🚨 Micron (MU) LEAPs Activity: $11.3M in 2028 Call Options as Memory Giant Consolidates Near All-Time Highs

📅 January 2, 2026 | 💰 $11.3M Premium Tracked

🎯 The Quick Take

We just spotted $11.3 million worth of activity in long-dated LEAP call positions on Micron Technology (MU) - these are 2028 expiration contracts moving in size. With the stock trading at $319.33 near record highs after a 239% surge in 2025, institutional players are actively positioning in the memory giant. The option activity shows three separate trades in calls struck at $250, $310, and $330 - significant institutional interest in MU's long-term trajectory.

💰 The Option Flow Breakdown

📊 What Just Happened

Here's the institutional activity in MU LEAPs today:

| Time | Type | Strike | Expiration | Volume | Premium |

|---|---|---|---|---|---|

| 10:30 AM | Call | $250 | 2028-01-21 | 184 | $2.6M |

| 10:06 AM | Call | $330 | 2028-01-21 | 456 | $5.0M |

| 10:30 AM | Call | $310 | 2028-01-21 | 435 | $4.3M |

Total Activity: 1,075 contracts representing $11.3 million in premium

🤓 What This Actually Means

Real talk: We're seeing massive institutional activity in 2028 LEAP call positions. All three strikes are in-the-money with MU at $319, and these contracts represent significant conviction in Micron's long-term trajectory (possibly established when the stock was trading in the $200-$250 range based on the strikes chosen).

This is not normal retail flow - these are highly unusual trades with size that we typically see only 3-4 times a year. The fact that all three positions are moving simultaneously suggests coordinated institutional activity by a sophisticated player who has been riding Micron's AI memory supercycle.

Translation: When you see LEAP activity at $11M+ size with the stock near all-time highs, pay attention. This represents significant institutional conviction in MU's direction. 📈

📈 Technical Setup & Chart Analysis

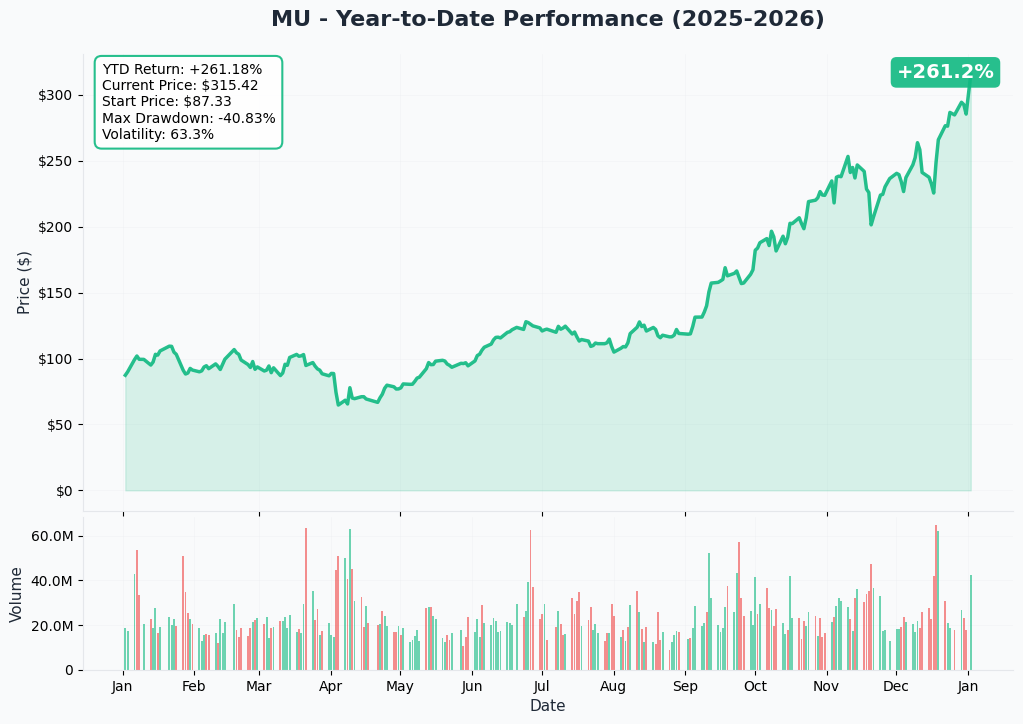

YTD Performance

The Chart Story: Micron Technology has been on an absolute tear, surging 239% in 2025 to become the top performer in both the Nasdaq 100 and S&P 500. The stock is currently consolidating just below the psychological $320 resistance level after hitting an all-time high of $310 in late December.

