🔄 MU: $2.9M Call Roll Shows Institutional Conviction - Rolling Up & Out to $350!

📅 January 6, 2026 | 🔥 Extreme Unusual Activity Detected

🎯 The Quick Take

Someone just rolled $2.9 MILLION in MU options - closing $1.4M in near-term $330 calls and opening $1.5M in longer-dated $350 calls! This isn't just a bullish bet; it's a strategic repositioning that screams continued conviction but with a twist: they want MORE TIME and a HIGHER target. Translation: The big money sees Micron pushing to $350+ but needs until January 23 to get there.

💰 The Option Flow Breakdown

📊 What Just Happened

Here's the EXACT trade that lit up our scanners at 9:59 AM:

| Time | Symbol | Side | Type | Strike | Expiry | Premium | Size | Spot | Option Price | Strategy | Z-Score |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:59:14 | MU | ABOVE_ASK | BUY CALL | $350.00 | 2026-01-23 | $1,500,000 | 1,350 | $332.06 | $10.76 | Long Call (BTO) | 21.25 🚨 |

| 09:59:14 | MU | ABOVE_ASK | BUY CALL | $330.00 | 2026-01-16 | $1,400,000 | 900 | $332.06 | $15.29 | Close Short Call (BTC) | 3.64 🔥 |

🐋 Combined Premium: $2,900,000

🤓 What This Actually Means

Real talk: This is a classic call roll - and it tells us a LOT about institutional thinking:

💡 What They Did:

- ✅ Closed out their Jan 16 $330 calls (took profits on the winning position)

- ✅ Rolled into Jan 23 $350 calls (extended time, raised strike)

- ✅ Paid ABOVE the ask on both sides (desperate to get filled - no patience for limit orders)

🧠 What They're Thinking:

- They STILL believe MU is going higher (otherwise they'd cash out completely)

- They needed more time - the original Jan 16 expiry was too tight

- They're targeting $350+ (17-day target, not 10-day)

- They're willing to move the strike UP by $20 because they see runway

🚨 Why It's Unusual:

- The new position has a Z-Score of 21.25 - that's EXTREME (happens maybe a few times a year)

- 1,350 contracts on the $350 strike when open interest was only 691

- Both trades executed at the SAME SECOND - coordinated institutional desk move

- Total volume on Jan 23 $350 calls hit 2,800 vs OI of 691 (4x normal)

🏢 Company Overview

Micron Technology (MU) is one of the largest semiconductor companies in the world, specializing in memory and storage chips. The company focuses on DRAM and NAND flash production, serving data centers, mobile devices, consumer electronics, and industrial/automotive sectors.

Key Stats:

