🧬 MRNA Sells $2.7M in Calls After Cancer Vaccine Data Sends Stock Soaring!

📅 January 22, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just sold $2.7 MILLION worth of MRNA calls after the stock exploded 15.8% on melanoma vaccine data! This trader sold 5,000 contracts of the July 17th $70 strike calls - collecting premium at what could be the peak of this cancer vaccine rally. With MRNA now trading near 52-week highs at $53.74 and critical Q4 earnings coming February 13-19, this looks like institutional profit-taking after the biggest single-day move in months. Translation: Big money is cashing in on the hype while retail chases the headline!

📊 Company Overview

Moderna (MRNA) is a commercial-stage biotech pioneer in mRNA technology:

- Market Cap: $19.46 Billion

- Industry: Biological Products (No Diagnostic Substances)

- Current Price: $53.74 (near 52-week high of $50.00 prior to rally)

- Primary Business: mRNA vaccines and therapeutics across infectious diseases, oncology, cardiovascular, and rare genetic diseases with 35+ development candidates in clinical trials

💰 The Option Flow Breakdown

📊 The Tape (January 22, 2026)

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order Type | Strategy |

|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-22 | 13:09:09 | MRNA | SELL | CALL $70 | 2026-07-17 | $70.00 | 5,000 | $2,700,000 | STO | Short Call |

🤓 What This Actually Means

This is a premium collection play after a massive rally! Here's the breakdown:

- 💸 Massive premium collected: $2.7M ($5.40 per contract x 5,000 contracts)

- 🎯 Strike selection: $70 is 30% above current price - betting stock WON'T reach that level

- ⏰ Strategic timing: 176 days to expiration, capturing Q4 earnings (Feb 13-19), Arbutus patent trial (March), and multiple pipeline readouts

- 📊 Vol/OI Ratio: 178.57 - HIGH ACTIVITY signal, this is not normal trading

- 🏦 Income generation: Trader collecting premium expecting stock to consolidate after the cancer vaccine pop

What's really happening here:

This trader is selling NAKED calls (or selling against a long stock position) betting that MRNA won't rally another 30% from here to $70 by July. After the stock jumped 15.8% in a single day on the melanoma vaccine five-year data, this institutional player is essentially saying: "The good news is priced in - time to sell the hype."

The Trade Logic:

- ✅ If MRNA stays below $70 by July 17 = Keep full $2.7M premium (100% profit)

- ⚠️ If MRNA rises above $70 = Obligation to sell/deliver at $70 (potential unlimited loss if naked)

- 🎯 Breakeven: $75.40 (strike + premium collected)

