🐻 MSFT: $50M Bear Call Spread Says Tech Giant Topped Out at $570!

📅 December 9, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped a massive $50M bet that Microsoft won't break above $570 through December 2026! This is a huge year-long bear call spread that collected $24M in premium, signaling that big money thinks MSFT's rally is capped despite all the AI hype. With the stock at $490.55, this trade suggests the upside is limited to 16% while protecting against unlimited losses above $675.

🏢 Company Overview

Microsoft Corporation (MSFT) is one of the world's largest software companies, developing and licensing consumer and enterprise software across three core business segments. The company's productivity solutions include Office 365, Exchange, and LinkedIn; its cloud infrastructure spans Azure and SQL Server; and its personal computing devices include Windows, Xbox, and Surface.

Key Stats:

- 💰 Market Cap: $3.65 trillion (2nd largest company globally)

- 🏢 Industry: Prepackaged Software

- 👥 Employees: 228,000 worldwide

- 📍 HQ: Redmond, Washington

- 📊 Current Price: $490.55

💰 The Option Flow Breakdown

📊 What Just Happened

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Premium | Volume | OI | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|

| 2025-12-09 | 10:23:02 | MSFT | SELL | CALL | 2026-12-18 | $570 | $37M | 12K | 12K | MSFT20261218C570 |

| 2025-12-09 | 10:23:02 | MSFT | BUY | CALL | 2026-12-18 | $675 | $13M | 12K | 12K | MSFT20261218C675 |

Strategy Details:

- 🎯 Strategy Type: Bear Call Spread

- 💵 Total Premium: $50M ($37M sold - $13M bought)

- 💰 Net Credit Collected: $24M

- 📈 Max Profit: $24M (if MSFT stays below $570 at expiration)

- 📉 Max Loss: $24M (if MSFT rises above $675 at expiration)

- 🎢 Confidence Level: HIGH (94% strategy confidence)

- 🔥 Z-Score: 9.18 on the short leg, 7.94 on the long leg - EXTREMELY UNUSUAL

🤓 What This Actually Means

Real talk: This isn't some retail trader dabbling with a few contracts. This is institutional-sized money - 11,689 contracts on each leg - betting that Microsoft's AI-fueled rally has run out of steam. Here's the translation:

The Setup:

- 🎪 Sold the $570 strike calls (collected $37M) - betting MSFT stays below this level

- 🛡️ Bought the $675 strike calls (paid $13M) - capping maximum loss if wrong

- 💵 Pocketed $24M upfront as credit

What They're Saying: This trader thinks MSFT will trade between $490 (current) and $570 (16% upside) over the next year. They're basically saying: "Microsoft is a great company, but at $3.65 trillion market cap, the easy money's been made. The stock might grind higher, but it's not exploding past $570."

The Risk/Reward:

- ✅ If MSFT stays below $570 by December 18, 2026: Keep all $24M

- ⚠️ Between $570-$675: Profits start shrinking

- ❌ Above $675: Max loss of $24M kicks in

This is a defined-risk bearish bet with a full year for the thesis to play out. The fact that someone put $50M to work on this trade tells you big money is nervous about MSFT's valuation at current levels.