- 💰 Market Cap: ~$386.5 billion

- 🏭 Industry: Semiconductors & Related Devices

- 📍 Headquarters: Boise, Idaho

📈 Technical Setup / Chart Check-Up

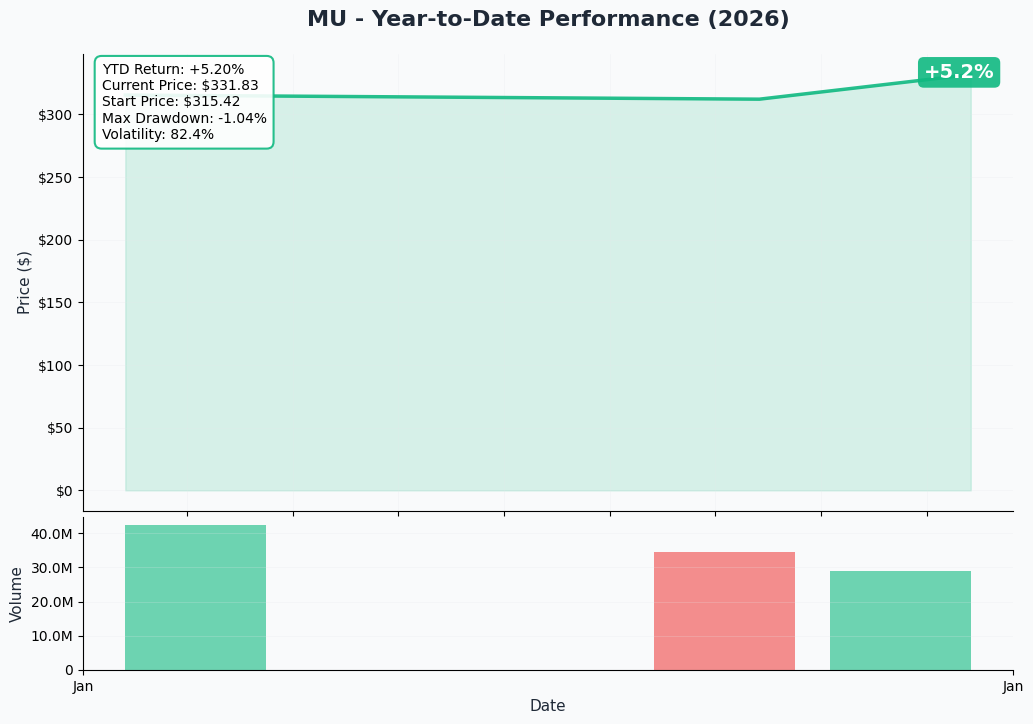

YTD Performance

Micron has delivered an absolutely explosive 2025, rallying approximately 245% year-to-date and reaching all-time highs. The stock closed at $322.47 on January 6, 2026, after spiking as high as $325.53 intraday on January 2, 2026. This parabolic move has been driven by insatiable demand for High Bandwidth Memory (HBM) used in AI infrastructure.

According to Bernstein's analysis, the firm raised their price target 20% on January 2, sending the stock up $30.03 (+10.52%) in a single session. With Rosenblatt's street-high $500 price target still on the table, the technical setup shows strong momentum but also signals that we're in "prove it" territory at these levels.