📈 Technical Setup / Chart Check-Up

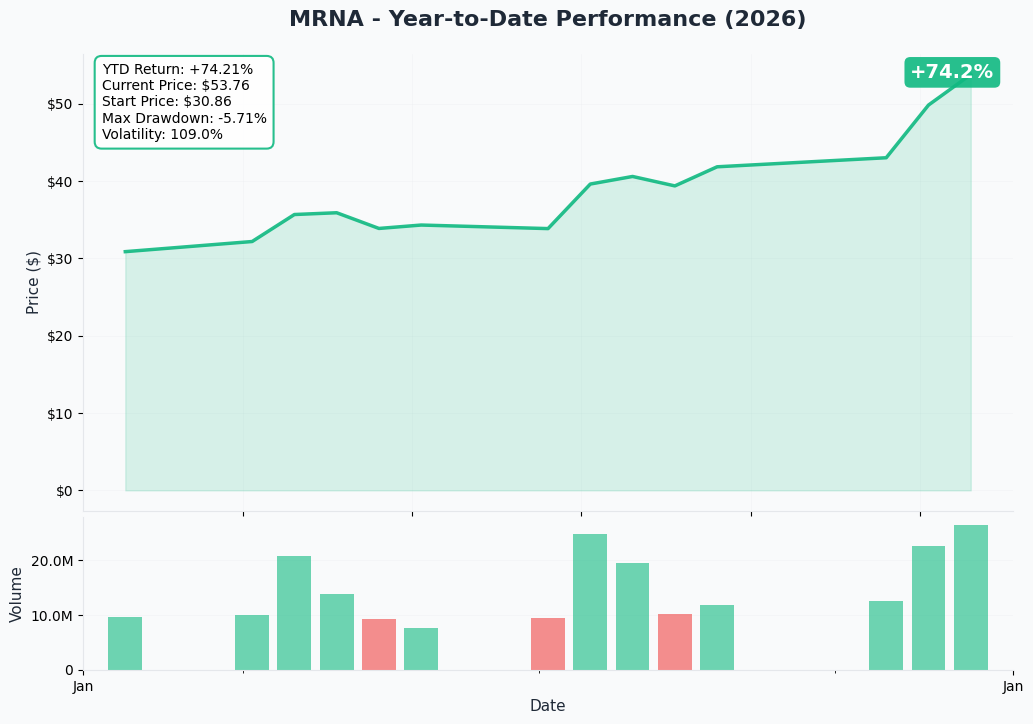

YTD Performance Chart

MRNA has been on a roller coaster ride - after hitting lows around $22.28 earlier in the cycle, the stock has now rallied to $53.74 following the January 21st melanoma vaccine catalyst. The 15.8% single-day jump brought the stock to fresh 52-week highs, but the question remains: is this a breakout or a blow-off top?

Key observations:

- 🚀 Massive rally: Stock more than doubled from 52-week lows on cancer vaccine optimism

- 📈 Breakout confirmed: Smashed through $50 resistance on huge volume

- 🎢 High volatility: Biotech stocks are notoriously volatile around clinical data

- 📊 Volume explosion: Institutional accumulation evident on the January 21st move