📈 Technical Setup & Chart Analysis

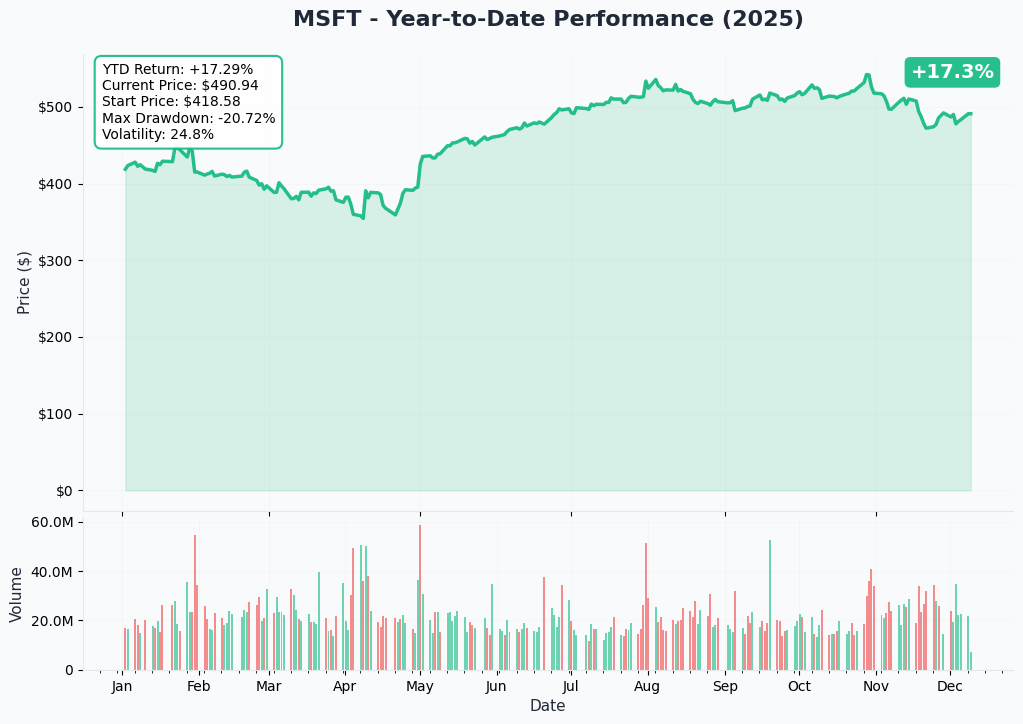

YTD Performance

Microsoft has delivered a solid +17.49% return over the past year, climbing from around $418 to the current $490.55 level. The stock hit a peak of $555.45 in the 52-week range before pulling back. The chart shows the rally has been driven by explosive AI and cloud growth, but recent price action suggests momentum is cooling. The 30-day performance shows a slight decline of -1.17%, with market cap sliding from $3.70T to $3.65T - a sign that institutional money might be taking chips off the table.