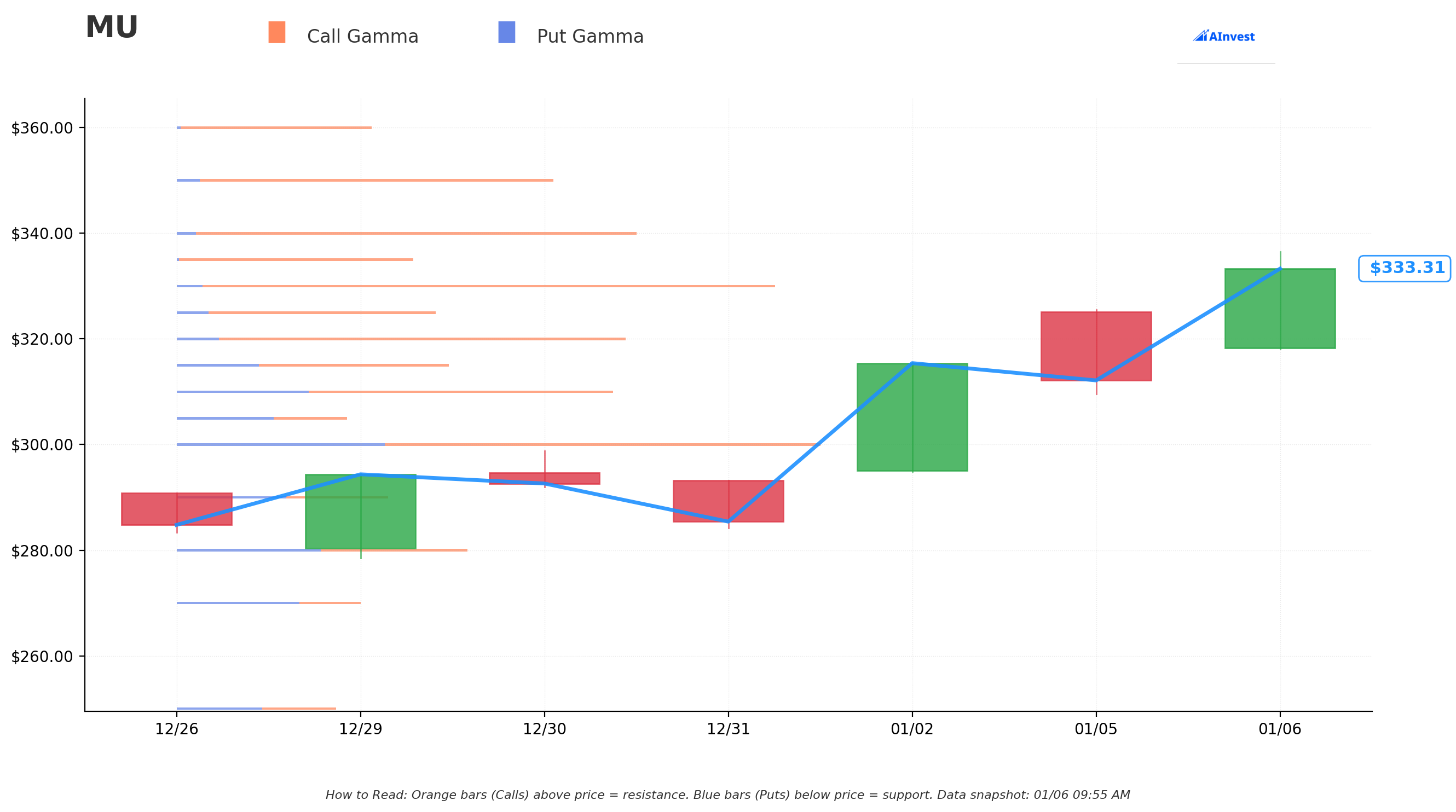

🎯 Gamma-Based Support & Resistance Analysis

Current Price: $333.76

The gamma exposure map reveals MU is trading in a narrow sweet spot with MASSIVE support below and building resistance above:

🔵 Support Levels (Put Gamma):

- $330.00 - STRONGEST SUPPORT (8.0B total gamma) 🛡️

- This is the "fortress" level - heavy put selling and dealer hedging create a powerful magnet

- Notice the call roll EXITED at $330 - institutions know this is the new floor

- $325.00 - Secondary support (3.5B gamma)

- $320.00 - Strong cushion (6.0B gamma)

- $300.00 - Deep safety net (8.8B gamma)

🟠 Resistance Levels (Call Gamma):

- $335.00 - First hurdle (3.2B gamma) ⚠️

- $340.00 - Intermediate ceiling (6.2B gamma) 🚧

- $350.00 - THE TARGET (5.1B gamma) 🎯

- This is where the new call position is struck - institutions expect price discovery here

- High gamma concentration suggests this is a magnet IF momentum continues

What This Means for Traders: The gamma structure is BULLISH but shows clear battlelines. Market makers are heavily short puts at $330, creating strong downside protection. The journey to $350 requires breaking through multiple resistance clusters, but the fact that institutions rolled UP to this strike suggests they see a catalyst coming that justifies the move. The $330 floor should hold on any pullbacks given the dealer positioning.

