💎 MU $1.9M Call Close - Smart Money Exits Before Earnings Thunder! ⚡

📅 December 10, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dumped $1.9 MILLION closing short calls in MU this morning at 09:35:31! This massive Buy-to-Close (BTC) trade covered 920 contracts of $300 strike calls expiring March 20th - unwinding a short position just 7 DAYS before Micron's critical Q1 FY2026 earnings on December 17th. With MU up 170% YTD at $252.41 and riding the AI memory supercycle, smart money is closing bearish bets at premium levels before the HBM earnings lottery. Translation: Someone who bet against MU is surrendering and taking their losses NOW rather than risk getting blown out if earnings explode!

📊 Company Overview

Micron Technology (MU) is one of the world's largest memory chip manufacturers riding the AI infrastructure wave:

- Market Cap: $284.1 Billion (semiconductor powerhouse)

- Industry: Semiconductors & Related Devices - Memory & Storage

- Current Price: $252.41 (near all-time highs of $260.58)

- Primary Business: DRAM memory chips, NAND flash storage, High Bandwidth Memory (HBM) for AI accelerators

What makes MU special: Micron is the ONLY U.S.-based major memory manufacturer, competing with South Korean giants SK Hynix and Samsung in the exploding HBM market that powers AI chips from Nvidia and AMD. With HBM supply completely sold out through 2026 and a $9.6 billion new factory in Japan breaking ground, Micron has transformed from commodity memory supplier to strategic AI infrastructure player.

💰 The Option Flow Breakdown

The Tape (December 10, 2025 @ 09:35:31):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:35:31 | MU | BID | BUY | CALL $300 | 2026-03-20 | $1.9M | $300 | 925 | 8,600 | 920 | $252.41 | $20.50 |

🤓 What This Actually Means

This is a Buy-to-Close (BTC) - meaning someone is EXITING a short call position! Here's the breakdown:

- 💸 Premium paid to close: $1.9M ($20.50 per contract × 920 contracts)

- 📈 Strike price: $300 is 18.9% above current price of $252.41

- ⏰ Critical timing: 100 days to expiration BUT earnings December 17th (just 7 days away!) changes everything

- 📊 Open Interest context: 8,600 existing contracts at this strike - this trader closing 10.7% of total OI

- 🏦 Institutional capitulation: Originally sold calls betting MU stays below $300, now buying them back at a loss

What's really happening here: This trader likely sold these $300 strike calls weeks or months ago when MU was trading lower (perhaps $220-230 range), collecting premium by betting MU wouldn't reach $300 by March. But with MU rallying from $102 in December 2024 to $252+ today (146% gain!), these calls have become DANGEROUSLY in-the-money territory with massive earnings risk 7 days away. Rather than risk unlimited losses if earnings send MU to $280-300+, they're paying $20.50 per share NOW to close the position before the December 17th earnings explosion.

Think of it like this: They initially collected maybe $5-8 per call, but now forced to buy back at $20.50 - taking a $12-15 loss per contract or roughly $1.1M-1.4M total realized loss. OUCH. But if MU gaps to $280 on earnings, those calls could be worth $30-40+, turning this into a $2M+ disaster.

Key insight: When short call sellers capitulate BEFORE earnings, it signals they're genuinely scared of upside. This is BULLISH - short covering removes overhead resistance!

📈 Technical Setup / Chart Check-Up

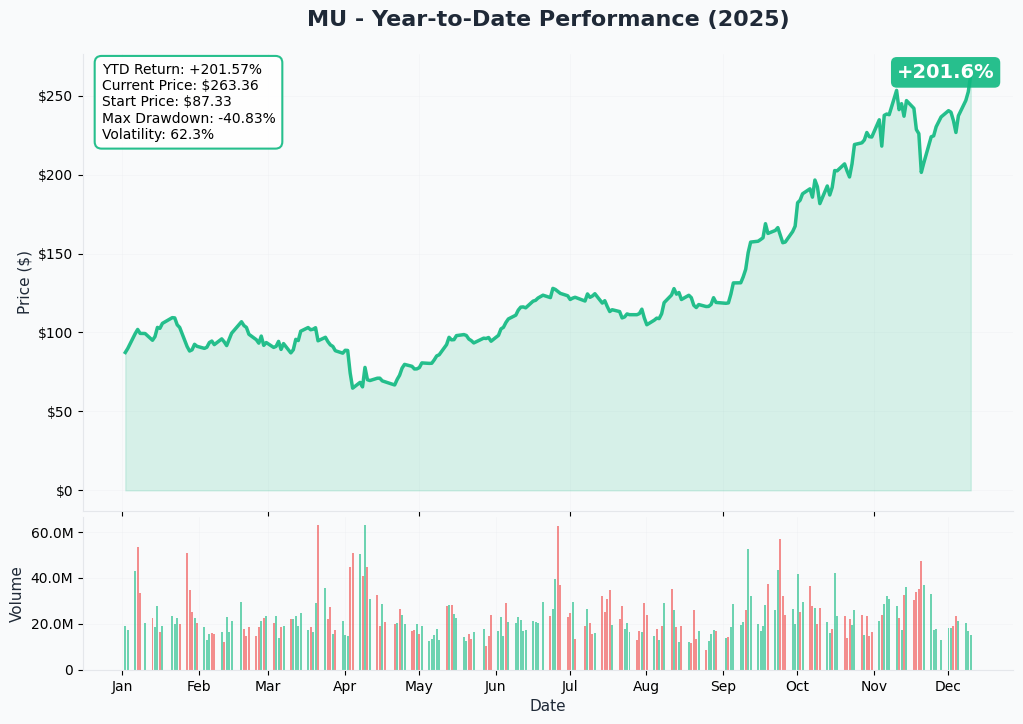

YTD Performance Chart

MU is absolutely on FIRE - up +170% YTD with current price of $252.41, starting the year at just $93.50. This is one of the top-performing semiconductor stocks of 2025, crushing even the red-hot AI chip sector!

