💎 Microsoft $9.4M Collar Trade - Institutional Risk Management Before AI Infrastructure Moment! 🛡️

📅 December 10, 2025 | 🔥 Defensive Strategy Detected

🎯 The Quick Take

A sophisticated institution just executed a $9.4M collar strategy on Microsoft at 10:53:23 AM - simultaneously selling 1,300 calls at the $545 strike and buying 1,300 puts at the $450 strike, both expiring January 15, 2027. This classic risk reversal locks in downside protection while capping upside at $545, protecting a position worth approximately $622M. With MSFT trading at $478.97 and massive AI infrastructure investments still showing limited ROI signals, smart money is implementing portfolio insurance while maintaining exposure to Microsoft's AI transformation. Translation: Institutions are hedging their mega-cap cloud bets before the next earnings cycle!

📊 Company Overview

Microsoft Corporation (MSFT) dominates enterprise software and cloud infrastructure while leading the charge in commercial AI deployment:

- Market Cap: $3.66 Trillion (2nd largest globally after Apple)

- Industry: Enterprise Software & Cloud Services

- Current Price: $478.97

- 52-Week Range: $344.79 - $555.45

- Primary Business: Office 365 productivity suite, Azure cloud infrastructure, Windows operating systems, LinkedIn, Xbox gaming, AI platforms (Copilot, GPT integration)

💰 The Option Flow Breakdown

The Tape (December 10, 2025 @ 10:53:23):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:53:23 | MSFT | BID | SELL | CALL $545 | 2027-01-15 | $4.8M | $545 | 1,300 | 323 | 1,300 | $478.97 | $36.72 |

| 10:53:23 | MSFT | ASK | BUY | PUT $450 | 2027-01-15 | $4.6M | $450 | 1,300 | 4,900 | 1,300 | $478.97 | $35.52 |

🤓 What This Actually Means

This is a zero-cost collar (risk reversal) - the ultimate institutional hedge! Here's what happened:

- 💸 Net premium: Approximately $0.20 debit per share ($4.8M calls sold - $4.6M puts bought = $200K net outlay)

- 🛡️ Downside protection: $450 put floor provides protection below $450 (6% cushion from current $479)

- 🚫 Upside cap: $545 call ceiling limits gains above $545 (14% above current price)

- ⏰ Long-dated protection: 401 days to expiration (13+ months) captures Q4 2024 earnings, all of 2025 earnings, and most of 2026

- 📊 Position size: 1,300 contracts represents 130,000 shares worth ~$62.2M at current prices

- 🏦 Classic institutional structure: Nearly zero-cost trade (sold call premium funds put purchase) while maintaining core long position

What's really happening here: This trader owns a SUBSTANTIAL MSFT position accumulated during the AI rally, likely from the $350-$450 range. Now, with MSFT near recent highs but facing execution risks on its $80B AI capex program, they're implementing a collar to protect against 6%+ downside while accepting a 14% upside cap. The structure says: "I believe in Microsoft's AI story long-term, but I need insurance against near-term disappointments while I wait for the $13B AI revenue run rate to materialize."

The nearly-zero net cost (just $200K on a $62M position = 0.3% insurance premium) is the hallmark of sophisticated risk management - using natural options pricing to hedge for "free."

Strategic message: This isn't bearish - it's prudent portfolio management. The trader maintains full upside to $545 (another 14% gain) while completely eliminating downside below $450. If you believe MSFT will trade $450-$545 over the next 13 months, this is the perfect structure.

📈 Technical Setup / Chart Check-Up

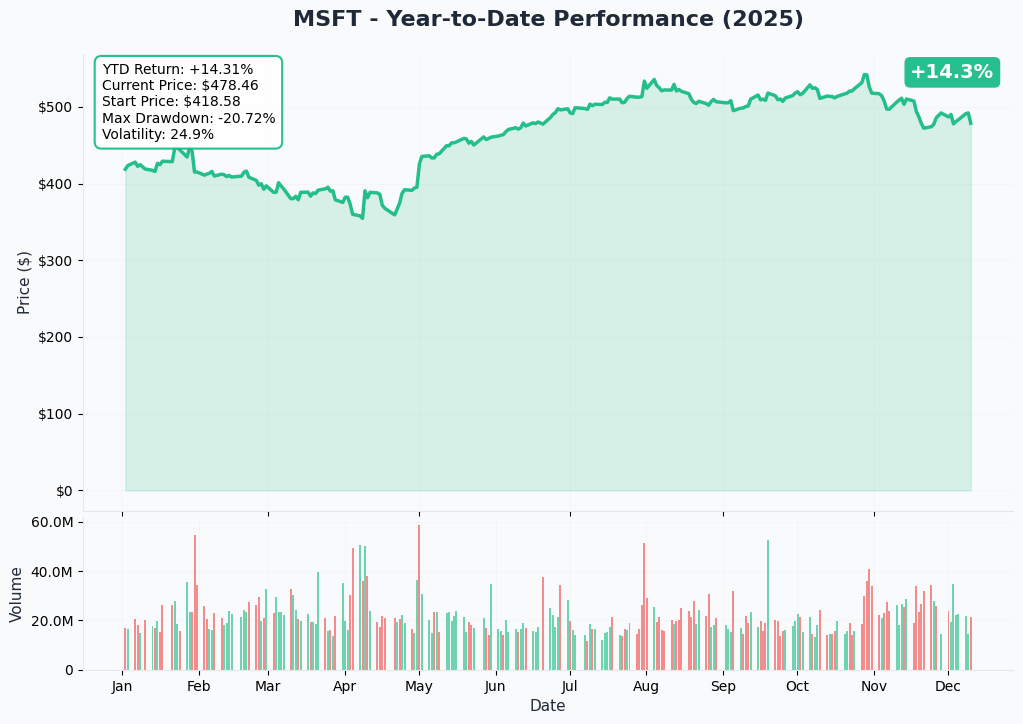

YTD Performance Chart

MSFT is showing measured strength in 2025, currently trading at $478.97 after touching all-time highs of $555.45 earlier this year. The stock demonstrated resilience during market volatility, maintaining support above the critical $450 level (exactly where this put is struck - not coincidental).