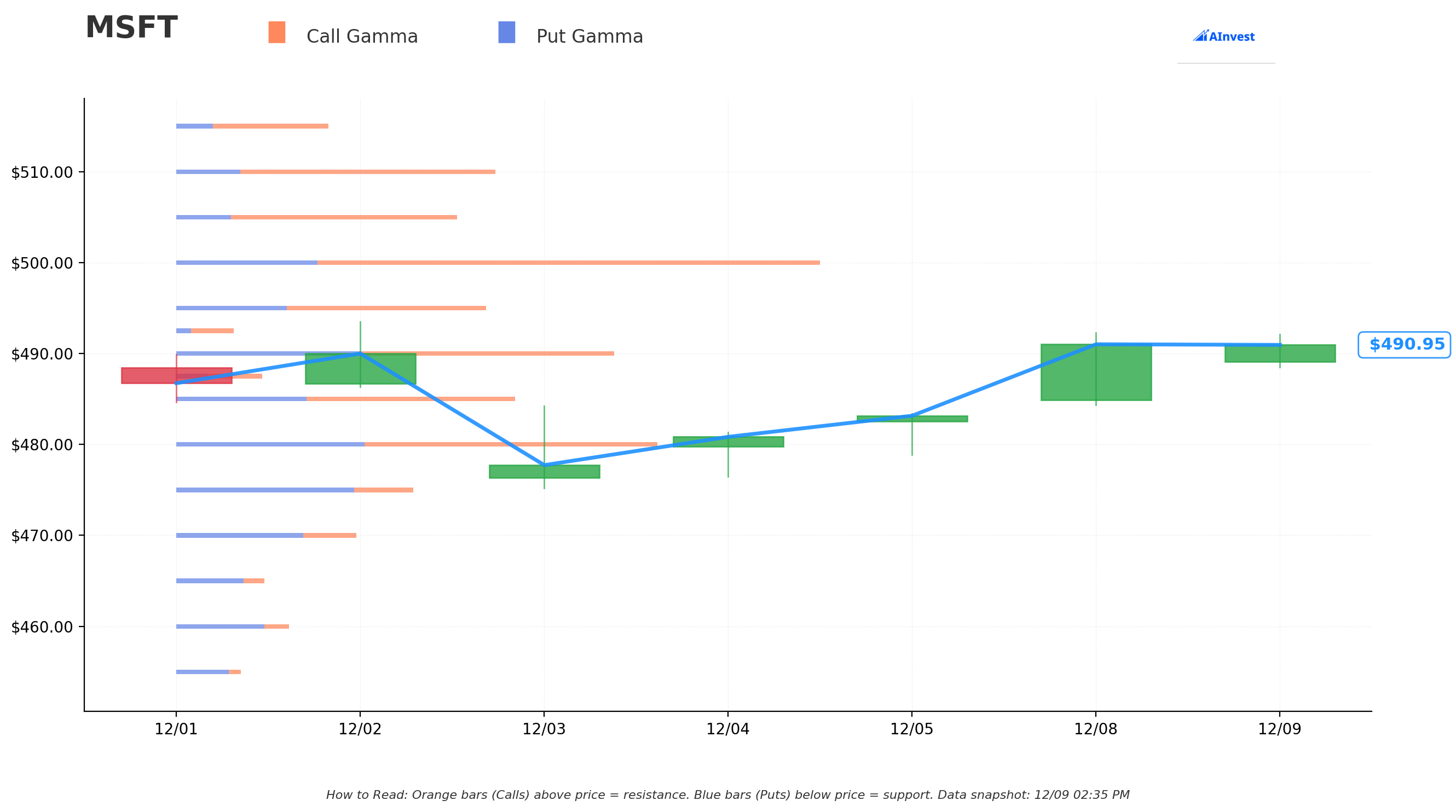

🎯 Gamma-Based Support & Resistance Analysis

Current Price: $490.72

Key Support Levels (Put Gamma = Blue Bars):

The gamma profile shows us where options market makers are positioned and where the stock might find natural support:

- 🔵 $490 Support - Strongest support level with 45.3M total gamma (7.1M net bullish). This is RIGHT at current price, making it a critical pivot point. If MSFT holds here, bulls maintain control.

- 🔵 $485 Support - Secondary support at 35.1M total gamma (8.1M net bullish). A break below $490 would likely find buyers at this level.

- 🔵 $480 Support - Solid floor at 49.9M total gamma (10.9M net bullish). This zone has heavy put protection, suggesting institutional hedging.

- 🔵 $475 Support - Deeper support at 24.6M total gamma (-12.3M net bearish). Note the negative net gamma here - if MSFT slides to $475, selling could accelerate.

Key Resistance Levels (Call Gamma = Orange Bars):

- 🟠 $495 Resistance - Immediate resistance at 32.0M total gamma (9.2M net bullish). Just 0.9% above current price - first test for bulls.

- 🟠 $500 Resistance - MAJOR resistance at 66.4M total gamma (37.3M net bullish). This is the STRONGEST gamma level in the entire chain. Huge call selling here creates a ceiling. Breaking $500 would be significant.

- 🟠 $505 Resistance - Secondary resistance at 28.7M total gamma (17.5M net bullish).

- 🟠 $510 Resistance - Strong resistance at 32.8M total gamma (19.7M net bullish).

- 🟠 $520 Resistance - Upper resistance at 29.9M total gamma (21.3M net bullish). Getting here would require a major catalyst.

Net GEX Bias: The summary shows total call GEX of 383.4M vs put GEX of 210.4M, creating a bullish bias from a gamma perspective. However, the concentrated resistance at $500 suggests that level will be tough to crack.

What This Means for Traders: The gamma profile supports the bear call spread thesis! The massive resistance at $500 (66.4M gamma) and progressive resistance zones from $495-$520 suggest MSFT will struggle to maintain momentum above current levels. The trade's $570 short strike is well above all major gamma resistance, giving the position significant breathing room. The support at $490 is holding for now, but a break below would target $485 then $480.