- ⚠️ Extended territory: After a 15.8% gap, near-term consolidation likely

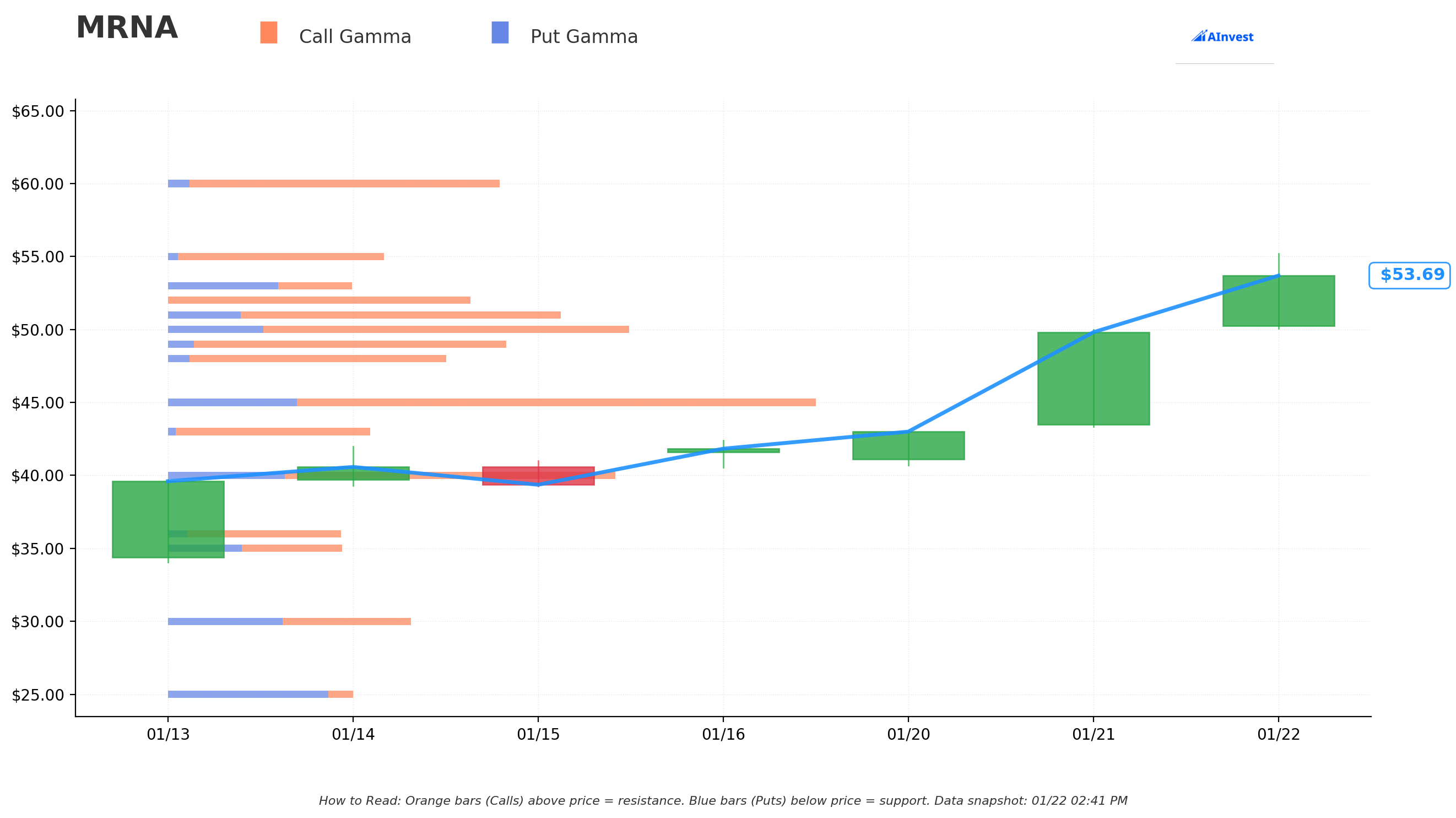

Gamma-Based Support & Resistance Analysis

Current Price: $53.60

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🔵 Support Levels (Below Price):

- $53 - Immediate support with -0.21 net GEX (closest floor)

- $52 - Strong support at 1.93 net GEX (dealers will buy dips here)

- $51 - Secondary support at 1.53 net GEX

- $50 - Major psychological floor with 1.72 net GEX (the LINE IN THE SAND)

- $49 - Extended support at 1.80 net GEX

- $48 - Deep support at 1.51 net GEX

- $45 - Major structural floor with 2.47 net GEX (highest activity below $50)

- $43 - Disaster floor at 1.18 net GEX

🟠 Resistance Levels (Above Price):

- $55 - Immediate ceiling with 1.23 net GEX (2.6% overhead)

- $60 - Major resistance at 1.81 net GEX (11.9% above current)

What this means for traders:

MRNA is trading just above the $53 support level with resistance at $55 and $60. The gamma data shows positive net GEX bias overall (30.6B call gamma vs 10.3B put gamma), which is BULLISH positioning. However, the call seller at $70 is betting that even with this bullish setup, the stock won't sustain another 30% rally.

Net GEX Bias: Bullish - Overall dealer positioning supports the upside, but immediate resistance at $55 creates a near-term ceiling.