Key observations:

- 🚀 Explosive rally: Vertical move from $102 in early December 2024 to $260+ by December 2025

- 📈 HBM breakthrough: Stock doubled from $120s in June to $260 in November on HBM market share gains

- 🎯 Near all-time highs: Trading at $252.41 vs ATH of $260.58 (just 3.2% below peak!)

- 💪 Relentless momentum: Multiple analyst upgrades in November-December with $300-$338 price targets

- 📊 Institutional accumulation: Heavy volume in Q4 as smart money positions for memory supercycle

- ⚠️ Stretched technically: After 170% YTD gain, near-term consolidation or pullback wouldn't be surprising

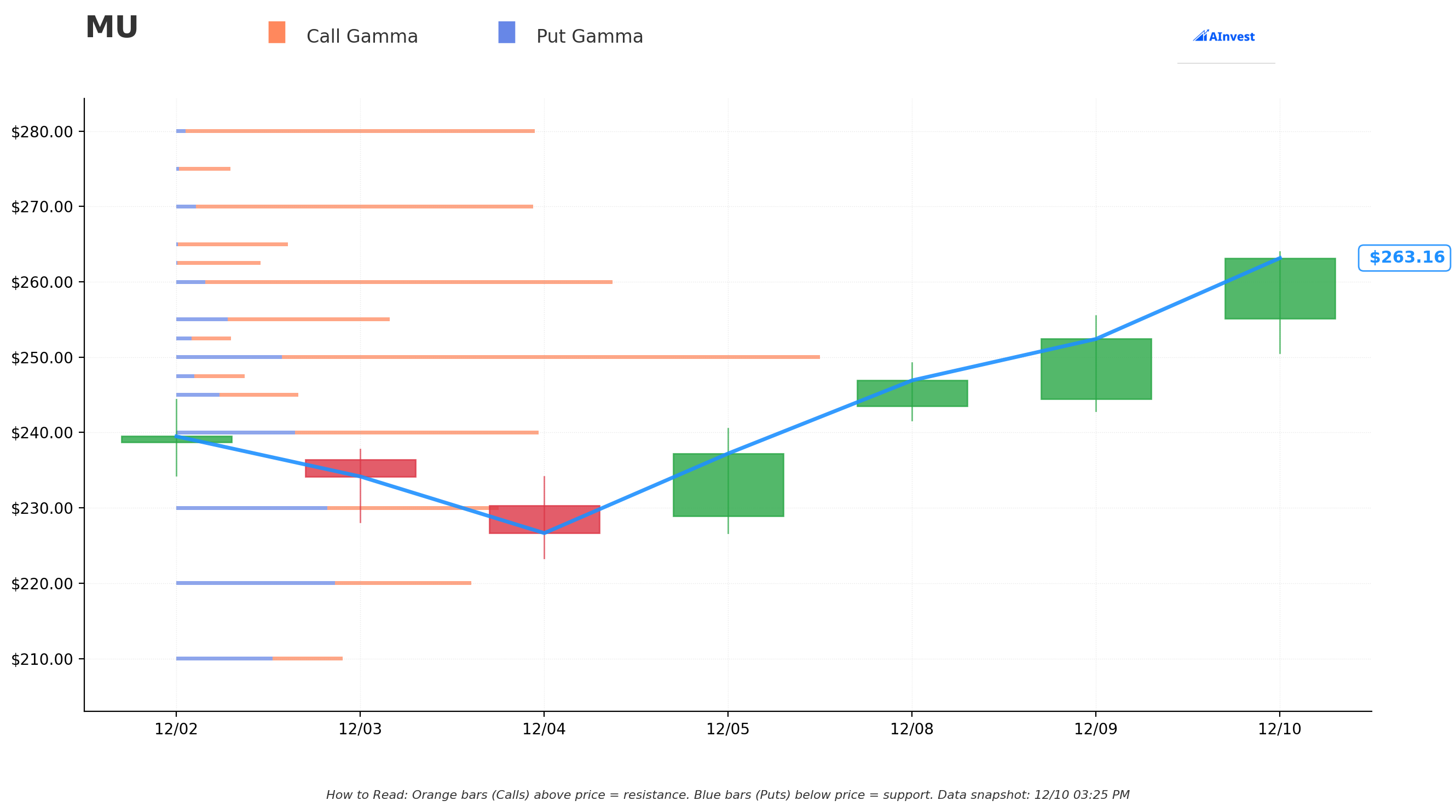

Gamma-Based Support & Resistance Analysis

Current Price: $263.48 (Note: Gamma data snapshot shows price at $263.48 vs trade execution at $252.41 - intraday move!)

The gamma exposure map reveals critical price magnets that will govern near-term price action around earnings:

🔵 Support Levels (Put Gamma Below Price):

- $260 - STRONGEST immediate support with 7.65B total gamma (this is the LINE IN THE SAND!)

- $255 - Secondary support at 3.72B gamma (dealers will buy dips here aggressively)

- $250 - Major structural floor with 11.37B gamma (HIGHEST total gamma on chart - massive magnet!)

