or on positive catalyst confirmation

Action plan:

- Watch March patent trial outcome closely

- Look for FDA flu vaccine PDUFA date announcement

- Monitor institutional accumulation patterns (13F filings)

- Set alerts for $35 (entry on weakness) or $45 (breakout confirmation)

- Consider entering after patent trial resolution for cleaner risk/reward

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Balanced: June Call Spread

Play: Buy call spread to reduce cost basis while maintaining upside exposure

Structure: Buy $40 calls, Sell $50 calls (June 18 expiration)

Why this works:

- Reduces cost from ~$6.90 (naked call) to ~$4.50-5.00 (spread)

- Capped at $10 max profit ($50-$40 spread width) but much cheaper entry

- Captures 25% upside ($40 to $50) while limiting premium at risk

- Aligned with implied move upper range of $52.06

- Gamma support at $40 protects downside thesis

Estimated P&L:

- Cost: ~$4.50-5.00 per spread

- Max profit: $5.00-5.50 if MRNA above $50 at June expiration (100%+ ROI)

- Max loss: $4.50-5.00 if MRNA below $40 (100% loss on spread)

- Breakeven: ~$44.50-45.00

Position sizing: Risk only 2-3% of portfolio (speculative biotech play)

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

Aggressive: Follow the Smart Money

Play: Replicate the institutional $40 call position at smaller scale

Structure: Buy $40 calls (June 18 expiration)

Why this could work:

- Directly copying a $12M institutional bet with high conviction

- 154 days to expiration captures multiple catalysts: Q4 earnings, patent trial, flu vaccine FDA progress

- At-the-money strike provides maximum gamma exposure for price movement

- Implied move suggests stock could reach $52+ by June

- Beaten-down valuation means positive surprises have outsized impact

- Cancer vaccine catalyst in September creates pre-event run-up opportunity

Why this could blow up:

- EXPENSIVE: $6.90 per contract is significant premium for a stock at $40

- TIME DECAY: Theta burns as stock consolidates

- CATALYST RISK: Patent trial could go against Moderna

- EXECUTION RISK: CMV failure shows not all Moderna programs succeed

- REGULATORY RISK: RFK Jr.-led HHS creates headline uncertainty

Estimated P&L:

- Cost: $6.90 per contract

- Breakeven: $46.90 (18% above current price)

- Target: $55-58 (profit of $8-11 per contract, 115-160% ROI)

- Loss scenario: Stock below $40 at expiration = lose entire premium

CRITICAL WARNING - DO NOT attempt unless you:

- Can afford to lose entire premium (real possibility!)

- Have conviction in Moderna's catalyst calendar

- Understand biotech binary event risk

- Plan to manage position actively (take profits on spikes, cut losses if thesis breaks)

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

Risk Factors

Don't get caught by these potential landmines:

-

Patent trial binary event in March: The Arbutus patent trial could result in significant royalty obligations on ALL Moderna products using LNP technology. This includes Spikevax and potentially mRESVIA. An adverse ruling could fundamentally change the company's economics. This catalyst occurs BEFORE the June expiration.

-

Pipeline execution risk after CMV failure: The CMV vaccine Phase 3 failure in October 2025 demonstrated that not all Moderna programs will succeed. The cancer vaccine Phase 3 (V940) is the company's most important program - any negative signals before September could crater the stock.

-

RFK Jr. regulatory headwinds: HHS Secretary RFK Jr. has terminated $500 million in federal funding for mRNA vaccine research, per NPR, and restructured the CDC's Advisory Committee for Immunization Practices. While approved products remain unaffected, headline risk persists. Children's Health Defense filed a petition asking FDA to revoke COVID vaccine licenses, per Axios.

-

Cash burn and breakeven timeline: Moderna pushed its breakeven target from 2026 to 2028, per Fierce Pharma. At ~$0.9 billion quarterly cash burn, the $6.6 billion cash position provides runway but leaves no room for execution missteps.

-

RSV competitive pressures: mRESVIA generated only $2 million in Q3 2025 revenue, per Yahoo Finance, as GSK and Pfizer maintain dominant market share with earlier entry and larger sales forces.