Key observations:

- 📈 Solid base: Built strong support at $450-$475 range over recent months

- 💪 Recovery mode: Bounced from October lows near $400, now consolidating near $480

- 🎢 Volatility contained: Relatively stable compared to high-growth tech peers

- 📊 Range-bound: Trading in well-defined $450-$550 channel - perfect for collar structure

- ⚠️ Overhead resistance: Previous highs at $555 creating natural ceiling near the $545 strike

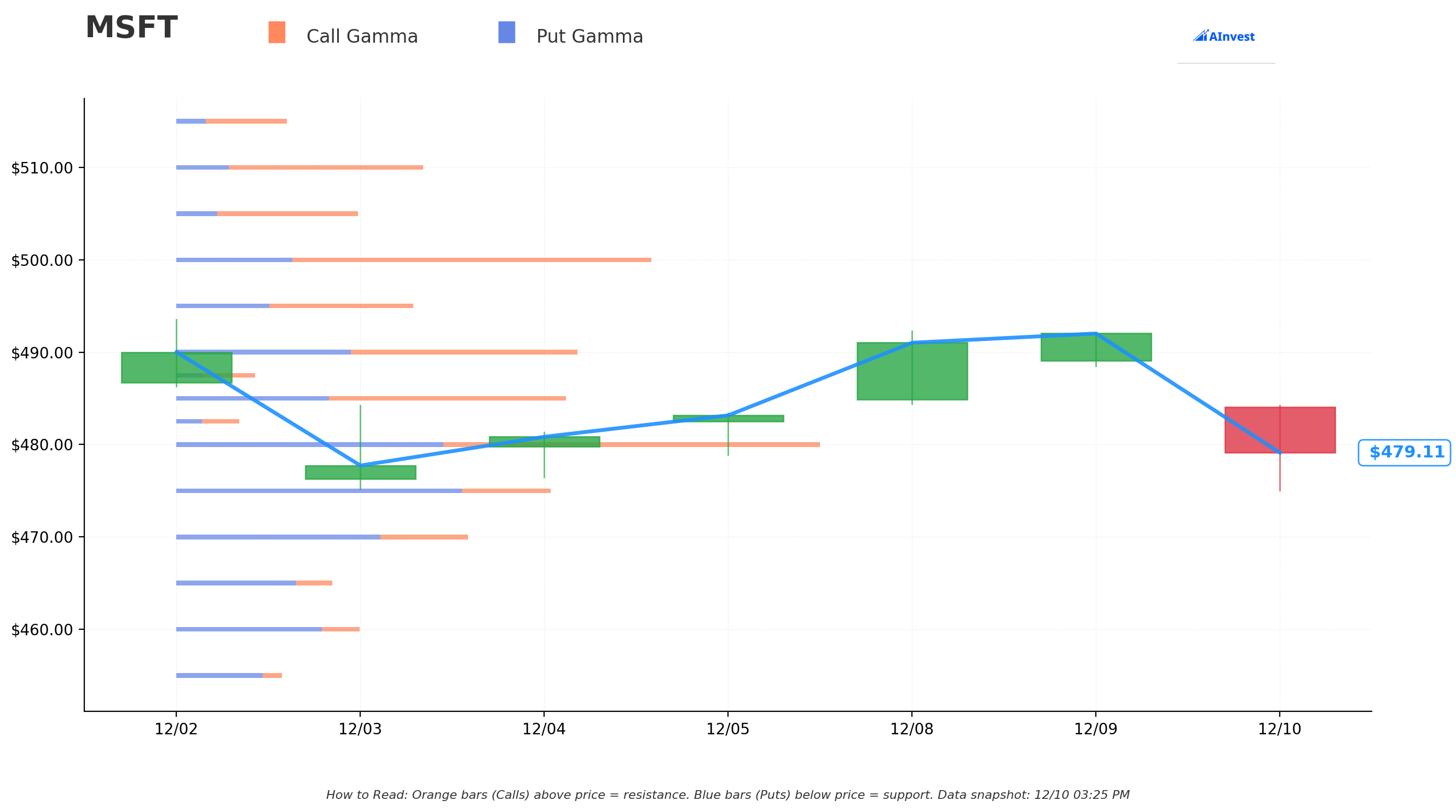

Gamma-Based Support & Resistance Analysis

Current Price: $479.50

The gamma exposure map reveals critical price magnets that align perfectly with this collar strategy:

🔵 Support Levels (Put Gamma Below Price):

- $475 - Immediate support with 36.08B total gamma exposure (strongest nearby floor - 0.9% below)

- $470 - Secondary support at 28.03B gamma (2% below current)

- $450 - MASSIVE structural floor with 23.81B put gamma (6.2% below - EXACTLY where the put is struck!)

🟠 Resistance Levels (Call Gamma Above Price):

- $480 - Immediate ceiling with 62.02B gamma (STRONGEST RESISTANCE - just overhead at 0.1%)

- $485 - Secondary resistance at 37.65B gamma (1.1% above)

- $490 - Major ceiling zone with 38.90B gamma (2.2% above)

- $500 - Extended resistance at 45.98B gamma (4.3% above)

- $520 - Upper band resistance with 22.00B gamma (8.4% above)

What this means for the collar strategy: The collar is PERFECTLY positioned around natural gamma zones! The $450 put strike sits at a major support level with significant put gamma (institutions protecting there), while the $545 call strike is well above current resistance levels at $520. This suggests the trader:

- Expects MSFT to consolidate in the $450-$520 range near-term

- Positioned the put at major institutional support ($450)

- Set the call strike above visible resistance to maximize retained upside

Net GEX Bias: Bullish (322.45B call gamma vs 246.46B put gamma) - Overall positioning remains constructive, supporting the long-biased collar strategy.