- $240 - Deep support at 7.30B gamma (critical psychological level)

- $230 - Extended support zone with 5.71B gamma

- $220 - Disaster floor at 5.20B gamma (20% drop from current levels)

🟠 Resistance Levels (Call Gamma Above Price):

- $270 - Immediate ceiling with 6.33B gamma (first overhead barrier post-earnings)

- $280 - Secondary resistance at 6.34B gamma (10.6% rally required)

- $290 - Major ceiling zone with 2.61B gamma (15.2% above current)

- $300 - MONSTER resistance at 5.89B gamma (THIS IS WHERE THE BTC TRADE STRUCK! Not coincidental)

What this means for traders: MU is sitting between MASSIVE support at $260 (7.65B) and major resistance at $270 (6.33B). The $250 level with 11.37B total gamma is THE anchor - this is where market makers have their largest positions and will defend aggressively. The real story is at $300 resistance with 5.89B gamma - this is exactly where the short call seller got trapped! There's enormous call open interest at $300 strike, creating natural selling pressure as price approaches.

Notice the BTC trade significance: The trader closed $300 calls which sit at a major gamma resistance zone with 5.89B exposure. If earnings send MU toward $280-290, that $300 strike becomes seriously threatened, and their short calls could go deep in-the-money. They're cutting losses now before that happens!

Net GEX Bias: Bullish (76.87B call gamma vs 28.60B put gamma = 2.7:1 ratio) - Overall positioning remains strongly bullish, with call buyers dominating. This short call closure adds fuel to potential upside squeeze!

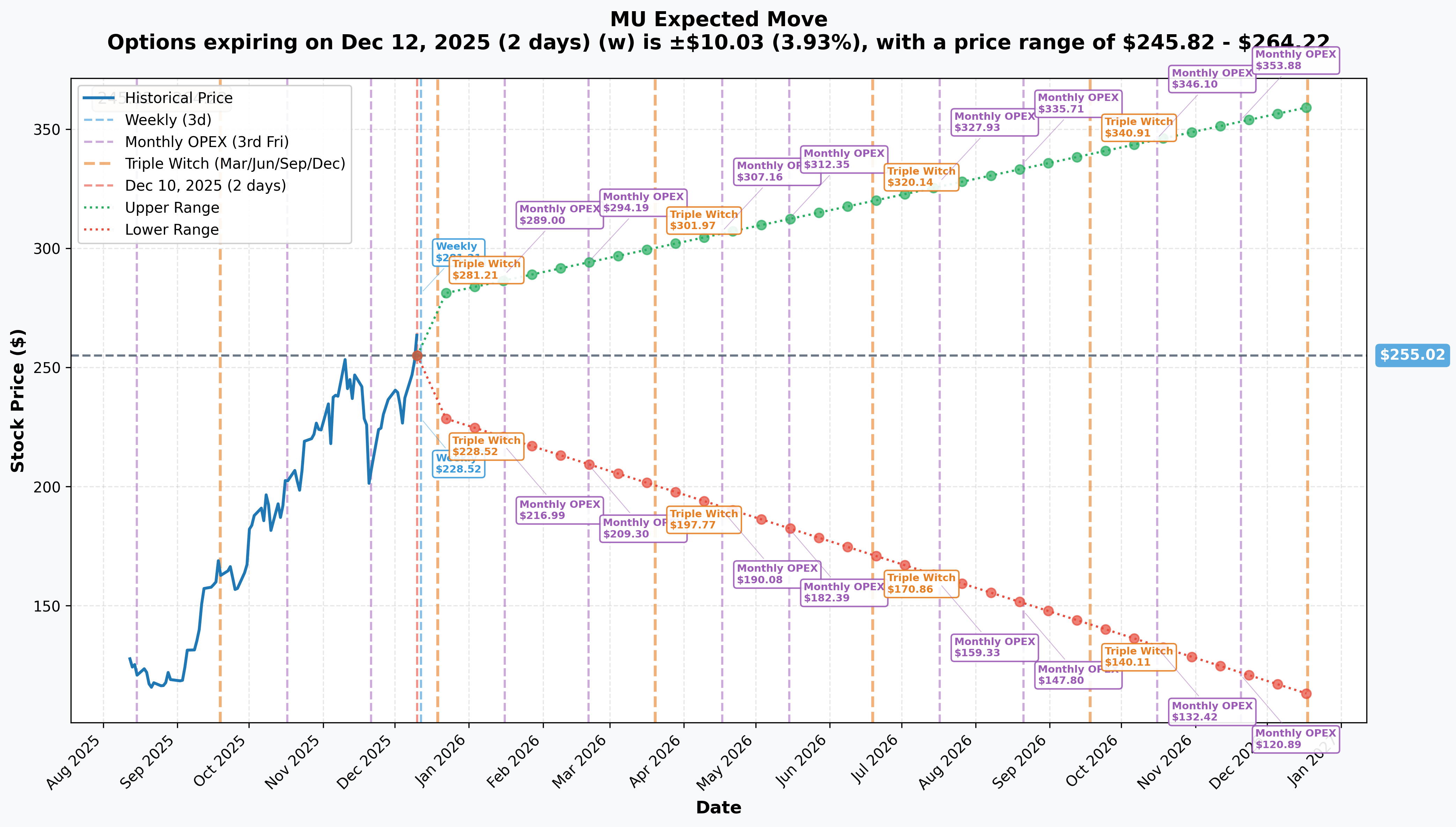

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 12 - 2 days): ±$10.03 (±3.93%) → Range: $245.82 - $264.22

- 📅 Monthly OPEX (Dec 19 - 9 days - INCLUDES EARNINGS!): ±$25.54 (±10.02%) → Range: $229.48 - $280.56

- 📅 Quarterly Triple Witch (Dec 19 - 9 days): ±$25.54 (±10.02%) → Range: $229.48 - $280.56

- 📅 March OPEX (Mar 20 - 100 days - THIS TRADE!): (Not shown in data, but ~±18-20% typical)

Translation for regular folks: Options traders are pricing in a 3.93% move ($10) by Friday for weekly expiration, but a MASSIVE 10% move ($25.54) through December 19th monthly OPEX which INCLUDES the December 17th earnings event. The market expects FIREWORKS on earnings day - that's a huge implied move for a $284B mega-cap stock!