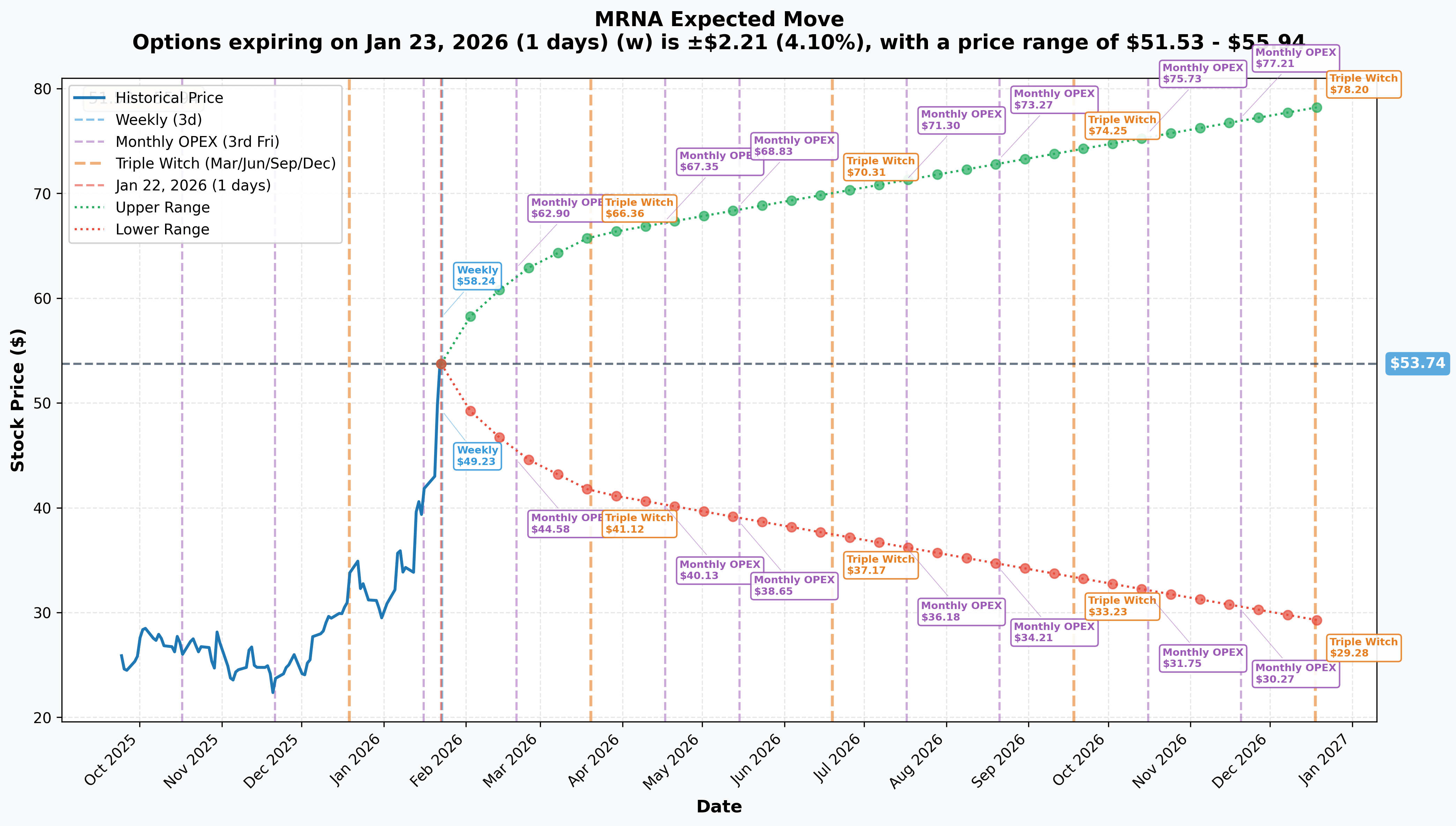

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 23 - 1 day): +/-4.1% ($2.21) → Range: $51.53 - $55.94

- 📅 Monthly OPEX (Feb 20 - 29 days): +/-16.09% ($8.65) → Range: $45.09 - $62.39

- 📅 Triple Witch (Mar 20 - 57 days): +/-22.74% ($12.22) → Range: $41.52 - $65.96

- 📅 July OPEX (Jul 17 - THIS TRADE!): Implied range: $36.18 - $71.30

Translation for regular folks:

Options traders are pricing in a massive 16% move by February OPEX which captures the Q4 earnings report. The market expects FIREWORKS around earnings - that's a huge implied move for a $19B biotech! By the July 17th expiration (when this $2.7M trade expires), the implied upper range is $71.30 - meaning the call seller is betting the stock stays below $70, just under the market's expected maximum.