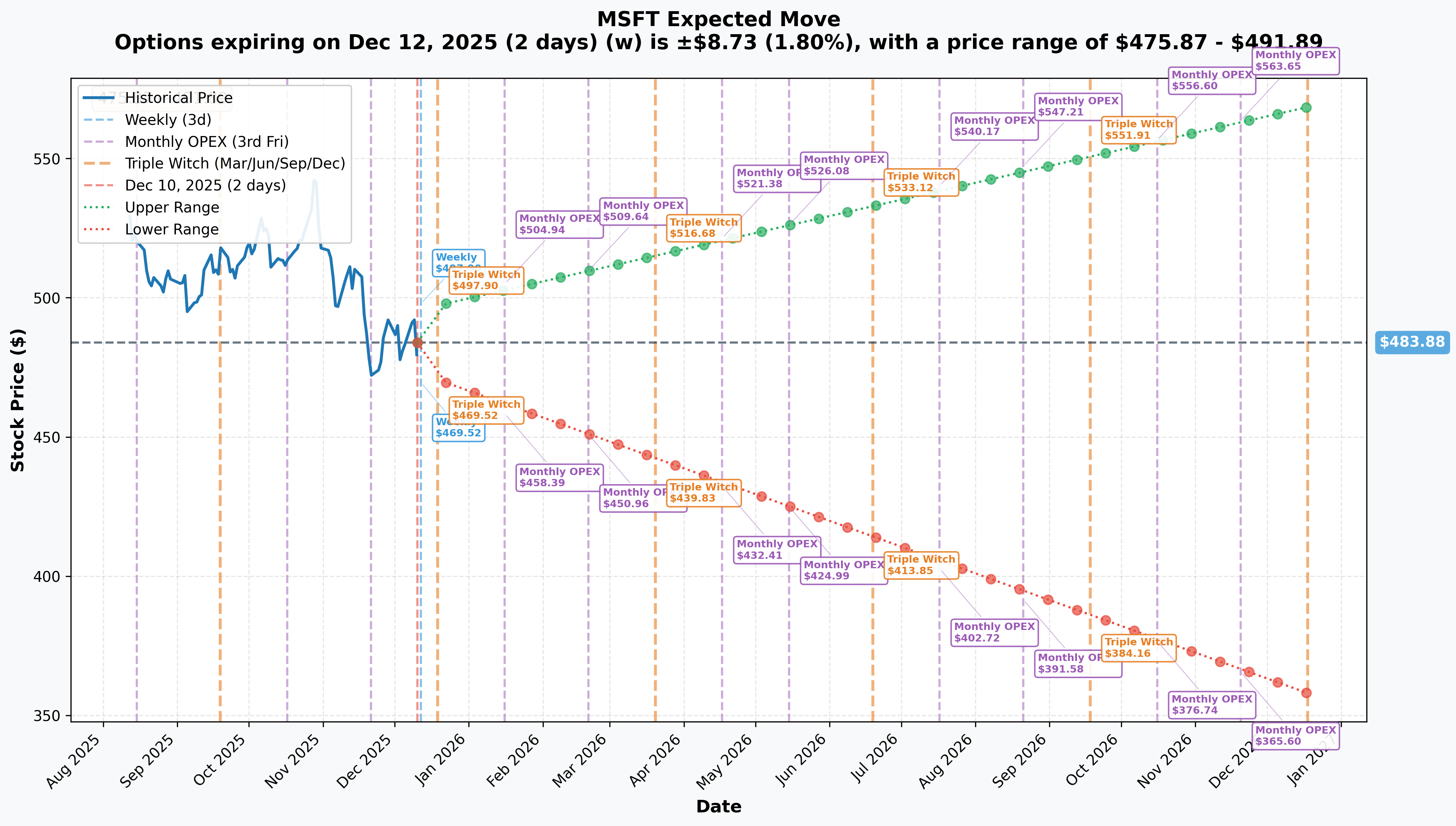

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 12 - 2 days): ±$8.73 (±1.8%) → Range: $475.87 - $491.89

- 📅 Monthly OPEX (Dec 19 - 9 days): ±$13.43 (±2.78%) → Range: $470.45 - $497.31

- 📅 Quarterly Triple Witch (Dec 19 - 9 days): ±$13.43 (±2.78%) → Range: $470.45 - $497.31

- 📅 Yearly LEAPS (Dec 2026 - 373 days): ±$92.97 (±19.21%) → Range: $357.87 - $568.54

Translation for regular folks: Options traders are pricing in a 1.8% move ($9) by December 12th for weekly expiration, and a 2.78% move ($13) through December 19th monthly OPEX. Looking out to the 2027 expiration (when this collar expires), the market expects a MASSIVE 19.21% range ($93) - meaning MSFT could trade anywhere from $358 to $569.

The collar structure captures this uncertainty perfectly:

- Upper LEAP range: $568.54 (market thinks possible) vs $545 call strike (where trader caps gains)

- Lower LEAP range: $357.87 (market thinks possible) vs $450 put strike (where trader floors losses)

The trader is giving up the extreme tails (potential move to $570+ on AI monetization success, or drop to $360 on AI disappointment) to eliminate risk in the "disaster scenario" below $450 while keeping most upside to $545.