The vertical move from $200 to $310 in Q4 2025 was fueled by blowout Q1 FY2026 earnings that crushed estimates - $13.64B revenue (+57% YoY) and $4.78 EPS (beating by 21%). The company's entire HBM production is sold out through 2026, creating a structural supply shortage that's driving record margins.

Company Overview: Micron is one of the largest semiconductor companies globally, specializing in memory and storage chips. With a market cap of $345.77 billion and 53,000 employees, the Boise-based manufacturer generates revenue primarily from DRAM (79% of sales) and NAND flash (20%). The firm serves data centers, mobile devices, consumer electronics, and automotive sectors - positioning it as critical infrastructure for the AI boom.

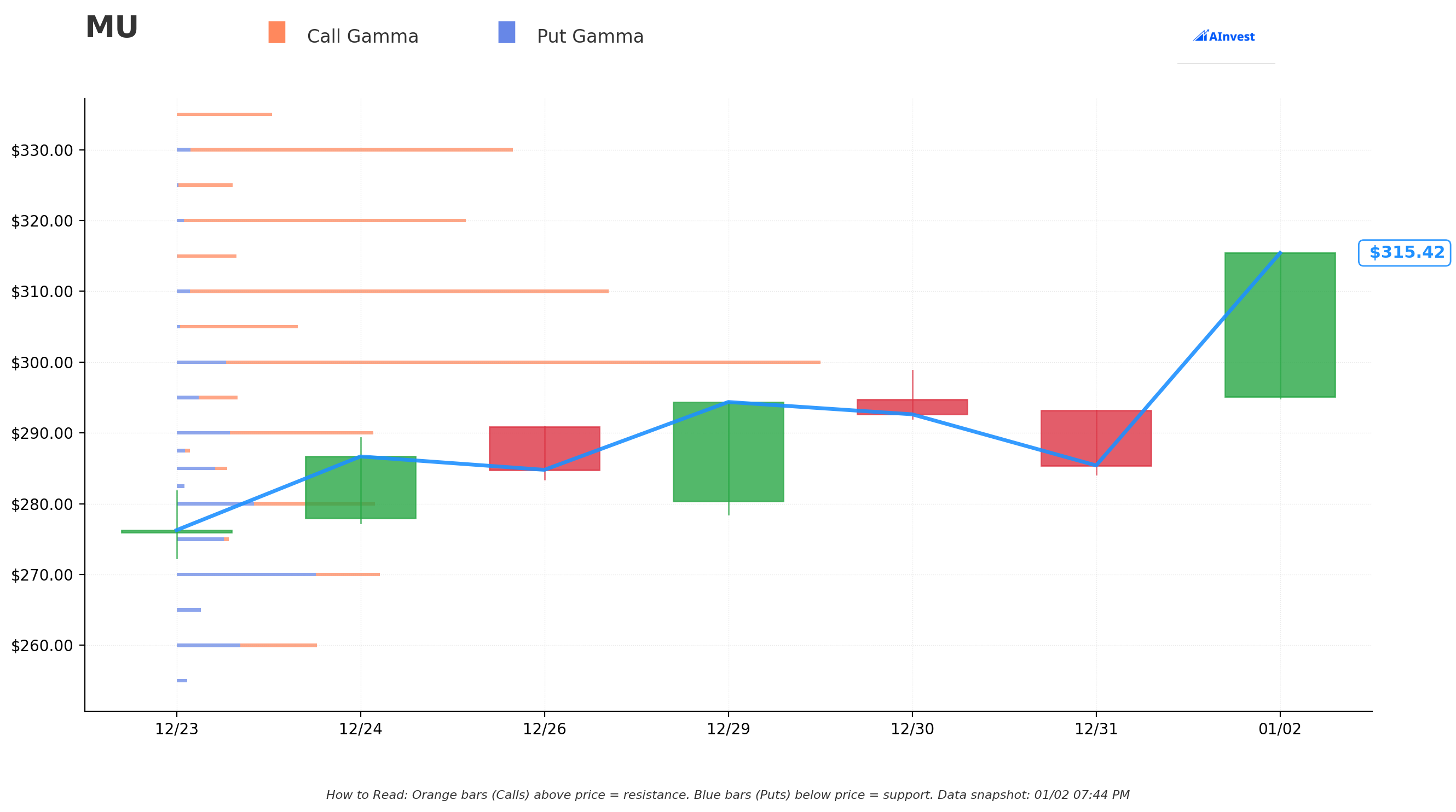

🎯 Gamma-Based Support & Resistance Analysis

What the Market Makers Are Telling Us:

The gamma profile shows MU is trading in a bullish zone with heavier call gamma above and declining put gamma below. Here's what matters:

🔵 Support Levels (Put Gamma):

- $310 (Strongest): Only 2.9% below current price - 6.14 call GEX vs 0.20 put GEX = strong bullish support

- $300: Secondary support at 6.1% down - 8.70 call GEX creates natural floor

- $290: Tertiary support at 9.2% down - still positive net GEX

🟠 Resistance Levels (Call Gamma):

- $320 (Immediate): Just 0.2% above - 5.01 call GEX creates magnet effect

- $330: Next resistance at 3.3% up - 4.74 call GEX with declining density

- $340: Major resistance at 6.5% up - thins out significantly above here

Market Maker Positioning: The net GEX bias is Bullish with 50.17 call GEX vs 18.82 put GEX. This creates a supportive environment where market makers need to buy the dips to stay delta-neutral. The clustering of gamma between $310-$330 suggests the stock wants to trade in this range near-term unless we get a major catalyst.

Key Insight: The $310 support is only 2.9% away - that's essentially air-tight support given the gamma profile. But resistance at $320 is real and may require fresh catalysts to break convincingly. 💪

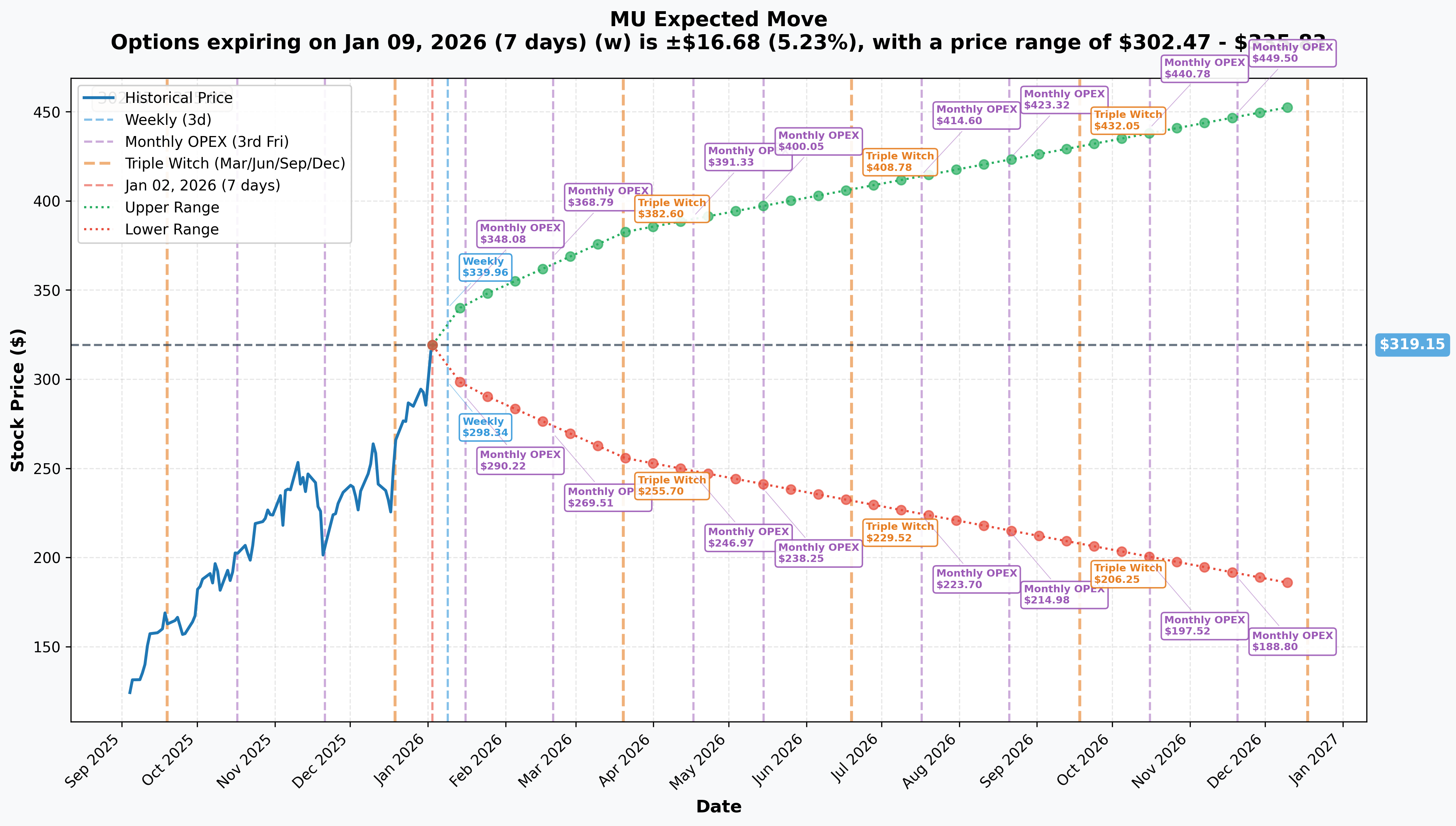

📊 Implied Move Analysis

What Options Pricing Is Telling Us:

The market is pricing in significant volatility across all timeframes, reflecting both the AI momentum story and the memory cycle uncertainty:

⏰ Key Timeframes:

- Weekly (Jan 9): ±5.23% ($302.47 - $335.83)

- Monthly OPEX (Jan 16): ±7.49% ($295.24 - $343.06)

- Quarterly Triple Witch (Mar 20): ±19.88% ($255.70 - $382.60)

- Yearly LEAPs (Dec 18): ±42.5% ($183.51 - $454.79)

Breaking It Down:

The weekly implied move of ±5.23% is elevated but reasonable for a high-beta semiconductor stock that just rallied 239%. That $16.68 swing translates to a range of $302-$336, which aligns perfectly with our gamma-based support at $310 and resistance at $330.

The quarterly move pricing in a potential drop to $255 or surge to $383 makes sense given the April 1 earnings catalyst where MU is guiding for record Q2 revenue of $18.7B and $8.42 EPS. That's a 76% sequential EPS jump - the kind of number that can cause violent moves in either direction.