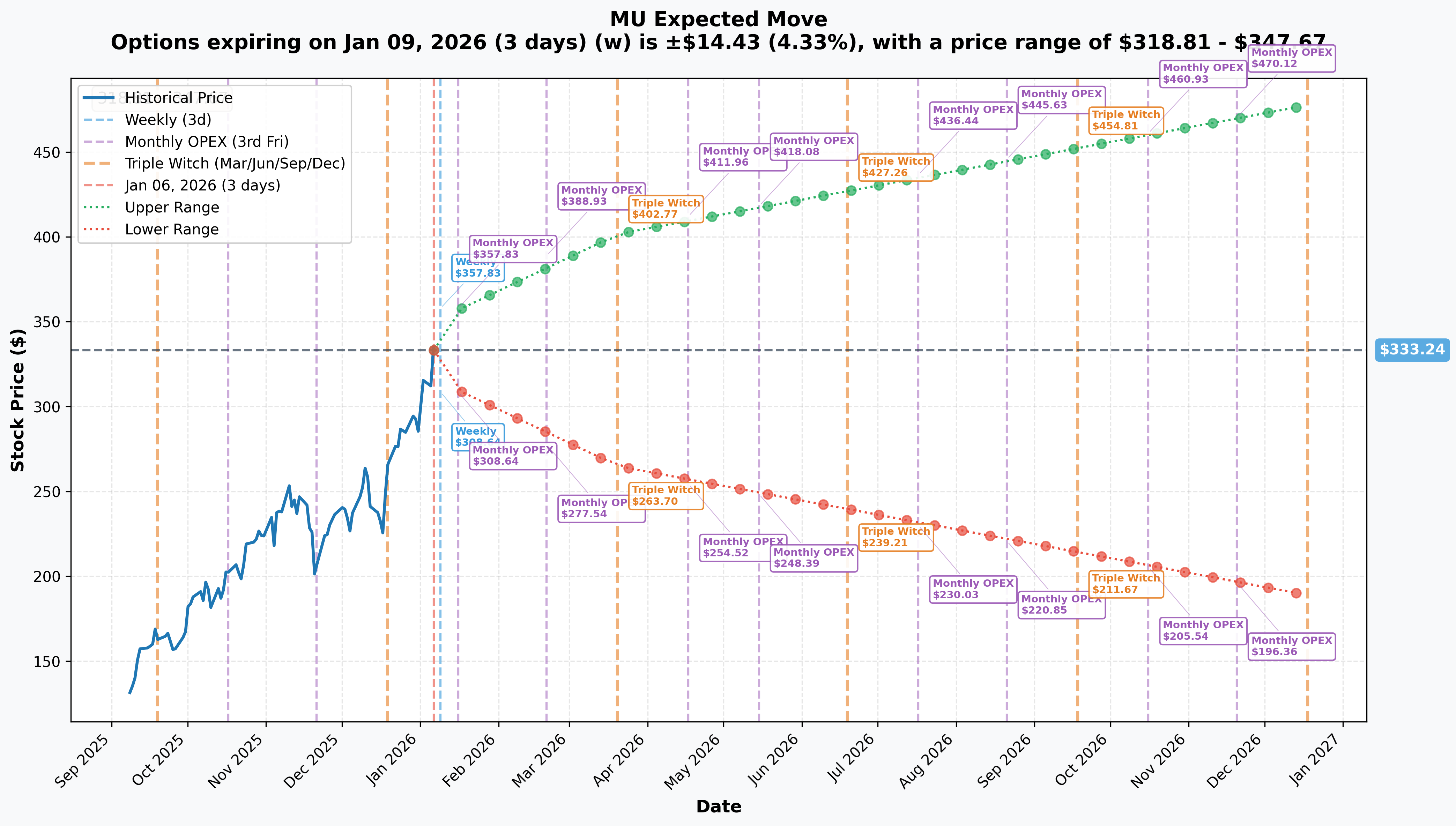

📊 Implied Move Analysis

Current Price: $333.24

Let's break down what the options market is pricing in for key dates:

📅 Weekly (Jan 9): ±4.33%

- Range: $318.81 - $347.67

- Modest move expected in the near term

📅 Monthly OPEX (Jan 16): ±7.17%

- Range: $309.35 - $357.12

- This is where the ORIGINAL position expired - upper band touches $357

📅 Jan 23 (New Trade Expiration): ±8-9%

- Estimated Range: ~$305 - $365

- The $350 strike sits RIGHT in the upper half of this range - achievable but requires follow-through