Key insight: The 19.21% annual implied volatility reflects genuine uncertainty about MSFT's $80B AI infrastructure investment ROI timeline. Smart money is hedging this binary outcome.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

December 19, 2025 - Triple Witch OPEX 📊

Major quarterly options expiration creates volatility as large institutional positions roll or close. With significant open interest clustering around $475-$500 strikes, expect elevated volume and potential range expansion. The $450 put floor becomes increasingly important as year-end positioning intensifies.

Year-End Portfolio Rebalancing (December 20-31) 💼

Institutional investors will rebalance mega-cap tech holdings for 2026, potentially creating volatility in MSFT. The collar structure protects against tax-loss selling or unexpected rotation out of cloud infrastructure names.

🚀 Near-Term Catalysts (Q1-Q2 2026)

Q2 FY2026 Earnings - Late January 2026 (Expected January 28-29) 📊

Microsoft's next earnings report represents THE critical catalyst for validating the AI investment thesis. Based on Q1 FY2026 guidance, consensus expectations and key metrics:

- 📊 Revenue: $79.5B-$80.6B guided (vs $77.7B in Q1) - driven by Azure and AI services

- 💰 Azure Growth: 37% constant currency guided (down from 40% in Q1 - deceleration watch!)

- 🤖 AI Revenue Run Rate: Must show progress from $13B annual run rate (up 175% YoY) toward $15B+ to justify valuation

- 💻 Microsoft 365 Copilot: Seat growth and ARPU expansion critical - watching for 100M+ users

- 📈 Gross Margins: Azure margins compressed to 71% in Q1 FY2025 - need stabilization signal

- 🎮 Gaming Integration: Activision Blizzard contribution tracking toward $23.4B annual run rate

Upside surprise potential: Microsoft 365 pricing increases (July 2026) and expanding Copilot adoption could drive revenue beat. OpenAI partnership restructuring (Microsoft secured 27% stake valued at $135B with $250B Azure commitment) provides massive long-term revenue visibility.

Downside risk factors: Any disappointment in Copilot monetization (some enterprises report insufficient $30/month ROI), Azure deceleration below 35%, or capex increase beyond $80B could trigger selloff. The collar's $450 put floor protects against this scenario.

Historical precedent: MSFT typically moves 2-4% post-earnings even on beats - the collar captures this range perfectly ($450-$545 allows for normal volatility).

Microsoft 365 Copilot Chat Launch - By March 2026 🤖

Announced at Ignite 2025, Copilot Chat expands to Outlook, Word, Excel, PowerPoint for users without full Copilot licenses:

- 📧 Inbox and calendar analysis in Outlook

- 🤝 Agent Mode for multi-step task collaboration

- 💰 Could accelerate adoption without requiring full $30/month tier

- 🎯 Success metric: Engagement rates and conversion to paid Copilot subscriptions

GPT-5 Integration - Rolling Out Now 🚀

OpenAI's latest GPT-5 model rolling out across Microsoft 365 Copilot and Copilot Studio:

- 🧠 Enhanced reasoning and multimodal capabilities

- 📊 Early customer feedback on performance vs GPT-4 Turbo

- ⚠️ Any quality issues or user disappointment could stall Copilot momentum

- 💪 Success here validates Microsoft's exclusive OpenAI partnership value

Windows 11 Migration Wave - Ongoing Through Mid-2026 💻

Windows 10 reached end of support in October 2025, creating massive upgrade catalyst:

- 📈 Windows 11 market share: 53.7% as of November 2025 (up from 45% in Q3)

- 💼 Remaining Windows 10 users: 42.7% (hundreds of millions of enterprise PCs)

- 🏢 Enterprise migrations are "10-12 points behind" previous cycles - slow but steady revenue

- 💰 Extended Security Updates (ESU) program generating recurring revenue

- ⏰ Timeline: Major enterprise migrations expected through mid-2026 (within collar window)

📊 Strategic Catalysts (H2 2026)

Microsoft 365 Pricing Update - July 1, 2026 💵

Commercial pricing changes effective July 2026 with expanded AI, security, and management capabilities:

- 📈 Expected to boost Microsoft 365 Commercial ARPU (average revenue per user)

- 🎯 Follows previous consumer price increases (42% for Personal, 31% for Family in January 2025)

- ⚠️ Risk: Customer pushback if value perception doesn't match price increases

- 💰 Opportunity: Could add $2-3B annual revenue if successfully implemented

OpenAI Partnership Revenue Acceleration 🤝

The $135B OpenAI stake with $250B Azure commitment represents transformative long-term catalyst:

- 💼 OpenAI revenue share increased to $865.8M in first three quarters of 2025 (vs $493.8M all of 2024)

- 🎯 Exclusive access to models through 2032 (including post-AGI)

- 📊 First major deployment milestones in H2 2026 will validate partnership value

- ⚠️ Risk: OpenAI can now work with third parties under restructured agreement

⚠️ Risk Catalysts (Negative)

FTC Antitrust Investigation - Ongoing Into 2026 🏛️

Microsoft faces expansive FTC probe that could impact cloud and AI businesses:

- 🔍 Scope: Software licensing practices, cloud computing business, AI operations, OpenAI funding

- ⚖️ Focus: Market power leverage, licensing restrictions, data center access

- 📅 Status: Proceeding confidentially; no public timeline for resolution

- 💥 Potential Impact: Licensing practice changes, cloud pricing restrictions, OpenAI relationship modifications

- 🎯 Worst case: Multi-billion dollar fines, forced unbundling of services

EU Antitrust Settlement - Expected 2026 🇪🇺

Microsoft negotiating settlement to avoid fines over bundling Teams with Office 365:

- 📋 Terms: Sell Teams separately, reduce Office pricing without Teams, improve interoperability

- 💸 Financial Impact: Potential revenue reduction from unbundling (estimated $500M-$1B annually)