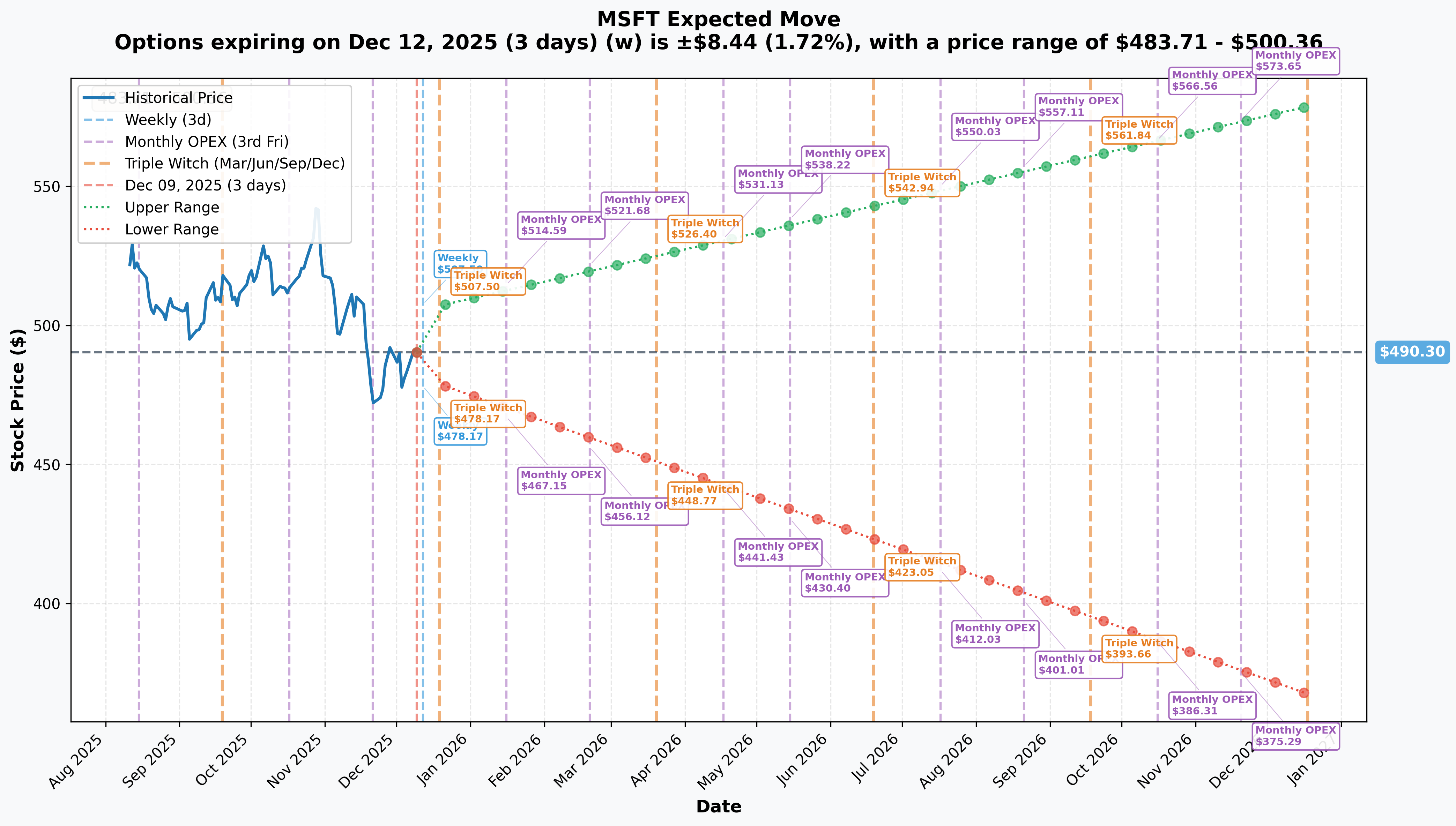

📊 Implied Move Analysis

The options market is pricing in specific movement expectations across multiple timeframes:

Weekly (December 12, 2025 - 3 days out):

- 📈 Implied Move: ±1.72% ($8.44)

- 🎯 Range: $483.71 - $500.36

- ⚡ What It Means: Market expects MSFT to trade in a tight 16-point range this week. Relatively calm expectations.

Monthly OPEX (December 19, 2025 - 10 days out):

- 📈 Implied Move: ±2.71% ($13.28)

- 🎯 Range: $478.78 - $507.11

- 🎪 What It Means: Triple Witch expiration! The upper end at $507 aligns with gamma resistance, suggesting $500-$510 is the ceiling for year-end.

Yearly LEAPS (December 18, 2026 - 374 days out):

- 📈 Implied Move: ±19.26% ($94.41)

- 🎯 Range: $367.33 - $578.77

- 🔮 What It Means: This is CRITICAL! The options market prices MSFT's 1-year expected range at $367-$579. The bear call spread's $570 short strike sits RIGHT at the top of this range. The trader is betting MSFT doesn't exceed the market's 1-year implied move on the upside.

Progressive OPEX Expectations: Looking at the OPEX labels through 2026, we see the implied upper range gradually expanding:

- December 2025: $507

- January 2026: $515

- February 2026: $522

- March 2026: $526

- June 2026: $543

- September 2026: $562

- November 2026: $574

Notice how the progression tops out around $574 by November 2026? The bear call spread's $570 strike is positioned right at this ceiling, suggesting the trader is aligned with market expectations that MSFT won't sustainably break above $570 over the next year.

🎪 Catalysts

⏰ Upcoming Catalysts (Next 6 Months)

Q2 FY2026 Earnings - February 4, 2026 🗓️ This is THE major near-term catalyst to watch! According to Nasdaq's earnings calendar, MSFT reports after market close.

- 💰 Consensus Revenue: $80.24 billion

- 📊 Consensus EPS: $3.92 (range: $3.56-$4.12) per TipRanks

- ☁️ Azure Growth Guidance: 37% at constant currency per Microsoft Investor Relations

Key Metrics to Watch:

- Azure revenue acceleration/deceleration - This drives the stock

- Microsoft Cloud revenue approaching $50B+ quarterly run rate

- Copilot monetization metrics - How much revenue is AI actually generating?