📅 Quarterly Triple Witch (Mar 20): ±20.53%

- Range: $264.81 - $401.66

- Massive range reflects uncertainty around Q2 earnings and HBM4 developments

🧠 Strategic Implications:

The roll from Jan 16 to Jan 23 makes perfect sense when you look at implied moves:

- Jan 16 upper bound: $357 ($350 strike was achievable but tight)

- Jan 23 upper bound: $365 ($350 strike is comfortably within range)

By extending duration by 7 days and moving the strike UP by $20, the trader is betting that: 1️⃣ A catalyst in the Jan 16-23 window pushes MU higher 2️⃣ The stock needs more time to break through $340 resistance 3️⃣ The risk/reward is better at a higher strike with more time

The probability math suggests the $350 target has roughly a 35-40% chance of being in-the-money by expiration - aggressive but not reckless given Micron's current momentum and upcoming catalysts.

🎪 Catalysts

🔮 What Already Happened

💥 Q1 FY2026 Blowout Earnings (December 17, 2025)

Micron absolutely CRUSHED it on December 17, reporting record-breaking Q1 FY2026 results:

- Revenue: $13.64B (+57% YoY) vs $8.71B last year

- EPS: $4.78 (non-GAAP) vs $1.79 last year (+167%)

- Gross Margin: 56.8% (up 2,070 bps YoY!)

- HBM Revenue: Nearly $2B in the quarter, entire 2026 supply SOLD OUT

The stock spiked 17% on the news according to Blocks and Files. CEO Sanjay Mehrotra stated: "Our Q2 outlook reflects substantial records across revenue, gross margin, EPS and free cash flow."

📊 Analyst Upgrades Bonanza (December 2025 - January 2, 2026)

Wall Street went ALL-IN on Micron post-earnings:

- Rosenblatt: Raised PT to $500 (Street High!) 🚀

- Bernstein: Raised PT to $330 on January 2 (20% bump)

- Bank of America: UPGRADED to Buy from Neutral, PT $300

- JPMorgan, Morgan Stanley, Citi, Cantor: All reiterated/raised to $330-350 range

Consensus: 28 Buy ratings, 2 Hold, 0 Sell - Average PT $307.69

🏭 CHIPS Act Funding Secured (December 2024)

Micron secured up to $6.4 billion in CHIPS Act funding, with $1.2B redirected from New York to Idaho to accelerate HBM production capacity. This shows government backing for domestic memory production.

🔜 What's Coming Next

🚀 Q2 FY2026 Earnings (Expected Late March 2026)

This is THE major catalyst and likely what the option traders are positioning for. Micron's guidance provided on December 17:

Q2 FY2026 Guidance:

- Revenue: $18.7B ± $400M (+132% YoY!) 📈

- Gross Margin: 67% ± 1% (up 3,100 bps YoY)

- EPS: $8.42 (non-GAAP) - explosive growth

According to CNBC's coverage, this would represent Micron's strongest quarter ever. Key metrics to watch:

- HBM revenue progression (targeting >$2B per quarter)

- DRAM/NAND pricing sustainability

- Updates on HBM4 sample shipments

🎮 CES 2026 (January 6-9, 2026)

Happening RIGHT NOW in Las Vegas! Micron typically showcases new products and announces partnerships at CES. Any major AI partnership or product announcements could be the catalyst the option traders are betting on for the Jan 16-23 window.

🤖 NVIDIA GTC 2026 (March 16-19, 2026)

NVIDIA's GTC conference is a major venue for AI/HBM partnership announcements. Given Micron's "preferred supplier" status with NVIDIA for HBM3E and HBM4, any platform launch updates or supply deal announcements could be material catalysts.