- ⏰ Timeline: Settlement expected in 2026

- ✅ Upside: Avoids multi-billion dollar fine if settled favorably

AI Monetization Execution Risk 🤖

Microsoft's massive $80B AI capex faces ROI pressure:

- 💰 Customer value concerns: Some enterprises report insufficient $30/month Copilot ROI

- 📊 Adoption friction: Only 82% of Microsoft customers adopted Copilot despite 90% Fortune 500 penetration

- 🎯 Pricing pressure: New $21/month tier could reduce ARPU expectations

- 🏗️ Capacity constraints: $80B may not suffice for demand; Microsoft may "adjust infrastructure in some areas"

- 📉 Margin pressure: Azure gross margins compressed to 71% as AI infrastructure scales

Azure Competition Intensifying ☁️

While Azure holds 20% market share (vs AWS 29%, Google Cloud 13%), competitive threats mounting:

- 📉 AWS maintains leadership with mature service portfolio

- 📈 Google Cloud showing 32% growth; operating income doubled in Q2 2025

- 🆕 Oracle investing heavily (4% market share gains targeting enterprise)

- 🤖 Open source AI: Models like Meta's Llama 3 reducing dependency on Microsoft/OpenAI

- 💰 Price wars: Cloud pricing pressure could compress margins further

🎲 Scenarios & Probabilities

Using gamma levels, implied move data, and catalyst timeline through January 2027 expiration:

📈 Bull Case (30% probability)

Target: $545+ (Call Strike Hit or Exceeded)

How we get there:

- 💪 Earnings consistently beat with Azure maintaining 35%+ growth through 2026

- 🚀 Copilot adoption accelerates to 150M+ users; pricing increases stick without churn

- 🤖 AI revenue run rate reaches $20B+ by end of 2026, validating $80B infrastructure investment

- 💰 OpenAI partnership delivers first major revenue milestones in H2 2026

- 📊 Regulatory investigations settle without major business model changes

- 🌐 Market share gains continue - Azure reaches 22-23% vs AWS declining to 27%

- 📈 Windows 11 migration drives $5B+ incremental revenue from ESU and hardware refresh

- 🎮 Gaming integration exceeds expectations with $25B+ annual run rate

Key metrics needed:

- Copilot monthly active users >150M with improving monetization

- Azure gross margins stabilize at 70%+ (stop the bleeding)

- AI revenue mix reaches 15-20% of total revenue

- Successful GPT-5 integration driving Copilot engagement

Collar P&L in Bull Case:

- Stock at $545 on Jan 15, 2027: Calls exercised, shares called away at $545

- Profit on collar: ($545 - $479) × 130,000 shares = $8.6M gain

- Total return: 13.8% over 13 months (10.5% annualized) - respectable but capped

- Opportunity cost: If stock reaches $580 (upper implied range), trader misses $4.6M in additional gains

Probability assessment: 30% requires strong but achievable execution. MSFT has demonstrated ability to beat expectations, and AI tailwinds are real. Regulatory risks create headwinds but unlikely to derail core business.

🎯 Base Case (50% probability)

Target: $450-$545 Range (Collar Fully Captured)

Most likely scenario:

- ✅ Earnings meet or slightly beat consensus with Azure growth decelerating to 30-35% range

- 📱 Copilot adoption continues but monetization remains mixed - slow grind to profitability

- ⚖️ AI revenue grows to $15-17B run rate by end of 2026 - solid but not spectacular

- 🤝 OpenAI partnership progresses but major revenue inflection delayed to 2027

- 🇪🇺 Regulatory settlements reached with minor business impact ($500M-$1B revenue)

- 🔄 Trading in well-defined $450-$520 range for most of 2026

- 💤 Market awaits clearer AI ROI signals before rewarding multiple expansion

- 📊 Azure competes effectively but doesn't meaningfully gain share vs AWS

This is the collar's perfect scenario: Stock consolidates in the $450-$545 range, trader maintains full position, downside completely protected, upside preserved up to $545. The near-zero cost means the trader essentially gets free insurance while waiting for AI thesis to materialize.

Key range dynamics:

- 🛡️ $450 put floor: Provides absolute downside protection - eliminates tail risk

- 🚀 $545 call ceiling: Retains 14% upside potential - plenty of room for appreciation

- 💰 Net cost: $0.20/share ($200K total) = 0.3% insurance premium for 13 months

Collar P&L in Base Case:

- Stock at $500 on Jan 15, 2027: Both options expire worthless

- Profit on collar: ($500 - $479) × 130,000 shares = $2.73M gain

- Cost of insurance: -$200K (net premium paid)

- Net profit: $2.53M (4.4% return over 13 months = 4.1% annualized)

- Risk eliminated: Full protection below $450 (zero drawdown possible)

Why 50% probability: Stock has demonstrated strong support at $450-$475 and faces natural resistance at $500-$520 gamma levels. Fundamentals solid but not explosive. Most likely path is steady appreciation with occasional volatility - exactly what the collar is designed for.

📉 Bear Case (20% probability)

Target: Below $450 (Put Floor Protects)

What could go wrong:

- 😰 Multiple earnings misses or Azure deceleration below 25% growth - AI skepticism grows

- 🚨 Copilot adoption stalls; enterprises cancel subscriptions citing poor ROI

- 💸 $80B capex fails to translate to revenue - margin compression without growth

- 🏛️ FTC forces major business model changes - Teams unbundling, cloud pricing caps

- 🇨🇳 Geopolitical tensions escalate - China revenue (15% of total) disappears

- 💥 Broader tech selloff drags mega-caps lower (recession fears, Fed policy error)

- 🤖 OpenAI partnership encounters major problems - model quality issues, deployment delays

- 📊 Azure loses share to AWS/Google Cloud as customers diversify

- 🔨 Break below $450 gamma support triggers cascade to $400-$420

Critical support levels:

- 🛡️ $475: Major gamma floor (36.08B) - initial defense

- 🛡️ $470: Secondary support (28.03B gamma)

- 🛡️ $450: MASSIVE floor (23.81B gamma) + PUT STRIKE - line in the sand!