- Capital expenditure trajectory - Investors nervous about $140B capex burn

- OpenAI investment impact on margins - Q1 saw $3.1B loss from OpenAI investments

Copilot Monetization Acceleration (Q2-Q4 FY2026): Per Business of Apps, over 90% of Fortune 500 now use Microsoft 365 Copilot. Early customers expanded seats by 10x over 18 months. CEO Satya Nadella expects AI to be the fastest division to reach $10 billion revenue run rate. GitHub Copilot has surpassed 1 million subscribers. This is the key monetization story for 2026.

Infrastructure Expansion (2026): According to Microsoft's earnings call, the Fairwater datacenter in Wisconsin comes online in 2026, scaling to 2 gigawatts. Total AI capacity increasing 80%+ in FY2026. Datacenter footprint doubling over next two years. This supports Azure growth but raises questions about ROI timeline.

Microsoft 365 Pricing Updates - July 1, 2026: Per Microsoft 365 Blog, commercial pricing updates for Microsoft 365 suite with expanded AI, security, and management capabilities. Price increases could boost margins but risk customer pushback.

✅ Recent Catalysts (Already Happened)

Q1 FY2026 Earnings - October 29, 2025 💚 MSFT crushed it! Revenue of $77.7B (+18% YoY), EPS $4.13 (+23% YoY). However, results were impacted by a $3.1 billion loss from OpenAI investments, reducing EPS by $0.41. Azure beat estimates with strong growth. Microsoft Cloud revenue hit $49B (+26% YoY). Commercial RPO reached nearly $400B (+50% YoY). Per CNBC, the stock initially popped on the results.

OpenAI Partnership Restructuring - December 2025 🤝 Per OpenAI announcement, Microsoft secures 27% stake in OpenAI's for-profit entity valued at ~$135 billion. Microsoft retains exclusive IP rights and Azure API exclusivity until AGI. IP rights extended through 2032, now includes post-AGI models. OpenAI commits to purchase incremental $250 billion of Azure services. This is massive for Azure revenue visibility but creates dependency risks. According to ET Edge Insights, Microsoft becomes the largest external shareholder.

Anthropic AI Investment - November 2025 🤖 Per TS2 Tech, $15 billion AI deal bringing Anthropic's Claude models to Azure. Locks in up to $30 billion of Azure compute demand. Azure becomes the only cloud offering both OpenAI and Anthropic models. Competitive moat growing stronger!

Microsoft Ignite 2025 - November 18-20 🚀 According to Microsoft Azure Blog, Claude Sonnet 4.5, Opus 4.1, and Haiku 4.5 added to Microsoft Foundry. Foundry ecosystem now includes 11,000+ models from OpenAI, xAI, Meta, Mistral AI, and others. This positions Azure as the most comprehensive AI platform.

Analyst Activity (October-December 2025):

- ✅ Wells Fargo: Raised price target to $675 from $650, reaffirmed Overweight (October 30, 2025) per Benzinga

- ❌ Rothschild & Co: Downgraded price target to $500 from $560 (November 18, 2025) - This is significant! Right after Ignite, a major firm cut their target to $500, suggesting caution on valuation.

🎲 Price Targets & Probabilities

Based on gamma levels, implied move analysis, and upcoming catalysts, here's how MSFT could trade through the bear call spread's December 18, 2026 expiration:

🚀 Bull Case: $540-$565 (25% probability)

Path: February earnings blow out estimates with Azure growth reaccelerating to 40%+, Copilot revenue hits $2B+ run rate, and enterprise AI adoption accelerates faster than expected. FTC antitrust concerns fade. Stock grinds higher through 2026.

Targets:

- Break above $500 gamma resistance (66.4M GEX) on earnings momentum

- Next stops at $510 and $520 gamma levels

- Progressive implied move targets: $522 (Feb), $543 (Jun), $562 (Sep)

- Upper Target: $565 - Just shy of the $570 bear call spread strike

Why It Could Happen:

- Copilot monetization inflecting - 90% of Fortune 500 already using it per Business of Apps

- $250B OpenAI Azure services commitment provides multi-year revenue visibility per OpenAI

- Azure growing 39% - best-in-class cloud growth per Microsoft IR

- Only cloud offering both OpenAI and Anthropic models = competitive moat

- Analyst consensus at $628 avg price target with 74 Buy ratings per Benzinga

Impact on Bear Call Spread: ⚠️ Profitable but narrowing. At $565, the spread still expires worthless, keeping the full $24M credit. But getting close to the danger zone at $570.

⚖️ Base Case: $475-$520 (50% probability)

Path: MSFT trades sideways to slightly higher as Azure growth remains strong (35-37%) but massive capex spending ($140B in FY2026) weighs on sentiment. Copilot adoption continues but monetization slower than bulls hope. Stock oscillates between gamma support at $475-$490 and resistance at $500-$510.