Key insight: The call seller is essentially betting AGAINST the upper bound of the implied move. If MRNA stays anywhere below $70, they win. The market gives this roughly 60-70% probability based on the options pricing.

🎪 Catalysts

🔥 Recent Catalysts (What Just Happened)

Cancer Vaccine Breakthrough (January 20, 2026) - THE BIG ONE!

Moderna and Merck released five-year data from the KEYNOTE-942 trial showing intismeran autogene + Keytruda demonstrated a 49% reduction in risk of recurrence or death vs Keytruda alone in high-risk melanoma:

- 🧬 Effect maintained identically from 3-year to 5-year mark, demonstrating durable immune system reprogramming

- 💰 GlobalData forecasts intismeran to become blockbuster with $2.3B in 2031 sales

- 📈 Stock surged 15.8% on January 21st on this news

- 🚀 This validates Moderna's mRNA platform for oncology applications beyond vaccines

Q3 2025 Earnings (November 6, 2025) - Beat Expectations:

- Revenue: $1.0B (beat consensus of $886.54M)

- EPS: -$0.51 (beat consensus of -$2.05 by 76.50%)

- Revenue down 45% YoY driven by COVID vaccine decline

- Cost discipline improving: R&D expenses reduced 30% to $801M

Preliminary 2025 Full-Year Results (January 2026):

- Revenue: $1.9B (exceeded upper guidance)

- Net Loss: ~$3.1B (improved from $3.56B in 2024)

- Cash Reserves: $8.1B including $1.5B term loan facility

📅 Upcoming Catalysts (Next 6 Months)

Q4 2025 Earnings Report: February 13-19, 2026 📊

Expected earnings date per Nasdaq:

- 2026 revenue and operating expense guidance update

- Cash runway and breakeven timeline clarity

- Pipeline progress updates on oncology programs

- RSV vaccine (mRESVIA) commercial traction vs GSK/Pfizer

Arbutus Patent Trial: March 2026 ⚖️

Critical U.S. trial over lipid nanoparticle (LNP) technology:

- Potential damages exceed $100B based on combined Spikevax sales

- Arbutus/Genevant seeking monetary relief AND injunctions against Spikevax and mRESVIA

- EPO revoked Arbutus patent EP 2279254 in January 2026 - potentially helping Moderna's European position

Cancer Vaccine Program Milestones:

- INTerpath-001 Phase 3 interim data (melanoma): Potentially 2026

- INTerpath-002 Phase 3 (NSCLC): Global enrollment underway

- INTerpath-009 Phase 3 (NSCLC post-neoadjuvant): First patients enrolling

- First regulatory approvals anticipated late 2026 to 2027

Respiratory Vaccine Updates:

- mRNA-1010 flu vaccine: FDA discussions ongoing

- mRNA-1083 combo flu/COVID: Resubmission expected late 2026

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through July 17th expiration:

📈 Bull Case (20% probability)

Target: $65-$75

How we get there:

- 🧬 INTerpath-001 Phase 3 interim data shows continued strong efficacy

- 💊 RSV vaccine mRESVIA gains significant market share in spring respiratory season

- ⚖️ Arbutus patent trial ruled in Moderna's favor or settled favorably

- 📈 Q4 earnings show better-than-expected cost discipline, 2028 breakeven moved forward

- 🚀 Additional oncology indications show promising Phase 2 data (NSCLC, bladder cancer)

- 💰 Institutional upgrades following melanoma data validation

Probability assessment: 20% because multiple catalysts need to align positively. The Arbutus trial creates significant binary risk, and RSV market share gains face intense GSK and Pfizer competition. Breaking $70 would invalidate the call seller's thesis.