Critical insight: The December 19th expiration (2 days AFTER earnings on Dec 17th) has an upper range of $280.56. If earnings beat drives MU toward that upper range, the $300 strike calls suddenly look VERY achievable by March 20th expiration. The short call seller is looking at this math and thinking "I need to exit NOW before implied volatility explodes pre-earnings and these calls become even more expensive to buy back."

Why the BTC makes sense: Closing short calls 7 days before earnings eliminates the risk of:

- Earnings beat sending stock to $270-280+ (making $300 strikes realistic)

- Implied volatility spike making buyback cost $30-40+ per contract

- Unlimited upside exposure if HBM revenue surprises massively

🎪 Catalysts

🔥 Immediate Catalysts (Next 7 Days)

Q1 FY2026 Earnings - December 17, 2025 (7 DAYS AWAY!) 📊

MU reports fiscal Q1 FY2026 results on Tuesday, December 17, 2025 after market close at 4:30 PM EST. This is THE event that the entire memory market is watching. Wall Street consensus and key expectations:

- 📊 Revenue: $12.5-12.6B (up 45% YoY from $8.71B in Q1 FY2025) - MASSIVE growth!

- 💰 EPS: $3.75-3.90 (vs. $1.79 in Q1 FY2025) - more than DOUBLING earnings

- 📈 Gross Margin: Company guidance ~51.5% (vs. 38.4% last year), Goldman expects 53.6%!

- 🤖 HBM Revenue: Expected to show sequential growth - analysts watching for $2B+ quarterly run rate

- 💻 Data Center Mix: Expected to exceed 56% of total revenue (was 56% in FY2025)

- 🎯 FY2026 Guidance: Wall Street models $60.8B full-year revenue (up from $37.38B in FY2025)

Why this earnings matters MORE than usual:

- HBM trajectory validation: Is Micron on track to $8B+ annual HBM revenue? Supply sold out through 2026 but execution matters

- Pricing power confirmation: Gross margins expanding to 51.5%+ proves memory pricing supercycle is real

- AI positioning credibility: Can MU reach its target of ~20% HBM market share to match overall DRAM share?

- Crucial exit impact: How much capacity freed up from exiting consumer business? When does it flow to HBM production?

- Japan facility update: Any timeline acceleration on the $9.6B Hiroshima HBM factory?

Upside surprise potential: Goldman Sachs models gross margin at 53.6% (above 51.6% consensus), suggesting significant margin expansion from pricing power. If HBM revenue exceeds $2B for the quarter, it validates the $10B+ annual run rate thesis.

Downside risk factors: Any disappointment in HBM ramp timing, margin compression from competitive pressure, or conservative FY2026 guidance could trigger sharp selloff. MU already up 170% YTD - high expectations baked in.

Historical context: MU tends to see 8-15% post-earnings moves on beats/misses. With 10% implied move already priced in, any massive surprise could exceed this range.

🚀 Near-Term Catalysts (Q4 2025 - Q2 2026)

Crucial Consumer Brand Exit - Completed February 2026 🏭

Micron announced exit from the Crucial consumer DRAM/SSD business by end of fiscal Q2 2026 (February 2026):

- 🎯 Strategic shift to prioritize AI and data center demand over low-margin consumer products

- 🏭 Frees constrained manufacturing capacity for HBM production (which commands 3-5x higher margins)

- 📊 While Crucial represents small revenue %, capacity reallocation is HUGE for HBM supply

- 💪 Leaves Samsung and SK Hynix as only major suppliers in consumer memory - pricing power improves

- ⚡ Expect Q1 earnings commentary on how much capacity shifts to HBM in coming quarters

Impact: This is extremely bullish for margins and HBM growth. Every wafer reallocated from $50 consumer SSDs to $500+ HBM modules is massive profit expansion.

Japan HBM Facility Investment - Construction Begins May 2026 🇯🇵

Micron investing approximately 1.5 trillion yen (~$9.6 billion) in next-generation HBM manufacturing in Hiroshima:

- 🏗️ Construction starts May 2026, production begins 2028 (critical long-term capacity)

- 🔬 Will incorporate extreme ultraviolet (EUV) lithography for advanced HBM manufacturing

- 💰 Japanese government contributing up to 500 billion yen in subsidies (government partnership validates strategic importance)

- 🚀 Represents Micron's first new fab project since 2019 - major capacity expansion

- 🎯 Positions MU for long-term HBM supply growth to match demand through 2028+

Timeline significance: Facility won't produce chips until 2028, but groundbreaking in May 2026 (5 months away!) will be major positive catalyst demonstrating commitment to HBM leadership.

HBM3E Supply Sold Out Through 2026 💰

Current-generation HBM3E inventory completely sold out through calendar year 2026:

- 🔥 Micron has reached agreements with "almost all customers" for vast majority of 2026 HBM3E supply

- 📈 Active discussions for HBM4 specifications and volumes

- 💪 Pricing power: when supply sold out 18+ months in advance, margins expand dramatically

- 🎯 Expected to sell out remaining 2026 HBM capacity in coming months

- 📊 HBM revenue trajectory: ~$2B in Q4 FY2025, targeting $8B+ annual run rate

Market share battle: Micron targeting ~20% HBM market share (to match overall DRAM share) by 2H 2025, up from 21% in Q2 2025. SK Hynix leads with 62%, Samsung struggling at 17%.