Reality Check: The yearly implied move suggesting MU could hit $455 or fall to $183 reflects the binary nature of memory cycles. If HBM demand sustains and DRAM prices continue rising 40-50% as TrendForce projects, we hit the high end. If AI spending moderates or competition intensifies, we test the lows. 🎢

🎪 Catalysts: What's Moving the Stock

🔮 Upcoming Catalysts

Q2 FY2026 Earnings - April 1, 2026 ⭐⭐⭐⭐⭐

This is the big one. Management guided for:

- Revenue: $18.7B (±$400M) - Would be a quarterly record

- EPS: $8.42 (±$0.20) - Represents 76% sequential growth

- Gross Margin: 68% (±100 bps) - Near-peak territory

According to Micron's December investor release, the company is experiencing "strong execution across end markets and products in a tight supply environment." Translation: They're printing money and can't make chips fast enough. 💰

HBM4 Mass Production - H2 2026 ⭐⭐⭐⭐

Micron is targeting second-half 2026 for HBM4 mass production - featuring 36GB modules with 11 Gbps data rates and 2 TB/s bandwidth. These specs are designed for NVIDIA's Vera Rubin AI architecture.

The company expects an annualized HBM revenue run-rate of ~$8 billion, and with the entire HBM4 supply already contracted on price and volume, this catalyst has high visibility. This is structural demand, not cyclical speculation.

DRAM Price Increases Throughout 2026 ⭐⭐⭐⭐

TrendForce analysis projects DRAM prices will rise 40-50% through H1 2026 due to structural supply shortages. Micron's CEO admitted on the Q1 call that they can only meet "half to two-thirds of customer demand".

When supply is this tight, pricing power = margin expansion = EPS beats. 📊

Hiroshima HBM Facility Construction - Expected May 2026 ⭐⭐⭐

A $9.6 billion partnership with Japan to build an HBM facility in Hiroshima is expected to break ground in May 2026, with first output in 2028. While revenue impact is distant, this de-risks long-term HBM supply and validates Micron's strategic positioning in the AI memory race.