- 🚨 Below $450: Trader fully protected - puts pay off dollar-for-dollar

Collar P&L in Bear Case:

- Stock at $400 on Jan 15, 2027: Puts worth $50/share

- Put profit: ($450 - $400) × 130,000 shares = $6.5M gain

- Stock loss: ($479 - $400) × 130,000 shares = -$10.3M loss

- Net loss: -$3.8M (6.1% drawdown vs -16.5% unhedged!)

- Protection value: Collar reduced loss by $6.5M (63% less pain than unhedged)

Extreme scenario (stock at $350):

- Unhedged loss: ($479 - $350) × 130,000 = -$16.8M (-26.9% drawdown)

- With collar: ($450 - $350) × 130,000 = $13M put gain, -$16.8M stock loss = -$3.8M (same as $400!)

- Protection value: Collar eliminated ALL incremental losses below $450!

Probability assessment: Only 20% because requires multiple negative catalysts. MSFT's business fundamentals remain strong (Azure growing, Office 365 dominant, diversified revenue). Even in bear case, the $450 put floor makes this scenario MANAGEABLE rather than catastrophic. The trader clearly thinks downside risk is real enough to warrant protection.

💡 Trading Ideas

🛡️ Conservative: Mirror The Institutional Collar (Lower Size)

Play: Implement scaled-down collar on existing MSFT long positions

Structure: For every 100 shares owned:

- Sell 1x Jan 2027 $545 Call (collect ~$3,672)

- Buy 1x Jan 2027 $450 Put (pay ~$3,552)

- Net credit: ~$120 per 100 shares (PAID to hedge!)

Why this works:

- ⏰ Nearly zero-cost insurance for 13 months - get PAID to reduce risk

- 📊 Defined risk structure ($450 floor) with retained upside to $545 (+14%)

- 🎯 Aligned with smart money positioning at identical strikes

- 🛡️ Protects against regulatory risks, AI monetization disappointments, macro selloffs

- 💰 Maintains exposure to AI thesis upside while eliminating tail risk

- ⚖️ Perfect for investors who believe in MSFT long-term but worried about near-term execution

Ideal for:

- 📈 Existing MSFT shareholders with unrealized gains who want to lock in profits

- 💼 Investors who can't stomach >10% drawdown but want cloud/AI exposure

- ⏰ Those willing to cap gains at $545 (still 14% upside!) for downside peace of mind

- 🧘 Risk-averse traders who sleep better knowing maximum loss is defined

When to enter:

- ✅ NOW if you own shares and want immediate protection

- 🎯 After any rally above $490 (get better call premium)

- ❌ Skip if you believe MSFT will exceed $570+ (you're capping too much upside)

Position sizing: Hedge 50-100% of MSFT holdings depending on risk tolerance

Risk level: Minimal (defined risk, nearly free) | Skill level: Intermediate

Expected outcome: Sleep well for 13 months knowing your downside is capped at $450 while keeping most upside to $545. Perfect for long-term investors who want to weather volatility.

⚖️ Balanced: Cash-Secured Put at the Floor

Play: Sell cash-secured puts at the collar's $450 strike for income

Structure: Sell Jan 2027 $450 Puts, collect ~$35.52/share ($3,552 per contract)

Why this works:

- 💰 Collect substantial premium ($3,552) for agreeing to buy MSFT at $450

- 🎯 Put strike aligned with major institutional support ($450 gamma floor)

- 📊 6% below current price provides margin of safety

- ⏰ 13-month timeline allows multiple quarters for AI thesis to develop

- 🛡️ Comfortable entry point if assigned - institutions protecting this exact level

- 💵 7.9% annualized return just for waiting to buy at better price

Estimated P&L:

- 💰 Collect: $3,552 premium per contract (7.9% return on $45,000 cash secured)

- 📈 Best case: MSFT stays above $450, keep premium, repeat trade

- 🎯 Assignment scenario: Acquire shares at $450, net cost $414.48 (current $479 - 13.5% discount!)

- 📉 Worst case: Stock at $400, assigned at $450, net cost $414.48 = -3.5% loss (vs -16.5% buying at $479!)

Risk management:

- 🎯 Only sell puts if you WANT to own MSFT at $450 (14% below current)

- 💵 Requires $45,000 cash per contract (margin requirements vary)

- ⚠️ Unrealized losses if MSFT drops sharply (but you wanted shares anyway!)

- 📊 Monitor $450 gamma support - if it breaks, consider rolling down

When to enter:

- ✅ NOW if you're bullish MSFT long-term but want better entry

- 🎯 After any spike above $490 (put premium increases with volatility)

- ⏰ Ideal for those sitting in cash waiting for pullback

Position sizing: 1-2 contracts per $100K cash (conservative income strategy)

Risk level: Moderate (naked put but cash-secured) | Skill level: Intermediate

Expected outcome: Either collect 7.9% premium and repeat, OR acquire MSFT at 13.5% discount to current price with 6% downside cushion. Win-win for patient capital.

🚀 Aggressive: Front-Run The Collar with Bull Call Spread

Play: Target the $450-$545 range with defined-risk leverage

Structure:

- Buy Jan 2027 $450 Calls (~$68/share)

- Sell Jan 2027 $545 Calls (~$37/share)

- Net debit: ~$31/share ($3,100 per spread)

Why this could work:

- 🎯 Profits from same $450-$545 range institutions are targeting

- 💰 Defined risk: Max loss $3,100, max gain $9,500 (3:1 reward/risk!)