Memory Pricing Supercycle - Continuing Through 2026 💵

Industry dynamics supporting continued price increases:

- 🔥 December 2025: Micron suspended all DRAM/NAND quotes for one week - signaling SEVERE supply constraints

- 📈 Notified channel partners of 20-30% price hikes on DRAM products

- 🏭 Industrial-grade and automotive DRAM seeing increases as high as 70%!

- ⚡ Some DRAM categories saw 80-100% month-over-month contract price increases in December

- 🎯 Supply constraints expected to worsen in Q1-Q2 2026 as distribution stockpiles exhaust

- 💰 First time in 30 years: simultaneous shortages across DRAM, NAND, and HDD

Revenue impact: Pricing power supports gross margin expansion toward 54%+ levels in fiscal 2026 vs 41% in fiscal 2025. This is MASSIVE profit expansion!

HBM4 Mass Production Ramp - H2 2026 🚀

Next-generation HBM4 samples shipping now, mass production planned for second half 2026:

- 🔬 36GB 12-high configuration built on 1β (1-beta) DRAM process

- 📊 Specifications: >2 TB/s bandwidth, 20% lower power vs HBM3E

- 🎯 Shipped samples to multiple key customers (Nvidia, AMD, hyperscalers) in June 2025

- 💪 Integrated into AMD Instinct MI350 Series - supports AI models with 520 billion parameters per GPU

- ⚡ Production ramp in H2 2026 coincides with Nvidia's next-gen GPU platforms

Why this matters: HBM4 will command even higher ASPs (average selling prices) than HBM3E, further expanding margins. Successful qualification with Nvidia would be game-changing catalyst.

📊 Analyst Activity & Market Sentiment

December 2025 Upgrades - SURGE of bullishness:

- HSBC (Dec 9): Initiated coverage with Buy rating, $330 price target (30-35% upside from current $252!)

- Bank of America (Dec 8): Raised to Neutral, price target $180 → $250 (major capitulation from bears)

- Susquehanna (Dec 8): Raised price target to $300 (exactly where this BTC trade struck!)

- Goldman Sachs (Dec 3): Raised to Neutral, price target $180 → $205 (still conservative but moving up)

November 2025 Upgrades - Building momentum:

- Morgan Stanley (Nov 24): Raised price target $325 → $338 (highest Street target!), maintained Overweight

- UBS (Nov 20): Raised price target $245 → $275, maintained Buy

- Rosenblatt (Nov 17): Raised price target $250 → $300, maintained Buy

- Mizuho: Raised price target to $270, maintained Outperform

Current Consensus:

- Average Price Target: $213.23 (outdated - recent upgrades pulling average higher)

- High Target: $338 (Morgan Stanley) - 34% upside!

- Rating Distribution: 26 Buy, 3 Hold, 0 Sell = Strong Buy consensus

- Key observation: Multiple firms raising targets to $270-$338 range suggests Street believes $300 achievable by late 2026

What the BTC trade reveals: With Street raising targets to $270-$338 and momentum building, the short call seller at $300 strike looked at this and thought "I'm on the wrong side of this trade." Analyst upgrades + earnings momentum = recipe for short covering.

⚠️ Risk Catalysts (Why Short Call Seller Was Scared)

Competitive Pressure from SK Hynix 🇰🇷

SK Hynix dominates HBM market with 62% share vs Micron's 21%:

- 💪 Primary HBM supplier to Nvidia with deep CUDA integration

- 🚀 Shipped first 12-high HBM4 samples in March 2025 (3 months before Micron)

- 🎯 First-mover advantage and technological parity or leadership

- ⚠️ If Nvidia prioritizes SK Hynix for next-gen GPUs, Micron's HBM growth could slow

Samsung Recovery Threat 📱

Samsung currently struggling at 17% HBM share due to thermal/yield issues:

- 💰 Massive capital resources could enable rapid market share recapture if technical issues resolved

- 🏭 If Samsung qualifies at Nvidia, intensifies 3-way competition

- ⚡ Samsung unlikely qualified for Blackwell Ultra, but could capture future platforms

Capacity Constraints Until 2028 🏭

Micron executives acknowledged company "lacks fab capacity for overall HBM production needs":

- ⏰ Japan facility won't produce until 2028 - 2.5 year gap

- 🎯 Hard supply limits could cap market share gains even with strong demand

- 📊 Can't outgrow competitors if constrained by manufacturing capacity

AI Spending Slowdown Risk 🤖

Micron's growth thesis depends on sustained multi-trillion-dollar AI infrastructure investment:

- 💰 Any slowdown in hyperscaler capex reduces HBM demand growth

- 📉 Commodity memory weakness in mobile/PC/automotive sectors already noted

- ⚠️ Economic recession could crater enterprise IT spending

Geopolitical & Export Control Risks 🌍

U.S.-China tensions create ongoing uncertainty:

- 🚨 Export controls on advanced memory technology to China could limit addressable market

- 🇹🇼 Taiwan supply chain dependence (TSMC packaging) creates concentration risk

- 💸 Japan facility relies on 500 billion yen government subsidies - compliance requirements

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are scenarios through March 20th expiration:

📈 Bull Case (35% probability)

Target: $290-$320

How we get there:

- 💪 December 17 earnings CRUSH with revenue toward $12.8B high-end and gross margins at 53.6%+

- 🚀 HBM revenue exceeds $2.2B for quarter, validating $10B+ annual trajectory

- 🤖 FY2026 guidance surprises to upside with $62-65B revenue (above $60.8B consensus)

- 📊 Crucial exit frees 10-15% capacity shifting to HBM faster than expected

- 🌐 Announcement of major Nvidia qualification or expanded customer wins

- 📈 Breakout above $270 gamma resistance triggers technical rally through $280 toward $300

- 🏭 Japan facility groundbreaking in May 2026 catalyst adds momentum

- 💰 Memory pricing supercycle commentary confirms margins expanding to 54%+ levels

Key metrics needed:

- HBM revenue >$2.2B and growing sequentially

- Gross margins 53%+ (proving pricing power)

- Data center revenue >60% of mix (up from 56%)

- Market share gains continuing vs Samsung

Why this happens: HBM sold out through 2026 + pricing power + capacity shifting from Crucial = explosive profit growth. Street targets at $270-$338 validate this scenario.