💾 HBM4 Mass Production Ramp (H1 2026)

According to DigiTimes, Micron is on track for HBM4 mass production in H1 2026. This next-generation memory offers:

- 2048-bit interface

-

2.0 TB/s per memory stack

- 60%+ better performance vs. previous generation

- 20%+ better power efficiency

TrendForce reports that Micron shipped HBM4 samples to key customers in late 2025. Volume ramp announcements could be the catalyst between now and month-end.

🎲 Price Targets & Probabilities

Based on the gamma levels, implied moves, catalyst timeline, and institutional positioning, here's how I see MU playing out:

🚀 Bull Case: $350-365 (35-40% Probability)

Path to $350:

- Clear $335 resistance (3.2B gamma) - First hurdle ✅

- Break through $340 (6.2B gamma) - Needs catalyst 🎯

- Reach $350 target zone (5.1B gamma) - Option strike achieved 💰

What Needs to Happen:

- Positive news from CES 2026 (partnership/product announcement)

- Continued memory shortage narrative driving DRAM pricing

- HBM4 production update or customer announcement

- Broader market stability (no macro shocks)

Timeframe: January 16-23 window (matches the new option expiration)

Reward: At $350, the rolled calls would be worth ~$20 ($5,000 profit per contract on the $10.76 entry), justifying the strategy. At $365 (upper implied move band), they'd be worth ~$35 ($24 profit per contract).

⚖️ Base Case: $330-340 (40-45% Probability)

The Consolidation Zone:

MU continues to trade in the $330-340 range as the market digests the massive 245% 2025 rally and waits for Q2 earnings confirmation. The gamma structure heavily supports this scenario:

- $330 acts as a fortress (8.0B put gamma)

- $340 provides interim resistance (6.2B call gamma)

- No major catalysts but no negative news either

What This Looks Like:

- Rangebound chop with support bounces at $330

- Multiple tests of $340 that get rejected

- Option traders experience time decay but maintain hope

- Volatility compression as we approach earnings

For the Call Roll: This is the "pain trade" - the rolled calls bleed theta but don't expire worthless. At $340 by Jan 23, they'd be worth ~$10 (breakeven), making the roll a wash. Below $335, the position starts losing money.

😰 Bear Case: $310-330 (20-25% Probability)

The Pullback Scenario:

MU retraces to test the $330 support or even breaks down to the $325 (3.5B gamma) or $320 (6.0B gamma) levels if:

- Broader semiconductor weakness (NVDA, AMD selling off)

- Profit-taking after 245% rally in 2025

- Delay in HBM4 production timeline

- China geopolitical tensions escalate

- Macro concerns (Fed policy, recession fears)

What Kills the Trade: Below $335 by Jan 23, the rolled calls are losing money. The original $330 calls that were closed would have fared better (in the money at expiration). This is the risk of rolling UP - you need the stock to not just hold, but ACCELERATE higher.

For the Trader: At $330, the $350 calls expire worthless (-$1.5M loss on the new position). However, they DID capture gains on the original $330 calls they closed, so the NET loss would be offset by those profits. Still, it's a failed roll strategy.

💡 Trading Ideas

🛡️ Conservative: Support-Based Put Spread

Strategy: Sell a $325/$320 Bull Put Spread expiring Jan 23

Setup:

- Sell $325 Put at ~$4.00

- Buy $320 Put at ~$2.50

- Net Credit: ~$150 per spread

- Max Risk: $350

- Breakeven: $323.50

Why This Works: The gamma data shows MASSIVE support at $330 (8.0B) and $325 (3.5B). As long as MU holds $325, you collect premium with strong probability of success (~70-75% PoP). You're betting WITH the institutional flow that sees $330 as the floor.

Risk Management:

- Close at 50% max profit to lock in gains

- Set stop loss if MU breaks below $328 (support compromise)

- Use position size where max loss is 1-2% of portfolio

Who This Is For: Traders who want to capitalize on the bullish structure without the aggressive directional bet. You're collecting premium while the big money targets $350.