📅 Recent Catalysts (Already Priced In)

Q1 FY2026 Earnings Beat - December 17, 2025 ✅

MU absolutely crushed it: $13.64B revenue vs. $13B expected (+57% YoY), $4.78 EPS vs. $3.94 expected (+21% beat). Operating margins hit 47% - up 20 percentage points year-over-year. This was the catalyst that drove the recent rally to $310. Full details here.

HBM Sold Out Through 2026 - December 2025 ✅

Management confirmed the entire 2026 HBM supply is "more than sold out" with completed price and volume agreements. This removed a major uncertainty and validated the AI memory supercycle thesis. Stock surged on this confirmation.

Analyst Upgrades - December 18, 2025 & January 2, 2026 ✅

Rosenblatt Securities raised to $500 (from $300), Citigroup maintained $330 Buy, and Bernstein boosted to $330 Outperform on January 2. Consensus across 40 analysts is $290.92 with a range of $86-$500. The upgrades are priced in but validate the bull case.

CHIPS Act Funding Finalized - December 2024 ✅

The U.S. government finalized $6.165 billion in CHIPS Act funding for Idaho and New York fabs, plus an additional $275M for Virginia. This de-risks domestic expansion and is fully in the stock now.

🎲 Price Targets & Probabilities

I'm using the gamma levels, implied move data, and catalyst timeline to map out three scenarios over the next 3 months (through April earnings):

🚀 Bull Case: $360-380 (30% probability)

Target: $370 (+16% from current)

Path: Q2 earnings on April 1 deliver another massive beat with revenue exceeding $19B (above the $18.7B guide) and gross margins holding above 68%. DRAM price increases accelerate beyond the projected 40-50%, and HBM4 production timeline gets pulled forward to Q2 2026.

Catalysts Aligned:

- Quarterly implied move shows $382.60 as the upper bound by March 20

- Gamma resistance at $340 gets cleared, opening path to $350-380

- TrendForce's DRAM price surge projections prove conservative

- Competing semiconductor names (NVDA, AMD) rally on AI infrastructure spend, lifting MU

What Needs to Happen:

- No deceleration in AI capex from hyperscalers

- HBM market share gains vs. SK Hynix (currently 53% vs MU's 11%)

- DDR5 adoption accelerates beyond current forecasts

Risk: This assumes everything goes perfectly and competitive dynamics don't worsen. Micron's 11% HBM market share trails SK Hynix and Samsung significantly, so gains here are speculative.

⚖️ Base Case: $310-340 (50% probability)

Target: $325 (+2% from current)

Path: MU consolidates in the $310-$340 range through Q2 earnings, trading between gamma support at $310 and resistance at $340. The stock digests the 239% 2025 gain while waiting for the April 1 catalyst. Earnings meet the guided $18.7B revenue and $8.42 EPS, but margin expansion slows as we approach peak gross margins.

Catalysts Aligned:

- Monthly implied move of ±7.49% keeps stock in $295-$343 range

- Gamma profile shows $320 resistance is real and needs catalyst to break

- April earnings beat but don't blow away like Q1 did

- DRAM prices rise as expected (40-50%) but don't accelerate

What Needs to Happen:

- Stable AI infrastructure spending from Microsoft, Google, Meta, Amazon

- No competitive surprises from SK Hynix or Samsung on HBM4 timing

- Memory supply stays tight through Q1 2026

Why This Is Most Likely: The stock just rallied from $200 to $310 in one quarter. Some consolidation is natural and healthy. The option flow we're seeing today - $11.3M of LEAP activity - shows significant institutional interest near $320. Let the story play out through April earnings before the next leg.

🐻 Bear Case: $260-290 (20% probability)

Target: $275 (-14% from current)

Path: Q2 earnings disappoint with revenue closer to the low end of guidance ($18.3B vs $18.7B midpoint), and management signals margin pressure as we approach peak memory pricing. Commentary suggests HBM competition is intensifying with SK Hynix and Samsung accelerating HBM4 to February 2026, ahead of Micron's H2 timeline.