Impact on BTC trade: Stock reaches $290-320 range, the $300 strike calls go deep in-the-money. The short seller would have faced $20-40+ losses per contract instead of current $12-15 loss. Taking the pain now looks smart in hindsight.

Probability assessment: 35% because it requires strong execution but all fundamentals aligned. Memory supercycle is real, HBM demand is real, capacity expansion is happening. Not a longshot.

🎯 Base Case (45% probability)

Target: $250-$280 range (CHOPPY POST-EARNINGS CONSOLIDATION)

Most likely scenario:

- ✅ Solid earnings meeting/slightly beating consensus ($12.5-12.7B revenue, $3.80-4.00 EPS)

- 📱 HBM revenue solid at $1.9-2.1B but not spectacular - steady progress

- ⚖️ Guidance in-line with expectations (~$60-61B FY2026 revenue)

- 🤖 Margins improve to 51.5-52.5% (good but not mind-blowing)

- 🔄 Post-earnings pullback from $260s to $250-255 support, then gradual grind higher

- 📊 Trading within gamma support ($250-260) and resistance ($270-280) bands for weeks

- 💤 Volatility crush post-earnings (IV drops from elevated levels)

- ⏰ Market waits for Q2 earnings and Japan facility groundbreaking for next catalysts

Why this is most likely: Stock up 170% YTD with high expectations already baked in. Even strong earnings often lead to "sell the news" profit-taking. Fundamentals remain solid but need time to digest massive gains.

This is actually WIN for BTC trader: Stock consolidates $250-280, never seriously threatens $300 strike. They paid $1.9M to close but avoided much larger losses if stock exploded to $300+. The $300 calls expire worthless or minimal value at March 20th expiration. Taking $1.2-1.4M realized loss now beats potential $2-3M+ loss in bull scenario.

Probability assessment: 45% because "good but not great" is usually what happens. Markets price in optimism, reality is always more nuanced.

📉 Bear Case (20% probability)

Target: $220-$245 (PULLBACK TO MAJOR SUPPORT)

What could go wrong:

- 😰 Earnings miss or guidance disappoints at current valuation - even small miss could trigger -10-15% gap down

- 🚨 HBM revenue comes in at $1.7-1.8B (below expectations) - questions about ramp trajectory

- ⏰ Gross margins only reach 50-51% (below 51.5% guidance) - margin compression fears

- 🇨🇳 Export control news or China revenue headwinds mentioned

- 💸 Conservative FY2026 guidance citing uncertainty - Street expects $60.8B, company guides $58-59B

- 📉 Broader tech/semiconductor selloff drags MU lower (Nvidia weakness, macro fears)

- 🔨 Break below $250 gamma support triggers cascade to $240, then deeper to $230

- 💰 Profit-taking after 170% YTD rally - institutions locking in gains

Critical support levels:

- 🛡️ $250: Major gamma floor (11.37B) - MUST HOLD or momentum shifts bearish

- 🛡️ $240: Deep support (7.30B gamma) - psychological level

- 🛡️ $230: Extended floor (5.71B gamma) - disaster scenario but still above 200-day MA

Why this is lower probability (20%): Fundamentals are too strong - HBM sold out through 2026, pricing power proven, capacity expansion happening. Would require multiple negative catalysts to align. Memory supercycle is real.

Impact on BTC trade: In this scenario, the $300 strike calls expire worthless, and the short seller's $1.9M closing cost looks like waste. BUT they eliminated tail risk of stock recovering to $280-300 by March. From their perspective, it's insurance cost against unlimited upside.

Key insight: The BTC trader ISN'T betting on this bear case - they're PROTECTING against the bull case by closing early!

💡 Trading Ideas

🚀 Aggressive: Ride The Short Squeeze (For Bulls)

Play: Buy calls after earnings if beat confirmed, targeting short squeeze to $280-300

Why this could work:

- 💪 This BTC trade shows short call sellers are CAPITULATING before earnings

- 📊 920 contracts closed = 92,000 shares of buying pressure removed from overhead

- 🎯 If earnings beat, remaining short calls at $280-300 strikes face forced covering

- 🔥 Gamma squeeze potential with 76.87B call GEX vs 28.60B put GEX (2.7:1 bullish)

- 📈 Street targets at $270-$338 suggest room to run if execution delivers

- ⚡ HBM supply sold out + pricing power = recipe for margin expansion surprise

Structure: Buy February or March ATM/slightly OTM calls AFTER earnings (wait for direction)

Estimated approach:

- ⏰ Wait for December 17th 4:30 PM earnings, review results

- 📊 If revenue >$12.6B, margins >52%, and guidance strong → consider call entries

- 🎯 Target strikes: $270-280 calls (March 20 expiration to match BTC trade timeframe)

- 💰 Post-earnings IV crush makes calls much cheaper than pre-earnings

- 🚀 Look for breakout above $270 gamma resistance as confirmation

- 📈 Take profits at $285-290 (don't get greedy waiting for $300)

Risk level: HIGH (directional bet, can lose 50-80% if stock doesn't cooperate) | Skill level: Advanced

Expected outcome: If bull case plays out, 50-100%+ returns possible. But requires timing and conviction.