⚖️ Balanced: Debit Spread Following the Flow

Strategy: Buy a $335/$345 Call Debit Spread expiring Jan 23

Setup:

- Buy $335 Call at ~$14.00

- Sell $345 Call at ~$8.50

- Net Debit: ~$550 per spread

- Max Profit: $450

- Breakeven: $340.50

Why This Works: You're following the institutional logic - targeting $350 - but capping risk with a defined max loss. If MU reaches $345+, you collect max profit (82% return). Your breakeven at $340.50 is the intermediate resistance level, so you need follow-through but not perfection.

Risk Management:

- Take profits at $342-343 (80% of max gain)

- Cut losses if MU fails to break $338 by Jan 20

- Consider rolling to Feb expiration if MU is at $340 on Jan 22

Who This Is For: Swing traders who believe in the institutional thesis but want defined risk. You're paying ~$550 to potentially make $450 (82% ROI) if MU follows through.

🚀 Aggressive: Mirroring the Whale

Strategy: Buy Jan 23 $350 Calls (Following the $1.5M Flow)

Setup:

- Buy $350 Call at ~$10.76 (current price)

- Max Risk: $1,076 per contract

- Unlimited upside above $360.76

- Breakeven: $360.76

Why This Works: You're LITERALLY copying the institutional trade. If they're willing to pay $1.5M to position for $350+, they likely have information or conviction we don't. The Z-Score of 21.25 says this is NOT a normal trade - it's a few-times-a-year event. When elephants move, sometimes it pays to follow.

Reality Check: This is a LOW probability trade (~30-35% chance of profit) but with ASYMMETRIC upside. If MU hits $365 (upper implied move band), each contract is worth $15 ($4 profit, 37% return). At $370, it's $20 ($9 profit, 84% return). But you need a CATALYST in the next 17 days.

Risk Management:

- Only risk what you can afford to LOSE entirely

- Consider taking 50% off at $355-360 to lock gains

- Watch for CES announcements Jan 6-9 for early tells

- If MU fails to clear $340 by Jan 16, cut losses

Who This Is For: YOLO traders with high risk tolerance who want lottery-ticket upside. You're betting on a near-term catalyst (CES, HBM4 news, partnership) that institutions may be front-running. Position size accordingly - this should be <5% of your options portfolio.

⚠️ Risk Factors

📉 Valuation Stretched After 245% Rally

Real talk: MU has gone PARABOLIC in 2025. While the fundamental story (AI memory supercycle, HBM sold out through 2026) is legit, the stock is trading above the average analyst price target of $307.69. At $333, it's already ahead of most Street expectations. Any disappointment could trigger profit-taking. According to Trefis analysis, the "AI memory re-rate" is now fully priced in.

🇨🇳 China Exposure Remains a Wildcard

China's Cyberspace Administration banned Micron products from critical infrastructure in May 2023. According to Astute Group reporting, Micron is preparing to end sales of server-grade DRAM to mainland China data centers and laid off ~300 China employees in August 2025. While China historically represented 10-12% of revenue, this geopolitical overhang could worsen. Any escalation in US-China tensions could trigger sell-offs.

🏭 Execution Risk on HBM4 Production

The bull case hinges on Micron executing flawlessly on HBM4 production ramp in H1 2026. Any delays, quality issues, or customer qualification problems could derail the $350 target. Remember, SK Hynix still dominates with 62% HBM market share vs Micron's 21%. Samsung is also fighting back - analysts forecast Samsung's market share could rebound to >30% by 2026 with full HBM4 deployment.

⏰ Time Decay is the Enemy

The rolled calls have just 17 days to expiration. Theta decay accelerates in the final 2-3 weeks. If MU stays rangebound at $335-340, these calls lose value DAILY. By Jan 20, time decay becomes brutal. The institutional trader clearly expects a catalyst in this window - if it doesn't materialize, the position bleeds.