Catalysts Aligned:

- Weekly implied move downside of $302 gets tested

- Gamma support at $290 (9.2% down) becomes new floor

- Broader tech correction driven by AI spending concerns

- Memory cycle peak fears return

What Would Trigger This:

- Hyperscaler capex guidance cuts (watch MSFT, GOOGL, META earnings)

- DeepSeek-style efficiency breakthroughs reduce memory requirements

- Competitive HBM4 launches undercut Micron's pricing power

- China CXMT ramps faster than expected, pressuring commodity DRAM

Why It's Lower Probability: Micron's HBM is sold out through 2026 with contracted pricing. The supply shortage is structural, not cyclical. Management would need to drastically miss on already-conservative guidance for this scenario to play out. But memory stocks can correct 30-40% in weeks when sentiment shifts, so ignoring this tail risk would be foolish.

💡 Trading Ideas

🛡️ Conservative: "Cash Secured & Waiting"

Strategy: Sell the February 21 $300 cash-secured puts

Setup:

- Sell $300 strike put expiring February 21, 2026

- Collect approximately $8-12 premium per contract

- Secure $30,000 cash per contract

Why This Works:

You're getting paid to potentially buy MU at $300 (5.7% below current price) - right at the secondary gamma support level. If the stock stays above $300, you keep the premium and walk away. If it falls below $300, you own shares at an effective cost basis of ~$288-292 after premium collected.

The monthly implied move shows a floor at $295, and gamma analysis confirms $300 as strong support with 8.70 call GEX. This strike is below 90% of analyst price targets, giving you a margin of safety.

Risk: If MU craters to $260-270 on a memory cycle scare, you're stuck owning at $300. But if you believe in the AI memory supercycle thesis, this is exactly where you want to enter.

Probability of Success: ~70% (stock stays above $300 through Feb OPEX)

⚖️ Balanced: "Defined Risk Bull Call Spread"

Strategy: April $320/$350 bull call spread

Setup:

- Buy April 17 $320 call

- Sell April 17 $350 call

- Net debit: ~$12-15 per spread

- Max profit: $15-18 per spread

- Max loss: $12-15 per spread

Why This Works:

You're positioned for MU to break through the $320 resistance and run toward the $350 level ahead of April 1 earnings. The spread caps your risk at the debit paid but gives you exposure to a 9.6% move (current price to $350).

The quarterly implied move shows $382 as the upper bound, so a move to $350 is well within the expected range. You benefit from DRAM price increases, HBM4 pre-production hype, and positive analyst commentary leading into the Q2 report.

Risk Management:

- Maximum loss is the debit paid (~$1,200-1,500 per spread)

- Breakeven is $320 + debit, around $332-335

- If MU consolidates at $310-320, you lose the premium

- Close early if stock hits $345+ before earnings for 80% max profit

Probability of Success: ~45% (stock above breakeven at expiration)

🚀 Aggressive: "Pre-Earnings Long Call Lottery"

Strategy: Buy April $340 calls ahead of April 1 earnings

Setup:

- Buy April 17 $340 calls (15 days after earnings)

- Cost: ~$8-12 per contract

- Leverage: ~30:1

- Breakeven: $348-352

Why This Is the YOLO Trade:

If MU delivers a monster Q2 beat on April 1 similar to the Q1 crusher, the stock could gap from $320 to $350+ overnight. You're paying for gamma resistance at $340 to get taken out by earnings euphoria. The quarterly implied move prices in a realistic path to $382 - your calls would be deep ITM in that scenario.

What You're Betting On:

- Revenue exceeding $19B (vs $18.7B guide)

- Gross margins expanding above 68%

- HBM revenue run-rate upgraded from $8B to $10B+

- Management pulling forward HBM4 timeline or announcing surprise capacity adds

Why This Can Work:

Look at what happened after Q1 earnings - stock jumped from $285 to $310 in two weeks. If Q2 is even better (76% sequential EPS growth), we could see a similar 8-10% gap that puts your $340 calls in-the-money instantly.

Real Talk on Risks:

This is a binary bet. If earnings merely meet expectations (even if they beat slightly), IV will crush and the stock might not move. You could lose 70-100% of the premium paid. Only risk capital you can afford to lose entirely.

Set a stop-loss at 50% of premium paid. If the trade goes against you before earnings and you're down 50%, cut it and walk away. Don't marry the position.

Probability of Success: ~25% (but 3:1+ payout if it works)

⚠️ Risk Factors

Let's be real about what could derail the MU bull case:

🥊 Competition Intensifies in HBM

SK Hynix completed HBM4 development in September 2025 and both SK Hynix and Samsung are accelerating production to February 2026 - potentially ahead of Micron's H2 2026 timeline.