🎯 Base Case (55% probability)

Target: $45-$60 range (CONSOLIDATION)

Most likely scenario:

- ✅ Stock consolidates after 15.8% gap-up, digests gains in $50-60 range

- 📊 Q4 earnings meet expectations with no major surprises

- ⚖️ Arbutus trial remains unresolved or partially settled

- 🤖 Oncology pipeline progresses but no breakthrough readouts before July

- 🔄 COVID revenue continues declining as expected

- 💤 Stock trades within gamma support ($45-50) and resistance ($55-60) bands

This is the call seller's TARGET scenario: Stock consolidates, $70 calls expire worthless, and they keep the full $2.7M premium. They're betting the melanoma news is "priced in" after the 15.8% pop.

Why 55% probability: Biotech stocks often give back gap gains when catalysts pass. The fundamental story is improving but monetization is 18+ months away. Trading range likely until next major data readout.

📉 Bear Case (25% probability)

Target: $35-$45

What could go wrong:

- ⚖️ Arbutus patent trial results in major damages or injunctions - potentially existential for Spikevax/mRESVIA

- 😰 Q4 earnings show worse-than-expected cash burn, 2028 breakeven pushed out

- 🦠 Norovirus vaccine Phase 3 remains on FDA clinical hold

- 📉 RSV market share losses to GSK and Pfizer's established sales forces

- 🏛️ FDA leadership instability under Commissioner Makary creates approval delays

- 💸 Broader biotech selloff drags MRNA lower with sector

Critical support levels:

- 🛡️ $50: Major psychological support + gamma floor

- 🛡️ $45: Strongest gamma support level (2.47 net GEX)

- 🛡️ $40: Disaster scenario - break here signals serious trouble

Probability assessment: 25% because the Arbutus trial is a genuine binary risk that could materially impair Moderna's business. Regulatory headwinds under new FDA leadership add uncertainty.

Call Seller P&L Scenarios:

- Stock at $60 on July 17: Calls expire worthless = +$2.7M profit (100% ROI)

- Stock at $65 on July 17: Calls expire worthless = +$2.7M profit (100% ROI)

- Stock at $70 on July 17: Calls expire at-the-money = +$2.7M profit (breakeven area)

- Stock at $80 on July 17: Calls worth $10.00, loss = -$2.3M net (-46% ROI)

- Stock at $90 on July 17: Calls worth $20.00, loss = -$7.3M net (-170% ROI!)

💡 Trading Ideas

🛡️ Conservative: Buy the Dip on Support

Play: Wait for pullback to $48-50 gamma support zone for long entry

Why this works:

- ⏰ After 15.8% gap, stocks typically consolidate and test support

- 📊 $50 psychological level with positive gamma support creates natural floor

- 💰 Getting 7-10% discount from current price reduces risk significantly

- 🧬 Long-term thesis remains intact - oncology pipeline is genuinely promising

- ⚖️ Avoids chasing after the gap - patient entry improves risk/reward

- 🛡️ Set stop at $43 (next major gamma support) for defined risk

Action plan:

- 👀 Watch for pullback to $48-50 zone in coming weeks

- 🎯 If support holds, enter long with 2-3% position size

- ✅ Add on confirmation above $55 with strong volume

- 📊 Target: $60 (immediate resistance) then $65-70 if momentum builds

- ⏰ Hold through Q4 earnings if entering with proper position size

Risk level: Moderate | Skill level: Beginner-friendly

⚖️ Balanced: Post-Earnings Bull Put Spread

Play: After Q4 earnings (Feb 13-19), sell bull put spread to collect premium

Structure: Sell $50 puts, Buy $45 puts (March 20 expiration)

Why this works:

- 🎢 IV crush after earnings makes spreads cheaper to buy protection

- 📊 Defined risk spread ($5 wide = $500 max risk per spread)