-

Flu vaccine market entry challenges: Even with FDA approval, Moderna faces entrenched competition from Sanofi, GSK, and others in the $5-6 billion flu vaccine market. Commercial execution has been challenging (see RSV).

-

COVID-19 market continues to decline: Revenue from Spikevax declined 45% YoY in Q3 2025. The endemic COVID-19 market is significantly smaller than pandemic peak, and FDA restrictions under RFK Jr. limit broader authorization.

-

Valuation requires execution: At $15.5 billion market cap with $1.9 billion in 2025 revenue, MRNA trades at roughly 8x revenue. This requires successful pipeline execution to justify - the cancer vaccine must work.

The Bottom Line

Real talk: Someone just bet $12 MILLION that Moderna's beaten-down stock bounces back before June. This isn't a small hedge - this is a HIGH CONVICTION directional play on a company that's been left for dead after COVID-19 demand normalized.

What this trade tells us:

- Sophisticated player expects MRNA to rally 18%+ from current levels by June

- They're positioning AHEAD of the September cancer vaccine catalyst, betting on anticipatory buying

- The $40 strike sits exactly at the strongest gamma support - smart strike selection

- 18,000 contracts (vs. 16,000 OI) means this is a NEW position, not rolling existing exposure

- Z-score of 23.28 = EXTREMELY UNUSUAL - this happens only a handful of times per year

This is a BET on Moderna's turnaround story - multiple catalysts could validate the thesis, but execution risk is real.

If you're bullish on MRNA:

- Consider smaller position sizes than the institutional whale - they can afford to lose $12M, you probably can't

- Call spreads offer better risk/reward than naked calls at current IV levels

- March patent trial is the next major catalyst - consider positioning AFTER for cleaner entry

- $35-38 pullback would offer better risk/reward than chasing at $40

If you're watching from sidelines:

- September cancer vaccine readout is the REAL inflection point - plenty of time

- March patent trial could create volatility and better entry opportunity

- Dense catalyst calendar (Q4 earnings, patent trial, flu vaccine FDA) means news flow will be active

- Current price represents potential value if you believe in mRNA platform long-term

If you're bearish:

- Stock already down 85% from highs - easy money on short side may be over

- $6.6 billion cash provides runway to 2028 - no imminent bankruptcy risk

- Patent trial adverse outcome or cancer vaccine pre-readout concerns could still push stock to $30

- Consider put spreads for defined-risk bearish positioning

Key dates to watch:

- February 12-19, 2026 - Q4/FY2025 Earnings Report

- March 2026 - Arbutus Patent Trial (CRITICAL!)

- Q1 2026 - H5N1 Bird Flu Vaccine Phase 3 Initiation

- Mid-2026 - mRNA-1010 Flu Vaccine FDA Decision

- June 18, 2026 - This $12M call trade EXPIRES

- September 2026 - V940 Cancer Vaccine Phase 3 Readout (THE BIG ONE)

Final verdict: Moderna is a HIGH RISK / HIGH REWARD turnaround play. The $12M institutional call purchase signals smart money sees value at current levels and is willing to bet on the catalyst calendar. However, this is NOT a recommendation to blindly follow - the buyer has a 5-month time horizon and can absorb total loss. For retail traders, smaller position sizes, defined-risk strategies (spreads), and patience for better entries (post-patent trial, post-earnings pullback) make more sense.

The mRNA platform is real. The cancer vaccine could be transformational. But at $40/share, you're paying for execution that hasn't happened yet. Size accordingly.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Biotechnology stocks carry significant pipeline and regulatory risk. The $12M trade represents institutional positioning that may not be appropriate for retail portfolios. Always do your own research and consider consulting a licensed financial advisor before trading.

About Moderna, Inc.: Moderna is a biotechnology company pioneering messenger RNA (mRNA) therapeutics and vaccines. The company's platform technology enables the body's cells to produce proteins that can prevent or treat diseases. Key products include Spikevax (COVID-19 vaccine) and mRESVIA (RSV vaccine), with a pipeline spanning oncology, infectious diseases, and rare diseases. Market cap of approximately $15.5 billion in the Biotechnology industry.