If competitors grab early HBM4 design wins with NVIDIA, Micron's pricing power could weaken faster than expected. Remember, MU only has 11% HBM market share vs SK Hynix's 53%. Being late to HBM4 could cement that gap.

📉 Memory Cycle Peak Fears

Micron's 68% gross margin guidance might represent the cyclical peak. Memory has historically been a boom-bust industry, and while the AI narrative suggests "this time is different," we've heard that before in 2018 and 2000.

If AI spending moderates or efficiency innovations like DeepSeek reduce memory requirements, DRAM and NAND prices could roll over quickly. The street would slash 2027 estimates overnight.

🌐 China Risks - Both Demand & Competition

Micron was banned from critical Chinese infrastructure in May 2023 due to geopolitical tensions. Meanwhile, Chinese competitor CXMT is targeting 8% DRAM market share by end of 2025 and developing domestic HBM capability.

If China accelerates CXMT support while maintaining Micron restrictions, it creates a double whammy: lost revenue + new low-cost competition.

📊 Valuation Is No Longer Cheap

At $319 with a P/E of 27.13 and market cap of $345B, MU is priced for perfection. The stock went from deep value in early 2024 to fairly valued to potentially expensive. If growth slows even slightly from the current 57% YoY revenue growth, multiple compression could be brutal.

Consensus price target of $290 is actually below current price, suggesting some analysts think we're ahead of ourselves.

🏭 Execution Risks on Capacity Expansion

Micron is spending $20B in FY26 capex (raised from $18B) across Idaho, New York, Virginia, and Hiroshima facilities. The new ID1 fab in the U.S. won't be operational until 2027, creating a capacity constraint window where competitors could gain share.

Any construction delays, equipment issues, or yield problems would be punished severely by the market. Memory manufacturing at scale is hard - ask Intel about their 10nm struggles.

💸 Insider Selling

According to the catalyst report, there have been "10 consecutive transactions by CEO" - all sells. While CEOs have many reasons to sell (taxes, diversification, comp plans), it's worth noting that insiders are reducing exposure at current levels.

That said, insider selling after a 239% run is expected and doesn't necessarily signal a bearish turn.

🎯 The Bottom Line

Real talk: The $11.3 million LEAP activity we saw today represents significant institutional positioning in 2028 calls. These are deep in-the-money contracts with strikes at $250, $310, and $330 - representing major conviction in MU's long-term trajectory after the 239% run.

But here's what matters: The fundamentals supporting MU remain intact. HBM capacity is sold out through 2026 with contracted pricing. DRAM prices are rising 40-50% and Micron can only meet half of customer demand. Q2 earnings on April 1 are setting up for another beat with $18.7B revenue guidance.

If you own it: This isn't a sell signal. It's a "maybe take some profits and let the rest ride" signal. The gamma support at $310 is only 2.9% away - that's your line in the sand. Below $310, reassess. Above $320, we're in breakout territory toward $340-350.

If you're watching: The $300-320 consolidation zone offers better risk/reward entries than chasing at $320 resistance. Consider selling cash-secured puts at $300 or waiting for a pullback to the monthly implied move support at $295. Don't FOMO into resistance.

If you're bearish: The 68% gross margin guide likely represents peak profitability in this cycle. Competition from SK Hynix and Samsung on HBM4 timing is real. Memory cycles always end badly. But fighting this tape before April earnings is dangerous - wait for technical breakdown below $300 or fundamental deterioration in the Q2 report.

Mark your calendar: April 1, 2026 earnings will be the next major inflection point. Until then, expect rangebound trading between $310-$340 with volatility around monthly OPEX dates.

⚠️ Disclaimer

Options trading involves substantial risk and is not suitable for all investors. This analysis is for educational and informational purposes only and should not be considered investment advice. The author may hold positions in securities discussed. Past performance does not guarantee future results. All option strategies carry risk of total loss. Please consult with a qualified financial advisor before making investment decisions. Trade data and analysis are subject to interpretation and error. Always do your own due diligence.

Analysis based on option flow data as of January 2, 2026. Market conditions can change rapidly. Micron Technology stock price referenced at $319.33. For real-time option chains and flow, visit ainvest.com.