📊 Memory Cycles Are... Cyclical

Despite the structural AI memory shortage narrative, memory markets have historically been boom-bust. According to Wikipedia's analysis of the 2024-2026 shortage, current conditions are unprecedented, but ANY slowdown in AI capex (NVDA, hyperscalers) could rapidly flip sentiment. TrendForce warns that memory prices surged 80-100% in December 2025 - this can't continue forever without demand destruction.

🎢 Implied Volatility Crush Post-Event

If there IS a catalyst (CES announcement, HBM4 news) that drives MU to $350, implied volatility will likely collapse afterward. This means even if the stock hits your target, option values may not increase as much as you'd expect due to vega risk. Conversely, if we trade sideways into late Jan with no news, IV could compress, hurting option values even if the stock doesn't fall.

🎯 The Bottom Line

Real talk: This $2.9M call roll is one of the most instructive institutional trades I've seen in weeks. Here's what the big money is telling us:

The Message: ✅ They're STILL bullish on MU (otherwise they'd cash out) ✅ They needed MORE TIME (7 extra days matter) ✅ They're targeting HIGHER ($350 vs $330) ✅ They expect a CATALYST between Jan 16-23

What's fascinating: They paid ABOVE the ask on both sides, moved the strike UP by $20, and extended just 7 days. This is surgical positioning, not blind optimism. They likely have conviction around:

- CES 2026 announcement this week (happening NOW)

- HBM4 production/customer update before month-end

- Continued memory shortage momentum into Q2 earnings

The Setup:

- Gamma levels support $330 floor with $350 as achievable target

- Implied move math gives $350 a 35-40% probability

- Catalyst calendar is dense (CES, potential HBM4 news, GTC prep)

- Technical momentum remains strong despite stretched valuation

Your Action Plan:

🟢 If You're Bullish: Follow the flow with a defined-risk spread ($335/$345 debit spread for balanced traders) or mirror the whale ($350 calls for aggressive accounts). Watch CES this week for early signals.

🟡 If You're Cautious: Sell premium at support levels ($325/$320 put spread) to capitalize on the strong $330 floor while collecting theta. Let the institutions take the directional risk.

🔴 If You're Bearish: Wait for a failed breakout at $340 or violation of $330 support before shorting. Fighting this tape with Micron's fundamental backdrop (HBM sold out, 132% revenue growth guided) is dangerous. The memory supercycle is REAL even if valuation is rich.

Mark Your Calendar:

- ✅ Jan 6-9: CES 2026 - Watch for partnership/product news

- ✅ Jan 16: Original call expiration - Key inflection point

- ✅ Jan 23: New call expiration - Target date for $350

- ✅ Late March: Q2 FY2026 earnings - The REAL event

Final Thought:

When a trader rolls UP in strike price and extends duration by paying nearly $3M, they're not gambling - they're positioning. The Z-Score of 21.25 on the new position tells us this happens maybe a few times per year. Either they're spectacularly wrong, or they know something the market hasn't fully priced in yet.

I'm leaning toward the latter. Micron's fundamental setup (AI memory supercycle, HBM supply sold out, 67% gross margins guided) combined with near-term catalysts (CES, HBM4, earnings prep) creates asymmetry that favors the bulls. But manage your risk - use spreads, size appropriately, and watch the $330 support like a hawk.

The memory boom is real. The question is whether it justifies $350 by January 23. The institutions just bet $1.5M that it does. 🎯

⚠️ Disclaimer: Options trading involves substantial risk and is not suitable for all investors. This analysis is for educational and informational purposes only and should not be construed as financial advice. The trades discussed involve significant risk of loss. Past performance is not indicative of future results. Always conduct your own due diligence and consider consulting with a licensed financial advisor before making investment decisions. The author may hold positions in securities discussed.

📚 Resources:

- Company Information: Micron Investor Relations

- Catalyst Research: Multiple financial news sources (see inline citations)

🔗 Related Resources:

Analysis prepared January 6, 2026 | Market conditions subject to change