⚖️ Balanced: Post-Earnings Bull Put Spread (Moderate Income)

Play: After earnings clarity, sell bull put spread collecting premium in consolidation range

Structure: Sell $250 puts, Buy $240 puts (March 20 expiration - SAME as BTC trade)

Why this works:

- 🎢 IV crush after earnings makes put spreads premium rich

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 🎯 Targets gamma support zone at $240-$250 where dealers have massive 18.67B combined gamma

- 🛡️ Bullish thesis: MU stays above $250 support, you keep premium

- ⏰ 90+ days post-earnings gives time for consolidation without time decay killing position

- 💰 Reasonable risk/reward if you're moderately bullish on MU's HBM story

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Collect ~$2.50-3.50 net credit per spread post-earnings

- 📈 Max profit: $250-350 if MU stays above $250 at March expiration (keep full credit)

- 📉 Max loss: $750-650 if MU below $240 (defined and limited to spread width minus credit)

- 🎯 Breakeven: ~$247-247.50

- 📊 Risk/Reward: ~2.5:1 (risk $700 to make $300) - acceptable for defined-risk bullish play

Entry timing:

- ⏰ Wait 1-2 days post-earnings (Dec 18-19) for IV to fully collapse

- 🎯 Only enter if stock trades $255+ (gives cushion above your short strike)

- ❌ Skip if stock already below $252 (too close to short strike for comfort)

Position sizing: Risk only 3-7% of portfolio per spread (this is moderate directional exposure)

Risk level: Moderate (defined risk, mildly bullish directional) | Skill level: Intermediate

🛡️ Conservative: Wait For Pullback, Buy Stock

Play: Stay on sidelines until after earnings volatility, buy shares on dip to $240-250 support

Why this is smart:

- ⏰ Earnings in 7 days creates binary event risk with ±10% implied move - too risky

- 💸 Stock at $252 after 170% YTD gain - zero margin of safety at current levels

- 📊 Even great earnings often lead to "sell the news" profit-taking

- 🎯 Better entry likely at $240-250 gamma support (5-10% lower) after IV settles

- 🤔 The BTC trade shows someone SCARED of upside, but also shows $300 resistance is real

- 💰 Long-term HBM story intact - buying dips makes more sense than chasing

Action plan:

- 👀 Watch Tuesday Dec 17th earnings for revenue ($12.5B+ target), margins (51.5%+ needed), HBM trajectory

- 🎯 Set limit orders at $245-250 range (major gamma support levels)

- ✅ Need to see HBM revenue progression and FY2026 guidance quality

- 📊 If stock pulls back to $240-245, that's 7-10% off current price with strong support

- ⏰ Long-term hold for Japan facility (2028), HBM market share gains, memory supercycle

Entry levels:

- Tier 1: $250-252 (minor pullback, good entry for aggressive buyers)

- Tier 2: $245-248 (better risk/reward, 5-7% off current)

- Tier 3: $240-243 (excellent entry if panic selloff, major gamma support)

Position sizing: Start with 30-50% of intended position size, add on further weakness

Risk level: LOW (patient, buying quality at support) | Skill level: Beginner-friendly

Expected outcome: Build position at better prices over 2-4 weeks. Participate in long-term HBM growth story without overpaying.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Earnings binary event in 7 days: Results December 17th after close create MASSIVE volatility risk. Stock could gap 10-15% either direction based on HBM revenue trajectory, gross margins (51.5% vs 53%+ makes huge difference), and FY2026 guidance. Options pricing ±10% implied move but actual move could exceed this. Even beats sometimes lead to selloffs if guidance conservative.

-

💸 Valuation stretched after 170% YTD gain: P/E ratio of 31.65 is 62% above 10-year average of 19.37. Stock at $252 vs starting year at $93 - massive gains already captured. This is EXTREMELY stretched - requires flawless HBM execution and margin expansion to justify. Any disappointment magnified at current valuation. Limited margin of safety.

-

🇰🇷 SK Hynix competitive dominance: SK Hynix controls 62% HBM market share vs Micron's 21%, with first-mover advantage at Nvidia. First to ship HBM4 samples (March vs MU's June). Technological parity or leadership. Deep CUDA/Nvidia integration creates switching costs. MU gaining share but from small base - can they really catch up?

-

🏭 Capacity constraints until 2028: Japan facility won't produce chips until 2028 - that's 2.5 years away! Management admitted company "lacks fab capacity for overall HBM production needs." Hard supply limits could cap market share gains even with strong demand. Can't outgrow competitors if manufacturing constrained.

-

🤖 AI spending concentration risk: Growth thesis depends on sustained multi-trillion-dollar AI infrastructure investment from hyperscalers (Microsoft, Google, Amazon, Meta). Any slowdown in capex budgets crater HBM demand. Already seeing commodity memory weakness in mobile/PC/automotive - what if AI slows too? Single sector dependency is risky.

-

🇨🇳 China export restrictions wildcard: U.S.-China tech tensions create ongoing uncertainty. Export controls on advanced memory to China could limit addressable market (historically 15-20% of sales). Taiwan supply chain dependence (TSMC packaging) adds geopolitical risk. Future controls could hit HBM products without warning.

-

💰 Memory pricing cycles historically volatile: Current supercycle shows 20-100% month-over-month price increases - this is NOT sustainable long-term. Memory markets are cyclical. New capacity coming online 2026-2027 could reverse pricing. If cycle turns, gross margins compress rapidly. Don't assume 51-54% margins are permanent.