- 📊 Leveraged exposure: Control $45,000 of MSFT for $3,100 (68% less capital)

- 🚀 Profits from any move above $481 (just 0.4% above current price)

- ⏰ 13 months allows plenty of time for AI catalysts to play out

- 💪 Avoids theta decay of near-term options - long-dated structure

Why this could backfire:

- 📉 Total loss if MSFT below $450: Entire $3,100 debit lost if AI thesis fails

- 🎯 Breakeven at $481: Stock must move just to break even (time decay risk)

- 💸 Opportunity cost: Tying up capital for 13 months vs shorter-term plays

- ⚠️ No dividends: Miss ~$3/share in dividends during holding period

- 🔨 Volatility collapse: If IV drops, spread value compresses even if MSFT flat

Estimated P&L:

- 💰 Cost: $3,100 per spread

- 📈 Max profit: $9,500 if MSFT above $545 (206% ROI!)

- 🎯 Breakeven: $481 (just $2 above current - achievable)

- 📊 50% profit: $4,750 gain if MSFT at $495 (3.3% move) = 153% ROI

- 💀 Total loss: $3,100 if MSFT below $450 (need 6%+ drop)

Probability analysis:

- 📈 Win: ~60% (stock just needs to stay above $481)

- 💰 Big win: ~30% (stock reaches $545+)

- 📉 Loss: ~20% (stock drops below $450 - bear case)

Risk management:

- 🎯 Take 50% profits at $495 (book $4,750 gain, reduce risk)

- 📊 Close if MSFT drops below $460 (preserve capital, accept small loss)

- ⏰ Monitor Q2 earnings closely (Jan 2026) - adjust if thesis changes

- ⚠️ Set mental stop at $450 break (collar support level)

When to enter:

- ✅ NOW if you're bullish but want defined risk

- 🎯 After pullback to $465-$470 (get better entry on long call)

- ❌ Skip if you need the capital for near-term opportunities

Position sizing: Risk only 2-5% of portfolio per spread (this is leveraged speculation)

Risk level: High (can lose 100% of debit) | Skill level: Advanced

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand bull call spreads and defined-risk mechanics

- ✅ Can afford to lose entire $3,100 debit (real possibility if MSFT disappoints)

- ✅ Comfortable with 13-month capital lockup

- ✅ Believe in MSFT AI thesis enough to risk capital

- 📊 Have successfully traded multi-month spreads before

Expected outcome: Likely profit if MSFT stays in expected $450-$545 range, with potential for 200%+ ROI if AI catalysts drive stock to call ceiling. But risk total loss if regulatory/execution issues push stock below $450 support.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q2 FY2026 Earnings in 6 weeks (Late January): Results expected January 28-29 represent CRITICAL test of AI monetization thesis. Azure growth guided at 37% (down from 40% in Q1) - further deceleration could trigger selloff. Copilot adoption and pricing commentary will move stock 3-5% either direction. Market expects $13B AI run rate to show acceleration - any disappointment magnified.

-

💸 $80B AI Capex with Limited ROI Visibility: Microsoft spending unprecedented $34.9B in Q1 FY2026 alone (up 74% YoY) on AI infrastructure. Azure gross margins compressed to 71% as infrastructure scales. If AI revenue doesn't accelerate proportionally, ROI concerns could crater valuation. Some enterprises reporting insufficient $30/month Copilot ROI - pricing power questioned.

-

🏛️ FTC Antitrust Investigation Escalating: Active probe into cloud licensing practices, AI operations, and OpenAI partnership proceeding confidentially with no resolution timeline. Potential outcomes: forced unbundling of services, cloud pricing restrictions, OpenAI relationship modifications. Worst case: multi-billion dollar fines plus structural business changes. EU Teams settlement (expected 2026) could cost $500M-$1B annual revenue.

-

⚖️ Azure Competition Intensifying from All Sides: While Azure holds 20% market share, AWS still dominates at 29% with mature ecosystem. Google Cloud growing 32% YoY with improving profitability. Open-source AI models (Meta Llama 3, Mistral) reducing dependency on Microsoft/OpenAI. Cloud pricing wars could compress margins further from already-pressured 71% levels.

-

🤖 Copilot Monetization Execution Risk: Despite 90%+ Fortune 500 adoption, only 82% of Microsoft enterprise customers have deployed Copilot. New $21/month tier (down from $30) signals pricing pressure. If enterprise adoption stalls or churn increases post-July 2026 price hikes, the entire AI growth thesis unravels. Requires 150M+ users by end of 2026 to justify current valuation - significant execution risk.

-

🇨🇳 Geopolitical and China Revenue Exposure: China represents 15-20% of historical revenue. Export restrictions, trade tensions, and push for domestic alternatives (Huawei, Alibaba Cloud) create ongoing tail risk. Any escalation could remove billions in revenue overnight with no warning. Taiwan/TSMC tensions add supply chain vulnerability.

-

🤝 OpenAI Partnership Restructuring Creates Uncertainty: While Microsoft secured 27% stake valued at $135B with $250B Azure commitment, new structure allows OpenAI to work with third parties and Microsoft to pursue independent AGI. This flexibility could dilute Microsoft's exclusive advantages. If OpenAI deploys alternative infrastructure or model quality disappoints, the partnership value proposition weakens.

-

📊 Valuation Stretched After Strong Run: From 52-week low of $344.79 to current $479, MSFT up 39% in 12 months. Trading at premium to historical averages on expectation of AI revenue acceleration. Limited margin of safety if execution stumbles. The collar's $450 floor represents only 6% downside cushion - real drawdown risk if multiple catalysts disappoint.

-

🔐 Cybersecurity and Operational Risks Escalating: Identity attacks surged 32% in H1 2025, processing 100 trillion+ daily signals. Azure vulnerabilities nearly doubled since 2020. Any major security breach could trigger enterprise customer losses and regulatory scrutiny. Windows 10 end-of-support issues and patch quality problems create reputational risks.