Targets:

- Hold $480-$490 support zone (49.9M and 45.3M total GEX)

- Test $500 resistance multiple times but fail to sustain above it

- Trade range: $475-$520 for most of the year

- Base Target: $495-$510 range

Why This Is Most Likely:

- December monthly implied move: $479-$507 range aligns with this view

- Massive gamma resistance at $500 (66.4M GEX) acts as ceiling

- Rothschild downgrade to $500 shows some institutional caution per Benzinga

- $3.65T market cap limits upside without exceptional growth

- P/E of 35.25 is premium - vulnerable to multiple compression per Stock Analysis

- FTC antitrust investigation ongoing, creating overhang per Bloomberg

Impact on Bear Call Spread: ✅ Perfect scenario. Spread expires completely worthless, trader keeps full $24M credit.

🐻 Bear Case: $420-$465 (25% probability)

Path: February earnings disappoint as Azure growth decelerates below 35%, Copilot revenue underwhelms, and $140B capex spend triggers margin compression concerns. Macro recession fears or tech selloff accelerates. FTC antitrust action intensifies. Stock breaks below $475 support.

Targets:

- Break below $475 gamma support (negative net GEX = -12.3M accelerates selling)

- Test $450-$465 zone (lower implied move range for early 2026)

- Downside Target: $420-$450 - back to mid-2025 levels

Why It Could Happen:

- Q1 FY2026 showed $3.1B loss from OpenAI investments (-$0.41 EPS) per Microsoft IR

- $140B FY2026 capex (+58% YoY) with unclear ROI timeline per CreditSights

- 50% of capex on short-lived GPU/CPU assets = depreciation risk per Sherwood News

- Copilot monetization challenges - customers questioning $30/user value per Lighthouse Global

- FTC investigation could drag on for years with potential structural remedies per Sam Expert

- Google Cloud gaining share (32% growth) vs Azure per Stansberry Research

Impact on Bear Call Spread: ✅✅ Dream scenario for the trade. Big decline means both strikes expire worthless, trader keeps full $24M credit with zero risk of assignment.

💡 Trading Ideas

🛡️ Conservative: The "Let Pros Lead" Strategy

Why This Works: Don't fight institutional flows! The $50M bear call spread suggests big money is nervous about MSFT above $570. For conservative traders, the safest play is to either avoid MSFT entirely or position for limited upside.

The Setup:

- Wait for MSFT to test $500 resistance (66.4M gamma ceiling)

- If it fails to break and hold above $500, sell a February 2026 $520 call for income

- Collect premium betting stock stays below $520 (well below the $570 ceiling)

- This gives you 2 months and room for the stock to appreciate 6% before you're tested

Position Sizing:

- Risk no more than 2% of portfolio on this trade

- 1 contract per $50K of portfolio value

- Use stop loss at $510 if MSFT breaks out above $500 with conviction

Probability of Success: ~70% (stock needs to fail at $500 resistance)

What Could Go Wrong:

- Blowout February earnings could launch MSFT past $520

- Unexpected catalyst (major acquisition, breakthrough product) changes thesis

- You'd have to buy back calls at a loss or risk assignment

⚖️ Balanced: The "Gamma Ranger" Strategy

Why This Works: Play the range! Gamma analysis shows strong support at $480-$490 and resistance at $500-$510. Trade the boundaries.

The Setup:

- Buy side: Purchase MSFT shares or March 2026 $485 calls if stock pulls back to $480-$485 support

- Sell side: Sell covered calls or naked calls at $510 strike when/if stock rallies to $495-$500

- Target 3-4% moves in each direction within the $480-$510 channel

- Rinse and repeat until stock breaks out of range

Example Trade:

- Buy 100 MSFT shares at $485 (if it dips from current $490)

- Immediately sell 1 January 2026 $510 covered call for ~$8-10

- Collect premium while capped at 5.2% upside ($485→$510)

- If stock drops further, sell February $510 call to lower cost basis

- If assigned at $510, take profit and wait for next dip to $480-$485

Probability of Success: ~60% (base case scenario of range-bound trading)

What Could Go Wrong:

- Stock breaks below $475 support and heads to $450 (you're holding depreciating shares)

- Stock rips past $510 and you miss the upside (but you still profit, just capped)

- Whipsaw action causes you to buy high and sell low in choppy markets

🚀 Aggressive: The "Anti-Spread" Bull Strategy

Why This Works (Contrarian Alert!): Fade the $50M institutional trade! While big money is betting MSFT tops out at $570, there's a contrarian case that AI monetization surprises to the upside. If you believe MSFT can break $600, you can position for an explosive move.