-

📊 Heavy insider selling signals concern: CEO Sanjay Mehrotra sold 400,025 shares on November 6 for $91M. Insiders executed 117 sales and 0 purchases in past 6 months - ALL transactions were sales in past 3 months. While potentially portfolio diversification, heavy selling at highs often precedes weakness.

-

🎯 $300 strike has MASSIVE open interest: 8,600 contracts at $300 strike create natural resistance. This BTC trade closed 920 (10.7% of OI), but 7,680 contracts remain. As stock approaches $280-290, those short calls will be defended aggressively. Gamma resistance at $300 (5.89B) creates ceiling.

-

📉 Post-rally consolidation or correction overdue: After 170% YTD gain with minimal pullbacks, stock is technically extended. RSI likely overbought, momentum indicators flashing yellow. Even with strong fundamentals, healthy pullback to $230-240 (10-15%) wouldn't be unusual. Don't assume straight line up continues.

🎯 The Bottom Line

Real talk: Someone just paid $1.9 MILLION to close short calls 7 days before the most important earnings report in Micron's history. This is CAPITULATION - they're surrendering and taking losses NOW rather than risk getting absolutely DESTROYED if earnings send MU toward $280-300+.

What this BTC trade tells us:

- 🎯 Short call seller SCARED of explosive upside through March 20th expiration

- 💰 Willing to realize $1.2-1.4M loss now to avoid potentially $2-3M+ loss if stock rallies to $300

- ⚖️ The timing (7 days pre-earnings) shows binary event risk too high to stomach

- 📊 They sold $300 calls weeks/months ago, but Street now raising targets to $270-$338 range

- ⏰ Closing before IV spike and earnings eliminates unlimited upside exposure

- 🚀 This is SHORT COVERING = removes overhead resistance, actually BULLISH for stock!

This IS a bullish signal - here's why:

When short sellers capitulate BEFORE a major catalyst, it signals:

- Fear of upside is real - they're not waiting to see if earnings disappoint

- Momentum shift - willing to take pain now rather than risk more pain later

- Reduced resistance - 920 contracts closed = less selling pressure at $300 strike

- Analyst upgrades working - Street targets at $270-$338 scared them out

- Fundamentals strengthening - HBM sold out, pricing power real, margins expanding

If you own MU:

- ✅ This trade VALIDATES your thesis - short sellers giving up!

- 📊 Set mental stop at $250 (major gamma support) to protect if earnings disappoint

- ⏰ December 17th earnings are CRITICAL - watch HBM revenue, margins, FY2026 guidance

- 🎯 If earnings beat and stock breaks $270, could run to $280-290 on short squeeze

- 💰 Consider trimming 10-20% at $260+ to lock in gains, let rest ride with stop protection

If you're watching from sidelines:

- ⏰ Tuesday December 17th after close is the moment of truth - wait for earnings!

- 🎯 Post-earnings dip to $240-250 would be excellent entry (major gamma support)

- 📈 Looking for confirmation: HBM revenue >$2B, margins >52%, strong FY2026 guidance

- 🚀 Long-term (12-18 months), HBM growth + Japan facility + memory supercycle support $280-320 targets

- ⚠️ Current valuation (31.6x P/E after 170% gain) requires perfect execution - margin for error is thin

If you're considering shorting:

- 🚨 DON'T - this BTC trade shows shorts are capitulating, not initiating!

- 📊 Fighting 170% momentum into earnings with bullish fundamentals is suicide

- ⏰ If you MUST be bearish, wait until AFTER earnings and look for failed breakout above $270

- 🎯 Only viable short entry is break below $250 support, targeting $240 then $230

- ⚠️ With HBM sold out and pricing power, fundamental short case is weak

Mark your calendar - Key dates:

- 📅 December 17 (Tuesday) 4:30 PM EST - Q1 FY2026 earnings report (7 DAYS!)

- 📅 December 18 (Wednesday) - Post-earnings price action, analyst reactions, guidance digestion

- 📅 December 19 - Monthly OPEX (±10% implied move window closes)

- 📅 February 2026 - Crucial consumer business exit completed, capacity shifts to HBM

- 📅 March 20, 2026 - Quarterly OPEX, expiration of this BTC trade (100 days out)

- 📅 May 2026 - Japan $9.6B HBM facility groundbreaking begins

- 📅 2028 - Japan facility production starts, major capacity expansion

Final verdict: Micron's long-term HBM story is COMPELLING - sold out supply through 2026, pricing power driving 51-54% margins, $9.6B Japan facility investment, and structural AI memory demand tailwinds. The BTC trade shows even skeptics are capitulating before earnings. BUT, at 31.6x P/E after 170% YTD gain with earnings in 7 days, the risk/reward for NEW aggressive positioning is mixed. Be patient, let earnings clear, look for pullbacks to $240-250 support. The AI memory supercycle will still be here in 2-4 weeks, and you'll get better entry points.

For earnings: Expect FIREWORKS. This BTC trade, combined with Street upgrades to $270-$338, sets up for explosive move either direction. The ±10% implied move ($25 in either direction) is just the starting point. If HBM revenue and margins crush, we could see $270-280. If disappointment, $230-240 is possible. Don't fight the tape - wait for direction, then act.

The memory supercycle is real. The HBM growth is real. The AI infrastructure build is real. Just don't overpay. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. This Buy-to-Close trade represents someone exiting a short position - it does NOT mean you should buy calls. Earnings create binary event risk with potential for 10-15%+ gaps either direction. Always do your own research and consider consulting a licensed financial advisor before trading.

About Micron Technology: Micron Technology is one of the largest semiconductor companies in the world, specializing in memory and storage chips including DRAM, NAND flash, and high-bandwidth memory (HBM) for AI accelerators, with a market cap of $284.1 billion in the Semiconductors & Related Devices industry.