-

💰 Gamma Ceiling at $480 Creates Natural Resistance: Massive 62.02B call gamma at $480 (STRONGEST RESISTANCE) means market makers will systematically SELL into rallies to hedge exposure. This creates mechanical selling pressure just 0.1% above current price. Would need sustained buying to break through $485-$490 secondary resistance (37.65B gamma). Current technical setup suggests consolidation rather than breakout.

-

🎢 Collar Structure Caps Upside at Critical Level: The $545 call ceiling limits participation in true AI breakthrough scenario. If Copilot adoption explodes, Azure accelerates back to 45%+, and OpenAI generates major revenue surprises, stock could reach $570-$600 (upper implied range) but collar trader misses $50-$120/share in gains. This is the COST of insurance - giving up the extreme upside tail.

-

📉 Macro Recession Risk Eliminates Cloud Budget Growth: At $3.66T market cap, MSFT is highly exposed to enterprise IT spending cycles. Economic downturn would force cloud budget cuts even if Azure/Office 365 provide value. Historical pattern: MSFT drops 30-40% in recessions regardless of execution. The collar's $450 floor would be tested hard in macro selloff scenario.

🎯 The Bottom Line

Real talk: An institution just constructed a $9.4M collar on $62M of Microsoft stock - selling upside at $545 to fund downside protection at $450 for the next 13 months. This isn't bearish on MSFT's transformational AI opportunity. It's sophisticated risk management by holders who've watched the stock run from $345 to $555 and don't want to give back gains if execution stumbles.

What this trade tells us:

- 🎯 Sophisticated player expects MSFT to trade in well-defined $450-$545 range (14% upside, 6% downside from current)

- 💰 They're willing to CAP gains at $545 (giving up potential move to $570+) to ELIMINATE risk below $450

- ⚖️ The near-zero cost ($0.20/share net debit = 0.3% annual premium) shows they're using natural options pricing for "free" insurance

- 📊 Positioned at major gamma support ($450 floor) and above visible resistance ($545 well above $520 ceiling)

- ⏰ January 2027 expiration captures ALL major catalysts: Q2/Q3/Q4 FY2026 earnings, Microsoft 365 price hikes (July 2026), Copilot Chat launch, Windows 11 migration, OpenAI milestones

This is NOT a "sell Microsoft" signal - it's a "protect unrealized gains while maintaining AI exposure" signal.

If you own MSFT:

- ✅ Consider implementing same collar structure on 50-100% of holdings (nearly free insurance!)

- 📊 The $450 floor protects against regulatory risks, AI monetization disappointments, competition

- ⏰ Keep exposure to AI upside - $545 target is 14% above current price (plenty of room!)

- 🛡️ Perfect for long-term believers who can't stomach 15-20% drawdown waiting for AI ROI

- 🎯 Especially compelling if you bought below $400 - lock in 50%+ gains while staying long

If you're watching from sidelines:

- ⏰ Late January earnings represent next major catalyst - wait for volatility before entering

- 🎯 Pullback to $450-$465 range would be EXCELLENT entry (aligned with institutional support)

- 📈 Looking for confirmation: Azure maintaining 35%+ growth, Copilot adoption >125M users, AI revenue >$15B run rate

- 🚀 Longer-term (12-18 months), OpenAI partnership and Microsoft 365 pricing power could drive $550-$600

- ⚠️ Current $479 offers limited margin of safety - be patient for better entry

If you're bearish:

- 🎯 First major support at $475 (36.08B gamma), critical support at $450 (23.81B gamma wall)

- 📊 Sell cash-secured puts at $450 to get paid for waiting (7.9% annualized premium)

- ⚠️ Fighting MSFT's cloud dominance and AI positioning is dangerous - use defined-risk structures only

- 📉 Bear thesis requires multiple failures: AI monetization flop + regulatory disaster + competition surge

- ⏰ Post-earnings (February 2026) offers better timing if thesis confirmed

Mark your calendar - Key dates:

- 📅 December 19, 2025 - Triple Witch OPEX (volatility spike likely)

- 📅 January 28-29, 2026 - Q2 FY2026 earnings (CRITICAL AI monetization update)

- 📅 March 2026 - Copilot Chat launch (adoption acceleration test)

- 📅 July 1, 2026 - Microsoft 365 commercial price increases (pricing power test)

- 📅 H2 2026 - OpenAI first deployment milestones (partnership validation)

- 📅 January 15, 2027 - Collar expiration (13-month trade window closes)

Final verdict: Microsoft's transformation into an AI-first enterprise platform is REAL - $80B infrastructure investment, $135B OpenAI partnership, 90%+ Fortune 500 Copilot penetration, and Azure's 37%+ growth all validate the thesis. BUT, at $479 with significant regulatory uncertainty (FTC probe, EU settlement) and execution risks on AI monetization, the risk/reward favors PROTECTION over naked long exposure. The $9.4M institutional collar provides the blueprint: stay long, eliminate downside below $450, accept upside cap at $545.

This is smart money playing it safe while staying in the game. Follow their lead. 🛡️

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Collar strategies cap both downside risk AND upside potential - understand the trade-offs before implementing. The institutional trade reflects specific portfolio hedging needs that may not apply to retail investors. Past performance doesn't guarantee future results. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings and regulatory events create binary risks with potential for significant price gaps.

About Microsoft Corporation: Microsoft develops and licenses consumer and enterprise software including Office 365, Azure cloud infrastructure, Windows operating systems, LinkedIn, Xbox gaming, and AI platforms. With a market cap of $3.66 trillion, Microsoft is the world's second-largest company and a leader in cloud computing and artificial intelligence deployment.