- 🎯 Targets gamma support zone at $45-$50 - profit if stock stays above $50

- ⏰ 30 days to expiration after earnings gives time for position to work

- 💰 Collect premium if bullish thesis holds post-earnings

Estimated P&L:

- 💰 Collect ~$1.50-2.00 net credit per spread post-earnings

- 📈 Max profit: $150-200 if MRNA above $50 at March expiration

- 📉 Max loss: $300-350 if MRNA below $45 (defined and limited)

- 🎯 Breakeven: ~$48-48.50

Entry timing:

- ⏰ Wait 2-3 days post-earnings (by Feb 16-20) for full IV collapse

- 🎯 Only enter if stock trades $50+ (gives cushion to support)

- ❌ Skip if stock already below $48 (too close to short strike)

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

🚀 Aggressive: Copy the Institutional Trade - Sell July $70 Calls

Play: Mirror the institutional call seller - collect premium betting against $70

Structure: Sell July 17 $70 calls (COVERED against 100 shares or as part of stock position)

Why this could work:

- 🐋 Following $2.7M institutional trade - smart money setting ceiling expectations

- 💰 Collect ~$5.40 per contract ($540 per 100 shares) in premium

- 📊 30% upside buffer before assignment risk

- ⏰ 176 days of theta decay working in your favor

- 🎯 Market implies ~30-35% chance of reaching $70 - betting against it

Why this is RISKY:

- 💸 Unlimited loss if naked: Stock could rally to $80, $90, $100 on positive trial data

- ⚖️ Arbutus trial binary: Favorable ruling could send stock parabolic

- 🧬 Pipeline optionality: Any positive Phase 3 readout could gap stock through $70

- 📈 Momentum risk: Stock already breaking out - don't fight the trend

- ⚠️ ONLY do this as covered call against existing shares or as part of collar strategy

CRITICAL WARNING - Only attempt if you:

- ✅ Already own MRNA shares you're willing to sell at $70

- ✅ Understand covered call mechanics and assignment risk

- ✅ Can afford to miss upside above $70 if stock explodes

- ✅ Have margin account if doing this as part of spread/collar

- ❌ DO NOT sell naked calls on biotech stocks - one trial readout can bankrupt you

Risk level: HIGH (potential for significant loss if naked) | Skill level: Advanced only

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⚖️ Arbutus Patent Trial (March 2026): Potential $100B+ damages exposure over lipid nanoparticle technology. Arbutus seeking injunctions against Spikevax AND mRESVIA. Unfavorable ruling could be catastrophic for Moderna's core products. This is THE single biggest near-term risk.

-

📉 Declining COVID Revenue: COVID vaccine sales down 45% YoY and continuing to decline. This remains 50%+ of revenue while oncology pipeline is 18+ months from commercialization. Cash burn continues at ~$3B annually.

-

🏛️ Regulatory Headwinds: FDA leadership instability under Commissioner Makary creating "slipping" review timelines. RFK Jr. revoked $500M in BARDA mRNA vaccine funding. FDA shifting away from immunogenicity as sufficient benchmark for mRNA vaccine approval.

-

🦠 Pipeline Setbacks: CMV vaccine failed Phase 3 in October 2025; HSV and VZV programs discontinued; Norovirus vaccine on FDA clinical hold since February 2025 due to Guillain-Barre case. mRNA is not a "silver bullet."

-

📊 RSV Market Competition: mRESVIA facing intense GSK and Pfizer competition with established sales forces and PBM formulary access. Late-mover disadvantage significant.

-

💰 Cash Burn Reality: Annual operating expenses of ~$4.9B in 2026 against $8.1B cash reserve. 2028 breakeven target requires successful oncology commercialization. Last 12-month revenue growth of -56.4%; operating margin of -157.3%.

-

🎢 Post-Gap Volatility: After 15.8% single-day move, expect heightened volatility and potential profit-taking. Biotech gaps often retrace 30-50% within weeks. Don't chase the move.