The Setup: This is the opposite of the bear call spread - it's a BULL call spread targeting the upside.

- Buy March 2026 $500 calls (after the Feb earnings catalyst)

- Sell March 2026 $560 calls to finance it

- This creates a defined-risk bet that MSFT breaks out to $520-$560 range post-earnings

- Max profit if stock reaches $560 by March

- Max loss is your net debit paid

Example Trade:

- Buy 1 March 2026 $500 call for ~$25

- Sell 1 March 2026 $560 call for ~$8

- Net cost: $17 per share ($1,700 per contract)

- Max profit: $43 per share if MSFT at or above $560 at expiration

- Breakeven: $517

- Risk/Reward: Risk $1,700 to make $4,300 (2.5:1 reward)

Sizing:

- Risk no more than 5% of portfolio (this is aggressive!)

- Understand you could lose 100% of premium paid

- Only do this if you have strong conviction MSFT breaks out

Probability of Success: ~35% (requires breakout above all major resistance and sustained move)

What Could Go Wrong:

- Stock stays below $500 and both calls expire worthless (lose full $1,700)

- Bearish case plays out and MSFT drops to $450 (lose full premium)

- You could be right directionally but wrong on timing (need move within 3 months)

Why Take This Risk:

- Copilot revenue could inflect dramatically - Nadella targeting $10B run rate per Business of Apps

- $250B OpenAI services commitment unprecedented per OpenAI

- Wells Fargo $675 price target suggests some bulls see $600+ potential per Benzinga

- If Azure reaccelerates to 42%+ growth, stock could rip higher

- You're positioned BELOW the $570 institutional ceiling, giving you room to be right

⚠️ Risk Factors

Let's be real about what could derail any bullish thesis on MSFT:

🔴 Regulatory Nightmare

FTC Antitrust Investigation (Active and Growing): Per Bloomberg, the FTC under Trump-appointed Chair Andrew Ferguson confirmed "big tech is one of the main priorities of the Trump-Vance FTC" in March 2025. The investigation focuses on:

- OpenAI investment structure designed to avoid antitrust reviews per Sam Expert

- Bundling Office products with cybersecurity and cloud services per ProPublica

- Cloud software licensing rules that favor Azure over competitors

Why This Matters: Investigation could take YEARS to resolve. Potential outcomes include structural remedies (forced divestitures), behavioral constraints (can't bundle products), or massive fines. This creates an overhang on the stock and could limit valuation multiples.

💸 Capex Spending Out of Control

$140 Billion Question: According to CreditSights, MSFT's FY2026 capex is projected at $140 billion (+58% YoY), triple FY2024 levels. Q1 FY2026 capex of $34.9 billion (+74% YoY) blew past expectations per DCD.

The Problem:

- CFO reversed guidance - previously said capex growth would slow in H2 FY2026, now expects acceleration per Sherwood News

- Nearly 50% of spending on short-lived GPU/CPU assets = rapid depreciation

- ROI timeline unclear - how long before this spending translates to profits?

- Margin compression risk if AI revenue doesn't scale as fast as spending

Investor Fear: Throwing money into a black hole with uncertain returns. If February earnings show margin pressure or slowing Azure growth, watch out below.

🤖 Copilot Monetization Mystery

The Adoption Paradox: Per Business of Apps, 90% of Fortune 500 use Microsoft 365 Copilot. Sounds amazing, right? But here's the catch:

- Most enterprises in pilot/phased rollout - NOT full deployment per CNBC

- Customer quote per Lighthouse Global: "Am I getting $30 of value per user per month? The short answer is no"

- Estimated $400M in direct Copilot revenue in 2024 vs $281.7B total revenue = rounding error

- Adoption is there, but are customers actually paying $30/user/month at scale?

The Risk: Market is pricing in Copilot being a $10B+ business soon. If monetization disappoints in February earnings, stock could get hammered.

🏦 OpenAI Dependency

$3.1 Billion Wake-Up Call: Q1 FY2026 showed a $3.1 billion loss from OpenAI investments, reducing EPS by $0.41 per Microsoft IR. Yes, MSFT gets 27% of OpenAI's upside, but they also take losses and have $250B in Azure services commitments.

What Could Go Wrong:

- OpenAI burns more cash than expected (Sam Altman raising TRILLIONS for chip factories)

- Microsoft no longer has right of first refusal on OpenAI compute per OpenAI

- AGI definition disputes could create commercial uncertainty

- Competitor models (Anthropic, Google Gemini) erode OpenAI's moat

📉 Valuation Risk

Simple Math:

- P/E Ratio: 35.25 (premium to market) per Stock Analysis

- Market Cap: $3.65 trillion (2nd largest company on Earth)

- Recent Performance: Down 1.17% over 30 days despite strong fundamentals

The Problem: At $3.65T, MSFT needs to generate MASSIVE earnings growth to justify further multiple expansion. The stock isn't cheap. In a recession or market correction, high P/E stocks get crushed first. Any disappointment on Azure growth, margin compression, or Copilot monetization could trigger a derating to 28-30x P/E = $420-$450 stock price.