-

🤝 Analyst Sentiment: Consensus rating is HOLD (1 buy, 15 hold, 4 sell) with average price target of $28-37 - stock now trading ABOVE consensus targets after rally. This creates downgrade risk.

🎯 The Bottom Line

Real talk: Someone just sold $2.7M worth of call options betting that MRNA WON'T reach $70 by July. After the stock gapped 15.8% on melanoma vaccine data, institutional money is taking chips off the table - not because they're bearish long-term, but because they think the good news is priced in at $53.74.

What this trade tells us:

- 🎯 Sophisticated player expects CONSOLIDATION through July - not a continued rally to $70+

- 💰 They're confident enough to collect $2.7M betting against a 30% further move

- ⚖️ The timing (day after catalyst) shows they see the pop as unsustainable in the near term

- 📊 They structured at $70 strike which aligns with the upper implied move range

- ⏰ July 17th expiration captures Q4 earnings, Arbutus trial, and several pipeline readouts

This is NOT a "sell everything" signal - it's a "the easy money has been made" signal.

If you own MRNA:

- ✅ Consider taking some profits at $53-55 levels after the 15.8% gift

- 📊 If holding, set MENTAL STOP at $45 (major gamma support) to protect gains

- ⏰ Don't get greedy - waiting for $70 could mean watching it retrace to $45 first

- 🎯 If you're bullish long-term, consider selling covered calls at $65-70 to generate income

- 🛡️ The institutional call sale suggests smart money sees near-term ceiling around current levels

If you're watching from sidelines:

- ⏰ Don't chase the gap - wait for pullback to $48-50 support for better entry

- 🎯 Q4 earnings (Feb 13-19) will be the next major catalyst - wait for clarity

- ⚖️ Arbutus trial (March) is binary risk that could move stock 20%+ either direction

- 📈 Long-term thesis is improving with oncology data - but patience pays in biotech

- ⚠️ At $53.74, you're paying for success that's 18+ months away from monetization

If you want to copy the institutional trade:

- 🎯 Only sell $70 calls if you ALREADY OWN shares (covered call strategy)

- ⚠️ NEVER sell naked calls on biotech - one trial result can create unlimited losses

- 💰 Consider bull put spreads ($50/$45) for defined-risk bullish exposure

- ⏰ Wait for post-earnings IV crush before entering premium-selling strategies

Mark your calendar - Key dates:

- 📅 January 23 (Thursday) - Weekly options expiration (high volatility expected)

- 📅 February 13-19 - Q4 2025 earnings report

- 📅 February 20 - Monthly OPEX (+/-16% implied move window)

- 📅 March 2026 - Arbutus patent trial

- 📅 March 20 - Triple witch quarterly expiration

- 📅 July 17, 2026 - Expiration of this $2.7M call sale trade

Final verdict: Moderna's long-term oncology story is genuinely exciting - the 49% melanoma risk reduction data validates the mRNA platform for cancer. BUT, at $53.74 after a 15.8% gap with the Arbutus trial looming, declining COVID revenue, and 18+ months until oncology revenue, the risk/reward favors patience over chasing.

The $2.7M institutional call sale is a CLEAR signal: smart money is selling premium at the peak, not buying calls for more upside.

Be patient. Let the gap settle. Wait for support. The oncology story will still be here when you get a better entry price.

This is biotech - the only thing certain is volatility. Manage your risk accordingly. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The biotech sector carries unique risks including clinical trial failures, regulatory setbacks, and patent litigation. The trade analyzed may have portfolio-level hedging considerations not visible from the single transaction. Always do your own research and consider consulting a licensed financial advisor before trading. Never sell naked calls on biotech stocks.

About Moderna: Moderna is a commercial-stage biotech that specializes in mRNA technology with applications across infectious disease, oncology, cardiovascular disease, and rare genetic diseases. The company maintains 35+ development candidates in clinical studies and has a market cap of $19.46 billion in the Biological Products industry.