🌍 Macro & Competition

Cloud Market Share Battle:

- AWS still leads at 29% share per Statista

- Azure at 20-22% (2nd place)

- Google Cloud growing faster (32% vs Azure's 39%) and closing gap per Stansberry Research

Economic Risks:

- Enterprise IT spending cuts in recession would hammer Azure and M365

- Strong dollar headwinds (already seeing 1-2% revenue impact)

- Gaming (Xbox) vulnerable to consumer spending weakness

🎯 The Bottom Line

Real talk: This $50M bear call spread is one of the most fascinating institutional trades I've seen on MSFT in a while. Here's how to think about it:

The Bull Argument: Microsoft is THE best-positioned company to monetize AI. They have Azure growing at 39%, exclusive deals with both OpenAI ($250B services commitment) and Anthropic ($30B compute lock-in), 90% Fortune 500 copilot adoption, and nearly $400B in commercial RPO. The fundamentals are undeniably strong. If Copilot revenue inflects in 2026 like Nadella predicts (fastest to $10B run rate), and Azure maintains 35%+ growth, this stock could absolutely grind toward $540-$565 over the next year.

The Bear Argument: But here's what keeps me up at night - $140B in capex spending (+58% YoY) with unclear ROI, Copilot monetization that's more promise than reality ($400M revenue vs $281B total), a $3.1B OpenAI loss in Q1, and an ongoing FTC antitrust probe. At 35x P/E and $3.65T market cap, there's limited margin for error. The Rothschild downgrade to $500 RIGHT after the bullish Ignite conference tells you some smart money is nervous. The concentrated gamma resistance at $500 and the 1-year implied move topping out at $579 suggest the market agrees with the bear call spread thesis.

My Take on the Trade: The $570/$675 bear call spread is a sophisticated, well-thought-out trade. The trader collected $24M in premium betting MSFT doesn't exceed $570 by December 2026. Based on:

- 1-year implied move: $367-$579 (their $570 strike is AT the upper bound)

- Progressive OPEX targets topping out at $574 by November 2026

- Massive gamma resistance at $500 that's hard to break

- Fundamental risks (capex, margins, monetization, regulation)

I'd give this trade a 65-70% probability of success. The base case is MSFT trades $475-$520 for most of 2026, gradually grinding toward $540-$560 by year-end but failing to break decisively above $570. The trader keeps the full $24M.

Action Plan Based on Your Position:

📊 If You Own MSFT:

- Hold through February 4 earnings

- If stock fails at $500 resistance post-earnings, consider trimming 25-30% and selling covered calls at $520-$540 strikes

- Set mental stop at $475 - break below suggests bearish case accelerating

- Don't get greedy chasing it above $550 - risk/reward deteriorates above there

👀 If You're Watching MSFT:

- Wait for a dip to $480-$485 gamma support zone to initiate

- Alternative: Wait for $500 breakout and HOLD above for 3+ days, then chase to $520

- Best entry: Post-February earnings pullback if it happens

- Mark your calendar: February 4, 2026 after market close - this will set the tone

🐻 If You're Bearish:

- The $50M institutional trade validates your thesis

- Consider February $510 puts if stock rallies to $500-$505

- Or mimic the bear call spread on a smaller scale: Sell March $540 calls, buy March $600 calls

- Don't get too aggressive - fundamentals are still strong, just expensive

Final Wisdom: This trade isn't saying Microsoft is a bad company - it's saying the stock is fairly valued to slightly overvalued at current levels, and the explosive upside is likely behind us. At $3.65T market cap, the law of large numbers matters. The easy money from $300 to $500 is done. The next $100 move will be a grind, not a moonshot.

Trade smart, size appropriately, and remember: Options are risky derivatives. You can lose 100% of your premium. Never bet money you can't afford to lose.

Disclaimer: This analysis is for educational and informational purposes only. It is not financial advice. Options trading involves substantial risk of loss and is not suitable for all investors. The author may hold positions in securities mentioned. Always conduct your own research and consult with a licensed financial advisor before making investment decisions.

Analysis Date: December 9, 2025 MSFT Price at Analysis: $490.55 Data Sources: Option flow data, gamma analysis, implied volatility calculations, and public company filings.